Enterprise Mobility Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

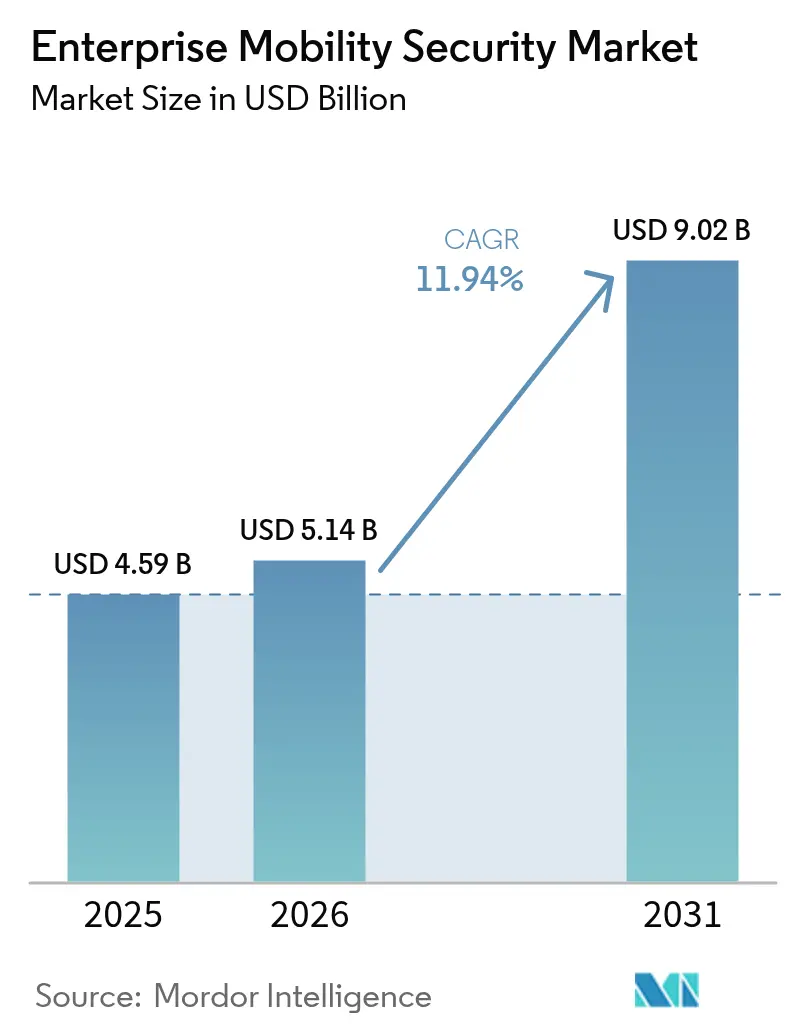

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 9.02 Billion |

| Growth Rate (2026 - 2031) | 11.94% CAGR |

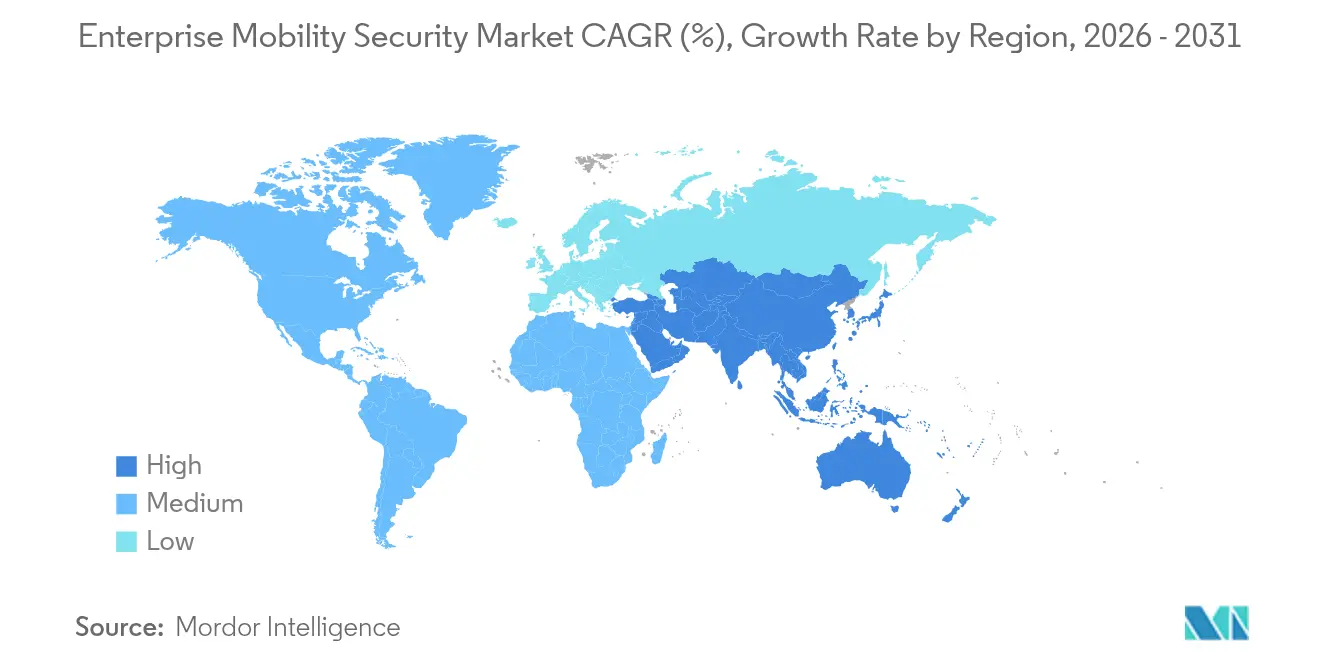

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

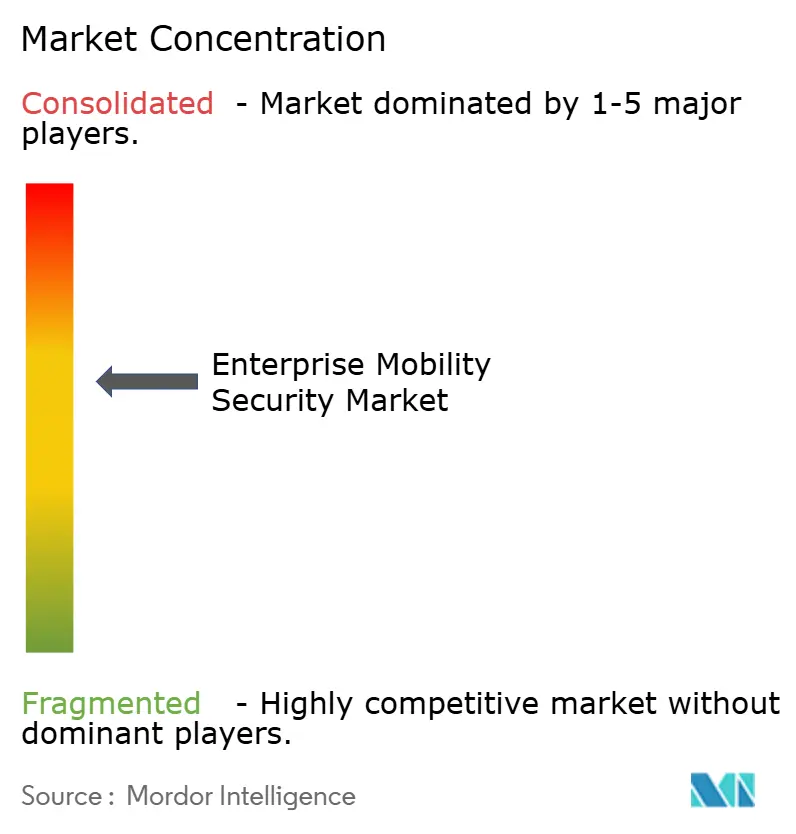

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Mobility Security Market Analysis by Mordor Intelligence

Enterprise Mobility Security market size in 2026 is estimated at USD 5.14 billion, growing from 2025 value of USD 4.59 billion with 2031 projections showing USD 9.02 billion, growing at 11.94% CAGR over 2026-2031. This expansion is catalyzed by normalized bring-your-own-device (BYOD) policies in highly regulated sectors, the surge in mobile-centric ransomware and phishing attacks, and an accelerated shift toward cloud-first architectures among small and medium enterprises (SMEs) that lack legacy perimeter defenses. Smartphones remain the primary corporate endpoint, yet growth momentum is tilting toward wearables as healthcare providers and manufacturers embed biometric sensors into everyday workflows. Cloud deployment retains a clear lead, but hybrid architectures are gaining traction where data-sovereignty laws require local processing. As artificial-intelligence (AI)-driven analytics mature, Mobile Threat Defense (MTD) platforms detect zero-day exploits faster than signature-based tools, pushing spending beyond basic Mobile Device Management (MDM). Competitive intensity is moderate because cross-suite vendors such as Microsoft, VMware, and Cisco leverage existing footprints to bundle mobility controls, while specialist disruptors capture share with stand-alone MTD subscriptions.

Key Report Takeaways

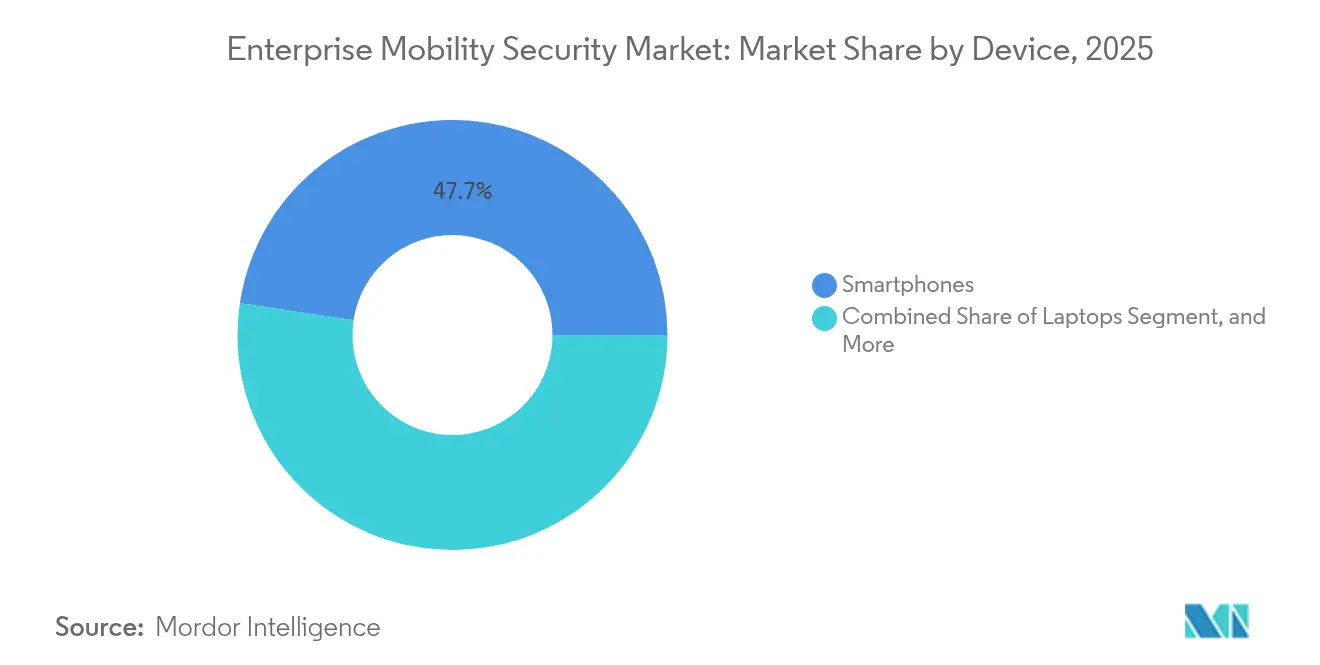

- By device, smartphones commanded 47.65% Enterprise Mobility Security market share in 2025, whereas wearables are advancing at a 14.54% CAGR through 2031.

- By deployment model, cloud captured 60.92% of 2025 revenue, yet hybrid environments are expanding at a 13.98% CAGR on the back of Middle-East sovereignty mandates.

- By security type, MDM accounted for 37.15% of 2025 value, while MTD leads growth at 15.12% annually as AI-driven analytics go mainstream.

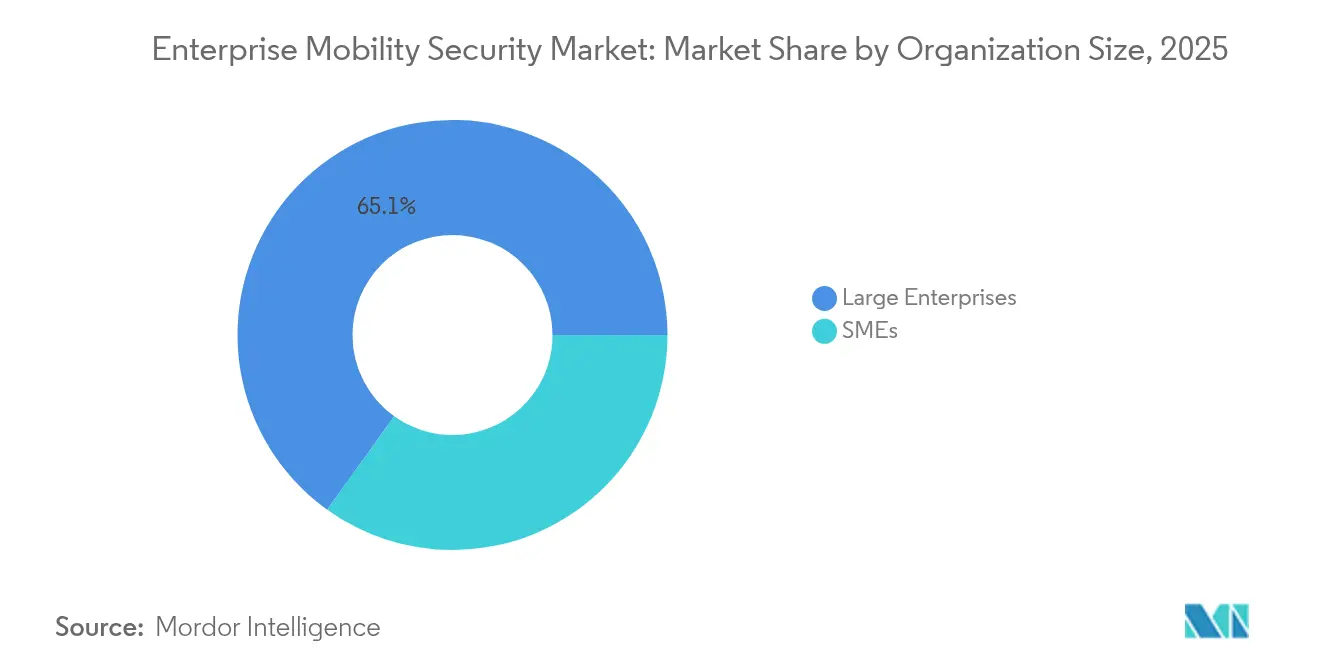

- By organization size, large enterprises generated 65.10% of spending in 2025, but SMEs are on course for a 13.79% CAGR due to managed-service bundles.

- By end user, banking, financial services, and insurance (BFSI) held 41.25% of 2025 revenue, whereas retail and eCommerce are projected to rise at a 15.55% CAGR as tablet-based point-of-sale (POS) terminals proliferate.

- By geography, North America led with 37.70% in 2025, while Asia Pacific is set for the fastest 15.45% CAGR on the strength of digital-first banking initiatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Mobility Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BYOD and remote-work proliferation | +2.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Escalating mobile cyber-threat landscape | +3.2% | Global, acute in BFSI-heavy regions (North America, Asia Pacific) | Short term (≤ 2 years) |

| Cloud-first adoption among SMEs | +2.1% | Asia Pacific, Latin America, emerging Europe | Medium term (2-4 years) |

| Tightening compliance mandates (GDPR, HIPAA, PCI-DSS) | +2.5% | North America, Europe, select Asia Pacific markets | Long term (≥ 4 years) |

| Zero-Trust architecture integration for mobile endpoints | +1.7% | North America, Europe, Middle East | Medium term (2-4 years) |

| Secure mobile DevOps pipeline demand in regulated verticals | +1.2% | North America, Europe (healthcare, BFSI focus) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BYOD and Remote-Work Proliferation

Permanent hybrid-work policies transform employee-owned smartphones into core corporate assets, yet fewer than 40% of organizations containerize personal and business data. Okta observed that 63% of authentication attempts to enterprise applications in January 2025 came from unmanaged mobile devices, up from 48% in 2023. Professional-services employees frequently toggle between consumer messaging and customer-relationship-management apps on the same handset, maximizing phishing exposure. Palo Alto Networks logged a 74% year-over-year rise in mobile phishing targeting remote staff during 1H 2024. Regulatory frameworks such as GDPR and HIPAA impose breach liability but offer scant prescriptive guidance for securing BYOD environments, compelling enterprises to stitch together vendor-specific controls.

Escalating Mobile Cyber-Threat Landscape

Ransomware, banking trojans, and vishing attacks now aim at specific verticals. Lookout identified 3.7 million distinct malware samples in 2024, a 58% increase over the prior year, and found that 22% of enterprise devices encountered at least one high-severity threat. Zimperium reported an 86% rise in voice-phishing events in the banking sector, frequently paired with SIM-swapping to intercept one-time passwords. Apple disclosed 14 exploited iOS zero-days in 2024, while Google patched 11 root-level Android flaws, demonstrating platform-agnostic risk.[1]Apple Security Response, “iOS Vulnerabilities 2024,” Apple, apple.com Generative-AI techniques make malicious messages context-aware, lifting click-through rates and compressing defenders’ reaction windows.

Cloud-First Adoption Among SMEs

SMEs adopt cloud-based unified endpoint management at double the rate of large enterprises, attracted by consumption-based pricing and elimination of infrastructure overhead. Microsoft noted that Intune subscriptions among companies with <1,000 employees grew 47% year-over-year in Asia Pacific by February 2025.[2]Microsoft Intune Product Team, “SMB Adoption Metrics 2025,” Microsoft, microsoft.com Yet Thales found 68% of SMEs lack mobile-security specialists, leaving generalist IT staff to prioritize connectivity over threat mitigation. Multi-cloud deployments compound visibility challenges, while PCI DSS v4.0 mandates encrypting mobile POS transactions, forcing small retailers either to retrofit systems or adopt cloud-native payment gateways.

Tightening Compliance Mandates

Enforcement escalated in 2024 as the European Union levied EUR 1.2 billion (USD 1.3 billion) in GDPR fines, 18% tied to weak mobile protections. The U.S. Department of Health and Human Services issued 14 HIPAA penalties totaling USD 28.5 million for lost or unencrypted devices. PCI DSS v4.0 introduced 53 new controls for mobile apps and POS systems. India’s Digital Personal Data Protection Act adds fines up to INR 2.5 billion (USD 30 million) for mobile-app misuse. Vendors are embedding automated audit trails to lower the manual burden of compliance reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity with legacy IT stacks | -1.8% | North America, Europe (mature enterprises) | Short term (≤ 2 years) |

| Budget constraints for mid-sized enterprises | -1.4% | Global, acute in Asia Pacific and Latin America | Medium term (2-4 years) |

| Talent shortage of mobile-security specialists | -1.1% | Global, most severe in North America and Europe | Long term (≥ 4 years) |

| Fragmented global regulatory requirements | -0.9% | Global, cross-border operations most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy IT Stacks

Organizations running on-premises Active Directory alongside cloud identity providers face multi-year migration paths. Cisco recorded that 54% of large enterprises see authentication failures when federating legacy directories with cloud-based unified endpoint management, necessitating latency-heavy middleware. VMware found 41% of Secure Access Service Edge pilots stall over hard-coded VPN dependencies. Mainframe-centric BFSI firms lack APIs for instant mobile policy updates, pushing synchronization lags to 24 hours and leaving exposure windows open.

Budget Constraints for Mid-Sized Enterprises

Companies employing 500–2,500 staff commit only 8–12% of IT outlays to security. PwC estimated that per-device MTD fees of USD 5–15 often exceed mid-market thresholds. An ISC2 survey showed 47% of these firms defer mobile-security investments in favor of growth initiatives. CrowdStrike pegs mobile-banking fraud losses at USD 1.2 billion in 2024, yet risk perception remains muted. Managed-service bundles aim to bridge gaps but adoption is sluggish in cost-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device: Wearables Build the Next Wave of Adoption

Wearables contributed a modest slice in 2025 but are forecast to expand at 14.54% annually through 2031, outpacing smartphones, laptops, and tablets. Samsung Knox for Wearables, launched April 2024, lets administrators encrypt and remotely wipe smartwatches used to access electronic health records, tackling HIPAA compliance needs. Honeywell’s rugged scanners integrate with VMware Workspace ONE to enforce role-based access, curbing unauthorized shop-floor actions. Smartphones retained 47.65% of device revenue in 2025 owing to BYOD ubiquity, yet their growth curve is flattening as saturation nears in developed markets.

The shift to wearables enlarges the threat surface. Lookout found 14 exploitable flaws in popular fitness-tracker firmware during 2024. Draft U.S. FDA guidance on wearable medical-device cybersecurity will not fully apply until 2027, leaving a multi-year gap wherein innovation outruns regulation. Vendors are rushing firmware-over-the-air update mechanisms to close that gap.

By Deployment Model: Hybrid Balances Sovereignty and Scale

Hybrid architectures are tracking a 13.98% CAGR as enterprises partition workloads between sovereign on-premises enclaves and scalable public clouds. The UAE’s Data Protection Law bars cross-border citizen-data transfers without consent, forcing local unified endpoint management servers while still tapping global threat-intelligence feeds. Cloud deployments commanded 60.92% in 2025, buoyed by subscription-based Intune, Workspace ONE Cloud, and Ivanti Neurons. Edge computing is surfacing as a third pillar, enabling factories to enforce policies on rugged tablets with <80 ms latency using Cisco edge-native modules.

On-premises footprints will decline as talent pools shrink, yet they endure in air-gapped defense networks and mainframe-reliant financial institutions. Vendors now pitch migration toolkits that replicate legacy policies in cloud consoles to ease the transition.

By Security Type: AI-Driven Mobile Threat Defense Outpaces Foundational Controls

Mobile Threat Defense is on track for a 15.12% CAGR through 2031 as behavioral AI models spot exploits before signatures exist. Zimperium’s z9 engine analyzes more than 1,000 device signals in real time, hitting 98.7% detection on unknown threats after its March 2025 update. Lookout now integrates mobile telemetry with Microsoft Defender to trace cross-device attack chains. MDM, while still the baseline at 37.15% of 2025 revenue, is commoditizing as major cloud suites bundle it at no extra cost.

Mobile Application Management encloses enterprise apps in encrypted containers, and unified consoles reduce operational overhead by merging device, application, and identity policy. Microsoft Entra introduced passkey authentication for iOS and Android in January 2025, underscoring the pivot to passwordless mobility. Certification frameworks such as ISO 27001:2022 now embed explicit mobile controls, nudging laggards toward audit-ready tooling.

By Organization Size: Managed Services Accelerate SME Uptake

SMEs are expected to post a 13.79% CAGR, nearly double that of large enterprises, thanks to managed services that substitute specialized staff. Ivanti’s Neurons MTD subscription starts at USD 3 per device per month for sub-500 endpoint fleets, eliminating capital hurdles. Large enterprises still accounted for 65.10% of the 2025 spend, but their growth is tapering as penetration exceeds 80% in mature regions.

Skills shortages persist: Thales reports that 68% of SMEs lack dedicated personnel for mobile security. The PCI DSS v4.0 encryption mandate for mobile POS terminals forces compliance-driven adoption, yet price-sensitive SMEs in less-regulated industries continue to defer rollouts. Vendors respond with outcome-based pricing and shared threat-intelligence feeds.

By End User: Retail and eCommerce Surge on POS Modernization

Retail and eCommerce are projected to grow at a 15.55% CAGR through 2031 as tablet-based POS terminals become mainstream. CrowdStrike tracked a 92% spike in POS malware targeting Android payment terminals during 2024. PCI DSS v4.0 now requires end-to-end encryption and tokenization, raising compliance spend for merchants. BFSI kept 41.25% of 2025 revenue, propelled by USD 1 billion in mobile-fraud losses.

Healthcare systems deploy unified endpoint management to secure wearables and tablets; HIPAA penalties for mobile breaches totaled USD 28.5 million in 2024. Manufacturing companies are embracing rugged tablets and scanners, with Honeywell’s Mobility Edge shipments up 34% in the first half of 2024. Government agencies face sovereignty mandates that favor on-premises deployments even as budgets tighten.

Geography Analysis

North America generated 37.70% of 2025 revenue, driven by strict HIPAA enforcement that prompted healthcare providers to adopt unified endpoint management. A U.S. federal directive required Mobile Threat Defense on all government devices by December 2024, unlocking a procurement wave for Lookout, Zimperium, and CrowdStrike. Canada’s PIPEDA amendment extended breach-notification rules to mobile endpoints, while Mexico’s fintech boom is spurring demand for banking-trojan detection. Growth is steadier than spectacular because the Enterprise Mobility Security market has reached deep deployment levels across Fortune 1000 firms.

The Asia Pacific is projected to have a 15.45% CAGR through 2031, as digital-banking initiatives in India and Indonesia bring millions of unbanked citizens online. Reserve Bank of India guidelines mandate device binding and multi-factor authentication for mobile transactions, driving unified endpoint rollouts at state-owned lenders. China’s data-localization laws favor domestic vendors, such as Huawei, while Japan’s extraterritorial privacy statutes oblige foreign SaaS providers to secure the data of Japanese citizens on mobile devices. Australia’s Notifiable Data Breaches scheme reported that 19% of 2024 incidents involved mobile endpoints, reinforcing purchasing urgency.

Europe tightened oversight via the Network and Information Security Directive 2 in October 2024, obliging telecom operators and clouds to ingest real-time mobile telemetry. GDPR fine volume reached EUR 1.2 billion in 2024, 18% tied to inadequate mobile safeguards. Germany’s BSI now requires Evaluation Assurance Level 4-certified unified endpoint management in critical infrastructure sectors. The United Kingdom’s NCSC is steering agencies toward Zero-Trust mobile architectures that enforce continuous posture checks. Middle-East jurisdictions impose sovereign-cloud laws that necessitate local servers, while Saudi Arabia’s Essential Cybersecurity Controls demand MTD across government devices by end-2025. South America’s opportunity concentrates in Brazil and Argentina, though budget pressures cap widespread rollouts.

Regulatory Landscape

Enterprise mobility security demand is strongly influenced by privacy rules, sectoral security mandates, and government hardening guidance. In the United States, federal requirements for securing mobile applications and devices were codified through GSA CIO-IT Security-12-67 Rev. 7 (October 2024) and OMB M-25-04 (January 2025) for federal information security and privacy management, while DISA published the Apple iOS/iPadOS 26 STIG (January 2026, NIST National Checklist Program ID 1317) to define configuration and compliance expectations for federal environments.

In 2026, national security and defense directives reinforced enterprise requirements that propagate into contractor and supplier ecosystems. OMB M-26-05 (January 2026) shifted federal assurance toward agency-specific, risk-based hardware and software security, and the FY2026 NDAA (P.L. 119-60, enacted April 2026) added cybersecurity requirements relevant to secure mobile device use in defense contracting, including encryption and continuous monitoring. NSPM-12 (June 2026) directed CNSS to develop secure configuration baselines for cloud-based systems and review cloud security policies (CNSSP-32), reinforcing the market shift toward cloud-integrated, zero-trust-aligned mobile controls.

Value Chain Analysis

The enterprise mobility security value chain begins with device OEMs and OS ecosystems, such as Samsung Knox and Android Enterprise, which provide hardware-backed security primitives and management APIs. It then moves to unified endpoint management (UEM/EMM) and identity providers, including Microsoft Intune and Microsoft Entra, which operationalize policy, enrollment, and access controls.

Mobile threat defense and analytics vendors sit on top of this layer, supplying telemetry, phishing and malware detection, and continuous risk scoring that is increasingly routed into SOC workflows and XDR tools. Channel partners and MSPs support downstream adoption by packaging deployments, managed operations, and compliance reporting for both large enterprises and SMEs. Buyer priorities are also shifting toward continuous compliance and update discipline rather than one-time rollout controls. For example, Microsoft enforced stricter Intune Mobile Application Management requirements in January 2026 by blocking outdated iOS and Android apps from launching, pushing more effort into application lifecycle governance and testing across managed fleets. Platform capabilities are further reshaping integration patterns, including Google introducing Device Trust from Android Enterprise (May 2025) to validate device posture via Android Management APIs without full EMM enrollment, and Samsung outlining a zero-trust endpoint strategy in 2026 that integrates Knox with partners such as Cisco Secure Access and Microsoft Intune for device attestation, increasing interoperability needs across identity, device, and network access layers.

Competitive Landscape

The Enterprise Mobility Security market remains moderately fragmented: the top five vendors—Microsoft, VMware, Cisco, BlackBerry, and Ivanti controlled roughly 45% of 2024 revenue. Microsoft Intune, bundled with Microsoft 365 E3/E5 suites, managed over 200 million endpoints by February 2025, cementing switching costs. VMware’s Workspace ONE layers mobility onto its virtual-infrastructure heritage, and its 2025 acquisition of Menlo Security’s mobile unit adds cloud browser isolation. Cisco has fused MTD and Cloud Access Security Broker functions into a Secure Access Service Edge offering priced at USD 12 per device for ≥5,000-endpoint fleets.

Specialists vie for differentiation through AI. Zimperium’s March 2025 z9 algorithm achieves a zero-day detection rate of 98.7%, while Lookout’s acquisition of CipherCloud combines mobile telemetry with cloud-access control for unified analytics. Jamf dominates Apple-centric deployments, holding a market share of over 70% among iOS-heavy organizations. Patent activity underscores the arms race: Microsoft filed 14 patents in 2024 on device attestation and hardware-rooted keys. Talent shortages add friction; ISC2 logs a 4 million-person global cybersecurity gap, and mobile specialists command salary premiums of 20–30%. This scarcity hampers smaller vendors’ ability to scale professional-services revenue.

Enterprise Mobility Security Industry Leaders

BlackBerry Limited

Ivanti Inc. (MobileIron)

VMware Inc.

Citrix Systems Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is securing the mobility management plane itself, as administrative workflows, enrollment processes, and audit logs become high-value targets alongside endpoints. Cloud Security Alliance research (March 2026) highlighted MDM/EMM infrastructure as an enterprise attack surface and pointed to elevated requirements such as phishing-resistant authentication (for example, FIDO2), separation of duties for destructive actions like wipe, unenroll, and policy rollback, and centralized cloud audit log collection. These themes create room for vendors to differentiate beyond baseline MDM features.

Opportunities also continue to form around tighter alignment between mobility security and standards used in procurement. ISO/IEC TS 23220-3:2026 (published June 2026) advances standards-based identity management using mobile devices, while EU product security requirements under the Cyber Resilience Act (Regulation EU 2024/2847) are being translated into harmonized technical standards work, including ETSI EN 304 623 on boot managers, which raises expectations for device integrity and secure startup. At the same time, frequent cloud service release cycles expand feature surface area for Android Enterprise and policy automation, including Microsoft Intune 2606 service release in June 2026, supporting demand for continuous configuration management, regression testing, and managed services that keep fleets compliant through frequent platform changes.

Recent Industry Developments

- July 2026: Ivanti announced a distribution partnership with QBS Software to expand coverage in the DACH region. The move strengthens Ivanti Neurons and mobility-security go-to-market reach through a regional channel that already serves mid-market and enterprise buyers, supporting faster procurement and localized delivery.

- March 2026: BlackBerry expanded and renewed its partnership with the Government of Canada, increasing deployments of BlackBerry UEM and BlackBerry SecuSUITE for sovereign communications. The contract extension reinforces demand signals from public-sector buyers that prioritize controlled data handling and hardened mobile communications stacks.

- August 2025: Broadcom (VMware) introduced VMware Cloud Foundation Advanced Cyber Compliance capabilities aimed at automated compliance management and cyber-risk governance in private-cloud environments. This broadens the compliance automation layer around hybrid and private cloud estates that commonly host mobility management back ends, tightening the linkage between endpoint controls and cloud governance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

Enterprise mobility security is defined as the solutions and related services used by organizations to protect mobile devices, apps, identities, and data when employees access corporate resources outside the office, including BYOD use.

Scope exclusions: Personal consumer security apps, non-enterprise antivirus sold directly to individuals, and telecom network security that is not tied to enterprise mobility controls are excluded.

Segmentation Overview

- By Device

- Smartphones

- Laptops

- Tablets

- Wearables

- By Deployment Model

- On-Premises

- Cloud

- Hybrid

- By Security Type

- Mobile Device Management (MDM)

- Mobile Application Management (MAM)

- Mobile Threat Defense (MTD)

- Unified Endpoint Management (UEM)

- Identity and Access Management for Mobility

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By End-User

- Banking and Insurance

- Healthcare

- IT and Telecom

- Government

- Retail and eCommerce

- Manufacturing

- Other End-User

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to anchor the model to real-world adoption signals. We relied on public, non-paywalled references such as NIST guidance for mobile security controls, CISA advisories, FCC and OECD indicators on mobile and broadband usage, and ITU connectivity statistics, followed by cross-checks from SEC filings and investor presentations of listed security and mobility providers.

For market math, inputs were pulled from enterprise mobility and security standards documentation, association publications, and credible press reporting on mobile threat patterns and enterprise device usage. Patent databases were also reviewed to understand where technical focus is moving, for example mobile threat defense and identity-led access. A paid subscription for company financials and news was used selectively to validate revenue direction and regional exposure. These desk sources are illustrative only, and many other public references were also used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work was used to test what the desk signals could not fully explain, especially how enterprises bundle mobility security with endpoint, identity, and management suites. We spoke with solution providers, channel partners, and enterprise security and IT mobility buyers across the Americas, EMEA, and APAC so assumptions on adoption timing, pricing movement, and the cloud versus on-premises split could be tightened.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 19% | APAC: 51% |

| Mid tier: 48% | Functional/Unit leaders: 25% | EMEA: 29% |

| Smaller Players: 21% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool where enterprise device footprint and remote work exposure are translated into a payable security control layer, which is then split by deployment preference and buying motion. The totals are then corroborated using selective bottom-up checks, such as sampling vendor revenue direction, channel feedback on deal sizes, and ASP times volume approximations for mobile threat defense and unified endpoint controls.

Key inputs used in the model include enterprise smartphone and tablet installed base trends, BYOD policy prevalence, mobile threat incident frequency, cloud identity usage growth, and average contract duration patterns that affect renewal timing. When a bottom-up checkpoint lacks coverage for small or private suppliers, the gap is handled through calibrated uplift factors that are tested against buyer-side spending ranges from interviews. For forecasting, scenario analysis is used around macro IT spending, regulatory pressure in regulated industries, and the pace of cloud migration, and then the final trajectory is adjusted through expert consensus on realistic adoption timing.

Data Validation & Update Cycle

Outputs are validated through multiple passes that compare the model against independent signals such as enterprise mobility management adoption, mobile threat defense attach rates, and stated security budget priorities. Outliers are reviewed, assumptions are re-checked for currency timing and inflation effects, and clarification calls are triggered when a variance looks structural rather than noise.

Before sign-off, the work is reviewed by another analyst to confirm logic, unit consistency, and year alignment. A final pre-delivery check is completed so the latest public updates are reflected. Reports are refreshed annually, with interim updates made when major market events materially change pricing, adoption, or regional demand.

Mordor Intelligence's Enterprise Mobility Security Market Sizing Compared With Other Published Estimates

Published market values for enterprise mobility security can vary a lot, even when the topic label looks the same. The differences usually come from what is counted as mobility security versus adjacent endpoint and identity spend, which year is treated as the starting point, and how fast pricing and adoption are assumed to move.

In practice, the biggest gap drivers are scope and bundling, because some estimates appear to roll in broad endpoint suites or general IAM spend even when it is not mobility-led, and then apply aggressive cloud adoption assumptions across all regions. A second driver is the refresh and currency handling, since FX timing and the chosen average exchange rates can move a global USD number noticeably, especially when APAC growth is modeled faster.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.14 B (2026) | |

| Global Consultancy A | USD 18.35 B (2025) | Uses an earlier base year and appears to capture a wider spend pool across devices, which can pull in broader endpoint or identity-led security budgets that are not strictly mobility-specific. |

| Regional Consultancy B | USD 15.18 B (2024) | Shows a larger starting value that is consistent with broader inclusion of cloud security and IAM themes, with limited clarity on how suite bundling and double counting are removed. |

The spread in the table is mainly explained by whether adjacent security categories are counted, and whether suite revenues are separated cleanly from mobility-only controls. By tying the spend pool to enterprise mobile access use cases and then checking it against pricing and adoption feedback from primary calls, the inclusion choices stay more traceable, a discipline applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the Enterprise Mobility Security market in 2026?

The Enterprise Mobility Security market size is USD 5.14 billion in 2026 and is projected to reach USD 9.02 billion by 2031 at a 11.94% CAGR.

Which device segment is growing the fastest?

Wearables are the fastest-growing segment, tracking a 14.54% CAGR as hospitals and factories embed biometric sensors into daily workflows.

Why are SMEs adopting Enterprise Mobility Security solutions quickly?

Managed-service bundles priced as low as USD 3 per device per month remove capital barriers and offset the shortage of dedicated mobile-security staff.

Which region offers the highest growth potential?

Asia Pacific is forecast for the strongest regional CAGR of 15.45% through 2031, driven by digital banking in India and Indonesia.

What regulatory changes are influencing vendor roadmaps?

PCI DSS v4.0, GDPR fines, HIPAA penalties, and Indias Digital Personal Data Protection Act all demand stronger mobile controls, prompting vendors to embed audit automation and AI-driven telemetry.

Who are the leading vendors?

Microsoft, VMware, Cisco, BlackBerry, and Ivanti head the pack, collectively accounting for ?45% of 2024 revenue, while Lookout, Zimperium, and Jamf lead in specialized niches.

Page last updated on: