Bahrain Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

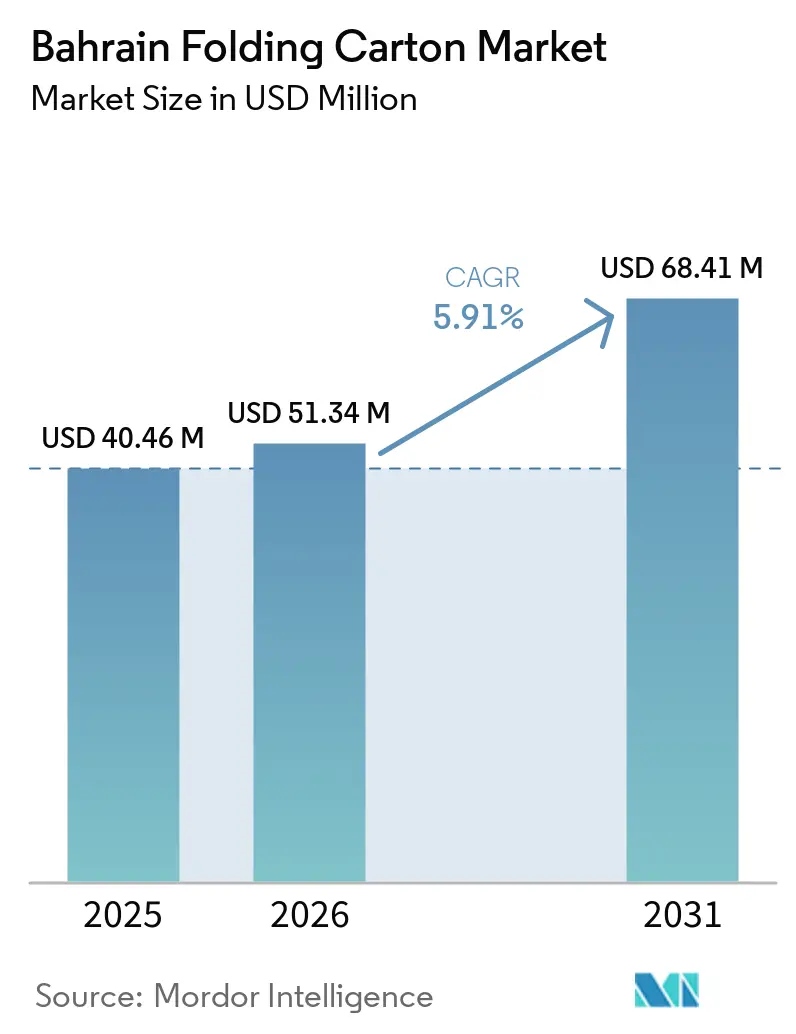

| Base Year Market Size (2025) | USD 40.46 Million |

| Market Size (2026) | USD 51.34 Million |

| Market Size (2031) | USD 68.41 Million |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

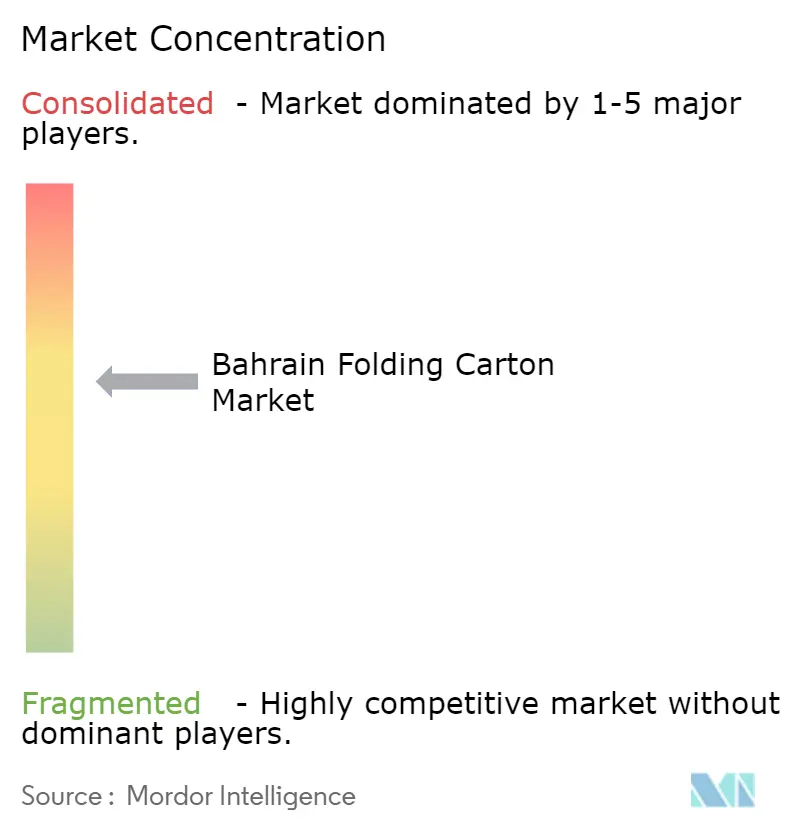

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Folding Carton Market Analysis by Mordor Intelligence

The Bahrain folding carton market size is expected to grow from USD 40.46 million in 2025 to USD 51.34 million in 2026 and is forecast to reach USD 68.41 million by 2031 at a 5.91% CAGR over 2026-2031. Demand accelerates as single-use plastics exit retail checkouts, e-commerce parcels travel farther, and ready-to-eat meals fill supermarket shelves. Converters that secure lightweight, food-safe substrates expand volume fastest because government sustainability mandates are strict and brand owners want cartons that advertise low carbon footprints. Imported pulp price spikes and shipping disruptions limit gross margins, yet automation and digital printing now shorten lead times, helping local plants offset cost volatility. The Bahrain folding carton market benefits from non-oil GDP growth, tourism-driven duty-free retail, and expanding premium cosmetics counters, even though its small absolute value constrains economies of scale.

Key Report Takeaways

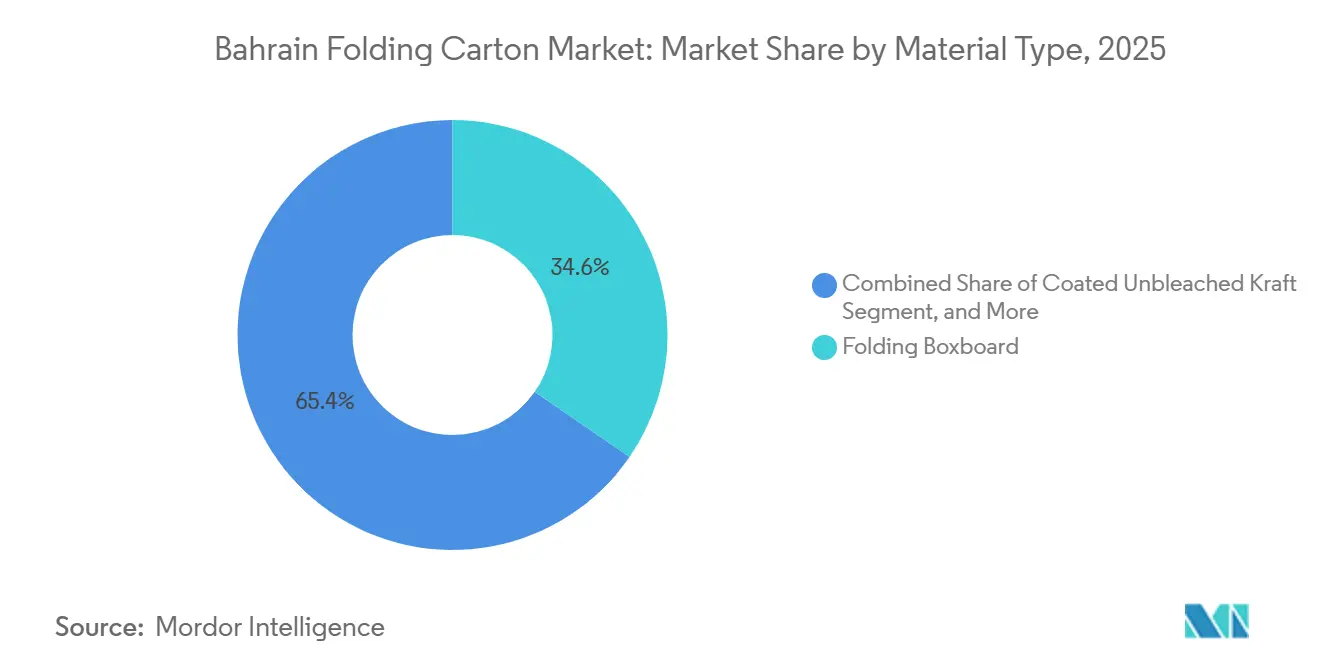

- By material type, folding boxboard captured with 34.61% of the Bahrain folding carton market share in 2025.

- By printing technology, the Bahrain folding carton market size for digital printing is projected to grow at a 7.84% CAGR to 2031.

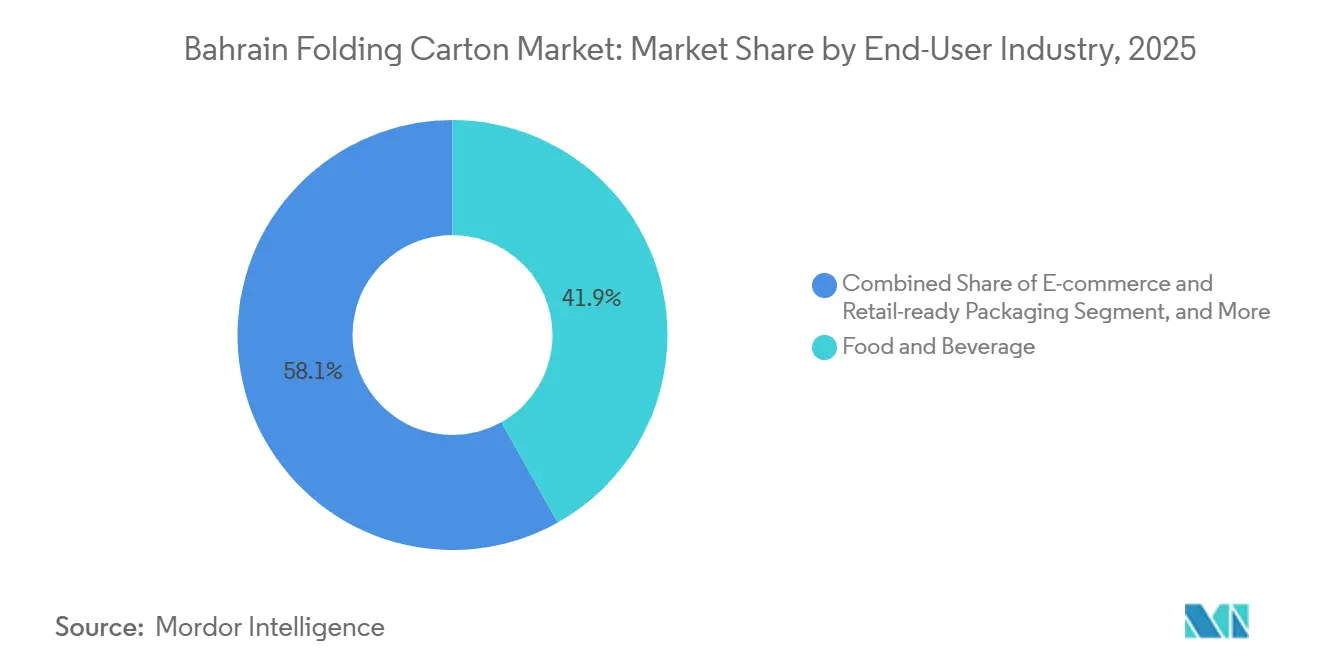

- By end-user industry, the food and beverage industry captured 41.86% of the Bahrain folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bahrain Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand from Bahrain's Booming E-Commerce Sector | +1.8% | National, Capital, and Muharraq Governorates | Medium term (2-4 years) |

| Growing Government Push for Eco-Friendly Packaging | +1.5% | National, aligned with GCC sustainability mandates | Short term (≤ 2 years) |

| Increasing Consumption of Packaged Ready-to-Eat Foods | +1.2% | National, urban households, and working professionals | Medium term (2-4 years) |

| Rise of Premium Personal Care Brands Requiring High-Quality Cartons | +0.9% | National spillover from GCC luxury retail expansion | Medium term (2-4 years) |

| Automation Investments Lowering Local Production Costs | +0.4% | National, larger converters, and joint ventures | Long term (≥ 4 years) |

| Tourism-Led Expansion of Duty-Free Retail Channels | +0.3% | National, Bahrain International Airport, and retail zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Bahrain's Booming E-Commerce Sector

Online revenue climbs rapidly as user penetration nears 40%. Beauty, fashion, and small electronics dominate digital baskets, each requiring fold-flat cartons that protect finishes and electronics during cross-border transit. Fulfillment centers prefer standardized, pre-creased styles because they accelerate pick-and-pack lines and reduce dunnage. Converters with partnerships to integrators in Dubai and Dammam win repeat volume because they can deliver mixed-SKU truckloads overnight. Variable-data printing further personalizes subscription boxes, a capability that differentiates domestic suppliers from lower-cost Asian imports.

Growing Government Push for Eco-Friendly Packaging

Ministerial Decision No. 7 of 2026 limits plastic-bag thickness to 57 microns, continuing a phased crackdown that already barred lighter gauges.[1]Medicircle Staff, “Ministerial Decision (7) of 2026 Prohibits Single-Use Plastic Bags,” medicircle.ae Policymakers also discuss banning plastic beverage bottles within two years, signaling wider substitution opportunities for paperboard. Brands facing compliance deadlines shift to cartons certified for chain custody, and retailers request ISO 14001 documentation in tenders. Early-moving converters that stock recyclable Folding Boxboard grades lock in multi-year supply agreements, while plants that are slow to qualify food-contact coatings risk losing shelf space.

Increasing Consumption of Packaged Ready-to-Eat Foods

Dual-income households seek microwaveable entrées and portion-controlled snacks, pushing supermarkets to list more chilled and frozen SKUs. These units need moisture-resistant boards that withstand cold chain conditions yet remain curbside recyclable. Yield-advantaged Folding Boxboard lowers cost per pack, and aqueous barriers replace fluorinated treatments. Urban convenience stores reorder weekly, so short batch runs with multiple flavor designs become common, a natural fit for digital presses that skip plate changes.

Rise of Premium Personal Care Brands Requiring High-Quality Cartons

International cosmetics labels such as e.l.f. Beauty enters Bahrain and insists on bright-white Solid Bleached Sulfate with foil accents. In omnichannel retail, secondary packaging doubles as a branding canvas, so converters invest in soft-touch and holographic coatings to elevate shelf appeal. Lot-code serialization combats parallel imports and counterfeit risks by integrating printed electronics or QR codes into closures. Luxury finishes command price premiums that partially offset higher SBS board costs, improving margins for plants with hybrid print lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Pulp and Paperboard Prices | -1.3% | National, exposure to GCC pricing indices | Short term (≤ 2 years) |

| Limited Domestic Recycling Infrastructure | -0.8% | National, affecting fiber recovery and circularity goals | Medium term (2-4 years) |

| Intensifying Competition from Flexible Packaging Formats | -0.5% | National, snack, and supplement categories | Medium term (2-4 years) |

| Small Market Size Deterring Large-Scale FDI | -0.3% | National, limiting economies of scale | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Pulp and Paperboard Prices

Geopolitical tensions near the Strait of Hormuz have driven container freight surcharges sharply higher, and spot kraft pulp trades well above historical averages. Bahrain’s converters, lacking domestic fiber, purchase on short contracts linked to PIX GCC indices, exposing them to monthly swings. Some buyers hedge with inventory buffers, yet that strains working capital in a market where finished goods turn over in excess of 8 weeks. Passing surcharges to brand owners risks losing bids to Saudi or Emirati converters with larger mills and internal board production.

Limited Domestic Recycling Infrastructure

Around 4,000 tonnes of municipal waste are sent to the Asker landfill daily, with negligible material recovery. Absent a commercial pulping line, carton offcuts and post-consumer boxes fail to re-enter the supply chain, and all recycled content arrives by sea. Start-ups propose shared baling hubs, but financing remains thin because recovered fiber volumes are modest relative to regional giants. Without local loops, Bahrain loses the carbon-saving narrative that multinationals increasingly demand, placing its folding carton sector at a strategic disadvantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Substrates Gain Share As Regulations Tighten

Folding Boxboard accounted for 34.61% of revenue in 2025, reinforcing its role as the baseline substrate for food, beverage, and household goods. The Bahrain folding carton market for this grade benefits from a high stiffness-to-weight ratio that lowers shipping costs while protecting retail displays. Converters lean on their multi-ply make-up, using reverse-side mechanical pulp to offset rising virgin-fiber prices. Environmental scorecards favor its lower carbon footprint, and lightweighting from 200 gsm toward 180 gsm frees up vessel capacity amid linerboard congestion.

Solid Bleached Sulfate, meanwhile, posts the fastest 7.17% CAGR through 2031 as premium cosmetics, pharmaceuticals, and gift confectionery flood duty-free zones. Its odor-free, bright-white finish enables six-color litho plus soft-touch varnish in one pass, a specification luxury brands consider non-negotiable. Though almost 20% costlier per tonne than Folding Boxboard, SBS cartons deliver higher unit margins because limited edition runs accept steeper pricing.[2]Brown Packaging, “Why SBS Is the Preferred Material for Folding Carton Packaging,” brownpackaging.com As a result, Solid Bleached Sulfate is expected to chip away at Folding Boxboard’s Bahrain folding carton market share, especially in small-format cartons that highlight brand storytelling.

By Printing Technology: Digital Adoption Accelerates for Short Runs and Personalization

Lithography accounted for 42.71% of output in 2025 because long-run confectionery sleeves, cereal boxes, and pharmaceutical leaflets still value tight registration and rapid multi-up die-cutting. High-speed six-color presses remain booked, and operators integrate inline cold foil to meet holiday-season peaks. For jobs under 10,000 sheets, however, setup time erases litho’s cost edge, so converters increasingly quote digital. The Bahrain folding carton market now sees digital printing rising by 7.84% per year, as subscription commerce and influencer drop launches drive demand for variable art.

Full-width inkjet lines print water-based inks directly onto pre-coated boards, eliminating the need for plates and reducing waste. Color-management suites let plants match Pantone libraries within Delta-E tolerances, keeping brand guardians satisfied. Although consumables remain expensive, digital earns premium pricing through speed-to-shelf. Hybrid presses that gang offset base layers with digital overlays emerge as a cost bridge, enabling printers to migrate gradually.

By End-User Industry: E-Commerce Reshapes Packaging Specifications

Food and beverage applications consumed 41.86% of volume in 2025, driven by the rapid turnover of frozen entrées, snack multipacks, and beverage carriers. Retailers emphasize tear-away shelf-ready trays that move straight from pallet to aisle, requiring high burst strength and double-wall corner posts. Moisture-resistant aqueous coatings ensure cartons survive chilled distribution yet remain repulpable. The e-commerce and retail-ready segment, though smaller, is growing fastest at a 7.42% CAGR.

Bahrain’s cross-border parcel lanes into Riyadh and Dubai expose boxes to long hauls, so tamper-evident closures and peel-away address labels become standard. Brands seek unboxing theatrics: interior print, personalized voucher inserts, and recycled crinkle paper. Converters offering digital twins for supply-chain tracking win bids from electronics and cosmetics sellers that must authenticate every shipment. As service expectations climb, folding cartons that double as return mailers gain share, reinforcing a shift from shrink-wrapped bundles to robust paperboard architecture.

Geography Analysis

The Capital Governorate accounts for the largest share of the Bahrain folding carton market, reflecting its dense retail corridors, financial centers, and airport duty-free storefronts. High disposable incomes and omnichannel shopping habits keep per-capita packaged-goods consumption above national averages. Muharraq and Northern Governorates follow, supported by industrial estates, seaport logistics, and growing residential complexes that stock neighborhood supermarkets.

Bahrain’s port proximity to Jebel Ali and King Abdulaziz allows overnight trucking, enabling converters to balance plant loads with work from neighboring states during slack periods. Yet the island economy remains exposed to regional chokepoints; when Red Sea diversions add ten transit days, Gulf importers pivot to Jeddah, increasing inland haulage charges that ripple into carton prices. Such cost escalations can significantly impact the competitiveness of local businesses.

Non-oil GDP is on track for 3.1% growth in 2026, buoyed by hospitality recoveries and infrastructure spending.[3]NBK Economic Research Department, “Economic Insight: Macroeconomic Outlook 2026-2027,” nbk.com Low single-digit inflation preserves household purchasing power, while bank liquidity programs encourage SMEs to finance machinery upgrades. Conversely, foreign reserves barely cover five weeks of imports, magnifying currency and freight risks. Businesses, therefore, favor local sourcing where feasible, a dynamic that anchors folding carton volumes despite small overall scale.

Competitive Landscape

Global majors such as Mondi, Huhtamaki, and Tetra Pak operate design hubs or sales offices, usually printing bulk volumes in Saudi Arabia or the United Arab Emirates and trucking finishing work into Bahrain. Regional independents Gulf Carton Factory, Arabian Packaging, and Obeikan Paper Industries compete on lead time, run-length flexibility, and after-sales support, keeping the Bahrain folding carton market moderately concentrated.

Joint ventures and strategic alliances illustrate the preferred growth path: Huhtamaki enlarged its stake in Arabian Paper Products Company to broaden coverage across the Middle East and North Africa, and Tetra Pak partnered with Union Paper Mills to build the region’s first carton-package recycling line.[4]Packaging MEA, “Tetra Pak and Union Paper Mills Launch UAE’s First Carton Package Recycling Line,” packagingmea.com Such moves marry brand trust with local agility, crucial in a jurisdiction where individual converters rarely exceed 30,000 tonnes annual capacity.

Investment priorities include robotic die-cutting to reduce setup hours, cloud-based prepress workflows for remote approvals, and expanded-color-gamut ink systems that cut spot-color plates. Firms highlighting ISO 14001 certification land multinational contracts ahead of rivals relying solely on price. Flexible pouch producers encroach in snacks and powdered supplements, yet Bahrain’s ongoing plastic bans and rising landfill fees tilt the competitive field toward paperboard.

Bahrain Folding Carton Industry Leaders

Easternpak Ltd.

Tetra Pak International SA

Gulf Carton Factory WLL

Bahrain Pack

Obeikan Paper Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bahrain’s Ministry of Industry, Commerce, and Tourism activated Ministerial Decision No. 7 of 2026 banning single-use plastic bags under 57 microns, granting retailers six months to exhaust inventory.

- January 2026: Gulf-based investors announced a new sustainable packaging business plan in Bahrain focusing on biopolymers and eco-friendly coatings for paperboard to address the growing demand for plastic-free takeaway containers.

- November 2025: e.l.f. Beauty rolled out across all 70 Sephora stores in the Gulf Cooperation Council, driving demand for high-finish Solid Bleached Sulfate cartons for premium cosmetics.

- August 2025: Tetra Pak and Union Paper Mills opened the United Arab Emirates’ first dedicated recycling line for carton packages, a USD 0.68 million investment processing 10,000 tonnes per year.

Bahrain Folding Carton Market Report Scope

The Bahrain Folding Carton Market report provides a comprehensive analysis of the market, focusing on the production and trade of folding cartons within Bahrain. The study examines key trends, growth drivers, challenges, and opportunities influencing the market. It also evaluates the competitive landscape, supply chain dynamics, and technological advancements shaping the industry.

The Bahrain Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Bahrain folding carton market size, and how fast is it growing?

The Bahrain folding carton market size stands at USD 51.34 million in 2026 and is forecast to reach USD 68.41 million by 2031 at a 5.91% CAGR.

Which material type leads volume in Bahraini folding cartons?

Folding Boxboard is the leading substrate, accounting for 34.61% of 2025 revenue because of its stiffness-to-weight efficiency and lower carbon footprint.

Why is digital printing gaining share among Bahraini converters?

E-commerce sellers require short runs and personalization, and digital presses eliminate plate costs and shorten setup, enabling converters to meet rapid fulfillment timelines.

How do government sustainability policies affect folding carton demand?

The 2026 ban on thin plastic bags and proposed bottle phase-outs shift retailers and brand owners toward recyclable paperboard, boosting carton volume across retail channels.

What challenges limit foreign direct investment in Bahrain’s carton sector?

Small absolute market value, imported pulp price volatility, and limited domestic recycling infrastructure reduce economies of scale and deter large-scale mill construction.

Which end-user industry will grow fastest through 2031?

E-commerce and retail-ready packaging is projected to expand at 7.42% CAGR as online shopping penetration increases and parcel specifications favor tamper-evident cartons.

Page last updated on: