Urology Laser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

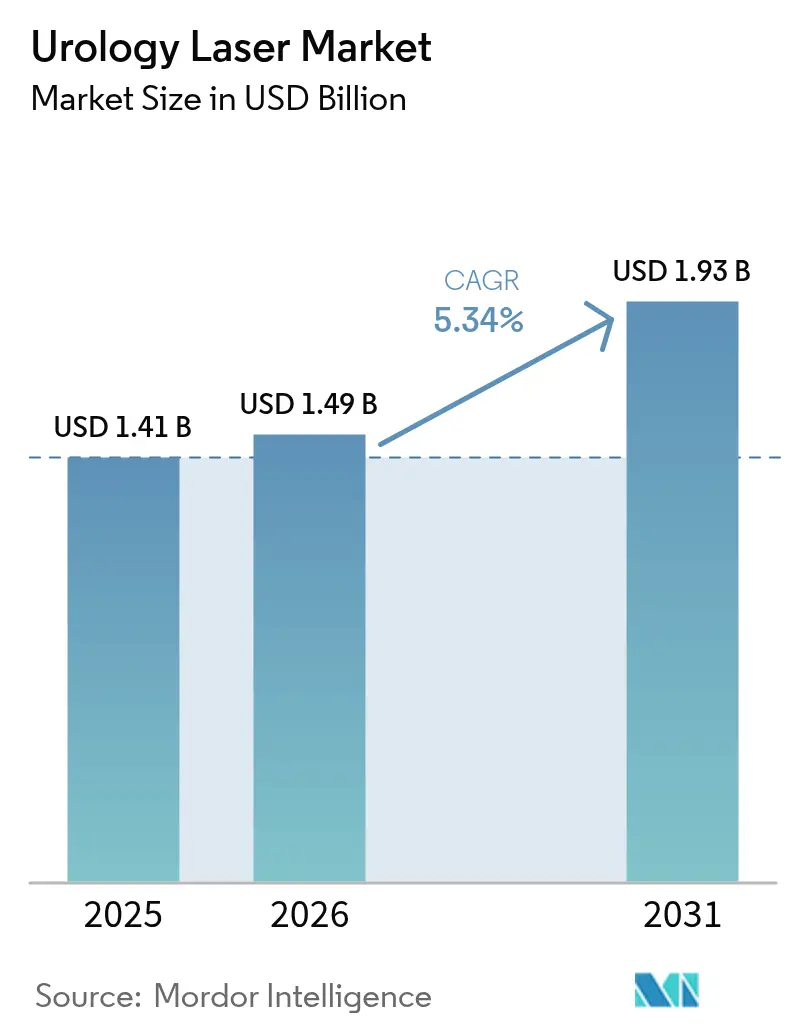

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 1.93 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urology Laser Market Analysis by Mordor Intelligence

The urology laser market size is expected to grow from USD 1.41 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 1.93 billion by 2031 at 5.34% CAGR over 2026-2031. Momentum comes from a steady shift toward minimally invasive techniques that shorten hospital stays, lower complication rates, and raise patient satisfaction. Ambulatory surgical centers (ASCs) now capture a growing share of laser procedures as same-day discharge protocols compress overall treatment costs. Hospital capital budgets reveal preference for multi-application holmium:YAG and thulium fiber platforms that handle lithotripsy, benign prostatic hyperplasia (BPH) surgery, and soft-tissue work in a single footprint. Thulium fiber lasers are winning interest for their reduced retropulsion and superior hemostasis, while pulse-modulated holmium systems equipped with MOSES technology deliver faster case times and clearer visualization. North America leads adoption thanks to stable reimbursement, yet Asia-Pacific is adding capacity the fastest as hospitals in China and India upgrade surgical suites. Supply chain scrutiny around holmium and thulium rare-earth sourcing remains an overhang, pushing vendors to diversify procurement beyond China.

Key Report Takeaways

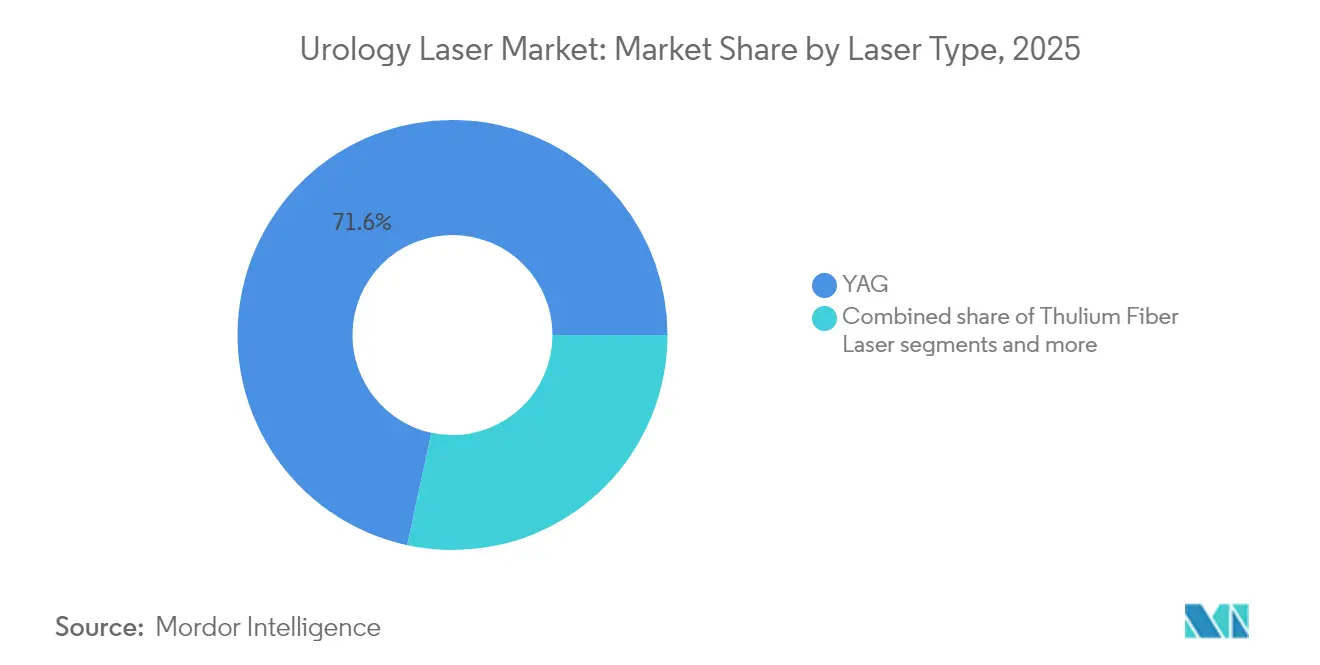

- By laser type, holmium:YAG held 71.62% of the urology laser market share in 2025, while thulium fiber laser platforms are projected to post the highest 5.55% CAGR through 2031.

- By application, stone fragmentation accounted for 48.35% of the urology laser market size in 2025; bladder tumor resection is set to grow the quickest at a 5.72% CAGR up to 2031.

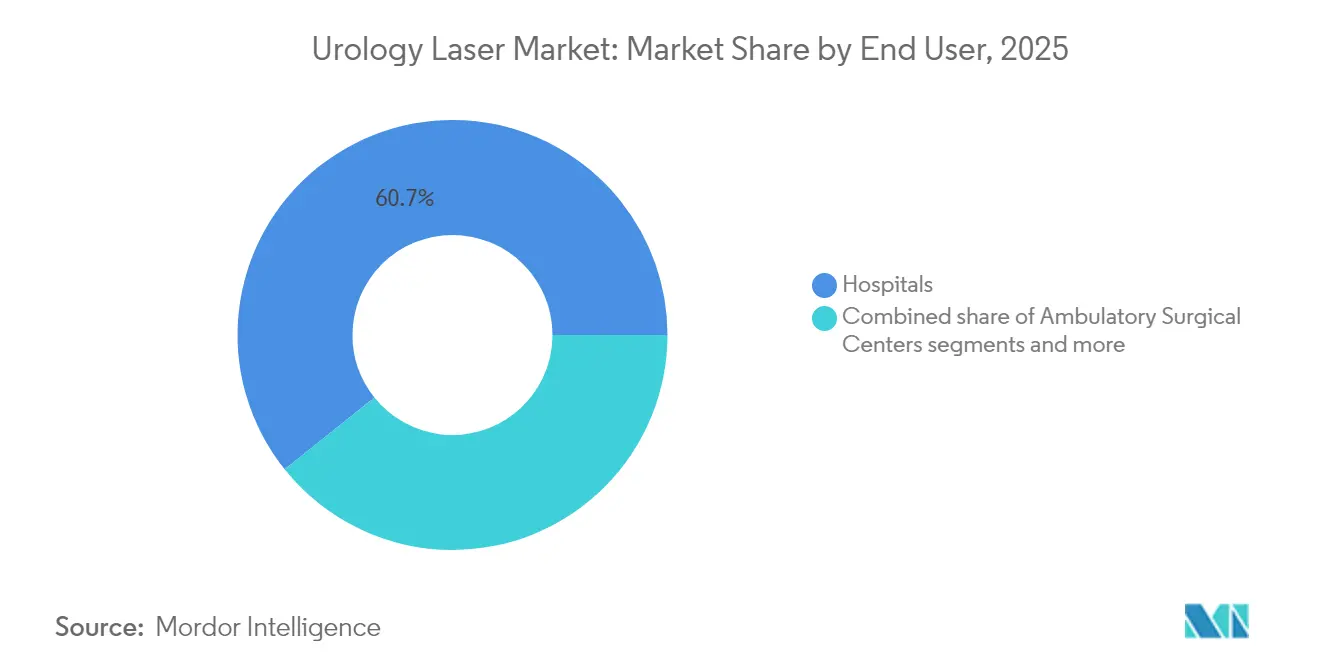

- By end user, hospitals commanded 60.74% revenue in 2025, whereas ambulatory surgical centers are anticipated to expand at a 5.89% CAGR through 2031.

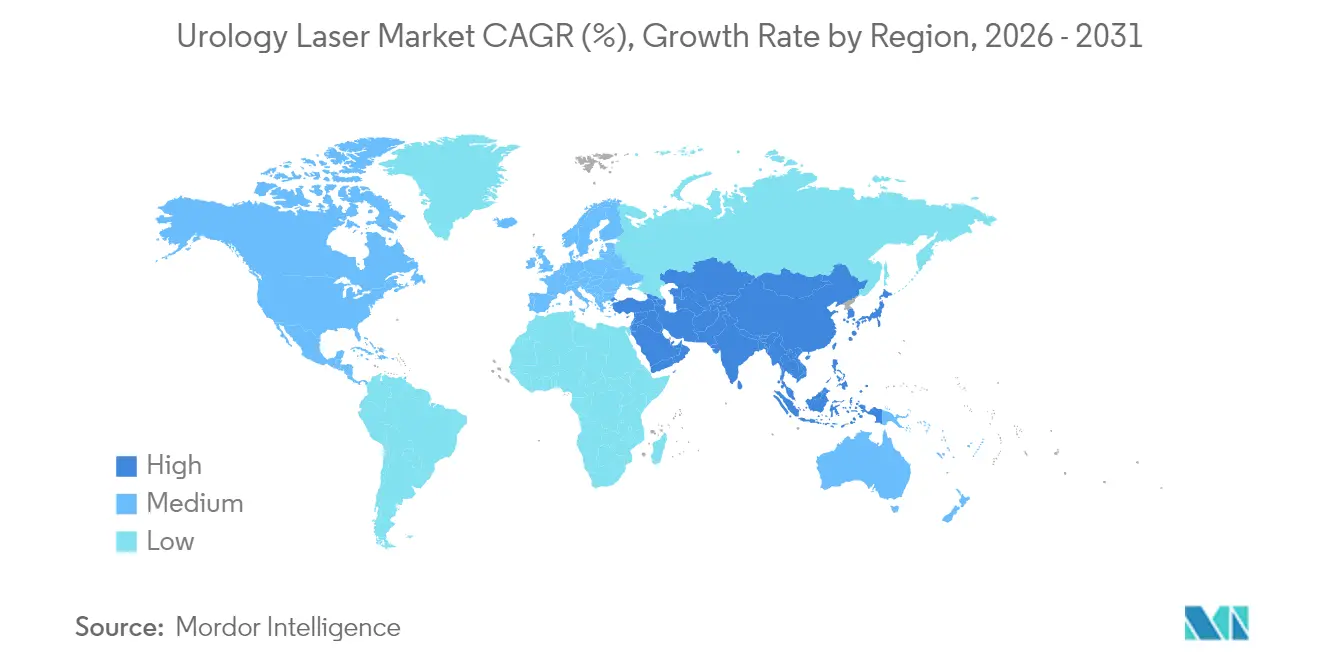

- By geography, North America secured 37.05% of global revenue in 2025; Asia-Pacific is forecast to register the fastest 6.01% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Urology Laser Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of urolithiasis | 1.2% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Growing adoption of minimally invasive BPH surgery | 1.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Technological advancements (e.g., pulse-modulated Ho:YAG) | 1.5% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Hospital CAPEX & reimbursement tailwinds | 0.9% | North America & Europe primarily | Short term (≤ 2 years) |

| ASC day-case surge for laser procedures | 1.1% | North America, expanding to Europe and Asia-Pacific | Short term (≤ 2 years) |

| AI-driven laser parameter optimisation | 0.7% | Global, concentrated in technology-advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Minimally Invasive BPH Surgery

Laser enucleation has replaced transurethral resection as the favored BPH therapy because it yields durable symptom relief, minimal bleeding, and reoperation rates below 1% at 10-year follow-up. MOSES pulse modulation further boosts efficiency, allowing over 90% of treated men to leave on the same day, which trims inpatient costs and frees operating room capacity. Favorable Medicare fee-schedule updates reinforce economic viability and accelerate equipment purchase cycles. Updated American Urological Association guidelines now list holmium laser enucleation as a first-line option for glands of any size, strengthening referral volumes to centers with advanced platforms. Collectively, these clinical and policy tailwinds elevate procedure counts and stimulate recurring fiber sales, underpinning the urology laser market.

Technological Advancements in Pulse-Modulated Ho:YAG Systems

MOSES technology shapes a vapor bubble at the fiber tip, enhancing energy transfer and lowering stone retropulsion. Clinical trials document treatment-time reductions near 40% and demonstrably better hemostasis during prostate enucleation compared with standard holmium pulses. Shorter case times lift surgeon throughput, translating into higher revenue per laser console. Multi-application capability—moving seamlessly from lithotripsy to soft-tissue ablation—improves return on capital investment, prompting hospitals to consolidate disparate devices into a single high-power workstation. Early adopters report standardized outcomes across varied tissue densities and anatomy, dampening the learning curve for complex cases and catalyzing broader uptake. Leading vendors are layering AI algorithms on pulse-modulated systems to auto-adjust parameters based on tissue feedback, pointing to the next wave of performance gains.

Rising Prevalence of Urolithiasis

Kidney-stone incidence has surged roughly 30% in the past decade, a trend linked to high-salt diets, obesity, and warmer climates that favor dehydration. Expanding patient pools translate directly into higher demand for laser lithotripsy, especially for complex calculi that resist shock-wave therapy. Thulium fiber lasers excel in dusting large stones owing to superior absorption in water and lower retropulsion, producing finer fragments that pass spontaneously. More efficient fragmentation allows a shift to outpatient settings, increasing case turnover and profitability for ASCs. As guidelines increasingly recommend laser lithotripsy for difficult stones, procedural volumes continue to climb, reinforcing recurring disposables revenue and widening the addressable urology laser market.

Hospital CAPEX and Reimbursement Tailwinds

Medicare’s 2025 physician fee schedule retains attractive payment for laser-based BPH and lithotripsy, and new CPT codes now reimburse advanced ablation methods. Hospitals responding to value-based mandates view laser consoles as revenue-generating assets that cut postoperative events and shorten length of stay, thus enhancing quality metrics. Vendors counter budget constraints with flexible leasing and usage-based models that smooth cash flow and de-risk procurement. Bundled service contracts lower downtime and simplify compliance, motivating health-system purchasing committees to standardize on single-vendor fleets. This virtuous cycle channels more capital toward upgraded holmium and thulium platforms, sustaining the urology laser market growth trajectory.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs | -1.3% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Steep HoLEP learning curve | -0.8% | Global, particularly in regions with limited training infrastructure | Long term (≥ 4 years) |

| Intra-renal thermal-injury concerns | -0.6% | Global, higher impact in markets with strict liability frameworks | Short term (≤ 2 years) |

| Rare-earth crystal supply-chain risk | -0.5% | Global, concentrated impact on holmium/thulium laser manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs

Advanced laser workstations can list above USD 300,000 and require precision fibers, annual service contracts, and periodic software upgrades that raise ownership costs by another 15-20% per year. Smaller community hospitals and clinics often lack the case volume to amortize such investments, delaying replacement cycles and inhibiting penetration—especially in emerging economies where import tariffs and currency swings inflate prices further. Vendors have responded with pay-per-use and revenue-share arrangements, but senior finance teams still weigh lasers against competing capital needs such as imaging or robotic systems. Until pricing falls or reimbursement rises in budget-sensitive regions, fiscal barriers will temper the otherwise robust growth of the urology laser market.

Steep HoLEP Learning Curve

Holmium laser enucleation demands mastery of anatomical planes and endoscopic dexterity; most surgeons need 50-100 cases before operative times plateau. This protracted learning period limits adoption at centers with low BPH volumes or insufficient mentoring pathways. Staff familiarity with laser safety, fiber handling, and anesthesia nuances is also essential, magnifying workforce training expenses. Simulation modules and proctorships mitigate these hurdles but cannot fully compress the skill-acquisition timeline. Consequently, some facilities defer laser purchases until they secure experienced surgeons, restraining near-term expansion of the urology laser market in less-developed training geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laser Type: Holmium Dominance Faces Fiber Challenge

Holmium:YAG systems retained a 71.62% slice of the urology laser systems market share in 2025, reflecting long-standing clinical proof and surgeon comfort. Yet thulium fiber units are projected to log a 5.55% CAGR and capture incremental revenue as centers seek lower retropulsion and finer dusting for complex calculi. The urology laser systems market size for thulium solutions is forecast to widen particularly in Asia-Pacific where replacement cycles coincide with green-field hospital builds that favor the newest technology.

GreenLight potassium-titanyl-phosphate lasers remain the preferred choice for photoselective vaporization in anticoagulated patients, preserving a focused niche. Diode lasers provide economical entry points for smaller clinics, though their lower power limits procedural breadth. Blue-light systems under investigation show promise for preserving sexual function after BPH surgery, hinting at future niche expansion. Holmium’s versatility in both high-power prostate work and lithotripsy, however, secures its leadership in the urology laser systems market, even as fiber lasers nibble share in select indications.

By Application: Lithotripsy Leadership with Emerging Opportunities

Stone fragmentation represented 48.35% of urology laser systems market revenue in 2025 and continues to anchor console utilization across hospital and ASC settings. Dusting strategies that leave sub-millimeter fragments have reduced scope reinsertion and shortened fluoroscopy exposure, making laser lithotripsy an attractive alternative to shock-wave therapy. Meanwhile, bladder tumor resection holds the fastest projected 5.72% CAGR as en-bloc laser techniques improve histopathological assessment and minimize perforation risk. The urology laser systems market size attributable to BPH procedures is also expanding due to rising life expectancy and guideline shifts favoring laser enucleation.

Ureteroscopic applications benefit from flexible fibers that enable intrarenal access without scope exchange, heightening success rates for proximal calculi. Additional opportunities lie in stricture management and pediatric indications, which leverage the precise ablation and shallow penetration of modern beams. As clinicians broaden procedural menus, the urology laser systems market gains volume resilience against cyclical swings in any single indication.

By End User: Hospital Dominance Amid ASC Surge

Hospitals controlled 60.74% of 2025 revenue owing to multidisciplinary teams, ICU proximity, and established referral flows for high-complexity cases. The urology laser systems market size within hospitals will still climb at mid-single-digit rates as replacement demand and technology upgrades continue. However, ASCs exhibit the highest 5.89% CAGR by harnessing lower overhead, quicker throughput, and rising payer support for outpatient laser surgery.

Specialty clinics carve a profitable niche where concentrated urology expertise ensures strong case density. Academic institutions, while smaller contributors, play an outsized role in proof-of-concept studies that validate new wavelengths and AI modules. The progressive diffusion of skill and technology from tertiary centers to community ASCs signals a gradual redistribution of urology laser systems market revenue toward decentralized care settings over the coming decade.

Geography Analysis

North America captured 37.05% of urology laser systems market revenue in 2025, underpinned by consistent Medicare and private-payer reimbursement, robust surgeon training pipelines, and FDA regulation that balances safety with timely clearances. Academic flagships in the United States set procedural standards that ripple across community hospitals, accelerating diffusion of innovations such as MOSES pulse modulation and AI-guided parameter selection. Consolidated group purchasing further supports large-scale console rollouts that lock in vendor partnerships and boost fiber pull-through.

Asia-Pacific is projected to advance at a 6.01% CAGR through 2031, the fastest regional clip in the urology laser systems market. China’s hospital-modernization push and India’s expanding insurance penetration are swelling procedure volumes, while manufacturers add regional assembly lines that temper import costs. Surgeons in Japan and South Korea—already adept with high-tech devices—are early adopters of thulium fiber and AI-enhanced consoles. Favorable government investments in medical tourism hubs, notably in Thailand and Singapore, foster demand for cutting-edge laser suites, further expanding the geographic footprint of the urology laser systems market.

Europe maintains steady mid-single-digit growth powered by universal coverage schemes that emphasize evidence-based care. Germany and the United Kingdom spearhead adoption of en-bloc bladder tumor resection, while the Nordic countries pilot AI-driven lasers within robotic programs. Harmonized CE requirements simplify vendor launches across the bloc, though budget austerity in Southern Europe slightly tempers capital spending. In emerging regions of South America and the Middle East & Africa, urology laser systems market penetration remains low but rising, led by private-sector centers catering to expatriate and affluent local populations.

Competitive Landscape

The urology laser systems market is moderately consolidated. Boston Scientific’s 2024 acquisition of Lumenis’s surgical unit fused holmium and thulium assets, creating a full-line franchise that spans consoles, fibers, and disposables. KARL STORZ in 2024 added Asensus Surgical to integrate digital-surgery analytics with its visualization and laser offerings. Olympus broadened its reach in 2025 with the European launch of air-cooled SuperPulsed thulium fiber systems that plug into standard outlets, directly targeting ASC buyers.

Strategic competition centers on three pillars: wavelength versatility, AI-enabled workflow, and lifetime service economics. Vendors bundle disposables, software upgrades, and onsite training in multi-year agreements that lock in share and raise switching costs. Supply-chain resilience has also become a differentiator as firms diversify rare-earth supply away from China, with several negotiating contracts in Australia and the United States.

White-space opportunities include pediatric urology, energy-based adjuvant oncology, and integration with miniaturized robotic scopes. The combined share of the top five participants hovers near 55%, implying room for mid-tier innovators but also setting the stage for further takeovers as incumbents seek incremental share in the expanding urology laser systems market.

Urology Laser Industry Leaders

Boston Scientific Corporation

Richard Wolf GmbH

Medtronic

ALLENGERS MEDICAL SYSTEMS LIMITED

biolitec AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: KARL STORZ completed the business transfer of medi-G, adding sustainable Meßkirch capacity for complex assemblies used in urology

- October 2024: Lumenis France signed a distribution pact with X-Derma to strengthen commercial reach in the French market

Global Urology Laser Market Report Scope

As per the scope of this report, urological lasers are medical devices used to treat various urological diseases, including benign prostatic hyperplasia, urolithiasis, and non-muscle-invasive bladder cancer. The urology laser market is segmented by laser type, application, and geography. By laser type, the market is segmented into holmium laser system, diode laser system, thulium laser system, and other laser types. By application, the market is segmented into benign prostatic hyperplasia, urolithiasis, non-muscle-invasive bladder cancer, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Holmium:YAG Laser |

| Thulium Fiber Laser |

| GreenLight (KTP/LBO) Laser |

| Diode Laser |

| Others (Er:YAG, CO₂, etc.) |

| Lithotripsy |

| Benign Prostatic Hyperplasia (BPH) |

| Ureteroscopy |

| Bladder Tumor Resection |

| Others (Stricture, Caruncle, Soft-tissue) |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Others (Academic/Research Labs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Laser Type | Holmium:YAG Laser | |

| Thulium Fiber Laser | ||

| GreenLight (KTP/LBO) Laser | ||

| Diode Laser | ||

| Others (Er:YAG, CO₂, etc.) | ||

| By Application | Lithotripsy | |

| Benign Prostatic Hyperplasia (BPH) | ||

| Ureteroscopy | ||

| Bladder Tumor Resection | ||

| Others (Stricture, Caruncle, Soft-tissue) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Others (Academic/Research Labs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the urology laser systems market?

The market is valued at USD 1.49 billion in 2026 and is set to hit USD 1.93 billion by 2031.

Which laser technology commands the largest market share?

Holmium:YAG platforms held 71.62% of 2025 revenue owing to versatile use in lithotripsy and BPH surgery.

Which application segment will grow the fastest through 2031?

Bladder tumor resection is forecast to post a 5.72% CAGR, outpacing other indications.

Why are ambulatory surgical centers important for future growth?

ASCs enable same-day discharge, lower facility fees, and are projected to log a 5.89% CAGR, bolstering equipment demand.

What is driving Asia-Pacific s rapid expansion?

Hospital build-outs, rising insurance coverage, and adoption of advanced thulium fiber systems fuel a regional 6.01% CAGR.

How are supply-chain risks being managed?

Vendors are diversifying rare-earth sourcing beyond China to stabilize holmium and thulium crystal availability and pricing.

Page last updated on: