Size and Share of Enterprise Mobility Market In Banking Industry

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

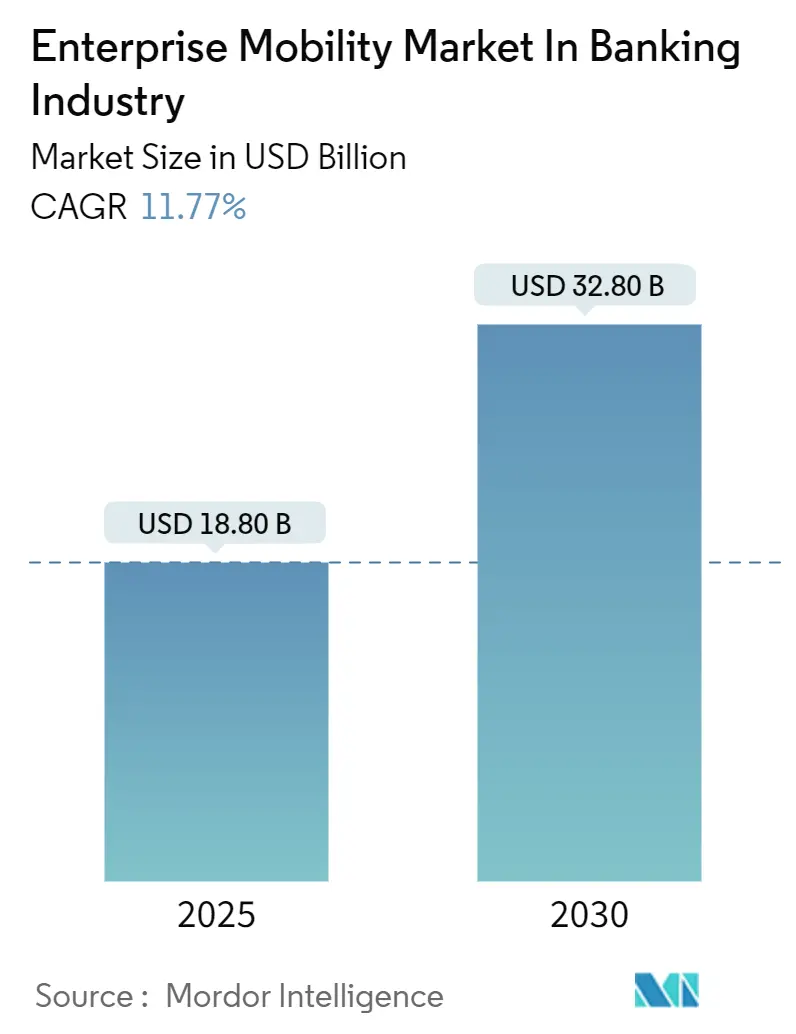

| Market Size (2025) | USD 18.80 Billion |

| Market Size (2030) | USD 32.80 Billion |

| Growth Rate (2025 - 2030) | 11.77% CAGR |

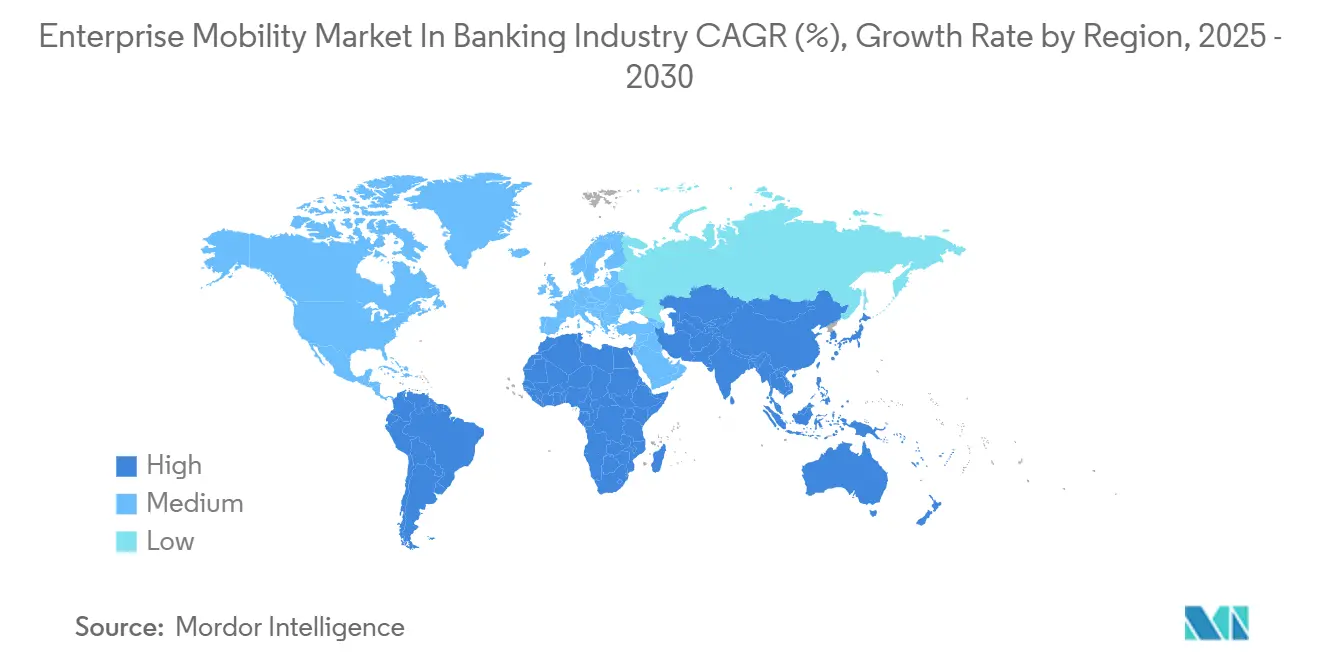

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Enterprise Mobility Market In Banking Industry by Mordor Intelligence

The Enterprise Mobility Market in Banking Industry is expected to grow from USD 18.80 billion in 2025 to USD 32.80 billion by 2030, at a CAGR of 11.77% during the forecast period (2025-2030). This growth links to banks redesigning security around endpoints instead of fenced data-centers, accelerated by hybrid work, zero-trust mandates, and real-time payment platforms that demand millisecond orchestration across mobile channels. Pandemic-era remote work entrenched mobile workflows, and legacy cores built on mainframes cannot easily expose the open APIs required for embedded finance. The enterprise mobility market in banking industry is also benefiting from the spread of private 5G, which supplies sub-10-millisecond latency critical for fraud detection, and from tighter Basel Committee resilience principles that compel investment in endpoint visibility.

Key Report Takeaways

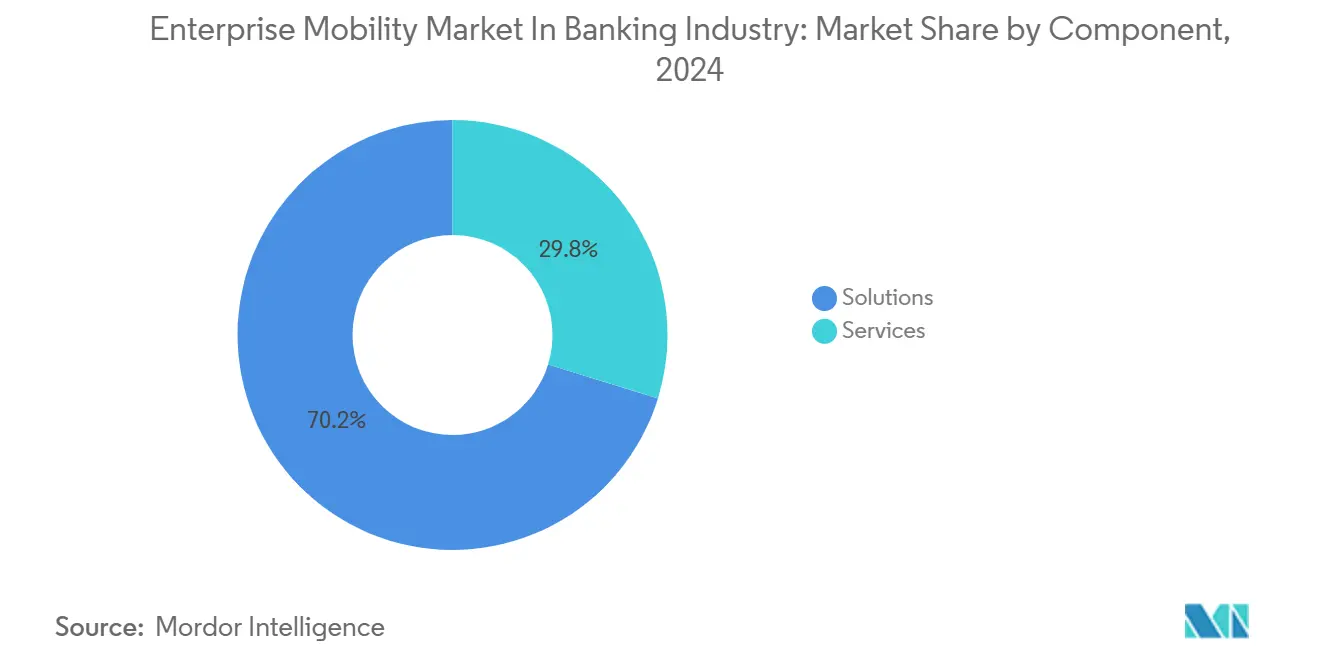

- By component, solutions captured 70.22% of the enterprise mobility market in banking industry share in 2024, while the services segment is forecast to expand at a 12.22% CAGR through 2030.

- By solution type, device management led with 42.45% revenue share in 2024, whereas application management is poised to grow at 14.25% CAGR to 2030.

- By deployment, on-premises and hybrid models held 59.54% share in 2024; cloud-native stacks are advancing at 13.45% CAGR over the forecast period.

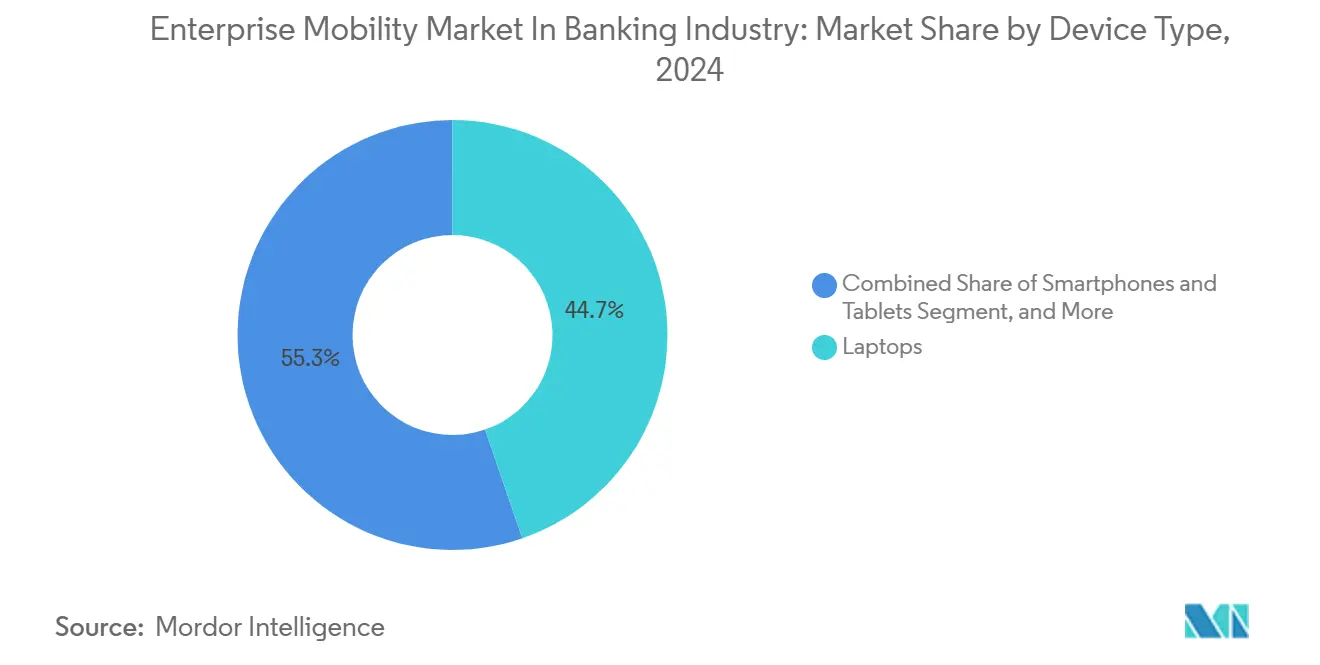

- By device type, laptops accounted for 44.72% of 2024 revenue, while smartphones and tablets are expected to post the fastest growth at 14.67% CAGR.

- By enterprise size, large banks controlled 75% share in 2024, yet small and mid-size banks are projected to expand at 13.54% CAGR through 2030.

- By geography, North America held 36.07% of 2024 revenue, whereas Asia Pacific is set to register the highest regional CAGR of 12.9% to 2030.

Insights and Trends of Enterprise Mobility Market In Banking Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Remote and Hybrid Banking Workforce | +2.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Shift to Cloud-Native Core and API-First Platforms | +2.3% | Global, led by Asia Pacific and North America | Long term (≥ 4 years) |

| Regulatory Push for Zero-Trust Endpoint Security | +1.8% | North America and Europe with spillover to Asia Pacific | Short term (≤ 2 years) |

| 5G-SA and Private-Wireless Roll-outs | +1.2% | Asia Pacific core, early adoption in Middle East | Long term (≥ 4 years) |

| Growth of Instant Real-Time Payments and Embedded Finance | +1.6% | Asia Pacific and Latin America with expansion in Europe | Medium term (2-4 years) |

| Consumer Mobile-Phishing Surge | +1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Zero-Trust Endpoint Security

Supervisors worldwide now examine whether banks can verify every user-to-device request in real time. The U.S. Federal Financial Institutions Examination Council issued 2024 guidance that requires continuous authentication and device-health checks, while the Monetary Authority of Singapore demands biometric controls in its Technology Risk Management Guidelines.[1]Monetary Authority of Singapore, “Technology Risk Management Guidelines,” mas.gov.sg These rules elevate unified endpoint management and access-management spending, because failure to comply risks enforcement, fines, and reputational loss. Vendors with audit-ready dashboards and ISO/IEC 27001:2022 alignment command procurement preference. As mandates tighten, the enterprise mobility market in banking industry witnesses steady budget allocation even when discretionary projects pause.

Shift to Cloud-Native Core and API-First Platforms

Banks retiring COBOL-based cores gain release velocity advantages: a 2024 McKinsey study showed 40-60% faster time-to-market for new mobile features once moved to cloud-native cores. API-exposed logic enables embedded-finance partnerships but widens the attack surface, prompting adoption of runtime application self-protection tools that inspect API calls. Containerized mobile-application management lets banks push updates instantly without user action. Regulatory bodies, such as the European Banking Authority under PSD2, reinforce the trend by mandating strong customer authentication for every mobile transaction.[2]European Banking Authority, “Revised Payment Services Directive Technical Standards,” eba.europa.eu

Rising Remote and Hybrid Banking Workforce

A 2024 PwC survey reported that 68% of financial-services leaders expect half their staff to remain hybrid through 2027. This shift dissolves perimeter defenses, so every laptop, smartphone, or tablet becomes a potential breach vector. Demand is rising for conditional-access policies, remote-wipe features, and per-app VPNs that separate personal and corporate data on bring-your-own devices. The ISO/IEC 27001:2022 standard now includes explicit remote-work controls, influencing procurement checklists and boosting the enterprise mobility market in banking industry.

Growth of Instant Real-Time Payments and Embedded Finance Workflows

India’s Unified Payments Interface processed 11.4 billion transactions in October 2024 alone, illustrating transaction volumes that require sub-second orchestration. Retailers, ride-hailing apps, and e-commerce platforms embed banking APIs, multiplying mobile endpoints that must be secured. Accenture projects embedded finance could generate 20% of banking revenue by 2030 if usability and security remain seamless. Banks, therefore, invest in application-management containers, runtime RASP, and low-latency 5G connections to meet both throughput and security needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cost-of-Ownership for Multi-UEM Stacks | -0.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Scarcity of Mobile-Security and Dev-Sec-Ops Talent | -0.7% | Global, most severe in North America and Asia Pacific | Medium term (2-4 years) |

| End-User Resistance to Device or Content Controls | -0.5% | Global, higher resistance in Europe | Short term (≤ 2 years) |

| Macroeconomic Tech-Budget Compression | -0.8% | Global, focus in Europe and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cost-of-Ownership for Multi-UEM Stacks

A 2024 Deloitte analysis found banks running three or more endpoint-management tools spend 30-40% more yet score worse on security posture due to policy inconsistencies. Consolidation is technologically feasible but politically complex as business units guard preferred features. Cost pressure forces institutions to delay advanced capabilities like private-5G slicing, slowing the overall enterprise mobility market in banking industry trajectory.

Macroeconomic Tech-Budget Compression

Inflation and interest-rate volatility trim discretionary IT spending, particularly across Europe and Latin America. Projects without direct revenue impact face deferral, and finance chiefs scrutinize license renewals. Nonetheless, non-negotiable compliance controls soften the blow, keeping core endpoint-security budgets intact but limiting expansion into experimental AI analytics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Outpaces Software

Solutions held 70.22% revenue in 2024, mainly unified endpoint management, mobile-threat defense, and identity-access suites. Yet services are predicted to grow at a 12.22% CAGR, indicating that integration and 24-hour monitoring trump pure software installations. Systems integrators such as Accenture and Tata Consultancy Services win multi-year contracts to migrate banks to zero-trust frameworks. This consultancy surge underscores how the enterprise mobility market in banking industry size for services complements the initial software outlay.

Regulatory divergence across jurisdictions fuels demand for advisory offerings, while consumption-based cloud pricing merges software and services into a single subscription. Banks prefer packaged compliance frameworks that reduce audit costs and accelerate go-live. As a result, the enterprise mobility market in banking industry continually shifts margin pools from licenses to managed services.

By Solution Type: Application Management Surges on Containerization

Device management captured 42.45% revenue in 2024, reflecting legacy provisioning of corporate devices. However, application management is forecast to expand at 14.25% CAGR, propelled by bring-your-own-device policies. Containerized enclaves isolate banking data even if the device is compromised, and app-level VPNs reduce friction. This capability allows institutions to satisfy both user privacy and regulator scrutiny. The enterprise mobility market in banking industry size allocated to container solutions is therefore rising faster than base UEM provisioning.

Concurrent growth in access-management stems from zero-trust rules. Biometric logins and behavioral analytics replace passwords prone to phishing. Vendors combine mobile-threat defense and secure browsers into unified dashboards, a strategy that simplifies operations for security centers and strengthens the enterprise mobility market in banking industry market value proposition.

By Deployment: Cloud-Native Gains Despite Regulatory Caution

On-premises and hybrid models held 59.54% share in 2024 because of data-residency rules and inertia. Yet cloud-native deployments are advancing at 13.45% CAGR as elastic compute, automated patching, and global failover lower mean-time-to-recovery by 50%, according to McKinsey research. The enterprise mobility market in banking industry benefits when regulators approve sovereign or dedicated clouds that meet encryption and exit-strategy conditions.

Small and mid-size banks spearhead adoption by subscribing to software-as-a-service UEM platforms, sidestepping large capital expenditure. As cloud control planes mature, larger banks gradually migrate non-core workloads, balancing between compliance and agility.

By Device Type: Smartphones and Tablets Overtake Laptops

Laptops retained 44.72% share in 2024 as risk, treasury, and compliance teams needed larger screens. Smartphones and tablets are projected to grow at 14.67% CAGR, driven by branch-less models where staff open accounts directly at customer sites. Deloitte found mobile-first retail bankers delivered 25% higher satisfaction scores. The enterprise mobility market in banking industry size tied to mobile devices therefore rises faster than traditional endpoints.

Generation-Z employees favor personal smartphones, pushing bring-your-own programs. While wearables and rugged tablets remain niche, they gain traction in cash-in-transit or remote branches, further diversifying endpoint fleets that security teams must manage.

By Enterprise Size: Small and Mid-Size Banks Accelerate Adoption

Large institutions owned 75% of 2024 revenue, leveraging deep budgets and multi-jurisdiction operations. They often juggle several endpoint-management tools acquired through mergers, inflating complexity yet sustaining services demand. However, small and mid-size banks are forecast to grow at 13.54% CAGR as cloud-native cores enable quick rollout without data-center investment. A Microsoft case study showed a 500-person U.S. bank completed a cloud-UEM deployment in six weeks.

Proportional regulation eases compliance burdens, allowing community banks to embrace zero-trust principles scaled to their risk profile. This trend broadens the enterprise mobility market in banking industry by bringing smaller players into advanced security capabilities once reserved for global giants.

Geography Analysis

North America held 36.07% revenue in 2024, shaped by FFIEC guidance and early zero-trust adoption. Regional banks invest heavily in phishing detection after an FBI advisory highlighted organized crime using SMS lures.[3]Federal Bureau of Investigation, “Mobile Phishing Advisory 2024,” fbi.gov Canadian and Mexican institutions likewise deploy biometrics and mobile platforms for inclusion goals.

Asia Pacific is set to record a 12.9% CAGR to 2030. Singapore, India, and China champion digital-banking licenses, real-time payment rails, and sovereign mobile operating systems. PwC reports rising deployment of private 5 G networks in branches for latency-sensitive applications. Japan, South Korea, and Australia upgrade mobile-security stacks to meet cybersecurity codes, while Indonesia and Vietnam leapfrog legacy cores with mobile-first platforms.

Europe maintains a sizable share under PSD2 and the Digital Operational Resilience Act. Latin America accelerates on open-banking mandates in Brazil and Mexico, whereas the Middle East and Africa deploy sovereign-cloud endpoints backed by wealth-fund financing. Together, these developments extend the enterprise mobility in the banking market footprint worldwide.

Competitive Landscape

The enterprise mobility market in banking industry remains moderately fragmented. Microsoft, VMware, and BlackBerry dominate unified endpoint management through enterprise licensing aligned with productivity suites. Niche vendors such as Jamf, Ivanti, and SOTI address Apple ecosystems or rugged devices, extracting premium margins. Mobile-threat defense specialists, including Sophos and Palo Alto Networks, use AI analytics to uncover zero-day exploits faster than signature databases, attracting banks under phishing siege.

Systems integrators Accenture, Infosys, Tata Consultancy Services, HCL Technologies, and Capgemini bundle consulting, deployment, and managed detection into multi-year deals. Their involvement reflects customer preference for a single throat to choke in multi-vendor rollouts. Consolidation continues: VMware bought a threat-defense startup in 2024 to fold AI phishing detection into Workspace ONE, while Cisco’s patent for machine-learning-based device-compromise prediction hints at future competition.

White-space opportunities remain in private 5G slices for latency-critical tasks and in AI-driven behavioral analytics that spot credential theft before data exfiltration. Vendors aligned with Basel principles and ISO standards win shortlist preference. As spending shifts from licenses to managed outcomes, platform providers court integrators, and integrators secure attach fees, shaping the next phase of the enterprise mobility market in banking industry.

Leaders of Enterprise Mobility Market In Banking Industry

Microsoft Corporation

VMware Inc.

IBM Corporation

Citrix Systems Inc.

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Microsoft integrated Intune with Azure Active Directory Conditional Access to enforce real-time device-health checks.

- September 2024: VMware acquired a mobile-threat-defense startup, adding AI phishing detection to Workspace ONE.

- August 2024: Accenture won a five-year, USD 150 million contract to design zero-trust architecture for a European bank covering 40,000 mobile endpoints.

- July 2024: Palo Alto Networks launched a cloud-delivered mobile-threat-defense service that integrates through open APIs with existing UEM platforms.

Scope of Report on Enterprise Mobility Market In Banking Industry

The Enterprise mobility market in banking refers to the technologies, solutions, and services that enable banks to securely manage mobile devices, mobile applications, and mobile-enabled workflows for both employees and customers.

The Enterprise Mobility Market in Banking Industry Report is Segmented by Component (Solutions, Services), Solution Type (Device Management, Access Management, Application Management, Other Solutions), Deployment (On-Premises/Hybrid, Cloud-Native), Device Type (Laptops, Smartphones and Tablets, Other Devices), Enterprise Size (Large Banks, Small and Mid-size Banks), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Device Management |

| Access Management |

| Application Management |

| Other Solution Types |

| On-Premises / Hybrid |

| Cloud-Native |

| Laptops |

| Smartphones and Tablets |

| Other Device Types |

| Large Banks |

| Small and Mid-size Banks |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Solution Type | Device Management | ||

| Access Management | |||

| Application Management | |||

| Other Solution Types | |||

| By Deployment | On-Premises / Hybrid | ||

| Cloud-Native | |||

| By Device Type | Laptops | ||

| Smartphones and Tablets | |||

| Other Device Types | |||

| By Enterprise Size | Large Banks | ||

| Small and Mid-size Banks | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 value of the enterprise mobility market in banking industry?

The market is valued at USD 18.80 billion in 2025.

How fast will spending on enterprise mobility market in banking industry grow through 2030?

Revenue is forecast to rise at an 11.77% CAGR, reaching USD 32.80 billion by 2030.

Which component segment is expanding the quickest?

Services are growing at a 12.22% CAGR as banks outsource integration and threat monitoring tasks.

Why is Asia Pacific the fastest-growing region?

Digital-banking licenses, UPI-scale real-time payments, and sovereign 5G investments drive a 12.9% regional CAGR.

How are banks managing bring-your-own-device risks?

They deploy application-management containers, per-app VPNs, and runtime self-protection to isolate corporate data.

What emerging technology could reshape endpoint strategies?

Private 5G networks promise sub-10-millisecond latency for real-time fraud detection and high-frequency trading.

Page last updated on: