Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.11 Billion |

| Market Size (2031) | USD 21.93 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

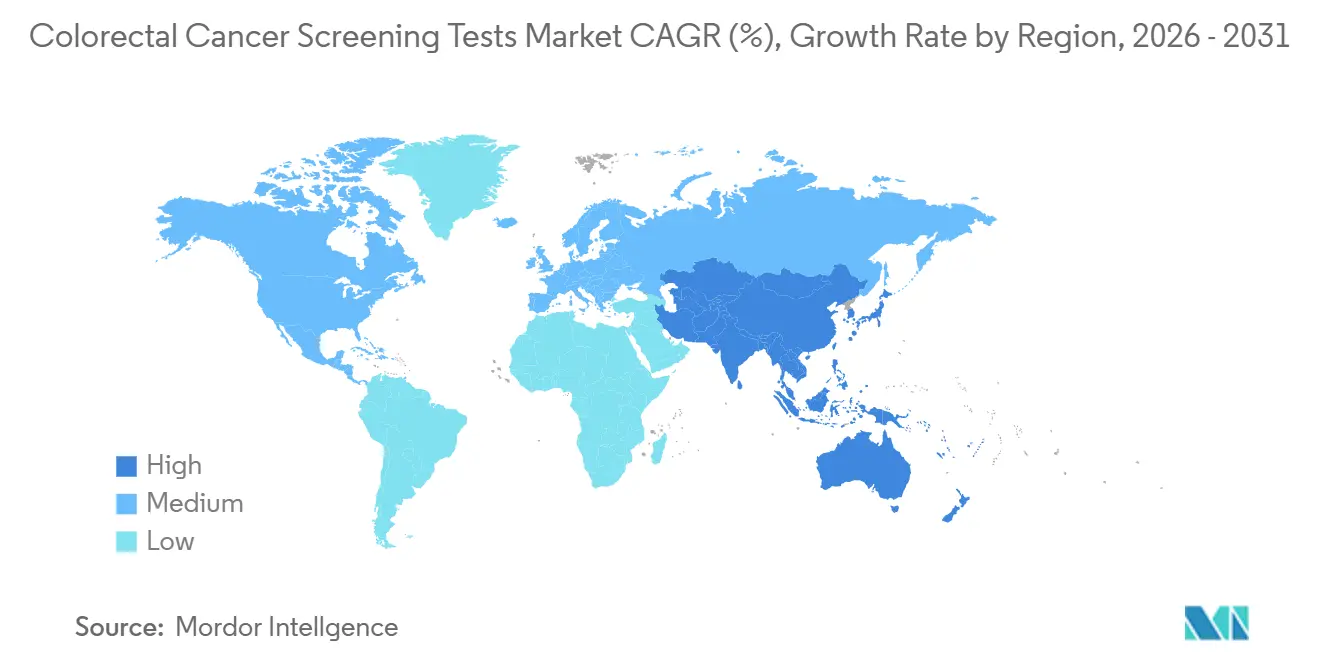

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colorectal Cancer Screening Tests Market Analysis by Mordor Intelligence

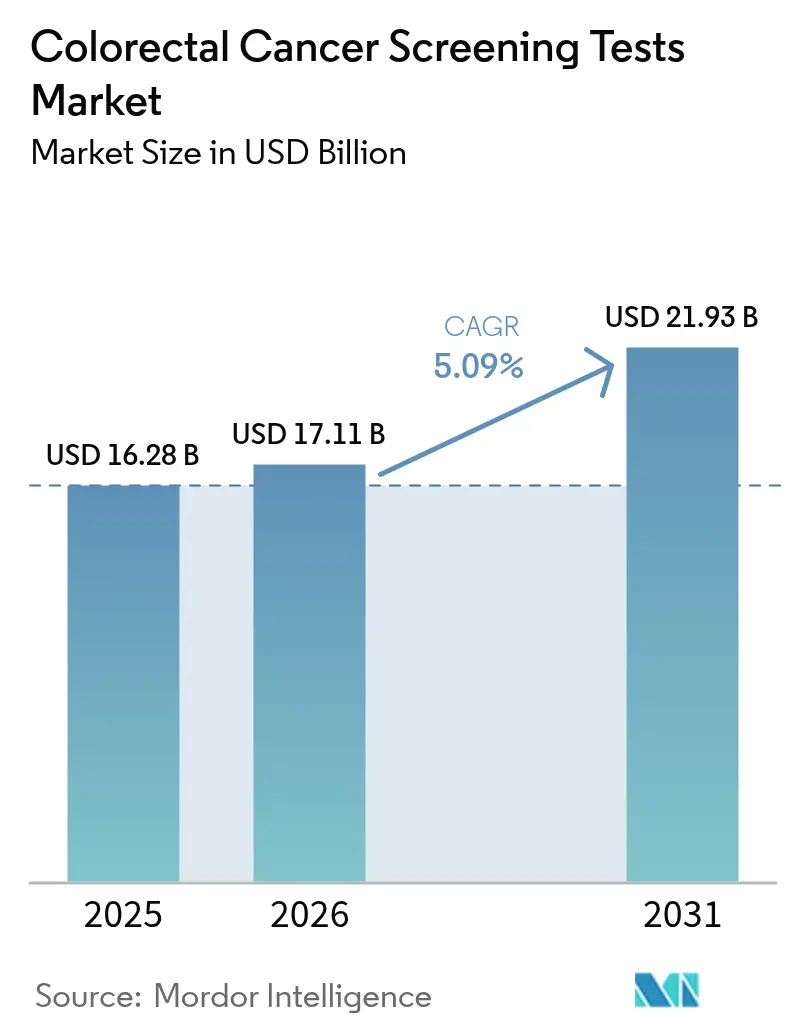

The colorectal cancer screening tests market size is expected to grow from USD 16.28 billion in 2025 to USD 17.11 billion in 2026 and is forecast to reach USD 21.93 billion by 2031 at 5.09% CAGR over 2026-2031. Uptake accelerates as clinical guidelines now recommend starting routine tests at age 45, enlarging the eligible cohort by 19 million people in the United States alone. Adoption of less-invasive modalities, especially stool DNA and blood-based assays, is rising as these options lower procedural anxiety and require no facility visits. Artificial-intelligence (AI) add-ons that raise adenoma detection rates are reshaping competitive positioning, while value-based reimbursement frameworks push payers to reward preventive care that reduces downstream treatment spending. Vendors that bundle digital navigation, at-home sample collection, and AI-augmented analytics are capturing early mover advantage across the colorectal cancer screening tests market.

Key Report Takeaways

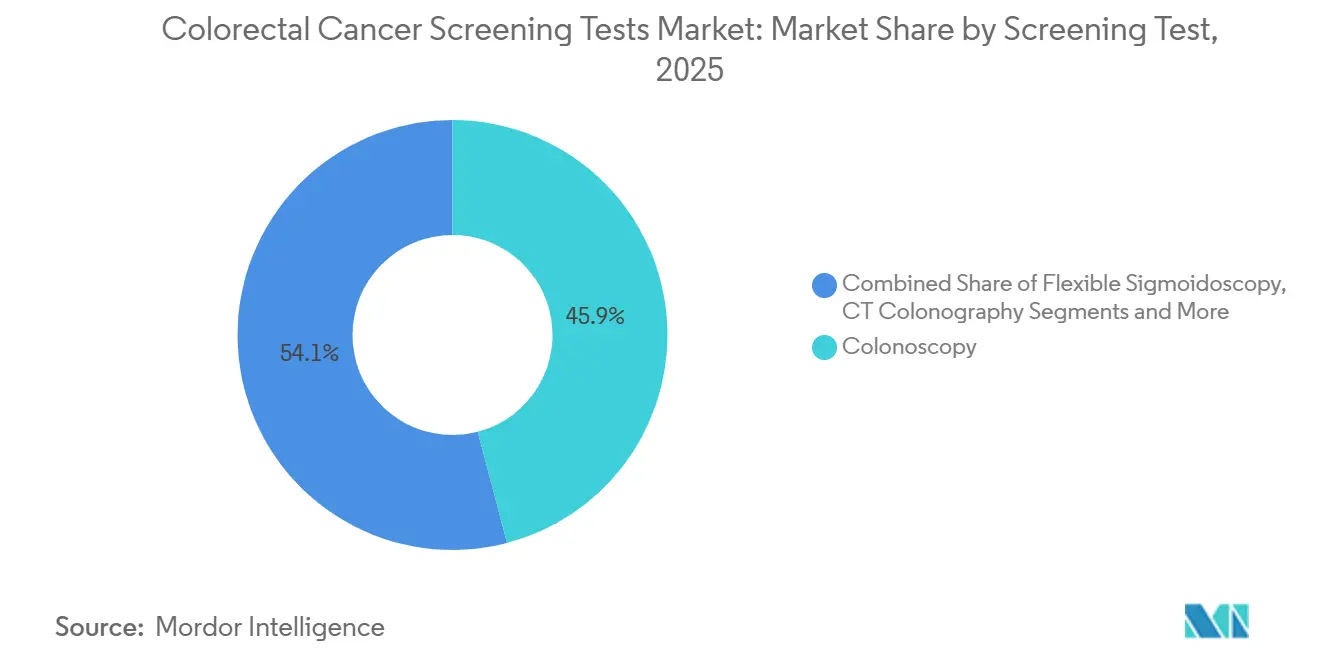

- By screening test, colonoscopy retained 45.95% of the colorectal cancer screening tests market share in 2025, whereas stool DNA assays are set to expand at an 11.05% CAGR through 2031.

- By product type, test kits and reagents commanded 52.85% share of the colorectal cancer screening tests market size in 2025; software-driven AI algorithms show the highest projected growth at 12.55% CAGR to 2031.

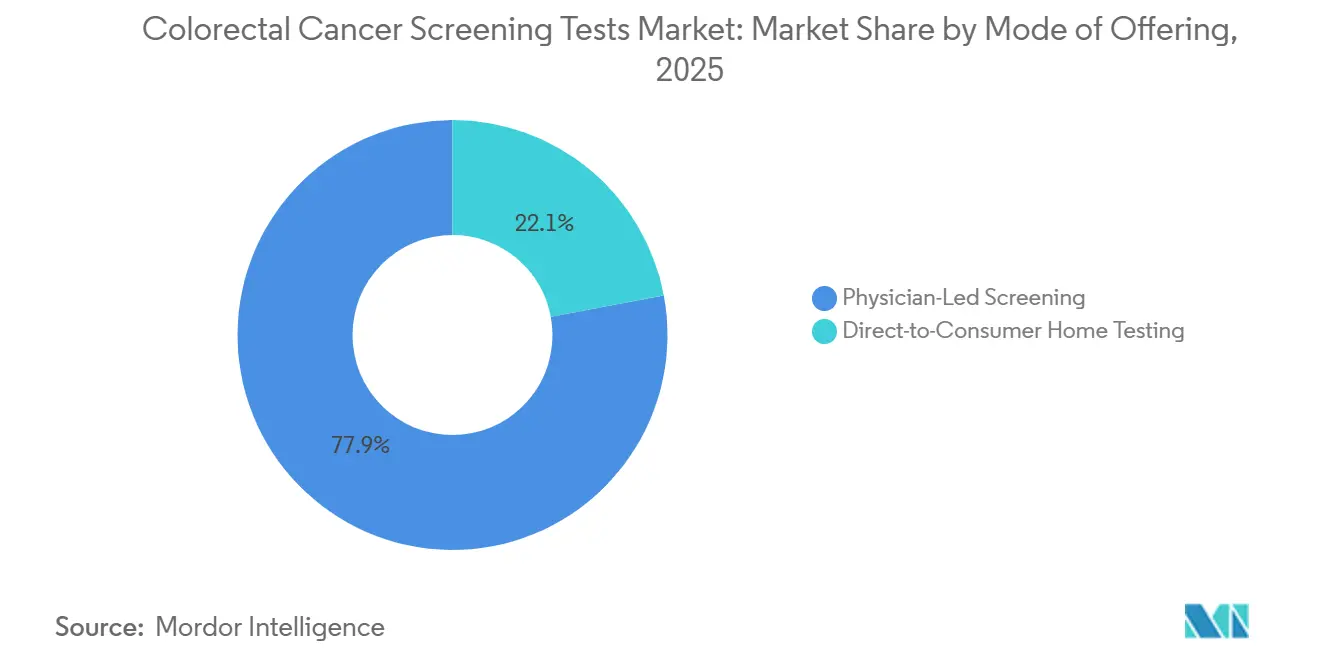

- By mode of offering, physician-led programs held 77.95% revenue share in 2025, while direct-to-consumer home testing is projected to grow 14.09% annually between 2026-2031.

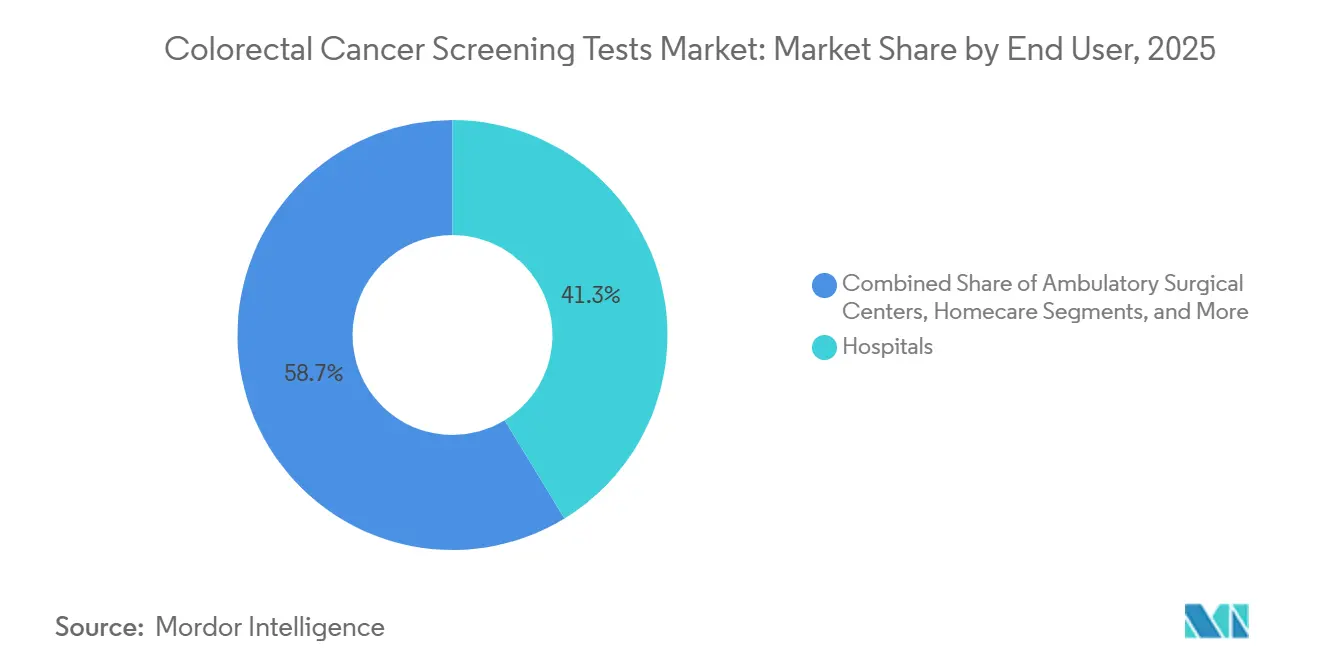

- By end user, hospitals captured 41.25% of the colorectal cancer screening tests market size in 2025; home-care settings are projected to progress at a 10.43% CAGR through 2031.

- By geography, North America dominated with 38.15% market share in 2025, while Asia Pacific is the fastest-growing region, tracking an 8.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Colorectal Cancer Screening Tests Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global incidence and earlier age-of-onset | +0.9% | Global, with high intensity in China and southern United States | Medium term (3-4 yrs) |

| Government-mandated lowering of screening age | +1.0% | North America & EU | Short term (≤ 2 yrs) |

| Rapid technology convergence toward minimally invasive biomarker platforms | +1.2% | Global | Long term (≥ 5 yrs) |

| Payer shift to value-based care models | +0.6% | North America, Western Europe | Medium term (3-4 yrs) |

| Rapid uptake of direct-to-consumer home collection kits | +0.8% | United States, Canada, Australia | Short term (≤ 2 yrs) |

| National adoption of FIT-based population screening and expanded reimbursement | +0.7% | EU core, APAC spill-over to MEA | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Escalating Global Incidence and Earlier Age-of-Onset of Colorectal Cancer

The demographic composition of colorectal cancer (CRC) is tilting toward younger age brackets, and that shift is quietly rewriting the market’s total addressable population. With clinical evidence confirming that early-onset tumors often display accelerated progression, health-system executives increasingly frame screening as a lifetime customer-relationship program rather than a late-career intervention. The implication for manufacturers is a longer monetization runway per individual, provided that product portfolios integrate digital engagement features familiar to working-age consumers. In parallel, payers are recalculating actuarial assumptions because a younger entrant pool extends the period over which preventive savings accrue; this is driving reimbursement models that reward longitudinal adherence rather than one-off test completion.

China’s sizable burden of new CRC cases underscores how incidence is decoupling from historical age curves, and regional oncology societies now caution that traditional screening start ages risk missing a clinically meaningful subset of patients. A corollary insight for hospital administrators is that existing endoscopy capacity, once tuned to Medicare-age demand, must be reallocated across a wider spectrum of risk profiles. Consequently, several integrated delivery networks are negotiating wholesale purchases of at-home kits to funnel low-risk cohorts into non-invasive pathways, preserving colonoscopy slots for advanced or symptomatic cases. The downstream effect is a subtle shift in revenue mix: margins once tied predominately to procedural throughput are migrating toward hybrid packages that bundle remote sample collection, algorithmic triage, and rapid escalation for positive results.

Government-Mandated Lowering of Screening Start Age Across Major Economies

Mandatory guideline changes have become the most powerful catalyst for volume growth. When the Centers for Medicare & Medicaid Services (CMS) began reimbursing average-risk beneficiaries at age forty-five in January 2023, private insurers moved quickly to align benefits, ensuring network adequacy in employer segments that demand parity.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2023 Physician Fee Schedule Final Rule,” cms.gov Vendors accustomed to targeting retirees must now craft messaging for human-resources managers and younger policyholders who weigh discretionary health purchases against out-of-pocket costs.

Modeling commissioned by CMS demonstrated that earlier detection curtails future chemotherapy and hospitalization outlays, allowing payers to justify expanded front-end spending. Commercial carriers are importing the same logic into shared-savings agreements with provider groups, stipulating that any technology selected must produce verifiable adherence data. This validation requirement elevates the strategic value of longitudinal evidence reservoirs; companies that can mine millions of historical test records to display five-year avoided-treatment curves negotiate preferred status on payer formularies. For investors, the lesson is clear: clinical sensitivity remains essential, yet the durability of market share increasingly depends on proprietary outcomes analytics that simplify budget-impact forecasting for actuaries.

Rapid Technology Convergence Toward Minimally-Invasive Biomarker Platforms

The US Food and Drug Administration (FDA) established a new competitive baseline in July 2024 by approving Guardant Health’s Shield blood assay for primary screening of average-risk adults.[2]Guardant Health, “FDA Approves Shield Blood Test for Colorectal Cancer Screening,” guardanthealth.comThat decision instantly reframed stakeholder expectations because it demonstrated that centralized laboratories could attain accuracy levels once attributed almost exclusively to optical procedures. Laboratories have seized the moment by bundling analytic services with patient-navigation hotlines that schedule confirmatory colonoscopies, giving them growing influence over downstream referral flows.

Stool DNA products, notably Exact Sciences’ Cologuard, have already proven that consumer-direct logistics and high-volume manufacturing can coexist profitably; the firm’s public disclosures report more than sixteen million completed tests since launch, reinforcing the scalability of home-collection economics. Blood-based assays now seek to replicate that momentum while sidestepping the perceived inconvenience associated with stool handling, offering venous draws that integrate smoothly into routine primary-care visits or employer wellness drives. The result is an ecosystem where multimodality pathways—blood, stool, and optical visualization—interlock to address varied patient preferences, each becoming an upstream lead generator for the others.

A second-order insight for device manufacturers is that biomarker proliferation changes capital-equipment depreciation curves. If a higher share of average-risk patients enters the system through laboratory tests, hospitals may prioritize scopes designed for therapeutic interventions over those optimized purely for screening. Commercial teams selling colonoscopy towers therefore emphasize advanced electrosurgical features and AI-enabled detection to validate the capital expense against a smaller, but higher clinical-acuity, procedure volume.

Payer Shift to Value-Based Care Models Increasing Reimbursement for Preventive Screening

Value-based reimbursement is redrawing incentive structures across the supply chain. Under shared-savings contracts, failure to meet guideline adherence targets generates financial penalties for provider groups, so C-suite discussions increasingly revolve around technologies that combine acceptable specificity with behavioral nudging. Exact Sciences capitalized on this shift by embedding multilingual reminders, return-status dashboards, and auto-escalation protocols into its service bundle, positioning those workflow tools as integral to the product rather than auxiliary features.

Payers, for their part, link bonus payments to documented improvements in population screening rates. The operational reality is that a technology’s test-sensitivity figures matter less if kit-return compliance falters; consequently, payer contract language frequently stipulates that vendors must deliver real-time adherence analytics. This requirement has steered venture funding toward start-ups specializing in digital coaching layers, with investment theses predicated on the notion that insurers will reward even modest percentage-point gains in compliance given their outsized impact on long-run oncology costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent cost and reimbursement gaps in LMICs | -0.7% | APAC core, spill-over to MEA | Long term (≥ 5 yrs) |

| Patient non-compliance due to cultural stigma and procedure anxiety | -0.5% | Saudi Arabia, United States, Japan | Short term (≤ 2 yrs) |

| Limited access to CT colonography infrastructure in emerging economies | -0.4% | National, with early gaps in Jakarta, Manila, Lagos | Medium term (3-4 yrs) |

| FIT reagent supply-chain bottlenecks post-COVID | -0.3% | Global, acute in Latin America | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Persistent Cost and Reimbursement Gaps in Low- and Middle-Income Countries

Resource-constrained markets present a markedly different commercial calculus. Ministries of health often juggle infectious-disease priorities alongside non-communicable burdens, delaying broad CRC program deployment. The resulting two-tier landscape forces suppliers to engineer price-study variants, typically by reducing reagent volumes per kit and localizing assembly to sidestep import tariffs. While such adaptations protect gross margin, they also necessitate rigorous supply-chain audits to retain regulatory approvals across multiple jurisdictions.

An increasingly relevant access channel in Asia and the Middle East is the employer-sponsored voucher. Multinational corporations fund screening for their urban workforce to curb absenteeism linked to late-stage diagnoses. Manufacturers that supply this niche build brand familiarity among insured employees, who subsequently act as informal ambassadors when national reimbursement eventually materializes. A related insight for strategic planners is that corporate programs generate early epidemiological datasets—often the first of their kind in those countries—which can later underpin dossier submissions to health-technology assessment bodies.

Patient Non-Compliance Due to Cultural Stigma and Procedure-Related Anxiety

Consumer psychology remains a stubborn bottleneck, even when economic obstacles recede. Surveys in high-income and emerging markets alike cite embarrassment, fear of sedation, and misconceptions about pain as leading refusal drivers. Product teams have responded by redesigning packaging for discretion and simplifying collection protocols to under ten minutes, thereby lowering the emotional activation energy required for first-time users.

The design enhancements yield more than cosmetic benefits; payer data indicate that each percentage point rise in completed tests per mailing translates into meaningful reductions in late-stage treatment claims three to four years out. Savvy suppliers now integrate those statistics into procurement decks, demonstrating to employer groups that investments in user-experience refinement possess tangible ROI. Concurrently, providers who once viewed at-home kits as competitive threats now incorporate them into omnichannel engagement strategies, because positive user experiences feed a virtuous loop of family referrals that ultimately lift procedure volume when confirmatory colonoscopies are necessary.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screening Test: Expanding Preference for Stool DNA Platforms

In 2025, colonoscopy generated the most significant proportion of test revenues, retaining 45.95% of colorectal cancer screening tests market share. Yet stool DNA assays posted the quickest revenue rise and are predicted to grow 11.05% annually through 2031. At-home kits resonate with busy younger adults who value convenience and privacy. The colorectal cancer screening tests market size attributed to stool DNA platforms stood at USD 3.54 billion in 2025 and is projected to double by 2031 alongside guideline-driven uptake. Rising accuracy, evidenced by analytical sensitivity above 90% for advanced lesions, keeps clinicians confident in recommending follow-up colonoscopy only when warranted.

Capital deployment pivots toward scalable laboratory infrastructure that accelerates turnaround time for millions of mailed-in samples. Public-private partnerships are emerging to co-finance regional processing hubs, adding redundancy and trimming logistics expenses. Marketing campaigns target primary-care networks that previously defaulted to colonoscopy referrals, stressing equal effectiveness for average-risk adults. Overall, competitive differentiation within this segment now hinges on kit price, logistics efficiency, and digital result delivery—factors that collectively expand coverage in the colorectal cancer screening tests market.

By Product Type: AI Software Accelerates Accuracy Gains

Diagnostic hardware, reagents, and kits accounted for 52.85% of market share in 2025, whereas AI-driven software modules are projected to post a 12.55% CAGR through 2031 as clinical evidence mounts. Systems that flag subtle polyps in real time or classify histology on-screen reduce miss rates and downstream pathology costs. The colorectal cancer screening tests market size attached to software modules is expected to surpass USD 2.18 billion by 2031, reflecting hospital procurement of AI licences embedded in endoscopy towers.

Software developers bundle cloud analytics and remote quality dashboards, enabling health-system leaders to benchmark adenoma detection across sites. This data transparency fuels pay-for-performance contracts under value-based care, reinforcing enterprise shifts toward software-centric solutions. Partnerships between endoscope makers and algorithm startups shorten integration timelines, making AI-enhanced workflows an expectation rather than a premium feature in the colorectal cancer screening tests market.

By Mode of Offering: Direct-to-Consumer Home Testing Gains Traction

Physician-ordered tests still dominate with 77.95% market share in 2025, but home kits delivered through online channels and pharmacy chains are scaling swiftly. Demand for self-collection supports a robust 14.09% CAGR outlook. Marketing emphasizes ease, no bowel prep, no dietary restrictions, no time off work, appealing to the 45–64 demographic, and newly covered for screening.

Innovators differentiate by bundling mobile reminders, teleconsultations, and prepaid logistics, simplifying the end-to-end path from kit order to result counseling. Retail pharmacies leverage loyalty programs to nudge repeat testing, while employers integrate kits into wellness benefits to curb absenteeism. This omni-channel expansion closes gaps for populations with limited access to gastroenterology services, bolstering overall growth in the colorectal cancer screening tests market.

By End User: Home-Care Settings Emerge as the Growth Frontier

Hospitals accounted for 41.25% of test volumes in 2025; however, home-care environments are posting a projected 10.43% CAGR through 2031. Pandemic-era capacity constraints coupled with consumer convenience have accelerated off-site sampling. The colorectal cancer screening tests market share for home-care solutions is forecast to reach 24.85% by 2031 as digital triage and courier logistics mature. Public health initiatives now dispatch FIT or DNA kits directly to households, allowing national programs to keep participation on target despite clinical workforce shortages.

For providers, home-based sampling unlocks scheduling flexibility and reallocates colonoscopy suites to therapeutic procedures. Health insurers bundle patient navigation services that secure follow-up colonoscopies after positive home tests, ensuring clinical completeness. As remote monitoring tools integrate symptom checkers and risk assessments, a broader continuum of care emerges, reinforcing the strategic weight of home settings within the colorectal cancer screening tests market.

Geography Analysis

North America holds a 38.15% market share in the market in 2025 due to expanded Medicare eligibility at age 45 and proactive outreach programs lifted national adherence rates, yet 30.3% of adults still miss recommended testing. That shortfall directs innovation toward digital reminders, community health partnerships, and culturally tailored messaging, all intended to convert non-compliant groups. Canada mirrors US trends, with provincial payers now funding stool DNA as a population-level option to expand coverage across rural territories. The scale of North American reimbursement propels supplier investment in AI-enabled colonoscopy towers and high-throughput laboratory automation for the colorectal cancer screening tests market.

Europe presents a patchwork landscape. Countries such as the Netherlands and the UK operate mature national programs, achieving 70-75% participation, whereas parts of Eastern Europe remain below 10% due to fiscal limitations. The European Society of Gastrointestinal Endoscopy’s endorsement of optical diagnosis accelerates the adoption of Narrow Band Imaging systems that can decrease polyp miss rates by 29%. Economic austerity in several member states directs procurement toward cost-effective FIT and DNA kits with minimal capital outlay. Vendors demonstrating comparative cost-utility in multicountry trials gain formulary precedence, reinforcing gradual convergence on AI-supported, quality-monitored solutions across the colorectal cancer screening market.

Asia-Pacific is the fastest-expanding region by patient volume. China’s 517,100 incident cases in 2024 spotlight both need and opportunity, although absence of a national screening program restrains uptake. Regional pilots in Shanghai and Shenzhen that subsidize stool-based tests are showing double-digit participation gains, prompting policy debate on broader rollout. Elsewhere, Japan’s aging population and high gastric screening penetration provide a template for integrating colorectal kits into existing check-up pathways. In the Middle East, Saudi Arabia’s 62% non-screened population underscores cultural and logistical hurdles; emerging home-based tests combined with teleconsultations in Arabic aim to bridge the gap. These developments reinforce Asia-Pacific’s pivotal role in shaping long-term expansion of the colorectal cancer screening market.

Competitive Landscape

The colorectal cancer screening tests market exhibits moderate concentration as incumbent diagnostics firms confront rapid entry by biotechnology and digital-health players. Exact Sciences leads the stool DNA niche; 16 million completed Cologuard tests underscore brand strength even as the firm recorded a Q3 2024 EPS loss of USD 0.21 on softer margins. Guardant Health reshaped the battlefield when its Shield blood assay won FDA clearance in July 2024 and secured Medicare reimbursement within weeks, effectively granting it first-mover leverage in the blood-based segment.

Endoscopy hardware vendors defend share through AI partnerships: Olympus integrates real-time image analytics into its Narrow Band Imaging platform, boosting adenoma detection by up to 48.3%. Medtronic’s GI Genius module offers vendor-neutral integration, giving smaller hospitals AI capabilities without wholesale tower upgrades. Cloud-based performance dashboards now accompany many algorithm packages, allowing providers to track quality metrics critical under value-based contracts in the colorectal cancer screening tests market.

Strategic collaboration is intensifying. Laboratory networks partner with pharmacy chains to shorten logistics cycles for mail-in kits, while payers pilot bulk-purchase agreements linking reimbursement to participation thresholds. Venture capital continues to fund multi-omics startups exploring breath and urine biomarkers that could bypass stool or blood entirely, hinting at future disruptive entrants. As the competitive field widens, pricing pressure escalates, making scalability and health-economic validation decisive success factors across the colorectal cancer screening industry.

Colorectal Cancer Screening Tests Industry Leaders

Exact Sciences Corporation

F. Hoffmann-La Roche AG

Siemens Healthineers AG

Olympus Corporation

Sysmex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Guardant Health, Inc. made its Shield Guardant blood-based screening test readily available to physicians nationwide through a partnership with Quest Diagnostics. This collaboration empowers clinicians across the U.S. to utilize this innovative blood-based screening for colorectal cancer (CRC), tapping into one of the country's largest diagnostic networks.

- August 2024: A study published in MedRxiv reported that mt-sDNA screening detected approximately 98,000 CRC cases and identified 525,000 individuals with advanced precancerous lesions over a 10-year period.

- July 2024: The FDA approved Guardant Health's Shield blood test for primary colorectal cancer screening. The test achieves an 83% sensitivity for detecting colorectal cancer in adults aged 45 and older with average risk.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global colorectal cancer screening tests market as the value generated by stool-based assays (FIT, gFOBT, multi-target stool DNA), visual tests (colonoscopy, CT colonography, flexible sigmoidoscopy), emerging blood or other biomarker assays, and supportive software or service fees charged at the point of screening. Geographies span North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa, with values converted to constant 2024 USD.

Scope exclusion: therapeutic drugs, surgical interventions, and post-diagnosis imaging are not counted.

Segmentation Overview

- By Screening Test

- Stool-Based Tests

- Fecal Immunochemical Test (FIT)

- Guaiac-based Fecal Occult Blood Test (gFOBT)

- Stool DNA Test (sDNA)

- Visual Tests

- Colonoscopy

- CT Colonography (Virtual Colonoscopy)

- Flexible Sigmoidoscopy

- Serology & Liquid Biopsy Tests

- Septin9 Blood Test

- microRNA Panels

- Other Screening Tests (Capsule Endoscopy, etc.)

- Stool-Based Tests

- By Product Type

- Test Kits & Reagents

- Analyzers & Imaging Systems

- Software & AI Algorithms

- Services

- By Mode of Offering

- Physician-Led Screening

- Direct-to-Consumer Home Testing

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Independent Diagnostic Laboratories

- Home Care Settings

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured calls with gastroenterologists, hospital lab managers, kit manufacturers, and reimbursement consultants across the United States, Germany, Japan, Brazil, and the GCC. These conversations clarify guideline adherence rates, kit pricing corridors, and future product mix shifts, anchoring assumptions flagged during desk work.

Desk Research

We begin by mapping publicly available sources such as WHO cancer incidence registries, OECD and CDC screening uptake dashboards, trade association briefs (e.g., World Endoscopy Organization), and customs/commerce portals listing annual imports of test kits. Company 10-Ks, Medicare payment files, and peer-reviewed journals on test sensitivity trends supply cost and utilization clues. Select paid databases, including D&B Hoovers for supplier revenue splits and Questel for patent velocity, give further context. This list is illustrative only; many additional repositories underpin our evidence stack.

Market-Sizing and Forecasting

A top-down model reconstructs the demand pool from age-eligible population, colorectal cancer incidence, and national screening coverage, which are then multiplied by weighted test modality shares and verified average selling prices. Select bottom-up checkpoints, such as annual colonoscope shipments and sampled FIT kit volumes, validate totals and reveal leakages. Key variables tracked include: 1) population aged 45-74, 2) guideline-mandated screening frequency, 3) hospital colonoscopy capacity utilization, 4) average FIT kit price, and 5) reimbursement policy changes. A multivariate regression with ARIMA overlay projects each driver five years out; scenario buffers adjust for sudden guideline shifts or disruptive blood tests. Data gaps in low-income regions are bridged using regional incidence-to-uptake proxies vetted with physicians.

Data Validation and Update Cycle

Output undergoes variance checks against independent incidence curves and insurance claim tallies. Senior analysts review anomalies before sign-off. The model refreshes annually, and ad-hoc updates trigger after major regulatory or product events, ensuring clients always access the current view.

Why Mordor's Colorectal Cancer Screening Baseline Earns Decision-Makers' Trust

Published estimates often diverge because firms frame the market differently and refresh at varied speeds.

Key gap drivers include differing inclusion of diagnostic follow-ups, mixing service revenue with kit sales, and one-off currency conversions. Mordor's disciplined boundary around screening-only revenue, annual refresh cadence, and dual-track validation keep our figure balanced and repeatable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.28 Bn (2025) | Mordor Intelligence | - |

| USD 17.83 Bn (2024) | Global Consultancy A | Combines select diagnostic imaging revenues and uses static ASPs |

| USD 40.00 Bn (2024) | Trade Journal B | Bundles screening with diagnostic services and therapeutic follow-ups |

| USD 17.21 Bn (2024) | Market Publisher C | Relies on kit shipment reports without adjusting for multi-year stockpiling |

Taken together, the comparison shows how narrower or broader scopes and unvalidated price multipliers inflate or depress market totals. Our approach, rooted in transparent variables and regular expert cross-checks, delivers a dependable baseline that planners can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the colorectal cancer screening tests market?

The colorectal cancer screening tests market size stands at USD 17.11 billion in 2026 and is forecast to grow at a 5.09% CAGR through 2031.

Why was the recommended screening age lowered to 45?

Rising early-onset incidence and modeling that shows long-term cost savings led US and other health authorities to shift eligibility to age 45, adding about 19 million potential participants in the United States.

How accurate are blood-based tests compared with colonoscopy?

Guardant Health’s Shield blood assay achieved 83% sensitivity for detecting colorectal cancer, while colonoscopy remains the gold standard with higher overall sensitivity but lower patient adherence.

Which segment is growing fastest in colorectal cancer screening?

Direct-to-consumer home testing—particularly stool DNA kits—is projected to post a 14.09% CAGR between 2026-2031 as consumers favor convenience and privacy.

What role does AI play in colonoscopy today?

AI modules integrated into endoscopy systems now provide up to 96% real-time polyp detection accuracy, boosting adenoma detection rates and supporting value-based care objectives.

How are payers incentivizing preventive screening?

Value-based reimbursement models reward health systems for long-term cost avoidance, leading insurers to cover at-home kits and proactive outreach programs that raise screening adherence.

Page last updated on: