Bladder Cancer Detection Kits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

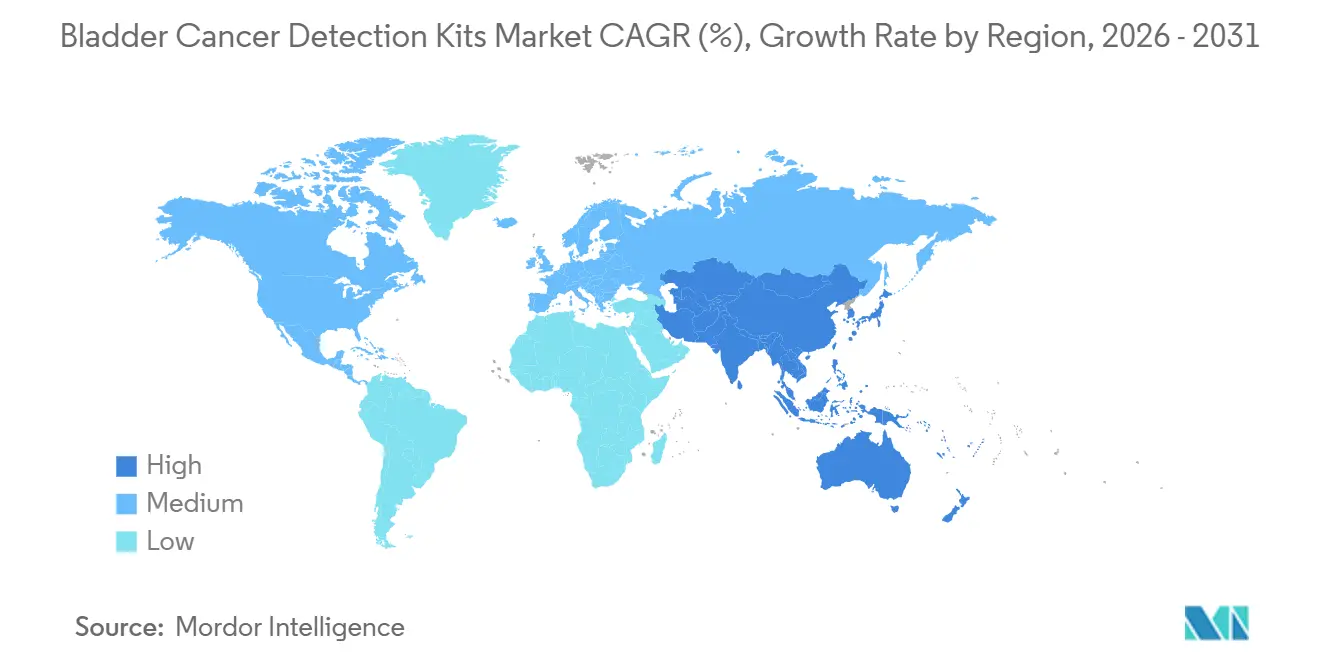

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

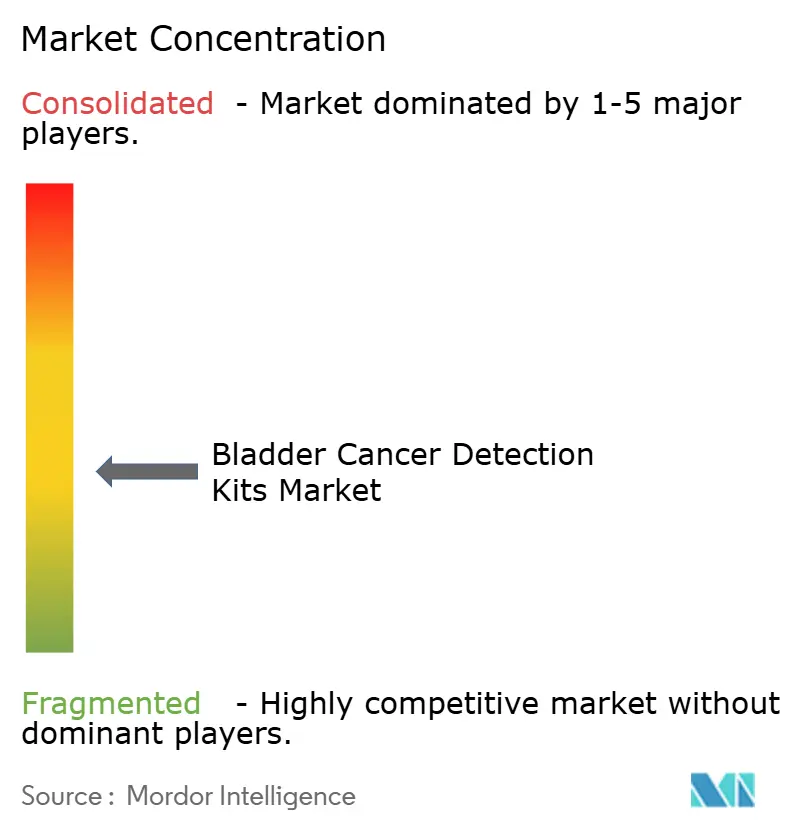

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bladder Cancer Detection Kits Market Analysis by Mordor Intelligence

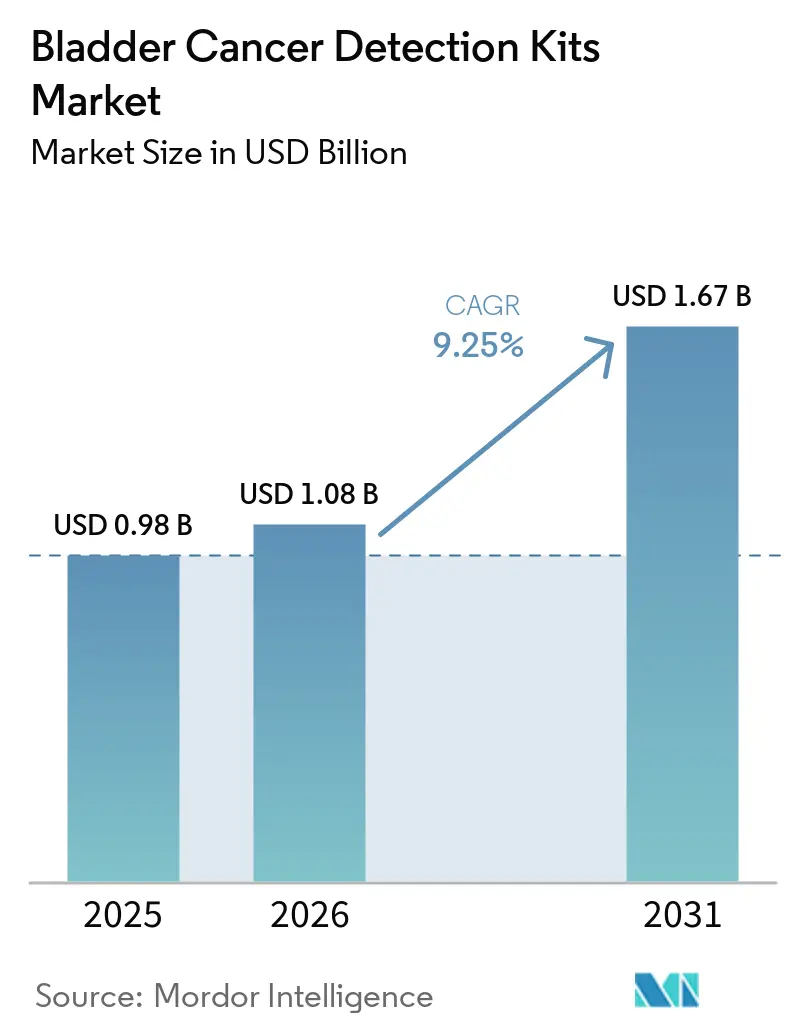

The Bladder Cancer Detection Kits Market size is projected to be USD 0.98 billion in 2025, USD 1.08 billion in 2026, and reach USD 1.67 billion by 2031, growing at a CAGR of 9.25% from 2026 to 2031.

The growth base for the bladder cancer detection kits market is supported by the large clinical burden of disease, with bladder cancer ranking as the 9th most commonly diagnosed malignancy worldwide. Demand is also being reinforced by the rise in absolute case counts since 1990, even as age-standardized incidence rates have eased, because more patients are moving into recurring surveillance and post-treatment monitoring pathways. The 2025 AUA guideline change widened the addressable testing pool in the bladder cancer detection kits market by recognizing urinary biomarkers as an evidence-based option for intermediate-risk microscopic hematuria patients who want to defer cystoscopy. Reimbursement continuity for established platforms and new companion diagnostic pathways are shaping commercial strategy, which favors companies that can combine clinical evidence, payer access, and laboratory integration. The bladder cancer detection kits market is therefore expanding through repeat-use surveillance demand, broader non-invasive triage, and a gradual widening of test settings beyond the traditional cystoscopy-led workflow.

Key Report Takeaways

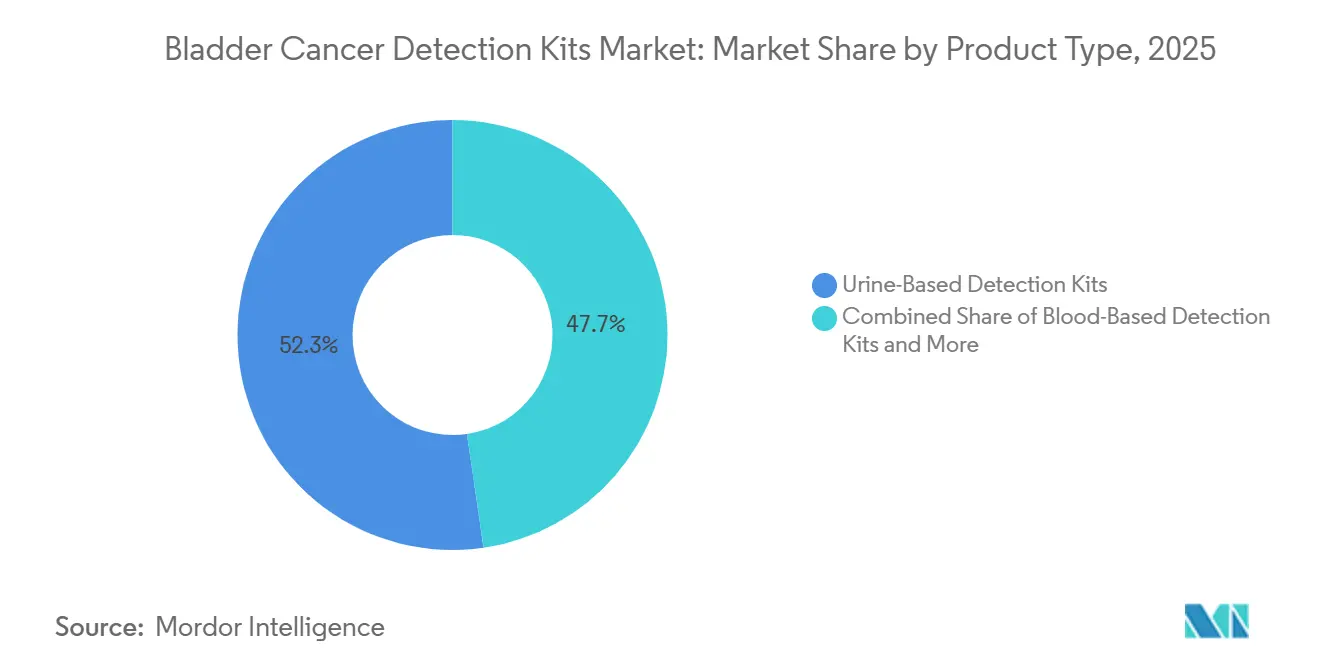

- By product type, Urine-Based Detection Kits led with 52.31% revenue share in 2025, while Blood-Based Detection Kits are forecast to expand at an 11.38% CAGR from 2026 to 2031.

- By technology, FISH Kits held 32.24% share in 2025, while DNA Methylation and RNA Signature Kits are projected to grow at a 12.52% CAGR over 2026 to 2031.

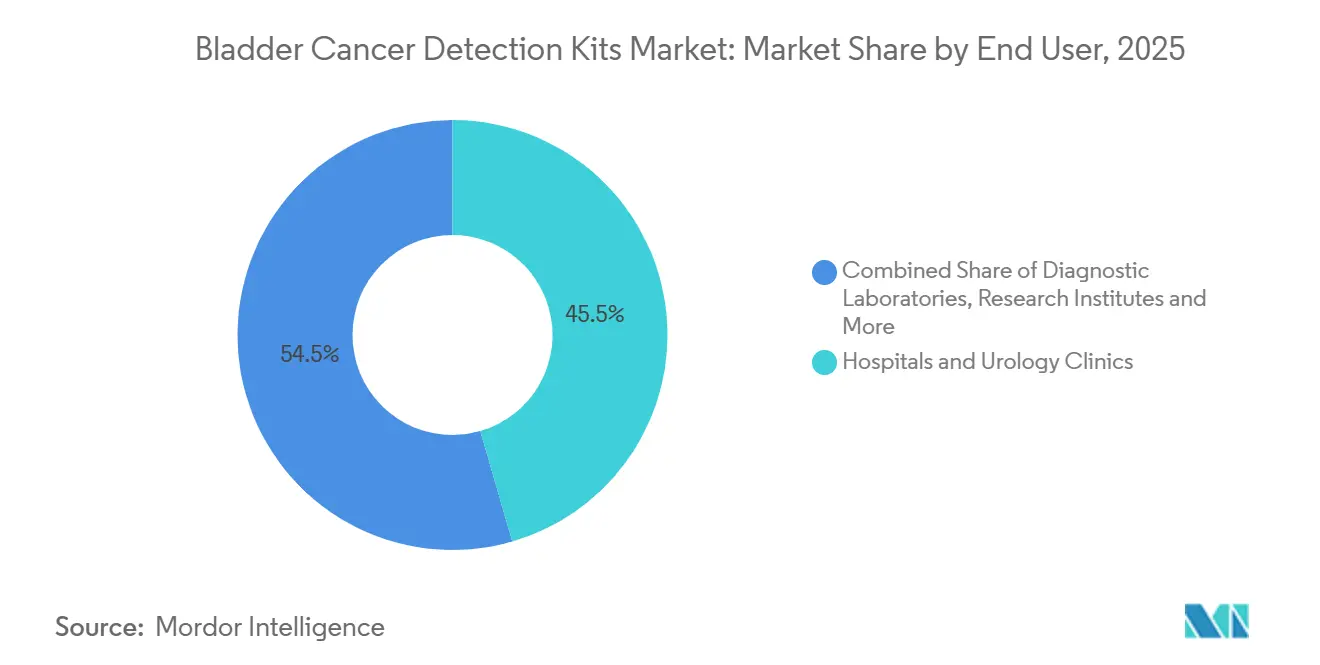

- By end user, Hospitals and Urology Clinics accounted for 45.52% of demand in 2025, while Diagnostic Laboratories are expected to record the highest CAGR at 11.25% through 2031.

- By geography, North America represented 38.22% of revenue in 2025, while Asia-Pacific is forecast to advance at an 11.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bladder Cancer Detection Kits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Bladder Cancer Surveillance Burden | +1.8% | Global, concentrated in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Shift Toward Non-Invasive Urine-Based Testing | +2.1% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| AI-Assisted Risk Stratification in Hematuria Workups | +1.5% | North America and Europe, early-stage adoption in APAC | Medium term (2-4 years) |

| Reimbursement Support for Adjunctive Urothelial Tests | +1.4% | North America, with spillover to Europe and APAC | Short term (≤ 2 years) |

| Rising Demand for Recurrence Monitoring in NMIBC | +1.2% | Global, highest density in high-income healthcare markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Bladder Cancer Surveillance Burden

The bladder cancer detection kits market is benefiting from a larger surveillance population because bladder cancer cases in adults aged 55 and older rose from 226,421 to 483,234 over the past three decades. This matters because older patients form the highest-risk group and remain the core population for repeated evaluation after diagnosis and treatment. Recurrence also keeps testing volumes elevated, since each NMIBC patient faces a lifetime average of 6.6 recurrences, which creates repeated monitoring demand even when new diagnosis growth slows. High-income regions in North America and Western Europe still carry the heaviest incidence burden, which supports steady utilization in markets with stronger reimbursement and laboratory capacity. China adds another durable volume base to the bladder cancer detection kits market, with male incidence projected to rise from 9.1 per 100,000 in 2021 to 11.2 per 100,000 by 2035.

Shift Toward Non-Invasive Urine-Based Testing

The bladder cancer detection kits market gained a clear clinical tailwind in 2025 when the AUA endorsed urinary biomarker tumor markers as an option for intermediate-risk microscopic hematuria patients who prefer to defer cystoscopy. That recommendation matters because a negative urinary biomarker result can reduce cancer probability for these patients from 0.2–3.1% to 0.1–0.4%, which changes the clinical path for a meaningful part of the workup population. The UroFollow trial also showed that urine markers combined with ultrasound can support a clinically non-inferior surveillance alternative to white-light cystoscopy in low- and intermediate-risk NMIBC patients[1]Lars Dreyer, “Results of the Prospective Randomized UroFollow Trial Comparing Marker-Guided Versus Cystoscopy-Based Surveillance in Patients with Low/Intermediate-Risk Bladder Cancer,” European Urology Oncology, sciencedirect.com. Technical performance has improved enough to support this shift, with multitarget urine DNA tests reporting 91.37% sensitivity, 95.09% specificity, and 0.9583 AUC in double-blinded multicenter prospective testing. As more decisions move from bundled cystoscopy encounters to separately ordered urine tests, the bladder cancer detection kits market is gaining a broader commercial base for standalone kit suppliers and centralized laboratories.

AI-Assisted Risk Stratification in Hematuria Workups

The bladder cancer detection kits market is also being helped by more structured triage in hematuria workups, because risk-based pathways make biomarker use easier to justify in settings where indiscriminate testing would face payer resistance. The commercial effect is important, since tests used at the decision point between immediate cystoscopy and short-term deferral have a clearer value proposition than tests added after the procedure decision is already made. In Europe, the EAU documented that AI algorithms paired with digital image processing improved urine cytology sensitivity for high-grade tumors to 92% in systems such as VitaDX’s VisioCyt Bladder. A combined approach using the Hematuria Cancer Risk Score and Oncuria-Detect achieved a higher diagnostic AUC than either tool alone in real-world evaluation and reduced unnecessary cystoscopy referrals. As that workflow becomes more common, the bladder cancer detection kits market can capture test demand earlier in the diagnostic sequence and in a more targeted way.

Reimbursement Support for Adjunctive Urothelial Tests

The bladder cancer detection kits market continues to respond quickly to reimbursement milestones because payer support determines whether a clinically validated assay reaches routine use or stays limited to specialist centers. In 2026, the FDA approval of Tecentriq with Natera’s Signatera CDx created a new blood-based monitoring channel in muscle-invasive disease, and that pathway is structurally separate from urine-led NMIBC surveillance. This type of approval supports payer acceptance because the test is linked directly to a treatment decision rather than only to diagnostic classification. Established reimbursement also protects incumbents in the bladder cancer detection kits market, since products that already sit inside recognized billing and laboratory frameworks face fewer adoption barriers than newer assays that still need local validation and coverage review. The result is a market where commercial upside is tied not only to analytical performance, but also to how quickly a company can convert evidence into a durable payment pathway.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Dependence on Cystoscopy as Diagnostic Anchor | -1.3% | Global, most pronounced in markets with established urology infrastructure | Long term (≥ 4 years) |

| Limited Clinical Standardization Across Biomarker Panels | -0.8% | Global, strongest in markets requiring centralized HTA approval | Medium term (2-4 years) |

| Reimbursement Variability Across Health Systems | -0.9% | Outside North America, highest variability in South America, Middle East and Africa, and South and Southeast Asia | Long term (≥ 4 years) |

| High Validation Cost for Novel Assays | -0.7% | Global, disproportionately affects emerging biomarker companies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Dependence on Cystoscopy as Diagnostic Anchor

The bladder cancer detection kits market still faces a structural ceiling because the 2025 EAU NMIBC Guidelines state that flexible cystoscopy cannot be replaced by cytology or any other non-invasive test in routine surveillance. That position reflects continued concern over missed detection in patients with multifocal disease or high-grade lesions, where negative predictive value remains under pressure at higher pre-test risk. The commercial effect is that urine markers are often adopted as adjuncts rather than as true substitutes, which limits how much cystoscopy spending can move into kit-based testing. Existing surveillance practice also reinforces itself, because high cystoscopy volumes keep the endoscopic visit at the center of follow-up care and make change slower even when supporting biomarker data improve[2]Jun Ma, “Low-Grade Non-Muscle-Invasive Bladder Cancer, Molecular Landscape, Treatment Strategies and Emerging Therapies,” Nature Reviews Urology, nature.com. The UroFollow trial is important in this setting because it is one of the strongest efforts to produce randomized evidence that could shift future surveillance pathways.

Limited Clinical Standardization Across Biomarker Panels

The bladder cancer detection kits market also remains constrained by the absence of a shared validation standard across urine protein panels, FISH assays, RNA signatures, DNA methylation tests, and emerging cfDNA approaches. This makes evidence harder to compare because each platform uses different analytical methods, specimen handling steps, and clinical endpoints. Without international agreement on minimum sensitivity and specificity thresholds for NMIBC surveillance use, each assay must still build its own body of utility data before guideline endorsement and payer acceptance can broaden. The burden falls more heavily on smaller specialists because long review cycles and repeated study requirements can delay revenue and weaken their position against diversified diagnostics groups. The need for local validation in several Asian markets adds another layer of delay, which slows entry for newer assays even when they perform well in early multicenter studies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Invasive Urine Kits Hold The Lead While Blood-Based Testing Opens A New Growth Channel

Urine-Based Detection Kits held 52.31% of product-type revenue in 2025, giving them the largest share in the bladder cancer detection kits market. Their leading position reflects how closely urine sampling fits the disease biology, since bladder tumors shed cells and biomarkers directly into urine during routine voiding. That specimen advantage gives urine assays a practical role across initial hematuria workups, NMIBC recurrence surveillance, and follow-up after treatment. Tissue-based kits still retain a narrower but stable role in histological confirmation and post-TURBT assessment, while lower-complexity strip formats keep a point-of-care presence in settings with limited molecular laboratory access.

Blood-Based Detection Kits are projected to grow at an 11.38% CAGR from 2026 to 2031, making them the fastest-growing product segment in the bladder cancer detection kits industry. BIOSPACE The growth step changed in May 2026, when the FDA approved Signatera CDx together with Tecentriq for ctDNA MRD-guided adjuvant treatment in post-cystectomy MIBC patients. That decision created oncologist-led blood test demand that is distinct from the urologist-led urine surveillance pathway in NMIBC. The product mix in the bladder cancer detection kits market is therefore becoming broader rather than shifting away from urine, because the two formats are serving different disease stages and clinical decisions.

By Technology: FISH Maintains Scale While Epigenetic Panels Post The Fastest Expansion

FISH Kits commanded 32.24% share of the bladder cancer detection kits market size in 2025, which kept them as the largest technology segment. Their position is supported by Abbott’s UroVysion assay, which remains the only FDA-approved FISH test in the category and sits inside a recognized Medicare molecular pathology framework. FISH also keeps an institutional advantage because community hospital laboratories are already familiar with fluorescence microscopy workflows and can add these tests without the same level of change required for sequencing-based platforms. Immunoassay and broader molecular diagnostic kits remain relevant in the bladder cancer detection kits industry because they address different use cases, from protein-based detection to mutation-focused surveillance in higher-risk patients.

DNA Methylation and RNA Signature Kits are forecast to advance at a 12.52% CAGR from 2026 to 2031, making them the fastest-growing technology group. A prospective study validated a urine Vimentin/POU4F2 methylation panel with 0.935 AUC, 86.44% sensitivity, and 96.08% specificity, while a separate study identified new methylation markers with strong early validation. China is adding commercial weight to that evidence, because its first dual methylation-plus-gene-mutation urothelial carcinoma detection product had reached clinical use by April 2025 and reported 92.5% sensitivity and 95.8% specificity across more than 1,000 cases. As validation improves across multiple settings, the bladder cancer detection kits market is giving epigenetic platforms more room to move from promising specialist tools into routine surveillance and triage pathways.

By End User: Hospitals Keep The Largest Base While Laboratories Build The Fastest Growth Profile

Hospitals and Urology Clinics represented 45.52% of demand in 2025 and held the largest end-user position in the bladder cancer detection kits market. Their lead comes from the fact that cystoscopy still anchors most follow-up encounters, and biomarker ordering often happens in the same patient visit. The urology clinic has become especially important in intermediate-risk hematuria evaluation, where clinicians can use urinary biomarkers to decide whether cystoscopy should proceed immediately or can be deferred. Research institutes still matter in the bladder cancer detection kits industry because they generate validation evidence that later supports payer review and wider clinical adoption.

Diagnostic Laboratories are projected to expand at an 11.25% CAGR from 2026 to 2031, which makes them the fastest-growing end-user segment and gives them a rising role in bladder cancer detection kits market size growth. Centralized laboratories are well suited to cfDNA and methylation testing because they can spread automation and sequencing costs across higher sample throughput. The September 2024 launch of the PAXgene Urine Liquid Biopsy Set by the QIAGEN and BD joint venture shows that suppliers are investing in pre-analytical tools that support urine molecular testing at scale. As more assays move into high-throughput workflows, the bladder cancer detection kits market is likely to reward companies that align assay design with laboratory economics, accreditation requirements, and routine sample logistics.

Geography Analysis

North America held 38.22% of the bladder cancer detection kits market share in 2025 and remains the most established regional base for adjunctive bladder cancer biomarker testing. The region benefits from a dense network of CLIA-certified laboratories, high urologist encounter volumes, and payer structures that can absorb new tests once coverage and coding become clear. The United States drives most of that demand because reimbursement decisions there can quickly widen or narrow access to specific assay formats. The May 2026 approval of Tecentriq with Signatera CDx adds a new commercial path in North America by linking blood-based MRD testing to a defined post-cystectomy treatment decision in muscle-invasive disease.

Europe remains a significant regional pillar in the bladder cancer detection kits market, with Germany standing out for evidence generation and laboratory readiness. The UroFollow trial was conducted across German centers, which shows that the region has the clinical infrastructure needed to test marker-guided surveillance pathways in routine practice. Europe also shapes adoption through guideline influence, since EAU recommendations continue to define how urine markers are used against cystoscopy in NMIBC follow-up. This keeps the region commercially important both as a demand center and as a proving ground for evidence that can support broader payer acceptance later.

Asia-Pacific is the fastest-growing region in the bladder cancer detection kits market and is projected to expand at an 11.65% CAGR through 2031. China is central to that trajectory because it carried 45,114 deaths and 570,636 prevalent bladder cancer cases in 2021, while male incidence is still projected to rise through 2035. The April 2025 launch of China’s first dual methylation-plus-gene-mutation urothelial carcinoma detection product shows that local development is beginning to move alongside local disease burden. Japan adds another layer of demand because its aging population supports recurring surveillance needs and creates a stable patient base for follow-up testing. South America and the Middle East and Africa remain smaller opportunity pools, but the pace of expansion there is still limited by weaker access to centralized molecular laboratories outside major urban centers.

Competitive Landscape

The bladder cancer detection kits market shows a moderately fragmented competitive structure, with several large diagnostics groups holding durable positions while specialist firms compete through narrower assay portfolios and urology-focused channels. Abbott, Roche, Siemens Healthineers, Becton Dickinson, and Danaher benefit from scale, installed laboratory relationships, and stronger ability to work through reimbursement and compliance requirements. Abbott’s UroVysion remains especially well placed because it is the only FDA-cleared FISH assay in this category with a clear Medicare coverage anchor. That kind of position gives larger companies a steadier footing in the bladder cancer detection kits market even when newer technologies attract attention.

Specialist players are still shaping competition because innovation in urine methylation, multiplex biomarker panels, and hematuria triage has not been fully absorbed by the large incumbents. Photocure’s June 2026 acquisition of Vesica Health for USD 30.5 million is a clear example, because it added AssureMDx, a urine-based molecular hematuria detection test with AUA guideline inclusion, Breakthrough Device Designation, and an AMA PLA billing code[3]Photocure ASA, “Photocure ASA to Acquire Vesica Health Inc., Strengthening Leadership in Bladder Cancer Diagnostics,” Photocure, photocure.com. Another strategic move came from the QIAGEN and BD joint venture, which launched the PAXgene Urine Liquid Biopsy Set in September 2024 to support reliable urine cfDNA analysis across qPCR, digital PCR, and NGS workflows. A third move came through the May 2026 Tecentriq and Signatera CDx approval, which pulled bladder cancer testing deeper into treatment-linked companion diagnostics and expanded the role of blood-based monitoring. These actions show that competition in the bladder cancer detection kits market is being shaped by platform expansion, targeted acquisitions, and tighter links between diagnostics and therapy.

Competitive pressure remains high because single-assay specialists still face payer uncertainty and long evidence cycles before adoption becomes broad. The most open white space remains in low- and intermediate-risk NMIBC surveillance, where strong evidence exists for marker-assisted follow-up but no single commercial pathway has closed the case for full cystoscopy replacement. Point-of-care and clinic-friendly risk stratification formats are another open area, because they could shift part of the diagnostic workflow away from hospital-centered testing without needing every patient to enter a centralized molecular laboratory pathway. This leaves the bladder cancer detection kits market open to further consolidation, especially if smaller innovators secure strong clinical data but still need larger commercial partners to scale reimbursement and distribution.

Bladder Cancer Detection Kits Industry Leaders

F. Hoffmann-La Roche Ltd

Abbott

Sysmex Corporation

Thermo Fisher Scientific Inc.

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Veracyte's TrueMRD Monitoring Test for muscle-invasive bladder cancer, covered by Medicare since May 2026, is made available to clinicians. The PAGER study showed TrueMRD detected MIBC recurrence 131 days earlier than imaging in 112 patients, making it a valuable surveillance tool.

- May 2026: The FDA approved Roche/Genentech's Tecentriq and Natera's Signatera CDx, the first ctDNA-guided cancer treatment globally, for post-cystectomy MIBC patients. The IMvigor011 Phase III trial reported a 36% lower risk of recurrence or death and a 41% drop in mortality for ctDNA-positive patients. This approval requires regular ctDNA testing and opens new opportunities for blood-based bladder cancer diagnostics.

Global Bladder Cancer Detection Kits Market Report Scope

As per the scope of the report, bladder cancer detection kits are diagnostic tools designed to identify the presence of bladder cancer cells or related biomarkers in urine or tissue samples. These kits typically use techniques such as urine cytology, molecular markers, or immunoassays to detect abnormal cells or specific substances associated with bladder cancer, aiding in early diagnosis and monitoring of the disease.

The segmentation of the bladder cancer detection kits market is categorized by product type, technology, end user, and geography. By product type, the market includes urine-based detection kits, blood-based detection kits, tissue-based detection kits, and other product types. By technology, it is segmented into fluorescence in situ hybridization kits, immunoassay kits, molecular diagnostic kits, DNA methylation and RNA signature kits, and other technologies. By end user, the market is divided into hospitals and urology clinics, diagnostic laboratories, cancer research institutes, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Urine-Based Detection Kits |

| Blood-Based Detection Kits |

| Tissue-Based Detection Kits |

| Other Product Types |

| Fluorescence In Situ Hybridization Kits |

| Immunoassay Kits |

| Molecular Diagnostic Kits |

| DNA Methylation and RNA Signature Kits |

| Other Technologies |

| Hospitals and Urology Clinics |

| Diagnostic Laboratories |

| Cancer Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Urine-Based Detection Kits | |

| Blood-Based Detection Kits | ||

| Tissue-Based Detection Kits | ||

| Other Product Types | ||

| By Technology | Fluorescence In Situ Hybridization Kits | |

| Immunoassay Kits | ||

| Molecular Diagnostic Kits | ||

| DNA Methylation and RNA Signature Kits | ||

| Other Technologies | ||

| By End User | Hospitals and Urology Clinics | |

| Diagnostic Laboratories | ||

| Cancer Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of bladder cancer detection kits in 2026?

The bladder cancer detection kits market size stands at USD 1.08 billion in 2026 and is forecast to reach USD 1.67 billion by 2031 at a 9.25% CAGR.

Which product category leads bladder cancer testing demand?

Urine-Based Detection Kits held 52.31% of product-type revenue in 2025 because urine remains the most practical specimen across hematuria workups and NMIBC surveillance.

Which technology is growing the fastest in bladder cancer diagnostics?

DNA Methylation and RNA Signature Kits are forecast to grow at a 12.52% CAGR through 2031, supported by strong multicenter validation and expanding clinical use.

Why are blood-based kits gaining attention after 2026?

Blood-Based Detection Kits are projected to grow at an 11.38% CAGR through 2031 because the May 2026 approval of Signatera CDx with Tecentriq created a treatment-linked ctDNA monitoring pathway in post-cystectomy MIBC.

Which region has the strongest growth outlook through 2031?

Asia-Pacific is the fastest-growing region with an 11.65% CAGR through 2031, supported by rising disease burden in China and the emergence of locally approved molecular testing products.

What is the main barrier to wider replacement of cystoscopy?

The key barrier is that the 2025 EAU guidelines still state that cystoscopy cannot be replaced by cytology or any other non-invasive test in routine NMIBC surveillance, which keeps biomarkers in an adjunct role in many settings.

Page last updated on: