GCC Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.21 Billion |

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

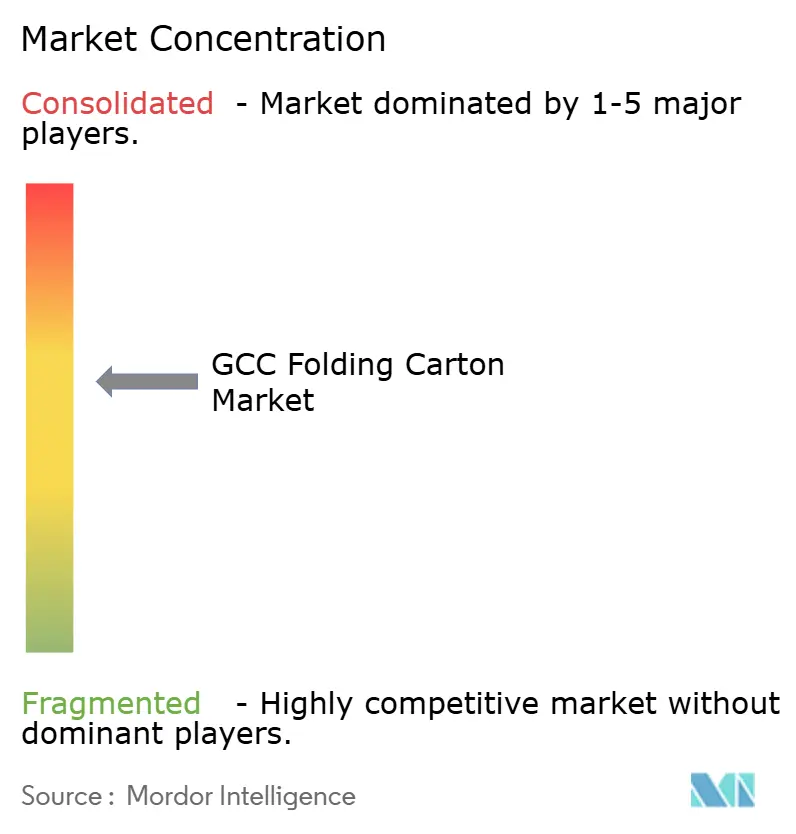

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Folding Carton Market Analysis by Mordor Intelligence

The GCC folding carton market size is expected to increase from USD 2.21 billion in 2025 to USD 2.32 billion in 2026 and reach USD 2.92 billion by 2031, growing at a CAGR of 4.73% over 2026-2031. The uplift comes from government localization mandates that anchor packaging production inside the Gulf, sustained demand from food and beverage processors, and a sharp pivot toward sustainable fiber solutions that comply with evolving Extended Producer Responsibility (EPR) schemes. Digital printing is lowering the economic threshold for short runs, enabling brand owners to personalize stock-keeping units and accelerate time-to-market. Luxury tourism projects such as NEOM and Expo City continue to specify premium metallic finishes, expanding average revenue per carton. Import-linked pulp cost risk and substitution by flexible pouches temper headline growth but do not derail the steady expansion trajectory of the GCC folding carton market.

Key Report Takeaways

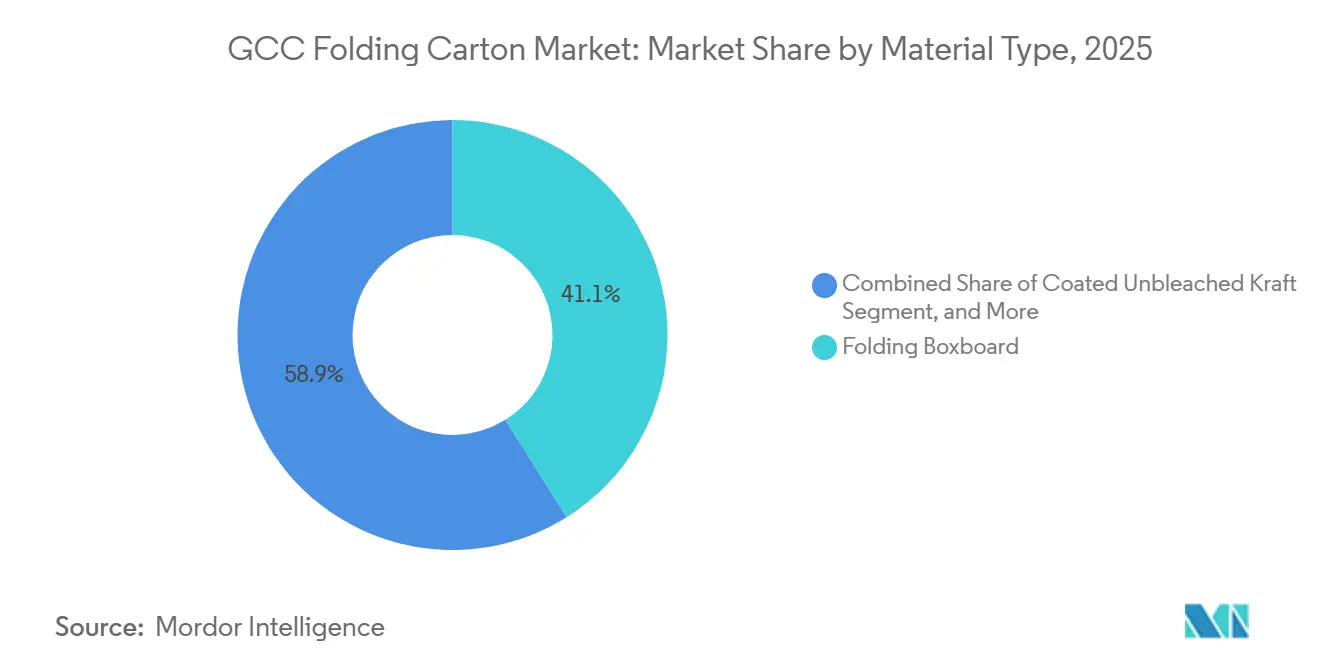

- By material type, folding boxboard captured with 41.09% of the GCC folding carton market share in 2025.

- By printing technology, the GCC folding carton market size for lithographic printing is projected to grow at a 5.71% CAGR to 2031.

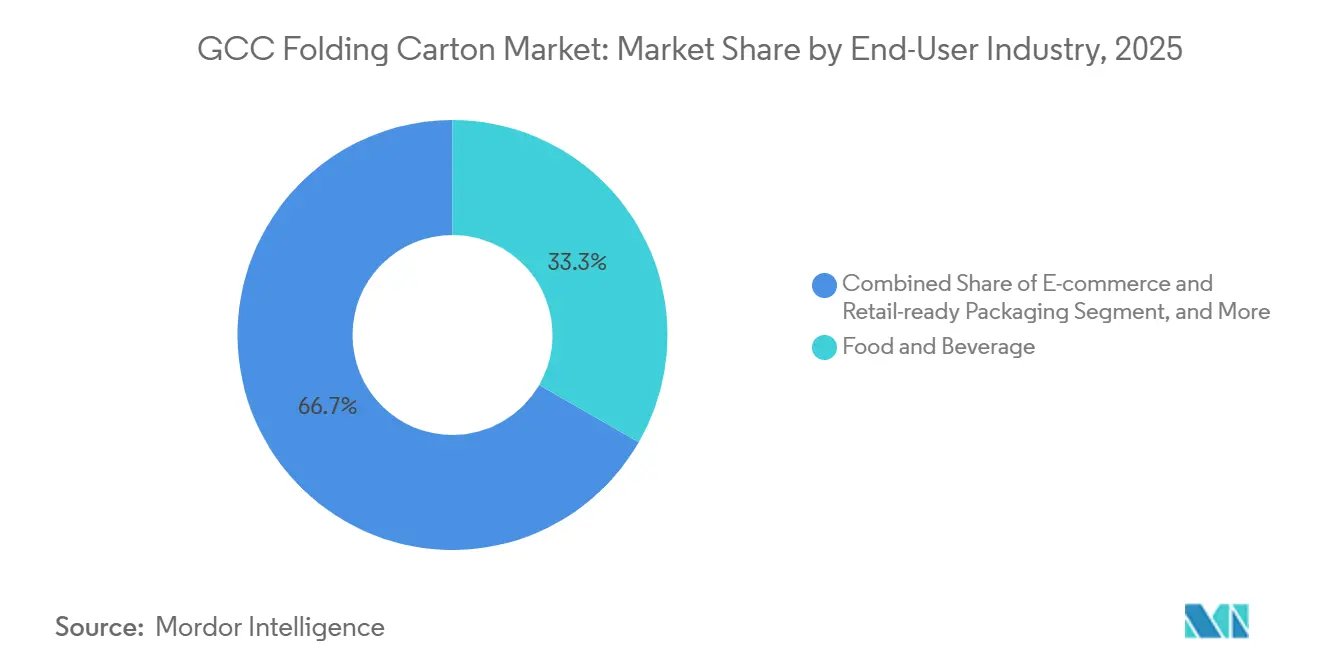

- By end-user industry, the food and beverage industry captured 33.32% of the GCC folding carton market share in 2025.

- By geography, the GCC folding carton market size for United Arab Emirates is projected to grow at a 5.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Sustainable-Fiber Mandates | +1.2% | Saudi Arabia, UAE (EPR pilots); spillover to Qatar, Oman | Medium term (2-4 years) |

| Packaged Food and Beverage Boom | +1% | GCC-wide, concentrated in Saudi Arabia, UAE urban corridors | Short term (≤ 2 years) |

| E-Commerce Demand for Lightweight Branded Boxes | +0.9% | UAE (Dubai, Abu Dhabi logistics hubs); Saudi Arabia (Riyadh, Jeddah) | Short term (≤ 2 years) |

| Digital Printing Enabling SKU Personalization | +0.7% | Saudi Arabia, UAE; early adoption in Qatar luxury retail | Medium term (2-4 years) |

| Localization Incentives Under GCC Industrial Visions | +0.6% | Saudi Arabia (Vision 2030), UAE (Operation 300bn), Oman (Tanfeedh) | Long term (≥ 4 years) |

| Premium Carton Uptake in Giga-Projects | +0.4% | Saudi Arabia (NEOM, Qiddiya, Red Sea Project); UAE (Expo City legacy) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Sustainable-Fiber Mandates

EPR pilots launched in July 2025 in the United Arab Emirates compel brand owners to finance collection and sorting, pushing converters toward recycled kraft substrates. Saudi Arabia’s National Waste Management Strategy requires 85% landfill diversion by 2035, further favoring fiber over non-recyclable plastics.[1]Saudi Ministry of Environment, Water and Agriculture, “National Waste Management Strategy,” mewa.gov.sa Compliance with GSO 1943/2016 and 2528/2016 obliges bilingual labeling and minimum recycled content, creating a pull effect for certified board grades. Large converters such as Hotpack are reallocating capital toward fiber assets to capture the opportunity.[2]Arab News, “Nestlé Signs Jeddah Plant Deal,” arabnews.com Together, these measures lift demand and add 1.2 percentage points to the forecast CAGR of the GCC folding carton market.

Packaged Food and Beverage Boom

Fast urbanization and female workforce participation have increased shelf-stable grocery sales; United Arab Emirates FMCG turnover grew 6.8% in 2024.[3]Gulf News, “UAE FMCG Sales Up 6.8%,” gulfnews.com Vision 2030 food-security programs attract multinational manufacturers, exemplified by Nestlé’s planned plant in Jeddah. Folding cartons remain the secondary pack of choice for cereals and snacks because they deliver stacking strength, printability, and tamper evidence in a single component. Although flexible stand-up pouches nibble at dry snack formats, regulatory recycling costs narrow the price gap, keeping cartons relevant. The confluence of volume growth and packaging localization adds 1.0 percentage point to the GCC folding carton market’s CAGR.

E-Commerce Demand for Lightweight Branded Boxes

Online penetration reached 14% of retail sales in the United Arab Emirates in 2025. Same-day fulfillment models rely on lightweight, stackable cartons that survive multi-touch distribution while doubling as marketing billboards. Digital printing allows individualized artwork so brands can ship in consumer-ready packs without outer corrugated shippers. Riyadh and Jeddah see parallel growth as logistics corridors mature under Vision 2030. These factors deliver a 0.9 percentage-point boost to the market’s CAGR.

Digital Printing Enabling SKU Personalization

Saudi Arabia’s paid print revenues are on track to hit USD 767 million by 2032 as converters install HP Indigo and Canon platforms. Hybrid workflows unveiled at Gulf Print and Pack 2026 combine digital for variable data with flexography for solid colors, balancing cost and flexibility. Personal care, cosmetics, and subscription food boxes gain most because regional flavor variants and influencer tie-ins need nimble artwork updates. While per-unit ink costs remain higher than offset, the ability to eliminate plates shortens lead time and lowers inventory risk, contributing 0.7 percentage point to CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| mport-Linked Pulp Price Volatility | -0.8% | GCC-wide; acute in Saudi Arabia, UAE due to import dependency | Short term (≤ 2 years) |

| Substitution by Flexible Pouches and Rigid Plastics | -0.6% | Saudi Arabia, UAE (dry foods, beverages); limited in pharma/cosmetics | Medium term (2-4 years) |

| Water-Scarcity Regulations on Regional Paper Mills | -0.3% | Saudi Arabia, UAE (industrial water-use permits); less severe in Oman | Long term (≥ 4 years) |

| Shortage of Skilled High-Colour Carton Converters | -0.2% | UAE, Qatar (luxury retail); emerging in Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import-Linked Pulp Price Volatility

Gulf converters import nearly all virgin kraft pulp, exposing them to Red Sea freight surcharges and spot-market swings; Fastmarkets PIX showed a 3-5% drop in testliner prices between December 2025 and January 2026. World Bank forecasts hint at a broader 7% commodity decline, yet pulp follows its own cycle driven by Scandinavian maintenance shutdowns. Margin compression limits funds available for digital presses and automated finishing lines. Recent backward integration, such as Star Paper Mill’s 135,000-tonne KEZAD facility, offers only partial relief because recycled fiber cannot meet brightness specs for premium folding box board. The drag translates into a -0.8 percentage-point impact on the GCC folding carton market CAGR.

Substitution by Flexible Pouches and Rigid Plastics

Polyethylene and polypropylene pouches deliver excellent barrier properties with lower material weight, enticing brand owners in dry food and powdered beverage lines. The cost advantage endures until EPR fees on non-recyclable plastics come fully into force, narrowing but not erasing the delta. Cartons retain an edge in pharmaceuticals and cosmetics, where tamper evidence and bilingual labeling are regulatory must-haves. Nevertheless, flexible packaging captures enough incremental share to shave 0.6 percentage point off the market’s CAGR projection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Kraft Board Gains Regulatory Tailwinds

Recycled kraft board is projected to grow at a 5.66% CAGR through 2031, benefiting from landfill-diversion mandates in Saudi Arabia and the United Arab Emirates that price virgin fiber at a regulatory premium. Folding box board led with 41.09% share in 2025 because it offers an optimal stiffness-to-cost ratio for high-volume food and beverage applications. Virgin kraft retains niche demand in export-oriented pharmaceuticals, where European customers stipulate contamination-free substrates.

Ongoing investment in brightness enhancement and de-inking technologies by regional mills such as MEPCO’s SAR 1.8 billion (USD 480 million) PM5 line aims to narrow the quality gap with European suppliers. However, water scarcity regulations require closed-loop cooling, inflating capital costs for new recycled mills. Converters weigh these expenses against the reputational upside of local sourcing, especially under Vision 2030 localization quotas. Overall, recycled kraft’s ascent diversifies supply and underpins the sustainability narrative of the GCC folding carton market.

By Printing Technology: Digital Disrupts Offset’s Volume Dominance

Offset lithography commanded 49.56% of 2025 volume on the back of long, repetitive food and beverage runs that amortize plate costs. Yet digital printing’s 5.71% CAGR reflects brand owners’ preference for agile SKU rollouts and variable data printing. Hybrid workflows demonstrated at Gulf Print and Pack 2026 combine the speed of flexography for flood colors with digital heads for serial numbers and personalization. Although per-sheet costs remain higher, the zero-setup model eliminates plate waste and minimizes obsolescence when campaigns change quickly.

Flexography retains territory in corrugated post-print and low-complexity cartons because of its higher throughput, while gravure and screen hold tiny but profitable niches in duty-free cosmetics where metallic inks and tactile varnishes rule. The continued shift toward digital compresses lead times from weeks to days, reshaping converter service models in the GCC folding carton market.

By End-User Industry: Personal Care Outpaces the Food Volume Base

Personal care and cosmetics are forecast to grow at 6.09% CAGR between 2026-2031. Demand stems from premiumization trends and regional sustainability commitments such as L’Oréal’s 2030 packaging roadmap. GSO labeling and tamper-evidence mandates align naturally with carton formats, making them cost-efficient for compliance. Food retained 33.32% of the GCC folding carton market share in 2025, supported by steady cereal and snack volumes, but its growth is slower due to the uptake of flexible pouches. Pharmaceuticals register stable mid-single-digit growth as blister packs and vials require secondary cartons to meet ISO 22716 good manufacturing practice standards.

Consumer surveys show 70% of Gulf shoppers prefer eco-friendly packaging, bolstering recycled-content cartons for beauty SKUs. E-commerce unboxing rituals further amplify the role of decorative finishes. In contrast, tobacco volumes decline under plain packaging rules, and electronics default to corrugated shippers, limiting carton penetration. As a result, the personal-care vertical delivers the greatest incremental value to the GCC folding carton market over the forecast horizon.

Geography Analysis

Saudi Arabia held 44.21% of regional volume in 2025. Local-content mandates, giga-project procurement, and a 35 million consumer base underpin demand, while United Carton Industries Company’s IPO-funded expansion cements domestic capacity. MEPCO’s PM5 doubled testliner output to 450,000 tonnes annually in April 2025, improving feedstock availability for local converters.[4]Gulf Industry Online, “MEPCO to showcase sustainability leadership,” gulfindustryonline.com Yet growth moderates relative to smaller Gulf peers because e-commerce adoption outside main cities remains nascent and substitution by flexible packages is more pronounced.

The United Arab Emirates is projected to outpace the Kingdom with a 5.89% CAGR, driven by free-zone incentives and the July 2025 EPR pilot, which lowers total lifecycle costs for recyclable fiber. Star Paper Mill’s 135,000-tonne recycled kraft facility at KEZAD has already trimmed import dependency, while Operation 300bn funnels industrial financing toward local converting lines. E-commerce penetration, now 14% of retail sales, accelerates demand for lightweight, digitally printed cartons in the Dubai-Abu Dhabi corridor.

Qatar, Kuwait, Oman, and Bahrain collectively supply the remaining volume. Qatar benefits from World Cup legacy retail, Kuwait rebounds as mall footfall returns, Oman’s Tanfeedh diversifies into agrifood processing, and Bahrain leverages proximity to Saudi Arabia’s Eastern Province for cross-border sales. These markets are smaller and logistically costlier, but GCC Customs Union rules permit Saudi and Emirati converters to serve them efficiently, reducing incentives for standalone greenfield plants. Consequently, the twin growth engines of Riyadh-Jeddah and Dubai-Abu Dhabi dictate the broader trajectory of the GCC folding carton market.

Competitive Landscape

United Carton Industries Company, Obeikan, and Napco together account for roughly half of the installed folding-carton capacity, giving the GCC folding carton market a moderate concentration profile. Star Paper Mill’s backward integration into recycled kraft, coupled with Al Jawdah Paper’s 250-tonne-per-day Saudi line, secures domestic fiber supply and hedges pulp volatility.

Technology investment is the main differentiation lever: Gulf Carton Factory has installed BW Papersystems flexographic presses and robotics in die-cutting to slash lead times, while smaller converters adopt HP Indigo machines to chase short-run personal-care jobs. Napco’s August 2025 purchase of Arabian Flexible Packaging adds horizontal breadth, permitting bundled rigid-and-flexible bids that appeal to multinational procurement teams.

Ethical sourcing is emerging as a new filter; Gulf Carton Factory’s Sedex certification unlocks European and North American contracts that demand visibility into labor practices. Still, fragmentation persists in pharmaceuticals, tobacco, and luxury cosmetics, where specialized coatings and regulatory hoops create sticky switching costs. The competitive intensity drives continuous upgrades in inline coating, hybrid presses, and digital workflow automation across the GCC folding carton market.

GCC Folding Carton Industry Leaders

Gulf Carton Factory Co.

NASR Packaging & Printing Co.

Obeikan Folding Carton Company L.L.C.

Al Kifah Paper Products Company

United Carton Industries Company (UCI)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Obeikan Folding Carton Company partnered with Tetra Pak to supply FSC-certified board for beverage packs, securing 15,000 tonnes per year through 2028.

- August 2026: Napco National Packaging Company acquired Arabian Flexible Packaging, creating a single-source rigid and flexible offering with USD 20 million cross-selling upside by 2027.

- July 2025: The United Arab Emirates launched a pilot EPR scheme that assigns the lowest fee tier to folding cartons, spurring substitution of rigid plastics.

- June 2025: Al Jawdah Paper began producing 250 tonnes per day of recycled kraft in Saudi Arabia, cutting freshwater usage 60% via closed-loop systems.

GCC Folding Carton Market Report Scope

The scope of the report covers the analysis of the folding carton packaging market, focusing on its current trends, growth drivers, challenges, and opportunities. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton packaging market.

The GCC Folding Carton Packaging Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the projected value of the GCC folding carton market in 2031?

The market is forecast to reach USD 2.92 billion by 2031.

Which end-user segment is expected to grow fastest through 2031?

Personal care and cosmetics lead with a projected 6.09% CAGR during 2026-2031.

Why is recycled kraft board gaining traction in the Gulf?

EPR schemes and landfill-diversion mandates assign lower fees to recycled fiber, making recycled kraft the preferred substrate for many brand owners.

How is digital printing changing the competitive landscape?

Digital presses eliminate plate costs, enabling short-run SKU personalization and faster lead times, especially for premium and e-commerce-focused brands.

Which country will post the highest growth rate in the region?

The United Arab Emirates is projected to register a 5.89% CAGR, outpacing other GCC members due to free-zone incentives and robust e-commerce adoption.

What are the main risks to market growth?

Import-linked pulp price volatility and substitution by flexible pouches are the most significant restraints, together trimming the forecast CAGR by 1.4 percentage points.

Page last updated on: