Mobility And Relocation Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

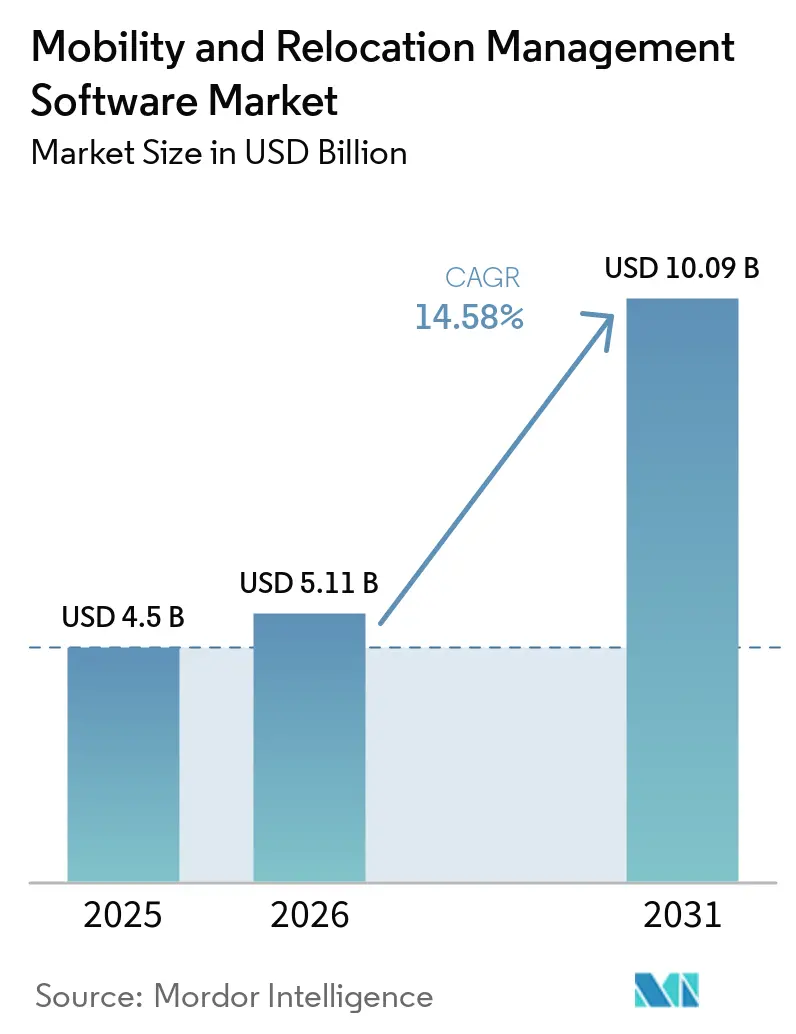

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2031) | USD 10.09 Billion |

| Growth Rate (2026 - 2031) | 14.58% CAGR |

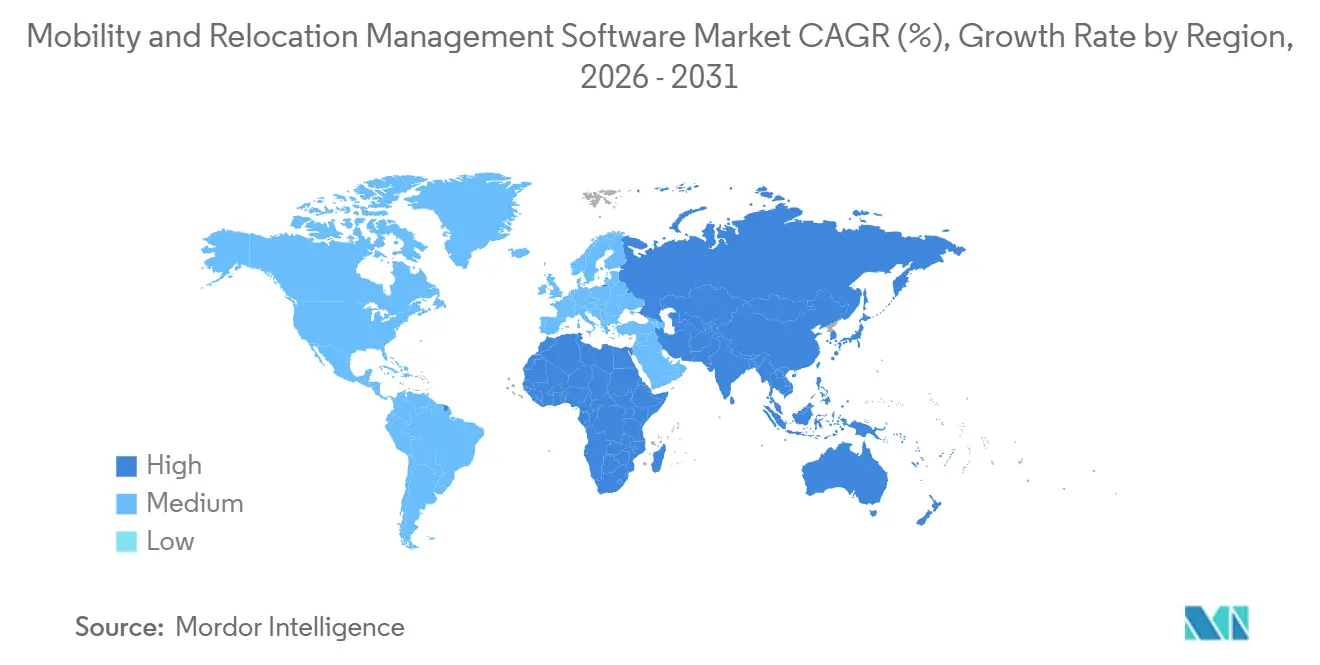

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobility And Relocation Management Software Market Analysis by Mordor Intelligence

The mobility and relocation management software market size is projected to expand from USD 4.50 billion in 2025 and USD 5.11 billion in 2026 to USD 10.09 billion by 2031, registering a CAGR of 14.58% between 2026 and 2031. The mobility and relocation management software market is growing as enterprises move away from manual tracking toward platforms that combine immigration workflows, assignment administration, and compliance reporting in a single operating system. Talent shortages continue to support demand, as employers are finding it harder to secure the skills they need across local labor markets, pushing more hiring and deployment activity across borders and into non-traditional corridors. Product demand is also being shaped by a broader platform refresh cycle, as mobility teams adopt generative and agentic AI tools but still face gaps in data trust, which increases spending on software to improve data quality and real-time visibility. North America remained the largest regional base in 2025, while Asia-Pacific is set to expand fastest as manufacturing growth, intraregional talent movement, and HR digitization lift software adoption across the region. Growth is also supported by rising demand for managed services, policy changes in the United States that are redirecting technical hiring flows to Canada, Mexico, and Ireland, and higher relocation costs that are making centralized control more important for enterprise mobility programs.

Key Report Takeaways

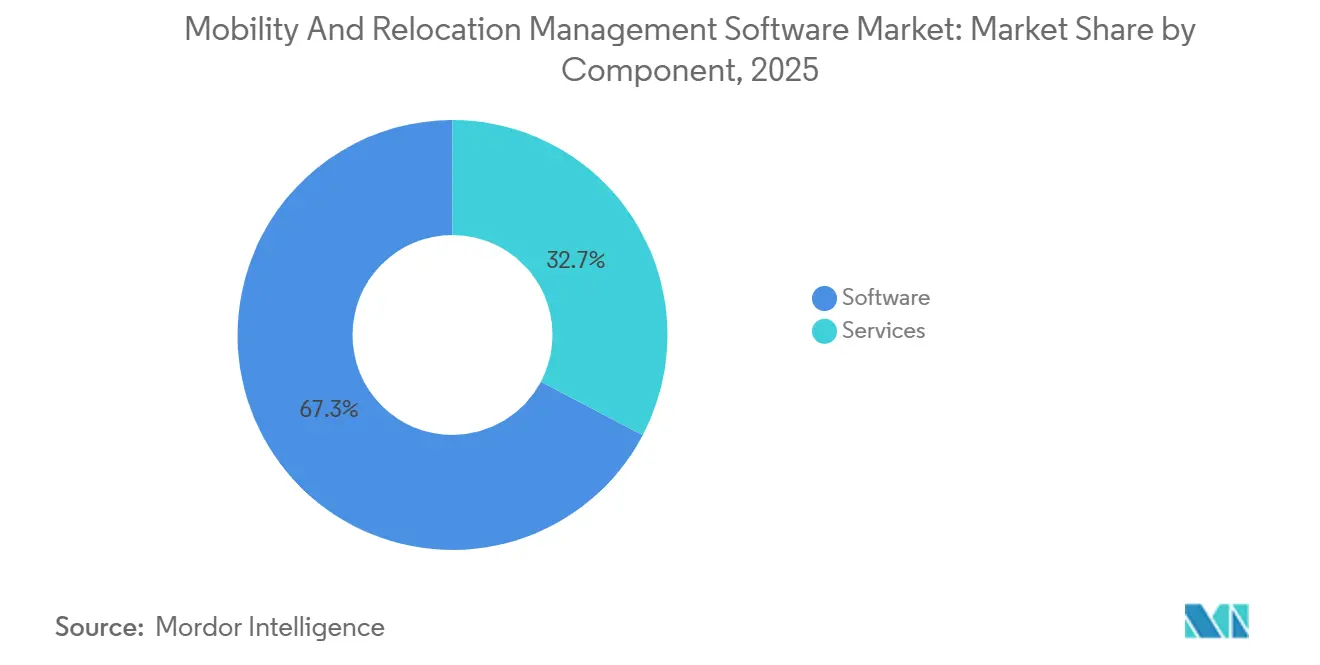

- By component, software held 67.28% of the market in 2025, while services are projected to expand at a 19.47% CAGR through 2031 in the mobility and relocation management software market. The mobility management platforms held the leading 32.31% share within the software component in 2025.

- By deployment mode, cloud-based deployment held 69.12% of the market in 2025, while hybrid deployment is projected to grow at a 20.36% CAGR through 2031.

- By end-user enterprise size, large enterprises accounted for 62.73% of the market in 2025, while small and medium-sized enterprises are projected to expand at a 21.28% CAGR through 2031.

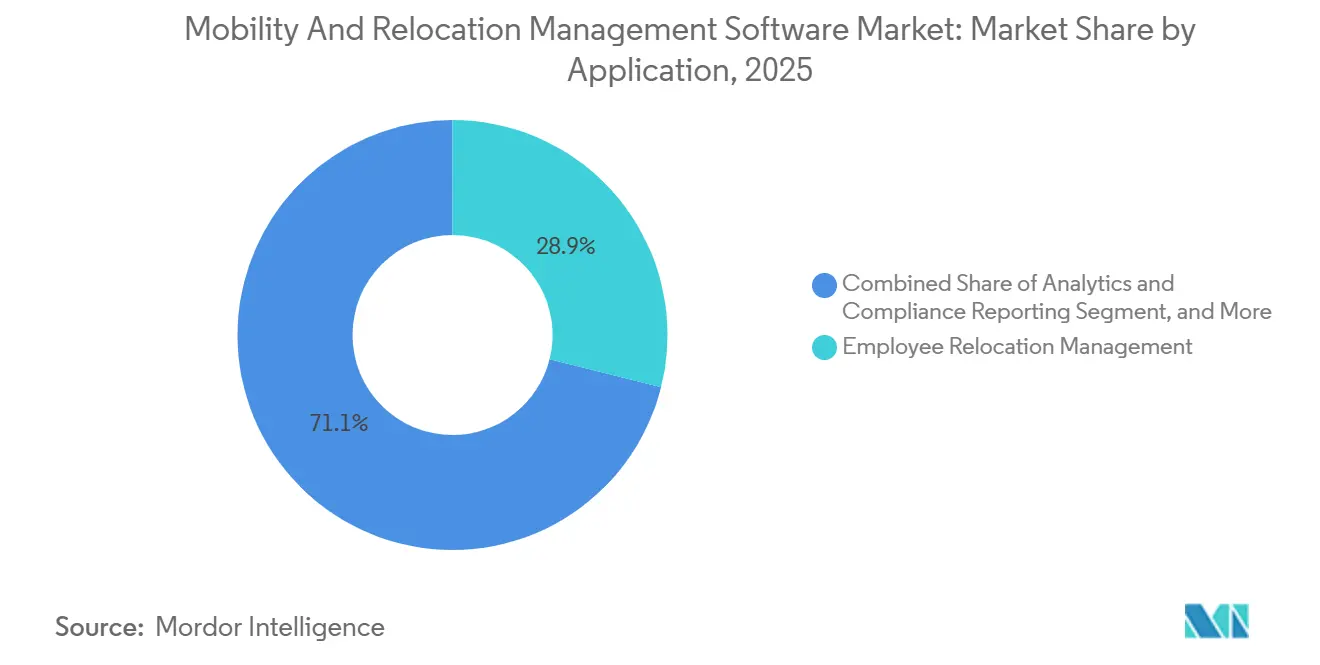

- By application, employee relocation management held 28.91% of the market in 2025, while analytics and compliance reporting are projected to grow at a 22.14% CAGR through 2031.

- By end-user industry, information technology and telecom accounted for 24.63% share of the mobility and relocation management software market in 2025, while healthcare and life sciences are projected to expand at a 23.58% CAGR through 2031.

- By geography, North America held 41.77% of the market in 2025, while Asia-Pacific is projected to grow at a 24.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobility And Relocation Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Cross-Border Hiring And Distributed Work Policies | +3.8% | Global, concentrated impact in North America, Europe, and APAC | Short term (≤ 2 years) |

| Rising Need For Centralized Immigration, Tax, And Payroll Compliance | +3.2% | Global, highest in North America and EU, growing in Middle East and APAC | Medium term (2-4 years) |

| Shift From Spreadsheets To Integrated Mobility Automation | +2.6% | Global, early gains in North America and Western Europe | Short term (≤ 2 years) |

| Growth In Flexible Mobility Policies Such As Lump Sum And Core-Flex Programs | +1.8% | North America and Europe core, spill-over to APAC and Middle East | Medium term (2-4 years) |

| Need To Govern Short-Term Project Moves, Group Moves, And Internal Talent Deployments | +1.3% | Global, highest in BFSI and IT sectors in North America and Europe | Long term (≥ 4 years) |

| Demand For Integrated Mobility Ecosystems Connecting Human Capital Systems, Payroll, Travel, And Vendors | +1.0% | Global, concentrated in large enterprise segments across North America, Europe, and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Cross-Border Hiring And Distributed Work Policies

Cross-border hiring moved from a selective workforce tactic to a core talent strategy between 2020 and 2025, and that shift has directly widened the addressable market for mobility and relocation management software. The International Bar Association reported that the weighted H-1B lottery introduced in March 2026 favored higher-wage candidates and pushed mid-tier technical hiring flows toward Canada, Mexico, and Ireland, increasing the number of corridors employers must manage simultaneously. Fragomen reported that 74% of employers globally struggled to find the talent they needed in 2025, and the projected worker shortfall could reach 85 million by 2030, underscoring the need to keep international hiring central to workforce planning rather than a secondary option.[1]Fragomen, Del Rey, Bernsen and Loewy LLP, “Fragomen Report Highlights Global Worker Shortfall of 85 Million by 2030,” Fragomen, fragomen.com As more companies hire across a wider mix of destinations, mobility teams must track more active jurisdictions, more assignment types, and more local compliance conditions than they managed in earlier operating models. That operating change makes spreadsheets and email chains harder to sustain, which supports software adoption across enterprises that now manage larger and more diverse mobility flows. It also increases demand for platforms that can support non-traditional corridors, because talent redeployment is no longer concentrated in a narrow group of destination countries.

Rising Need for Centralized Immigration, Tax, And Payroll Compliance

The mobility and relocation management software market is also being driven by a sharper need to manage immigration, tax, and payroll compliance from a single system rather than across disconnected teams and files. EY found that 95% of respondents said regulatory and compliance complexity was slowing mobility delivery, which shows how widely this issue is affecting program execution in 2026. The EU Entry/Exit System is replacing manual passport stamp checks with biometric registration and automated stay tracking, which means enterprise programs increasingly need systems that can maintain current compliance dashboards instead of retrospective summaries. The European Data Protection Board also approved Europrivacy in April 2026 as a certified mechanism for international personal data transfers under GDPR Articles 42 and 46, which reflects how quickly cross-border data governance is becoming part of software qualification requirements. As digital border systems and transfer rules become more formalized, buyers are placing higher value on platforms that can trigger payroll and immigration workflows in real time. That raises the pricing power of vendors whose products can support audit-ready reporting, faster alerts, and cleaner integration between mobility, tax, and payroll functions.

Shift From Spreadsheets to Integrated Mobility Automation

The mobility and relocation management software market is still benefiting from the ongoing shift away from spreadsheet-based program control toward integrated workflow automation. The remaining spreadsheet-heavy base appears to be concentrated in smaller programs and public sector settings, where technology adoption has trailed large multinational employers and where system integration has often been delayed by existing HR infrastructure. That creates a fresh pool of demand, because these buyers are now facing the same assignment complexity, data quality needs, and compliance reporting pressures that already pushed larger companies toward platform adoption. In practice, the change is favoring vendors with pre-built connectors and lower implementation friction, since buyers want to reduce manual coordination rather than add another isolated tool. This driver remains important because operational complexity is now reaching buyer groups that had previously relied on low-cost manual administration for smaller mobility volumes.

Growth In Flexible Mobility Policies Such As Lump Sum And Core-Flex Programs

Flexible mobility design is reshaping how companies purchase mobility and relocation management software, as policy administration now requires more case-level variation than standard assignment packages did in prior cycles. EY found that 88% of mobile employees said flexibility in mobility policies mattered in 2026, up from 70% in 2025, which shows how quickly employee expectations are changing. Atlas Van Lines reported that 61% of companies expected to increase relocation budgets in 2026, indicating that larger benefit menus and more exception handling are moving from the policy design stage into active programs. Core-flex and lump-sum structures require systems that can record individual benefit elections, vendor changes, tax gross-ups, and policy exceptions across multiple categories simultaneously. That workload is difficult to manage manually when volumes rise, especially across international programs with different tax and reporting rules. As a result, flexible policy adoption is increasing the value of configurable software and making policy engines a more important product buying criterion.[2]Atlas Van Lines, “Atlas Van Lines' 59th Annual Corporate Relocation Survey, Family, Flexibility and the Economy Are Driving Relocation Decisions,” Atlas Van Lines, atlasvanlines.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Sales Cycles and Complex Enterprise Integrations | -1.5% | Global, most pronounced in large enterprise segments in North America and Europe | Medium term (2-4 years) |

| Data Privacy, Cross-Border Transfer, and Security Requirements | -1.2% | EU core, spill-over to North America, APAC, and South America via GDPR, LGPD, and PIPL | Long term (≥ 4 years) |

| Fragmented Destination-Service and Supplier Data Standards | -0.9% | Global, highest impact in APAC and Middle East and Africa where data standards vary widely | Medium term (2-4 years) |

| Program Budget Volatility From Housing, Tax Gross-Up, and Exception Costs | -0.7% | Global, concentrated in high-cost destination markets, UK, Singapore, US, and Switzerland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Long Sales Cycles and Complex Enterprise Integrations

Long enterprise sales cycles continue to slow revenue conversion in the mobility and relocation management software market, even when buyer demand is visible. Procurement decisions in this category usually involve legal, tax, HR, IT, and finance teams, and each group evaluates the product through a different operating lens, which extends approval time. The input also shows that large buyers often expect pre-built, bidirectional connections to 3-5 HRIS and payroll systems before final selection, which removes many smaller vendors from serious consideration early in the process. This pushes newer suppliers toward the mid-market, where deployment requirements are lighter, and decision cycles are shorter, while established vendors remain stronger in large-enterprise contracts. The result is a split market structure where product capability alone does not determine win rates, because integration depth and financial stamina matter throughout the buying cycle. That slows the recognition of innovation as revenue, even as the underlying need for automation grows.

Data Privacy, Cross-Border Transfer, And Security Requirements

Data privacy and cross-border transfer rules remain a second major drag on the mobility and relocation management software market because a single relocation case can trigger many separate flows of employee information across jurisdictions. The European Data Protection Board's April 2026 approval of Europrivacy created a new transfer pathway under the GDPR, but vendors still need to manage broader compliance obligations across storage, consent, and documentation.[3]European Data Protection Board, “EDPB Adopts Decision on Europrivacy as Data Transfer Mechanism,” IGDPR, igdpr.eu The user input also highlights how GDPR, China's PIPL, and Brazil's LGPD require vendors to address data residency and transfer requirements across multiple cloud environments simultaneously. That raises legal and engineering costs and favors vendors that already offer ISO 27001, SOC 2 Type 2, GDPR-aligned storage, and PIPL-ready consent architecture as part of a standard enterprise offer. Regional specialists can still compete within narrower footprints, but expansion across several regulated regions is harder without dedicated compliance resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Is Rising As Buyers Add Managed Delivery To Core Platforms

Software held 67.28% of the 2025 market, giving it the largest mobility and relocation management software market share among components and confirming its role as the main system of record for assignment management, policy administration, immigration tracking, and reporting. Mobility management platforms held the largest software sub-type share at 32.31% in 2025, indicating that buyers continue to prefer consolidated platforms over single-function tools when managing large mobility programs. In the mobility and relocation management software market, that preference supports vendors that can cover the full assignment lifecycle rather than just one process area. Relocation workflow software, immigration and compliance management software, analytics platforms, and employee self-service portals still address different user groups within the same customer account, giving vendors room to extend contracts through bundled subscriptions and module expansion.

Services is the fastest-growing component, with a 19.47% CAGR through 2031, as buyers increasingly ask vendors and partners to manage more of the operating workload rather than just deliver software access. In the mobility and relocation management software industry, this reflects a broader move toward software-plus-services models as compliance complexity rises across more jurisdictions. Mid-market buyers are a key source of this demand because they often want predictable outcomes without building a full internal mobility team. That trend also aligns with user input that cost-control accountability is being split between software providers and implementation partners, making service depth a more practical buying factor than an add-on feature.

By Deployment Mode: Hybrid Models are Becoming More Important For Regulated Global Programs

Cloud-based deployment accounted for 69.12% of the 2025 mobility and relocation management software market, underscoring how closely SaaS delivery aligns with enterprise buying preferences for faster implementation and vendor-managed updates. This position was supported by the practical benefit of receiving immigration and compliance rule changes through the vendor environment without client-side patching. On-premises deployment still matters in regulated settings such as government, defense, and parts of the financial services industry, where data sovereignty requirements or legacy infrastructure make full cloud migration difficult. In the mobility and relocation management software market, those constraints keep deployment choices closely tied to sector risk profiles and national data rules.

Hybrid deployment is the fastest-growing mode and is projected to expand at a 20.36% CAGR through 2031 as global employers try to balance front-end flexibility with tighter control over sensitive HR and tax data. This model is particularly relevant in countries where certain categories of employee information must remain within national borders, making full cloud deployment impractical for some multinational programs. The structure also helps vendors serve global and regional needs within a single customer relationship, rather than forcing clients to maintain parallel systems by geography. As a result, hybrid architecture is becoming a strategic product attribute rather than a temporary compromise between legacy and modern deployment models.

By End User Enterprise Size: Mid-Market Adoption Is Lifting The Next Growth Layer

Large enterprises accounted for 62.73% of the 2025 market, reflecting the scale, geographic reach, and compliance exposure of their mobility programs in the mobility and relocation management software market. These organizations operate hundreds or thousands of active assignments, which makes automated case handling, integration with multiple HR systems, and real-time reporting necessary for program control. They also face larger risk costs from missed payroll triggers, expired work authorizations, and permanent establishment exposure, which helps justify higher software spending. This keeps large employers as the current revenue anchor for the category, even as other buyer groups accelerate.

Small and medium-sized enterprises are projected to grow at a 21.28% CAGR through 2031, supported by SaaS delivery, modular pricing, and lower infrastructure requirements that reduce the adoption barrier for smaller programs. Atlas Van Lines reported that mid-sized companies with 500-4,999 employees were investing most aggressively in AI-powered mobility tools in 2026, which suggests that platform competition will intensify in this part of the buyer base. EY also found that 80% of employees were more likely to stay with their employer after an international assignment, giving smaller buyers a stronger retention-based case for technology spending than in earlier years. The mobility and relocation management software market is therefore widening beyond large multinationals, with mid-market demand now supported by both operating efficiency and talent retention goals.

By Application: Analytics Is Gaining Ground As Programs Need Better Control And Proof Of Value

Employee relocation management accounted for 28.91% of the 2025 mobility and relocation management software market, making it the largest application, as nearly every enterprise program uses relocation workflows as a basic operating function. That scale reflects the fact that domestic and international moves both depend on case coordination, policy authorization, and service delivery tracking. Immigration and visa management have also become more prominent as processing timelines lengthen and early-warning alerts become more valuable for business continuity. In the mobility and relocation management software market, these application layers are increasingly connected rather than managed as separate administrative steps.

Analytics and compliance reporting are the fastest-growing applications and are projected to post a 22.14% CAGR through 2031 as mobility teams are asked to demonstrate cost control, program value, and regulatory readiness in real time. Assignment management and policy administration remain important because they capture exceptions, approval logic, and documentation that support internal audit and tax review. Expense and compensation management has also gained weight as housing costs, tax gross-ups, and exception rates become harder to predict across destinations. EY found that only 51% of mobility teams trusted their underlying data enough to advance AI analytics programs, underscoring the need for a platform upgrade cycle focused on data governance and reporting quality.

By End-User Industry: Healthcare And Life Sciences Is Emerging As A High-Growth Vertical

Information technology and telecom accounted for 24.63% of the market in 2025, making it the largest end-user vertical in the mobility and relocation management software market, as the sector has a high concentration of internationally mobile talent and mature HR technology buying practices. BFSI also contributes meaningful demand because organizations in that sector need auditable records across jurisdictions and maintain broad international operating footprints. Retail and e-commerce, industrial manufacturing, and government programs each use mobility software in different ways, but all depend on stronger visibility into assignment handling and policy execution. This broad use base keeps the category relevant across several sectors, even though software buying maturity varies by industry.

Healthcare and life sciences are the fastest-growing verticals and are projected to expand at a 23.58% CAGR through 2031 as labor shortages increase the need for cross-border recruitment. Fragomen reported a projected global worker shortfall of 85 million by 2030, and user input noted that healthcare systems in countries such as Japan, Germany, and the United States bear a disproportionate share of this pressure. ManpowerGroup also identified cross-border recruitment as a critical scaling mechanism for healthcare and life sciences employers facing demographic strain, which supports greater use of mobility software in this vertical. Because healthcare mobility often includes credential verification, license reciprocity, and specialized visa handling, vendors that support this complexity can command higher software spend per assignee than general-purpose offerings typically achieve.[4]ManpowerGroup, “2026 Healthcare and Life Sciences Vertical Report,” ManpowerGroup, manpowergroup.se

Geography Analysis

North America accounted for 41.77% of the 2025 market, giving the region the highest market share in mobility and relocation management software and reflecting its concentration of multinational headquarters, mature HR technology buying practices, and established relocation service networks. The United States remained the largest country market in the region, but the 2026 policy environment increased the compliance burden through a USD 100,000 fee for new H-1B petitions, a wage-weighted lottery, and tighter work authorization conditions, pushing employers toward broader corridor management needs. Canada and Mexico are benefiting from this redirection of technical hiring, which increases demand for multi-country case handling inside existing enterprise platform deployments. Atlas Van Lines reported that 54% of companies increased relocation volume in 2025 and that 61% expected to raise budgets in 2026, reinforcing the region's strong demand base even as policy design becomes more flexible and employee-experience issues gain weight. Mexico's rising position as a nearshore technology and manufacturing hub is also adding a newer assignment corridor that did not carry the same weight in earlier software adoption cycles.

Asia-Pacific is projected to grow at a 24.39% CAGR through 2031, making it the fastest-growing regional segment in the mobility and relocation management software market. The user input ties this growth to manufacturing expansion, greater intraregional deployment of talent, and faster digitization of enterprise HR systems across India, China, Japan, South Korea, and Australia. The region is also benefiting from stronger corporate travel activity, creating a higher-volume environment where automated mobility control becomes more economical for a wider range of program sizes. India and China remain especially important because inbound mobility, domestic deployment, local-language support, and data residency requirements all shape how vendors configure products for these markets.

Europe remains a large and compliance-intensive market because GDPR, the EU Entry/Exit System, and the EU Pay Transparency Directive all increase the need for audit-ready documentation and stronger data controls inside the mobility and relocation management software market. ECA International reported in April 2026 that the European Commission had launched a public consultation on ESSPASS, signaling a near-term need for platforms to connect with national social security systems across EU member states. Germany, the United Kingdom, and France continue to anchor regional demand because they combine large multinational workforces with stricter procurement expectations around data protection and compliance readiness. The Middle East, especially the UAE and Saudi Arabia, is growing as government diversification programs bring in more skilled international workers and require software that can manage local sponsorship and quota rules. South America presents a moderate growth opportunity led by Brazil, where LGPD compliance adds another layer of software qualification for cross-border deployments, while Africa remains earlier-stage but is drawing more vendor attention through expanding service coverage in non-traditional corridors.

Competitive Landscape

The mobility and relocation management software market is moderately fragmented, with Equus Software, Topia, and Benivo holding meaningful positions in large-enterprise accounts while many regional specialists and single-module providers compete for mid-market and vertical demand. This structure means vendor choice is still wide for buyers, but scale, compliance credibility, and integration depth matter much more in enterprise deals than in smaller program rollouts. Boundless Immigration strengthened its global coverage with the October 2025 acquisition of Localyze GmbH, which created a broader immigration and compliance platform spanning the Americas, Europe, and APAC and reduced the need for multinational customers to manage separate regional vendors. Envoy Global also expanded geographic capability through acquisitions in Africa and Germany, showing how providers are using targeted deals to enter jurisdictions that would take years to build organically. These moves are compressing the pool of independent providers without eliminating the long tail of specialists that still compete effectively in narrower geographic or functional niches.

Technology now has a larger role in shortlist decisions across the mobility and relocation management software market because buyers increasingly favor vendors with established security credentials, pre-built integrations, and self-service tools that reduce operating friction. Products with ISO 27001 and SOC 2 Type 2 positioning, along with bidirectional connectivity to systems such as Workday and SAP SuccessFactors, are better placed to defend renewals and expand account scope when procurement teams compare risk and implementation effort. Topia's April 2026 launch of Horizon showed how the category is moving toward AI-native design, with natural-language policy building and embedded agents intended to shift mobility teams from reactive case handling to more proactive program control. That direction is especially relevant because the user input also showed that many mobility teams want advanced analytics but still lack complete confidence in their underlying data, which makes integrated data integrity and compliance logic more valuable than isolated automation features.

White-space demand remains open in healthcare-focused modules, SME-oriented managed-service overlays, and real-time permanent establishment monitoring, where most vendors still offer partial rather than complete coverage in the mobility and relocation management software market. WorkFlex's March 2026 funding round of EUR 37 million (USD 40.7 million) showed that focused compliance automation plays can still attract capital when they address a well-defined pain point with clear operating value. Equus Software's May 2026 tax trend analysis, which tracked legislative changes across 155 supported tax authorities and 72 sub-authorities in the United States, Canada, and Switzerland, also showed how vendors are trying to deepen their role in ongoing compliance monitoring rather than limiting their position to transaction processing. Vendors that built broad connector libraries across payroll, travel, destination services, and human capital systems remain hard to displace because the cost of switching rises as customers connect more workflows into the same operating layer. This is why competition is not only about feature breadth, but also about how deeply a platform is embedded in the buyer's wider mobility operating model.

Mobility And Relocation Management Software Industry Leaders

Equus Software, LLC

Topia Mobility Inc.

Benivo Limited

Localyze GmbH

Jobbatical OÜ

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Equus Software published a global tax trend analysis covering 155 tax authorities and 72 sub-authorities for real-time legislative tracking.

- April 2026: Topia launched Horizon, an agentic AI platform for global mobility with natural-language policy building and MCP integrations.

- April 2026: Atlas Van Lines released its 59th Corporate Relocation Survey: 54% increased relocation volume in 2025, 61% expect higher budgets in 2026, and 46% saw more declined offers.

- April 2026: Relocity added multilingual support to its relocation app, enabling automatic device-language configuration for global employees.

Global Mobility And Relocation Management Software Market Report Scope

The Mobility and Relocation Management Software market refers to technology platforms and services that streamline and automate global workforce mobility processes, including employee relocation, immigration and visa management, assignment and policy administration, expense and compensation tracking, and analytics-driven compliance reporting. These solutions encompass mobility management platforms, relocation workflow software, immigration and compliance management tools, mobility analytics systems, and employee self-service portals, supported by professional services. Delivered through cloud-based, on-premise, and hybrid deployment models, they cater to both large enterprises and small and medium-sized enterprises across industries such as BFSI, healthcare and life sciences, information technology and telecom, retail and e-commerce, industrial manufacturing, government and public sector, and other end-user industries. The core purpose of this market is to enhance workforce mobility efficiency, ensure compliance with international regulations, reduce administrative overhead, and improve employee experience through digital automation and data-driven insights.

The Mobility and Relocation Management Software market report is segmented by Component (Software, [Mobility Management Platforms, Relocation Workflow Software, Immigration and Compliance Management Software, Mobility Analytics Platforms, and Employee Self-service Mobility Portals] and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Application (Employee Relocation Management, Immigration and Visa Management, Assignment Management and Policy Administration, Expense and Compensation Management, and Analytics and Compliance Reporting), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Mobility Management Platforms |

| Relocation Workflow Software | |

| Immigration and Compliance Management Software | |

| Mobility Analytics Platforms | |

| Employee Self-service Mobility Portals | |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Employee Relocation Management |

| Immigration and Visa Management |

| Assignment Management and Policy Administration |

| Expense and Compensation Management |

| Analytics and Compliance Reporting |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Mobility Management Platforms |

| Relocation Workflow Software | ||

| Immigration and Compliance Management Software | ||

| Mobility Analytics Platforms | ||

| Employee Self-service Mobility Portals | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Application | Employee Relocation Management | |

| Immigration and Visa Management | ||

| Assignment Management and Policy Administration | ||

| Expense and Compensation Management | ||

| Analytics and Compliance Reporting | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and future value of the mobility and relocation management software market space?

It was valued at USD 4.50 billion in 2025, stood at USD 5.11 billion in 2026, and is projected to reach USD 10.09 billion by 2031 at a 14.58% CAGR.

What is driving demand for mobility and relocation management software in 2026?

Demand is being supported by cross-border hiring, tighter immigration and tax compliance needs, broader use of AI-enabled workflows, and rising pressure to replace manual tracking with integrated systems.

Which component is growing fastest in mobility and relocation platforms?

Services is the fastest-growing component, with a 19.47% CAGR through 2031, as more buyers prefer managed-service overlays alongside SaaS tools.

Which application area is seeing the fastest growth?

Analytics and compliance reporting is expanding fastest at a 22.14% CAGR through 2031 because mobility teams need better cost visibility, stronger reporting, and more reliable compliance monitoring.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is the fastest-growing region, with a 24.39% CAGR, supported by manufacturing expansion, intraregional talent mobility, and faster HR system digitization.

Which end-user vertical is creating the strongest new demand?

Healthcare and life sciences is the fastest-growing vertical, with a 23.58% CAGR through 2031, as global labor shortages and cross-border recruitment needs raise software spend per assignee.

Page last updated on: