Next Generation Cancer Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

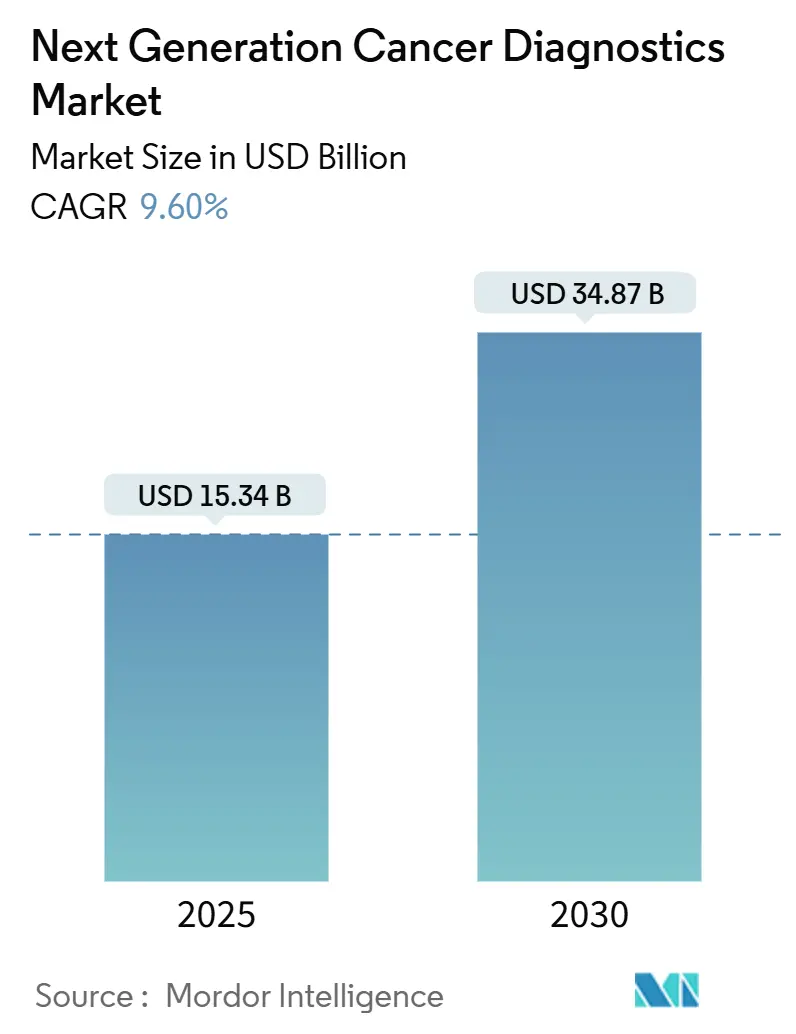

| Market Size (2025) | USD 15.34 Billion |

| Market Size (2030) | USD 34.87 Billion |

| Growth Rate (2025 - 2030) | 9.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next Generation Cancer Diagnostics Market Analysis by Mordor Intelligence

The next-generation cancer diagnostics market size stood at USD 15.34 billion in 2024 and is forecast to reach USD 34.87 billion by 2030, advancing at a 9.6% CAGR. Strong pricing declines in next-generation sequencing (NGS) platforms, improved analytical accuracy, and expanding regulatory support are combining to accelerate routine genomic testing adoption in oncology. Ultra-low reagent costs now make whole-genome analysis financially viable for community hospitals, while artificial-intelligence (AI) algorithms detect circulating tumor DNA (ctDNA) several years before clinical symptoms appear, enabling earlier and more cost-effective interventions. Rapid test-development cycles, companion-diagnostic co-development with pharmaceutical pipelines, and growing preference for minimally invasive liquid biopsies are reshaping clinical workflows. Heightened data-sovereignty requirements are simultaneously driving on-premises AI deployment, giving regional vendors strategic opportunities to differentiate through compliance features.

Key Report Takeaways

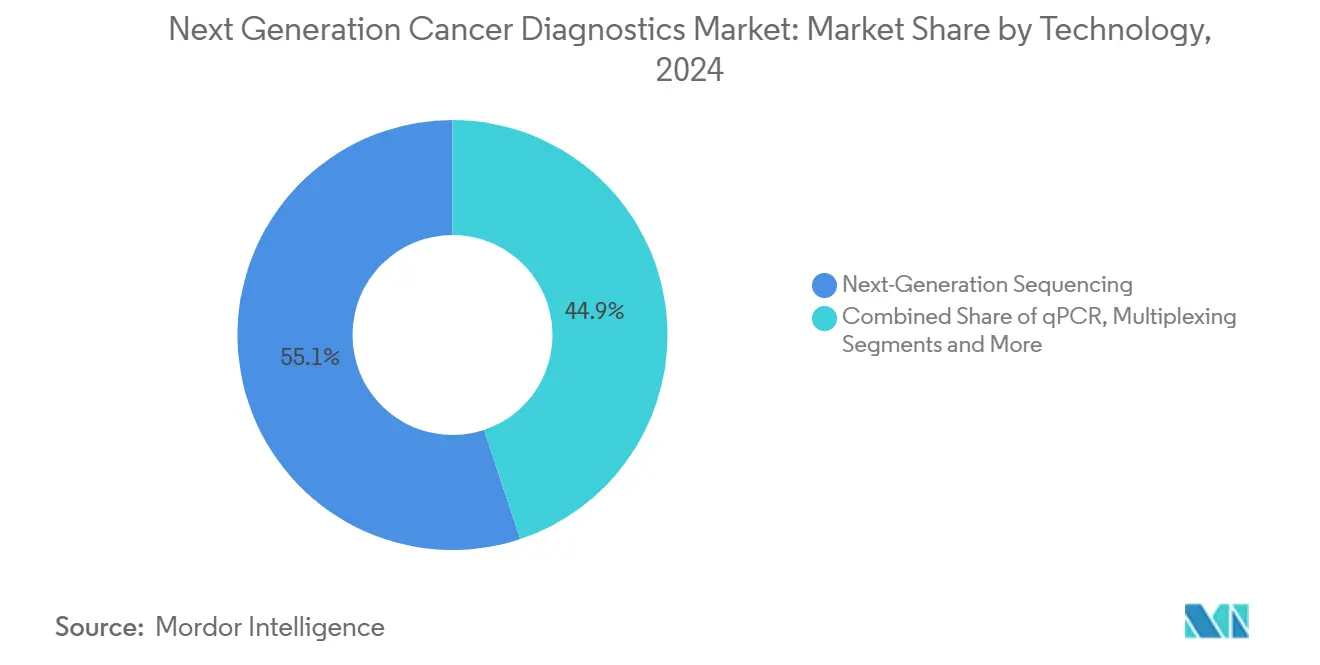

- By technology, next-generation sequencing commanded 55.1% of Next Generation Cancer Diagnostics market share in 2024; liquid biopsy is projected to expand at a 14.2% CAGR through 2030.

- By cancer type, lung cancer diagnostics led with 28.3% revenue share in 2024, while prostate cancer diagnostics are forecast to grow at a 12.1% CAGR to 2030.

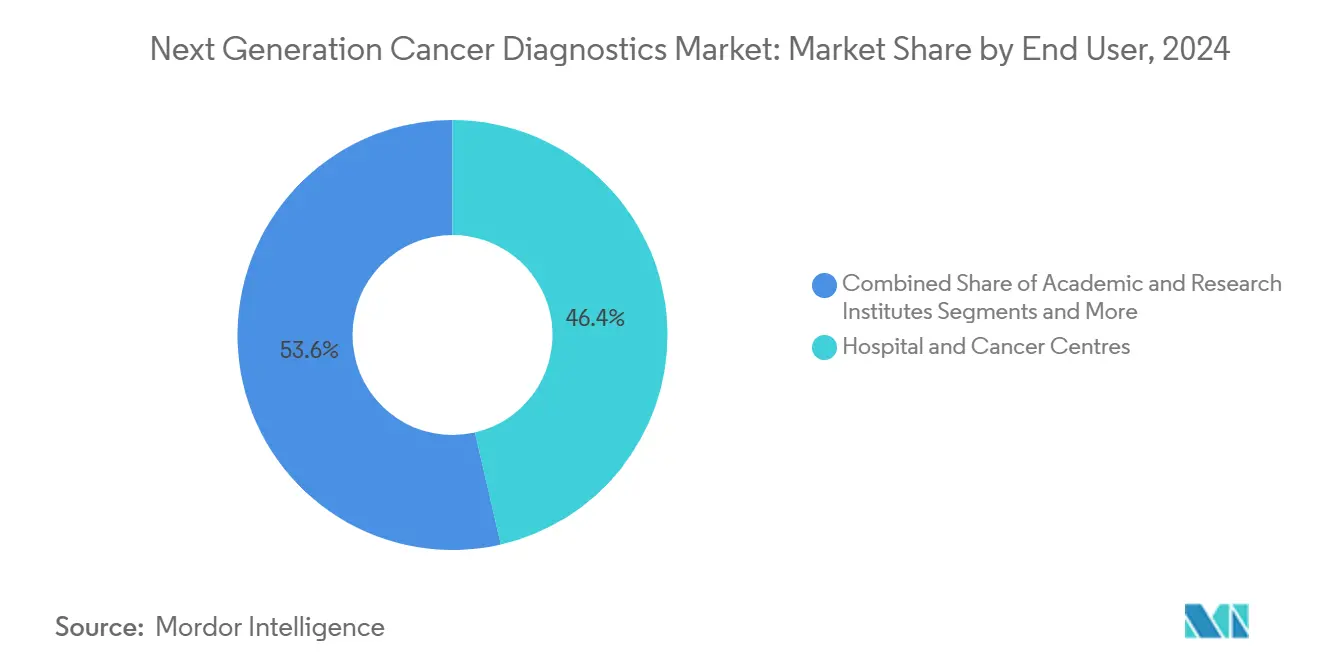

- By end user, hospitals and cancer centers held 46.4% of the Next Generation Cancer Diagnostics market size in 2024; contract research organizations are advancing at an 11.3% CAGR during the same period.

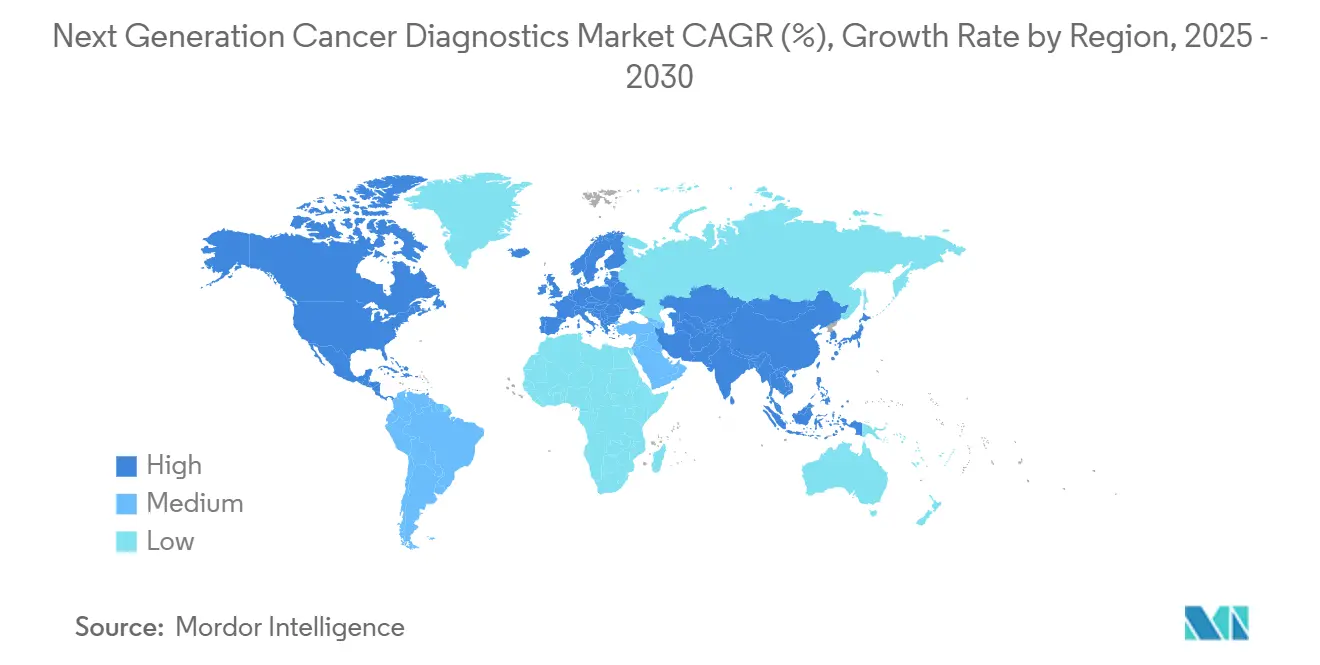

- By geography, North America accounted for 41.7% of Next Generation Cancer Diagnostics market share in 2024, whereas Asia-Pacific is set to register an 11.8% CAGR to 2030.

Global Next Generation Cancer Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cost-decline & accuracy gains in NGS platforms | +2.10% | Global, with strongest impact in North America & Europe | Short term (≤ 2 years) |

| Accelerating adoption of liquid biopsy for therapy selection | +1.80% | Global, led by North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Expanding companion-diagnostic (CDx) approvals for targeted oncology drugs | +1.50% | North America & EU regulatory leadership, Asia Pacific following | Medium term (2-4 years) |

| Rising global cancer incidence & screening mandates | +1.20% | Global, with highest impact in aging populations (Japan, Europe, North America) | Long term (≥ 4 years) |

| AI-powered multi-modal analytics unlocking early-stage detection | +0.90% | North America & EU leading, China rapidly advancing | Short term (≤ 2 years) |

| Home-collection microsampling kits enabling decentralised testing | +0.70% | APAC core, spill-over to MEA, rural market penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Decline and Accuracy Gains in NGS Platforms

Whole-genome sequencing costs dropped 60% in 2024, bringing routine tumor profiling under USD 1,000 per patient.[1]Wellcome Sanger Institute, “Genomics Gets Faster, Cheaper, and More Accurate,” sangerinstitute.ac.uk Element AVITI systems cut prices a further 20%, matching Illumina’s highest-throughput instruments while improving run-time to less than 24 hours. These economics allow community hospitals to integrate genomic testing into standard oncology workflows, reducing sample send-outs and shortening therapeutic turnaround. Simultaneously, improved base-calling accuracy lowers false-negative rates, increasing oncologist confidence in precision-medicine decisions. Large integrated-delivery networks are therefore scaling in-house genomic labs, driving the Next Generation Cancer Diagnostics market toward broader regional penetration.

Accelerating Adoption of Liquid Biopsy for Therapy Selection

Liquid biopsy is transitioning from early detection to frontline therapeutic guidance, with ctDNA assays predicting treatment response within four weeks of regimen initiation, compared with 8–12 weeks for imaging.[2]Johns Hopkins Kimmel Cancer Center, “‘Fast-fail’ AI Blood Test Could Steer Patients with Pancreatic Cancer Away from Ineffective Therapies,” sciencedaily.com The ARTEMIS-DELFI approach demonstrates robust sensitivity for pancreatic cancer, allowing rapid regimen shifts that improve progression-free survival. Multiple FDA breakthrough-device designations in 2024 have validated AI-based urine and blood assays with area-under-curve scores above 0.90. Oncologists now report 73% confidence in ctDNA-guided therapy adjustments, propelling liquid biopsy into community-practice protocols and enlarging its share of the next-generation cancer diagnostics market.

Expanding Companion-Diagnostic Approvals for Targeted Oncology Drugs

The FDA cleared 15 new companion diagnostics in 2024, underscoring the regulator's focus on pairing therapeutics with genomic assays that identify high-responder patient subsets.[3]U.S. Food and Drug Administration, “Laboratory Developed Tests Regulatory Impact Analysis (Final Rule),” fda.gov Platforms such as FoundationOne CDx broadened solid-tumor indications, while Guardant360 CDx added new therapy partnerships, illustrating the move toward assay-agnostic, multi-tumor solutions. EMA alignment under the In-Vitro Diagnostic Regulation (IVDR) has reduced European approval timelines by up to nine months, enabling simultaneous U.S.–EU launches. Pharmaceutical sponsors increasingly embed diagnostic development into Phase I trial designs, creating a widening moat for integrated companies in the Next Generation Cancer Diagnostics market.

Rising Global Cancer Incidence and Screening Mandates

Annual new-cancer diagnoses are projected to reach 28.4 million by 2040, with the sharpest rise in Southeast Asia’s rapidly aging populations. Governments are responding with broader screening mandates, piloting multi-cancer early-detection (MCED) blood tests within national programs. Stage migration offers compelling economics: Stage I treatment averages USD 50,000 versus USD 300,000 at Stage IV. India’s Bharat Cancer Genome Atlas shows how population-level genomics identifies region-specific mutation patterns, tailoring screening priorities and supporting equitable expansion of the next-generation cancer diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement uncertainty & high test cost | -1.40% | Global, most severe in emerging markets and US private insurance | Short term (≤ 2 years) |

| Complex, fragmented regulatory pathways across regions | -0.80% | Global, with highest impact on companies seeking multi-regional approvals | Medium term (2-4 years) |

| Data-privacy & genomic-sovereignty concerns | -0.60% | EU & China leading restrictions, North America moderate impact | Long term (≥ 4 years) |

| Shortage of bioinformatics & variant-interpretation talent | -0.40% | Global, most acute in emerging markets and specialized applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Uncertainty and High-Test Cost

Many liquid biopsy assays remain outside payer formularies despite FDA clearance, forcing patients to self-fund tests priced at USD 3,000–6,000. Medicare Local Coverage Determinations regularly demand additional clinical-utility evidence beyond regulatory approval, delaying broad reimbursement. Variability among U.S. private insurers further limits uptake, whereas single-payer systems in Europe adopt a more streamlined assessment. As value-based oncology contracts evolve, early-stage detection savings of 40–60% could spur reimbursement reform, but interim friction suppresses immediate Next Generation Cancer Diagnostics market growth.

Complex, Fragmented Regulatory Pathways Across Regions

Despite FDA rule finalization for laboratory-developed tests, divergent requirements persist worldwide. Japan’s PMDA frequently mandates local clinical validation even for U.S.-approved assays, extending launches by 12–18 months. ASEAN harmonization efforts are underway, yet inconsistent timelines across member states prolong dossier preparations. Compliance complexity disproportionately burdens small innovators, restraining competitive intensity and slowing the Next Generation Cancer Diagnostics market’s pace in multinational rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: NGS Platforms Drive Clinical Adoption

NGS delivered 55.1% of the Next Generation Cancer Diagnostics market share in 2024, reflecting its role as the definitive platform for comprehensive tumor profiling. Average run-cost declines and same-day sequencing turnarounds have lowered barriers for mid-tier hospitals, enabling broader penetration. The segment’s leadership is bolstered by high parallelization, which supports companion-diagnostic and minimal-residual-disease (MRD) panels in one workflow.

Liquid biopsy holds the fastest growth trajectory at a 14.2% CAGR through 2030, aided by non-invasive sampling and longitudinal monitoring capabilities. ctDNA panels, exosome assays, and AI-enhanced fragmentation analyses provide actionable insights even when tissue samples are unavailable. Meanwhile, qPCR and multiplex immunoassays retain relevance in community settings for single-biomarker testing due to low instrumentation costs. Protein arrays and DNA microarrays continue to decline as the Next Generation Cancer Diagnostics market size migrates toward richer multi-omics methodologies, while emerging nanopore and quantum-based sequencers create future competitive inflection points.

By Cancer Type: Lung Cancer Diagnostics Lead Market Share

Lung cancer diagnostics captured 28.0% of 2024 revenue, supported by established low-dose CT screening programs and multiple targeted therapies requiring EGFR, ALK, and ROS1 testing. Tissue and plasma assays together underpin robust reimbursement frameworks, reinforcing volume leadership.

Prostate cancer diagnostics are forecast to grow at a 12.1% CAGR, fueled by genomic classifiers that stratify active-surveillance candidates and guide androgen-receptor-targeted treatments. Breast and colorectal cancer segments maintain steady contributions, with HER2 and KRAS companion assays well entrenched. Tumor-agnostic approvals for NTRK and MSI markers blur traditional cancer-type boundaries, encouraging multi-cancer panels that extend the Next Generation Cancer Diagnostics market size across rare tumor applications.

By End User: Hospitals Dominate While CROs Accelerate

Hospitals and cancer centers held 46.0% of the Next Generation Cancer Diagnostics market share in 2024, underpinned by integrated pathology-oncology teams and capital resources to operate high-throughput sequencers. Tumor boards rely on on-site genomic data for same-day treatment planning, reinforcing institutional investment.

Contract research organizations, however, lead growth at an 11.3% CAGR. Pharmaceutical sponsors outsource biomarker discovery, patient-stratification, and clinical-trial companion-diagnostic development, adding predictable revenue streams for specialized CROs. Academic medical centers remain hubs for technology validation, while reference laboratories fill capabilities gaps for community clinics, ensuring diversified demand across the Next Generation Cancer Diagnostics market.

Geography Analysis

North America accounted for 41.70% of 2024 revenue, anchored by sophisticated reimbursement mechanisms and rapid FDA breakthrough-device designations. National Comprehensive Cancer Network guidelines routinely embed genomic assays, and payer coverage for several CDx tests approaches nationwide parity. Major academic centers drive early adoption of AI-fusion diagnostics, and venture financing supports startup proliferation. Yet payer scrutiny over test-utilization management introduces near-term volatility in the Next Generation Cancer Diagnostics market.

Europe contributes a sizeable share, shaped by universal healthcare and growing IVDR compliance. Germany and the United Kingdom spearhead uptake, while France and Italy expand precision-oncology budgets. The European Health Data Space promotes cross-border genomic research, although stringent General Data Protection Regulation provisions necessitate decentralized data processing. Harmonized HTA frameworks promise swifter market entry, but interim administrative overhead raises costs. Nevertheless, multi-cancer early-detection pilots in the United Kingdom and Spain foreshadow broader public-health adoption, supporting revenue visibility for vendors in the Next Generation Cancer Diagnostics market.

Asia-Pacific is the fastest-growing region at an 11.8% CAGR. China’s national genomics initiative subsidizes sequencing for lung, gastric, and liver cancers, rapidly scaling domestic test manufacturing. Japan pairs advanced reimbursement with high cancer-screening participation, while India’s Bharat Cancer Genome Atlas uncovers mutation patterns that will influence localized panel design. Singapore positions itself as the regional innovation hub, offering fiscal incentives and streamlined approvals that attract multinational diagnostic firms. Diverse economic profiles across Southeast Asia necessitate tiered-pricing strategies, but rising middle-class demand and expanding insurance coverage create strong underpinnings for the Next Generation Cancer Diagnostics market.

Competitive Landscape

The Next Generation Cancer Diagnostics industry remains moderately fragmented, with platform players, niche specialists, and regional champions jostling for share. Large incumbents leverage scale and regulatory expertise to navigate the FDA’s new laboratory-developed test standards that impose USD 1.29 billion in compliance costs over four years. Companies possessing quality-management infrastructure and pan-cancer assay portfolios are well-positioned to consolidate volumes from smaller laboratories facing rising compliance hurdles.

Strategic acquisitions underpin competitive positioning. RadNet’s USD 60 million purchase of iCAD deepened its AI-enabled breast-imaging pipeline, while Quest Diagnostics expanded its digital-pathology partnership with PathAI to accelerate slide-level analytics. AI algorithm intellectual-property filings surged in 2024–2025, reflecting a race to secure proprietary models that deliver both speed and interpretability. Vendors increasingly emphasize explainable AI features to satisfy clinician adoption criteria within the Next Generation Cancer Diagnostics market.

White-space competition is emerging around decentralized and point-of-care modalities. Quantum-enhanced nanopore detectors promise ultra-low-limit mutation detection for gastrointestinal cancers. Portable plasma-analysis cartridges coupled to smartphone-based readers are under validation in national health systems, challenging centralized laboratory throughput models. As intellectual-property landscapes evolve, collaboration between device makers, reagent suppliers, and cloud-AI vendors is intensifying, reshaping the long-term structure of the Next Generation Cancer Diagnostics market.

Next Generation Cancer Diagnostics Industry Leaders

Roche Diagnostics

Illumina

Thermo Fisher Scientific

Guardant Health

QIAGEN

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Spanish National Cancer Research Centre reported an AI-driven blood test detecting early tumors with 78% accuracy and zero false positives.

- July 2025: Korea Institute of Materials Science unveiled a multifunctional nanodisk enabling simultaneous cancer diagnosis and immune activation.

- May 2025: Chiba University demonstrated microcone-enhanced microfluidic capture of circulating tumor cells exceeding 90% efficiency.

Global Next Generation Cancer Diagnostics Market Report Scope

| Next-Generation Sequencing (NGS) |

| qPCR & Multiplexing |

| Lab-on-a-chip (LOAC) & Reverse Transcriptase-PCR (RT-PCR) |

| Circulating Tumor DNA (ctDNA) Assays |

| Protein Microarrays |

| DNA Microarrays |

| Other Multi-Omics Platforms |

| Breast Cancer |

| Lung Cancer |

| Colorectal Cancer |

| Prostate Cancer |

| Other Cancers |

| Reference Laboratories |

| Hospital & Cancer Centres |

| Academic & Research Institutes |

| Pharmaceutical & Biotech Companies |

| CROs & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Next-Generation Sequencing (NGS) | |

| qPCR & Multiplexing | ||

| Lab-on-a-chip (LOAC) & Reverse Transcriptase-PCR (RT-PCR) | ||

| Circulating Tumor DNA (ctDNA) Assays | ||

| Protein Microarrays | ||

| DNA Microarrays | ||

| Other Multi-Omics Platforms | ||

| By Cancer Type | Breast Cancer | |

| Lung Cancer | ||

| Colorectal Cancer | ||

| Prostate Cancer | ||

| Other Cancers | ||

| By End User | Reference Laboratories | |

| Hospital & Cancer Centres | ||

| Academic & Research Institutes | ||

| Pharmaceutical & Biotech Companies | ||

| CROs & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Next Generation Cancer Diagnostics market in 2025?

The market is valued at USD 15.34 billion in 2024 and is on track to maintain a 9.6% CAGR, implying a 2025 value just above USD 16.8 billion under the current trajectory.

Which technology leads adoption in Next Generation Cancer Diagnostics?

Next-generation sequencing remains the leading technology, holding 55.0% of market share in 2024 due to falling costs and fast turnaround times.

Why is liquid biopsy growing so quickly?

Liquid biopsy offers non-invasive sampling, faster therapy-response insights, and expanding regulatory endorsements, supporting a 14.2% CAGR through 2030.

Which region is expanding fastest in precision-cancer diagnostics?

Asia-Pacific is projected to grow at 11.8% annually as China, Japan, and India ramp up national genomics and screening programs.

How will FDA laboratory-developed test regulations affect the market?

The rule raises compliance costs but also standardizes quality, favoring well-capitalized players and potentially driving industry consolidation over the next four years.

How is Novartis defending Cosentyx against upcoming biosimilars?

Strategies include new indications, device upgrades, patient-support platforms, and multi-region manufacturing expansions.

Page last updated on: