Recruitment Marketing Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

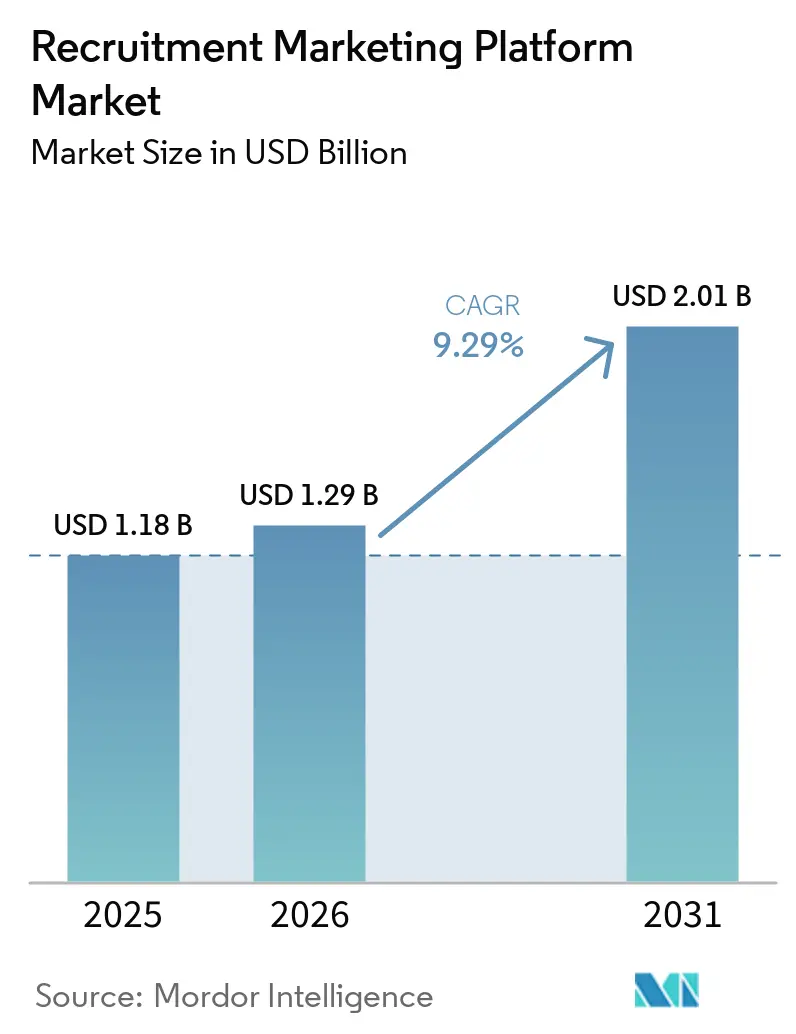

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

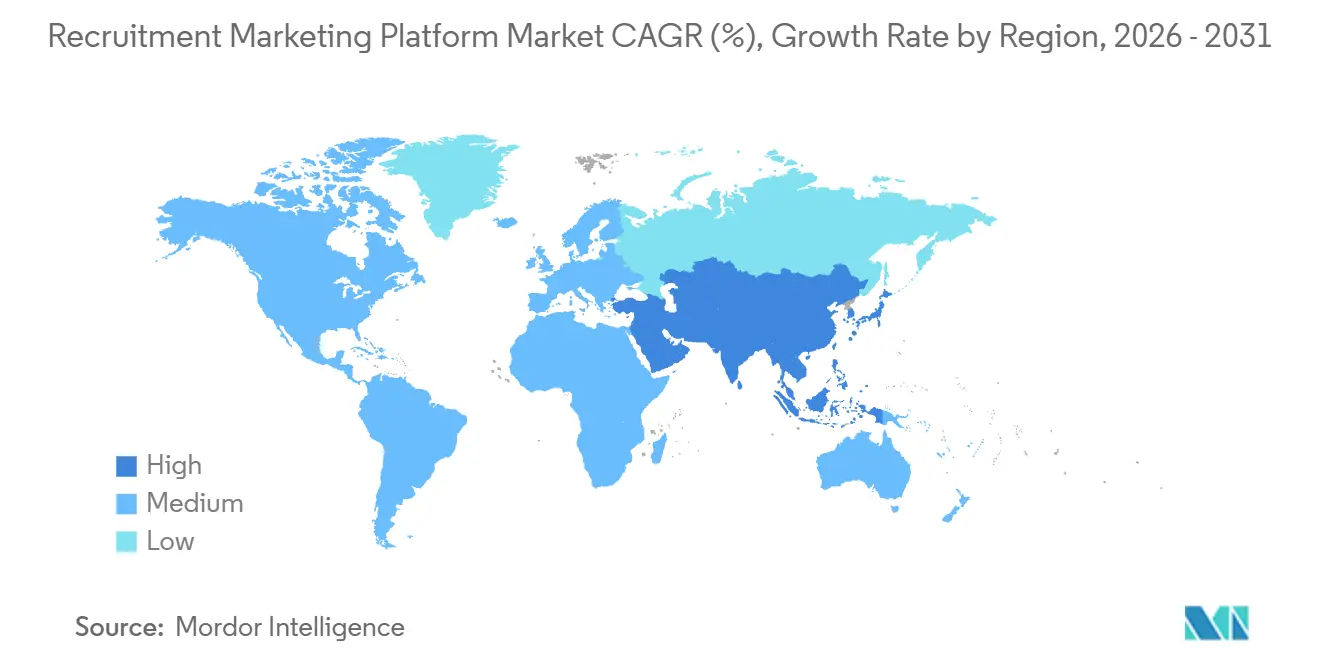

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

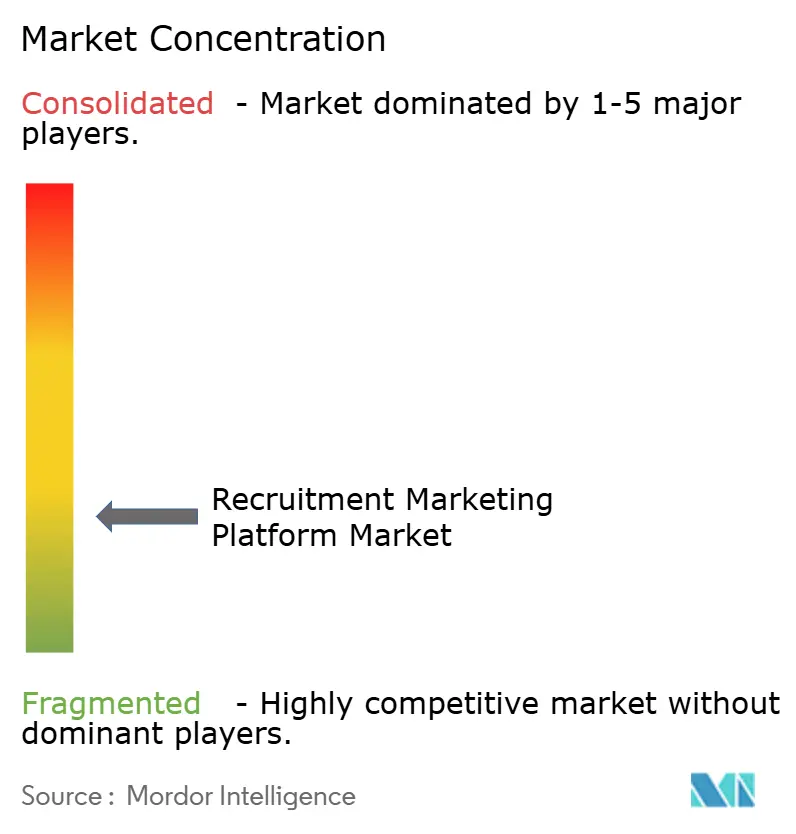

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recruitment Marketing Platform Market Analysis by Mordor Intelligence

The recruitment marketing platform market size is projected to expand from USD 1.18 billion in 2025 and USD 1.29 billion in 2026 to USD 2.01 billion by 2031, registering a CAGR of 9.29% between 2026 and 2031. The recruitment marketing platform market is growing because employers are moving away from basic job posting models and are building structured candidate engagement systems with clearer performance tracking. The market is also benefiting from the separation of recruitment marketing from applicant tracking, which is pushing buyers to invest in dedicated platforms rather than depend on general HR tools alone. Consolidation among major HCM vendors is raising competitive pressure and is making product depth, integration strength, and service capability more important in enterprise buying decisions. Demand is widening across cloud delivery, analytics-led campaign management, and employer branding workflows, while implementation and integration services are becoming more central as hiring environments become more complex. Regional momentum remains uneven, with North America holding the largest base while Asia-Pacific is creating the strongest expansion path for the recruitment marketing platform market through mobile-first hiring, digital adoption, and broader use of cloud-based talent technology.

Key Report Takeaways

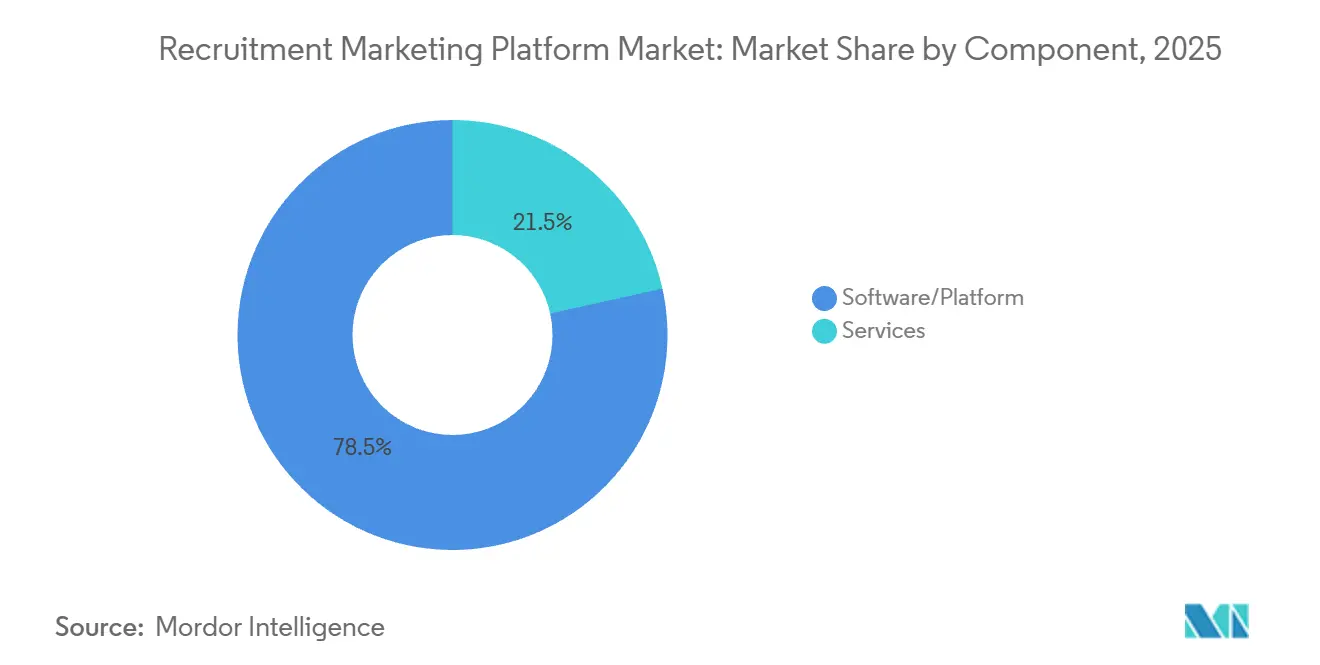

- By component, software and platforms held 78.46% of revenue in 2025, while services are forecast to grow at a 10.84% CAGR through 2031.

- By deployment type, cloud-based deployment accounted for 71.18% of revenue in 2025 in the recruitment marketing platform market and is also the fastest-growing segment with a 10.21% CAGR through 2031.

- By organization size, large enterprises held 69.72% of revenue in 2025, while SMEs are projected to expand at a 10.67% CAGR through 2031.

- By functionality, job distribution and posting led the recruitment marketing platform market with a 27.84% share in 2025, while programmatic job advertising is expected to grow at a 12.46% CAGR through 2031.

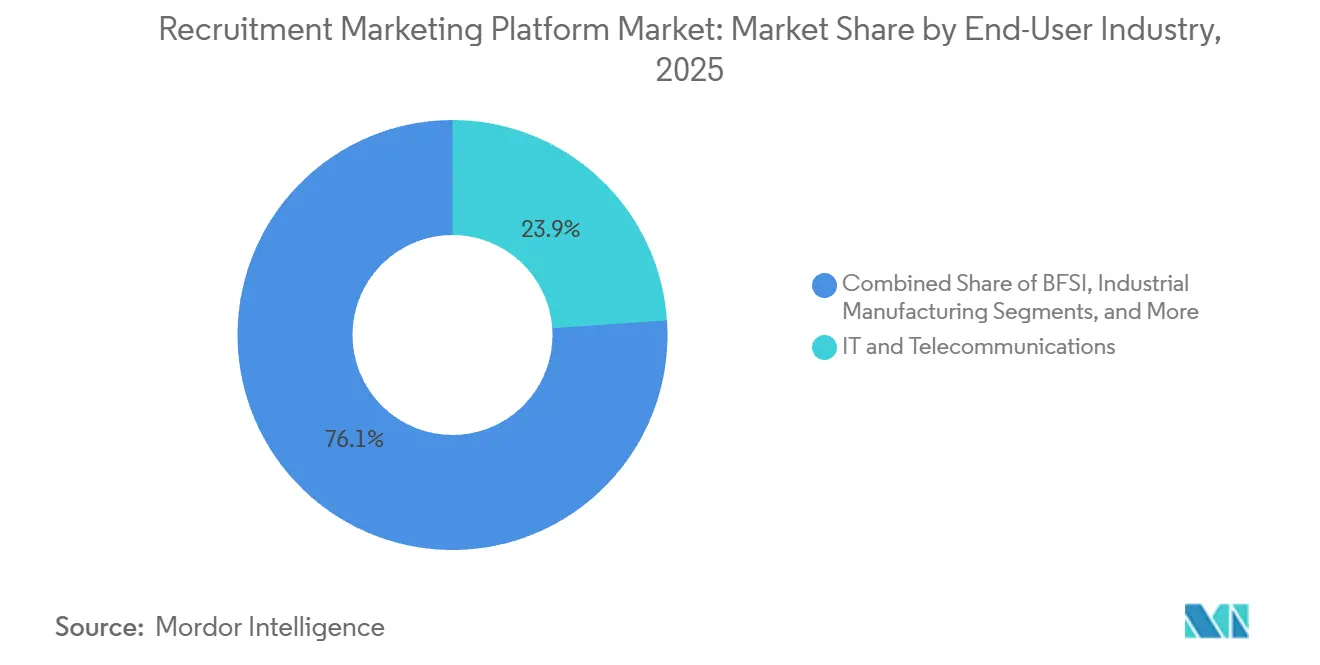

- By end-user industry, IT and telecommunications accounted for 23.91% of revenue in 2025, while healthcare and lifesciences is projected to grow at an 11.28% CAGR through 2031.

- By geography, North America held 38.64% of global revenue in 2025, while Asia-Pacific is projected to record the fastest regional CAGR of 11.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recruitment Marketing Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In Programmatic Job Advertising Adoption | +2.1% | Global, with concentration in North America and Western Europe | Short term (≤ 2 years) |

| Increasing Use Of AI-Powered Candidate Relationship Management | +1.8% | Global, strongest in North America and core Asia-Pacific, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Expansion Of Employer-Branding Budgets Among Enterprises | +1.4% | North America and Europe, with early gains in Australia and New Zealand | Medium term (2-4 years) |

| Surge In Mobile-First Job Search Behavior | +1.1% | Core Asia-Pacific, South America, the Middle East and Africa, with secondary impact in North America | Short term (≤ 2 years) |

| Rising Demand For Data-Driven Recruiting Metrics | +0.8% | North America and Europe | Medium term (2-4 years) |

| Acceleration Of Remote and Hybrid Work Hiring Models | +0.6% | Global, with early gains in North America and Northern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth In Programmatic Job Advertising Adoption

Programmatic job advertising is moving from a specialist workflow into a more standard buying layer within the recruitment marketing platform market. Employers are using it to shift spending across channels in real time instead of relying on fixed job board allocations. This change matters because the value of the system improves as campaign history builds and as bid and conversion data become more useful over repeated hiring cycles. That feedback loop is helping algorithmic media buying pull ahead of manual placement methods, especially where employers recruit continuously across many roles. The pace of that shift is reflected in programmatic job advertising being the fastest-growing functionality segment in the recruitment marketing platform market, with a projected 12.48% CAGR through 2031.

Increasing Use Of AI-Powered Candidate Relationship Management

AI-led candidate relationship management is becoming more central to how the recruitment marketing platform market supports hiring between active requisition cycles. Employers increasingly want platforms that can help them maintain warm talent pools, personalize outreach, and guide recruiters toward higher-probability candidates. This is changing CRM from a passive contact database into an active operating layer for sourcing, re-engagement, and campaign timing. It also raises the importance of governance, because buyers now expect human oversight, documentation, and auditability in AI-supported recruiting workflows. As a result, the recruitment marketing platform market is favoring vendors that combine automation with control features rather than vendors that add AI tools without a clear compliance structure.

Expansion Of Employer-Branding Budgets Among Enterprises

Employer branding is taking a larger role in the recruitment marketing platform market because employers are treating it as a measurable part of candidate demand generation rather than as a simple awareness activity. Budget decisions now reflect the need to improve attraction quality before an application even begins. That shift supports platforms that can manage career content, campaign consistency, and brand performance in one place. It also reduces dependence on paid posting channels when a stronger employer presence improves direct traffic and lowers paid acquisition pressure. The recruitment marketing platform market is therefore seeing stronger demand for platforms that connect branding activity with candidate engagement and downstream hiring results.

Surge In Mobile-First Job Search Behavior

Mobile behavior is reshaping the recruitment marketing platform market because job discovery and application activity now happen primarily on phones for many candidate groups. PeopleScout reported that 91% of job seekers applied by mobile, while 30% used mobile exclusively, which shows how central phone-based workflows have become in candidate engagement.[1]PeopleScout, “Outthink Index: Employer Brand Study Finds Critical Gaps,” Stock Titan, stocktitan.net Appcast also reported that mobile devices accounted for 66.7% of all job applications, reinforcing the importance of mobile-first design across job search and apply flows. This behavior is pushing vendors to improve form completion, profile reuse, and re-engagement tools such as SMS-based follow-up. In the recruitment marketing platform market, that pressure is strongest in high-volume hiring, where speed, ease of use, and shorter application steps directly affect conversion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy ATS and HRIS | -1.5% | Global, most acute in North America and Europe where legacy ATS penetration is highest | Medium term (2-4 years) |

| Data-Privacy and Compliance Constraints | -1.2% | Europe and North America, with spillover to core Asia-Pacific and the Middle East and Africa | Short term (≤ 2 years) |

| Budget Pressures in SME Segments During Economic Downturns | -0.9% | Global, with concentration in South America and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Limited Analytics Maturity in Emerging Markets | -0.5% | Africa, the Middle East, and the rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity With Legacy ATS And HRIS

Integration with older HR systems remains one of the clearest limits on expansion in the recruitment marketing platform market. Remote reported in 2025 that 51% of HR leaders were searching for a new HRIS, and 36% were considering a full system switch, which points to broad dissatisfaction with fragmented system environments.[2]Remote, “Remote Global Workforce Report,” Remote, remote.com The same report noted that a single compliance incident linked to integration failure could cost USD 42,000, which turns technical gaps into a direct financial risk for buyers. This is why vendors with pre-built connectors to major ATS and HCM systems enter enterprise evaluations from a stronger position. In the recruitment marketing platform market, broad native integration support is becoming a buying requirement rather than a feature advantage.

Data-Privacy And Compliance Constraints

Privacy rules are slowing some deployments in the recruitment marketing platform market because candidate data handling now carries legal, process, and product design obligations across multiple jurisdictions. GDPR and CCPA have already increased the amount of governance employers expect from recruiting technology providers. The EU AI Act adds another layer by classifying most recruitment AI use cases as high risk, requiring transparency, documented oversight, and reviewability. These conditions raise engineering and legal costs for vendors and lengthen decision cycles for employers, especially in Europe. In the recruitment marketing platform market, compliance capability is therefore becoming part of product value, not a separate legal consideration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Points To Deeper Operational Dependence

Software/platform licenses accounted for 78.46% of revenue in 2025, giving them the largest revenue base in the recruitment marketing platform market. That weighting reflects how deeply SaaS subscriptions are embedded in hiring technology environments across large enterprise and mid-market buyers. The software layer still anchors most buying decisions because employers need campaign management, workflow control, and candidate engagement within a single operating system. Even so, the faster movement is occurring in services, which are forecast to expand at a 10.84% CAGR through 2031. This shows that the recruitment marketing platform market is moving into a phase where successful adoption depends on more than license access.

Services are growing faster because buyers increasingly need implementation help, integration work, reporting design, and managed analytics support after the initial software purchase. This pattern suggests that the recruitment marketing platform industry is becoming more operationally complex as platforms connect with ATS, HRIS, analytics, and media systems across different regions and business units. It also indicates that platform value is being judged on measurable usage and performance, not just on feature breadth. At the same time, basic distribution and engagement features are becoming easier for broader HCM suites to bundle, which narrows room for mid-tier software-only vendors. SHRM reported that HR technology spending rose 9.1% year over year in 2025, but that spending was increasingly tied to tools that could show return from source to hire, which supports the stronger services outlook in the recruitment marketing platform market.[3]SHRM, “CHRO Benchmarking Data Brief,” SHRM, shrm.org

By Deployment Type: Cloud Expansion Continues To Narrow On-Premises Headroom

Cloud-based deployment accounted for 71.18% of the recruitment marketing platform market size in 2025, making it the dominant delivery model across buyer groups. It is also forecast to grow at a 10.21% CAGR through 2031, which confirms that most new adoption is staying on the cloud path. The appeal is practical because cloud architectures support faster product updates, easier compliance changes, and broader integration maintenance across clients. These advantages are especially important where AI models, channel connectors, and campaign tools need frequent adjustment. For that reason, the recruitment marketing platform market is continuing to consolidate around multi-tenant SaaS models.

On-premises demand remains prevalent in regulated settings such as government, defense, and selected financial services environments, where infrastructure control and data residency continue to influence procurement decisions. A meaningful secondary shift is the rise of private cloud and hybrid models for large institutions that want more control without full on-premises cost and maintenance. That flexibility matters because some large employers are reevaluating system architecture through the lens of integration quality, governance, and data flow rather than deployment style alone. Remote found that unified system integration was the main driver of HRIS replacement decisions in 2025, which supports the view that cloud selection is now tied closely to ecosystem fit. In the recruitment marketing platform market, vendors that can support cloud-led deployment with reliable integration into legacy and modern HR systems are in a better position to capture replacement cycles.

By Organization Size: SME Momentum Broadens The Buyer Base

Large enterprises held 69.72% of revenue in 2025, which shows that the recruitment marketing platform market still depends heavily on larger employers with established hiring technology budgets. Their lead reflects longer adoption cycles, larger recruiting teams, and greater need for cross-channel coordination at scale. Enterprise buyers also tend to require stronger analytics, more integrations, and broader governance controls, which lifts contract value. However, the faster growth path belongs to SMEs, which are projected to expand at a 10.67% CAGR through 2031. This makes SMEs a key source of new logo growth for the recruitment marketing platform market.

SME demand is rising because cloud-native tools have lowered entry barriers for candidate relationship management, employer branding, and job distribution. Pipedrive reported in 2026 that a majority of small and medium businesses planned to expand headcount, which aligns with rising interest in digital hiring tools among smaller employers.[4]Pipedrive, “Pipedrive Releases State of SMB Hiring Report: Majority of Businesses Plan to Expand Headcount in 2026,” Pipedrive, pipedrive.com Vendors are responding with modular offers that let smaller buyers adopt selected capabilities without committing to a full suite from day 1. That approach matters because subscription churn in smaller accounts is often higher, and buyers want visible results quickly after deployment. The recruitment marketing platform industry is therefore adapting its onboarding, pricing, and reporting models to fit a customer base that values speed to proof of value as much as long-term platform breadth.

By End-User Industry: Healthcare Gains Speed While IT And Telecom Hold Scale

IT and telecommunications accounted for 23.91% of the recruitment marketing platform market share in 2025, making it the largest end-user industry. That lead reflects constant hiring demand across software engineering, cloud infrastructure, cybersecurity, and other specialist digital roles. Employers in this vertical usually need a continuous pipeline-building approach rather than campaign activity tied only to open requisitions. This makes them strong users of CRM-led engagement, talent communities, and analytics-driven sourcing. As a result, the recruitment marketing platform market still draws a large part of its installed base from technology-oriented employers.

Healthcare and lifesciences, however, are projected to grow at an 11.28% CAGR through 2031, which gives the vertical the strongest forward pace in the recruitment marketing platform market size. That acceleration is tied to persistent shortages in clinical and specialized roles, which are pushing employers away from reactive agency-heavy hiring models. Hospitals and life sciences employers increasingly need candidate nurturing, mobile-ready career journeys, and targeted outreach for hard-to-fill positions. BFSI, industrial manufacturing, and retail and e-commerce also remain important because each brings a distinct hiring profile, with compliance-heavy workflows in BFSI, volume hiring in manufacturing, and seasonal campaign pressure in retail. Government adoption is developing more slowly, but the need for secure digital hiring infrastructure means the recruitment marketing platform market still has a longer-run opportunity in public sector accounts.

By Functionality: Programmatic Spend Control Is Redefining Feature Value

Job distribution and posting held 27.84% of revenue in 2025, which kept it as the largest functional layer in the recruitment marketing platform market. That position makes sense because distribution is often the first structured capability employers buy when moving beyond manual recruitment processes. It remains the most common entry point for employers that want visibility across channels without rebuilding the full recruiting stack immediately. Still, the highest growth is moving toward programmatic job advertising, which is projected to rise at a 12.46% CAGR through 2031. This shift shows that the recruitment marketing platform market is placing more value on spend efficiency and channel optimization than on posting reach alone.

Candidate relationship management and employer branding are also gaining importance, as employers seek to reduce reliance on paid distribution by improving direct attraction and re-engagement. Analytics and reporting functions are becoming more central as HR leaders face stronger pressure to connect spend with cost-per-hire, source quality, and acceptance outcomes. SHRM reported a median cost-per-hire of USD 5,475 in 2025, providing employers with a concrete benchmark for evaluating the return on workflow automation and channel performance tools. The broader result is that standalone point features are less persuasive unless they connect to a shared data model and clear attribution path. In the recruitment marketing platform market, platforms that unify distribution, CRM, branding, and analytics are better placed to defend value as functional expectations rise.

Geography Analysis

North America held 38.64% of the recruitment marketing platform market share in 2025, which kept the region in the top position. That lead came from mature HR technology adoption, strong enterprise buying capacity, and a well-developed recruiting software ecosystem. SHRM reported that HR budgets rose 9.1% year over year in 2025 and that the median HR-expense-to-operating-expense ratio was 2.4%, which suggests that hiring technology spending remained protected despite broader cost discipline. The United States remained the core market, while Canada followed a similar enterprise-buying pattern, and Mexico remained earlier in its adoption curve. Across the recruitment marketing platform market, the region also stood out for major consolidation activity, including SAP’s acquisition of SmartRecruiters and Workday’s acquisition of Paradox, which changed the competitive landscape for many independent vendors.

Europe remained the second-largest regional market in the recruitment marketing platform market, supported by enterprise demand in Germany, the United Kingdom, and France. Germany carried particular weight because strict privacy and consent requirements there often functioned as a practical compliance benchmark for wider EU platform adoption. Enterprise buyers across Germany and the Nordics increasingly treated information security certification as a basic procurement requirement rather than as a differentiator. The EU AI Act is likely to drive a medium-term platform refresh cycle as employers review current systems for transparency, documentation, and human oversight needs.

Asia-Pacific is projected to grow at an 11.93% CAGR through 2031, making it the fastest-growing regional segment in the recruitment marketing platform market size. The region is gaining from rapid digital hiring adoption, large candidate pools, and strong mobile engagement behavior across India and Southeast Asia. In September 2025, eRoad reported that AI adoption in Chinese recruitment reached 84.13% of surveyed companies, pointing to a market where AI-enabled hiring tools are already mainstream.[5]eRoad, “AI Recruitment in China: Survey of 84.13% Adoption Rate,” eRoad, ersoft.com The Middle East is also advancing through localization-driven hiring programs in Saudi Arabia and the UAE, while Africa remains earlier stage with South Africa and Nigeria as the clearest adoption hubs. South America continues to build from Brazil and Argentina, where local language capability and labor reporting fit remain important selection criteria in the recruitment marketing platform market.

Competitive Landscape

The recruitment marketing platform market remains fragmented, with a concentrated top tier and a wide field of specialists competing below it. Large HCM vendors are increasing their role in the space because recruitment marketing capabilities now support broader talent-suite retention and expansion. SAP completed its acquisition of SmartRecruiters in September 2025, adding a platform that served more than 140 million candidates and 4,000 organizations to its SuccessFactors portfolio. Workday also completed its acquisition of Paradox in October 2025, reinforcing the view that conversational AI and candidate experience tools are now core components of enterprise talent suites. These moves are tightening differentiation windows for independent vendors in the recruitment marketing platform market.

Independent platforms are responding by building deeper ecosystem links and by pushing into specialized feature areas where large suites still have execution gaps. Phenom launched a new partner program and marketplace in September 2025, with integrations and co-selling arrangements with Deloitte, SAP, Workday, and UKG, expanding its route to enterprise accounts without requiring the same direct sales footprint as suite vendors. Beamery announced LinkedIn CRM Connect in May 2025, which strengthened the way sourcing and engagement workflows connect inside its platform. These moves show that the recruitment marketing platform market is increasingly rewarding vendors that can sit inside larger HR technology ecosystems while still offering distinct workflow value. Vendors that lack integration depth or differentiated intelligence are likely to face stronger pricing pressure as the market matures.

White-space remains strongest in frontline and high-volume hiring, where candidate behavior is mobile-first and application journeys often depend on SMS or conversational flows. Eightfold AI launched Recruiter Agent in August 2025 and positioned it around high-volume hiring, with reported gains of up to 50% more candidate coverage per role and time savings of around 4 hours per role in sourcing and screening. Symphony Talent launched Career Finder in April 2026 to replace keyword-driven job search with conversational discovery on career sites, reflecting the same push toward simpler candidate matching and lower drop-off. In this setting, AI model quality, data network effects, and compliance-ready design are becoming stronger sources of competitive separation. The recruitment marketing platform market is therefore moving toward a structure where platform scale matters, but workflow specialization still creates room for focused vendors with clear product depth.

Recruitment Marketing Platform Industry Leaders

Jobvite Inc.

iCIMS Inc.

Beamery Ltd.

SmartRecruiters Inc.

Avature Holding Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launched TalentForge at its Cultivate 2026 conference, enabling enterprises to build custom HR software natively within the platform; the announcement included an Oracle integration for agentic interviewing, extending AI-orchestrated hiring workflows across enterprise ERP ecosystems.

- March 2026: iCIMS introduced iCIMS Frontline AI, targeting high-volume frontline hiring via SMS, WhatsApp, and web channels. Early deployments reported up to 75% reduction in time-to-fill and 10x more hires per recruiter, demonstrating material efficiency gains for retail, healthcare, and logistics clients.

- February 2026: Phenom completed the acquisition of Be Applied, a behavioral assessment company, ahead of the Plum acquisition two months later, as part of a capability-build strategy targeting skills-based and bias-reduced hiring workflows.

- December 2025: Symphony Talent launched Tala, an AI recruiting assistant, and a GenAI Email Builder embedded within its CRM module, enabling recruiters to generate personalized candidate outreach communications without leaving the core platform.

Global Recruitment Marketing Platform Market Report Scope

The recruitment marketing platform market includes software platforms and related services used by enterprises to attract, engage, nurture, and convert job candidates through employer branding, programmatic job advertising, candidate relationship management (CRM), recruitment analytics, career-site optimization, automated communication workflows, and multi-channel recruitment campaign management.

The Recruitment Marketing Platform Market Report is Segmented by Component (Software/Platform, and Services), Deployment Type (Cloud-based, and On-premises), Organization Size (Large Enterprise, and SMEs), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, Healthcare and Lifesciences, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), Functionality (Candidate Relationship Management, Job Distribution and Posting, Recruitment Analytics and Reporting, Employer Branding, Programmatic Job Advertising, and Other Functionality Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software/Platform |

| Services |

| Cloud-based |

| On-premises |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecommunications |

| BFSI |

| Industrial Manufacturing |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| Candidate Relationship Management |

| Job Distribution and Posting |

| Recruitment Analytics and Reporting |

| Employer Branding |

| Programmatic Job Advertising |

| Other Functionality Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software/Platform | |

| Services | ||

| By Deployment Type | Cloud-based | |

| On-premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-User Industry | IT and Telecommunications | |

| BFSI | ||

| Industrial Manufacturing | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Functionality | Candidate Relationship Management | |

| Job Distribution and Posting | ||

| Recruitment Analytics and Reporting | ||

| Employer Branding | ||

| Programmatic Job Advertising | ||

| Other Functionality Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the recruitment marketing platform space?

The recruitment marketing platform market is estimated at USD 1.29 billion in 2026 and is forecast to reach USD 2.01 billion by 2031, growing at a 9.29% CAGR.

Which region leads global demand for recruitment marketing platforms?

North America led with 38.64% of revenue in 2025, supported by mature enterprise HR technology adoption and strong spending capacity.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to record the fastest growth at an 11.93% CAGR through 2031 because of digital hiring expansion, mobile-first engagement, and broader cloud adoption.

Which function is expanding the fastest in recruitment marketing platforms?

Programmatic job advertising is projected to grow at a 12.46% CAGR through 2031, showing that employers are shifting toward algorithmic spend optimization and away from manual posting allocation.

Why are services growing faster than software licenses?

Services are forecast to grow at a 10.84% CAGR because employers increasingly need implementation, integration, analytics support, and managed optimization alongside software subscriptions.

Page last updated on: