Pakistan Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

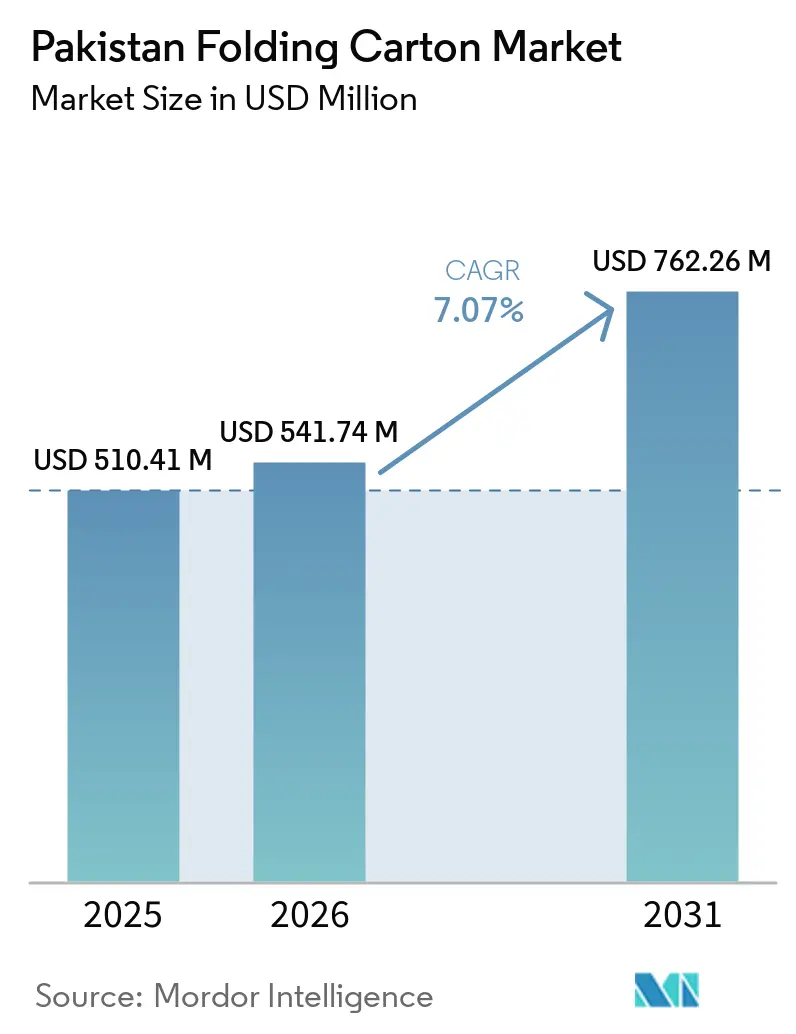

| Base Year Market Size (2025) | USD 510.41 Million |

| Market Size (2026) | USD 541.74 Million |

| Market Size (2031) | USD 762.26 Million |

| Growth Rate (2026 - 2031) | 7.07% CAGR |

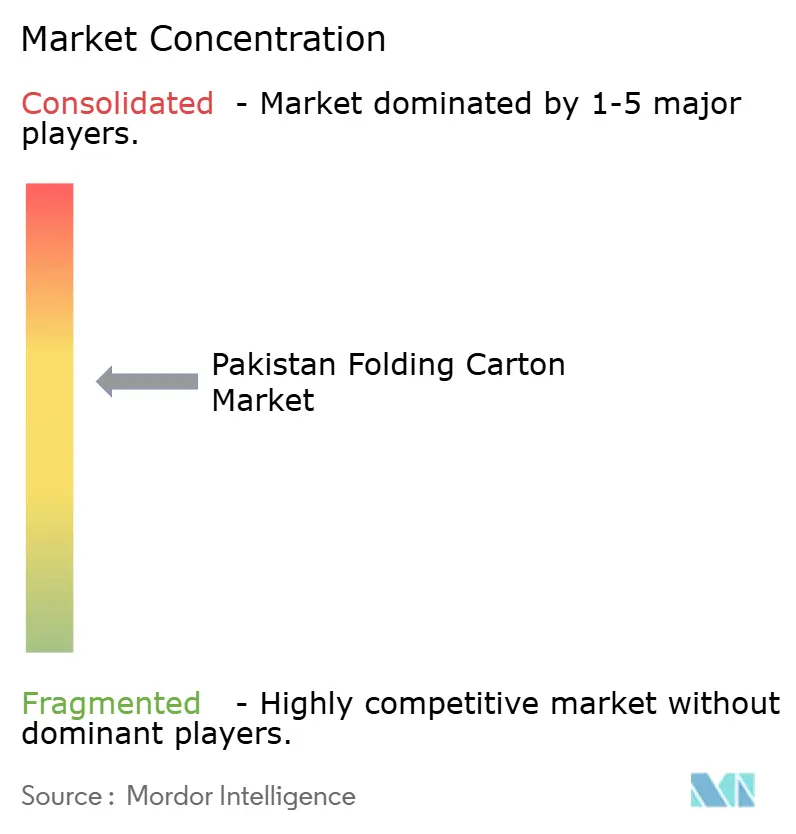

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Folding Carton Market Analysis by Mordor Intelligence

The Pakistan folding carton market size is projected to expand from USD 510.41 million in 2025 and USD 541.74 million in 2026 to USD 762.26 million by 2031, registering a CAGR of 7.07% between 2026 to 2031. Structural shifts in urban consumption, tariff incentives favoring local board mills, and a surge in pharmaceutical investments are boosting demand for higher-specification substrates and serialized cartons. Brand owners are specifying paper-based formats that are recyclable to meet retailer sustainability scorecards, while converters are widening grammage ranges to defend against flexible-packaging substitution. Imports of Solid Bleached Sulfate (SBS) remain significant, yet new capacity additions in Coated Unbleached Kraft (CUK) and Folding Boxboard (FBB) are narrowing the cost gap. Competitive intensity is rising as Packages Limited, Mondi, and Graphic Packaging build digital-printing capacity that supports short-run, variable-data jobs for e-commerce fulfillment.

Key Report Takeaways

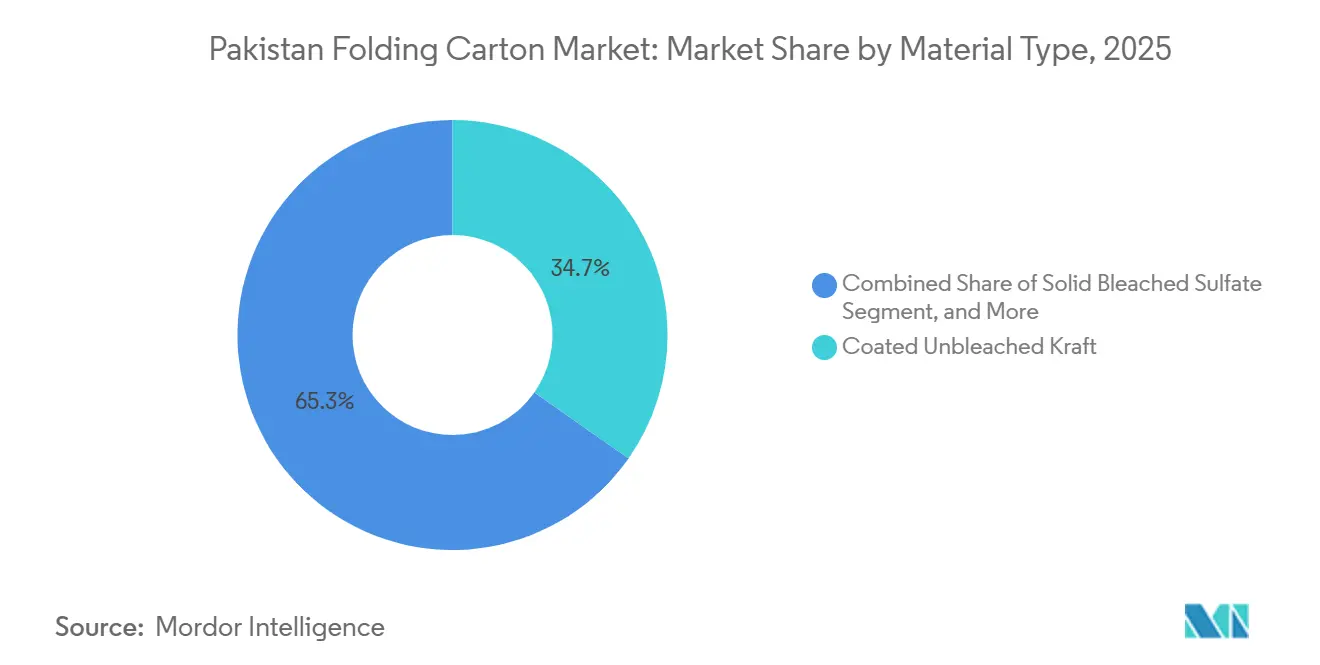

- By material type, coated unbleached kraft captured with 34.73% of the Pakistan folding carton market share in 2025.

- By printing technology, the Pakistan folding carton market size for digital printing is projected to grow at a 8.47% CAGR to 2031.

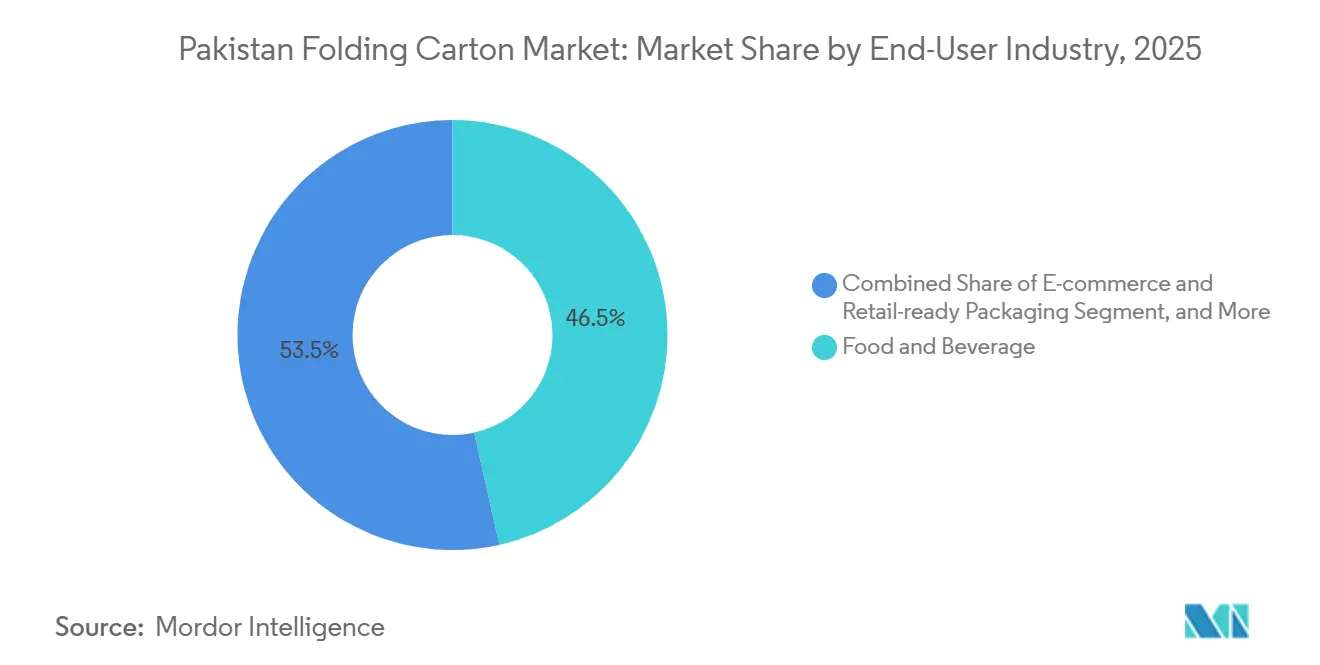

- By end-user industry, the food and beverage industry captured 46.52% of the Pakistan folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Pakistan Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urban Middle-Class Consumption of Packaged Goods | +1.2% | National, concentrated in Karachi, Lahore, Islamabad, and Faisalabad | Medium term (2-4 years) |

| Growth in Organized Retail Channels Including E-commerce Fulfillment | +1.5% | National, with early gains in Karachi, Lahore, and Rawalpindi | Short term (≤ 2 years) |

| Government Initiatives Promoting Import Substitution in Packaging | +0.9% | National | Medium term (2-4 years) |

| Rapid Expansion of Pharmaceutical Manufacturing Capacity | +1.3% | National, major hubs in Karachi, Lahore, and Peshawar | Short term (≤ 2 years) |

| Adoption of Digital Printing Enabling Short-Run Customization | +0.8% | National, led by Lahore and Karachi converters | Medium term (2-4 years) |

| Sustainability Push Favoring Recyclable Paper-Based Packaging | +0.7% | National, export-oriented converters aligning with EU and GCC standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Middle-Class Consumption of Packaged Goods

Rising disposable incomes in Karachi, Lahore, and Islamabad are nudging households toward branded snacks, ready-to-eat meals, and portion-controlled beverages. Pack sizes below 300 grams multiply SKU counts, so converters receive more frequent short-run orders that reward agile die-cutting and quick-set printing lines. PSQCA’s PS:383-2023 biscuit rule now prescribes barrier coatings and grease-proof layers that few legacy lines can achieve, steering contracts to plants with BRCGS or ISO 9001 certification. Frozen food volumes climbed 6% in 2025, and microwave-safe cartons with heat-seal films are now standard, lifting average selling prices and motivating mill upgrades to higher-brightness FBB grades.

Growth in Organized Retail Channels Including E-commerce Fulfillment

Hypermarkets such as Imtiaz and Metro demand shelf-ready trays that open quickly and present branding on every visible panel. Pakistan’s online retail value reached USD 14.11 billion in 2025 and is tracking toward USD 20.41 billion by 2029, intensifying needs for reinforced corners and scuff-resistant varnishes that withstand courier handling.[1]Statista, “Pakistan E-commerce Revenues,” statista.com Cash-on-delivery inspection extends the logistics chain, so converters are adding 350-400 gsm boards that resist collapse after multiple touchpoints. In 2025, the Tetra Pak and Bulleh Shah recycling alliance created domestic feedstock for recycled liners, reducing input costs and shortening lead times for e-commerce shippers.

Government Initiatives Promoting Import Substitution in Packaging

The National Industrial Policy 2025-30 eliminates additional customs duties on pulp and machinery, cutting landed costs by 3-5 percentage points and enabling board-mill debottlenecking. Cherat Packaging’s PKR 1.4 billion (USD 9.5 million) extrusion project qualifies for concessional financing, while Bulleh Shah’s 115,000 tpy corrugation line enjoys a 10-year tax holiday, illustrating how tariff reform is stimulating local capacity. Industry-status designation under review would unlock priority gas allocations, protecting mills from load-shedding episodes that lengthen production cycles.

Rapid Expansion of Pharmaceutical Manufacturing Capacity

Highnoon Laboratories, Haleon, Citi Pharma, and a Russian insulin venture collectively invested more than USD 150 million in new lines during 2025-2026, each mandating GS1 DataMatrix codes on secondary cartons. Converters have responded with single-pass digital presses equipped with vision cameras that verify barcodes at 200 cartons per minute, raising capital intensity but doubling value-added per square meter of board. Packages Limited’s PKR 1.40 billion equity infusion into StarchPack ensures ready access to pharmaceutical-grade modified starches, bundling ingredient and packaging solutions under one umbrella.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Pulp Prices and Foreign Exchange | -1.1% | National, acute for converters without long-term contracts | Short term (≤ 2 years) |

| Persistent Energy Shortages Increasing Operating Costs | -1.4% | National, most severe in the Punjab and Sindh industrial zones | Medium term (2-4 years) |

| Competition of Flexible Plastic Packaging Alternatives | -0.6% | National, concentrated in snack foods and confectionery | Medium term (2-4 years) |

| Limited Availability of Food-Grade SBS Board Domestically | -0.5% | National, export-oriented food and cosmetics converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Pulp Prices and Foreign Exchange

Pulp imports dominate the raw-material mix, so a PKR depreciation or a USD-denominated pulp spike quickly erodes margins. Kraft-paper benchmarks rose by PKR 3-4 per kg (USD 0.01-0.014 per kg) in 2024, a squeeze reflected in tender renegotiations and shortened quote validity periods. Smaller converters lacking forward cover exited high-spec niches, evidenced by Merit Packaging’s PKR 1 billion (USD 3.5 million) asset sale in 2025. Mills are countering by contracting with Scandinavian, North American, and Southeast Asian suppliers for staggered deliveries and expanding OCC recycling to dampen exposure to virgin fiber.

Persistent Energy Shortages Increasing Operating Costs

Average industrial tariffs hit 13.5 cents per kWh in 2025, almost double those in Vietnam and Indonesia, while load-shedding disrupted continuous-process lines during summer peaks. Packages Limited tapped a USD 25 million IFC loan to finance biomass boilers and rooftop solar that save 43,000 MWh annually, a template for large mills, but hard for mid-tier plants to replicate. Circular-debt overhangs point to sustained tariff pressure, compelling converters to factor energy-cost escalators into multi-year supply agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Substrate Momentum

Coated Unbleached Kraft retained 34.73% of the Pakistan folding carton market share in 2025 by supplying detergent, industrial goods, and export cartons that prioritize tensile strength over visual appeal. Solid Bleached Sulfate, although pricier, is forecast to pace the segment at an 8.13% CAGR as halal pharmaceuticals, premium cosmetics, and convenience foods migrate to bright-white, odor-neutral boards. Pakistan's folding carton market share gains for FBB are anchored in mid-tier cereals and personal-care SKUs that seek a cost-quality balance, while White Line Chipboard targets low-margin footwear and toy boxes.

Bulleh Shah’s liquid-packaging board remains the only domestic-grade replacement for imported SBS in aseptic beverage cartons.[2]The News, “Bulleh Shah Board Expansion,” thenews.com.pk FSC-certified SBS imports from Scandinavia still dominate baby-food and nutraceutical cartons, but tariff-free pulp under the 2025-30 policy is encouraging pilot trials of multi-ply SBS blends at Punjab mills. E-commerce growth is also elevating demand for higher-grammage FBB that survives courier chains, potentially trimming CUK’s lead unless refiners enhance fiber classification. End-users now evaluate carton suppliers on their compliance with PS:5474-2021 during migration testing, reinforcing the business case for ISO 22000 upgrades.

By Printing Technology: Digital Acceleration

Lithographic presses accounted for 51.53% of the Pakistan folding carton market share in 2025, buoyed by existing investments and their cost advantage for runs of 20,000 units or more. Pakistan's folding carton market size is growing in digital printing, at an 8.47% CAGR, driven by weekly SKU refreshes at hypermarkets and by serialization rules that only inkjet or electrophotography can economically satisfy. Hybrid lines from Nilpeter that combine digital CMYK printing with flexo varnish units enable converters to deliver personalized campaigns in 5 days rather than 3 weeks.

Offset houses face capex pressure as plates, chemicals, and make-ready waste inflate job costs at volumes below 10,000 impressions. Flexographic post-print is growing inside corrugated divisions but remains resolution-constrained for high-impact folding cartons. Gravure cylinders continue in tobacco and luxury cosmetics, yet plain-pack legislation clouds its outlook. Digital’s margin upside is bolstered by value-added features, such as scannable QR loyalty codes and embedded security inks, demanded by pharmaceutical clients.

By End-User Industry: E-commerce Upshift

Food and beverage converters supplied 46.52% of 2025 demand, riding protein-rich snack launches and fortified juice lines that require grease-proof coatings and peel-open closures. The Pakistan folding carton market, tied to e-commerce and retail-ready SKUs, is projected to grow fastest at an 8.66% CAGR, buoyed by online retail’s migration toward USD 20.41 billion in sales by 2029. Click-and-collect models prefer easy-open shelf-ready packs that double as last-mile shippers, pushing design-for-logistics into creative briefs.

Healthcare and pharmaceuticals will lift serialized carton volumes as insulin, oncology, and generics lines come onstream, while personal care brands chase unboxing theatrics with foil stamping on SBS substrates. Electrical and electronics makers are trialing molded-pulp inserts that complement drought-resilient carton exteriors. Tobacco’s volume erosion is steady but gradual, and household goods remain a price-play arena where CUK outcompetes plastics on sustainability messaging.

Geography Analysis

Karachi anchors the Pakistan folding carton market with port proximity that slashes containerized pulp freight and unlocks Asian export lanes. The city hosts Packages Limited, Bulleh Shah Packaging’s converting hub, and Merit Packaging’s offset complex, all serving multinational FMCGs clustered in the Korangi industrial area. Lahore and its Sheikhupura corridor represent the second pole, housing International Packaging Films Limited’s 152,660 tpy films complex and a dense network of mid-tier carton houses that supply Punjab’s textile and food processors.

Faisalabad adds industrial cartons for yarn exports, while Islamabad and Peshawar absorb rising pharmaceutical volumes as capacity relocates inland. International Packaging Films’ April 2024 BOPP and BOPET lines at Quaid-e-Azam Business Park illustrate the lure of such incentives.[3]Packaging MEA, “IPAK Film Lines,” packagingmea.com Karachi’s higher real-estate costs and security premiums are offset by deeper logistics networks and faster customs clearances, a trade-off that Punjab’s special economic zones counter with 10-year tax holidays and subsidized plots.

Export-oriented converters use Dubai-based subsidiaries such as Packages Trading FZCO to re-invoice GCC customers in USD, insulating margins from PKR swings and bypassing shipping bottlenecks during monsoon congestion. Domestic demand still drives 70-75% of consumption, but halal compliance, Arabic-label expertise, and ISO 14064 carbon disclosures are giving Karachi and Lahore converters an edge in winning GCC contracts. Central Asian markets remain exploratory due to currency inconvertibility, while African penetration is limited by shipping lead times and fragmented retail networks.

Competitive Landscape

Packages Limited and affiliates dominate the Pakistan folding carton market by combining integrated pulp, board, and converting assets with investments in coatings and digital printing. In 2025, stand-alone profits hit PKR 2.37 billion (USD 8.2 million). This profit facilitated a PKR 1.40 billion (USD 4.8 million) investment in StarchPack. Additionally, in April 2026, a deal was struck to acquire Akzo Nobel Pakistan for PKR 16.2 billion (USD 55 million), aimed at bolstering in-house barrier-coatings capabilities.[4]Process Worldwide, “Packages Group to Buy Akzo Nobel Pakistan,” process-worldwide.com Meanwhile, Mondi and Graphic Packaging, though smaller, emphasize technology and target premium cosmetics and pharma cartons that require holographic laminates.

International Packaging Films Limited’s 101,400 tpy BOPP and BOPET startup intensifies competition, tempting snack brands to switch to resealable stand-up pouches when shelf life trumps shelf presence. Cherat Packaging’s PKR 1.4 billion barrier-film extrusion line widens in-house laminate options, while Merit Packaging’s divestiture signals a squeeze on mid-tier players that lack economies of scope. Digital adoption is uneven: top five converters deploy SAP S/4HANA and AI-enabled maintenance analytics, yet 60% of regional plants still schedule jobs in spreadsheets, widening productivity disparities.

White-space opportunities revolve around domestic SBS production, GS1 serialization services, and mono-material recyclable cartons that comply with EU circularity rules effective 2028. Bulleh Shah’s biomass boilers and IFC-funded upgrades showcase the payback of energy self-generation, but upstream pulp integration remains elusive. Consolidation is likely as tariff incentives favor scale and traceability mandates raise capex thresholds.

Pakistan Folding Carton Industry Leaders

Century Paper & Board Mills Limited

Tetra Pak Pakistan Limited

Mandiali Paper Mills (Pvt) Ltd

Roshan Packages Limited

Liberty Packaging Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Packages Group, via IGI Investments, agreed to acquire Akzo Nobel Pakistan for PKR 16.2 billion (USD 55 million), with closing expected in H2 2026, targeting coatings for premium folding cartons.

- April 2026: Punjab’s school-meal program adopted recyclable cartons, signaling public-sector appetite for fiber-based packaging.

- January 2026: Highnoon Laboratories commissioned a new pharma facility, escalating demand for serialized cartons.

- August 2025: Tetra Pak Pakistan and Bulleh Shah Packaging signed an MoU to build a nationwide beverage-carton recycling chain.

Pakistan Folding Carton Market Report Scope

The scope of the report covers the analysis of the folding carton market in Pakistan, focusing on its current trends, growth drivers, challenges, and opportunities. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton market in Pakistan.

The Pakistan Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Pakistan folding carton market size?

The Pakistan folding carton market size stands at USD 541.74 million in 2026 and is projected to reach USD 762.26 million by 2031, according to Mordor Intelligence.

Which material type leads demand?

Coated Unbleached Kraft led with 34.73% of Pakistan folding carton market share in 2025 and remains the baseline substrate for detergent, industrial, and export cartons.

How fast is digital printing growing in this market?

Digital printing is forecast to increase at an 8.47% CAGR between 2026-2031 as brand owners demand short runs and variable data.

What factors are driving pharmaceutical carton growth?

Capacity additions by Highnoon Laboratories, Haleon, and Citi Pharma and DRAP’s GS1 serialization mandates are fueling higher-specification pharmaceutical cartons.

How are energy costs impacting converters?

Industrial tariffs averaging 13.5 cents per kWh in 2025 and frequent load-shedding have intensified investment in biomass and solar self-generation among large mills.

Which region in Pakistan offers the strongest growth prospects?

Punjab’s Sheikhupura corridor is attracting new capacity through special economic-zone incentives, yet Karachi maintains a logistics edge due to its seaports.

Page last updated on: