Canada Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

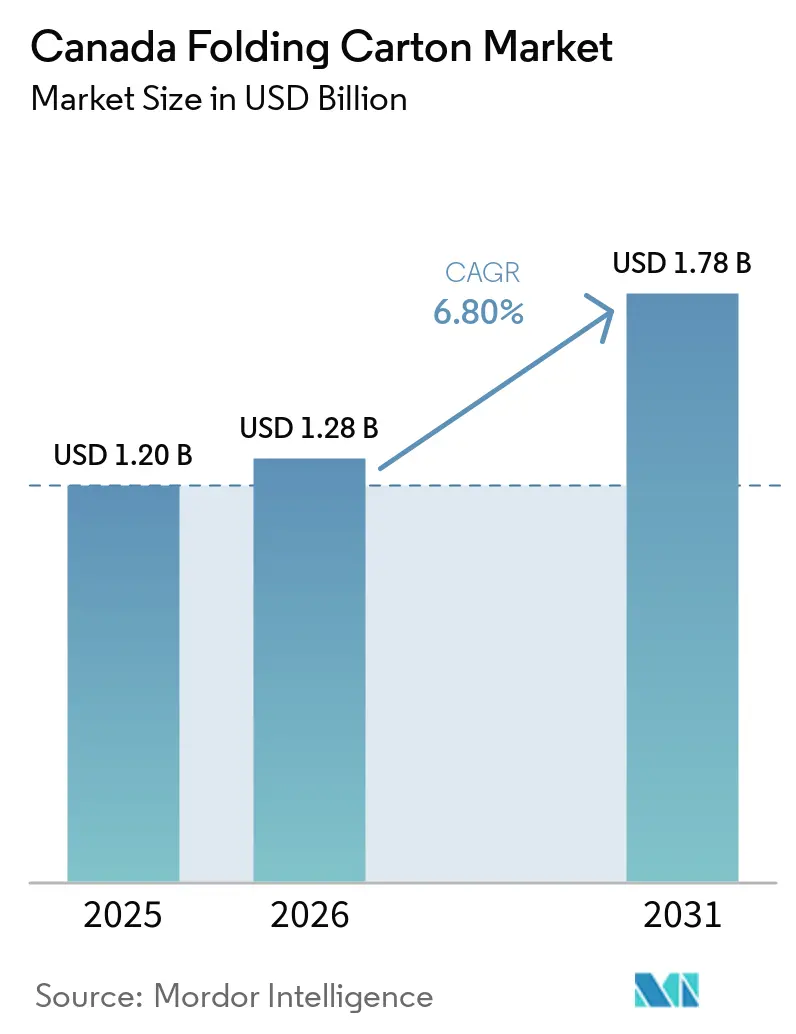

| Base Year Market Size (2025) | USD 1.20 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

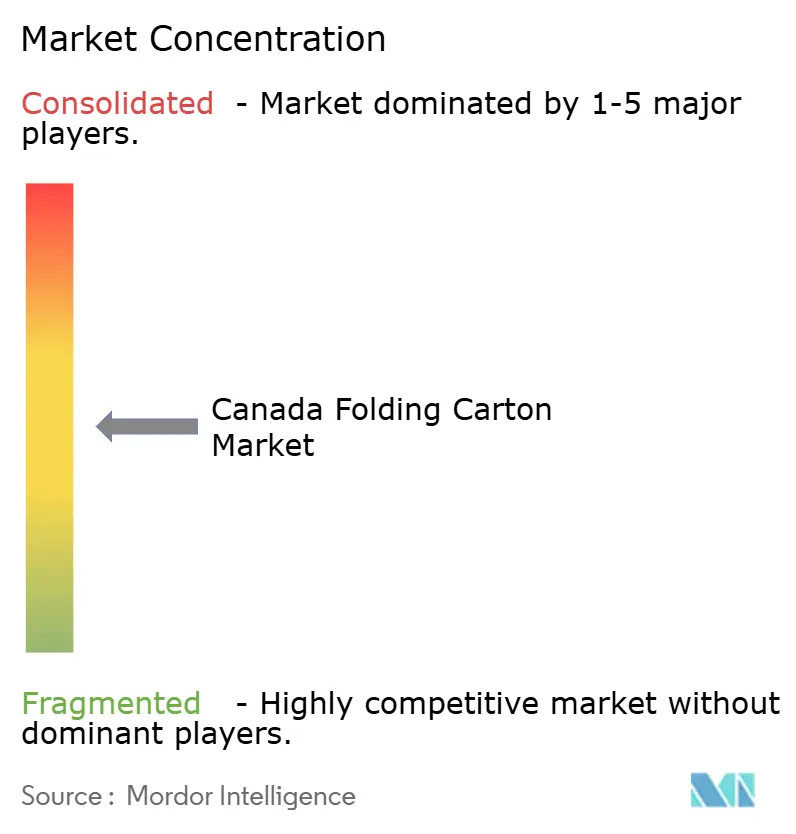

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Folding Carton Market Analysis by Mordor Intelligence

The Canada folding carton market size is expected to be USD 1.20 billion in 2025, USD 1.28 billion in 2026, and reach USD 1.78 billion by 2031, growing at a CAGR of 6.8% from 2026 to 2031. Demand acceleration is tied to overlapping provincial Extended Producer Responsibility fees, cannabis-sector compliance costs, and the surge in e-commerce fulfillment, all of which are redefining converter economics and raw-material selection. Federal plastics-registry rules are steering brand owners toward fiber-based formats, while plain-packaging laws in regulated categories such as cannabis are widening the addressable base for premium boxboard grades. Converters that combine digital printing with high-throughput automation are gaining share because they shorten the design-to-shelf cycle, a critical advantage as product-refresh calendars tighten and mass customization becomes mainstream. Price pressure from recycled-fiber volatility and energy-tariff hikes persists, yet converters with certified circular-economy credentials are capturing long-term contracts that lock in margin despite cost headwinds.

Key Report Takeaways

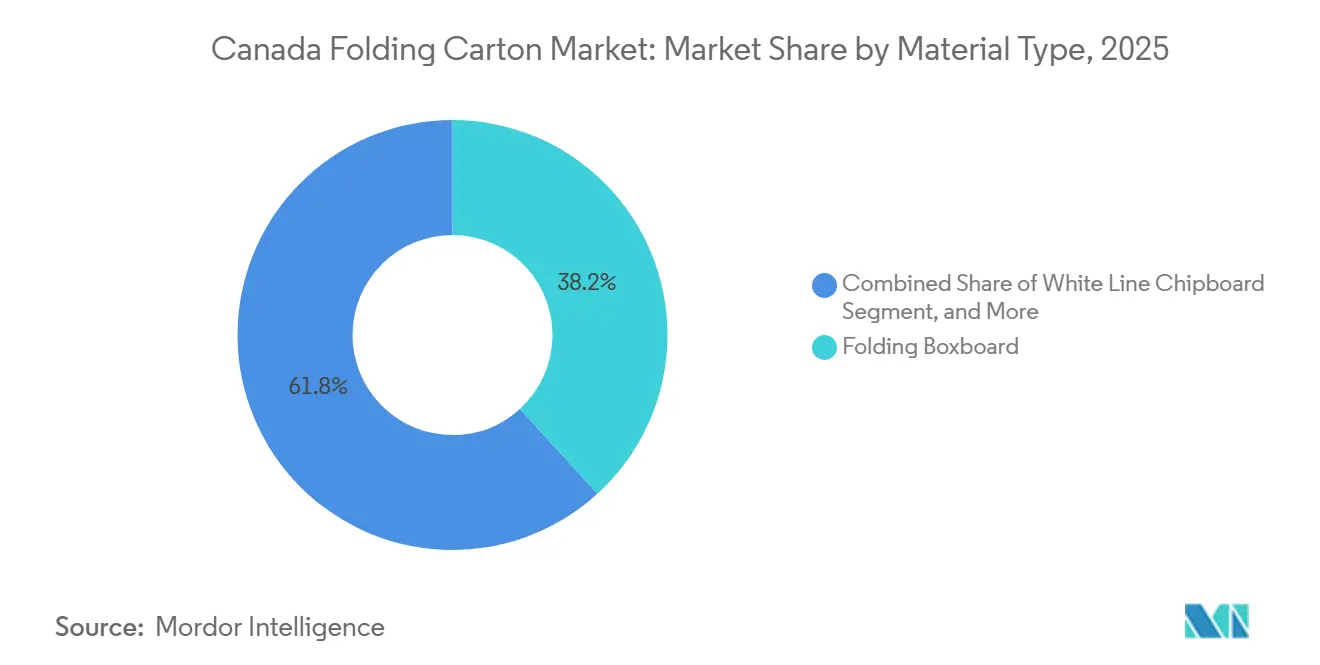

- By material type, folding boxboard captured 38.23% of the Canada folding carton market share in 2025.

- By printing technology, the Canada folding carton market size for the digital printing segment is forecast to advance at a 9.38% CAGR through 2031.

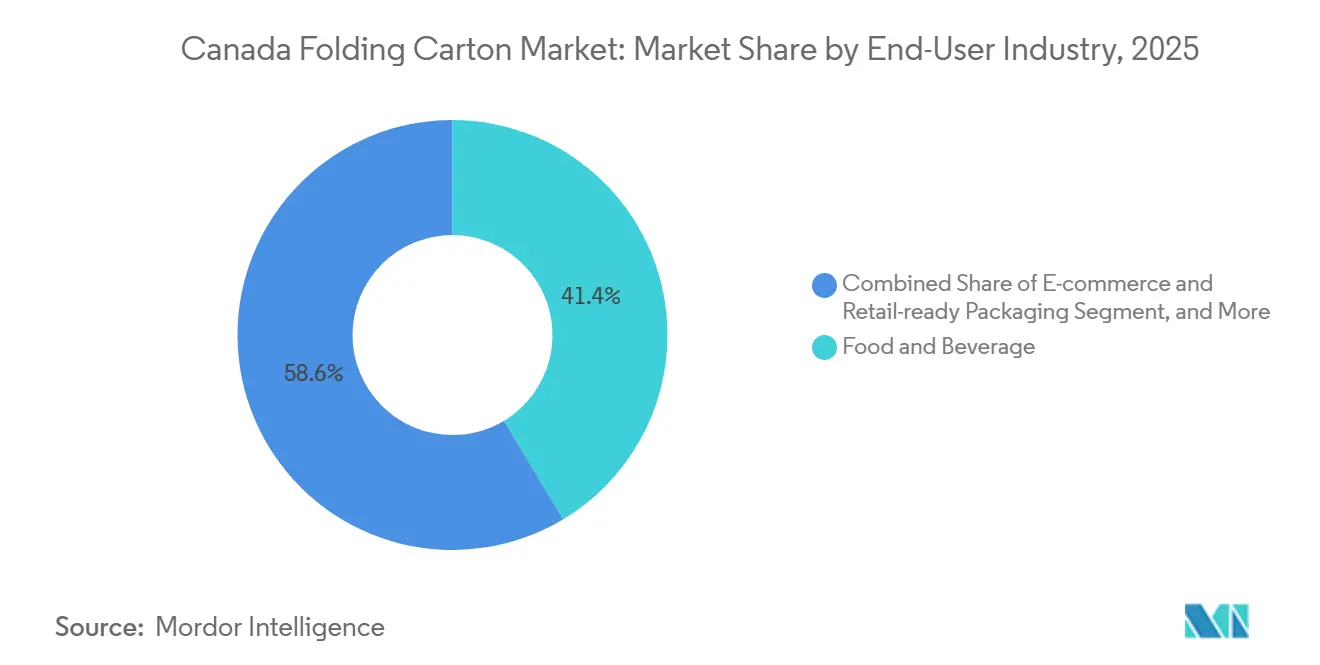

- By end-user industry, food and beverage captured 41.38% of the Canada folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Sustainable Packaging In Canadian FMCG Sector | +1.80% | National, concentrated in Ontario and Quebec | Medium term (2-4 years) |

| Shift Toward Lightweighting To Cut Transport Emissions | +1.20% | National, early adoption in British Columbia and Alberta | Short term (≤ 2 years) |

| Expansion Of Cannabis Packaging Requirements | +1.10% | National, peak demand in Ontario, Quebec, Alberta, British Columbia | Short term (≤ 2 years) |

| Provincial EPR Regulations Accelerating Recyclability Mandates | +1.00% | British Columbia, Quebec, Ontario, Nova Scotia | Medium term (2-4 years) |

| Surge In Craft Food Exports Requiring Premium Carton | +0.70% | Quebec and Ontario export hubs | Long term (≥ 4 years) |

| Automation Investments By Converters Reducing Lead-Times | +0.60% | Southern Ontario and Greater Montreal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Packaging in Canadian FMCG Sector

Retailers now stipulate minimum recycled-content thresholds for primary packaging, pushing brand owners toward fiber-based designs that align with provincial waste-diversion targets. Food and beverage retail sales reached CAD 16.7 billion (USD 13.2 billion) in November 2025, a 5.6% year-over-year gain that translated directly into higher carton volumes.[1]Statistics Canada, “The Daily — Retail Commodity Survey, November 2025,” statcan.gc.ca Plastics-registry fees imposed under the Canadian Environmental Protection Act have increased cost differentials between paperboard and rigid plastics, accelerating format substitution.[2]Environment and Climate Change Canada, “Plastics Registry,” canada.ca Ontario and Quebec, which together account for more than 60% of fast-moving consumer-goods output, provide converters in those provinces with scale advantages and early visibility into packaging-spec changes. National grocery chains are also scoring suppliers on packaging sustainability, a metric that increasingly determines shelf space for competing brands. As a result, the Canada folding carton market is seeing a wave of design refreshes that elevate recycled-content messaging on-pack, reinforcing carton demand and supporting price premiums.

Shift Toward Lightweighting to Cut Transport Emissions

Transport Canada’s Clean Transportation Action Plan targets a 40% reduction in freight greenhouse-gas emissions by 2030, which has triggered packaging redesign projects aimed at trimming gram-weight per unit.[3]Transport Canada, “Clean Transportation Action Plan,” tc.gc.ca Converters are deploying micro-flute structures and high-strength recycled liners that maintain crush resistance while reducing material use by up to 15%. Early adopters in British Columbia and Alberta report that lightweighted formats already represent one-third of new project briefs, underscoring how carbon-reduction mandates are reshaping material-engineering priorities. National retailers estimate that a 10% cut in carton mass across their Canadian distribution networks can unlock annual fuel savings exceeding CAD 1 million (USD 0.8 million), a cost incentive that accelerates adoption. Lightweighting, therefore, not only meets sustainability scorecards but also supports operational savings, reinforcing its role as a structural growth driver for the Canada folding carton market.

Expansion of Cannabis Packaging Requirements

Health Canada’s plain-packaging and child-resistance rules have spawned a dedicated carton niche with stringent compliance checkpoints. Retail cannabis sales totaled CAD 478 million (USD 377.6 million) in November 2025, rising 4.6% year-over-year, and virtually every product format relies on folding carton that carry standardized warnings and tamper-evident features. Solid bleached sulfate grades dominate the segment because they offer opacity, odor barriers, and crisp print reproduction demanded by regulatory graphics. Frequent updates to mandated warning statements have made digital print capability essential, allowing converters to pivot artwork without plate-making delays. Ontario, Quebec, Alberta, and British Columbia generate more than 80% of national cannabis turnover, creating regional hubs where specialized converters can amortize compliance expertise over multiple micro-runs. This regulatory intensity ensures a dependable, high-margin channel for the Canadian folding carton market even as other packaging formats vie for share.

Provincial EPR Regulations Accelerating Recyclability Mandates

British Columbia, Quebec, Ontario, and Nova Scotia each operate Extended Producer Responsibility frameworks that levy material-specific fees, with fiber-based carton enjoying the most favorable schedules. Recycle BC assigns lower assessments to paperboard than to multilayer laminates, directly lowering bill-back costs for brand owners. Quebec’s Éco Entreprises program reported a 75% recovery rate for paperboard in 2024, more than double that of flexible plastics. Ontario’s Resource Recovery and Circular Economy Act enforces escalating diversion targets, including financial penalties of up to CAD 500,000 (USD 357,653) per infraction. To avoid a province-by-province SKU matrix, multinational brands are adopting a single carton specification that meets the toughest jurisdictional test, effectively creating a quasi-national standard that further embeds folding carton in primary-pack portfolios. Converters demonstrating multi-province compliance credentials, therefore, move to the front of bid lists, reinforcing their revenue visibility within the Canada folding carton market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Recycled Fiber Supply After U.S. Export Bans | -0.90% | National, most acute in British Columbia and Quebec | Short term (≤ 2 years) |

| Rising Energy Costs For Board Converting Lines | -0.70% | National, highest exposure in Ontario and Quebec | Medium term (2-4 years) |

| Competitive Pressure From Flexible Stand-Up Pouches | -0.50% | National, greatest share loss in snack-food and pet-treat lines | Long term (≥ 4 years) |

| Capital-Intensive Compliance With Health Canada Labeling | -0.30% | National, disproportionate burden on smaller converters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Recycled Fiber Supply After U.S. Export Bans

Canada's folding carton market participants face margin compression whenever recycled-fiber spot prices spike, as tight U.S. export controls limit cross-border flows. Natural Resources Canada recorded a 7.5% drop in domestic pulp output during 2023, and printing-and-writing grades, a key feedstock for recycled content, fell 22.9%.[4]Natural Resources Canada, “How does the forest sector contribute to Canada’s economy?,” nrcan.gc.ca British Columbia’s carton exports slid 26% year over year in September 2025, signaling that fiber scarcity is reducing production scale. Converters in Quebec and Ontario now lock in multi-year fiber contracts to protect against quarterly price swings, even though that hedging reduces sourcing agility. The Canadian folding carton market, therefore, carries a built-in cost-volatility premium that competitors in regions with deeper secondary-fiber pools do not face. To mitigate the squeeze, large players invest in in-house recycling plants that capture converting scrap and post-consumer board, but smaller independents must absorb the price shocks or cede volume. Until U.S. policymakers relax recovered-paper export limits, fiber turbulence will remain a structural brake on Canada's folding carton market growth.

Rising Energy Costs For Board Converting Lines

Electricity and natural-gas price hikes in Ontario and Quebec threaten EBITDA margins for converters operating energy-intensive UV-curing and die-cutting equipment. Hydro-Québec lifted industrial power rates 3% in April 2025, while Ontario tariffs rose 4.2% in 2024. A 5% utility jump can erode margins by up to 80 basis points when pre-tax profitability averages 6-9%. The Canadian folding carton market, therefore, prizes energy-efficiency retrofits such as variable-frequency drives and LED-curing stations, yet capital outlays compete with investments in digital presses and automation. Smaller converters struggle to secure favorable time-of-use contracts, forcing production shifts to off-peak windows that complicate just-in-time delivery. Persistent rate escalation could accelerate plant rationalization, concentrating capacity in provinces with cheaper hydropower and leaving regional demand underserved. Energy inflation thus acts as a persistent drag on Canada's folding carton market competitiveness relative to U.S. peers, which enjoy lower natural-gas costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Dual Growth Paths For Virgin And Recycled Grades

The 38.23% share held by folding boxboard in 2025 places it at the center of everyday grocery and household SKUs, yet solid bleached sulfate is pacing the field with a forecast 7.19% CAGR because cosmetics, pharmaceuticals, and cannabis brands demand pristine print surfaces and moisture barriers. Smurfit WestRock’s La Tuque shutdown removed 127,000 tonnes of domestic SBS capacity, nudging converters to import from larger U.S. mills and tightening local supply. This squeeze elevates unit prices while also underlining SBS's premium positioning within the Canadian folding carton market. Recycled, coated, unbleached kraft continues to win niche applications in craft-beer carriers and organic snack multipacks, where earthy aesthetics resonate with sustainability messaging. White line chipboard, largely confined to toys and hardware, competes strictly on the lowest landed cost and shows minimal innovation. Parallel growth tracks therefore exist mainstream FMCG relies on high-recycled-content boxboard to meet EPR cost targets, while prestige and regulated verticals gravitate toward virgin-fiber SBS for compliance and visual impact. Converters that can switch between these substrates without line-change delays will capture an outsized share of the Canadian folding carton market by 2031.

Heightened e-commerce activity also influences material choice. Online grocery orders generate last-mile bumps and drops that demand tougher crease strength, steering some brands toward hybrid micro-corrugated grades that blend cushion and graphics. Meanwhile, cannabis edible launches require SBS with aroma barriers to prevent terpene transfer, reinforcing virgin-fiber demand. The coexistence of lightweight boxboard and premium SBS confirms that Canada's folding carton industry players must carry multi-grade inventories. Those with mill integration or long-term offtake contracts hedge against fiber tightness, whereas independents lean on flexible converting fees to offset purchase-price volatility. Material agility, therefore, defines competitive edge as the Canada folding carton market evolves.

By Printing Technology: Digital Workflows Redefine Speed And SKU Turnover

Flexographic lines delivered 44.01% of 2025 output thanks to high speeds and water-based inks that meet environmental norms, but digital presses are expanding at a 9.38% clip because they eliminate plate costs and allow variable-data campaigns. Cannabis carton change legally required text whenever Health Canada updates warnings, making digital essential for a compliant turnaround. Likewise, direct-to-consumer snack brands launch seasonal flavors every quarter, requiring small-batch runs that flexo economics cannot accommodate. Lithographic offset retains a foothold in long-run cosmetics work where high-gloss coatings must pop on the shelf, yet the quality gap to high-resolution inkjet narrows with each release cycle. Gravure is used only in multi-hundred-thousand-unit projects, such as gift-box liners for holiday confectionery. Hybrid presses flexo units fitted with digital modules—are emerging as middle-ground solutions for converters hedging against run-length uncertainty.

Digital’s ability to print serialized QR codes links physical packaging to online loyalty programs, aligning with omnichannel marketing playbooks. As e-commerce volumes mount, brands treat the shipper box as an owned-media channel, driving incremental demand for full-bleed digital graphics on mailers. Converters investing in inline inspection and cloud-based job management cut makeready waste and accelerate cycle time from brief to finished shipper. These capabilities help them win contracts that embed annual volume floors, stabilizing revenue even when individual SKU runs shorten. Because capital budgets are finite, plants prioritizing digital often phase out legacy offset lines, reshaping asset bases across the Canada folding carton market.

By End-User Industry: E-Commerce And Regulated Verticals Accelerate

Food and beverage retained 41.38% of 2025 shipments, anchored by cereal, confectionery, and frozen entrées, which still move primarily through brick-and-mortar grocery stores. Yet online grocery penetration is climbing, and retail-ready shelf-trays that convert to on-site display units are issuing fresh RFQs that blur the lines between primary and secondary roles in the Canadian folding carton market. E-commerce-specific formats are projected to grow at a 9.16% CAGR, more than double legacy FMCG, as direct-to-consumer brands prioritize customized unboxing. Healthcare and pharmaceuticals continue to expand because Canada’s population ages and prescription volumes rise. Serialization mandates force each carton to carry a unique alphanumeric code, further cementing digital workflow adoption. Personal care and cosmetics maintain premium SBS demand, where embossing, foil stamping, and spot-UV create shelf differentiation.

Electronics brands headquartered in Ontario are replacing plastic clamshells with molded-pulp inserts nested in carton outers, reducing resin use and improving recyclability grades in provincial scorecards. Cannabis remains a standout, with all dried-flower, pre-roll, and gummy SKUs shipping in carton that comply with Health Canada’s child-resistant rules. Pet-food treats have begun migrating from stand-up pouches back to folding carton to gain billboard space for sustainability messaging. Tobacco volumes continue their secular decline, yet still contribute steady baseline tonnage. This fragmentation obliges converters to master regulatory, temperature, and barrier nuances across verticals, reinforcing the complexity that defines discussions of the Canada folding carton market size.

Geography Analysis

Ontario and Quebec together command roughly two-thirds of the Canadian folding carton market because they cluster food processing, pharmaceutical pack-off, and brand-owner headquarters. Toronto-area converters leverage short delivery windows and co-design studios that pull retailers into rapid prototyping sessions, shrinking time-to-shelf for seasonal launches. Quebec’s integrated pulp-and-paper network supplies both virgin and recycled fiber at shorter trucking radii, containing freight costs and lowering carbon footprints relative to imported board. British Columbia, though smaller in volume, serves Asia-facing exporters of seafood and craft beverages, requiring moisture-resistant carton engineered for reefer containers. The province’s cannabis producers push premium graphics that reflect West Coast branding aesthetics, adding to SBS demand.

Alberta rides energy-sector cyclicality yet benefits from a rapidly growing cannabis retail footprint that reached CAD 478 million (USD 341.9 million) in November 2025. Prairie-province converters invest in digital lines to serve microbrewery and artisanal snack clients that value short runs and quick reorders. Atlantic Canada remains the smallest slice of the Canada folding carton market share but posts steady gains on the back of frozen seafood exports. New Brunswick carton plants capitalize on proximity to U.S. Eastern seaboard buyers, offsetting domestic scale limits. Northern territories generate marginal tonnage, yet population growth in Yukon and Nunavut sparks interest in lightweight, flat-pack formats that assemble on site to slash inbound freight volume.

Regulatory mosaics further shape regional dynamics. Recycle BC’s fee matrix makes fiber clearly cheaper than multilayer plastics, encouraging more rapid carton migration than in provinces with looser schedules. Ontario’s Resource Recovery and Circular Economy Act imposes minimum diversion thresholds that influence national brand guidelines, effectively harmonizing designs around the strictest provincial rulebook. Converters able to navigate each system without customizing SKUs protect margin and widen customer appeal, reinforcing Ontario- and Quebec-centric manufacturing dominance within the Canada folding carton market.

Competitive Landscape

The market remains moderately fragmented, scoring a mid-range concentration as regional independents coexist with global majors. TC Transcontinental’s USD 2.1 billion sale of its packaging arm to ProAmpac in March 2026 removed a vertically integrated incumbent, redistributing volume to rivals able to step into customer contracts. Cascades channeled CAD 6.9 million (USD 5.0 million) into recycling upgrades at Kingsey Falls to capture Extended Producer Responsibility cost advantages and guard fiber access.

Graphic Packaging shuttered its recycled-paperboard mill at East Angus in December 2025, illustrating cost-pressure attrition among smaller, less-automated sites. Strategy now hinges on circular-economy validation, lead-time compression, and digital-print breadth rather than brute capacity. ProAmpac inherits TC Transcontinental’s Eastern Canada footprint and can cross-sell flexible formats alongside carton, giving it a portfolio breadth that resonates with omnichannel brands.

Cascades’ FSC and SFI chain-of-custody certifications are table stakes in most retail tenders, while Great Little Box Company secures niche wins by pairing design services with 72-hour turnarounds. Automation adoption separates winners from laggards; robots and inline vision cut defect rates and labor spend, fortifying margins despite energy cost creep. Converters are slow to digitize or document ESG compliance risk exclusion from strategic supplier rosters, a trend that pushes the Canada folding carton industry toward higher capability thresholds.

Canada Folding Carton Industry Leaders

Smurfit Westrock plc

Graphic Packaging Holding Company

Cascades Inc.

TC Transcontinental Inc.

Atlantic Packaging Products Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: TC Transcontinental finalized the USD 2.1 billion divestiture of its packaging business to ProAmpac, refocusing on printing and digital media.

- March 2026: Cascades invested CAD 6.9 million (USD 5.0 million) in Kingsey Falls to boost recycled-fiber yield and align with EPR fee structures.

- February 2026: Smurfit WestRock permanently shut a 127,000-tonne SBS machine at La Tuque, Quebec, citing scale inefficiencies.

- January 2026: Cascades exited the West Coast by selling its Richmond, British Columbia plant to Crown Paper Group for CAD 65.5 million (USD 47.5 million).

Canada Folding Carton Market Report Scope

The Canadian folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into carton for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Canada Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare and Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Canada folding carton market size?

The Canada folding carton market size is estimated at USD 1.28 billion in 2026 and is projected to reach USD 1.78 billion by 2031.

Which segment is growing fastest within folding carton in Canada?

E-commerce and retail-ready applications are forecast to expand at a 9.16% CAGR through 2031 due to rising online grocery penetration.

Why is solid bleached sulfate gaining share?

Solid bleached sulfate offers superior printability and barrier properties demanded by cosmetics, pharmaceuticals, and cannabis brands, driving a projected 7.19% CAGR to 2031.

How are provincial EPR fees shaping material choices?

Provinces levy lower fees on recyclable fiber carton than on multilayer plastics, incentivizing brand owners to switch to paperboard formats to control compliance costs.

What role does digital printing play in market growth?

Digital presses enable variable-data artwork and rapid SKU refreshes, making them essential for cannabis packaging and direct-to-consumer brand strategies.

Which regions dominate demand for folding carton?

Ontario and Quebec together generate about two-thirds of national demand thanks to dense clusters of food processing, pharmaceuticals, and brand headquarters.

Page last updated on: