Surgical Kits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.48 Billion |

| Market Size (2031) | USD 25.57 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

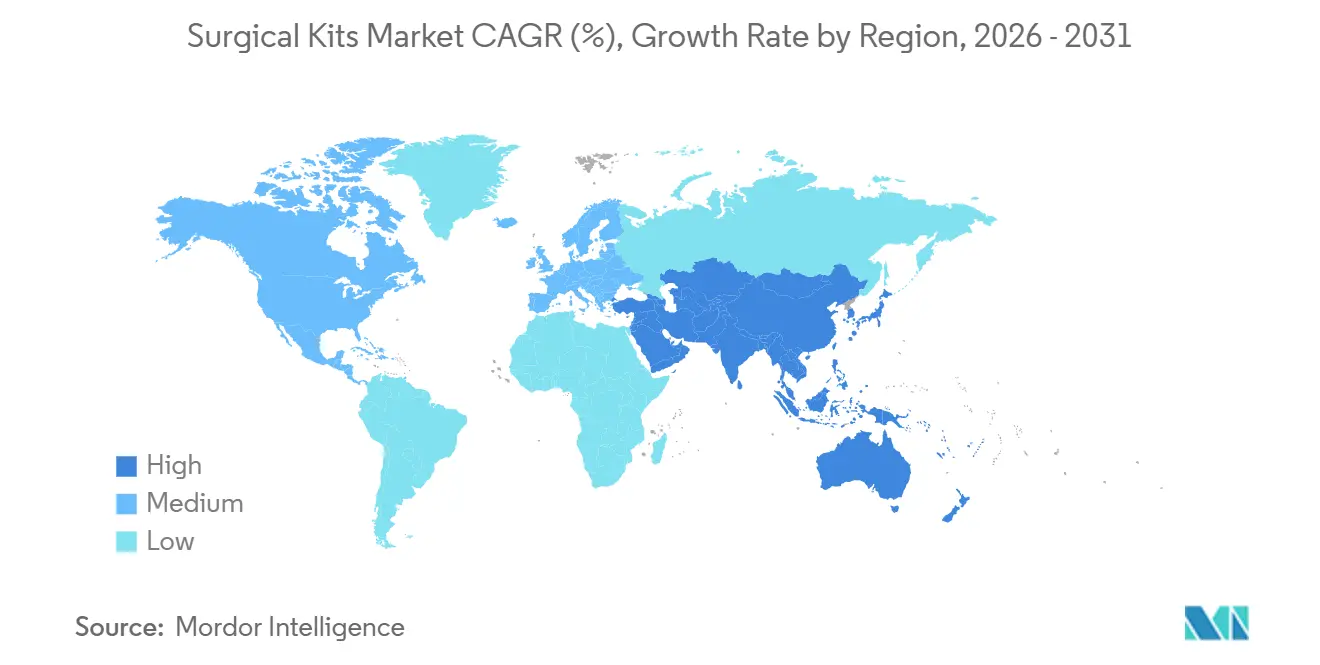

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

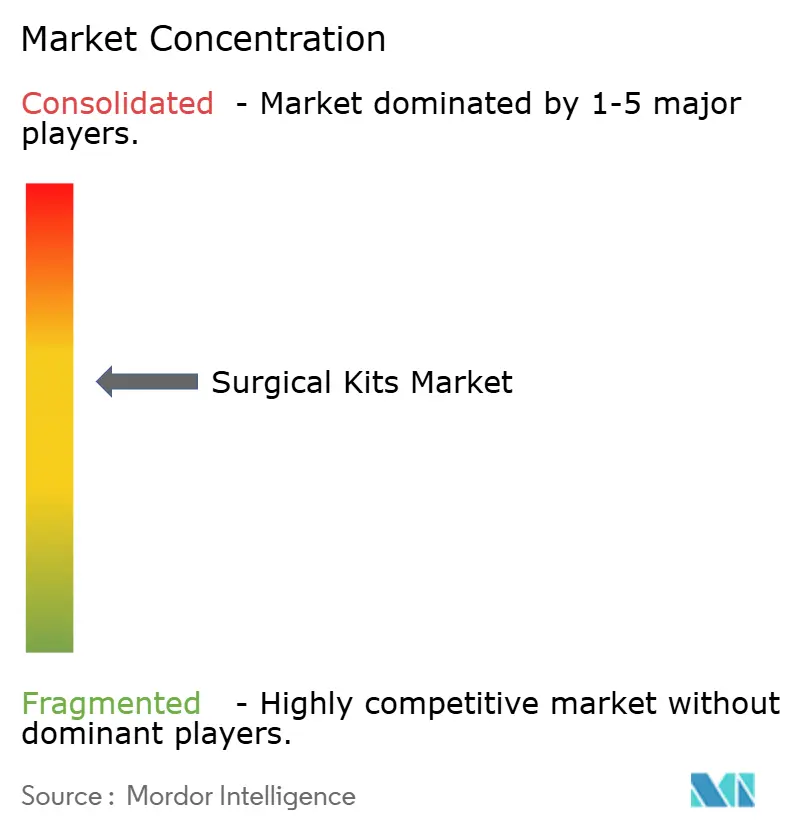

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Kits Market Analysis by Mordor Intelligence

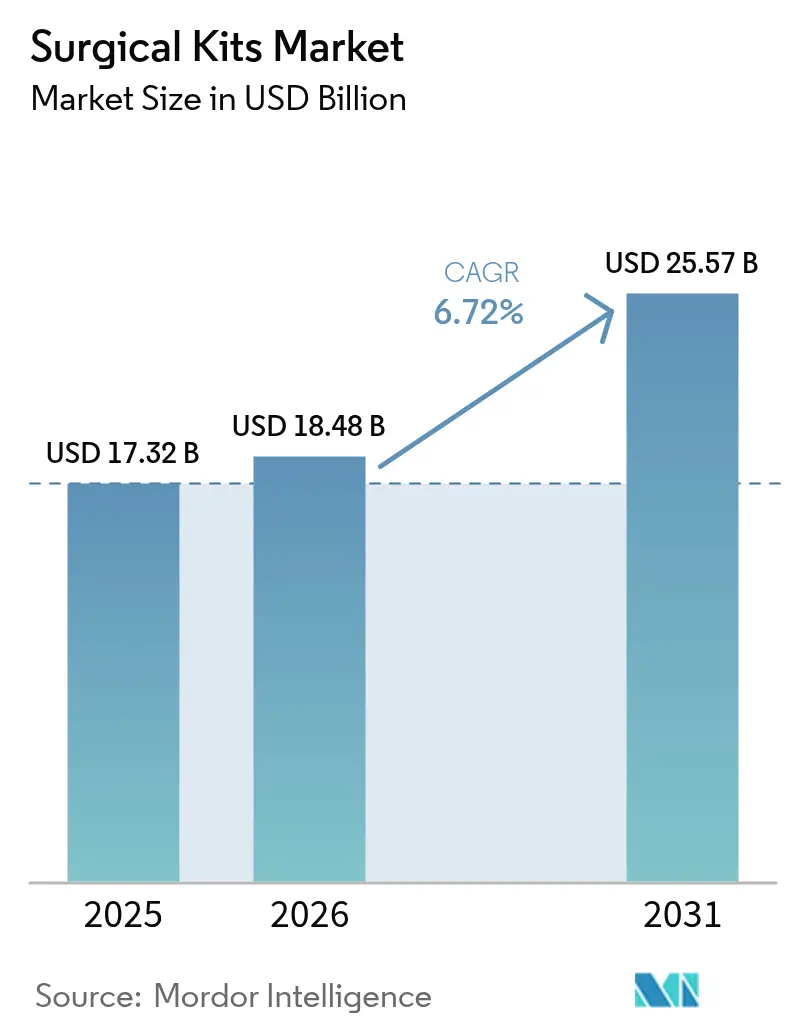

The surgical kits market size was valued at USD 17.32 billion in 2025 and is estimated to grow from USD 18.48 billion in 2026 to reach USD 25.57 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). Growth is underpinned by hospitals replacing reusable trays with single-use procedure packs that embed infection-control compliance and digital traceability. Demand intensifies as governments mandate unique-device identification, driving vendors to serialize every pouch for real-time inventory analytics. Ambulatory surgery centers favor standardized packs that trim supply expense, while regulations limiting ethylene-oxide emissions accelerate low-temperature plasma sterilization investments. Sustainability statutes in Europe and selected U.S. states spur experimentation with bio-based drapes and gowns, creating white-space opportunities for suppliers of compostable polymers. Meanwhile, vendor-managed just-in-time case carts convert hospitals’ fixed assets into variable costs, lowering inventory days on hand and tightening the competitive landscape.

Key Report Takeaways

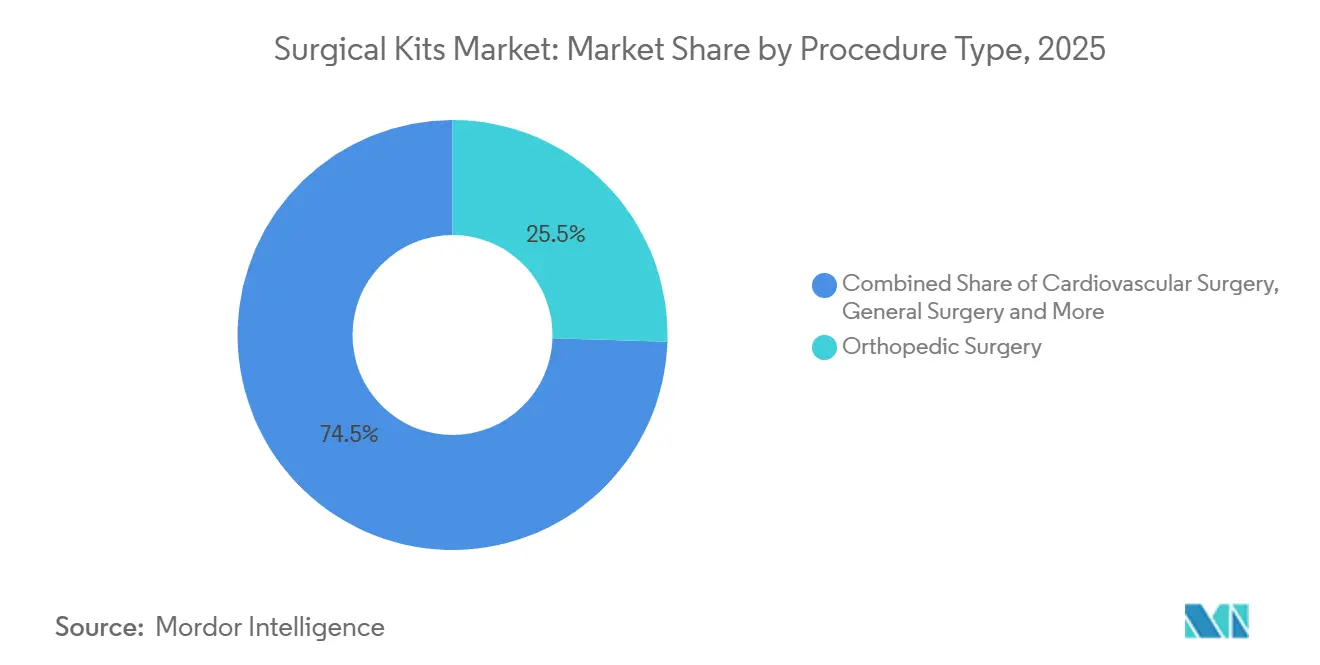

- By procedure type, orthopedic surgery led with 25.54% of the surgical kits market share in 2025, whereas ENT & thoracic surgery is projected to expand at a 9.25% CAGR through 2031.

- By component, drapes & gowns commanded 26.54% revenue share in 2025; sutures & adhesives are advancing at an 8.65% CAGR over 2026-2031.

- By kit configuration, customized procedure packs held 54.15% of the surgical kits market size in 2025, while emergency & trauma packs register the highest 9.82% CAGR.

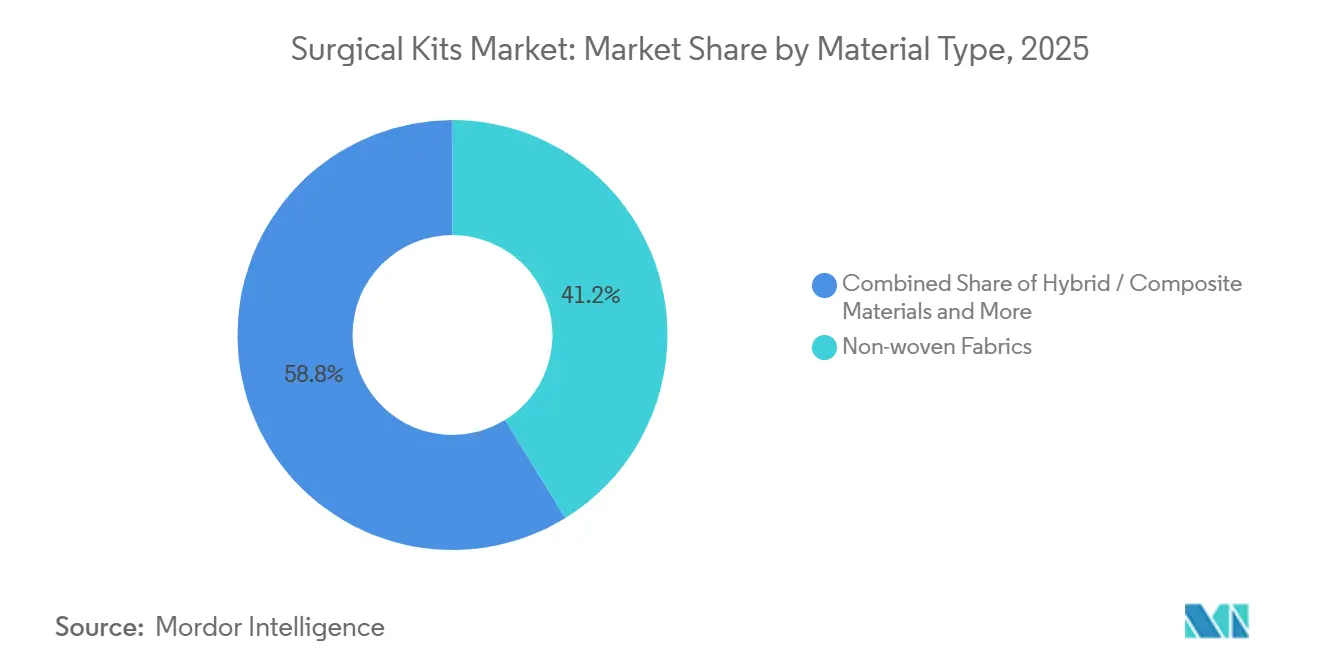

- By material type, non-woven fabrics captured 41.23% revenue share in 2025, yet bio-based/compostable materials are growing at a 12.42% CAGR.

- By sterilization method, ethylene oxide dominated with 45.83% share in 2025; plasma sterilization is the fastest riser at 11.22% CAGR.

- By sterility, sterile kits represented 92.23% of 2025 sales, whereas non-sterile kits are increasing at a 10.52% CAGR.

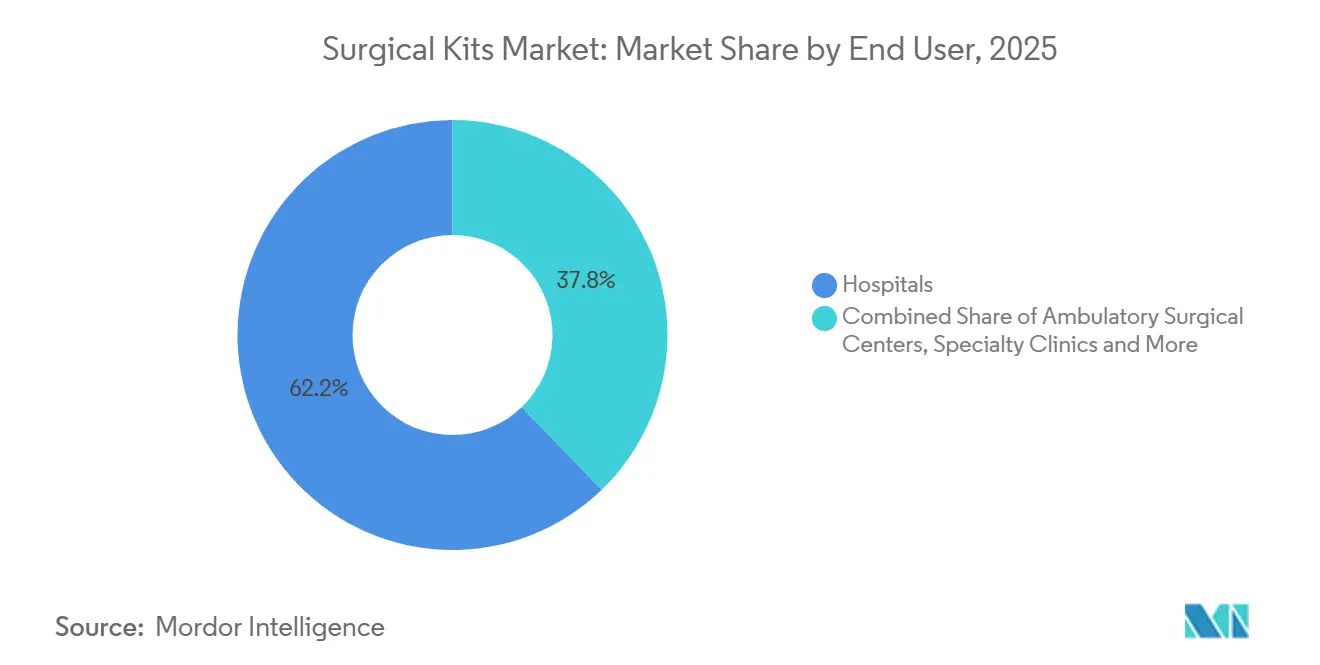

- By end user, hospitals accounted for 62.22% of revenue in 2025; ambulatory surgical centers are expanding at an 8.62% CAGR.

- By distribution channel, direct institutional sales formed 49.43% of sales in 2025, but e-commerce platforms accelerate at a 12.12% CAGR.

- By geography, North America led with 45.53% revenue share in 2025, while Asia-Pacific posts a robust 10.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Kits Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing surgical procedure volume worldwide | +1.8% | Global, notably Asia-Pacific & North America | Long term (≥ 4 years) |

| Shift toward customized procedure packs for OR efficiency | +1.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Stricter infection-control regulations boosting single-use sterile kits | +1.3% | Global, led by EU & U.S. | Medium term (2-4 years) |

| Expansion of ambulatory surgery centers demanding standardized kits | +1.2% | North America, spill-over Europe & Australia | Long term (≥ 4 years) |

| Digital traceability mandates enabling real-time inventory analytics | +0.7% | North America & EU | Short term (≤ 2 years) |

| OEM–CPT vendor partnerships for just-in-time case-cart delivery models | +0.6% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Surgical Procedure Volume Worldwide

Global surgical volume climbed to 421 million procedures in 2024 from 387 million in 2022 as aging populations and chronic diseases lifted elective interventions. The World Health Organization projects 62% of incremental demand to emanate from low- and middle-income nations by 2030, prompting governments to standardize essential-procedure packs that shave 18 minutes off set-up time and raise theater utilization. China expanded its surgical reimbursement catalog to 1,200 procedures in 2025, spurring a 23% rise in kit purchases by provincial hospitals[1]National Healthcare Security Administration, “Reimbursement Catalog Expansion,” nhsa.gov.cn. India deployed 3,400 mobile surgical units equipped with trauma packs in rural districts, demonstrating how procedure growth extends beyond fixed facilities. As case volumes swell, the surgical kits market benefits from predictable, repeat demand cycles that underpin vendor capacity-planning.

Shift Toward Customized Procedure Packs for OR Efficiency

Tailored packs cut tray set-up by 14 minutes per orthopedic case and save USD 47 in nursing labor, according to a 2024 multicenter U.S. study. Seventy-eight percent of knee-replacement surgeries used surgeon-specific packs in 2025, transferring inventory risk to assemblers. Workflow complexity remains a concern; 34% of circulating nurses reported tray discrepancies weekly, delaying cases. Vendors now integrate barcode scanning with electronic health-records to verify contents in real time before a patient enters the room, reinforcing the value proposition of customization without eroding efficiency.

Stricter Infection-Control Regulations Boosting Single-Use Sterile Kits

FDA guidance issued in 2024 obliges manufacturers of reusable instruments to validate cleaning against prion contamination, adding USD 120,000 per instrument family in annual compliance costs and nudging hospitals toward disposables. EU Medical Device Regulation Article 5.5 enforces biofilm surveillance of reusable devices, compelling 14 national health systems to restrict reusable laparoscopic tools. Single-use kits reduced surgical-site infection by 0.8 percentage points across 47 randomized trials, solidifying their clinical merit. Hospitals weighing litigation and readmission penalties see disposable packs as insurance against adverse events.

Expansion of Ambulatory Surgery Centers Demanding Standardized Kits

U.S. ASCs performed 28.4 million cases in 2025, up 19% from 2023, driven by Medicare payment parity on 11 added procedure codes[2]Centers for Medicare & Medicaid Services, “ASC Payment Parity,” cms.gov. Supply expense per ASC case averages USD 412 versus USD 687 in hospitals; standardized packs ease budget pressure and slash expired inventory. Eighty-one percent of centers trimmed their kit suppliers from four to two, leveraging volume for double-digit price cuts. Staff turnover of 22% annually amplifies the appeal of pre-configured trays that shorten onboarding and curb errors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement pressure in low-income settings | -0.9% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Supply-chain volatility in non-woven barrier materials | -0.7% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Sustainability concerns over disposables driving regulatory scrutiny | -0.5% | EU, emerging U.S. & Australia | Medium term (2-4 years) |

| Customization complexity causing workflow mis-alignment | -0.3% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement Pressure in Low-Income Settings

Public payers in 38 low-income nations reimburse procedures at 40-60% below the cost of single-use packs, forcing hospitals to rely on reusable sets and autoclaves[3]World Health Organization, “Surgical Financing in Low-Income Countries,” who.int. Kenya’s national insurer allotted just USD 0.32 per surgical case for disposables in 2025, far below the USD 8-12 needed for basic drape-and-gown sets. Resin inflation of 11% annually from 2023-2025 widened the gap. Donor initiatives, such as Gavi’s advance-market commitment covering 2 million kits yearly at USD 6 apiece, remain confined to 11 countries.

Supply-Chain Volatility in Non-Woven Barrier Materials

Polypropylene spot prices spiked 34% between January 2024 and March 2025 after outages at U.S. Gulf Coast petrochemical plants. Four leading kit assemblers invoked force-majeure clauses, delaying deliveries up to six weeks and paying USD 18 million in penalties. Hospitals responded by dual-sourcing packs and tying contracts to the plastics producer price index. An ongoing U.S. antidumping probe into Chinese spunbond imports heightens uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Orthopedic Anchors Spend While Endoscopic ENT Accelerates

Orthopedic surgery held 25.54% of the surgical kits market share in 2025, buoyed by USD 1,200-1,800 joint-replacement packs that bundle implant trials and cement systems. Yet ENT & thoracic kits are growing briskly at 9.25% CAGR on the back of minimally invasive sinus and video-assisted thoracoscopic procedures that favor disposable trocars. An evidence review showed video-assisted lobectomy shaved 2.1 days off inpatient stay, bolstering payer support for single-use instrument sets that speed discharge. Cardiovascular kits tick along at mid-single-digit growth as transcatheter valves eclipse open-heart volumes. General surgery and obstetrics draw steady demand, the latter lifted by rising institutional deliveries in Asia-Pacific.

Shifting procedures to ambulatory sites compress kit footprints; ENT cases in U.S. ASCs jumped 27% between 2023-2025. Vendors now unbundle orthopedic implant trials to shave 15-20% off pack cost. Regulatory reclassification of laparoscopic instruments to Class II intensified 510(k) hurdles, favoring incumbents with robust validation labs.

By Component: Drapes Dominate While Sutures Race Ahead

Drapes & gowns generated 26.54% of component revenue in 2025, mandated by universal-barrier protocols. Sutures & adhesives, however, outpace at 8.65% CAGR, propelled by bioresorbable polymers that erase follow-up removal visits. A 2025 meta-analysis reported cyanoacrylate adhesives cut infection by 1.2 percentage points in clean-contaminated wounds. Instruments, disposables, and implants each add incremental value but mirror overall market trajectory.

Innovation fuels component economics. Antimicrobial-coated drapes slashed contamination 34% in controlled trials, commanding a 25% premium. RFID-tagged suture packs reduced stockouts nearly 30%, underscoring tech’s growing role in inventory stewardship.

By Kit Configuration: Customization Reigns, Trauma Packs Surge

Customized packs absorbed 54.15% of the surgical kits market size in 2025 as surgeons fine-tuned instruments to personal technique. Emergency & trauma packs, by contrast, post a 9.82% CAGR, catalyzed by standardized hemorrhage-control kits in ambulances and field hospitals. The American College of Surgeons’ Stop the Bleed campaign trained 2.3 million civilians by 2025, expanding demand for public-access trauma kits.

Digital configurators now let surgeons drag-and-drop components in a 3-D workspace, previewing the tray before orders lock. Regulatory oversight intensifies when drug-device combos appear in a pack, elongating approval by up to nine months.

By Material Type: Non-Woven Leads while Bio-Based Disrupts

Non-woven fabrics represented 41.23% of 2025 revenue, prized for barrier and breathability at sub-USD 3.50/m². Bio-based/compostable materials grow 12.42% CAGR, helped by life-cycle assessments showing 48% lower greenhouse emissions for polylactic-acid drapes. Yet price premiums curb uptake outside sustainability-budgeted hospitals.

Material science advances: spunlace cellulose blends achieved ASTM F1671 viral-barrier status, granting biodegradability without sacrificing protection. Antimicrobial nanoparticle additives trim bacterial loads 99.7%, though regulators monitor migration risk.

By Sterilization Method: Ethylene Oxide Dominates as Plasma Gains

Ethylene oxide retained 45.83% share in 2025 for heat-sensitive kits, yet plasma sterilization races ahead at 11.22% CAGR, completing cycles in under 45 minutes and leaving no toxic residue. Tougher EPA emission caps may inflate ethylene-oxide costs, compelling a shift toward plasma and e-beam irradiation. Gamma capacity tightens as cobalt-60 replacement costs shutter facilities, lengthening lead times.

By Sterility: Sterile Kits Rule, Non-Sterile Finds a Niche

Sterile kits held 92.23% of 2025 sales, compulsory for devices touching sterile tissue. Non-sterile packs, however, log a 10.52% CAGR where hospitals autoclave instruments in-house to capture 30-40% savings. Infection-prone specialties remain wary; a 2024 CDC investigation tied seven surgical-site infections to improperly cleaned non-sterile orthopedic sets.

By End User: Hospitals Command, ASCs Accelerate

Hospitals captured 62.22% revenue in 2025, supported by high-acuity caseloads and in-house sterile processing. ASCs gain at 8.62% CAGR on procedural migration after payment-parity reforms. Value-analysis committees in hospitals now weigh total cost of ownership, pushing vendors toward outcome-based contracts. Specialty clinics, military units, and office-based suites round out demand, each with tailored kit requirements.

By Distribution Channel: Direct Sales Prevalent, E-Commerce Gains Traction

Direct institutional sales formed 49.43% of 2025 revenue, reflecting hospitals’ appetite for field reps and clinical in-service. E-commerce platforms, nonetheless, grow 12.12% CAGR as GPOs aggregate 400-plus SKUs with live pricing, slicing order cycle times by 25%. Vizient’s 2025 EDI pilot chopped USD 14 off processing costs per order, underlining digital efficiencies.

Geography Analysis

North America led at 45.53% in 2025, fueled by rigorous UDI mandates and robust value-analysis cultures. The U.S. added 4.8 million outpatient procedures to ASC settings between 2023-2025, fortifying demand for standardized packs. Ethylene-oxide emission curbs and polypropylene price swings pose near-term headwinds.

Asia-Pacific advances 10.1% CAGR to 2031. China installed 12,000 surgical suites under Healthy China 2030, driving bulk-buying of procedure packs. India reimbursed 18 million surgical episodes in 2025 through Ayushman Bharat, ratcheting kit uptake. Japan’s cataract volumes rose 11% in 2024-2025, and new minimally invasive orthopedic codes won coverage in 2024.

Europe occupies a sturdy mid-30s share, but sustainability and post-market surveillance requirements inflate compliance spend by 15-20%, uplifting barriers against low-cost entrants. Middle East & Africa grow modestly, concentrated in GCC medical-tourism hubs, while South America relies on public-private partnerships to expand theater capacity.

Competitive Landscape

The top suppliers—Johnson & Johnson (Ethicon), Medline Industries, Cardinal Health, B. Braun Melsungen, and Medtronic—collectively hold a significant share, signaling moderate concentration. Scale players exploit vertical integration from fabric extrusion to distribution, securing 18-22% gross margins. Mid-tier assemblers compete on customization agility and regional regulatory fluency. Sustainability disruptors such as Mölnlycke command premium contracts with carbon-neutral drapes certified under ISO 14067. Technology differentiators embed RFID tags and cloud preference-card systems, winning 25-30% share gains at digitally mature hospitals. Regulatory moats deepen as EU MDR and FDA 510(k) requirements extend validation timelines and costs, deterring greenfield entrants.

Surgical Kits Industry Leaders

Medline Industries, LP

Medtronic plc

Johnson & Johnson (Ethicon)

Cardinal Health, Inc.

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: New Medtek Devices (NMD) secured Class IIb certification from Australia’s Therapeutic Goods Administration for its RrhoidCath Surgical Kit, documented under Conformity Assessment Certificate AU Q00548.

- May 2025: Minerva Surgical introduced the HERizon Hysto-Kit, a single-use, pre-assembled solution that simplifies office-based hysteroscopy procedures.

Global Surgical Kits Market Report Scope

As per the scope of the report, the surgical kit contains the instruments necessary for minor surgical procedures. Surgical instruments are tools or devices for performing specific actions or carrying out desired effects during a surgery or operation, such as modifying biological tissue or providing access for viewing it.

The surgical kits market is segmented by procedure type, including cardiovascular surgery, orthopedic surgery, obstetrics and gynecology, general surgery, neurosurgery, ophthalmic surgery, urology surgery, ENT and thoracic surgery, and other procedures. By component, the market is categorized into instruments and tools, drapes and gowns, disposable supplies, sutures and adhesives, implants and fixation accessories, and other components. Based on kit configuration, the segmentation includes standardized procedure packs, customized procedure packs, and emergency and trauma packs. By material type, the market is divided into non-woven fabrics (SMS, spunlace), woven textiles, hybrid/composite materials, and bio-based/compostable materials. The market is further segmented by sterilization method into ethylene oxide, gamma radiation, e-beam irradiation, steam/autoclave, and plasma. By sterility, the market is classified into sterile kits and non-sterile kits. Based on end user, the segmentation includes hospitals, ambulatory surgical centers, specialty clinics, military and field hospitals, and home and office-based surgical suites. By distribution channel, the market is divided into direct institutional sales, group purchasing organizations (GPOs), third-party distributors, and e-commerce platforms. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Cardiovascular Surgery |

| Orthopedic Surgery |

| Obstetrics & Gynecology |

| General Surgery |

| Neurosurgery |

| Ophthalmic Surgery |

| Urology Surgery |

| ENT & Thoracic Surgery |

| Other Procedures |

| Instruments & Tools |

| Drapes & Gowns |

| Disposable Supplies |

| Sutures & Adhesives |

| Implants & Fixation Accessories |

| Other Components |

| Standardised Procedure Packs |

| Customized Procedure Packs |

| Emergency & Trauma Packs |

| Non-woven Fabrics (SMS, Spunlace) |

| Woven Textiles |

| Hybrid / Composite Materials |

| Bio-based / Compostable Materials |

| Ethylene Oxide |

| Gamma Radiation |

| E-beam Irradiation |

| Steam / Autoclave |

| Plasma |

| Sterile Kits |

| Non-sterile Kits |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Military & Field Hospitals |

| Home & Office-based Surgical Suites |

| Direct Institutional Sales |

| Group Purchasing Organizations (GPOs) |

| Third-Party Distributors |

| E-commerce Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Cardiovascular Surgery | |

| Orthopedic Surgery | ||

| Obstetrics & Gynecology | ||

| General Surgery | ||

| Neurosurgery | ||

| Ophthalmic Surgery | ||

| Urology Surgery | ||

| ENT & Thoracic Surgery | ||

| Other Procedures | ||

| By Component | Instruments & Tools | |

| Drapes & Gowns | ||

| Disposable Supplies | ||

| Sutures & Adhesives | ||

| Implants & Fixation Accessories | ||

| Other Components | ||

| By Kit Configuration | Standardised Procedure Packs | |

| Customized Procedure Packs | ||

| Emergency & Trauma Packs | ||

| By Material Type | Non-woven Fabrics (SMS, Spunlace) | |

| Woven Textiles | ||

| Hybrid / Composite Materials | ||

| Bio-based / Compostable Materials | ||

| By Sterilization Method | Ethylene Oxide | |

| Gamma Radiation | ||

| E-beam Irradiation | ||

| Steam / Autoclave | ||

| Plasma | ||

| By Sterility | Sterile Kits | |

| Non-sterile Kits | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Military & Field Hospitals | ||

| Home & Office-based Surgical Suites | ||

| By Distribution Channel | Direct Institutional Sales | |

| Group Purchasing Organizations (GPOs) | ||

| Third-Party Distributors | ||

| E-commerce Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the surgical kits market be by 2031?

It is projected to reach USD 25.57 billion by 2031, growing at a 6.72% CAGR over 2026-2031.

Which segment shows the fastest growth in surgical kits?

ENT & thoracic procedure packs lead with a projected 9.25% CAGR through 2031.

Why are ambulatory surgery centers important for kit demand?

Medicare payment parity shifted millions of procedures to ASCs, and these centers prefer standardized packs that lower per-case supply costs.

What material innovations are influencing kit design?

Bio-based drapes and antimicrobial-coated non-woven fabrics are gaining traction as hospitals pursue sustainability and infection-control targets.

How is regulation shaping sterilization choices?

Stricter EPA rules on ethylene-oxide emissions and hospital demand for faster turnover are accelerating adoption of low-temperature plasma systems.

What is driving e-commerce growth in surgical kit distribution?

Group purchasing organizations are deploying digital catalogs that give hospitals live pricing and cut procurement cycle times by about 25%.

Page last updated on: