Urinary Tract Infection Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 717.49 Million |

| Market Size (2031) | USD 894.56 Million |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urinary Tract Infection Testing Market Analysis by Mordor Intelligence

The Urinary Tract Infection Testing Market size is estimated at USD 717.49 million in 2026, and is expected to reach USD 894.56 million by 2031, at a CAGR of 4.51% during the forecast period (2026-2031).

Rapid escalation of antimicrobial resistance, demographic aging, and payers’ push for evidence-based prescribing are steering laboratories and clinicians toward faster, more accurate pathogen identification. Hospitals rely on molecular panels that deliver results within 90 minutes to comply with sepsis bundles, while pharmacies, retail clinics, and telehealth portals popularize smartphone-read dipsticks priced below USD 15 per test. The United States drives early adoption through Medicare reimbursement for CLIA-waived analyzers. Yet, the Asia-Pacific build-out of 150,000 wellness centers under India’s National Health Mission is propelling the fastest regional growth. Competitive intensity is rising as digital-health entrants challenge incumbent diagnostics firms with FDA-cleared apps that match laboratory sensitivity and add subscription pricing. Susceptibility testing is the hottest product niche, with a 6.54% CAGR, driven by mandates requiring culture and sensitivity data before prescribing fluoroquinolones or third-generation cephalosporins.

Key Report Takeaways

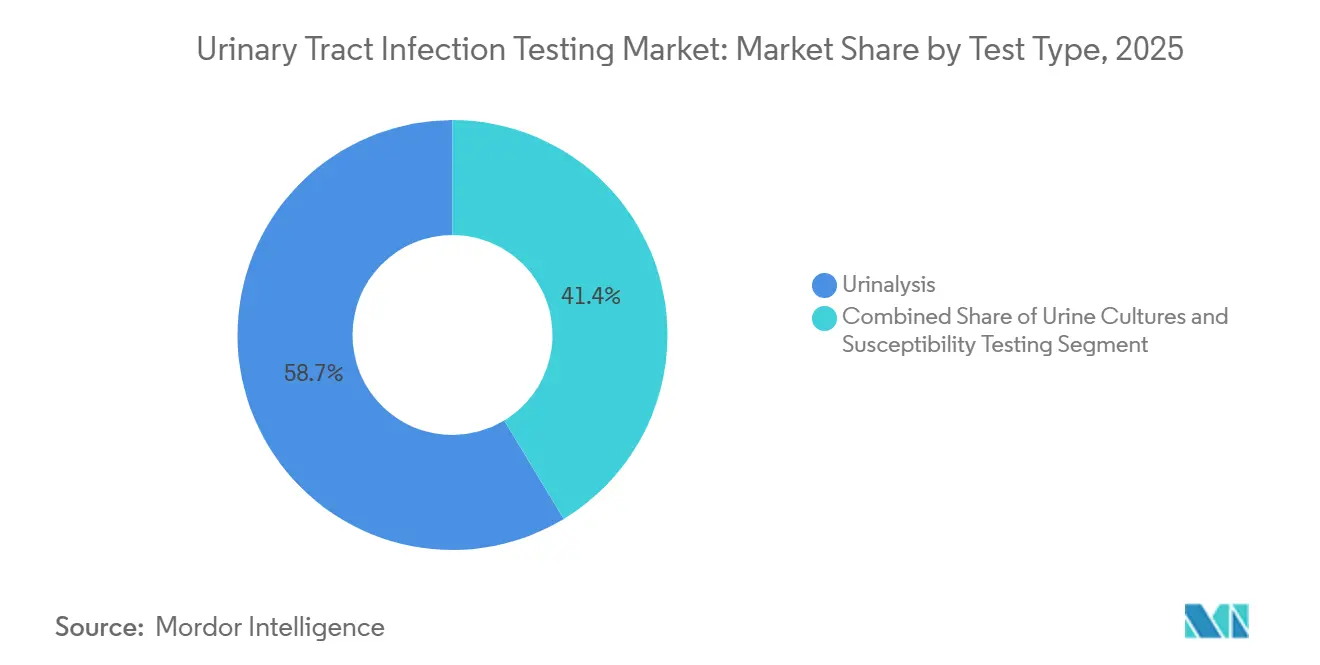

- By test type, urinalysis led with 58.65% revenue share in 2025, while susceptibility testing is advancing at a 6.54% CAGR through 2031.

- By kit type, laboratory test kits accounted for 72.45% of 2025 revenue, whereas home test kits are expanding at a 6.76% CAGR to 2031.

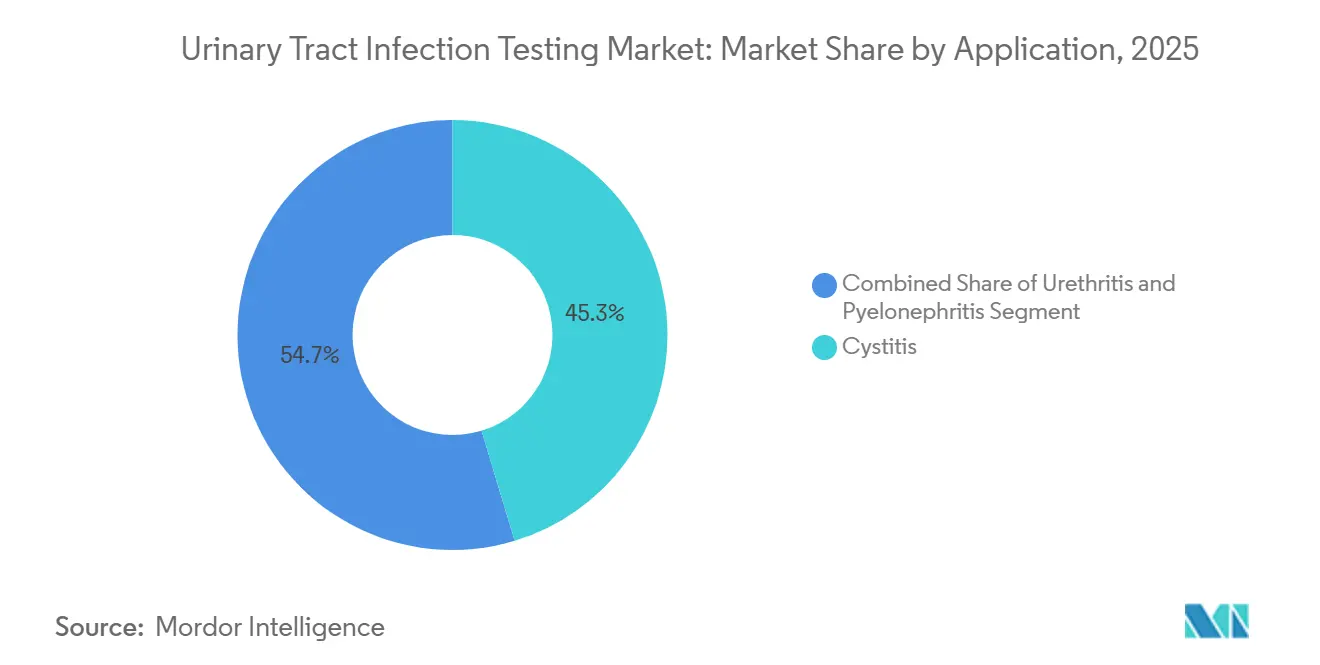

- By application, cystitis held 45.32% of 2025 revenue, and pyelonephritis testing is growing at a 7.21% CAGR through 2031.

- By end user, hospitals captured a 57.65% share in 2025, yet home care settings are progressing at a 7.86% CAGR to 2031.

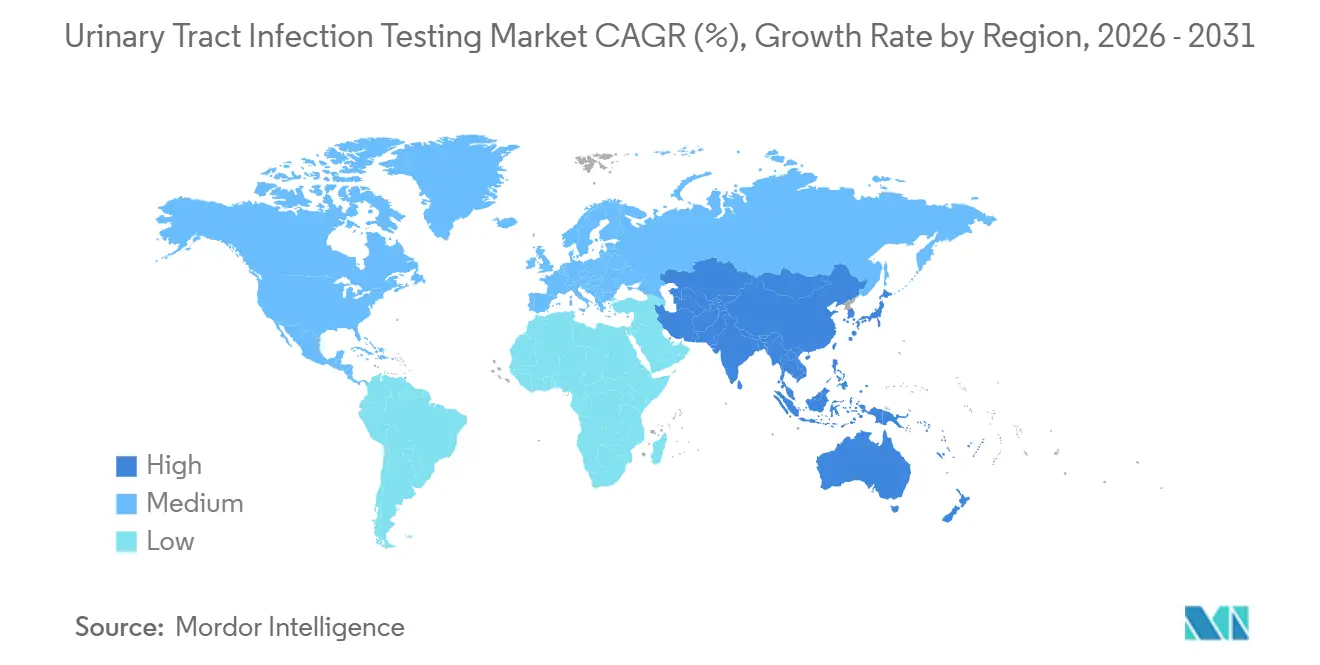

- Geographically, North America retained 42.65% of 2025 revenue; Asia-Pacific is the fastest-growing region, with a 5.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Urinary Tract Infection Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Urinary Tract Infections Worldwide | +1.2% | Global, with highest burden in low-middle SDI regions | Long term (≥ 4 years) |

| Growing Geriatric And Immunocompromised Populations | +1.0% | North America, Europe, Japan; emerging in China | Medium term (2-4 years) |

| Increasing Adoption Of Point-Of-Care Urinalysis Devices | +0.9% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Expanding Healthcare Expenditure And Infrastructure | +0.7% | APAC core, Middle East, Latin America | Long term (≥ 4 years) |

| Integration Of At-Home UTI Self-Testing With Telehealth Platforms | +0.5% | North America, Northern Europe | Short term (≤ 2 years) |

| AI-Driven Image-Based Urinalysis Enhancing Diagnostic Accuracy | +0.4% | North America, select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Urinary Tract Infections Worldwide

The Global Burden of Disease Study 2021 recorded 404.6 million prevalent UTI cases and 236,790 related deaths, a 63.5% rise in age-standardized prevalence since 1990. Women face a 60% lifetime risk and recurrent infection rates of 25% within six months, driving repeated testing volumes in primary care. CDC surveillance showed 15.3% of 2024 Escherichia coli urine isolates carried extended-spectrum beta-lactamases, up from 11.2% in 2019, compelling laboratories to run susceptibility panels. Catheter-associated UTIs account for 75% of healthcare-associated infections in intensive care units, and CMS penalizes hospitals in the worst-performing quartile, promoting proactive screening. Low- and middle-income countries experience the highest morbidity yet maintain the lowest laboratory capacity, underscoring the need for affordable dipstick tests.

Growing Geriatric and Immunocompromised Populations

Adults aged 65 plus register UTI incidence three times higher than younger adults due to incomplete bladder emptying, estrogen decline, and prostatic hypertrophy[1]National Institute on Aging, “Urinary Tract Health,” nia.nih.gov. The United Nations data project 1.6 billion seniors by 2050, doubling from 2022, with Japan, Italy, and Germany already exceeding 28% elderly share. Immunocompromised cohorts—including transplant recipients, HIV patients, and cancer survivors—experience five- to ten-fold higher UTI risk. Diabetes affects 537 million adults worldwide, and glycosuria doubles their infection probability. Long-term care facilities log 1.8 episodes per 1,000 resident-days, making UTIs the top reason for antibiotic use and a focal point for stewardship programs.

Increasing Adoption of Point-Of-Care Urinalysis Devices

CLIA-waived analyzers such as Siemens Clinitek Novus and Roche cobas u 411 deliver results in under 10 minutes, slashing the traditional 24-hour wait. Medicare boosted reimbursement to USD 4.12 per CLIA-waived urinalysis in 2024, improving office economics. Molecular panels like Cepheid Xpert Xpress UTI detect over 20 pathogens and 10 resistance genes within 90 minutes, cutting emergency-department antibiotic adjustment time by 8.3 hours in a 2025 study. EU in vitro diagnostic regulations now require equivalence studies, raising compliance costs but bolstering clinician confidence.

Integration of At-Home UTI Self-Testing with Telehealth Platforms

Smartphone-based dipsticks from Scanwell Health and Healthy.io enable patients to complete testing, a virtual consultation, and an e-prescription within 2 hours. Anthem and UnitedHealthcare began reimbursing up to USD 25 per home test when linked to a telehealth visit, encouraging the use of payer-approved pathways. A 2025 JAMA Network Open study reported 94.2% concordance between smartphone-read dipsticks and laboratory urinalysis for leukocyte esterase and nitrite results. FDA’s 2025 draft guidance on digital health requires algorithm performance data across lighting and user profiles, raising the accuracy bar. Subscription models, such as MyUTI’s USD 19.99 monthly unlimited testing offer, target the 15% of women who have 3 or more annual episodes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced molecular and culture-based tests | -0.8% | Global, most acute in low- and middle-income regions | Medium term (2-4 years) |

| Stringent regulatory approval pathways for novel kits | -0.6% | North America, Europe | Short term (≤2 years) |

| Environmental disposal concerns for single-use plastic test kits | -0.4% | Global, heightened in regions with strict green mandates | Medium term (2-4 years) |

| Rising false-positive rates prompting clinician skepticism | -0.3% | North America, Europe, selected APAC markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Molecular and Culture-Based Tests

Molecular panels range from USD 75 to USD 150 per test, versus USD 8 to USD 15 for conventional culture, limiting uptake in cost-constrained systems. Cepheid cartridges retail near USD 90, while Medicare reimburses USD 68.40, leaving modest margins for rural hospitals. BioFire FilmArray Torch needs a USD 50,000 capital outlay and USD 120 per test, confining use to tertiary centers. India’s National Health Mission reimburses urine culture at INR 150 (USD 1.80), rendering molecular diagnostics unaffordable in public hospitals. UnitedHealthcare restricts molecular panels to complicated infections, denying coverage for routine cystitis. Roche introduced the cobas Liat UTI panel at USD 65 yet demand still concentrates in high-acuity sites.

Stringent Regulatory Approval Pathways for Novel Kits

FDA 510(k) submissions require 500-plus participant clinical studies and average 18-24 months, costing USD 2 million-USD 5 million[2]U.S. Food and Drug Administration, “Premarket Notification 510(k) Guidance,” fda.gov. AST devices now need head-to-head comparisons against broth microdilution across 20 organisms and 15 drug classes, delaying launches. EU rules reclassified many UTI tests to Class C, mandating notified-body audits that add EUR 500,000-EUR 1 million in compliance costs[3]European Commission, “In Vitro Diagnostic Regulation Overview,” ec.europa.eu. Home-use kits must show lay-user accuracy within 5% of that of laboratory technicians; two startups withdrew their 2025 applications after missing this bar. Post-market vigilance is stricter, with 2025 label updates mandated for 18 dipstick brands following false-positive alerts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Susceptibility Testing Gains as Resistance Escalates

Urinalysis commanded 58.65% of 2025 revenue, anchored by its role as the first screen in primary care and emergency departments. Yet its single-digit growth contrasts with the 6.54% CAGR recorded by susceptibility testing, the fastest-growing component of the urinary tract infection testing market. Bruker’s MALDI-TOF Biotyper now integrates with MBT-ASTRA software to provide species identification and MIC results within 6 hours, enabling same-day antibiotic optimization. Accelerate Diagnostics’ PhenoTest BC offers morphokinetic analysis, delivering results in seven hours. Regulatory guidance aligning AST interpretive categories with CLSI breakpoints is reinforcing clinician trust.

The urinary tract infection testing market size for susceptibility testing is projected to grow from USD n/a in 2026 to USD n/a in 2031 as hospitals embed antibiotic-stewardship dashboards. Molecular resistance marker panels, such as Cepheid Xpert Carba-R, identify ESBL and carbapenemase genes in 90 minutes, corresponding to the 15.3% ESBL burden found in 2024 U.S. surveillance. These rapid phenotypic and genotypic tools are displacing two-day culture workflows, cutting broad-spectrum antibiotic exposure and associated costs.

By Test Kit Type: Home Kits Accelerate Amid Telehealth Integration

Laboratory kits held a 72.45% share in 2025, powered by high-throughput analyzers such as Sysmex UN-Series and Siemens Atellica UAS 800, which process up to 240 samples per hour. Culture workflows using BD Phoenix or Beckman Coulter MicroScan remain the gold standard for definitive diagnosis, maintaining the largest share of the hospital urinary tract infection testing market.

Home kits deliver the growth upside, rising 6.76% annually as dipstick readers integrate into virtual care pathways. Scanwell Health shipped 1.2 million tests in 2025 through 9,000 U.S. pharmacies. Healthy.io entered employer wellness bundles, and Everly Health bundles UTI and STI screening. FDA-cleared smartphone readers showed 94.2% concordance with laboratory analyzers in 2025 validation, diffusing earlier doubts. Reimbursement support from Anthem and UnitedHealthcare is cementing demand and broadening consumer access.

By Application: Pyelonephritis Testing Intensity Rises with Sepsis Protocols

Cystitis accounted for 45.32% of 2025 revenue, the most prevalent presentation. Rising fluoroquinolone resistance, touching 25% in some U.S. regions, is increasing culture orders even for outpatient cases. Urethritis remains niche, mostly in sexual-health clinics, combining urinalysis and NAATs for sexually transmitted pathogens.

Pyelonephritis is growing fastest, with a 7.21% CAGR. CMS requires blood cultures and broad-spectrum antibiotics within three hours of presentation for suspected sepsis, driving hospitals to adopt rapid molecular UTI panels like Cepheid Xpress, which cut inappropriate carbapenem use by 18% in 2024 emergency-department studies. Imaging-confirmed upper-tract infections double hospital stays and increase diagnostic costs, reinforcing intensive testing with susceptibility panels.

By End User: Homecare Settings Surge as Virtual Care Expands

Hospitals captured 57.65% of 2025 demand, anchored by emergency departments, which process 12 million U.S. UTI visits each year. Reference laboratories such as Quest Diagnostics and Labcorp use automation to handle 80 million urine cultures annually. However, home care dominates growth, with a 7.86% CAGR, as payers push uncomplicated UTI management out of emergency departments and onto virtual platforms.

Direct-to-consumer channels completed 8 million tests in 2025, lowering payer costs by USD 22 million for Anthem members when tied to telehealth visits. Long-term care facilities adopt CLIA-waived analyzers to satisfy CMS infection-prevention mandates. Medicare’s 2025 fee schedule uplift for remote therapeutic monitoring supports home health agencies in embedding UTI screening in chronic-disease protocols.

Geography Analysis

North America remained the largest region, accounting for 42.65% of 2025 revenue. CMS reimbursement for CLIA-waived urinalysis and Medicare penalties for catheter-associated infection rates incentivize rapid testing adoption. Canada pilots point-of-care urinalysis in remote Indigenous communities to offset a 40% higher UTI burden. Mexico’s social-security system procured 2.3 million rapid kits to relieve emergency stalls.

The urinary tract infection testing market in the Asia-Pacific is growing at a 5.64% CAGR. China’s USD 850 billion Healthy China 2030 plan equips 150,000 township clinics with urinalysis capability, and India is deploying the same number of wellness centers under its National Health Mission. Japan approved reimbursement for AI-augmented sediment analysis in 2025 to serve its 29.1% share of the senior population. Australia subsidizes home kits under the Pharmaceutical Benefits Scheme, and South Korea funds molecular panels for immunocompromised patients.

Europe maintains broad testing through statutory insurance; Germany reimburses urinalysis at EUR 3.50, supporting volumes across 1,900 laboratories. The United Kingdom’s 2024 pathway requires culture after the third cystitis episode, lifting laboratory tests 18%. Saudi Arabia installed 22 high-throughput analyzers across 500 centers, and Brazil’s Unified Health System bought 1.2 million rapid kits for urban favelas. South Africa’s mobile units shrink rural turnaround from seven days to 24 hours.

Competitive Landscape

Five global companies—Abbott, F. Hoffmann-La Roche Ltd, BD, Siemens Healthineers, and Danaher’s Cepheid—held roughly 45% combined share in 2025, giving the urinary tract infection testing market a moderately concentrated profile. Incumbents protect hospital channels through long-term reagent contracts and integrated data systems, yet digital-health startups like Scanwell Health and Healthy.io bypass these moats by selling smartphone-read dipsticks through retail pharmacies. Abbott ID NOW and Cepheid GeneXpert sustain emergency-department demand by delivering sub-90-minute results with resistance markers. MALDI-TOF systems from Bruker and bioMérieux are displacing biochemical methods by shortening species-identification time from 24-48 hours to six hours. Smaller vendors, including Sysmex and 77 Elektronika, undercut capital prices by 15-20% to penetrate mid-tier hospitals.

Regulation drives consolidation. FDA 510(k) requirements mandate multi-site clinical validation, and the EU IVD Regulation requires notified-body audits, prompting large firms to acquire startups with promising technology pipelines. AI-enabled sediment analysis received 12 FDA clearances between 2024 and mid-2025, signaling software differentiation as a new competitive axis. White-space remains in long-term care surveillance and in low-income regions that need low-cost, CLIA-waived analyzers and smartphone-read dipsticks.

Urinary Tract Infection Testing Industry Leaders

F. Hoffmann-La Roche Ltd

Abbott Laboratories

Becton, Dickinson And Company

Danaher Corporation

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Biotia launched a new “test to treat” option for patients suffering from recurrent urinary tract infections (UTIs), moving UTI care forward. This solution allows patients to collect a urine sample for more advanced laboratory testing, and receive virtual care from clinicians trained specifically in recurrent UTI treatment – all from the privacy of their home.

- January 2025: F. Hoffmann-La Roche Ltd launched the cobas Liat UTI panel in the United States, delivering 20-pathogen, 10-gene results in 20 minutes at USD 65.

- September 2024: Mankind Pharma Ltd. launched RAPID NEWS self-test kits to detect health issues like dengue, UTIs, and early menopause. The innovation promotes accessible and private healthcare for individuals across India. This launch marks a significant step toward convenient, rapid testing solutions.

Global Urinary Tract Infection Testing Market Report Scope

As per the scope of the report, urinary tract infection (UTI) testing involves analyzing urine samples to detect bacterial infections in the urinary system. It helps diagnose the presence of bacteria, white blood cells, or blood indicating an infection. UTI tests are essential for guiding appropriate treatment and management of the condition.

The Urinary Tract Infection Testing Market is Segmented by Test Type (Urinalysis, Urine Cultures, and Susceptibility Testing), Test Kit Type (Laboratory Test Kits and Home Test Kits), Application (Urethritis, Cystitis, and Pyelonephritis), End User (Hospitals, Diagnostic Laboratories, Homecare Settings, and Other End User), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Urinalysis |

| Urine Cultures |

| Susceptibility Testing |

| Laboratory Test Kits |

| Home Test Kits |

| Urethritis |

| Cystitis |

| Pyelonephritis |

| Hospitals |

| Diagnostic Laboratories |

| Homecare Settings |

| Other End User |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Urinalysis | |

| Urine Cultures | ||

| Susceptibility Testing | ||

| By Test Kit Type | Laboratory Test Kits | |

| Home Test Kits | ||

| By Application | Urethritis | |

| Cystitis | ||

| Pyelonephritis | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Homecare Settings | ||

| Other End User | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the urinary tract infection testing market in 2026?

The urinary tract infection testing market size stands at USD 717.49 million in 2026.

What is the projected CAGR for urinary tract infection testing through 2031?

The market is forecast to expand at a 4.51% CAGR between 2026 and 2031.

Which test type is growing fastest?

Susceptibility testing is advancing at a 6.54% CAGR as antibiotic-stewardship rules demand documented sensitivity results.

Why are home UTI test kits gaining popularity?

Smartphone-read dipsticks tied to telehealth visits deliver results and prescriptions within two hours and now receive payer reimbursement up to USD 25 per test.

Which region is the fastest-growing for UTI testing?

Asia-Pacific leads with a 5.64% CAGR, driven by China's and India's primary-care infrastructure expansion.

What technology trends shape competitive advantage?

Rapid molecular panels, AI-augmented sediment analysis, and MALDI-TOF identification shorten turnaround times, meeting sepsis bundle and stewardship requirements.

Page last updated on: