Enterprise Mobility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

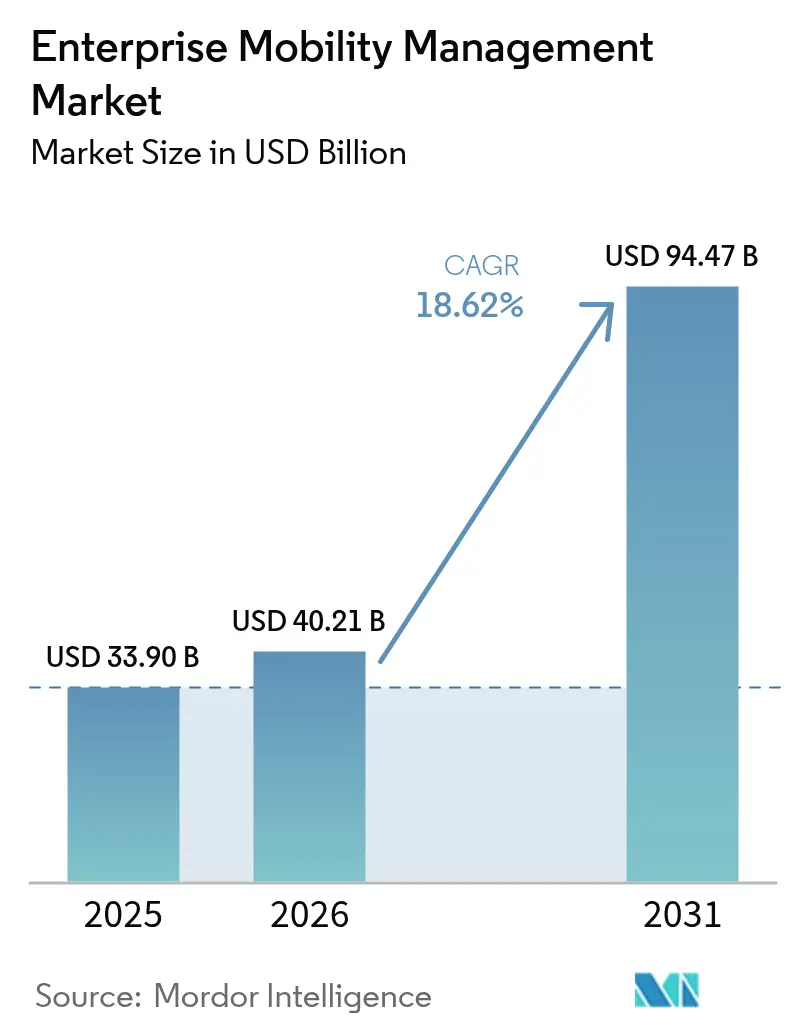

| Market Size (2026) | USD 40.21 Billion |

| Market Size (2031) | USD 94.47 Billion |

| Growth Rate (2026 - 2031) | 18.62% CAGR |

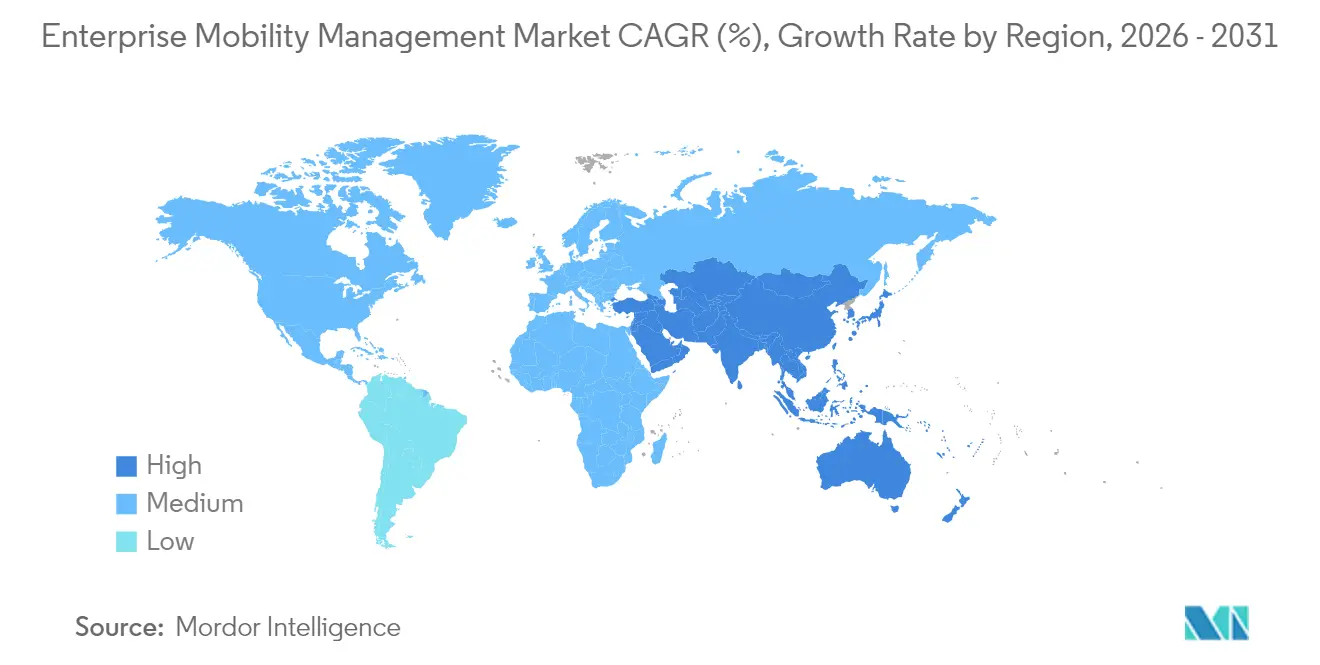

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Mobility Management Market Analysis by Mordor Intelligence

The Enterprise mobility management market size was valued at USD 33.90 billion in 2025 and estimated to grow from USD 40.21 billion in 2026 to reach USD 94.47 billion by 2031, at a CAGR of 18.62% during the forecast period (2026-2031). Heightened adoption of Zero Trust security, rapid cloud migration, and the embedding of artificial intelligence in policy orchestration are accelerating demand for unified mobility platforms. Organizations now view endpoint control as a business-continuity priority rather than an IT add-on, catalyzing record investments in device, application, and content governance. North American enterprises drive premium spending as regulators tighten breach-reporting rules, while Asia Pacific firms scale deployments fastest on the back of mobile-first digital-transformation programs. Vendors are differentiating through low-latency edge architectures that keep verification processes local, reducing user friction and lowering incident-response times.

Key Report Takeaways

- By type, solutions commanded 62.35% of the Enterprise mobility management market share in 2025; the security management subsegment is advancing at a 20.41% CAGR through 2031.

- By deployment mode, cloud platforms held 58.10% of the Enterprise mobility management market size in 2025 and are expanding at a 18.93% CAGR to 2031.

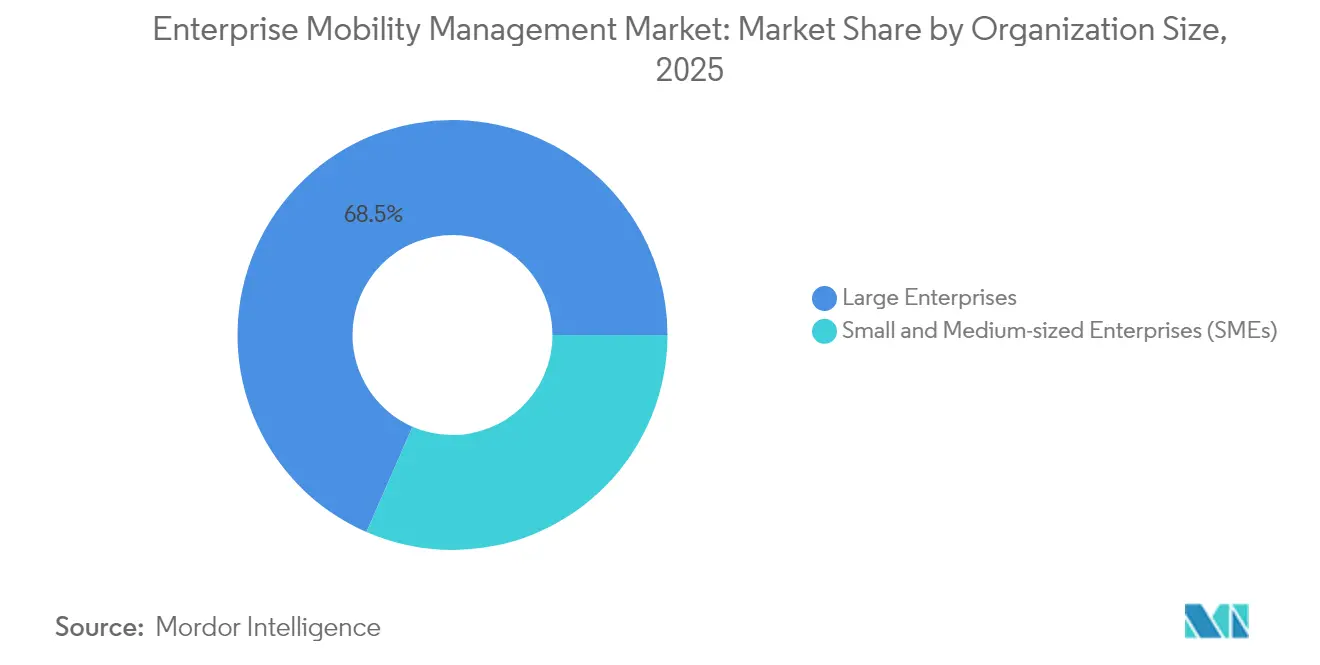

- By organization size, large enterprises contributed 68.45% revenue share in 2025, while SMEs are growing at 20.97% CAGR owing to lower up-front costs.

- By end-user industry, IT and Telecom led with 27.20% revenue share in 2025, while Healthcare is poised for the fastest 19.78% CAGR through 2031 as HIPAA mandates MFA and encryption.

- By geography, North America accounted for 32.30% of 2025 revenue, but Asia Pacific is set to record the highest 21.74% CAGR on robust mobile-device proliferation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Mobility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of enterprise mobile devices and apps | +3.2% | North America and Asia Pacific | Medium term (2-4 years) |

| Rising BYOD and remote-work culture | +2.8% | North America and Europe | Short term (≤ 2 years) |

| Escalating mobile cybersecurity threats | +4.1% | Global BFSI and Healthcare hot spots | Short term (≤ 2 years) |

| Emergence of Zero-Trust EMM frameworks | +2.3% | North America and Europe | Long term (≥ 4 years) |

| Integration of AI-driven analytics in EMM solutions | +3.5% | Global Tech and Retail sectors | Medium term (2-4 years) |

| Growing regulatory compliance requirements (GDPR, HIPAA) | +2.9% | Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Enterprise Mobile Devices and Apps

Retailers, utilities, and public-sector agencies now oversee device fleets that rival telecom operators in scale. Seven-Eleven Japan centrally manages 300,000 tablets across 21,000 stores, demonstrating how cloud orchestration delivers uniform policy enforcement at national reach. Microsoft Intune’s new policy set for Apple Vision Pro indicates a widening endpoint mix that EMM consoles must secure without sacrificing user experience.[1]“What’s new in Microsoft Intune: May 2025,” techcommunity.microsoft.com Predictive analytics embedded in device agents surface battery-health and update-compliance anomalies before they become downtime events. Corporate-owned-personally-enabled (COPE) models are replacing restrictive lockdowns, boosting employee satisfaction while preserving data custody.

Rising BYOD and Remote-Work Culture

Ninety-two percent of global firms now allow some form of remote access, up from 76% in 2023, forcing security teams to isolate corporate data from personal content through encrypted containers. Healthcare systems face twin pressures of HIPAA compliance and clinician convenience, pushing uptake of virtual workspace tools that stream applications without persisting ePHI on unmanaged phones. The U.S. Federal Mobility Group, comprising 45 agencies, is codifying shared BYOD assessment checklists to streamline procurement and speed FedRAMP approvals. Shift-based access control and rapid enterprise-wipe functions are now baseline requirements.

Escalating Mobile Cybersecurity Threats

BlackBerry logged 600,000 attacks against critical-infrastructure endpoints in Q3 2024, with 45% aimed at financial institutions. Supply-chain exploits surged as attackers piggybacked on third-party SDKs; 75% of surveyed software pipelines suffered at least one breach last year. IoT expansions aggravate risk: 96% of power-grid operators deploy sensors that lack central patch enforcement. In response, the Cybersecurity and Infrastructure Security Agency published an Enterprise Mobility checklist that prioritizes phishing-resistant authentication and removes SMS-based MFA from recommended practices.[2]“Mobile Device Cybersecurity Checklist,” cisa.gov

Emergence of Zero-Trust EMM Frameworks

NIST guidelines now position continuous verification of both identity and device posture as foundational to modern mobility stacks.[3]“Project Overview - Implementing a Zero Trust Architecture,” National Institute of Standards and Technology, pages.nist.gov Germany certified BlackBerry UEM for Apple iNDIGO, illustrating how federal agencies operationalize Zero Trust down to classified mobile workflows. AI-assisted policy engines correlate risk signals location drift, unusual app launches, or edge-latency spikes and auto-elevate authentication tiers. Secure edge compute keeps validation local, minimizing round-trip delays for field engineers using AR overlays in low-latency contexts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and upgrade costs | -2.1% | Emerging-market SMEs | Medium term (2-4 years) |

| Legacy system integration complexity | -1.8% | North America and Europe | Long term (≥ 4 years) |

| Limited skilled workforce for advanced EMM deployment | -1.9% | Asia Pacific and Latin America | Medium term (2-4 years) |

| Data privacy concerns and regulatory hurdles | -2.4% | Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation and Upgrade Costs

Total-cost-of-ownership remains opaque for firms new to enterprise mobility. Surveys of 150 corporate phone managers show 31.3% cite “cost clarity” as the top barrier to platform selection. Hidden spend on compliance audits, certificate renewals, and end-of-life device disposal often exceeds the first-year subscription fee. Vendors respond with feature unbundling; Microsoft now prices Enterprise Application Management at USD 2 per user per month so smaller firms can add advanced patching without a full SKU uplift. Cloud delivery lowers capex but converts budgets into recurring opex, challenging organizations with fluctuating headcount.

Legacy System Integration Complexity

Decades-old HR, ERP, and SCADA stacks frequently lack REST APIs, hampering single-console governance. Forty-six percent of firms report limited endpoint visibility when traditional asset databases do not synchronize with EMM records. The EU Cyber Resilience Act gives companies until 2027 to harden connected devices, accelerating modernization roadmaps or forcing risk-acceptance decisions. Specialized integrators and API brokers lengthen deployment schedules, creating budget overruns that deter late-stage adopters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solutions Dominate Through Security Innovation

Solutions accounted for 62.35% of 2025 revenue, confirming their role as the control nexus across device, application, and content layers. Security Management stood out with a 20.41% CAGR, reflecting relentless threat evolution. Device Management continues as the entry point for new customers yet increasingly bundles AI-guided remediation. Application containers now isolate corporate data on personal phones, meeting privacy statutes in Europe and California. Content and Email Management shifts from basic encryption to policy-driven watermarking that deters unauthorized sharing. Telecom Expense Management remains niche but gains traction among logistics firms seeking SIM-level cost control.

Service lines complement product portfolios. Professional Services teams de-risk rollouts through readiness assessments and phased cut-over plans. Managed Services supply round-the-clock telemetry review, crucial for understaffed IT groups in healthcare and retail. Microsoft’s Advanced Analytics module packages anomaly detection APIs that partners monetize via consulting engagements. As AI matures, domain specialists that can fine-tune models on vertical data will capture margin uplift, giving incumbents an edge over generic MSPs.

By Deployment Mode: Cloud Transformation Accelerates

Cloud options captured 58.10% of 2025 spend and posted the fastest 18.93% CAGR. The Enterprise mobility management market is therefore gravitating toward scalable SaaS consoles that auto-update compliance libraries. One national retail chain ran a proof of concept across 5,000 endpoints and achieved full production in four weeks, a timeline unthinkable on legacy on-premise stacks. Hybrid-cloud remains the bridge for banks requiring data-residency assurance; sensitive tokens stay on-site while policy logic executes in the provider’s regionally fenced cloud. On-premise persists in defense deployments where air-gapped servers satisfy classified-data mandates.

Cost elasticity explains cloud traction. Consumption-based models let SMEs mirror device adoption curves without large license blocks. Government blanket-purchase agreements such as the U.S. GSA’s Best-in-Class Mobility contract tilt procurement toward cloud and 5G-ready services. The EU Digital Identity Wallet regulation compels member states to spin up cloud-native credential vaults within 24 months. Vendors that pre-certify for local pseudonymization standards will outpace rivals still reliant on single-tenant offerings.

By Organization Size: SME Growth Disrupts Traditional Patterns

Large enterprises held 68.45% revenue share in 2025, but the fastest 20.97% CAGR is now logged by SMEs. Cloud onboarding, simplified per-user pricing, and pre-configured compliance templates eliminate the multi-quarter consulting engagements that once deterred smaller buyers. Unified endpoint platforms consolidate mobility, PC, and IoT governance, sparing SMEs the cost of parallel toolchains. The Enterprise mobility management market share of SMEs is forecast to climb to 34.20% by 2031 as regional distributors bundle EMM with cellular data plans.

Enterprises still shape roadmap priorities; Bechtle’s framework to deliver 300,000 Apple devices worth EUR 770 million (USD 869 million) to German agencies illustrates how volume deals influence vendor certification pipelines. Yet smaller schools under Japan’s GIGA program chose mobiconnect because its UI masks policy complexity, proving that ease-of-use can outweigh feature depth in the mid-market. Vendors are subdividing portals—advanced analytics for Fortune 100, low-touch wizards for 100-seat customers—to maximize share of wallet across company scales.

By End-user Industry: Healthcare Leads Digital Transformation

IT and Telecom contributed 27.20% of 2025 turnover thanks to early 5G rollouts and large remote workforces. Healthcare, however, is accelerating at 19.78% CAGR as new HIPAA rules make MFA and encryption compulsory for clinical apps. Banking and insurance firms continue to invest heavily to meet zero-downtime expectations and to satisfy Basel III operational-resilience tests.

Manufacturers deploy rugged tablets tethered to IoT sensors, using edge compute to run anomaly-detection models on plant floors. Government agencies consolidate legacy radios, smartphones, and wearables under one console for disaster-response readiness, with the U.S. Defense Information Systems Agency publishing Android 13 STIGs that drive procurement alignment. Retailers optimizing curb-side pickup integrate EMM APIs with workforce-scheduling engines, cutting order-handoff times during peak seasons. Logistics operators tag pallets with eSIM-enabled trackers managed via the same portal as driver handhelds, delivering end-to-end chain-of-custody visibility.

Geography Analysis

North America generated 32.30% of 2025 revenue as public-sector breach mandates accelerated spending on device posture checks and continuous authentication. The Cybersecurity and Infrastructure Security Agency’s mobile checklist now underpins procurement templates across 15 federal departments. Canadian privacy law amendments mandate that service providers store identifiable data domestically, raising demand for in-country SaaS regions. Mexico’s automotive corridor deploys edge-enabled tablets on factory floors, pushing industrial integrators to certify bilingual UIs and local-telco eSIM profiles.

Asia Pacific posts the highest 21.74% CAGR, propelled by smartphone ubiquity and national digital agendas. Japan’s convenience-store and education pilots showcase hyperscale deployments, underscoring operational efficiency gains from centralized patching. India’s Digital Personal Data Protection Act adds breach-reporting windows as short as 72 hours, compelling SMBs to adopt policy engines with audit-ready logs. China dominates device volume but restricts foreign cloud ingress, so multinationals operate hybrid architectures to meet cybersecurity reviews. Australia’s Protective Security Direction 001-2025 explicitly lists mandatory encryption algorithms for enterprise mobility endpoints, creating standardized tender language.

Europe tightens product-security oversight via the Cyber Resilience Act, requiring CE-mark conformity and incident-response processes by 2027. Germany’s BSI clearance for BlackBerry UEM paves the way for classified Apple deployments, evidencing national preference for certified solutions. The U.K. refines its post-Brexit data-transfer rules yet remains interoperable with EU adequacy arrangements, sustaining cross-border SaaS adoption. Southern European states prioritize digital-ID wallets that ride on EMM cryptographic modules, shortening citizen-service queues and expanding inclusive governance.

Mordor Intelligence provides coverage of the enterprise mobility management market across other key regional markets. Detailed country-level analysis extends to Indonesia incorporating local coverage and market participation, as required.

Regulatory Landscape

Enterprise mobility management deployments increasingly align with prescriptive mobile-security guidance, alongside tighter data portability and sovereignty requirements. In May 2026, the Canadian Centre for Cyber Security updated its ITSM.80.001 guidance on securing enterprise mobility, reinforcing baseline expectations around device hardening, authentication, and risk management that feed into enterprise procurement and MSP runbooks. In the United States, NIST guidance for managing mobile device security and NIST SP 1800-22 for BYOD continue to anchor policy design, while DISA STIG-aligned configurations and approved extensions such as Samsung Knox Service Plugin (KSP) shape government-grade Android enforcement patterns.

In Europe, interoperability and data access mandates increasingly intersect with EMM console capabilities. In May 2026, the European Commission published a Digital Markets Act (DMA) interoperability and data portability factsheet that outlines obligations for smartphone OS gatekeepers, raising the importance of open APIs and exportable telemetry for enterprise controls. Separately, the EU Data Act (Regulation (EU) 2023/2854) sets a 12 September 2026 deadline tied to connected-device "data by design" requirements, which pushes device makers, OS providers, and EMM vendors to operationalize compliant data access, minimization, and auditability across managed fleets.

Value Chain Analysis

The EMM value chain begins with endpoint and OS or platform providers (Apple, Android Enterprise ecosystem, rugged device OEMs), then moves to mobility and UEM software vendors (MDM/MAM/UEM consoles, policy engines, analytics). From there, the stack extends into identity and security layers (IdP, PKI, conditional access, SIEM/ITSM integrations). Distribution and implementation often run through cloud marketplaces, channel partners, and integrators that package licensing, enrollment, configuration, and compliance validation, with managed service providers handling 24x7 monitoring, incident response, and lifecycle operations such as patching and app governance.

Recent platform changes show how upstream OS and productivity-suite ecosystems increasingly steer downstream feature roadmaps and delivery. Microsofts June 2026 Intune Service Release 2606 added general availability for Enterprise Application Management (EAM) auto-updates for Windows, expanded managed macOS PKG app auto-updating, and brought EAM support into GCC High and DoD environments, reinforcing compliance-driven requirements as a design input across the chain. Bundling also changes go-to-market motions: Microsoft initiated automatic provisioning of the Intune Suite into Microsoft 365 E5 subscriptions, with completion targeted by August 1, 2026. That shift moves value capture toward suite platforms and pushes specialists toward differentiated integrations, vertical compliance, and higher-touch services.

Competitive Landscape

The Enterprise mobility management market hosts a moderately fragmented set of incumbents and specialists. Microsoft leverages Azure scale and AI analytics to embed preventive controls that auto-quarantine risky applications before execution. VMware refocuses after divesting its end-user computing assets, reallocating R&D toward spatial-computing workspace orchestration. BlackBerry differentiates through government-grade certifications, enabling premium pricing in defense and critical-infrastructure tenders. Jamf’s planned Android support shows platform convergence as customers demand single-pane oversight across mixed estates.

Edge computing integration becomes a new battleground; Qualcomm’s on-prem AI appliance offers inference at site level, lowering cloud egress fees for vision models examining worker safety. MSP ecosystem partnerships intensify as vendors chase mid-market expansion; TeamViewer’s acquisition of 1E strengthens its digital employee-experience module, moving the company beyond remote assistance into proactive endpoint health. Government certifications act as high entry barriers, and vendors securing early approvals lock in multi-year framework agreements, as evidenced by Bechtle’s Apple contract with Germany’s interior ministry.

Pricing competition remains disciplined as buyers prioritize risk reduction over lowest cost. Nonetheless, freemium tiers emerge for sub-50-device companies to seed market share. Strategic alliances between telecom operators and EMM providers bundle connectivity with security, creating stickier contracts and lowering customer-acquisition cost. Open-standard APIs are increasingly table stakes, allowing integration with SIEM, ITSM, and business-workflow tools to support continuous compliance narratives during board audits.

Enterprise Mobility Management Industry Leaders

Citrix Systems, Inc.

Microsoft Corporation

BlackBerry Limited

IBM (MaaS360)

VMware (AirWatch)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is operationalizing Zero Trust mobility as a continuous signal source for identity and security orchestration, particularly where regulators and auditors require demonstrable controls and traceable actions. CISA mobile guidance that deprioritizes SMS-based MFA and emphasizes phishing-resistant authentication, along with NIST mobile-device security guidance, supports demand for EMM capabilities that continuously attest device posture, manage certificates, and produce audit-ready logs across BYOD and COPE models. Government and regulated enterprises also create an opening for vendors that can deliver sovereign and segmented operations across tenants and geographies, as reflected in BlackBerrys June 2026 UEM updates positioned around sovereign endpoint control, expanded multi-tenant support, and cryptographic modernization.

Another opportunity centers on reducing administrative effort and improving fleet consistency through autonomous lifecycle controls, especially app updating, vulnerability remediation, and policy assignment at scale. Microsoft Intune updates in June 2026 (including EAM auto-updates and new endpoint privilege management support for shared devices) and enforced tooling baselines for Intune MAM SDK and wrapping tools (January 2026) point to a shift toward standardized, vendor-enforced management pipelines rather than bespoke, manual processes. Large-scale deployments such as Seven-Eleven Japans centrally managed 300,000 tablets across 21,000 stores highlight the demand for low-touch governance, while SMEs add further whitespace through simplified onboarding and modular pricing that preserves compliance without requiring multi-quarter integration projects.

Recent Industry Developments

- June 2026: BlackBerry announced enhanced capabilities for BlackBerry Unified Endpoint Management (UEM), including on-premises macOS management, post-quantum cryptography upgrades, and expanded multi-tenant support aligned to sovereign endpoint control requirements. The update strengthens BlackBerrys positioning in government and regulated verticals that prioritize data residency, cryptographic assurance, and tenant isolation, and it raises the competitive bar for certified, high-assurance UEM stacks.

- April 2026: IBM introduced MaaS360 Smart Device Groups to enable near real-time device classification and automatic policy assignment across managed fleets. The capability supports faster policy convergence in large, mixed estates and reduces manual segmentation work, which is increasingly important as organizations add new endpoint types and tighten compliance timelines.

- March 2026: IBM released MaaS360 Kiosk Designer to visually configure and validate Android kiosk experiences. This simplifies rollout for frontline and shared-device use cases in retail, logistics, and public-sector workflows, where standardized, locked-down modes and repeatable configuration are key to reducing support costs and limiting misuse.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers enterprise mobility management platforms and related services that help organizations secure, manage, and monitor employee and corporate devices, apps, and data access across mobile and endpoint environments. It includes policies, administration tools, and ongoing support delivered through cloud, on-premise, or hybrid setups.

Scope exclusions: We exclude one-time mobile device procurement services and stand-alone mobile threat defense platforms that are sold and used outside an EMM program.

Segmentation Overview

- By Type

- Solutions

- Device Management

- Application Management

- Security Management

- Content and Email Management

- Telecom Expense Management

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- On-premise

- Cloud-based

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- IT and Telecom

- Manufacturing and Industrial

- Retail and E-commerce

- Government and Public Sector

- Transportation and Logistics

- Other End-user Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and to build the first-pass demand signals for enterprise mobility management adoption. We reviewed public sources such as NIST publications on device and data security, U.S. FCC resources relevant to enterprise mobility usage, ISO standards references, and statistical releases from bodies such as OECD and the World Bank that track digitalization and workforce trends.

To connect these signals to market spend, we also relied on company filings and investor presentations to understand revenue mix signals across software and services. We then cross-checked with trade association websites and reputable press coverage on device management and remote work security practices. Patent databases were referenced for directional checks on innovation themes tied to endpoint management and policy enforcement, and we used a paid subscription for company financials and news to validate timelines and cross-check reported business momentum. The sources listed above are illustrative, and additional public and paid references were used to collect, validate, and clarify the final assumptions.

Primary Interviews and Surveys

Primary work focused on validating adoption, pricing direction, and how buyers package EMM across solutions and services in real deployments. We spoke with a mix of enterprise IT and security decision-makers, implementation partners, and managed service providers across major regions, so the assumptions could be tested against renewal behavior, deployment choices, and policy scope (BYOD versus corporate-liable).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 17% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 18% | Managers: 46% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable spend pool using enterprise digital workplace adoption signals, device and endpoint policy needs, and security and compliance requirements that typically trigger EMM rollouts. Once this demand pool is structured by deployment mode and organization size, we pressure-test the totals with selective bottom-up checks such as sampled vendor price ranges, partner channel checks, and a simple ASP-times-managed-device or managed-user approximation where consistent data was available.

Key inputs used in the model include the pace of remote and hybrid workforce expansion, BYOD versus corporate-owned policy mix, and cloud-based deployment preference. We also model how EMM suites package MDM, MAM, MCM, and identity controls, and we incorporate the services attach rate for implementation and ongoing support. Where data gaps showed up in bottom-up checks (for example, when services revenue is bundled with broader IT contracts), the estimates were normalized back to EMM-specific scope using interview-led allocation factors, then rechecked against regional adoption patterns.

For forecasting, scenario analysis was used because budgets and security priorities can shift with regulatory updates and macro conditions. Assumptions for adoption and pricing were refreshed using consensus ranges from primary respondents, and then applied consistently across regions and buyer types to keep the projection steps easy to follow and repeat.

Data Validation & Update Cycle

Validation is done through multiple passes so the final numbers do not rely on one data stream. We compare model outputs against independent signals such as deployment preference shifts, services attach trends, and buyer policy changes, and then we run variance checks across regions and organization sizes to confirm whether any segment looks out of line.

When a large swing is observed, the assumptions are revisited, and targeted re-contacts are made to confirm whether the change is real or driven by timing, currency, or scope interpretation. Before sign-off, the work is reviewed by another analyst to catch arithmetic issues and inconsistent boundaries. Reports are refreshed annually, and interim updates are made when material events could change adoption or pricing, followed by a final pre-delivery check so clients receive the latest updated view.

Mordor Intelligence's Enterprise Mobility Management Market Size Compared With Other Published Estimates

Published market sizes for enterprise mobility management can vary because the underlying scope is not always handled the same way, and year choices and currency timing can also shift the stated value. Differences usually show up around whether services are fully included, how endpoint coverage is treated, and how quickly cloud migration assumptions are applied.

By tracking deployment mix, services attach rates, and suite scope boundaries, Mordor Intelligence keeps the EMM total tied to what buyers actually procure across solutions and ongoing support. This reduces over-counting from adjacent security tools that sit outside EMM programs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.90 B (2025) | |

| Global Consultancy A | USD 19.05 B (2024) | Uses a different base year and a narrower component structure that emphasizes software categories, with services growth treated separately, which can understate the combined solutions plus services total in a given year. |

| Industry Research Publisher B | USD 75.37 B (2023) | States the figure as a forecast increase anchored to a 2023 base and may blend broader mobile security and regional focus coverage into the EMM definition, which can inflate totals when adjacent security spend is counted inside EMM. |

The spread in the table mainly comes from how each publisher draws the boundary around EMM suites versus nearby mobile security tools, and whether services are fully bundled into the same market number. When the scope is kept consistent and assumptions are checked against deployment behavior and buying patterns, the final estimate becomes easier to trace back to clear drivers and to update in a repeatable way.

Key Questions Answered in the Report

What is the projected value of the Enterprise mobility management market by 2031?

It is expected to reach USD 94.47 billion, reflecting an 18.62% CAGR during the forecast period (2026-2031).

Which deployment mode is growing fastest?

Cloud-based platforms exhibit the strongest 18.93% CAGR through 2031 as firms shift from capex to scalable SaaS.

Why is healthcare adoption accelerating?

New HIPAA rules mandating MFA and encryption push hospitals to deploy compliant mobility solutions quickly.

How will Zero Trust affect mobility strategies?

Continuous verification of user and device health will become default, reducing reliance on traditional VPN perimeters.

What regions offer the highest growth potential?

Asia Pacific leads with a 21.74% CAGR thanks to mobile-first policies and expanding 5G coverage.

Are SMEs significant buyers of EMM?

Yes; cloud subscription models and simplified consoles drive a 20.97% CAGR among small and medium enterprises.

Page last updated on: