Lung Cancer Liquid Biopsy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

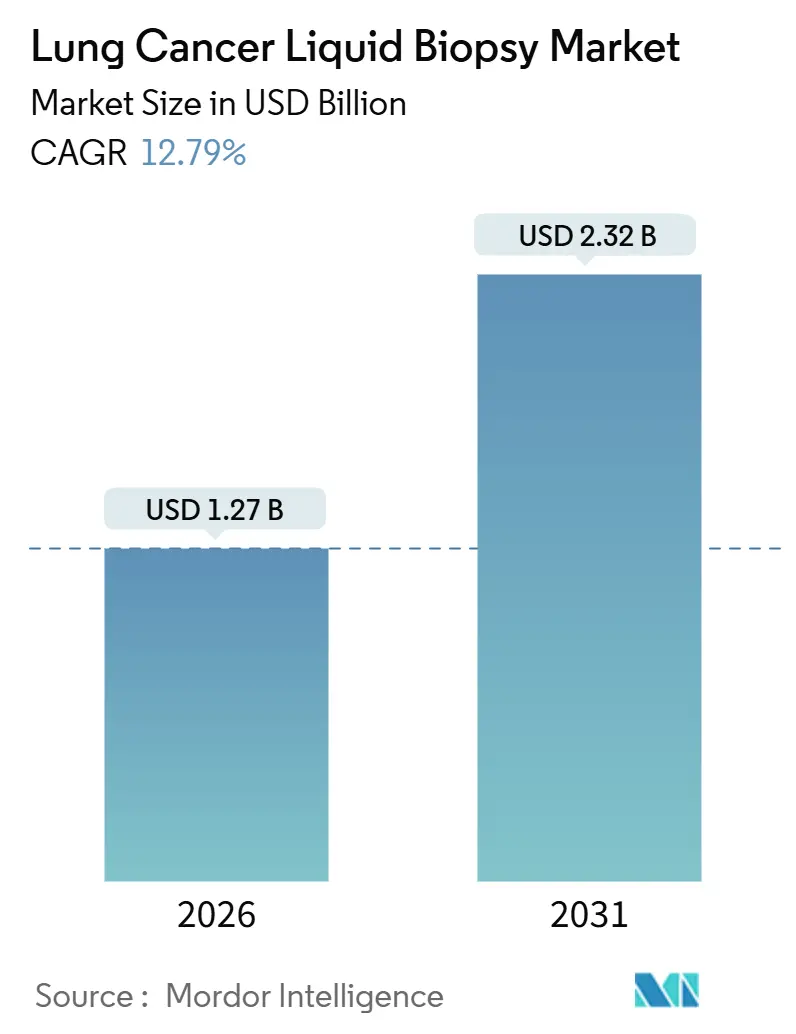

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 12.79% CAGR |

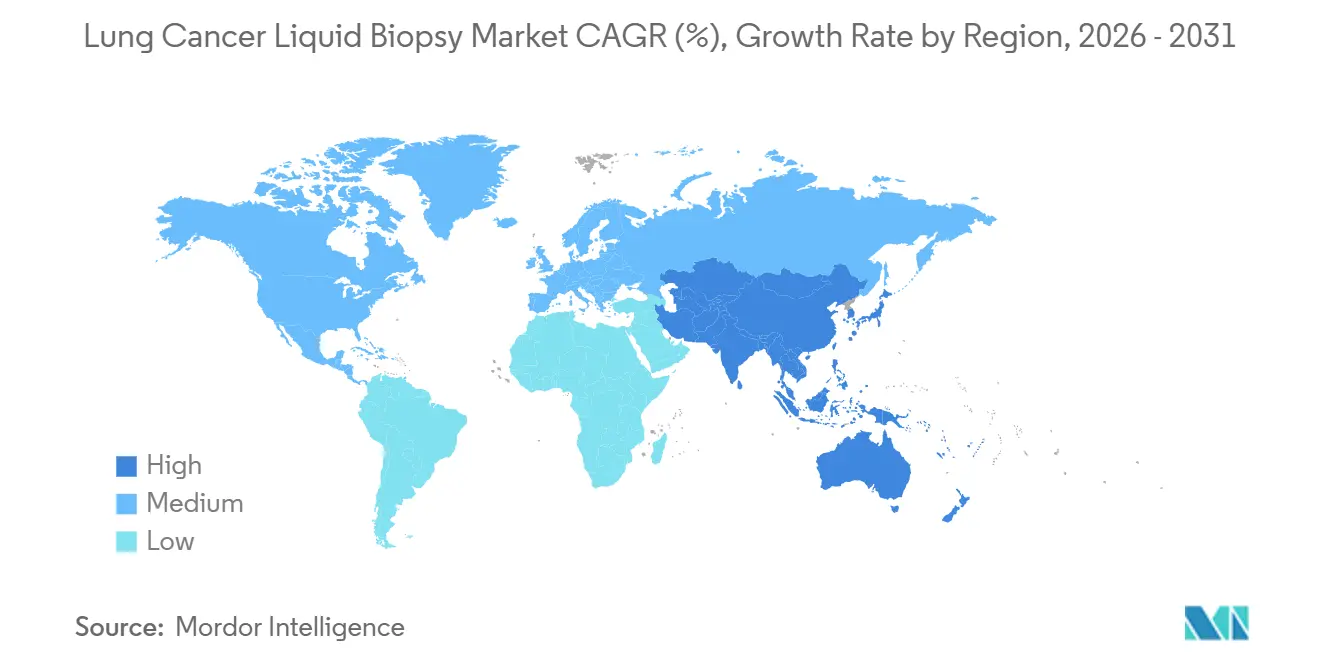

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lung Cancer Liquid Biopsy Market Analysis by Mordor Intelligence

The lung cancer liquid biopsy market size is anticipated to reach USD 1.27 billion in 2026 and USD 2.32 billion by 2031, at a 12.79% CAGR, underscoring how regulatory clarity, broader reimbursement, and robust clinical validation have made blood-based genomic profiling a frontline diagnostic option. Clinical guideline upgrades, rising disease incidence, and pharmaceutical demand for molecular monitoring keep test volumes climbing, while multi-analyte innovation attracts new investors despite lingering analytical-sensitivity gaps. Vendors with FDA-cleared assays enjoy early-mover advantages as Medicare payment now anchors commercial pricing, and health-system laboratories are internalizing workflows to protect margin. Competitive rivalry centers on securing pharma co-development deals and on building datasets large enough to power machine-learning algorithms that refine biomarker interpretation. Asia-Pacific is emerging as the fastest-growing region thanks to recent reimbursement decisions by China and Japan, even though North America still commands the largest share of global revenue.

Key Report Takeaways

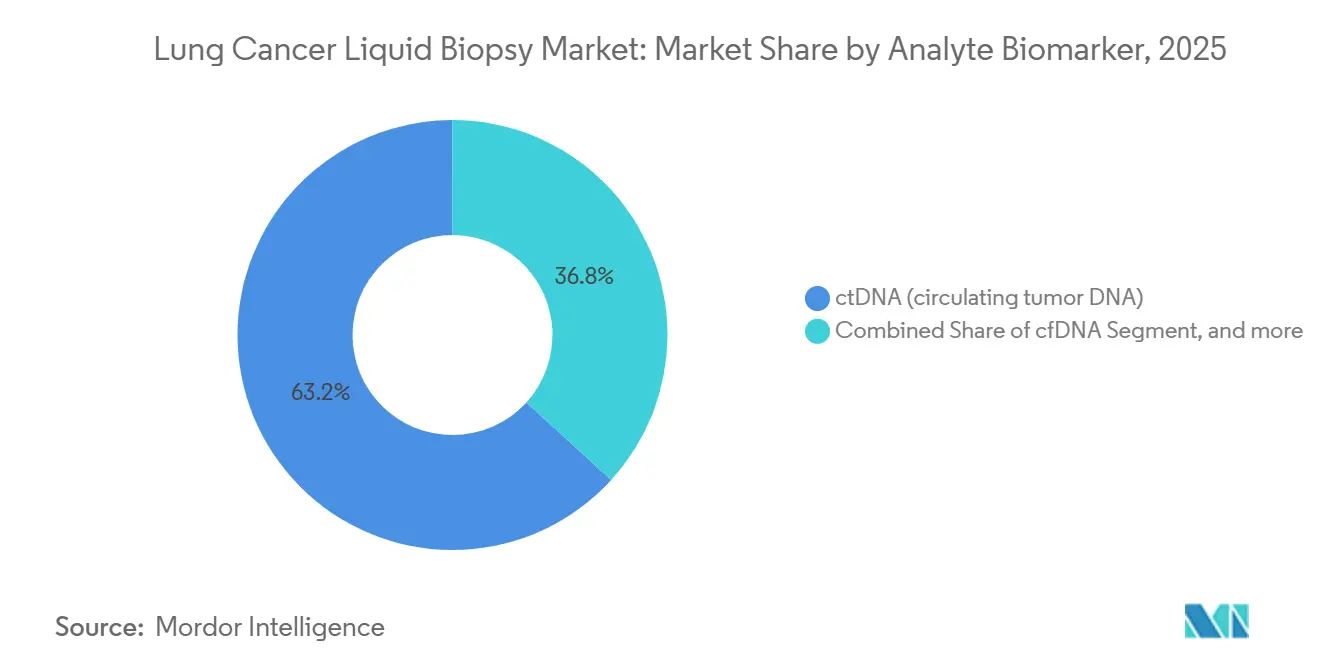

- By analyte, circulating tumor DNA held 63.23% of the lung cancer liquid biopsy market share in 2025, while exosomes and extracellular vesicles are forecast to expand at a 14.54% CAGR through 2031.

- By technology, next-generation sequencing accounted for 54.32% of 2025 revenue, whereas fragmentomics and methylation analytics are expected to post a 14.22% CAGR through 2031.

- By clinical use case, therapy selection led with 41.54% of revenue in 2025; minimal residual disease surveillance is projected to grow at a 14.88% CAGR through 2031.

- By subtype, non-small cell disease accounted for 82.45% of 2025 test volume, but small cell disease is set to grow at a 14.67% CAGR by 2031.

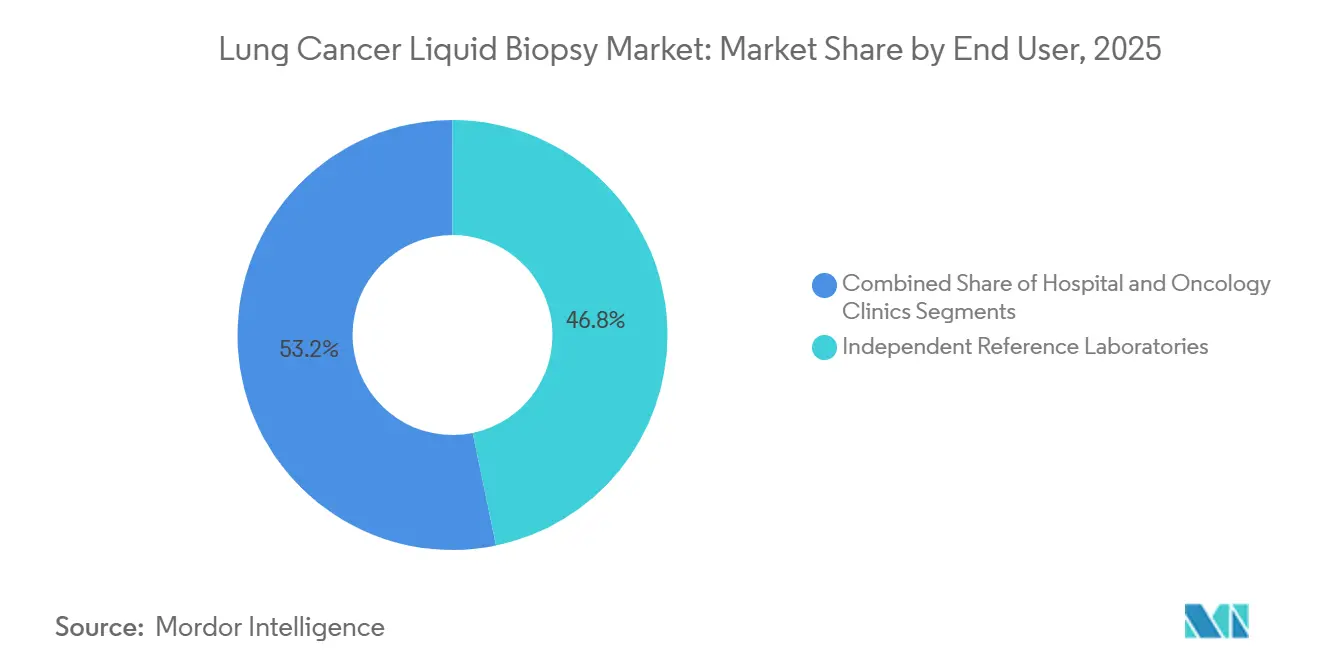

- By end user, independent reference laboratories accounted for 46.76% of 2025 revenue; hospital laboratories are forecast to expand at a 15.43% CAGR through 2031.

- By specimen, plasma accounted for 78.65% of 2025 samples; serum is anticipated to rise at a 15.11% CAGR thanks to legacy biobank access.

- By geography, North America captured 43.56% of 2025 sales, whereas Asia-Pacific is predicted to accelerate at a 13.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lung Cancer Liquid Biopsy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and clinical guideline endorsements for liquid biopsy in lung cancer | +2.8% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Expansion of reimbursement coverage for liquid biopsy-based genomic profiling | +2.5% | North America, selective EU markets (Germany, UK, France), emerging in APAC | Short term (≤ 2 years) |

| Rising incidence of lung cancer and growing preference for minimally invasive diagnostics | +2.1% | Global, with highest absolute growth in APAC (China, India) and aging populations in North America and Europe | Long term (≥ 4 years) |

| Continued launch of targeted and immuno-oncology therapies requiring molecular monitoring | +2.3% | Global, with fastest uptake in North America and EU due to drug approval timelines | Medium term (2-4 years) |

| Integration of liquid biopsy into multicancer early detection pilots | +1.6% | North America and UK (NHS-Galleri), exploratory in APAC | Long term (≥ 4 years) |

| Adoption of ultra-sensitive minimal residual disease assays in surgical lung cancer pathways | +1.5% | North America and Western Europe, with academic centers leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory and Clinical Guideline Endorsements for Liquid Biopsy in Lung Cancer

Publication of the FDA draft guidance in November 2024 set explicit analytic validity thresholds for circulating tumor DNA minimal residual disease assays, catalyzing investment in ultra-deep sequencing platforms. ASCO’s 2024 living guideline and NCCN’s version 4.2024 now recommend comprehensive blood-based genomic profiling when tissue is inadequate, expanding the eligible patient pool by 20-30%[1]American Society of Clinical Oncology, “Living Guideline v2024.3,” asco.org. ESMO’s 2024 consensus statements added plasma testing for resistance-mechanism identification after targeted therapy failure, reinforcing payer confidence across Europe. Collectively, these endorsements normalize liquid biopsy as standard of care, reduce payer push-back, and shorten hospital committee approval cycles.

Expansion of Reimbursement Coverage for Liquid Biopsy-Based Genomic Profiling

CMS in 2025 placed Guardant360 CDx at USD 5,000, FoundationOne Liquid CDx at USD 3,500, and Signatera at USD 3,500 on its Advanced Diagnostic Laboratory Test list, instantly setting a de facto national floor for commercial insurers. Germany, the United Kingdom, and France followed with procedure codes that reimburse plasma testing when tissue biopsy is contraindicated, raising European access by 10-15% in one year. Japan’s health insurance system began covering liquid biopsy for high-risk tissue sampling, boosting domestic uptake despite historically conservative coverage policies. These moves improve vendor cash flow visibility and prompt hospital laboratories to invest in on-site sequencing infrastructure.

Rising Incidence of Lung Cancer and Growing Preference for Minimally Invasive Diagnostics

GLOBOCAN projects global lung-cancer incidence will rise from 2.48 million cases in 2022 to 4.62 million by 2050, a demographic wave that expands the testing addressable market. High pneumothorax rates associated with transthoracic biopsy drive patient and physician preference toward blood draws, reducing median diagnostic turnaround time from 24 days to under 10 days in a U.S. community oncology practice. Surveys in 2024 show 78% of advanced-stage patients would choose a blood test over re-biopsy when accuracy is equivalent. This persistent demand supports double-digit growth even if payer policy fluctuates.

Continued Launch of Targeted and Immuno-Oncology Therapies Requiring Molecular Monitoring

Eight novel targeted regimens approved between 2024-2026 depend on accurate mutation status, propelling serial liquid-biopsy orders throughout a patient’s therapy arc. Plasma monitoring detects resistance mechanisms such as C797S and MET amplification months before imaging progression, guiding timely second-line treatments and reinforcing clinical utility. Pharma trials embed circulating tumor DNA endpoints to accelerate drug registration, adding thousands of research samples annually and anchoring vendor-pharma alliances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Analytical sensitivity limitations in early-stage disease and low tumor shedding | -1.4% | Global, particularly impacting screening and MRD applications | Medium term (2-4 years) |

| Inconsistent global reimbursement policies for screening and MRD applications | -1.2% | Global, with highest impact in APAC and Latin America; selective EU markets | Short term (≤ 2 years) |

| Need for complementary tissue biopsy to capture non-DNA biomarkers | -0.8% | Global, affecting immunotherapy selection workflows | Long term (≥ 4 years) |

| Emerging laboratory regulation increasing compliance costs for smaller service providers | -0.6% | EU (IVDR), United States (FDA LDT rule), selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Analytical Sensitivity Limitations in Early-Stage Disease and Low Tumor Shedding

Stage I detection rates hover at 50-70%, well below those of radiologic modalities, due to variant-allele fractions below the 0.05% assay threshold[2]Nature Reviews Clinical Oncology, “ctDNA Sensitivity in Early Lung Cancer,” nature.com. Shedding heterogeneity, clonal hematopoiesis artifacts, and pre-analytical inconsistencies further erode accuracy, so clinicians still prioritize tissue confirmation to avoid false reassurance. Vendors are countering with molecular barcoding chemistries that reduce limits of detection to 0.01%, but broad validation remains a work in progress.

Inconsistent Global Reimbursement Policies for Screening and MRD Applications

CMS’s refusal to cover multicancer early detection and its stance on minimal residual disease in evidence development create revenue bottlenecks in the United States. Elsewhere, coverage differs by province or insurer, compelling vendors to mount dozens of country-level health-economic dossiers and delaying scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Analyte: Exosome Uptake Strengthens Beyond ctDNA Dominance

The lung cancer liquid biopsy market size for circulating tumor DNA commands the lion’s share, but exosome-based assays are expanding the fastest, growing at a 14.54% CAGR as investigators leverage cell-free RNA and protein cargo to illuminate resistance mechanisms. Vendors such as Exosome Diagnostics and academic spin-outs are aligning with pharma partners to validate exosomal programmed death-ligand 1 expression, addressing the tissue-complementary gap. Although exosome workflows require ultracentrifugation or immuno-capture steps that lengthen processing, automated microfluidic kits launched in 2026 promise to cut hands-on time by half, encouraging hospital adoption. The lung cancer liquid biopsy market is therefore likely to evolve toward dual-analyte panels that couple ctDNA mutations with exosomal RNA for a richer biological context.

By Technology: Fragmentomics Challenges Next-Generation Sequencing

Next-generation sequencing dominated 54.32% of 2025 revenue, yet fragmentomics and methylation analytics are surging at a 14.22% CAGR. These low-coverage assays trim sequencing depth by 20x, enabling 80-90% cost cuts and same-week turnaround, appealing to budget-sensitive health systems in Latin America and Southeast Asia. Illumina’s NovaSeq X compatibility has prompted tertiary hospitals to internalize 500-gene ctDNA panels and retain billing margin. Conversely, the polymerase chain reaction and droplet-digital polymerase chain reaction segments continue to shrink as clinical guidelines shift away from single-gene reflex testing.

By Clinical Use Case: MRD Surveillance Tops Growth Tables

Therapy-selection testing led to 2025 revenue of 41.54%, but minimal residual disease surveillance is rising fastest at a 14.88% CAGR, as trials show that post-operative circulating tumor DNA status predicts benefit from adjuvant immunotherapy. Real-time resistance monitoring during targeted therapy extends assay cadence to every 6–8 weeks across an entire treatment continuum, effectively doubling per-patient lifetime test counts. Early detection and screening remain exploratory until CMS reverses its coverage stance, yet results from the SUMMIT cohort in 2028 could unlock a vast new population of risk-screened individuals.

By Cancer Subtype: Small Cell Momentum Emerges

Non-small cell histologies represented 82.45% of the 2025 volume, but small cell cases will show a market-leading 14.67% CAGR through 2031. Rapid tumor doubling and high shedding make small cell disease ideally suited to liquid biopsy for real-time chemotherapy response tracking, even though actionable mutations remain scarce. DLL3-targeted conjugates and PARP inhibitors under development may soon tie drug eligibility to plasma biomarkers, further boosting small-cell test demand.

By End User: Hospitals Repatriate Testing for Speed and Margin

Independent reference laboratories still account for 46.76% of 2025 revenue, but hospital labs are expanding at a 15.43% CAGR as capital budgets fund NovaSeq X and TSO500-ctDNA setups. Academic centers seek to cut report turnaround time to under 7 days, improving the precision of therapy initiation during first-line treatment windows. Community hospitals lacking test volume continue to outsource, thereby sustaining reference-lab-scale economics in the medium term.

By Specimen: Serum Revival Driven by Legacy Biobanks

Plasma captured 78.65% of 2025 samples on the back of Streck and PAXgene stabilization tubes, yet serum is growing at 15.11% CAGR as researchers unlock two-decade serum archives to validate fragmentomics signatures. Vendors now market extraction kits optimized for degraded serum DNA, positioning the format for retrospective discovery and low-resource clinical settings.

Geography Analysis

North America led the lung cancer liquid biopsy market with a 43.56% revenue contribution in 2025 as Medicare payment cemented commercial price floors and fifteen of the top twenty vendors based their operations in the United States. Vendor–pharma collaborations, a mature clinical-trial ecosystem, and hospital investment in onsite sequencing sustain double-digit domestic growth despite payer limits on screening coverage.

Europe exhibits mixed momentum; Germany, the United Kingdom, and France now reimburse plasma testing for advanced disease, but divergent coding policies fragment adoption across other member states. The lung cancer liquid biopsy market size for leading European laboratories remains tethered to therapy-selection cases while IVDR compliance costs delay the launch of innovative assays.

Asia-Pacific is the fastest-growing region at a 13.45% CAGR to 2031. China’s National Medical Products Administration approval of multiple ctDNA panels and provincial pilot reimbursement boost domestic uptake, while Japan’s insurers cover liquid biopsy when tissue sampling risks complications. Local champions Burning Rock and Singlera replicate Guardant’s and Natera’s business models at lower price points, accelerating penetration into tier-2 Chinese hospitals.

Competitive Landscape

Three vendors—Guardant Health, Foundation Medicine, and Natera—collectively control roughly 60% of U.S. revenue, placing the global structure in the moderately consolidated band. Each company aligns with pharma sponsors to integrate circulating tumor DNA endpoints into registrational trials, locking in predictable sample flow and strengthening evidence dossiers. Mergers and partnerships, such as Roche’s backing of Foundation Medicine and Guardant’s vertical expansion into colorectal screening, illustrate a playbook of portfolio diversification that amortizes sequencing infrastructure across multiple oncologic indications.

Fragmentomics specialists Delfi Diagnostics and Singlera are disrupting on price, delivering early-stage sensitivity near mutation-based next-generation sequencing at half the cost, a value proposition that resonates across emerging markets. Heightened regulatory rigor under EU IVDR and the pending FDA Laboratory Developed Test rule raises the bar for analytical validation, favoring well-capitalized incumbents able to fund USD 0.5–2 million per assay in compliance. Competitive focus therefore shifts toward multi-analyte fusion, data-science differentiation, and rapid result delivery that compresses oncologist decision cycles.

Lung Cancer Liquid Biopsy Industry Leaders

Guardant Health

F. Hoffmann-La Roche AG

Thermo Fisher Scientific

Natera

Illumina, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The Cancer Research Institute enrolled the first patient in the second stage of BR.36 (NCT04093167), a Phase 2/3 clinical trial using circulating tumor DNA (ctDNA) to measure early responses to immunotherapy and guide treatment decisions for patients with advanced lung cancer.

- June 2025: M42, AstraZeneca, and SOPHiA GENETICS launched a UAE Liquid Biopsy Initiative. This collaboration aims to revolutionize cancer diagnosis and treatment through advanced liquid biopsy technology. The initiative is expected to enhance personalized cancer care in the UAE.

- May 2025: The NHS became the first in the world to introduce a groundbreaking 'liquid biopsy' blood test for cancer patients. This test enables faster access to targeted therapy for lung and breast cancer, potentially up to two weeks earlier. It also helps some patients avoid additional tests and treatments like chemotherapy.

Global Lung Cancer Liquid Biopsy Market Report Scope

As per the scope of the report, lung cancer liquid biopsy is a minimally invasive test that detects cancer-related genetic mutations and biomarkers in a patient's blood or other body fluids. It provides real-time information about tumor genetics without the need for tissue biopsy. This method helps in early detection, monitoring treatment response, and identifying targeted therapy options.

The Lung Cancer Liquid Biopsy Market is Segmented by Analyte/Biomarker (ctDNA, cfDNA, CTCs, Exosomes/Extracellular Vesicles/cfRNA, and Methylation/Fragmentomics Signatures), Technology/Method (NGS-based CGP, PCR/ddPCR, BEAMing/Hybrid Methods, and Fragmentomics/Methylation Analytics), Clinical Use Case (Therapy Selection, Treatment-Response Monitoring, MRD/Recurrence Surveillance, and Early Detection/Screening), Cancer Subtype (NSCLC and SCLC), End User (Independent Reference Laboratories, Hospital, and Oncology Clinics), Specimen Type (Plasma, Serum, and Other Specimen Types), and Geography (North America, South America, Europe, APAC, and Middle East & Africa). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| ctDNA |

| cfDNA |

| CTCs |

| Exosomes / Extracellular Vesicles / cfRNA |

| Methylation / Fragmentomics Signatures |

| NGS-based CGP |

| PCR / ddPCR |

| BEAMing / hybrid methods |

| Fragmentomics / methylation analytics |

| Therapy Selection |

| Treatment-response Monitoring |

| MRD / Recurrence Surveillance |

| Early Detection / Screening |

| NSCLC | Adenocarcinoma |

| Squamous Cell Carcinoma | |

| SCLC |

| Independent Reference Laboratories |

| Hospital |

| Oncology Clinics |

| Plasma |

| Serum |

| Other Specimen Types |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Analyte / Biomarker | ctDNA | |

| cfDNA | ||

| CTCs | ||

| Exosomes / Extracellular Vesicles / cfRNA | ||

| Methylation / Fragmentomics Signatures | ||

| By Technology / Method | NGS-based CGP | |

| PCR / ddPCR | ||

| BEAMing / hybrid methods | ||

| Fragmentomics / methylation analytics | ||

| By Clinical Use Case | Therapy Selection | |

| Treatment-response Monitoring | ||

| MRD / Recurrence Surveillance | ||

| Early Detection / Screening | ||

| By Cancer Subtype | NSCLC | Adenocarcinoma |

| Squamous Cell Carcinoma | ||

| SCLC | ||

| By End User | Independent Reference Laboratories | |

| Hospital | ||

| Oncology Clinics | ||

| By Specimen Type | Plasma | |

| Serum | ||

| Other Specimen Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the lung cancer liquid biopsy market and how fast is it growing?

The lung cancer liquid biopsy market size is USD 1.27 billion in 2026 and is projected to reach USD 2.32 billion by 2031, expanding at a 12.79% CAGR.

What is a liquid biopsy for lung cancer?

A liquid biopsy is a blood test that detects tumor-derived DNA or other biomarkers, offering a minimally invasive way to profile mutations, monitor treatment response, and check for residual disease.

How accurate are plasma tests compared with tissue biopsy in advanced disease?

For stage III-IV non-small cell lung cancer, FDA-cleared circulating tumor DNA panels report analytical sensitivities above 99% when variant allele fractions exceed 0.5%, making them clinically interchangeable with tissue genomic profiling in most cases.

Which regulatory actions have recently boosted adoption?

November 2024 FDA draft guidance defined analytic-validity standards for minimal residual disease assays, and CMS in 2025 set national payment rates up to USD 5,000, prompting rapid payer alignment.

What patient groups gain the most benefit today?

Individuals with advanced or metastatic lung cancer whose tissue samples are insufficient, and postoperative patients being monitored for minimal residual disease, derive the clearest clinical value.

How much does a Medicare-reimbursed liquid biopsy cost in the United States?

Current CMS rates are USD 5,000 for Guardant360 CDx and USD 3,500 each for FoundationOne Liquid CDx and Signatera.

Who are the leading suppliers of FDA-cleared lung cancer liquid biopsy tests?

Guardant Health, Foundation Medicine (Roche), and Natera together account for roughly 60% of U.S. testing revenue, making them the dominant providers.

Page last updated on: