Portable Ultrasound Bladder Scanner Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

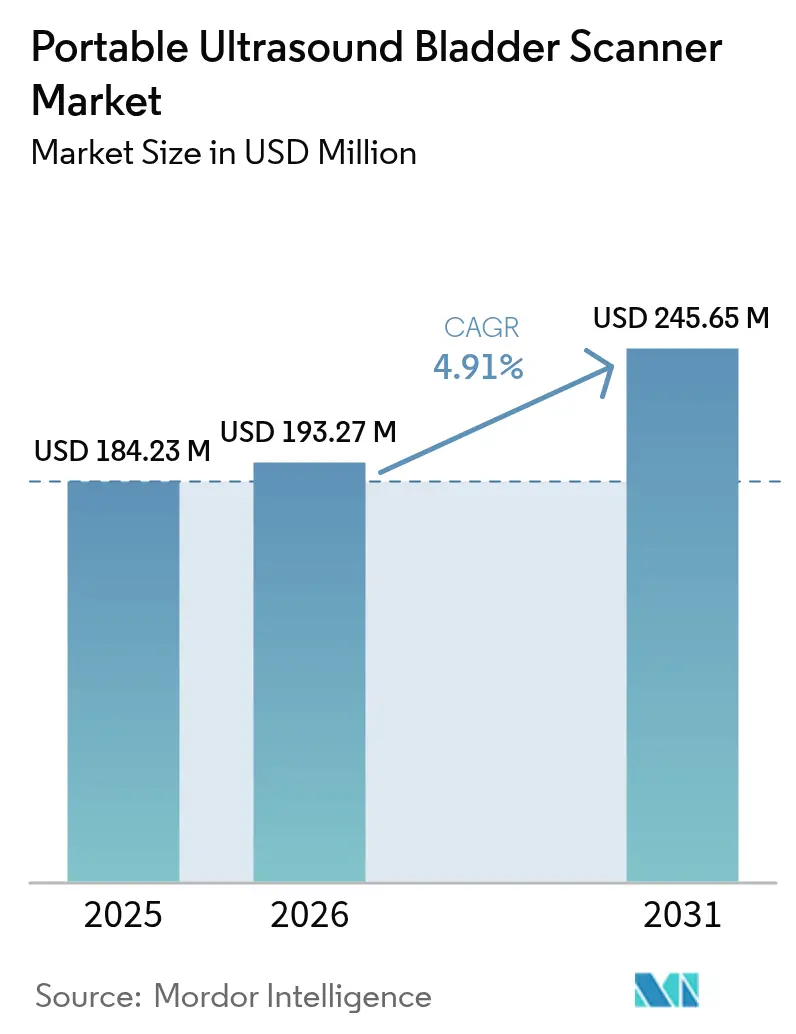

| Market Size (2026) | USD 193.27 Million |

| Market Size (2031) | USD 245.65 Million |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

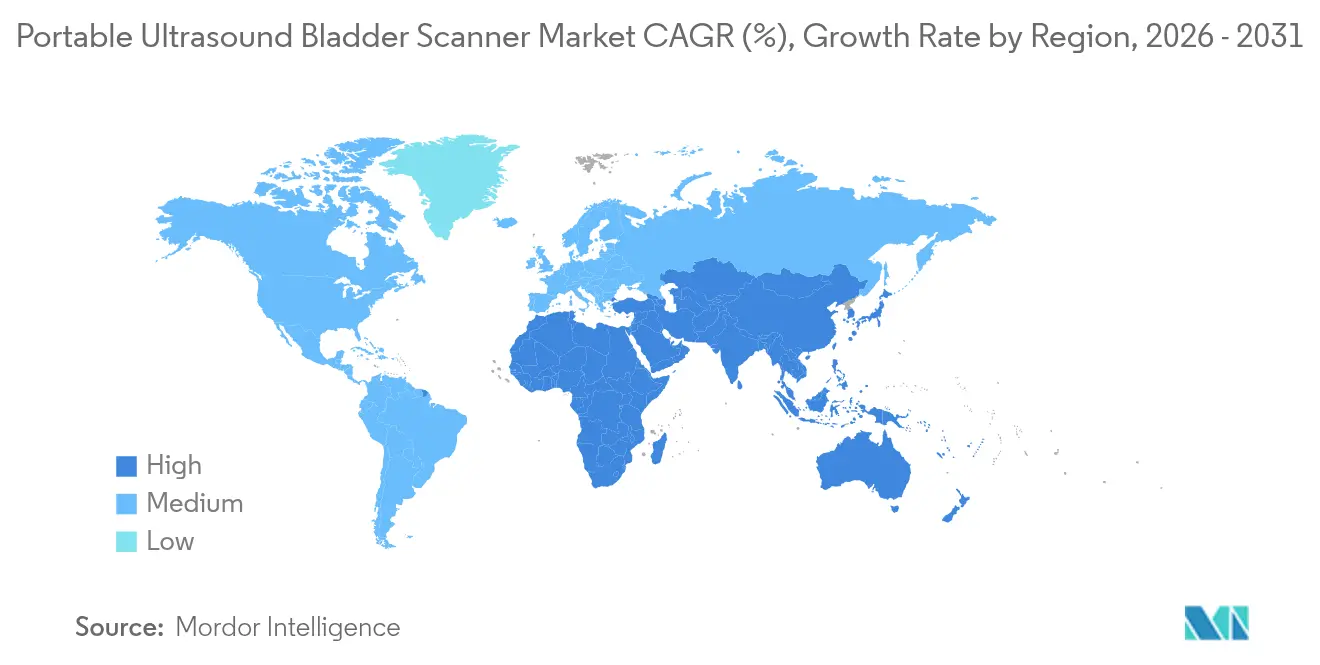

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portable Ultrasound Bladder Scanner Market Analysis by Mordor Intelligence

Portable Ultrasound Bladder Scanner market size in 2026 is estimated at USD 193.27 million, growing from 2025 value of USD 184.23 million with 2031 projections showing USD 245.65 million, growing at 4.91% CAGR over 2026-2031.

This growth continues even as the technology matures and competition intensifies. Aging populations, miniaturization of ultrasound components and favorable reimbursement updates sustain demand, while regulatory complexity and operator-training gaps temper adoption. Market leaders are responding with AI-enabled automation, portfolio expansion and targeted solutions for long-term care, home-care and ambulatory environments. Alongside these drivers, the market is witnessing sharper segmentation dynamics and geographic expansion. Competition features global imaging giants and agile start-ups; both groups are embedding AI to improve accuracy and cut scan time. The single biggest barrier is the persistent shortage of trained users, partly offset by AI tools that automate image capture and interpretation.

Key Report Takeaways

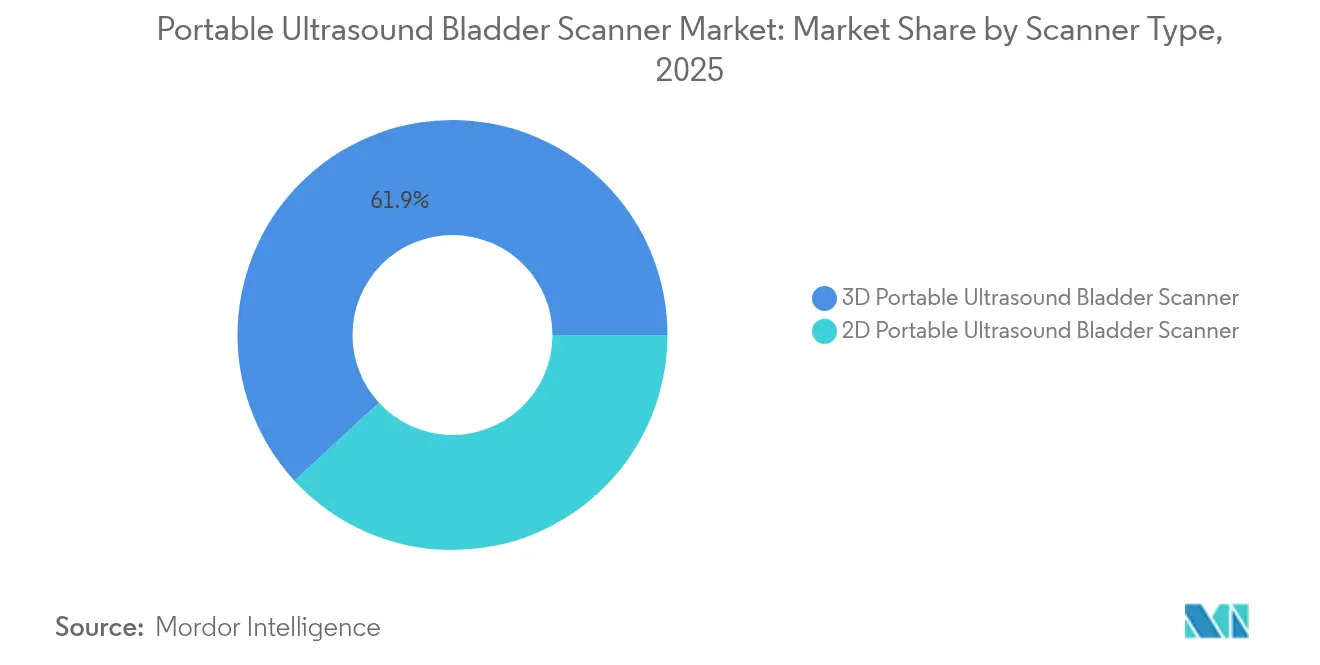

- By scanner type, 3D technology captured 61.85% of the portable ultrasound bladder scanner market share in 2025; 2D technology is expanding at an 8.61% CAGR through 2031.

- By device type, handheld units led with 54.10% revenue share in 2025, while the same segment is projected to post an 10.91% CAGR between 2026 and 2031.

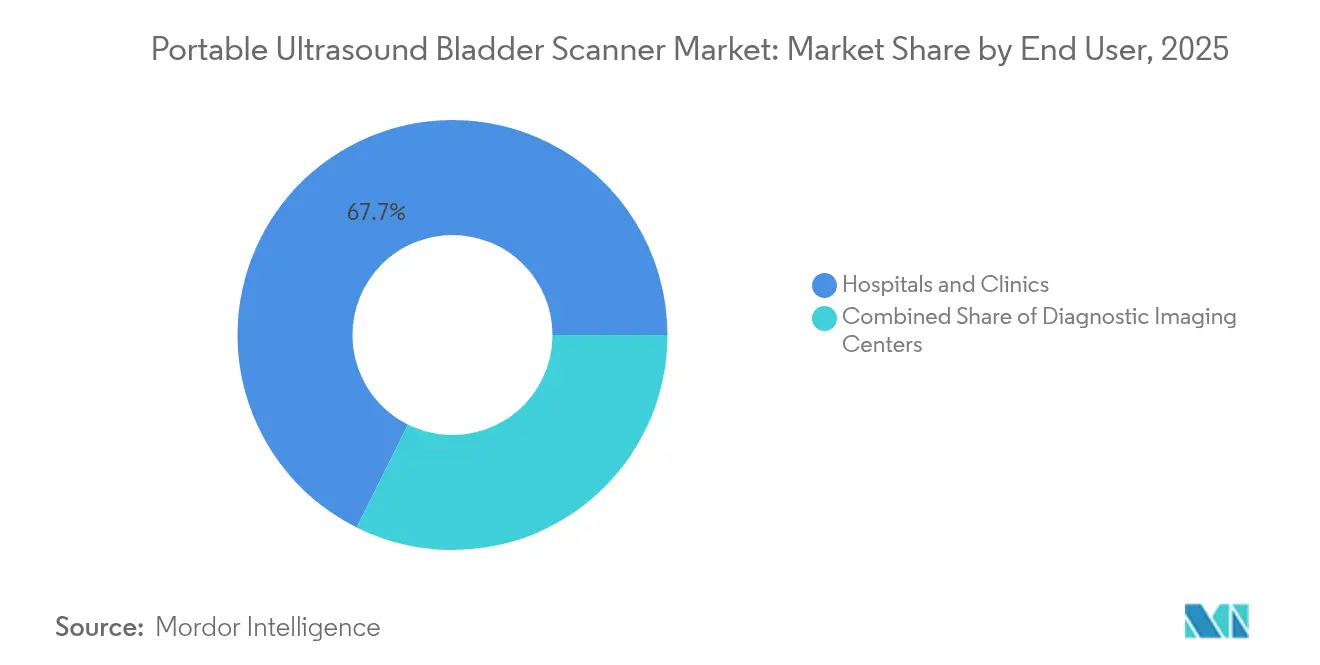

- By end-user, hospitals and clinics held 67.65% of the 2025 portable ultrasound bladder scanner market size, whereas home-care and long-term care facilities are accelerating at 12.83% CAGR during 2026-2031.

- By geography, North America commanded 39.25% of the 2025 portable ultrasound bladder scanner market share; Asia-Pacific is set to grow at 9.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Portable Ultrasound Bladder Scanner Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population surge | +1.8% | North America, Europe, East Asia | Long term (≥4 years) |

| Healthcare shift toward non-invasive POC | +1.5% | North America, Western Europe | Medium term (2-4 years) |

| Continuous innovation in portable platforms | +1.2% | Global | Medium term (2-4 years) |

| Growing adoption of POCUS | +1.0% | Developed healthcare markets | Short term (≤2 years) |

| Rising prevalence of urological disorders | +1.6% | Global | Long term (≥4 years) |

| Integration of AI & smart imaging | +1.4% | Global, innovation hubs in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Population Surge Elevating Demand for Bladder-Volume Monitoring

The number of people aged 65 years and older is climbing at an unprecedented pace, escalating incidence of benign prostatic hyperplasia and related urinary complications. Scientific Reports highlighted 112.5 million BPH cases globally in 2024, with highest prevalence in Eastern Europe, Central Latin America and Andean Latin America. Medicare data further indicate urinary incontinence in 11.2% of beneficiaries, rising to 20.6% in skilled nursing facilities. These demographics elevate routine bladder-volume monitoring, making a compelling clinical and economic case for the portable ultrasound bladder scanner market.

Healthcare Shift Toward Non-Invasive Point-of-Care Diagnostics

Clinical protocols now prioritize infection reduction, patient comfort and rapid decision-making. A 2024 acute-stroke study showed UTIs falling to 4.0% after portable bladder ultrasound adoption, while length-of-stay dropped simultaneously.[1]Tao Chen, “Portable Bladder Ultrasound Lowers UTI Rates in Stroke Care,” BMC Neurology, biomedcentral.com Medicare’s 2025 Physician Fee Schedule introduced telehealth and caregiver-training codes that encourage remote diagnosis tools.[2]Centers for Medicare & Medicaid Services, “CY 2025 Physician Fee Schedule Final Rule,” cms.gov These reforms directly support accelerated uptake in home-care and community settings.

Continuous Innovation in Portable & Handheld Ultrasound Platforms

Manufacturers improve hardware and embed AI algorithms that automate bladder detection and volume calculation. Verathon’s ImageSense keeps error within ±7.5% between 100-999 mL. Samsung Medison bought Sonio to infuse AI across its line-up. Memory-efficient segmentation algorithms further boost 2D performance on resource-constrained chips, cutting cost while sustaining quality .

Growing Adoption of POCUS in Emergency, Critical-Care & Primary Settings

POCUS devices shorten triage times and enhance bedside decision-making. A 2024 cross-sectional comparison of six handheld units found narrowing image-quality gaps; factors like battery life and probe size now drive purchasing.[3]Aarti Soni, “Cross-Sectional Evaluation of Six Handheld Ultrasound Devices,” Ultrasound Journal, springeropen.com Robotic ultrasound prototypes combine sonographer and radiologist roles into one reinforcement-learning-guided unit, pointing to lower operator dependency. Oncology departments use bladder ultrasound to ensure accurate CyberKnife dosing, illustrating expanding application breadth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled operators | -1.3% | Emerging markets, rural areas | Medium term (2-4 years) |

| Variable reimbursement frameworks | -0.9% | Fragmented healthcare systems | Short term (≤2 years) |

| Complex regulatory approval processes | -0.7% | Regions with multi-agency oversight | Medium term (2-4 years) |

| Limited accuracy in complex cases | -0.6% | Patients with pelvic organ prolapse or obesity | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Operators for Ultrasound Interpretation

Formal ultrasound training remains limited across primary-care and long-term care facilities. Although AI features such as automated bladder outlining cut learning curves, these tools still require integration spending and user confidence. Smaller providers hesitate to invest without immediate reimbursement certainty.

Variable Reimbursement & Coding Frameworks Across Regions

Medicare’s 2025 rule acknowledged telehealth ultrasound but omitted specific bladder-scan codes, creating ambiguity. The NIH SEED program emphasized that reimbursement clarity can equal regulatory approval in importance. Manufacturers must customize commercial strategies country by country, delaying uniform rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scanner Type: 3D Lead, 2D Accelerating

3D scanners held 61.85% of 2025 revenue within the portable ultrasound bladder scanner market. Their volumetric precision suits complex anatomy, including prolapse cases where catheterization error risk is high. Nonetheless, 2D scanners are scaling at 8.61% CAGR during 2026-2031 as algorithmic upgrades tighten accuracy bands. Memory-efficient segmentation now runs on lower-cost processors, driving down average selling prices and widening addressable demand. Procurement teams increasingly compare price-performance ratios rather than absolute accuracy, allowing 2D to penetrate resource-constrained settings. The portable ultrasound bladder scanner market size for 2D systems is therefore projected to expand faster than for 3D, though the latter retains hospital preference for high-acuity wards.

Advances in handheld form factors compound the 2D opportunity. Integrated AI makes capturing orthogonal views less operator-dependent, while Wi-Fi connectivity streamlines record transfer. Leading 3D vendors respond by bundling software licenses and extended warranties. Resulting competition improves total cost of ownership for all scanner types, sustaining double-digit shipment growth across emerging economies.

By Device Type: Handhelds Outperform Cart-Based Units

Handheld devices generated 54.10% of 2025 revenue and are on track for 10.91% CAGR to 2031 double the overall portable ultrasound bladder scanner market rate. Clinical trials show handhelds match cart-based diagnostic accuracy for bladder measurements, yet offer bedside convenience and lower maintenance. This parity expands their use in emergency rooms, nursing homes and home-visit programs. The portable ultrasound bladder scanner market size attached to handhelds is forecast to breach USD 151.3 million by 2031, representing the category’s sustained dominance.

Traditional mobile-cart and bench-top units still serve intensive-care wards needing large displays and multi-probe capability. They integrate with hospital PACS systems and remain crucial where traceability rules mandate full DICOM compliance. AI add-ons now optimize these larger systems too, making them relevant even as handhelds gain ground. Decision-makers thus allocate budgets across both tiers, ensuring ecosystem continuity and driving software subscription revenues for manufacturers.

By End User: Home-Care Gains Momentum over Hospitals

Hospitals and clinics controlled 67.65% revenue in 2025 due to entrenched procurement cycles and procedure volumes. Yet the portable ultrasound bladder scanner market is tilting toward decentralized care. Home-care and long-term care facilities record a 12.83% forecast CAGR, underpinned by bundled reimbursement for remote diagnostics and a shift of geriatric services out of hospital walls. Studies show catheterization rates fall 80% when care teams adopt portable scanners, verifying economic returns in community settings.

Diagnostic imaging centers and ambulatory surgery centers are secondary but strategic buyers. They deploy scanners to accelerate throughput and reduce urinary retention complications in day-case procedures. Vendors therefore tailor service contracts, offering mobile-first designs for home-care providers and networked configurations for centralized imaging chains. Such segmentation strategies assure manufacturers access to varied growth pockets inside the portable ultrasound bladder scanner market.

Geography Analysis

North America leads with 39.25% 2025 revenue in the portable ultrasound bladder scanner market, powered by Medicare beneficiaries’ high urinary-incontinence prevalence and supportive device coding. FDA down-classification has shortened time-to-market, fostering quicker portfolio refreshes. Canada trails the United States yet follows similar adoption trajectories, whereas Mexico’s private hospitals spearhead demand within Latin America.

Europe ranks second. Germany posts the highest unit volumes, driven by multi-facility nursing home adoption where indwelling catheter prevalence reached 13.4%. The United Kingdom and France follow, leveraging national health priorities that target hospital-acquired infection reduction. Southern Europe accelerates as aging demographics stretch public healthcare budgets, elevating interest in cost-effective bladder monitoring.

Asia-Pacific delivers the swiftest growth at 9.57% CAGR. China benefits from state investments in primary clinics and the world’s largest elderly cohort. Domestic vendors supply affordable scanners, but multinationals retain premium hospital tiers. Japan’s super-aged society drives high per-capita utilization, while India’s growing middle class catalyzes urban uptake. Strategic acquisitions, such as Samsung Medison’s AI push, further stimulate the regional portable ultrasound bladder scanner market.

Middle East & Africa and South America show steady but uneven progress. GCC states’ hospital modernizations include bladder-scanner deployments, yet rural access lags. Brazil and Argentina dominate South American sales within private urban networks. Urban-rural divides therefore shape localized marketing tactics and after-sales footprints.

Competitive Landscape

Market concentration is moderate. Verathon tops the field through its BladderScan line and ImageSense AI, reinforcing brand loyalty via accuracy claims. GE Healthcare Technologies and Philips diversify from broad ultrasound portfolios into dedicated bladder units, leveraging global service channels. Samsung Medison’s purchase of Sonio signals major imaging vendors’ intent to secure AI talent.

Disruptors include Butterfly Network and Clarius Mobile Health. Butterfly pivoted beyond general ultrasound, launching iQ+ Bladder in May 2024 to address specialized workflows. Clarius won FDA clearance for Bladder AI in January 2024, offering cloud-enabled volume calculation. Start-ups emphasize SaaS revenue, remote updates and subscription models, challenging legacy hardware-centric approaches.

Strategic moves also target underserved segments. Exo’s Iris handheld integrates SweepAI, positioning for home-visits and paramedic fleets. Partnerships with telehealth providers embed bladder scanning into virtual care pathways. The resulting ecosystem competition enhances device capability, lowers unit prices and broadens access across the portable ultrasound bladder scanner market.

Portable Ultrasound Bladder Scanner Industry Leaders

Becton, Dickinson and Company

dBMEDx Inc.

GE Healthcare Technologies Inc.

Caresono Technology Co., Ltd.

Echo-Son SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The County Durham and Darlington NHS Foundation Trust (CDDFT) Charity, patients across County Durham and Darlington are benefiting from new portable bladder scanners costing GBP 10,000 (USD 13,362.4) each. These ultrasound-based devices enable nurses to instantly assess common bladder problems in community clinics or even patients’ homes, providing a non-invasive, quick alternative to catheterization. The scanners help detect incomplete bladder emptying, allowing for timely diagnosis and management, which can prevent deterioration and reduce hospital admissions. The expanded availability of these scanners enhances patient care by enabling immediate results and tailored treatment plans, supported by an increasing specialist nursing team.

- May 2024: Butterfly Network entered the bladder scanner market with the launch of iQ+ Bladder, expanding its portfolio beyond general-purpose ultrasound into specialized clinical applications.

- May 2024: Samsung Medison acquired AI ultrasound company Sonio, signaling a strategic move to enhance its diagnostic capabilities through artificial intelligence integration.

- January 2024: Clarius received FDA 510(k) clearance for its new Bladder AI tool, designed to enhance the capabilities of portable ultrasound bladder scanners by automating volume calculations and reducing operator dependency.

Global Portable Ultrasound Bladder Scanner Market Report Scope

As per the scope, a bladder scanner is a portable, hand-held ultrasound device that can perform a quick, easy, and non-invasive scan of the bladder. Over the years, using such portable ultrasound bladder scanning to detect urinary retention and incomplete bladder emptying has taken over from urethral catheterization.

The portable ultrasound bladder scanner market is segmented by type (2D portable ultrasound bladder scanner and 3D portable ultrasound bladder scanner), end-user (hospitals & clinics and diagnostic centers), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD million) for the above segments.

| 2D Portable Ultrasound Bladder Scanner |

| 3D Portable Ultrasound Bladder Scanner |

| Handheld Portable |

| Mobile-Cart |

| Bench-top |

| Hospitals & Clinics |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Home-Care & Long-Term Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Scanner Type | 2D Portable Ultrasound Bladder Scanner | |

| 3D Portable Ultrasound Bladder Scanner | ||

| By Device Type | Handheld Portable | |

| Mobile-Cart | ||

| Bench-top | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Home-Care & Long-Term Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current portable ultrasound bladder scanner market size and projected growth?

The portable ultrasound bladder scanner market size is USD 193.27 million in 2026 and is forecast to reach USD 245.65 million by 2031, growing at a 4.91% CAGR.

Which scanner technology leads the market today?

3D scanners dominate with 61.85% revenue share in 2025 due to superior volumetric accuracy.

Why are handheld scanners gaining popularity?

Handheld units combine hospital-grade accuracy with portability, fueling an 10.91% CAGR between 2026 and 2031.

Which end-user segment is expanding the fastest?

Home-care and long-term care facilities are advancing at 12.83% CAGR as care shifts outside hospitals.

What role does AI play in new bladder scanners?

AI automates bladder detection and volume calculation, reducing operator dependency and improving workflow efficiency.

Which region offers the highest growth potential?

Asia-Pacific exhibits the fastest expansion at 9.57% CAGR, driven by large elderly populations and rising healthcare investment.

Page last updated on: