Belgium Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

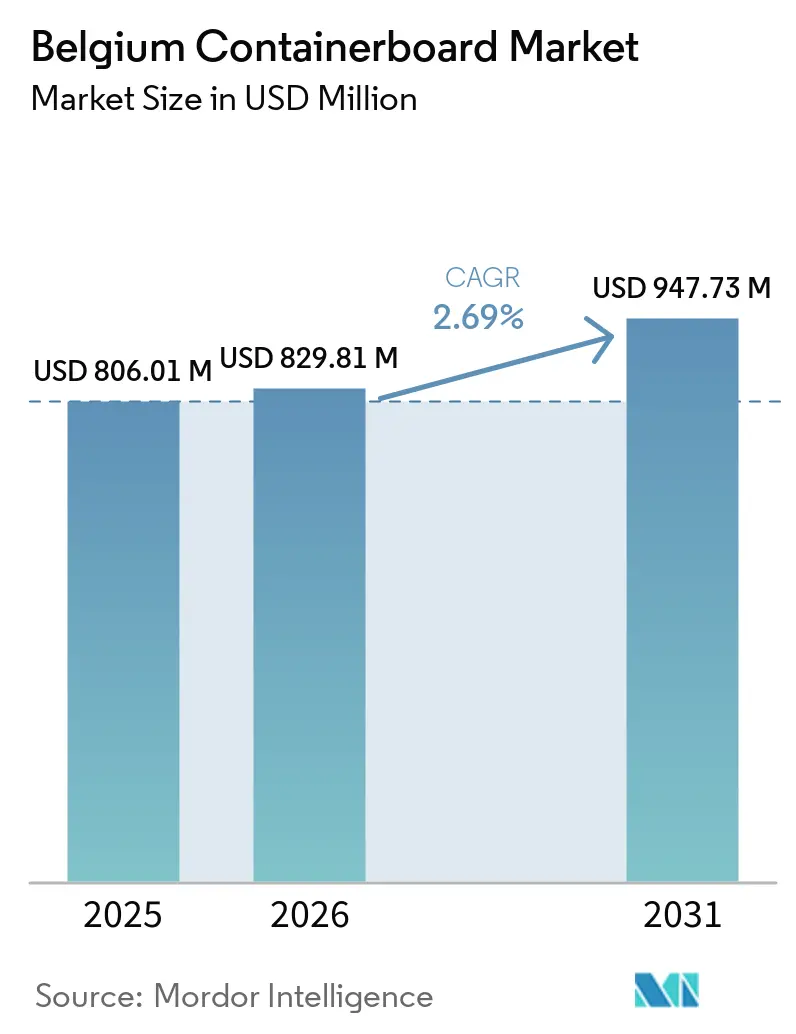

| Base Year Market Size (2025) | USD 806.01 Million |

| Market Size (2026) | USD 829.81 Million |

| Market Size (2031) | USD 947.73 Million |

| Growth Rate (2026 - 2031) | 2.69% CAGR |

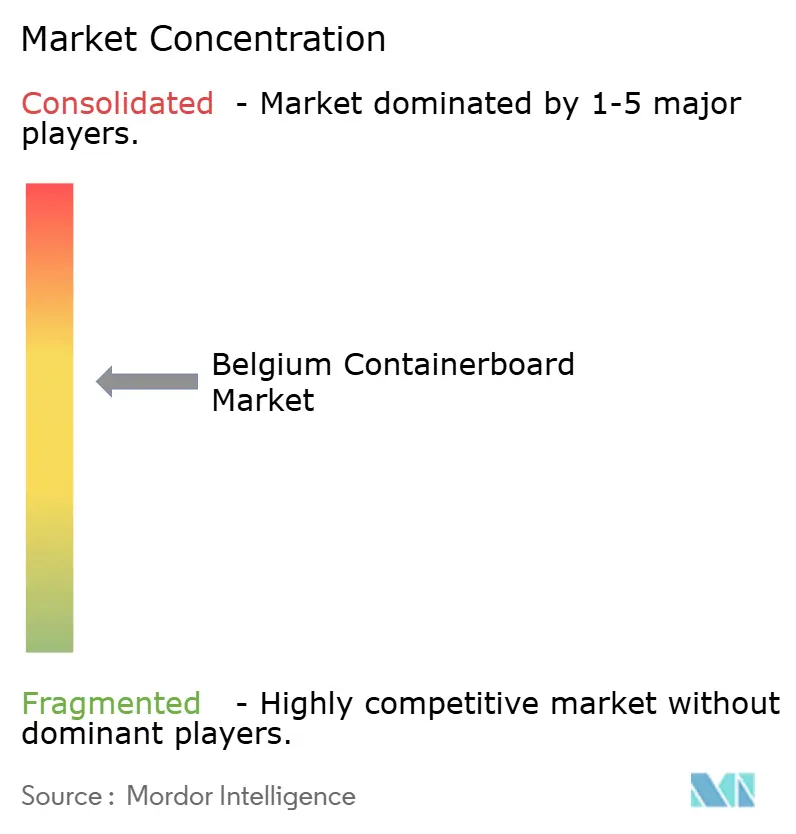

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Containerboard Market Analysis by Mordor Intelligence

The Belgium containerboard market size is expected to grow from USD 806.01 million in 2025 to USD 829.81 million in 2026 and is forecast to reach USD 947.73 million by 2031 at 2.69% CAGR over 2026-2031. The Belgium containerboard market is supported by Belgium's role as a high-throughput European logistics gateway and by its mature recycled fiber base. Repacking activity around Antwerp-Bruges lifts apparent domestic demand above local retail consumption because imported cargo is converted into corrugated shippers for onward EU distribution. Belgium's paper and cardboard recycling rate reached 107.7% of declared industrial volumes in 2024, with 461,000 tonnes recovered from commercial and industrial sources, which gives local producers a stable feedstock base and helps reduce exposure to raw material shortages. PPWR rules that start applying from August 12, 2026, along with steady food and beverage export flows, keep fiber-based transit packaging in a favorable position during the forecast period. Competition remains moderately consolidated, with VPK Group, Smurfit Westrock, Mondi, Stora Enso, and other integrated suppliers shaping capacity, premium grades, and converting reach, while energy costs and trade disruptions remain the main risks.

Key Report Takeaways

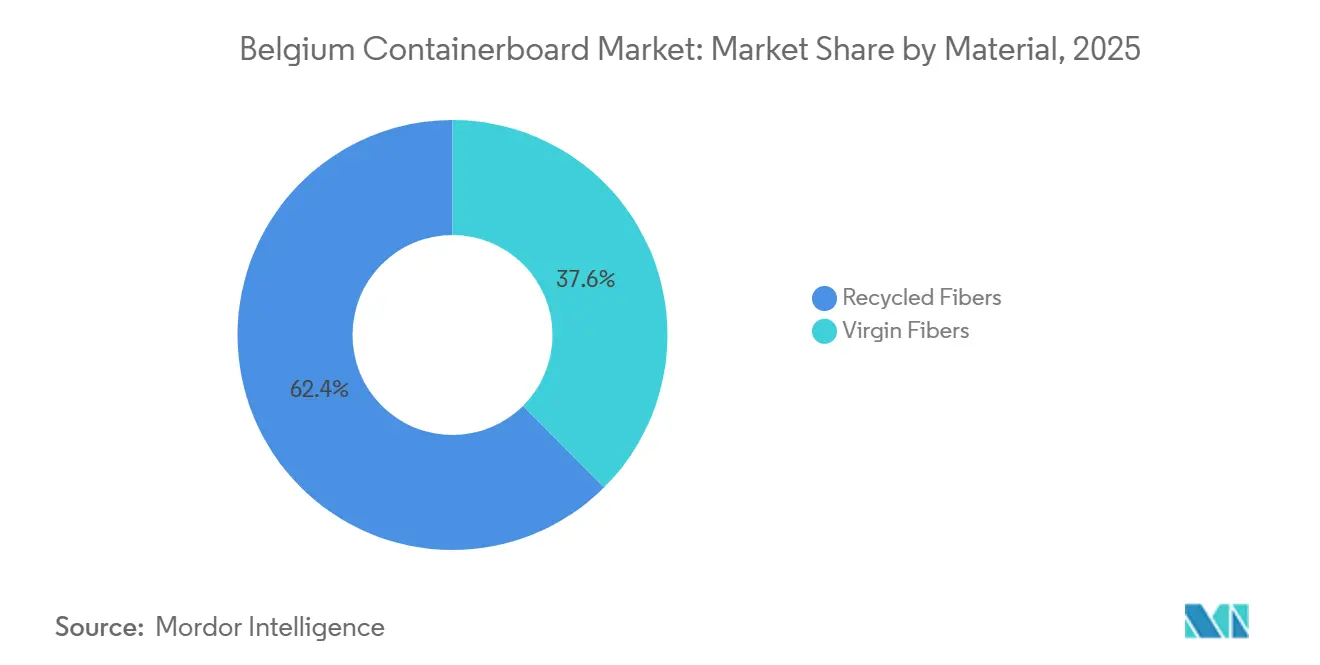

- By material, recycled fibers captured 62.44% of the Belgium containerboard market share in 2025.

- By product type, the Belgium containerboard market size for the kraftliners segment is forecast to advance at a 3.04% CAGR through 2031.

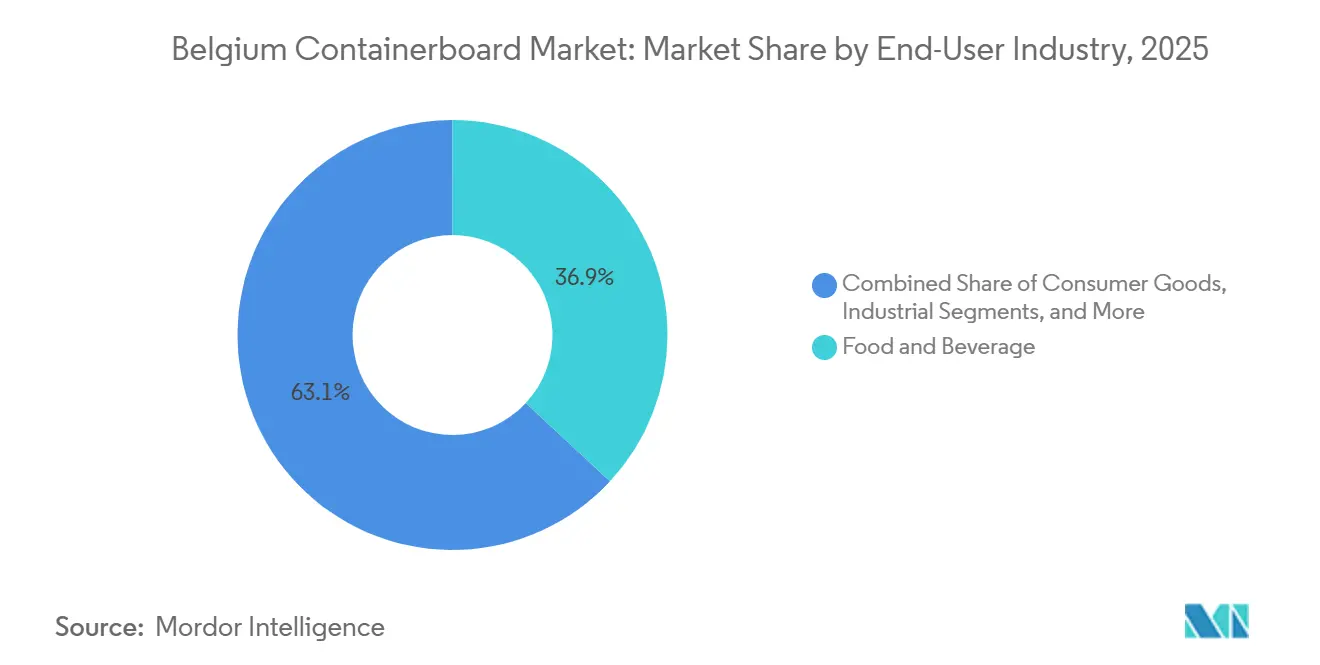

- By end-user industry, food and beverage captured 36.91% of the Belgium containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Belgium Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Repacking Through Antwerp-Bruges Logistics Corridors | +0.7% | Flanders, particularly Antwerp, Zeebrugge, and Liège logistics parks | Short term (≤ 2 years) |

| PPWR-Driven Shift Toward Fiber-Based Transit Packaging | +0.6% | EU-wide mandate with Belgian compliance from August 2026 | Medium term (2-4 years) |

| Food And Beverage Export And Fresh-Chain Packaging Demand | +0.5% | Belgium-wide, concentrated in Flanders and Hainaut agri-food clusters | Medium term (2-4 years) |

| Lightweighting And Performance Upgrades In Corrugated Packaging | +0.3% | EU-wide R&D, with Belgian mill-level investment | Medium term (2-4 years) |

| Belgian Mill Automation Improving Recovered Fiber Yield | +0.2% | Flanders mill cluster, including Oudegem, Erembodegem, and Ghent | Short term (≤ 2 years) |

| Retail Shelf-Ready And Private-Label Packaging Expansion | +0.2% | Belgium-wide, with spillover to the Netherlands and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Repacking Through Antwerp-Bruges Logistics Corridors

Flanders hosts nearly 800 European Distribution Centers, which keeps Belgium at the center of regional warehousing and cross-border fulfillment. The same logistics base is reinforced by a waterway network that places 80% of Flemish companies within 10 km of an inland waterway, which lowers inbound and outbound transport costs for fiber and boxed goods. The Port of Antwerp-Bruges is using its Container Plan 22-30 to reduce dwell times and improve multimodal links, thereby supporting faster cargo turnover and increased repacking activity around Antwerp and Zeebrugge. In March 2025, the port also launched a tender for an 8.5-hectare Maritime Logistics Zone in Zeebrugge for cold chain, consumer goods, and heavy cargo operators, adding more space for value-added logistics work. This setup means the Belgian containerboard market draws demand from cargo that is redistributed across the EU, not only from Belgian retail sales. That feature provides the Belgian containerboard market with a demand buffer when local consumption softens, as logistics-linked box use continues to track regional trade flows.

PPWR-Driven Shift Toward Fiber-Based Transit Packaging

Regulation (EU) 2025/40 entered into force in February 2025, and its provisions will apply from August 12, 2026, making packaging compliance a near-term commercial issue in the Belgian containerboard market.[1]Publications Office of the European Union, “Regulation (EU) 2025/40 - Packaging and Packaging Waste Regulation,” Publications Office of the European Union, op.europa.eu The regulation requires packaging to be recyclable by January 1, 2030, and limits space in e-commerce and transport packaging to 50%, thereby supporting lighter, more recyclable corrugated formats. The European Commission also highlights PFAS restrictions in food-contact packaging under the new framework, which strengthens the case for fiber-based transit packaging in sensitive applications. VBO-FEB stated in 2025 that modulated EPR fees will penalize non-recyclable and hard-to-recycle packaging, which creates a direct cost gap between compliant fiber solutions and less recyclable alternatives.[2]VBO-FEB, “Nouvelles Règles Européennes En Matière D'emballages (PPWR) Impact À Partir De 2026,” VBO-FEB, vbo-feb.be Valipac reported that Belgium recycled 107.7% of the declared volumes of industrial paper and cardboard packaging in 2024, giving local producers a credible compliance position as PPWR enforcement expands. The Belgium containerboard market is therefore moving closer to a compliance-led purchasing model, where converters with stronger documentation and traceable fiber systems will hold a clear advantage.

Food And Beverage Export And Fresh-Chain Packaging Demand

Food and beverage remains the largest end-user in the Belgium containerboard market because export-oriented corrugated cases must protect products throughout long distribution chains and amid temperature variations. Flanders Investment and Trade identifies agri-food as one of the region's largest export verticals, and North Sea Port Ghent serves cargo segments such as bio-energy, fruit juice, and temperature-controlled products.[3]Flanders Investment and Trade, “Logistics Ecosystem,” Flanders Investment and Trade, flandersinvestmentandtrade.com Those flows rely on packaging that can meet moisture resistance, stacking strength, and handling standards without shifting to harder-to-recycle formats. Belgian food processors are also expanding shelf-ready formats across multiple EU markets, which underscores the value of consistent testliner surfaces and improved print presentation. Flanders Investment and Trade lists omni-channel retail logistics as a focus domain, which shows ongoing support for the infrastructure that connects food manufacturing and packaging demand. This combination keeps the Belgium containerboard market less exposed to short demand swings than segments tied to more discretionary industrial output.

Lightweighting And Performance Upgrades In Corrugated Packaging

Lightweighting in the Belgium containerboard market is moving beyond simple grammage reduction and toward grades that preserve compression strength with less material. That shift aligns with PPWR rules requiring packaging weight and volume to be reduced to the functional minimum by 2030. VPK Group stated that its Oudegem plant replaced 40-50% of coal with sustainably sourced wood pellets in 2024 and targeted a reduction of 25,000 tonnes of CO2-equivalent Scope 1 emissions. STI Group invested over EUR 8 million (USD 8.66 million) in lightweight laminating technology for very low grammage paper grades, citing PPWR compliance as a commercial driver.[4]STI Group, “Lightweight Corrugated Board,” STI Group, sti-group.com For mills and converters, the payoff is not only lower material use but also better transport efficiency and a clearer compliance story for customers. This makes lightweighting one of the more practical routes for the Belgium containerboard market to defend margins while meeting regulatory and customer requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Paper And Energy Cost Volatility | -0.4% | Belgium-wide, with exposure to European gas and OCC price cycles | Short term (≤ 2 years) |

| Competition From Reusable Plastic Transit Packaging | -0.3% | EU-wide, concentrated in Belgian automotive and chemical industrial logistics | Medium term (2-4 years) |

| PPWR Documentation And Design-Compliance Costs | -0.2% | EU-wide, disproportionate for Belgian small-to-mid-size converters | Medium term (2-4 years) |

| Recovered Fiber Quality Drift From Contamination And Moisture | -0.1% | Belgium and the broader EU, particularly OCC from e-commerce return streams | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Paper And Energy Cost Volatility

Recovered paper and energy remain the main cost pressure points in the Belgium containerboard market because recycled board still needs energy-intensive pulping, drying, and refining. EMIS Flanders stated that energy costs account for 10-25% of total production costs in the Belgian paper industry. The same source noted that recycled-fiber paper uses 2-3 times less energy than virgin-fiber production, but it still depends heavily on thermal energy per tonne of output. Billerud reported in late 2025 that European containerboard pricing faced pressure from structural overcapacity after trade flows shifted following new US import tariffs. That combination narrows margins for smaller single-site operations that lack scale, sourcing leverage, or strong downstream integration. The Belgium containerboard market can absorb some of this pressure through integrated players, but the constraint still limits how fast supply can respond when demand improves.

Competition From Reusable Plastic Transit Packaging

Reusable plastic transit packaging poses a targeted threat to the Belgian containerboard market, primarily in closed-loop industrial systems rather than in broad consumer distribution. Valipac reported that industrial plastic packaging in Belgium was 91% reusable by market volume in 2024, with strong use in rigid logistics formats. Regulation (EU) 2025/40 also sets reuse targets for transport and sales packaging, including 40% for packaging moving between EU member states by 2030 and 100% for intra-member-state transport packaging. That framework provides reusable systems with greater support in automotive, chemical, and manufacturing chains where return logistics are already established. Bruxelles Environnement highlighted Loopipak's reusable corrugated-tarpaulin solution for e-commerce returns, suggesting that the competitive response may come from hybrid multi-trip formats rather than plastic crates. Producers that certify reusable or multi-trip fiber designs will be in a better position to defend their share as this pressure builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Retain Structural Lead, Virgin Fibers Grow Faster

Recycled fibers held 62.44% of Belgium's containerboard market share in 2025, which reflected the country's strong collection and recovery system. Fost Plus reported 282 kT of household paper-cardboard packaging recycled in 2024, with 82% processed domestically and the remainder in the Netherlands. Valipac also documented 461,000 tonnes of commercial and industrial paper and cardboard packaging recycled in 2024, at 107.7% of declared volumes. EMIS Flanders stated that around two-thirds of the fibers used in Belgian paper production come from recycled feedstock, which strengthens the cost position of mills centered on recovered feedstock. This setup keeps recycled grades at the center of domestic production economics and supports the long-standing scale advantage of local mills.

Virgin fibers are the fastest-growing material segment, and the Belgium containerboard market size for virgin grades is projected to expand at a 2.96% CAGR from 2026 to 2031. Demand is rising in premium e-commerce and retail-ready packs where white-top or bleached liner surfaces improve print clarity and shelf appearance. Stora Enso started its first customer deliveries from its new Oulu consumer board line in Q2 2025, adding 750,000 tonnes of annual folding boxboard and coated unbleached kraft capacity that matters for Benelux supply chains. Billerud reported SEK 1,355 million (USD 138.08 million) in European containerboard net sales in Q1 2025, but later described weak European conditions and structural overcapacity, meaning growth in this segment will depend more on product performance than on broader market tightness.. Within the Belgian containerboard industry, this balance keeps recovered grades dominant, while premium virgin grades win incremental applications that require stronger presentation and cleaner surfaces.

By Product Type: Testliners Hold Scale, Kraftliners Gain Premium Demand

Testliners accounted for 41.16% of Belgium's containerboard market share in 2025, making them the leading product type for mainstream corrugated applications. That lead is closely tied to the country's recycled fiber strength, because testliners depend on a stable secondary fiber supply and disciplined input costs. Belgian mills and converters continue to favor grades that balance burst strength, stacking performance, and printability for shipments of food, consumer goods, and industrial products. VPK Group's Belgian paper operations include 3 paper machines at Oudegem, with a combined annual capacity of 550,000 tonnes of recycled corrugated case material and greyboard. The October 2025 commissioning of a new BHS corrugator at Erembodegem increased corrugated board output capacity from 100 million m² to 170 million m², strengthening the local converting base that relies heavily on recycled grades.

Kraftliners are the fastest-growing product type, and the Belgium containerboard market size for kraftliner grades is set to grow at a 3.04% CAGR through 2031. Growth is coming from export-grade food and beverage cases and more premium e-commerce boxes that need higher burst strength and cleaner surfaces at comparable grammage. Billerud launched CrownBoard Light and CrownBoard Carry in Q3 2025 for cold, moist, and beverage multipack applications, demonstrating how suppliers are targeting performance gaps beyond standard recycled liners. Within the Belgium containerboard industry, this split keeps testliners dominant in volume while kraftliners expand where performance and presentation matter more than the lowest cost.

By End-User Industry: Food And Beverage Anchor Volumes, Consumer Goods Expand Faster

Food and beverage accounted for 36.91% of the Belgium containerboard market in 2025, making it the main volume anchor across converting and logistics networks. Flanders Investment and Trade identifies agri-food as one of the region's largest export verticals, and North Sea Port Ghent serves fruit juice, bio-energy, and temperature-controlled cargo. These flows require corrugated cases that can hold stacking load, resist moisture, and travel through export channels without product loss. Belgian food processors are also pushing shelf-ready packaging across several EU markets, which raises demand for controlled surface quality and consistent converting performance. This makes food and beverage the most stable application base for suppliers that serve both domestic distribution and export channels.

Consumer goods are the fastest-growing end-user, with a 3.11% CAGR expected from 2026 to 2031. Growth comes from e-commerce parcel formats, private-label expansion, and the shift away from plastic outer packaging under PPWR rules. DS Smith invested nearly EUR 2 million (USD 2.18 million) in its Harelbeke plant in December 2025 to install new inline processing, printer-slotter, pallet strapping, and baling equipment to meet regional corrugated demand. This part of the Belgian containerboard industry is likely to remain active because right-sized packs and retail-ready boxes provide converters with a clear route to serve branded and private-label customers.

Geography Analysis

The Belgium containerboard market is centered in Flanders, where most of the country's paper production, converting capacity, and distribution infrastructure are located. VPK Group's Oudegem mill operates 3 paper machines with a combined annual capacity of 550,000 tonnes of recycled corrugated case material and grey board. Its Erembodegem plant raised corrugated board output capacity from 100 million m² to 170 million m² after the new BHS corrugator was commissioned in October 2025. Flanders hosts nearly 800 European Distribution Centers, at a rate of close to 5 per 100 km², making it one of Europe's densest logistics clusters. Its inland waterway network extends more than 1,300 km, and 80% of Flemish companies are within 10 km of a navigable waterway, which lowers bulk transport costs for recovered fiber and finished board.

Within the Belgian containerboard market, Wallonia and the Brussels-Capital Region play supporting but important roles in demand formation. Wallonia's food processing, pharmaceutical, and industrial manufacturing base supports demand for export-grade corrugated cases and fulfillment packaging. Liège's logistics position adds to e-commerce and distribution flows into wider European networks, which extend box demand beyond the main Flemish mill cluster. Brussels remains important because multinational consumer goods groups often influence packaging specifications and supplier choices from regional headquarters located there.

Belgium's national role in the recovered fiber trade gives the Belgian containerboard market an additional structural advantage. Valipac reported that 15% of Belgium's industrial paper and cardboard recycling volumes were processed in Asia in 2024, indicating the country was already a meaningful supplier to wider recovered paper flows. As European rules tighten around recyclability and waste movement, keeping more of that fiber within Europe will become more valuable for local mills. Belgium's 107.7% recycling rate in 2024 means it is a net contributor of high-quality recovered fiber to the regional OCC stream. That position will matter more as recyclability grading and EPR fee modulation push packaging buyers toward traceable fiber content.

Competitive Landscape

The Belgium containerboard market is moderately consolidated, with integrated groups controlling much of the mill and converting base while regional converters still serve local demand. VPK Group is the main domestically headquartered integrated player, with more than 70 manufacturing plants across 21 countries and FY2024 net sales of EUR 1.849 billion (USD 1.999 billion). The company also reported a 5-year CAGR of 7% and stated that all paper mill output uses recycled fibers, which underlines its circular position in the Belgium containerboard market. Smurfit Westrock reported FY2025 net sales of USD 31,179 million and said its EMEA mills ran near full utilization through 2025. That utilization picture matters because disciplined capacity management can support pricing even when European supply conditions remain uneven.

Mondi strengthened its position in the Belgian containerboard market by investing EUR 1.2 billion (USD 1.298 billion) across its paper mills and packaging plants over the 3 years through 2024. The same company completed the acquisition of Schumacher Packaging's Western European assets for EUR 634 million (USD 685.6 million), expanding its corrugated converting footprint in Belgium. Stora Enso used its 2025 Capital Markets Day to confirm its position as the second-largest corrugated packaging producer in Benelux and to reorganize reporting around consumer packaging and integrated packaging. This competitive set shows that scale, converting reach, and product mix now matter as much as mill ownership alone.

Strategic moves in 2025 and 2026 show that capacity quality is as important as capacity volume in the Belgium containerboard market. VPK Packaging Belgium commissioned a new 2.80 m BHS corrugator at Erembodegem in October 2025 and later raised its stake in Ribble Packaging to 50% in December 2025, which strengthened both domestic output and e-commerce fanfold exposure. DS Smith invested nearly EUR 2 million (USD 2.18 million) in Harelbeke to expand corrugated processing for regional consumer goods demand. Billerud introduced CrownBoard Light and CrownBoard Carry in late 2025, targeting cold-chain and beverage multipack applications where wet strength and tear resistance matter. Together, these moves show a market where investment is focused on smarter formats, compliance readiness, and customer-specific performance rather than on undifferentiated tonnage alone.

Belgium Containerboard Industry Leaders

VPK Group NV

Smurfit Westrock plc

International Paper Company

Stora Enso Oyj

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: His Majesty the King of Belgium visited VPK Group's Erembodegem site as part of the first Interregional Economic Visit between Flanders and Wallonia, with discussions centered on innovation and the circular economy, recognizing VPK's role as a flagship Belgian containerboard and fiber packaging producer.

- March 2026: Mondi confirmed an EUR 1.2 billion (USD 1.298 billion) packaging expansion program and finalized the acquisition of Schumacher Packaging's Western Europe assets, including converting plants in Belgium, at an enterprise value of EUR 634 million, USD 685.6 million, materially expanding its corrugated converting footprint in Belgian and Benelux markets.

- February 2026: Smurfit Westrock reported FY2025 net sales of USD 31,179 million, confirmed it exceeded its USD 400 million synergy target, and increased its quarterly dividend by 5% to USD 0.4523 per share, with EMEA operations cited as delivering outstanding performance throughout the year.

- January 2026: DS Smith, part of International Paper following the January 31, 2025, combination, formalized an investment of nearly EUR 2 million (USD 2.18 million) in its Harelbeke packaging plant in West Flanders, installing a new inline processing machine, printer-slotter, pallet strapping machine, and baler to expand corrugated capacity for regional consumer goods demand.

Belgium Containerboard Market Report Scope

The Belgium Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Belgium Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and outlook for the Belgium containerboard market?

The Belgium containerboard market stood at USD 806.01 million in 2025, reaches USD 829.81 million in 2026, and is forecast to reach USD 947.73 million by 2031 at a 2.69% CAGR.

What is driving demand for containerboard in Belgium?

The main demand drivers are logistics-linked repacking around Antwerp-Bruges, PPWR-led preference for recyclable fiber packaging, and stable food and beverage export packaging needs.

Which material segment leads in Belgium, and which one grows the fastest?

Recycled fibers led with a 62.44% share in 2025, while virgin fibers are projected to grow the fastest at a 2.96% CAGR through 2031.

Why does Antwerp-Bruges matter so much for box demand?

Belgium serves as a repacking and redistribution base for wider EU cargo flows, so corrugated demand is supported by logistics activity, not only by domestic retail consumption.

Which end-user segment holds the strongest position?

Food and beverage led with 36.91% share in 2025 because export-grade and fresh-chain packaging needs remain steady and require reliable corrugated performance.

Which companies are shaping competitive activity in Belgium?

VPK Group, Smurfit Westrock, Mondi, Stora Enso, DS Smith, and Billerud are shaping competition through capacity additions, acquisitions, premium grade launches, and compliance-oriented investments.

Page last updated on: