France Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.28 Billion |

| Market Size (2026) | USD 2.36 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Folding Carton Market Analysis by Mordor Intelligence

The France folding carton market size is expected to increase from USD 2.28 billion in 2025 to USD 2.36 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 4.04% over 2026-2031. Robust growth reflects the accelerated switch from plastic to fiber packaging imposed by France’s Anti-Waste for a Circular Economy law and the European Union Packaging and Packaging Waste Regulation, both of which require full recyclability by 2030. Brand owners are spending on mineral-oil-free inks, water-based barrier coatings, and recycled-content boards, driving capital investment in converting lines that can certify compliance at scale. Structural changes in online retail, where EUR 175.3 billion (USD 198.1 billion) in e-commerce sales in 2024 increased demand for direct-to-consumer formats, add further momentum to the French folding carton market. Meanwhile, the merger of International Paper and DS Smith sparked plant divestitures that preserved regional rivalry, ensuring converters still compete on service, substrate agility, and print sophistication rather than price alone. Players that can navigate regulatory costs, secure dual-fiber sources, and offer both lithographic speed and digital flexibility are positioned to capture premium work as the French folding carton market tips decisively toward fiber-based solutions.

Key Report Takeaways

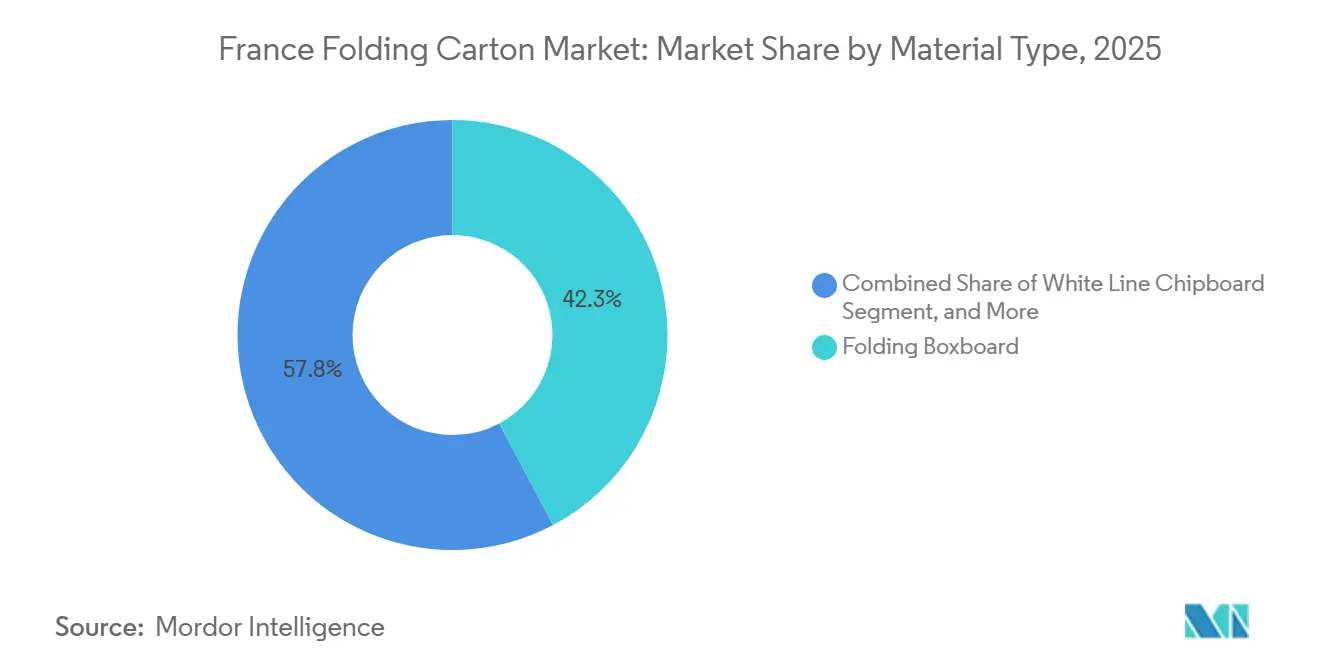

- By material type, folding boxboard captured 42.25% of the France folding carton market share in 2025.

- By printing technology, the France folding carton market size for the digital printing segment is forecast to advance at a 5.44% CAGR through 2031.

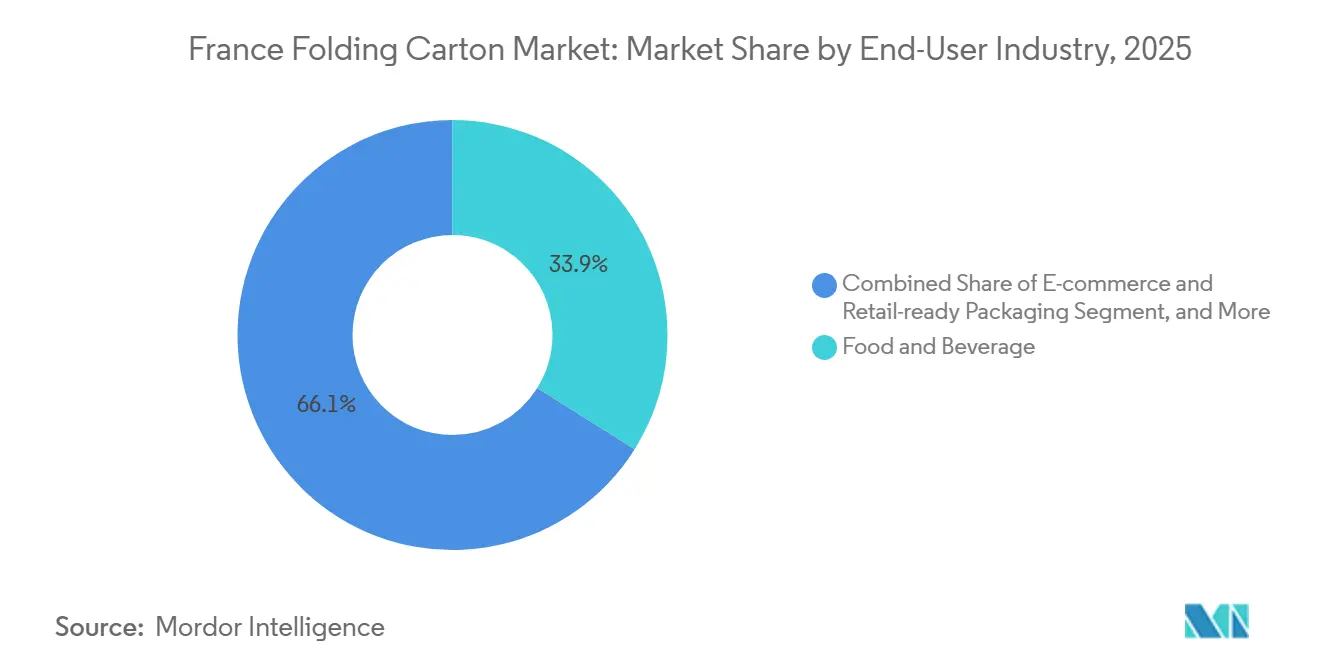

- By end-user industry, food and beverage captured 33.91% of the France folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban On Single-Use Plastics And Shift To Fiber-Based Packaging | +1.20% | National with spillover to broader EU compliance | Medium term (2-4 years) |

| Growth Of E-Commerce And Delivery Services | +0.90% | Île-de-France, Lyon, Marseille metro areas | Short term (≤ 2 years) |

| Rising Demand For Premium Packaged Food And Cosmetics | +0.70% | Paris and Grasse luxury clusters | Medium term (2-4 years) |

| Advances In Digital And Flexographic Printing | +0.50% | Early adoption nationwide | Short term (≤ 2 years) |

| Adoption Of Smart Anti-Counterfeit Inks And QR-Coded Carton | +0.30% | Pharmaceutical and luxury sectors | Long term (≥ 4 years) |

| Scaling Of Molded Fiber Barrier Coatings For Chilled Meals | +0.40% | Ready-to-eat and fresh-meal providers nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ban on Single-Use Plastics and Shift to Fiber-Based Packaging

France set a 20% reduction target for single-use plastics by 2025, backed by a comprehensive phase-out roadmap toward 2040. The European Union regulation, which comes into force on 12 August 2026, intensifies pressure by requiring all packaging sold in the bloc to be economically recyclable by 2030.[1]Vinetur Staff, “European Union Sets 2026 Start Date for Strict Packaging Rules Targeting Waste Reduction,” Vinetur, vinetur.com Brand owners are therefore re-engineering multilayer films into mono-material carton solutions for confectionery overwraps, ready-meal trays, and personal-care sleeves. Nestlé France has already switched several confectionery SKUs to carton sleeves, citing reduced compliance risks and gains in shelf appeal.[2]Agro Media Editors, “PPWR : Un tournant réglementaire majeur,” Agro-Media, agro-media.fr Converter R&D now focuses on aqueous coatings, PVOH dispersions, and cellulose-based barriers that can withstand high-water-vapor environments without compromising recyclability. As compliance deadlines loom, substrate innovations are migrating from lab scale to commercial print runs, lifting value per tonne and reinforcing the premium position of the French folding carton market.

Growth of E-Commerce and Delivery Services

E-commerce in France generated EUR 175.3 billion (USD 198.1 billion) during 2024, and 62% of consumers shop online at least monthly.[3]Fédération du e-commerce et de la vente à distance, “Chiffres Clés 2024,” Fevad, fevad.com Retailers now specify folding carton that work as both last-mile shipping containers and shelf-ready displays, combining reinforced corners, peel-away fronts, and integrated handles. These hybrid formats shorten store replenishment times and boost brand visibility on arrival, but they require shorter print runs and frequent artwork revisions. Digital presses can swap graphics in minutes, letting converters tailor outer carton for seasonal campaigns while holding litho for base volumes. Carriers such as La Poste and Chronopost are simultaneously tightening dimensional weight rules, which forces right-sizing and drives unit growth for smaller blank sizes, further supporting the French folding carton market.

Rising Demand for Premium Packaged Food and Cosmetics

French luxury cosmetics houses and premium chocolatiers increasingly specify virgin-fiber boards above 300 GSM to enable foil stamping, multi-level embossing, and soft-touch lamination. Stora Enso responded with Ensovelvet, an uncoated SBS grade launched in September 2025, which delivers a tactile, matte surface prized by fragrance brands. Virgin fiber also meets the 2026 migration rules of the Directorate-General for Competition, Consumer Affairs, and Fraud Prevention, which extend food-contact scrutiny to secondary packaging. As gourmet food exporters seek to preserve terroir credentials abroad, solid bleached sulfate volumes are climbing, supporting healthier margins for converters that can handle both SBS and coated folding boxboard within the same press hall.

Advances in Digital and Flexographic Printing

Inkjet platforms that integrate inline die-cutting and automatic color management have reduced makeready times from hours to minutes. French converters deploy hybrid lines pairing flexographic units for base colors with digital modules for serialized QR codes, variable nutrition panels, and limited-edition designs. The transition is helped by LED-UV curing, which reduces energy use and allows immediate downstream folding. Water-based ink sets have displaced mineral-oil formulations to stay under the 0.1% MOSH and MOAH thresholds.[4]Leko Regulatory Team, “Focus Réglementaire 2025,” Leko, leko-organisme.fr Converters that invested early now enjoy a two-year lead in qualifying pharmaceutical artwork and securing brand budgets committed to real-time promotion, pushing overall technology adoption forward in the French folding carton market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Virgin Fiber And Recovered Paper Prices | -0.60% | Nordic pulp benchmarks and pan-European recovered-paper flows | Short term (≤ 2 years) |

| Competition From Flexible Plastic Pouches | -0.40% | Snack foods, pet food, liquid applications nationwide | Medium term (2-4 years) |

| Capacity Constraints In French Converting Plants | -0.30% | Normandy, Île-de-France, Auvergne-Rhône-Alpes | Short term (≤ 2 years) |

| Stricter MOSH/MOAH Compliance Requirements | -0.20% | Recycled-fiber users and offset printers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber and Recovered Paper Prices

French cartonboard producers withdrew listed price increases twice in 2025 after downstream customers destocked inventories in response to sharply falling Nordic pulp and recovered-paper quotations. In April 2026, Sonoco announced an EUR 80 (USD 90) per tonne rise for uncoated recycled paperboard alongside an 8% uplift for tube and core products, citing energy and chemical inflation. Such swings squeeze converters that lock in multi-year SBS volumes yet still face quarterly pulp resets. Smaller family-owned plants, lacking hedging tools, reported negative margins in late 2025 and lost contracts to vertically integrated rivals, delaying planned machinery upgrades and constraining capacity additions within the French folding carton market.

Competition From Flexible Plastic Pouches

Stand-up pouches carry spouts, zippers, and higher moisture barriers at lower gram weights, making them a formidable option in snack, pet food, and aseptic beverage lines. Although life-cycle studies show fiber carton deliver smaller carbon footprints, price-sensitive private-label brands still select flexible formats for cost and shelf-life benefits. Converters fight back with carton sleeves plus internal monofilm pouches, yet these hybrids complicate recycling streams and could face penalties under the 2026 EU design-for-recycling criteria. Unless fiber formats match the weight-to-volume ratio and barrier performance of pouches at comparable cost, the France folding carton market risks losing growth in select high-volume food categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Virgin Fiber Boards Capture Premium Demand

The France folding carton market size for solid bleached sulfate is projected to expand at a 5.19% CAGR, capturing incremental value from luxury cosmetics, pharmaceuticals, and gourmet confectionery applications. Folding boxboard retained 42.25% France folding carton market share in 2025 because cereals, frozen meals, and household cleaners prioritize cost and availability over brightness. Demand for coated unbleached kraft is rising in organic food segments that communicate natural positioning through a brown-fiber aesthetic, while white line chipboard remains the low-cost option for toys and DIY hardware. Nordic suppliers are bringing 950,000 tonnes of new SBS and FBB capacity online by 2027, allowing French converters to hedge against North American supply tightness and slim lead times. Lighter-basis-weight innovations, dropping from 350 GSM to 280 GSM, further lower material use without compromising compression strength, aligning with eco-contribution fee structures that reward low-mass designs.

Converters that straddle commodity and premium lines exploit the bifurcated substrate landscape. Smurfit Westrock has recurring lead-time constraints on SBS grades, which pushes some brands to dual source with European mills, while Mayr-Melnhof recorded EUR 436.7 million (USD 494 million) in France sales for H1 2025 yet warned of destocking pressure that hit folding boxboard volumes. The flexibility to switch SKUs between grades underpins service competitiveness in the France folding carton market.

By Printing Technology: Digital Gains Short-Run Share

Lithography accounted for 37.88% of the total French folding carton market revenue in 2025, leading in long runs that demand consistent ink laydown and fine highlight retention. Digital printing is forecast to grow at a 5.44% CAGR, driven by personalization, test marketing, and regional promotions, capped at a few thousand units. Flexographic systems, equipped with high-definition anilox and LED-UV lamps, narrow the quality gap with litho while matching its line speeds, making flexo the workhorse for mid-volume food and beverage carton. Gravure maintains a role in ultra-long-run tobacco and duty-free alcohol sleeves, where metallic inks and tactile varnishes justify the cost of cylinders.

French converters embrace integrated workflows. Autajon feeds product information management data directly to hybrid presses, cutting order-to-delivery cycles from weeks to days and enabling serialized track-and-trace for pharma carton. Digital’s higher per-impression cost remains a hurdle for mass-market breakfast cereals, but ink pricing is falling 7% annually, and the breakeven run length versus litho now sits near 2,500 units. As supply chains shorten, those economics tilt further toward digital, reinforcing technology upgrading across the French folding carton market.

By End-User Industry: E-Commerce Redefines Carton Geometry

Food and beverage accounted for 33.91% of the French folding carton market in 2025, spanning everything from shelf-stable cereals to chilled seafood packs. The directive that all packaging be recyclable by 2030 cross-cuts every subcategory, diverting R&D budgets toward mono-material, grease-resistant coatings for ready-to-eat meals. Healthcare and pharmaceuticals demand tamper-evident tuck-in flaps and serialized codes that can be printed in a single pass, raising barcoding and die-cutting complexity at the plant floor. Luxury cosmetics specify embossed SBS above 300 GSM to accommodate hot-foil features that convey exclusivity, with the Grasse perfume cluster anchoring these volumes.

E-commerce and retail-ready packaging is expected to grow at 6.61% during 2026-2031, the fastest of all segments, as omnichannel models merge secondary and tertiary packaging functions. Carton ship in pure brown kraft outside yet reveal litho-laminated graphics inside for an “Instagrammable” unboxing experience. Electrical and electronics brands integrate anti-static coatings and molded-fiber inserts, while tobacco still rewards gravure for its fine thermochromic print elements even as overall stick volumes slide. Such heterogeneity forces plants to offer rapid setup changes and multifaceted finishing, driving automation spend across the French folding carton market.

Geography Analysis

Île-de-France anchors demand for virgin-fiber premium carton serving Parisian luxury cosmetics houses and big-pharma headquarters, where compliance and shelf appeal trump cost. Normandy and Brittany host seafood, dairy, and bakery processors that consume high volumes of commodity folding boxboard, while Auvergne-Rhône-Alpes focuses on cosmetics, fine chemicals, and personal-care goods near Lyon and Grasse. International Paper’s divestiture of three Normandy plants to PALM Group in July 2025 preserved competitive tension locally after its DS Smith takeover, an outcome keenly watched by antitrust bodies.

France’s 2026 DGCCRF guidelines expanded food-contact testing to secondary packs, obligating migration studies for inks, coatings, and adhesives, even on carton that never directly contact food. Extended producer responsibility rules that took effect in January 2025 require higher eco-contributions for non-recyclable formats, prompting retailers to ask converters for design-for-recycling certificates before quotation. Saica and Brodart have invested EUR 70 million (USD 79 million) in energy-efficient corrugators, digital presses, and automated gluing cells since 2025 to offset future eco-fees and reduce scope-one emissions. La Rochette installed a EUR 10 million (USD 11 million) biomass boiler to lock in renewable energy credits and lower steam costs, aiding compliance and improving bid competitiveness.

The geographic clustering of mills near customers limits empty-truck miles, an advantage as road taxes and low-emission zones proliferate around large French cities. Proximity also helps converters run quick reruns for cosmetic launch cycles and pharmaceutical change orders, sharpening the local-service premium embedded within the French folding carton market.

Competitive Landscape

The French folding carton industry features a balanced mix of multinational integrated board producers and nimble regional specialists. Smurfit Westrock, Graphic Packaging, and International Paper collectively capture close to one-quarter of domestic folding carton output, benefiting from captive pulp, proprietary barrier coatings, and multi-country backup plants. Mid-tier players like Saica, Autajon, and Mayr-Melnhof leverage geographic proximity to deliver 24-hour artwork changes and low minimum order quantities, traits valued by luxury and pharmaceutical accounts. Below that tier, over 90 family-owned converters operate one- to three-press facilities, focusing on regional food processors and seasonal agricultural packs.

Technology deployment drives share gains. Bobst’s hybrid flexo-inkjet presses enable converters to handle both bulk litho reruns and small personalized editions without additional floor space, reducing labor hours per thousand carton. Stora Enso’s patent portfolio around bio-based grease barriers differentiates bulk SBS grades, opening an opportunity as the EU tightens PFAS restrictions in 2027. Co-op buying groups among small printers reduce virgin-fiber purchase costs by up to 6%, but they still struggle to fund the EUR 3-5 million (USD 3.38-5.64 million) needed for next-generation digital lines.

Mergers remain on the horizon as the PPWR’s 2026 compliance trigger accelerates capital needs faster than some independents can finance them. Nonetheless, customer intimacy, local flavor, and the ability to accommodate emergency runs within 48 hours keep niche converters relevant, maintaining a moderate concentration profile in the French folding carton market.

France Folding Carton Industry Leaders

Smurfit Westrock plc

Graphic Packaging Holding Company

International Paper Company

Mayr-Melnhof Karton AG

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sonoco raised EMEA prices by EUR 80 (USD 90) per tonne for uncoated recycled paperboard and 8% for tube and core goods to cover higher energy and chemical costs, impacting downstream carton converters.

- April 2026: The European Commission cleared the International Paper and DS Smith merger subject to five plant divestitures, including two sites in southwest France, to ease regional competition worries.

- February 2026: DGCCRF released updated guidance that extends food-contact regulations to secondary and outer packaging, intensifying migration testing for inks, coatings, and adhesives in folding carton.

- July 2025: International Paper completed the sale of three Normandy corrugated plants to PALM Group, fulfilling antitrust obligations tied to the DS Smith acquisition.

France Folding Carton Market Report Scope

The France folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into carton for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The France Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-Commerce and Retail-Ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-Commerce and Retail-Ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the France folding carton market?

The France folding carton market size is estimated at USD 2.36 billion in 2026, on track to reach USD 2.87 billion by 2031.

Why are French brands switching from plastic to folding carton?

National anti-waste legislation and the European Union's requirement that all packaging be recyclable by 2030 accelerate the move from plastic films to fiber carton that can pass curbside collection standards.

Which material grade is growing fastest in French folding carton?

Solid bleached sulfate, favored by luxury cosmetics and pharmaceuticals, is projected to grow at a 5.19% CAGR through 2031, outpacing other board grades in the France folding carton market.

How is e-commerce influencing folding carton design in France?

Online retail growth pushes converters to produce retail-ready carton that double as shipping boxes, feature tear-away fronts for shelf display, and come in right-sized dimensions that reduce carrier surcharges.

What printing technology is gaining share in French carton converting?

Digital printing is expanding at a 5.44% CAGR because it enables low-order quantities, variable data, and quick artwork swaps critical for personalized promotions and regulatory changes.

Which regulation affects food-contact compliance for folding carton in 2026?

The DGCCRF's February 2026 guidelines extend food-contact testing to secondary packaging, compelling French converters to validate inks, adhesives, and coatings used on folding carton.

Page last updated on: