United Kingdom Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

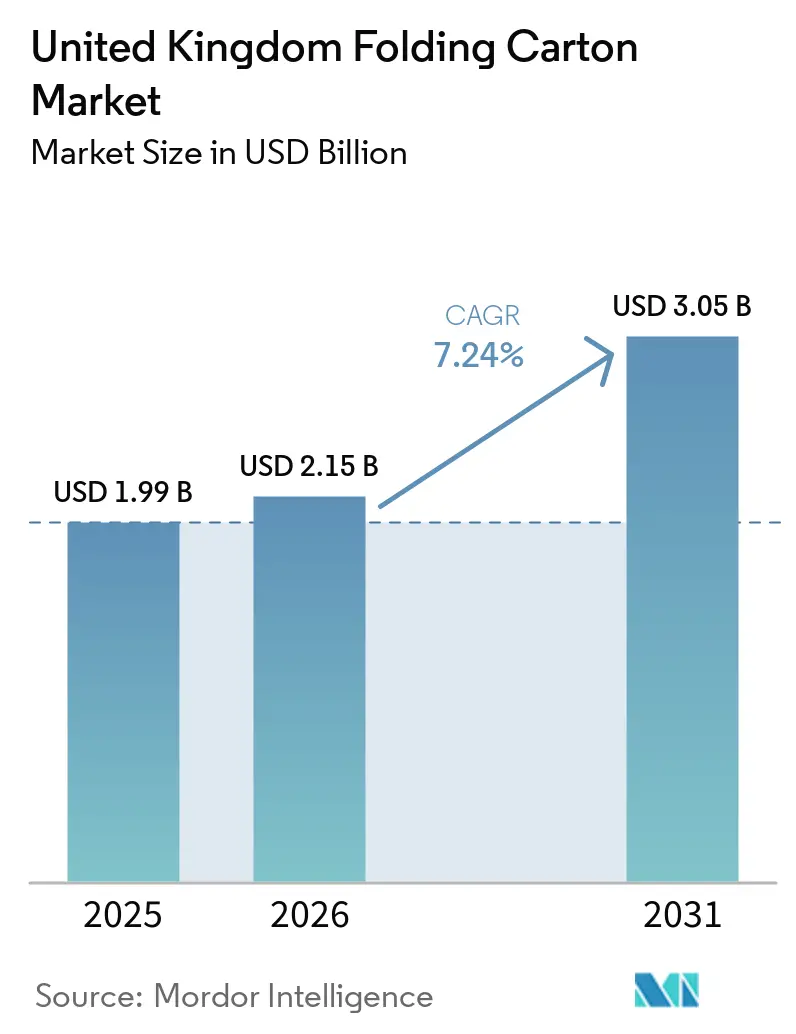

| Base Year Market Size (2025) | USD 1.99 Billion |

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 3.05 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

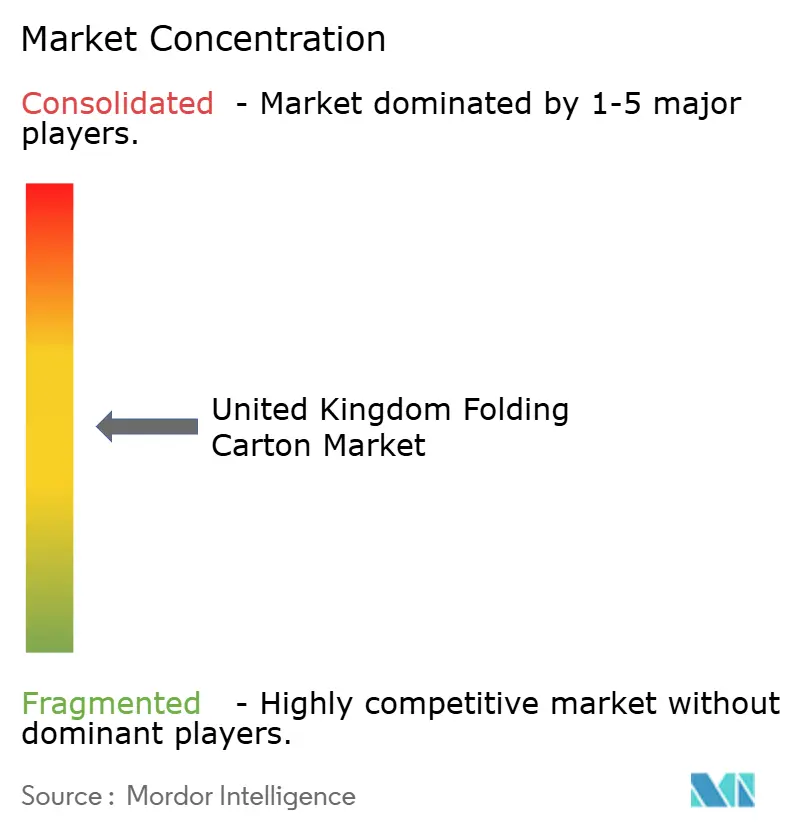

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Folding Carton Market Analysis by Mordor Intelligence

The United Kingdom folding carton market size was valued at USD 1.99 billion in 2025 and is estimated to grow from USD 2.15 billion in 2026 to reach USD 3.05 billion by 2031, at a CAGR of 7.24% during the forecast period (2026-2031). Heightened regulatory pressure, the rapid build-out of e-commerce logistics, and brand owners’ pivot toward fiber packaging to avoid Plastic Packaging Tax liabilities are the central growth catalysts. Mandatory Simpler Recycling collections that started in March 2026 have tightened quality requirements on household fiber streams, encouraging converters to lock in certified recycled content contracts. Investments in barrier-coated cartonboard and digital print capacity are enabling converters to replace plastic laminates while supporting SKU proliferation and regional promotions, themes that are strengthening pricing resilience despite pulp cost turbulence. Competitive intensity remains moderate because the top five suppliers command only 35% revenue, which leaves consolidation headroom for mid-tier players that need scale to fund digital transformation and recyclability testing.

Key Report Takeaways

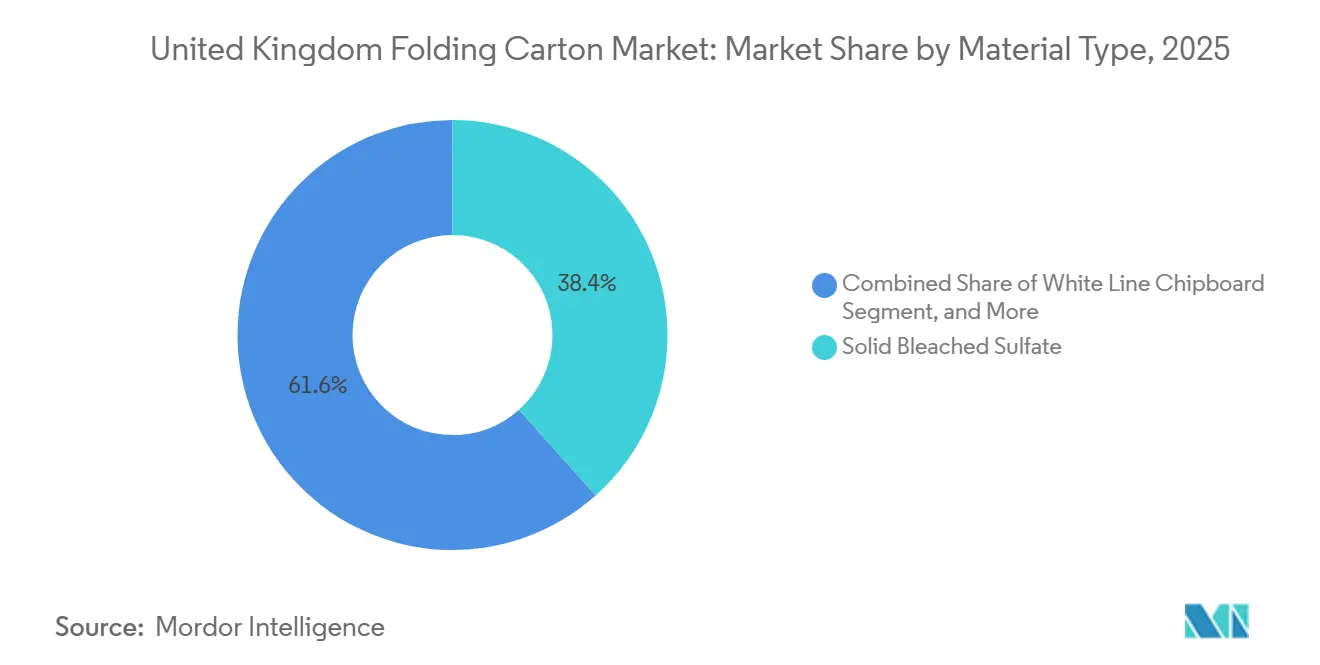

- By material type, solid bleached sulfate captured 38.41% of the United Kingdom folding carton market share in 2025.

- By printing technology, the United Kingdom folding carton market size for the digital printing segment is forecast to advance at a 9.02% CAGR through 2031.

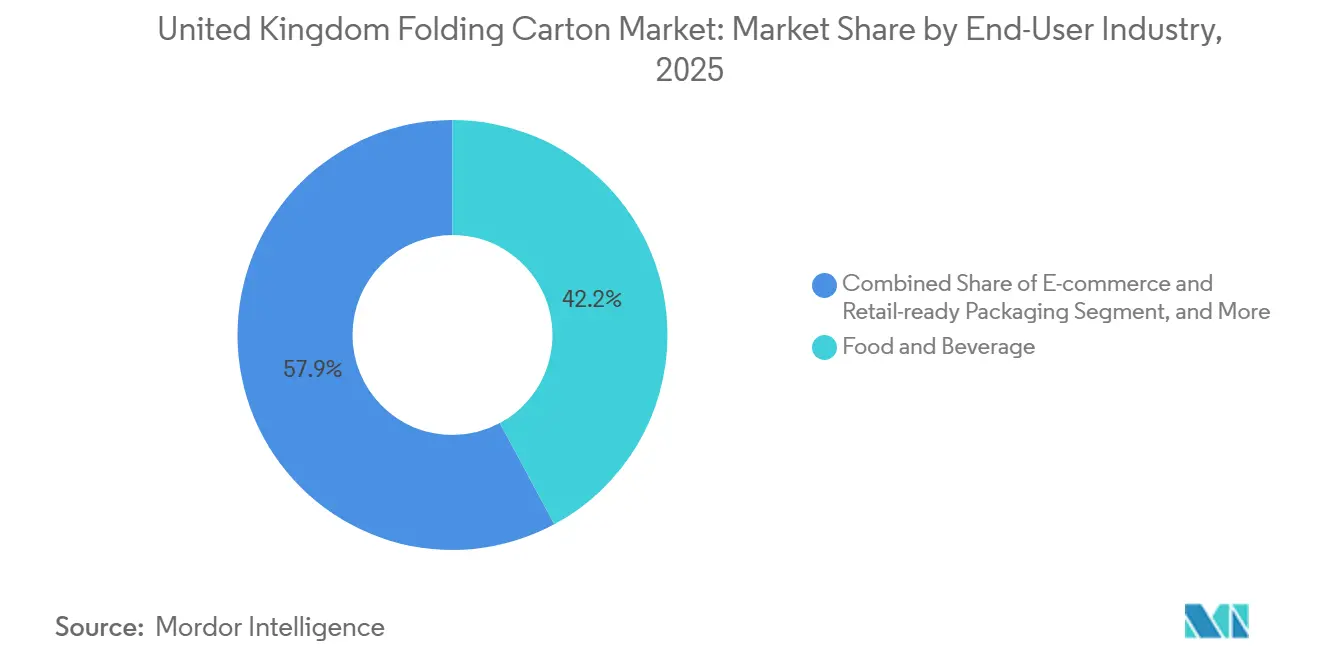

- By end-user industry, food and beverage captured 42.15% of the UK folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Phase-Out of Single-Use Plastics Under the UK Plastic Packaging Tax | +1.80% | UK-wide, spillover to EU-facing exporters | Medium term (2-4 years) |

| E-Commerce Growth Fueling Demand for Lightweight Letterbox-Friendly Carton | +1.50% | National, dense in urban logistics hubs | Short term (≤ 2 years) |

| Adoption of Digital Printing for Short Runs and SKU Proliferation | +1.20% | UK-wide, early adoption in Southeast England and Scotland | Medium term (2-4 years) |

| Brand Premiumization Raising Demand for High-Quality Graphic Carton | +0.90% | National, led by London beauty and personal care brands | Long term (≥ 4 years) |

| Investments in Recyclable Barrier Coatings Enabling Carton Replacement of Plastic Laminates | +0.70% | UK and EU, technology transfer from Finland and Germany | Medium term (2-4 years) |

| Government Incentives for Domestic Recycling Capacity Boosting Supply of Recycled Fiber | +0.60% | England-focused, devolved variations in Scotland and Wales | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Phase-Out of Single-Use Plastics Under the UK Plastic Packaging Tax

The April 2026 tax hike to GBP 228.82 (USD 291) per tonne on packaging containing less than 30% recycled plastic has raised immediate compliance costs for hybrid carton with plastic windows or barrier films, prompting brand owners to redesign packs in favor of mono-material board solutions.[1]Multiplastics, “Plastic Packaging Tax – April 2026,” multiplastics.co.uk From April 2027, a mass-balance allowance for chemically recycled plastic will provide relief, but the additional auditing burden is likely to keep the momentum of fiber substitution intact. Categories such as frozen vegetables and confectionery have begun migrating from plastic pouches to dispersion-coated carton that meet moisture and grease barriers without compromising recycling yields. HM Revenue and Customs expects the policy mix to lift recycled plastic use in UK packaging by roughly 40%, saving nearly 200,000 t of CO₂ annually.[2]Department for Environment, Food and Rural Affairs, “Simpler Household Recycling Rules Come Into Force Across England,” gov.uk Converters that can certify near-zero plastic inputs are therefore winning incremental shelf space in supermarkets and on direct-to-consumer platforms.

E-Commerce Growth Fueling Demand for Lightweight Letterbox-Friendly Carton

Secondary packaging volumes for European e-commerce are projected to climb 45% between 2023 and 2030, outpacing overall packaging demand by a factor of four.[3]Packaging News, “Packaging Innovations 2026: Global Secondary Packaging Market,” packagingnews.co.uk Letterbox-compatible formats under 25 mm in height reduce delivery failures and curb logistics emissions, but still need to balance cushioning with material minimization. Right-sizing automation and dynamic pack-dimensioning have become standard investments at UK fulfillment centers, enabling converters to deliver custom carton blanks in 24 hours. Upcoming EU rules capping empty space to 50% for grouped and e-commerce packs add cross-border urgency for UK sellers, reinforcing the adoption of lightweight folding cartonboard that delivers both structural integrity and recyclability.

Adoption of Digital Printing for Short Runs and SKU Proliferation

A USD 50 million agreement between HP and ePac to add ten Indigo 200K presses underscores the acceleration of digital economics, with 30% faster speeds and AI-assisted defect detection trimming waste on short jobs.[4]HP Newsroom, “HP Indigo and ePac Scaling Flexible Packaging,” hp.com For folding carton converters, the break-even point versus litho has fallen below 5,000 units for four-color work, making digital print the go-to choice for regional promotions, subscription boxes, and seasonal cosmetics. Bobst’s Digital Master 55, capable of 15-minute job changes, allows same-day dispatch of personalized carton. Investment decisions now hinge less on ink cost and more on recruiting print technologists in a tight labor market, a challenge that industry federations flagged at cross-association meetings in March 2026.

Brand Premiumization Raising Demand for High-Quality Graphic Carton

Beauty and personal care labels are turning carton into display assets by combining custom-colored papers, blind debossing, and matte foils that deliver both tactility and recyclability. Stora Enso’s Performa Lumi, launched in January 2026, offers GC1 board at 205-310 gsm with FiberLight Tec technology that maintains stiffness while reducing weight, aligning with luxury positioning without violating the Extended Producer Responsibility fee modulation. Premium mono-material carton simplify recycling streams and avoid EPR surcharges on metalized or plastic-lined packs, aligning cost control with visual impact for prestige portfolios.

Investments in Recyclable Barrier Coatings Enabling Carton Replacement of Plastic Laminates

Henkel’s Loctite Liofol CS 7106 RE cold-seal, certified for mechanical paper recycling, gives snack and ice-cream brands a resealable paper option without heat-seal energy loads. Archroma’s PFAS-free Cartaseal OGB F10 and Walki’s EVO Line dispersion coats round out a toolbox that matches grease and moisture resistance traditionally delivered by polyethylene or fluorochemical layers. As the EU’s Packaging and Packaging Waste Regulation advances recyclability criteria to 2030, UK converters with approved barrier systems are front-running specifications for multinational food brands.

Government Incentives for Domestic Recycling Capacity Boosting Supply of Recycled Fiber

A GBP 1.1 billion (USD 1.4 billion) grant package announced in July 2025 is funding new sortation lines and mill upgrades to improve recovered fiber quality. Simpler Recycling rules mandate separate paper-and-card collections nationwide, increasing feedstock purity for domestic reprocessors. Waste contractors such as Veolia project an extra 40,000 tonnes of plastics and paired tonnage of fiber entering closed-loop supply annually, improving converters’ access to certified recycled pulp. Over the long term, cheaper and cleaner domestic furnishings are expected to shave compliance costs associated with 30% recycled-content thresholds in both plastic and paper legislation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Pulp Prices Squeezing Converter Margins | -1.10% | UK and continental Europe, reliant on Nordic and North American imports | Short term (≤ 2 years) |

| Competition From Flexible Plastic Pouches for Food Products | -0.80% | National, centered in frozen food, snacks, confectionery | Medium term (2-4 years) |

| Capacity Constraints in UK White-Fiber Recycling Infrastructure | -0.50% | England-focused, gaps in Scotland and Wales | Long term (≥ 4 years) |

| Skill Shortages in Print and Converting Labor Limiting Scaling of Digital Carton Production | -0.40% | UK-wide, acute in Southeast England and Scotland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Pulp Prices Squeezing Converter Margins

Cartonboard prices stayed under downward pressure through early 2026, even as energy and transport costs climbed, reflecting soft demand and discount imports from Asia. Graphic Packaging’s FY 2025 results showed EBITDA margins slipping to 16.2% on weaker pricing and deliberate production curtailments. Unless converters secure long-term pulp contracts or integrate backward, margin squeeze risks delaying capex on digital presses and barrier-coating lines.

Competition From Flexible Plastic Pouches for Food Products

Flexible suppliers are not standing still; National Flexible’s 60%-recycled film for Premier Foods’ Paxo stuffing eliminates PVdC, sidesteps the Plastic Packaging Tax, and cuts virgin resin use by 37 tonnes per year. Such innovations reduce the cost difference between pouches and carton and preserve the barrier superiority of pouches for moisture-sensitive goods. Folding cartonmakers must therefore continue improving greaseproof coatings and lightweight structural designs to avoid losing ground in the snack and frozen segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Substrates Gain on Sustainability and Authenticity

Solid Bleached Sulfate captured 38.41% of the United Kingdom folding carton market in 2025, thanks to its high whiteness and pharmaceutical-grade purity, which meet stringent regulatory and branding requirements. Coated Unbleached Kraft is on track for a 6.80% CAGR to 2031 as organic and craft food brands embrace its natural brown hue and food-contact compliance. The United Kingdom folding carton market benefits from brands seeking visible sustainability cues, and kraft substrates deliver that message without secondary labeling. In addition, lighter grammages enabled by FiberLight Tec technology in grades such as Performa Nova trim material inputs while maintaining box compression strength.

Consumer willingness to pay for premium, eco-friendly packaging is fueling trials of unbleached liners in frozen meals and chocolate assortments, although printability trade-offs still favor SBS for intricate graphics. Recycled White Line Chipboard remains a price fighter in household goods, yet limited stiffness bars it from premium shelves. Overall, Kraft’s advance signals that visible fiber identity is now a marketing feature, not a defect, positioning unbleached grades to lift unit share within the UK folding carton market.

By Printing Technology: Digital Gains Share as Litho Holds Volume

Lithography retained a 46.21% share of the United Kingdom folding carton market in 2025, on the back of depreciated press fleets and unbeatable economics beyond 20,000 units. Yet digital platforms are projected to grow 9.02% annually through 2031 as converters chase on-demand production for e-commerce startups and subscription services. The UK folding carton market share for digital remains low today, but falling click costs and variable-data capabilities are closing the gap each quarter.

Converters now deploy hybrid workflows, running litho for base quantities and layering digital embellishment in post-press to localize campaigns. Bobst’s Novafold speed upgrade to 350 m/min ensures folder-gluer lines no longer throttle faster inkjet presses. Flexography continues to serve mid-range volumes where spot colors suffice, whereas gravure is receding to niche tobacco applications due to tooling cost inflation. Overall, digital’s ascent is less about flashy personalization and more about inventory risk reduction, a strategic advantage in volatile demand cycles.

By End-User Industry: E-Commerce Disrupts Food’s Dominance

Food and beverage remained the largest consumer, accounting for 42.15% demand in 2025, buoyed by stricter recyclability rules for frozen and chilled products. However, e-commerce and retail-ready formats are forecast to grow at a 9.45% CAGR, as parcel carriers prize letterbox-friendly, curbside-recyclable carton that reduce failed deliveries. This expansion will steadily increase the United Kingdom's folding carton market devoted to online fulfillment through 2031.

Pharmaceutical and healthcare applications exhibit defensive growth because aging demographics boost demand for tamper-evident, serialized carton. Personal care brands are leveraging premium board grades and tactile finishes to stand out in crowded digital storefronts, boosting average selling price per unit. Electronics, household supplies, and industrial spares remain smaller but stable niches, with electronics seeing incremental lifts from hard-molded plastic swap-outs driven by retailer take-back schemes. Collectively, shifting retail channels oblige converters to balance food safety credentials with the logistical realities of parcel networks.

Geography Analysis

England drives the bulk of the United Kingdom's folding carton market, reflecting its population density, concentration of FMCG headquarters, and the early rollout of Simpler Recycling, which segregates paper and card at the curbside. The GBP 1.1 billion (USD 1.4 billion) funding pool is channeling capex into new material recovery facilities that raise fiber purity and support local board mills. London’s brand ecosystem accelerates demand for digitally printed promotional carton, while logistics hubs in the Midlands anchor high-volume litho production.

Scotland’s converters face apprenticeship funding of only GBP 1,200-3,200 (USD 1,524-4,064) per trainee, markedly below English allowances, hampering talent pipelines for press technicians. Wales adopts the same EPR framework but deploys a distinct redistribution formula that can elongate reimbursement cycles for local authorities, creating cash-flow friction for smaller municipal recycling operators. Northern Ireland benefits from Saica Pack’s GBP 10 million (USD 12.7 million) warehouse in Hartlepool, boosting regional inventory buffers for quick-turn corrugated and folding carton deliveries.

Cross-border trade with the EU remains material; UK exporters must pre-empt the 2027 EU Packaging and Packaging Waste Regulation, which restricts space and bans certain single-use plastics, thereby nudging procurement toward recyclable cartonboard. Variations in devolved policy implementation continue to create compliance and cost asymmetries, but national brand owners are increasingly stipulating pan-UK specifications to streamline audits. Overall, geography-specific challenges from labor support in Scotland to collection quality in Wales shape localized investment priorities yet collectively reinforce the trajectory of the UK folding carton market toward fiber-based, readily recyclable formats.

Competitive Landscape

The top five suppliers account for only 35% of revenue, confirming a moderately fragmented structure that favors consolidation plays in the United Kingdom folding carton market. International Paper’s agreement to buy DS Smith for USD 7.54 billion signals renewed interest from global majors in European fiber assets, intensifying competitive benchmarking on EPR readiness and recycled-content verification. Grenadier Packaging’s December 2025 purchase of MM Packaging Leeuwarden gives it its first mainland-EU beachhead, illustrating the “string of pearls” model for mid-tier groups seeking cross-border scale.

Smurfit Westrock’s medium-term plan targets USD 7 billion in EBITDA by 2030, with below-mid-market board pricing, leveraging disciplined capacity management and AI-enabled design platforms such as ShelfSmart to capture value without volume chasing. Coveris is exiting labels and board to focus on flexibles, divesting its paper unit to Kingswood Capital and rebranding it Paragon Print and Packaging, a move that will sharpen its plastics focus while freeing the board unit to pursue dedicated capital budgets.

Technology strategy is emerging as the key differentiator. Bobst Connect and HP PrintOS give data-rich converters visibility into uptime and defect analytics, an edge when brand owners demand traceability and carbon accounting. Firms lacking digital workflows risk price erosion and disintermediation as e-commerce brands bypass traditional converters in favor of web-to-pack platforms. The United Kingdom folding carton market thus rewards players that couple scale purchasing of virgin and recycled fiber with agile, data-enabled converting capabilities, positioning them to pass EPR audits, deliver rapid personalization, and hedge raw-material volatility.

United Kingdom Folding Carton Industry Leaders

Smurfit Westrock plc

Graphic Packaging International, LLC

Mayr-Melnhof Karton AG

Mondi plc

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Henkel introduced Loctite Liofol CS 7106 RE, a certified recyclable cold-seal for barrier-coated paper targeting snack and confectionery packs.

- February 2026: Smurfit Westrock set medium-term targets of USD 7 billion EBITDA by 2030 and opened headroom for share buybacks from 2027.

- February 2026: HP and ePac agreed on a USD 50 million rollout of ten Indigo 200K presses across Europe and North America.

- January 2026: Stora Enso launched Performa Lumi GC1 folding boxboard produced on its BM6 line in Oulu, Finland.

United Kingdom Folding Carton Market Report Scope

The United Kingdom folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into carton for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The United Kingdom Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-Commerce and Retail-Ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-Commerce and Retail-Ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the United Kingdom folding carton market?

The United Kingdom folding carton market size stands at USD 2.15 billion in 2026 and is projected to reach USD 3.05 billion by 2031.

How fast is e-commerce packaging demand growing in the UK?

E-commerce and retail-ready folding carton are forecast to register a 9.45% CAGR between 2026-2031 as online retail volumes accelerate.

Which material grade is gaining the most market share?

Coated Unbleached Kraft is expected to expand its footprint fastest, advancing at a 6.80% CAGR thanks to its natural aesthetic and food-contact compliance.

Why are digital presses becoming important for carton converters?

Digital printing supports short runs, rapid artwork changes, and personalization, letting converters serve SKU proliferation while cutting plate costs and waste.

How will the Plastic Packaging Tax influence material choice?

The higher GBP 228.82 per tonne levy on plastic-heavy packs is steering brand owners toward mono-material cartonboard that sidesteps the tax and simplifies recycling.

What is driving consolidation among UK carton converters?

Rising compliance costs, the need for recycled-content verification, and capital requirements for digital and barrier-coating technology are pushing mid-tier firms to merge or be acquired.

Page last updated on: