Russia Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.48 Billion |

| Market Size (2026) | USD 3.57 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 1.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Containerboard Market Analysis by Mordor Intelligence

The Russia containerboard market size is projected to expand from USD 3.48 billion in 2025 and USD 3.57 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 1.63% between 2026 to 2031. This pace points to a market that remains structurally stable, but it is operating under pressure from tighter domestic financial conditions and a growing supply overhang from recent greenfield investments. Russia’s paper and cardboard output reached 10,658 thousand tons in 2024, up 5.4% from the prior year, and that increase outpaced downstream demand absorption, adding to pricing pressure in 2025. Domestic corrugated packaging consumption declined 0.7% in 2025, its first annual drop in a decade, as high Central Bank key rates, slower food manufacturing activity, and softer household spending affected several end-use sectors. Large integrated producers are responding with scale, fiber self-sufficiency, and export channel development, while smaller mills and converters are dealing with tighter margins as recycled-fiber costs rose faster than selling prices. Over the forecast period, the main opportunities in the Russia containerboard market will center on deeper integration, selective capacity rationalization, and packaging demand tied to localization, recycling compliance, and eastbound trade expansion.

Key Report Takeaways

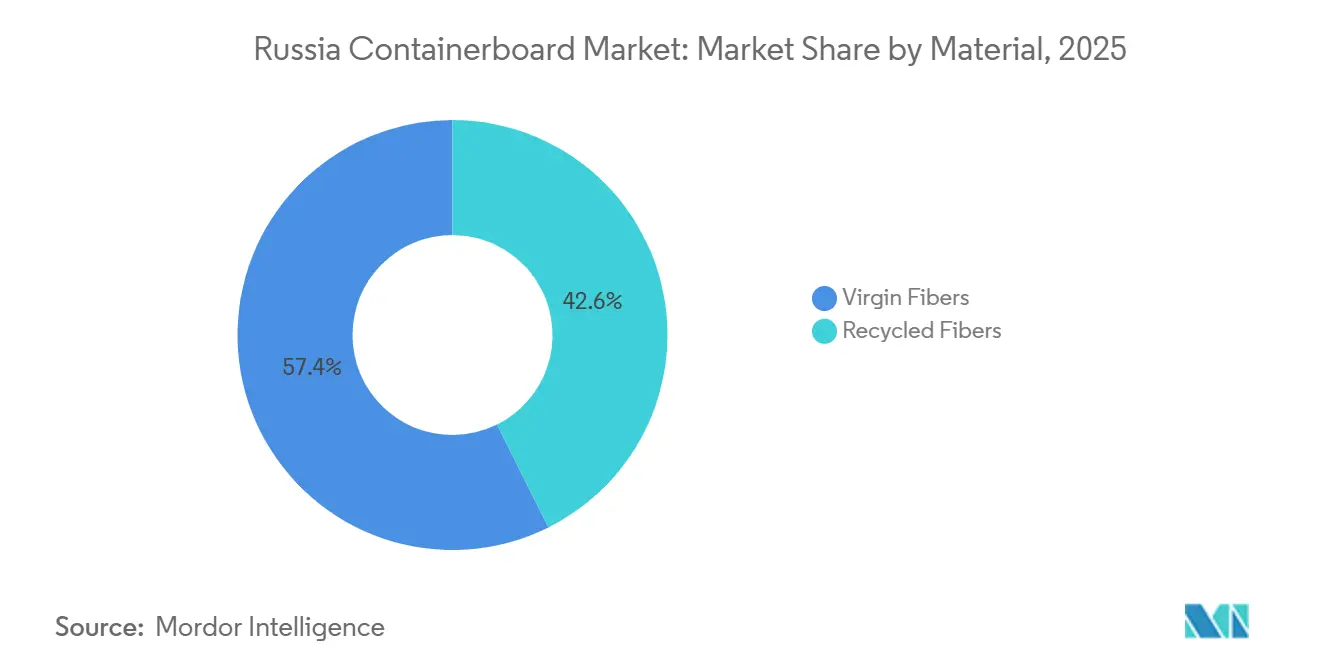

- By material, virgin fibers captured 57.36% of the Russia containerboard market share in 2025.

- By product type, the Russia containerboard market size for the testliners segment is forecast to advance at a 1.88% CAGR through 2031.

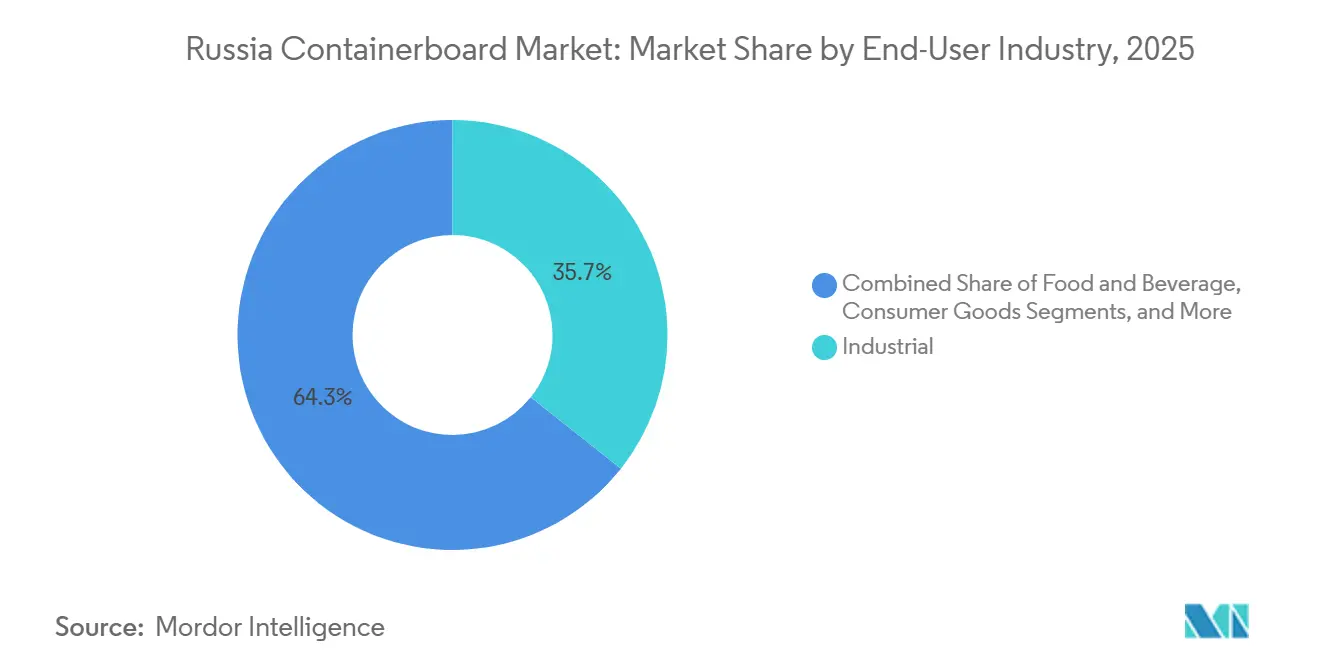

- By end-user industry, industrial applications captured 35.68% of the Russia containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food And Beverage Packaging Resilience | +0.4% | National, with concentration in Central and Volga Federal Districts | Medium term (2-4 years) |

| E-commerce Cartonization Demand | +0.4% | National, with early gains in Moscow, St. Petersburg, Krasnodar, Yekaterinburg | Short term (≤ 2 years) |

| Domestic Virgin Kraftliner Capacity Ramp-Up | +0.2% | Siberian and Northwestern Federal Districts, with spill-over to CIS and APAC export corridors | Medium term (2-4 years) |

| Import Substitution In Consumer And Industrial Goods | +0.2% | National, with early localization gains in Central and Volga Federal Districts | Medium term (2-4 years) |

| Extended Producer Responsibility Tailwinds For Fiber Packaging | +0.1% | National, concentrated in regions with EPR recycling infrastructure | Long term (≥ 4 years) |

| Eastbound Export Corridor Packaging Demand | +0.1% | Siberian Federal District, Far Eastern Federal District, with spill-over to ASEAN corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food And Beverage Packaging Resilience

The Russia containerboard market maintains a durable demand base in food and beverage packaging, even as broader economic activity weakens. The food sector accounted for up to 60% of corrugated packaging in Russia, and that share remained stable during the 2025 contraction cycle.[1]“Analysis Of The Cardboard And Corrugated Packaging Market In Russia, 2024-2025 And Key Trends,” RosUpack, rosupack.com Demand inside this segment kept shifting toward secondary and tertiary formats as major retailers expanded private-label programs and needed more transport-ready packaging. X5 and Magnit set internal targets to increase private-label packaging to 50%- 100% of materials using recyclable or compostable materials during 2025-2026, which improved the position of fiber-based board with established recyclability credentials.[2]Margarita Parfenenkova, “Rules Of Extended Producer Responsibility Are Reforming The Retail Market,” Vedomosti, vedomosti.ru This change mattered because it protected a large portion of packaging demand from weaker spending in non-food retail. As a result, food-linked consumption continued to anchor baseline mill utilization and helped the Russia containerboard market remain steadier than several adjacent packaging categories.

E-commerce Cartonization Demand

The Russia containerboard market is also being supported by faster carton turnover in online retail and parcel delivery. E-commerce packaging moves through the system quickly, so demand for new boxes and supply of recovered fiber both react faster than in traditional store-led retail channels. This short use cycle keeps board demand visible even when broader consumption slows, because parcel fulfillment still requires transport packaging for each order. Marketplace networks are spreading into Tier 2 and Tier 3 cities, widening corrugated packaging use in areas that historically relied more on bulk plastic substitutes. GOFRO projected online trade volumes to rise by 60% over the three years following 2025, suggesting a durable packaging tailwind across the forecast period. That regional diffusion is enlarging the addressable demand pool for domestic converters and keeps the Russia containerboard market closely linked to logistics network expansion.

Domestic Virgin Kraftliner Capacity Ramp-Up

The most important supply-side change in the Russia containerboard market has been Ilim Group’s Ust-Ilimsk pulp and cardboard complex. The project involved RUB 100 billion (USD 1.1 billion) in investment and added 600,000 tons per year of virgin kraftliner capacity.[3]“Tskk In Ust-Ilimsk Will Reach Design Capacity In 2025,” Publish.ru, publish.ru The cardboard machine can run at up to 1,200 meters per minute and generate 2,150 tons per day, which materially shifted Russia’s domestic kraftliner availability. Ilim stated that total group output was targeted at 4 million tons in 2024 and is planned to reach 4.5 million tons by 2028. Greater domestic kraftliner availability reduces import dependence and lowers exposure to procurement disruption tied to currency movement and sanctions. At the same time, the added volume creates surplus risk when Chinese demand softens, so pricing discipline and utilization management are likely to remain central through the forecast period.

Import Substitution In Consumer And Industrial Goods

Import substitution has become a practical support factor for the Russia containerboard market, as local manufacturing now depends more heavily on local packaging supply. Paper-based packaging has moved faster than several complex film and laminate formats because production barriers are lower and domestic mills can supply base material with fewer bottlenecks. This shift intensified after large foreign packaging suppliers exited the country, which increased the need for localized sourcing across consumer and industrial goods. A clear example came in 2025 when MoloPak opened a second production complex in Chekhov with capacity of 1.2 billion aseptic packaging units per year and up to 90% local raw material content.[4]Dmitry Alekseenko and Anastasia Solovyova, “Import Substitution Program Implemented At An Enterprise In Chekhov,” REGIONS.RU, regions.ru The project was backed by a RUB 600 million (USD 6.5 million) Federal Industrial Development Fund loan, demonstrating continued public support for localized packaging chains. As more finished goods are produced domestically, the related packaging demand is also staying inside the country, which supports steady board consumption through the forecast period

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Paper Feedstock Ceiling | -0.30% | National, most acute in regions lacking sorting infrastructure, with concentration in Siberian and Ural Federal Districts | Medium term (2-4 years) |

| Export-Netback And Domestic Surplus Volatility | -0.25% | Siberian Federal District for export-oriented producers, national for domestic price spillover | Short term (≤ 2 years) |

| Alternative Packaging Format Competition | -0.15% | National, concentrated in FMCG, cosmetics, and household chemicals sectors | Medium term (2-4 years) |

| Sanctions-Era Machinery And Chemical Dependence | -0.10% | National, with acute pressure on mills dependent on European-origin capital equipment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Paper Feedstock Ceiling

The recycled side of the Russia containerboard market is running into a hard feedstock ceiling that new processing investments cannot solve quickly. Russia generates 7.5 to 8 million tons of waste paper per year, but only 4.5 to 4.6 million tons are collected, leaving processing capacity ahead of supply by 1 to 1.5 million tons. That imbalance pushed prices higher in 2025, and waste paper costs rose by more than 30% and crossed RUB 20,000 (USD 217.4) per ton. Quality is weakening as well, because waste paper in Russia now passes through an average of 12 recycling cycles, up from 8 in the early 2010s, and mills cannot keep extending that loop without virgin fiber input. Collection infrastructure remains insufficient, with a shortage of 129,000 container platforms and 7,000 specialized waste trucks, and closing that gap by 2030 would require nearly RUB 1 trillion (USD 10.9 billion) in investment. These constraints keep recycled-fiber input costs structurally elevated and force producers to optimize product mix, which limits how far virgin-fiber demand can soften inside the Russia containerboard market.

Export-Netback And Domestic Surplus Volatility

The Russia containerboard market is also exposed to sharp price corrections when domestic output rises faster than local converter demand and export economics turn less favorable. Containerboard production rose 6.3% to 4.1 million tons in the first 8 months of 2025, while domestic demand increased only 2.1% to 2.9 million tons, leaving a surplus equal to 800,000 tons of raw materials. Testliner prices fell to RUB 49,300 (USD 535.9) per ton by late May 2025 and were expected to decline by more than RUB 5,000 (USD 54.3) per ton by June 2025. Logistics costs made the imbalance harder to manage because transportation tariffs increased by 33% over the two years ending in 2025, which reduced export netbacks even as shipments to China rose in value. China remained an important outlet, with Russia’s paper and cardboard exports there reaching USD 1.004 billion in 2025, up 15.5% year on year, but stronger ruble conditions and rail cost inflation reduced how much relief exports could provide. With corrugated packaging production expected to remain flat or slightly negative in 2026, domestic converters have limited capacity to absorb upstream surpluses, keeping pricing conditions unstable across the Russia containerboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Fiber Dominance Under Structural Challenge

Virgin fibers held 57.36% of the Russian containerboard market share in 2025, maintaining their leading position across the sector. This position rests on the strength of integrated mill systems and a domestic timber base, which give large producers more control over pulp availability than recycled-fiber producers can claim. The ramp-up of large kraftliner capacity at Ust-Ilimsk reinforced the lead and expanded the supply of domestic premium board for converters. Greater self-sufficiency in virgin fiber has reduced dependence on imported board and lowered exposure to procurement disruption linked to sanctions and exchange-rate swings. The trade-off is that new virgin-fiber output can become surplus volume when eastbound export demand weakens, so producers must balance scale advantages against price discipline.

Recycled fibers remained the smaller input stream in 2025, but the Russia containerboard market size for recycled fibers is projected to expand at a 1.92% CAGR through 2031. EPR reform and fee incentives for secondary raw materials are pushing more packaging users toward higher recycled-content formats, which improves the economics of recycled-fiber mills. That policy pull is important because it works across the full packaging chain, from brand owners to board producers, and supports incremental investment even in a slow-growth environment. Even so, average recycling depth has already reached 12 cycles, and pure recycled grades still struggle to meet heavy-duty performance needs without virgin blending. For that reason, the Russia containerboard industry is likely to keep both raw material routes active, with recycled fiber gaining share gradually but not displacing virgin fiber in applications that require higher burst and stacking strength.

By Product Type: Kraftliner Leadership Facing Testliner Competition

Kraftliners captured 39.94% of Russia containerboard market share in 2025, supported by demand for stronger board in food, industrial, and consumer goods packaging. The Ust-Ilimsk ramp-up, together with the January 2025 modernization of JSC Volga’s PM-6, strengthened Russia’s position in premium and lightweight containerboard supply. Volga added 140,000 tons of capacity and raised total site output to 450,000 tons annually, with close to half of production intended for China and Southeast Asia. Fluting remains less visible than kraftliner, but it stays central to box economics because converters depend on it for structural performance and cost balance. Lightweighting is spreading across converter operations, reducing board intensity per box and placing a natural ceiling on tonnage growth even as shipment counts continue to rise.

Testliners are the fastest-growing product segment, and the Russia containerboard market size for testliners is projected to expand at a 1.88% CAGR through 2031. Producers have favored testliner because new capacity generally needs less capital and can rely on a broader OCC-based feedstock base for standard domestic packaging applications. That expansion outpaced converter uptake in 2025, and average testliner prices fell by 8%, pushing many mills closer to minimum profitability thresholds. Higher-quality testliner with better printing performance is becoming a clearer differentiation path, and premium variants can command 10% to 15% price premiums over standard recycled grades. This quality tier matters because the Russia containerboard industry needs margin-supporting niches, while bulk recycled grades remain exposed to oversupply.

By End-User Industry: Industrial Anchor, Consumer Goods Acceleration

Industrial applications accounted for 35.68% of the Russia containerboard market in 2025, keeping this end-user group in first place. Demand came from chemicals, machinery, metals, and building materials, where packaging must withstand stacking loads, transport stress, and longer distribution cycles. Some industrial sub-sectors weakened in 2025, including ceramic tiles and washing machines, but defense-linked manufacturing offset part of that decline. Food and beverage remained a close second and the most stable demand source because the sector continued to absorb a large share of domestic corrugated packaging. This dual structure, one tied to industrial shipping and the other to food packaging, kept the Russia containerboard market from seeing a steeper demand decline in 2025.

Consumer goods are the fastest-growing end-user segment, and the Russia containerboard market size for consumer goods is projected to expand at a 2.01% CAGR between 2026 and 2031. The core shift has been from imported finished goods toward domestic brands in cosmetics, personal care, household chemicals, and other FMCG categories that now need local packaging inputs. That change links packaging demand more directly to domestic manufacturing rather than import flows, which benefits paper-based board suppliers over the medium term. Other end-user industries, including pharmaceuticals and agriculture, are among the earliest adopters of moisture-resistant and anti-static liner grades as mills try to fill specialized gaps left by former European suppliers. That specialization path is one reason the Russia containerboard industry is still finding pockets of selective growth, even though headline market growth remains low.

Geography Analysis

The Northwestern Federal District accounted for 49.7% of domestic unbleached kraft linerboard production in 2024, which made it the leading supply cluster in the Russia containerboard market. Mills around Arkhangelsk, especially APPM’s Novodvinsk complex, benefit from close links to the regional timber and pulp base. These assets historically had better access to European sea routes, and they now send more volume by rail toward converters in the Central Federal District as trade patterns shift. APPM signed an agreement in June 2025 to build a recycled corrugated case material mill in Kashira, with a planned investment of RUB 23 billion (USD 250 million) and a capacity of 350,000 tons per year, with start-up targeted for the end of 2028. That project shows a clear effort to place new supply closer to Russia’s main consumption zone and reduce freight disadvantages in the country’s largest packaging market.

The Siberian Federal District became the most strategically important production zone from 2024 to 2026 because Ilim’s Ust-Ilimsk complex reshaped eastbound supply in the Russia containerboard market. Its location near the Trans-Siberian corridor and Chinese border routes makes it the main node for kraftliner exports to Asia. Ilim exported a record 2.1 million tons across all product lines to China in 2024, with China accounting for more than half of the group's total output. A separate linerboard project tied to Russian-Chinese industrial cooperation is also moving forward in Arkhangelsk, with equipment supplied by Yunda Paper Machinery for a 350,000-ton-per-year installation.

Consumption is concentrated in the Central, Volga, and Southern Federal Districts, where most FMCG manufacturing, food processing, e-commerce fulfillment, and retail infrastructure are located. Moscow and the surrounding region form the single largest consumption center because major food producers, logistics operators, and online platforms are concentrated there. The Southern Federal District is gaining importance as a secondary production base, and SFT Group’s Kartontara facility in Maykop already produces more than 300 million m² of corrugated packaging annually. SFT also plans to add 250,000 tons of containerboard capacity in the south by 2030 to address the raw material deficit in that region. Rising Russia-ASEAN trade turnover, which reached USD 23.2 billion in 2024 and was projected to exceed USD 30 billion in 2025, is creating additional packaging demand along eastbound and Caspian-Iran logistics corridors that Russian mills are increasingly targeting.

Competitive Landscape

The Russia containerboard market is moderately concentrated in integrated production and more fragmented in conversion, which creates very different operating conditions across the value chain. Ilim Group and APPM have the clearest advantages in virgin fiber, as scale and raw-material self-sufficiency give them better control over costs and supply continuity. Independent converters face a more difficult position because recovered-fiber costs rose while recycled containerboard selling prices weakened in 2025. Waste paper prices increased by 32% while recycled containerboard prices declined by 8%, creating a 40-point margin squeeze for many downstream players. Gotek remained under pressure and reported a 2025 net loss of RUB 231 million (USD 2.6 million) even though operating profit improved after earlier efficiency measures.

Competitive strategy in 2026 centers on deeper integration, regional expansion, and equipment modernization across the Russian containerboard market. Kappa Rus followed that logic in January 2025, when it acquired Okulovskaya Paper Mill and added 90,000 tons per year of fluting and testliner capacity, plus 100 million packaging units per year. SFT Group is pursuing a similar path through a program of up to RUB 30 billion (USD 326.1 million) by 2030 to build new containerboard and corrugated assets in Adygea. APPM’s Kashira project shows the same logic, with supply moving closer to Moscow-region demand rather than relying only on long-haul deliveries from legacy northern mill locations.

White-space opportunities remain strongest in moisture-resistant, anti-static, and food-contact-compliant grades, where Western suppliers' exits have left domestic gaps that are still unfilled. Producers are also moving toward lightweight, high-print-quality board specifications to better serve automated filling lines and premium-branded packaging. Chinese machinery vendors, especially Yunda Paper Machinery, have become more visible as suppliers for new Russian projects, easing part of the sanctions-era equipment constraint. That shift reduces one bottleneck, but it also creates a new dependency on Chinese components and service networks for future maintenance cycles. Taken together, these patterns suggest the Russia containerboard market is likely to remain led by a few large producers at the mill level, while remaining much more open and contested in converting and specialty niches.

Russia Containerboard Industry Leaders

Ilim Group

Arkhangelsk Pulp and Paper Mill

Joint Stock Company Volga

Joint Stock Company Syktyvkarskiy LPK

Mari Pulp and Paper Mill

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ilim Group's Ust-Ilimsk cardboard machine (KDM) reached a cumulative production milestone of 1 million tons of containerboard since commissioning, marking the first major output milestone for Russia's largest-ever single containerboard investment, which totaled RUB 100 billion (USD 1.1 billion), and the company outlined plans to continue raising productivity and expanding output volumes at the facility.

- February 2026: SFT Group disclosed plans to sign a cooperation agreement at the St. Petersburg International Economic Forum in June 2026 for RUB 4 billion (USD 44.9 million) in expansion investment at its Aleksinskaya Paper and Board Mill in Aleksin, Tula region, through 2031, targeting capacity increases to 190,000 tons of containerboard and 180 million m² of corrugated packaging annually, backed by Tula regional government support.

- September 2025: Ilim Group launched "Polar Bear," a premium-grade bleached softwood pulp produced at the Ust-Ilimsk mill, positioned exclusively for China’s premium paper and packaging market and developed following trial runs with Chinese customers on their own converting equipment, extending Ilim’s China product portfolio beyond bulk containerboard into higher-margin specialty grades.

- September 2025: SFT Packaging Taganrog completed a full modernization of its corrugated unit, replacing cross-cutting machinery and sheet-stacking equipment over an 11-day installation window, raising the site’s annual corrugated production capacity to 200 million m² and achieving a target productivity of 27.2 thousand m² per hour within the first month of operation.

Russia Containerboard Market Report Scope

The Russia Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacturing of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The increasing demand for sustainable, lightweight, and durable packaging solutions drives the market.

The Russia Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast size of the Russia containerboard market?

The Russia containerboard market was valued at USD 3.48 billion in 2025, is estimated at USD 3.57 billion in 2026, and is forecast to reach USD 3.87 billion by 2031 at a 1.63% CAGR.

Which material segment leads in Russia containerboard demand?

Virgin fibers led with a 57.36% share in 2025, supported by integrated pulp and paper capacity and stronger control over raw material supply.

Which product type is growing fastest in Russia?

Testliners are the fastest-growing product type, with a projected 1.88% CAGR through 2031, even though oversupply pressure affected prices in 2025.

Which end-user group contributes the most to board consumption?

Industrial applications led with a 35.68% share in 2025, while food and beverage remained one of the most stable demand anchors for corrugated packaging.

What is the main constraint on recycled-fiber growth in Russia?

The biggest limit is feedstock availability, because waste paper collection remains below processing needs and recycled fiber quality weakens after repeated use.

How are leading producers responding to market pressure?

Large players are focusing on integration, capacity expansion near demand centers, export corridor development, and upgrades in lightweight and higher-quality grades.

Page last updated on: