U.S. Colorectal Cancer Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

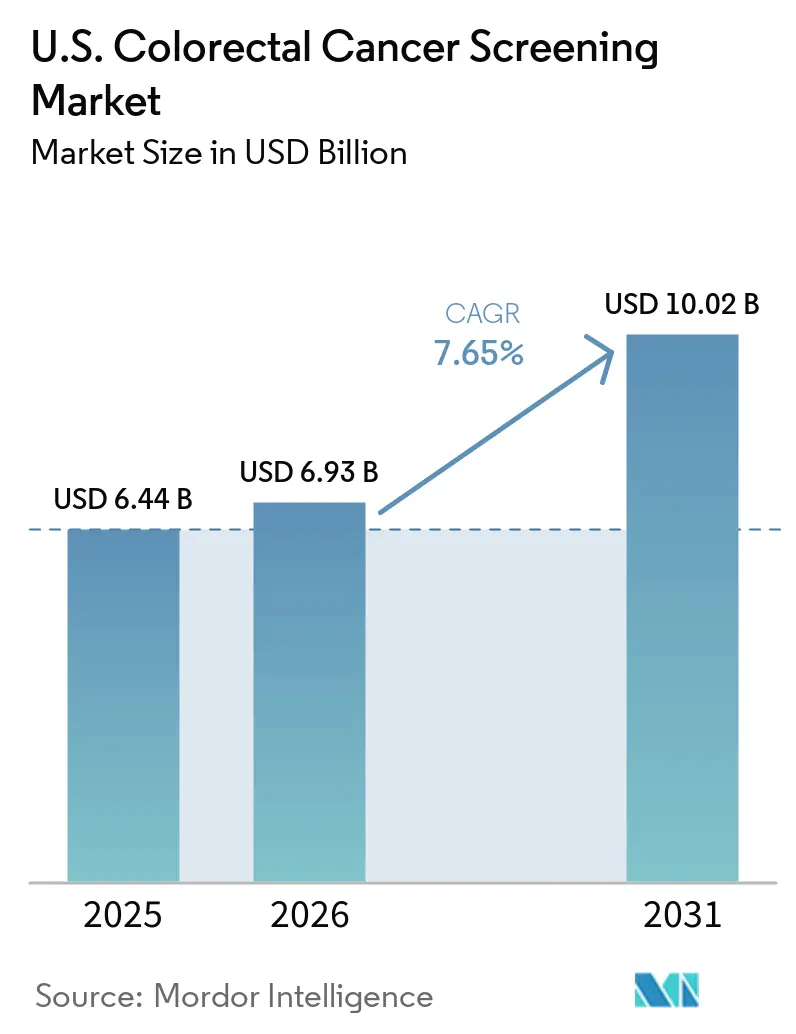

| Base Year Market Size (2025) | USD 6.44 Billion |

| Market Size (2026) | USD 6.93 Billion |

| Market Size (2031) | USD 10.02 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

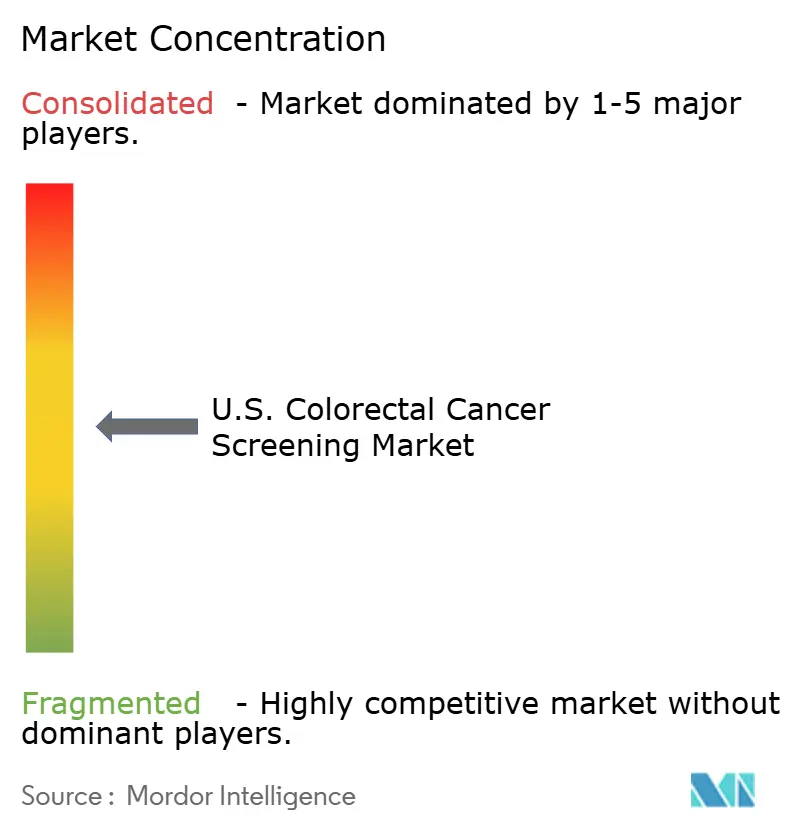

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Colorectal Cancer Screening Market Analysis by Mordor Intelligence

The U.S. Colorectal Cancer Screening Market size was valued at USD 6.44 billion in 2025 and is estimated to grow from USD 6.93 billion in 2026 to reach USD 10.02 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031).

The addressable patient pool has expanded significantly as screenings now begin earlier for average-risk adults. Screenings for adults aged 45-49 increased by 62% between 2019 and 2024, highlighting the steady addition of new eligible patients to the system.[1]American Cancer Society, “Early Diagnosis Surge for Colorectal Cancer,” American Cancer Society Press Room, pressroom.cancer.org The United States colorectal cancer screening market is undergoing transformation, driven by the FDA's 2024 approval of the first blood-based primary screening test and the American Cancer Society's 2026 guideline updates, which incorporated blood-based and advanced at-home stool testing options. This shift is fostering consolidation among leading players while creating opportunities for developers focused on improving completion rates, lesion detection, and payer acceptance.

Key Report Takeaways

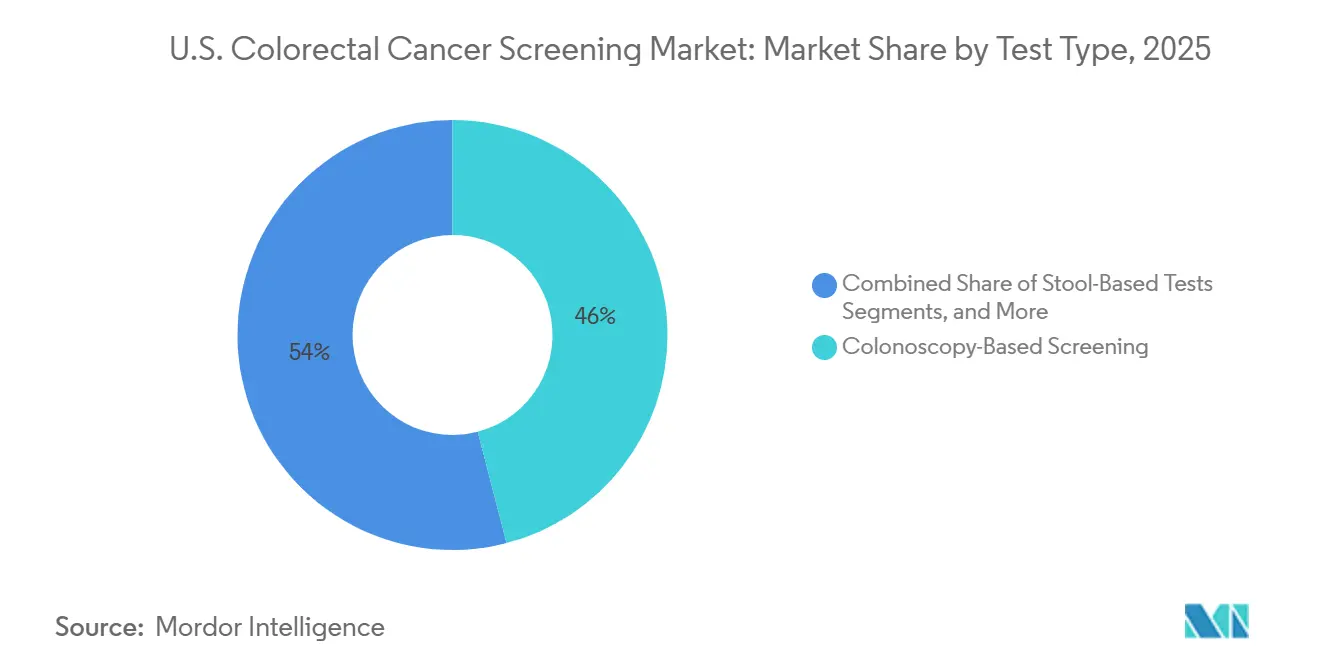

- By test type, colonoscopy-based screening held 45.95% of the U.S. colorectal cancer screening market share in 2025, while stool-based tests are forecasted to expand at a 9.65% CAGR through 2031.

- By technology, FIT and gFOBT accounted for 32.65% of the U.S. colorectal cancer screening market size in 2025, while cell-free DNA and methylation-based assays are projected to grow at an 8.55% CAGR during 2026-2031.

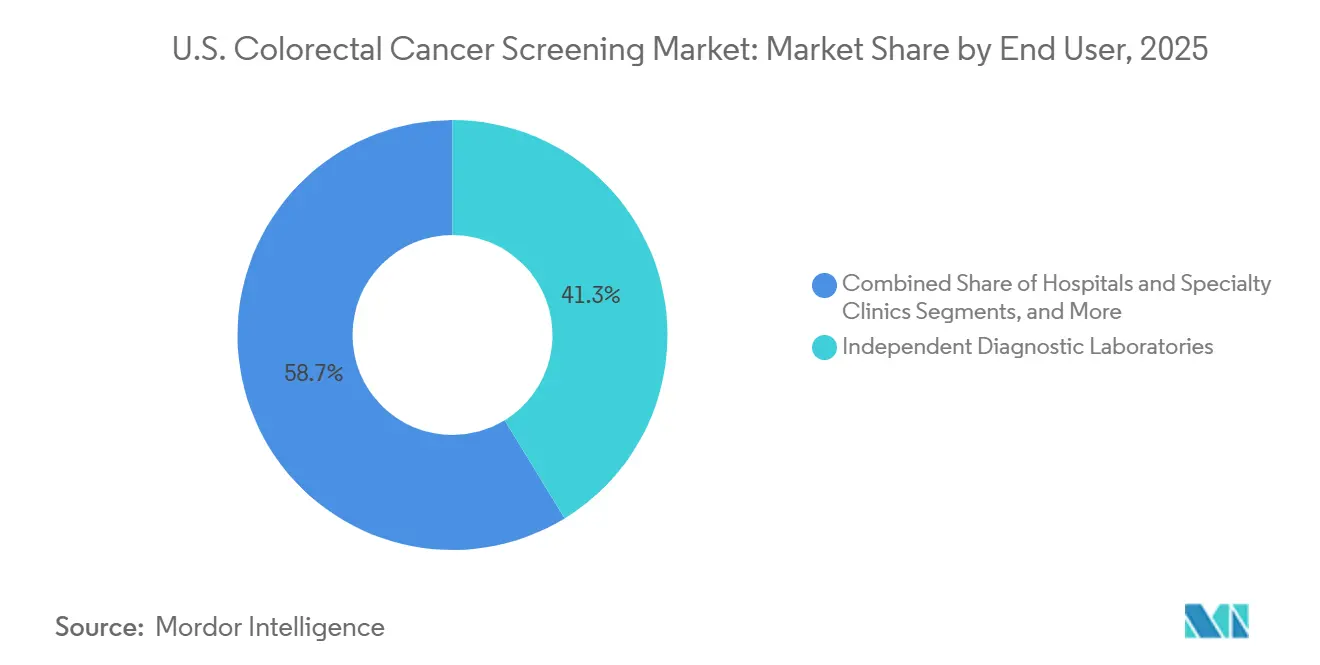

- By end user, independent diagnostic laboratories held 41.25% share in 2025, while hospitals and specialty clinics are expected to record the fastest growth at an 8.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Colorectal Cancer Screening Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increased screening eligibility after age 45 expansion | +2.0% | National, with early gains in states with high Medicaid expansion coverage, including California, New York, and Florida | Short term (≤ 2 years) |

| Rising adoption of non-invasive screening pathways | +1.7% | National, with accelerated uptake in rural and underserved areas across the South and Midwest | Short term (≤ 2 years), Medium term (2-4 years) |

| Payer preference for earlier detection and lower downstream treatment costs | +1.2% | National, strongest in Medicare Advantage and value-based care networks | Medium term (2-4 years) |

| FDA-backed innovation in blood-based and stool RNA testing | +1.3% | National, with concentrated uptake in states with broad guideline adherence | Medium term (2-4 years) |

| CMS and commercial coverage broadening for approved tests | +1.4% | National, with near-term concentration among Medicare Part B beneficiaries aged 45-85 | Short term (≤ 2 years), Medium term (2-4 years) |

| Primary care workflow shift toward at-home screening completion | +0.8% | National, with stronger effect in high-volume primary care markets such as Texas, California, and New York | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Screening Eligibility After Age 45 Expansion

The expansion of routine screening to include individuals aged 45-49 has significantly increased the eligible population in the United States colorectal cancer screening market. Between 2019 and 2024, screenings for this age group rose by 62%, with their share of total screenings increasing from 2.9% to 17.8%. Monthly screenings for ages 45-49 surged by 955%, compared to a 46% rise for adults aged 50-75.[2]American Cancer Society, “American Cancer Society Updates Colorectal Cancer Screening Guideline, Major Changes Emphasize Blood-Based and At-Home Stool Testing,” PRNewswire, prnewswire.com This younger demographic, largely employed and commercially insured, enhances reimbursement quality across test categories. Despite this growth, screening penetration for ages 45-49 remains below older adults, leaving room for further market expansion. Colorectal cancer is now the leading cancer killer in men under 50 and the second in women under 50, driving early detection efforts through employer plans and awareness programs.

Rising Adoption of Non-Invasive Screening Pathways

The shift toward non-invasive testing is transforming the United States colorectal cancer screening market by prioritizing access and completion. Stool-based testing has gained widespread acceptance, with Exact Sciences reporting over 20 million cumulative uses of Cologuard and Cologuard Plus, generating USD 2.53 billion in screening revenue for 2025, a 20.2% year-over-year increase. Cologuard Plus reduced false positives by nearly 40%, improving clinical workflows and reducing follow-up burdens.[3]Exact Sciences Corporation, “Exact Sciences Announces Record Fourth Quarter and Full Year 2025 Results,” BusinessWire, businesswire.com At-home sample collection addresses barriers like scheduling and travel, giving vendors with streamlined logistics a competitive edge. As non-invasive adoption grows, effective follow-up management becomes critical to ensure positive patients proceed to confirmatory colonoscopy.

FDA-Backed Innovation in Blood-Based and Stool RNA Testing

Regulatory approvals are driving innovation in the United States colorectal cancer screening market. The FDA approved Guardant Health’s Shield in July 2024, the first blood-based test for primary colorectal cancer screening, setting a benchmark for future entrants. Geneoscopy’s ColoSense, the first FDA-approved noninvasive multi-target stool RNA test, expanded screening options beyond FIT, gFOBT, DNA-only stool testing, and colonoscopy. Freenome’s SimpleScreen CRC, submitted to the FDA in August 2025, and Abbott’s entry into stool and blood-based screening further diversify the market. Innovation now focuses on molecular approaches that enhance adoption and clinical credibility.

CMS and Commercial Coverage Broadening for Approved Tests

Coverage policies are accelerating growth in the United States colorectal cancer screening market by enabling newer tests to scale. Medicare began covering CT colonography as a screening option effective January 1, 2025, offering once-every-60-month coverage for average-risk patients aged 45 and older and once-every-24-month coverage for high-risk patients. Broader coverage supports early detection, reduces treatment burdens, and aligns with value-based care models. As more tests gain regulatory and guideline support, coverage breadth will determine their scalability in the market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Follow-up colonoscopy attrition after positive non-invasive tests | -1.1% | National, most pronounced in rural markets and in communities with Medicaid or uninsured populations | Short term (≤ 2 years), Medium term (2-4 years) |

| Sensitivity gap for precancerous lesions in blood-based tests | -0.8% | National, with stronger impact in Medicare-age populations where coverage decisions are closely tied to evidence thresholds | Medium term (2-4 years) |

| High cost and coverage friction for newer modalities | -0.9% | National, with heavier pressure in states without Medicaid expansion and in employer plans with restrictive coverage design | Short term (≤ 2 years), Medium term (2-4 years) |

| Patient preference bias toward existing colonoscopy networks | -0.6% | Regional, strongest in urban markets with established gastroenterology practice networks across the Northeast and Mid-Atlantic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Follow-Up Colonoscopy Attrition After Positive Non-Invasive Tests

Follow-up rates after positive non-invasive test results highlight a critical gap in the United States colorectal cancer screening market. Across 38 health systems, only 47.9% of patients with abnormal stool-based results completed a colonoscopy within six months, with rates ranging from 13.1% to 66.9%. An Optum database analysis showed just 43.3% follow-up within 90 days, which the American Academy of Family Physicians deemed inconsistent with clinical screening recommendations. A 2026 study in the Journal of General Internal Medicine demonstrated that structured outreach could achieve a 59.6% colonoscopy completion rate within 180 days. This indicates that the challenge lies not only in patient reluctance but also in the transition from screening results to scheduling and completion. Low diagnostic completion rates impact the commercial value of screening kits and reduce payer confidence.

Sensitivity Gap for Precancerous Lesions in Blood-Based Tests

Blood-based testing has improved acceptability in the United States colorectal cancer screening market but faces a significant clinical limitation. The American Society for Gastrointestinal Endoscopy reported that the Shield test detected only 13% of advanced precancerous lesions, falling short of the sensitivity required to compete with established preventive methods. A 2025 comparative study found blood tests meeting current CMS thresholds reduced colorectal cancer incidence by 40% and mortality by 52%, while multi-target stool DNA and annual FIT tests achieved a 68% to 79% reduction in incidence. The USPSTF has not issued an A or B recommendation for blood-based screening, limiting its commercial coverage under preventive care. Blood-based methods could become more viable if sensitivity to advanced precancerous lesions exceeds 40% at competitive pricing, but they remain a complement rather than a replacement for stool testing or colonoscopy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Non-Invasive Options Are Expanding While Colonoscopy Keeps a Structural Role

In 2025, colonoscopy screenings accounted for 45.95% of the United States colorectal cancer screening market, maintaining its position as the leading test category. Its dual role as a primary screening method and a follow-up for positive non-invasive results ensures consistent demand. While non-invasive tests are gaining traction, colonoscopy remains central for confirmation, diagnosis, and surveillance.

Stool-based tests are projected to grow at a 9.65% CAGR from 2026 to 2031, driven by broader coverage and improved product performance. Exact Sciences reported USD 2.53 billion in screening revenue for 2025, a 20.2% year-over-year increase, highlighting the growing adoption of stool-based testing. Cologuard Plus has reduced false positives by nearly 40%, enhancing workflow efficiency. Blood-based screenings, such as Shield, are gaining attention but face adoption challenges due to evidence requirements and uneven insurance coverage. CT colonography has gained momentum with Medicare coverage, while flexible sigmoidoscopy remains limited to specific clinical settings.

By Technology: Established Stool Methods Hold the Base While Molecular Platforms Gain Ground

FIT and gFOBT tests held a 32.65% market share in 2025, supported by their clinical history, insurance coverage, and cost-effectiveness. Their simplicity makes them suitable for routine primary care and public screening workflows. Mailed FIT kits achieved a 26.2% completion rate among newly eligible adults aged 45-49, emphasizing the role of direct outreach. Multi-target stool DNA tests, with a 71.3% adherence rate compared to 32.1% for FIT, demonstrate a behavioral advantage in overcoming engagement barriers.

Cell-free DNA and methylation-based assays are expected to grow at an 8.55% CAGR from 2026 to 2031, driven by advancements in blood-based screening and platform development. Guardant expanded Shield availability through Quest Diagnostics, enhancing physician access. Stool RNA assays gained prominence after ColoSense received FDA approval and was recognized as a preferred option by the American Cancer Society in 2026. Competition in blood-based screening is intensifying with new platforms entering the market. Imaging and endoscopic technologies remain critical, with Olympus reporting a 7.3% improvement in adenoma detection rates using its CADDIE AI system.

By End User: Laboratory Networks Lead Current Volume While Hospitals Gain Faster Momentum

Independent diagnostic laboratories held a 41.25% market share in 2025, benefiting from the centralized processing model that supports stool DNA, stool RNA, and blood-based tests. Guardant's collaboration with Quest Diagnostics connected Shield to a vast network of clinicians, hospitals, and patient service centers, further strengthening this model.

Hospitals and specialty clinics are the fastest-growing segment, with an 8.77% CAGR from 2026 to 2031. Their role is expanding due to AI-assisted colonoscopy systems, hospital-based physician networks, and Medicare's CT colonography coverage, which reimburses USD 108.68 for the professional component and USD 699.98 globally for imaging centers. Hospitals are critical for diagnostic resolution and polyp management following positive non-invasive results, while ambulatory surgical centers remain relevant for surveillance and diagnostic colonoscopy.

Geography Analysis

The United States colorectal cancer screening market is influenced by state policies, provider access, payer mix, and screening outreach rather than international trade patterns. The Northeast demonstrates stronger screening maturity due to dense specialist networks, higher commercial insurance penetration, and established public health systems, which ensure consistent patient follow-through. States like New York, Massachusetts, and New Jersey are well-positioned to adopt newer molecular tests while maintaining procedural capacity.

Western markets, particularly California, are key growth areas for non-invasive testing due to Medicaid expansion, extensive primary care networks, and community health programs that align with mailed and at-home screening pathways. The market is also benefiting from standardized access to newer modalities through public coverage, with ColoSense covered by 19 state Medicaid programs, including California, Florida, Texas, and New York. This broad coverage expands access beyond commercial populations, strengthens physician confidence, and positions large-population states as early demand centers for new tests transitioning into routine use.

Midwestern states leverage strong primary care networks and proximity to major laboratory and diagnostic infrastructures tied to leading manufacturers. States like Wisconsin and Ohio align well with value-based care programs that emphasize mailed outreach, centralized lab processing, and compliance tracking. Regions with better navigation and reimbursement alignment are converting eligibility into completed screenings more effectively than those relying on passive referral flows. Future growth in the United States colorectal cancer screening market will depend on both product launches and the equitable improvement of access and follow-up systems across states.

Competitive Landscape

The United States colorectal cancer screening market is moderately concentrated at the top but remains fragmented across test technologies, care settings, and laboratory channels. Abbott significantly strengthened its position with the acquisition of Exact Sciences in March 2026, consolidating USD 2.53 billion in annual colorectal cancer screening revenue and establishing the broadest stool-based platform in the industry. Guardant Health leads the blood-based screening category with Shield, while Quest Diagnostics and Laboratory Corporation of America maintain strong positions as channel partners due to their control over physician access, sample handling, and laboratory service relationships.

Recent strategic moves highlight efforts to secure competitive advantages. Abbott’s acquisition of Exact Sciences integrated Cologuard, Cologuard Plus, and future blood-based options under a unified platform strategy. Guardant expanded Shield’s reach through Quest Diagnostics, accessing approximately 650,000 clinician accounts, 2,000 patient service centers, and 6,000 in-office phlebotomists. Olympus validated AI-assisted lesion detection through the EAGLE Trial, which demonstrated a 7.3% improvement in adenoma detection rates without disrupting workflow in a multicenter randomized study.

Opportunities remain in advanced precancerous lesion detection and follow-up infrastructure. Blood-based testing has improved patient acceptance, but its broader success depends on achieving higher lesion sensitivity to gain payer confidence and guideline inclusion. Operational execution is critical, as structured outreach achieved a 59.6% follow-up colonoscopy completion within 180 days after a positive stool test, compared to 43.3% within 90 days in passive care settings. The United States colorectal cancer screening market rewards companies that combine scientific credibility, extensive channel reach, and effective care coordination, ensuring a competitive environment despite consolidation among major players.

U.S. Colorectal Cancer Screening Industry Leaders

F. Hoffmann-La Roche Ltd

Olympus Corporation

Siemens Healthineers AG

Guardant Health, Inc.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The American Cancer Society expanded its colorectal cancer screening guidelines to include blood-based tests such as Shield, along with two newer stool-based options: the updated mt-sDNA (Cologuard Plus) and mt-sRNA (ColoSense). This update applies to average-risk adults aged 45 and older.

- May 2026: Freenome’s SimpleScreen CRC, a blood-based test, was incorporated into the updated ACS guideline. The test was submitted to the FDA in August 2025, and Abbott retained the U.S. commercialization rights.

- March 2026: Guardant Health, in partnership with Quest Diagnostics, expanded the availability of its Shield test. This collaboration provides physicians access through approximately 650,000 clinician accounts, 2,000 patient service centers, and 6,000 in-office phlebotomists.

- February 2026: Olympus reported results from the EAGLE Trial, demonstrating a 7.3% improvement in adenoma detection rates. This advancement was observed in over 800 patients utilizing its cloud-based CADDIE AI system during colonoscopies.

U.S. Colorectal Cancer Screening Market Report Scope

As per the scope of the report, colorectal cancer screening is defined as the process of testing asymptomatic individuals to detect early-stage colorectal cancer or precancerous growths called polyps. The primary goal is prevention and early intervention; finding and removing polyps before they turn into cancer can stop the disease from developing entirely.

The U.S. colorectal cancer screening market is segmented by test type, technology, and end-user. By test type, the market includes stool-based tests, colonoscopy-based screening, blood-based screening tests, CT colonography, and flexible sigmoidoscopy. By technology, the market is segmented into FIT and gFOBT, multitarget stool DNA, cell-free DNA and methylation-based assays, stool RNA assays, and imaging and endoscopic systems. By end-user, the market is categorized into hospitals and specialty clinics, independent diagnostic laboratories, ambulatory surgical centers, and primary care and physician offices. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Stool-Based Tests |

| Colonoscopy-Based Screening |

| Blood-Based Screening Tests |

| CT Colonography |

| Flexible Sigmoidoscopy |

| FIT and gFOBT |

| Multitarget Stool DNA |

| Cell-Free DNA and Methylation-Based Assays |

| Stool RNA Assays |

| Imaging and Endoscopic Systems |

| Hospitals and Specialty Clinics |

| Independent Diagnostic Laboratories |

| Ambulatory Surgical Centers |

| Primary Care and Physician Offices |

| By Test Type | Stool-Based Tests |

| Colonoscopy-Based Screening | |

| Blood-Based Screening Tests | |

| CT Colonography | |

| Flexible Sigmoidoscopy | |

| By Technology | FIT and gFOBT |

| Multitarget Stool DNA | |

| Cell-Free DNA and Methylation-Based Assays | |

| Stool RNA Assays | |

| Imaging and Endoscopic Systems | |

| By End User | Hospitals and Specialty Clinics |

| Independent Diagnostic Laboratories | |

| Ambulatory Surgical Centers | |

| Primary Care and Physician Offices |

Key Questions Answered in the Report

How large is the U.S. colorectal cancer screening market in 2026?

The U.S. colorectal cancer screening market is valued at USD 6.93 billion in 2026 and is forecast to reach USD 10.02 billion by 2031 at a CAGR of 7.65%.

What is driving growth in U.S. colorectal cancer screening through 2031?

Growth is being supported by earlier screening eligibility, wider use of non-invasive tests, FDA-backed innovation in blood and stool RNA testing, and broader Medicare coverage for approved screening options.

Which test type is growing fastest in colorectal cancer screening in the United States?

Stool-based tests are the fastest-growing test type, with a projected CAGR of 9.65% during 2026-2031, supported by at-home collection and improving assay performance.

Which technology segment leads current colorectal cancer screening demand?

FIT and gFOBT held the largest technology share at 32.65% in 2025 because they remain low cost, broadly covered, and easy to deploy through primary care and outreach programs.

Why do independent diagnostic laboratories lead among end users?

Independent diagnostic laboratories held 41.25% share in 2025 because at-home stool and blood testing routes specimen processing to centralized, high-throughput lab networks.

What is the main challenge for newer blood-based colorectal cancer tests?

The main issue is lower sensitivity for advanced precancerous lesions, which limits payer confidence and broader guideline support even though blood tests improve patient acceptability.

Page last updated on: