Prostate Cancer Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.42 Billion |

| Market Size (2031) | USD 13.86 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

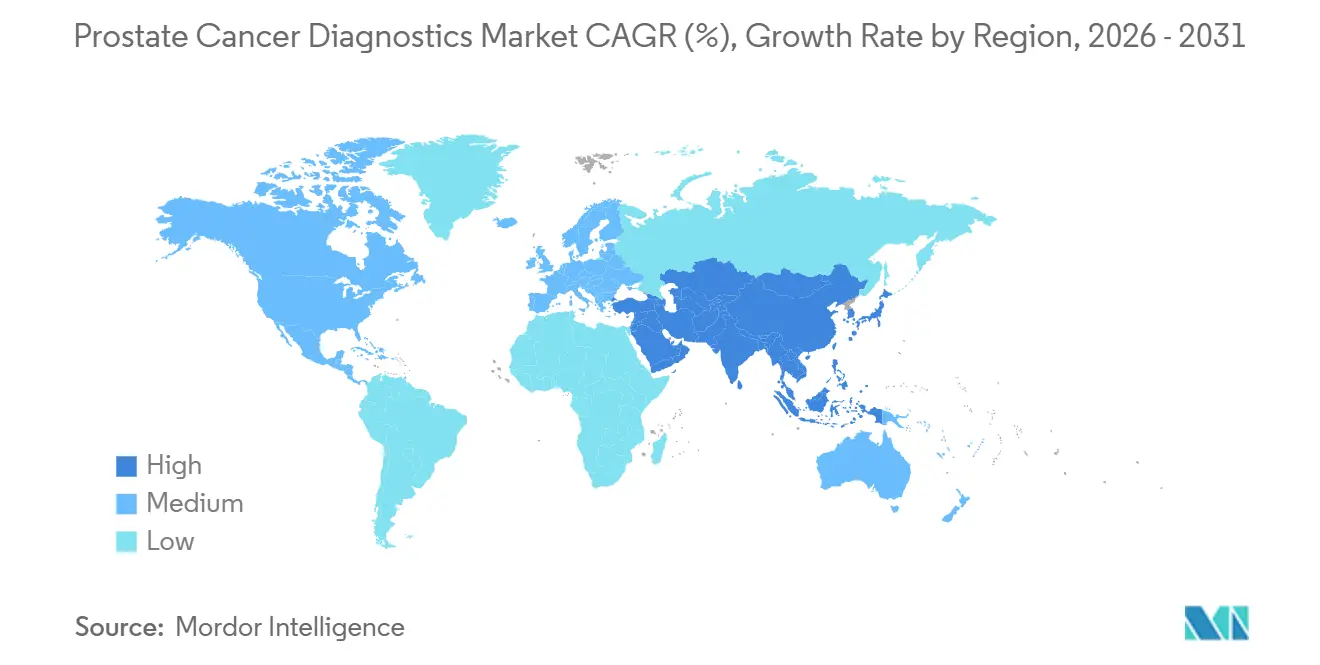

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

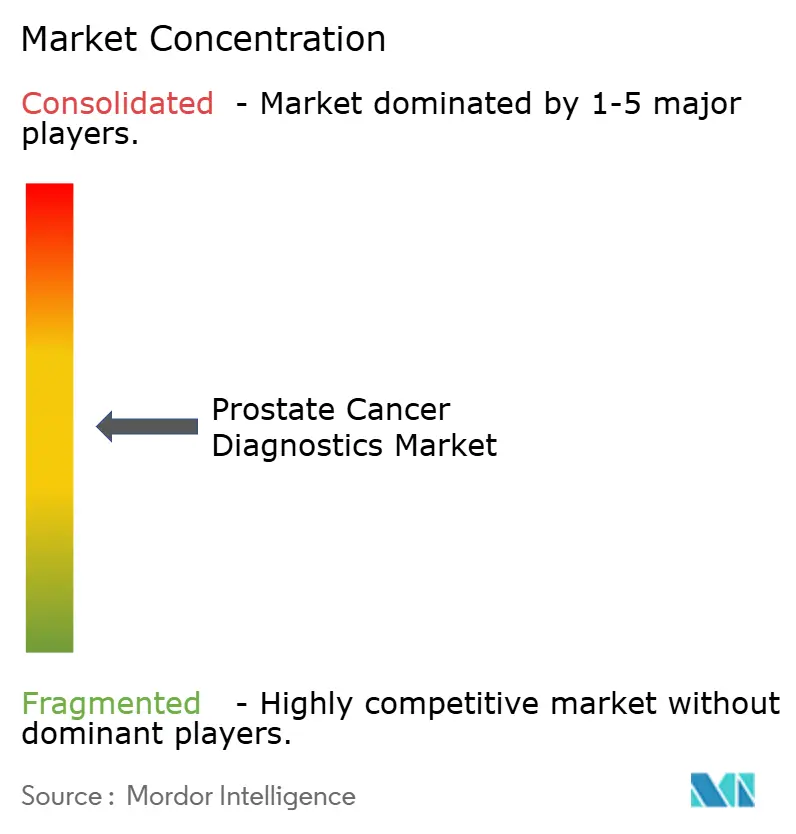

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prostate Cancer Diagnostics Market Analysis by Mordor Intelligence

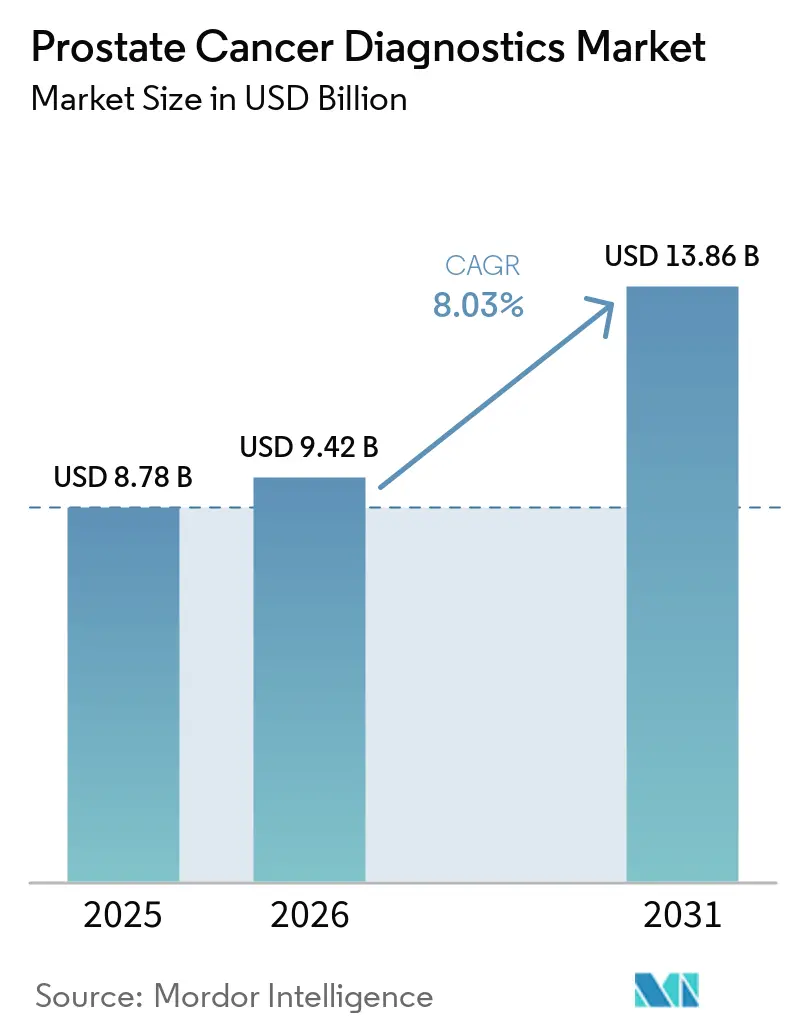

The Prostate Cancer Diagnostics Market size was valued at USD 8.78 billion in 2025 and is estimated to grow from USD 9.42 billion in 2026 to reach USD 13.86 billion by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

The prostate cancer diagnostics market is supported by a disease burden that continues to rise, with the American Cancer Society projecting 333,830 new prostate cancer cases in the United States in 2026 and a global study projecting 2.41 million cases by 2040 from 1.5 million at present. The prostate cancer diagnostics market also benefits from a 3% annual increase in U.S. incidence between 2014 and 2022, which shows that testing demand is being sustained by epidemiology as well as by practice changes. Screening policy shifts, broader reimbursement for selected genomic tools, and stronger use of multimodal workflows are improving the clinical position of the prostate cancer diagnostics market in several developed healthcare systems. The prostate cancer diagnostics market is also being reshaped by AI-supported imaging, ctDNA monitoring, and other tools that give clinicians more selective and longitudinal decision support across the care pathway. Cost barriers and uneven access to advanced imaging and molecular testing still limit the full commercial reach of the prostate cancer diagnostics market, while large diagnostic companies continue to use acquisitions and partnerships to strengthen coverage, distribution, and platform breadth.

Key Report Takeaways

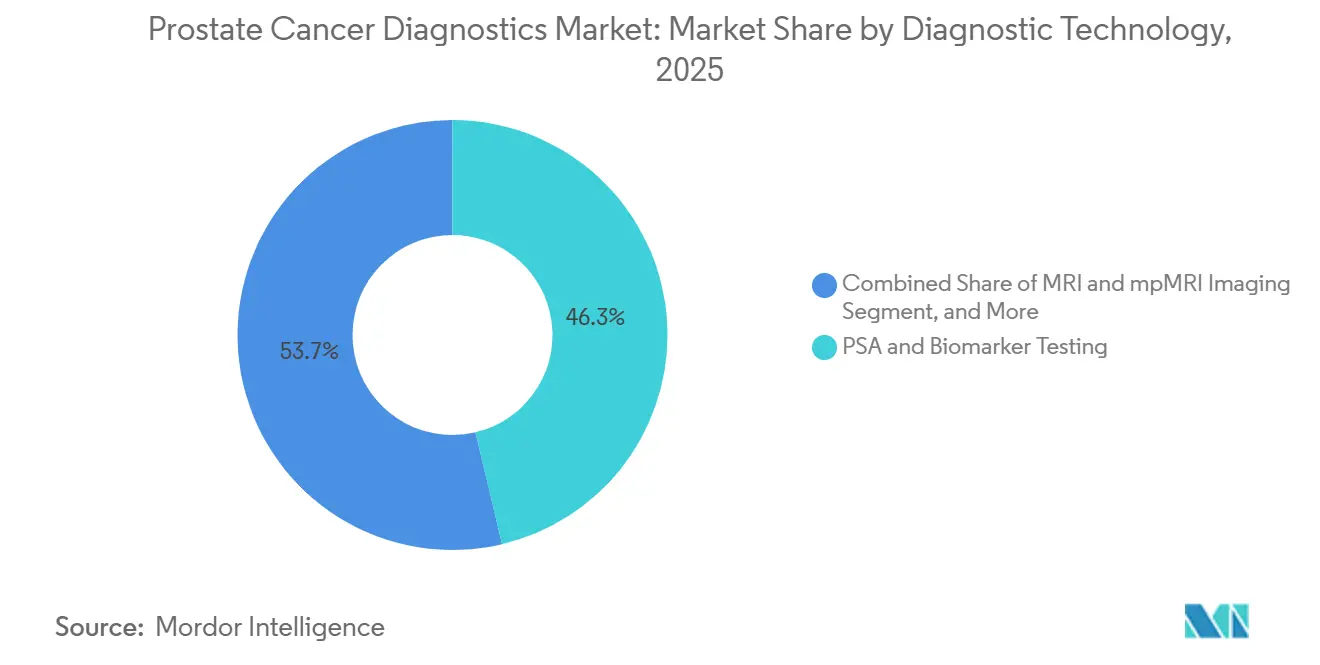

- By diagnostic technology, PSA and biomarker testing led with 46.31% of the prostate cancer diagnostics market share in 2025, while PSMA PET and CT imaging recorded the highest projected CAGR at 8.68% through 2031.

- By sample type, blood-based testing accounted for 46.68% of the prostate cancer diagnostics market size in 2025, while tissue-based testing is forecast to expand at a 10.12% CAGR through 2031.

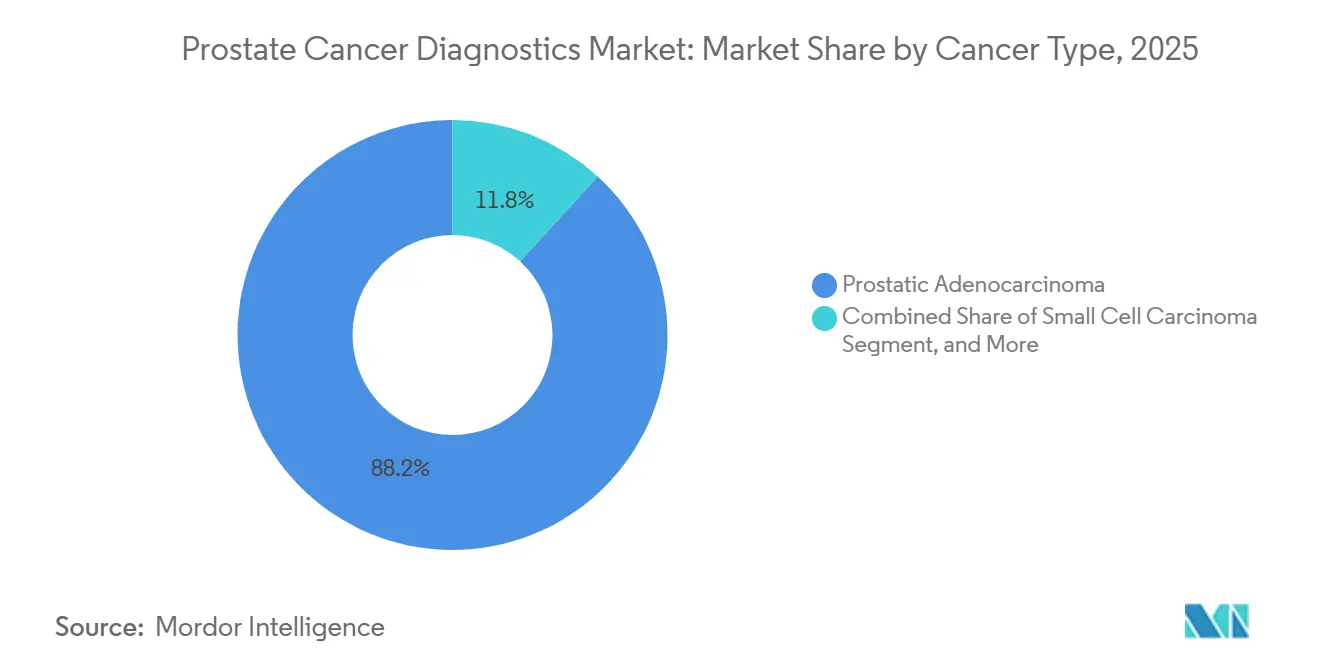

- By cancer type, prostatic adenocarcinoma held 88.16% share in 2025, while small cell carcinoma of the prostate is projected to grow at a 9.34% CAGR through 2031.

- By stage, localized prostate cancer represented 53.62% share in 2025, while castration-resistant prostate cancer is expected to advance at a 10.98% CAGR through 2031.

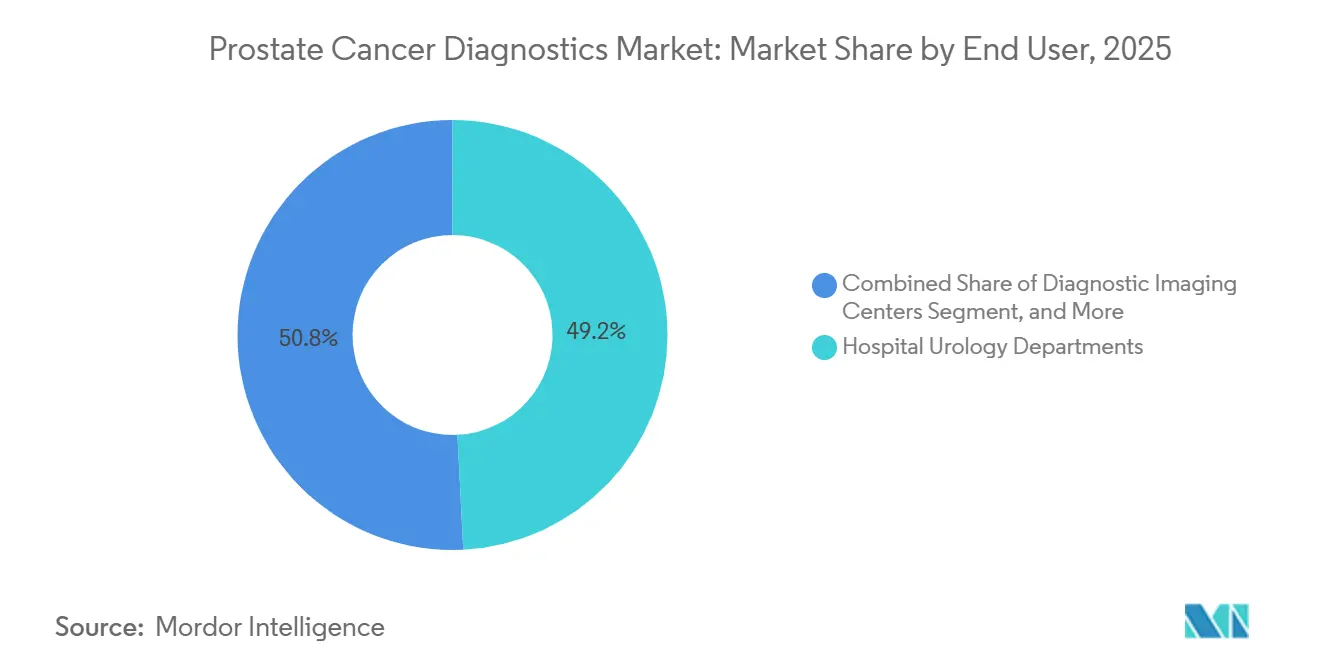

- By end user, hospital urology departments held 49.19% share in 2025, while oncology reference laboratories posted the fastest projected CAGR at 8.57% through 2031.

- By geography, North America held 43.64% share in 2025, while Asia-Pacific is projected to expand at a 9.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Prostate Cancer Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prostate Cancer Screening Volume | +1.8% | Global, concentrated in North America, Europe, Japan | Short term (≤ 2 years) |

| Shift Toward Multimodal Diagnostic Pathways | +1.2% | North America, Western Europe | Medium term (2-4 years) |

| Expanding Reimbursement for Advanced Biomarker and Imaging Tests | +1.5% | North America, Germany, UK, Japan | Short term (≤ 2 years) |

| Decentralization of Testing to Outpatient and Ambulatory Settings | +0.9% | North America, Western Europe, Australia | Medium term (2-4 years) |

| AI-Enabled Imaging and Risk Stratification Adoption | +1.1% | Global, early gains in North America, UK, Asia-Pacific | Medium term (2-4 years) |

| Liquid Biopsy and Genomic Testing Uptake | +1.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prostate Cancer Screening Volume

The prostate cancer diagnostics market is gaining from a broader rise in organized and semi-organized screening activity across several countries. Prostate cancer is now the most commonly diagnosed cancer in men in 118 of 185 countries, which supports the need for more routine testing pathways in both mature and under-screened health systems. Japan’s 2025 clinical practice guidelines introduced the first weak recommendation in favor of PSA screening for middle-aged men, which marked a clear shift from the long period of uncertain official guidance.[1]Japanese Urological Association, “Prostate Cancer Clinical Practice Guidelines 2025 Edition,” Minds Clinical Practice Guideline, minds.jcqhc.or.jp In the United States, the prostate cancer death rate fell by 50% between 1993 and 2022, which keeps the case for earlier detection central to screening decisions. Lombardy’s multilevel screening pilot enrolled 8,558 men by June 2025 and recorded a 15.9% referral rate without evidence of overdiagnosis, which gives the prostate cancer diagnostics market a practical model for urban screening scale-up. Higher screening volume supports repeat demand for PSA reagents, follow-on biomarker work, imaging, and biopsy across the wider prostate cancer diagnostics market.

Expanding Reimbursement for Advanced Biomarker and Imaging Tests

The prostate cancer diagnostics market is also being lifted by coverage decisions that reduce ordering uncertainty for clinicians and laboratories. CMS updated its Local Coverage Determination for the Decipher Prostate Cancer Classifier Assay, effective July 3, 2025, and that decision covered use in localized prostate cancer patients with at least 10 years of life expectancy under NCCN-aligned criteria.[2]Centers for Medicare & Medicaid Services, “MolDX, Prostate Cancer Genomic Classifier Assay for Men with Localized Disease (L38341),” CMS, cms.gov Once a molecular test gains reimbursement, it becomes easier for similar tools to frame their own value in terms that payers already recognize. The same pattern matters for advanced imaging, because reimbursement changes shape referral behavior, budget planning, and vendor investment decisions across the prostate cancer diagnostics market. The direct effect is stronger in systems where coverage policy quickly translates into everyday clinical pathways, especially in the United States and other reimbursement-led markets. Over time, this creates a more stable commercial floor for the prostate cancer diagnostics market than clinical enthusiasm alone could provide.

Liquid Biopsy and Genomic Testing Uptake

The prostate cancer diagnostics market is moving toward a more longitudinal testing model, and liquid biopsy is part of that shift. ASCO guidance in 2025 supported ctDNA use when tissue is inaccessible or when serial monitoring is needed, which moved liquid biopsy further into routine metastatic care.[3]M. Hussain, “Germline and Somatic Genomic Testing for Metastatic Prostate Cancer, ASCO Guideline,” Journal of Clinical Oncology, ascopubs.org A 2026 prospective cohort study in Nature Cancer found that ctDNA positivity after 6 to 12 weeks of combination androgen deprivation therapy was independently associated with 12-month and 24-month survival outcomes in high-volume metastatic disease. That evidence matters because it gives molecular testing clinical relevance beyond a single baseline readout. It also supports repeat-testing economics for the prostate cancer diagnostics market, especially where physicians need to track response or progression without repeated tissue sampling. As these use cases expand, the prostate cancer diagnostics market gains a higher-value layer that is less exposed to standard screening price pressure.

The prostate cancer diagnostics market is also being shaped by AI systems that aim to reduce unnecessary biopsies and improve MRI interpretation consistency. A multicenter UK study published in European Radiology in 2026 validated an AI decision-support tool that combined PI-RADS scores, automated PSA density, and deep learning imaging risk scores across 6 centers. A 2025 Nature Communications study reported prospective clinical use of ProAI, a fully automated deep learning system that improved diagnostic performance and workflow efficiency in real hospital settings. A 2026 study in npj Digital Medicine reported that Prost-LM achieved an internal validation AUC of 0.954 for prostate cancer versus benign conditions across a 3,940-patient multicenter cohort, compared with 0.868 for MRI-only models. These results favor companies that can pair algorithm development with prospective validation and regulatory discipline. That dynamic can widen the role of the prostate cancer diagnostics market in radiology and urology workflows without displacing the underlying need for pathology confirmation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Cost for Advanced Diagnostics | -1.2% | United States, South & Southeast Asia, MEA | Short term (≤ 2 years) |

| Variable Clinical Utility and PSA Overdiagnosis Concerns | -0.9% | Global, concentrated in Europe and Japan | Long term (≥ 4 years) |

| Limited Access to Advanced Diagnostics in Price-Sensitive Markets | -0.8% | India, Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Workflow and Integration Complexity Across Legacy Care Settings | -0.7% | Eastern Europe, Latin America, APAC emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost for Advanced Diagnostics

The prostate cancer diagnostics market still faces a clear affordability barrier in advanced testing categories. ASCO’s 2025 guideline noted that ctDNA liquid biopsy tests are priced at USD 1,000 to USD 3,000 per test, and genomic classifiers often fall into a similar range. Those price levels can suppress both physician ordering and patient uptake outside strong reimbursement frameworks. Access differences are not only financial, because a 2025 Medicare claims study in Cancer Imaging found materially lower PSMA PET use among rural patients and the sharpest gap among Black patients in rural settings. This means advanced testing volume remains concentrated in insured, urban, and academically linked populations. That concentration limits how fully the prostate cancer diagnostics market can reflect the true epidemiological burden of disease across broader populations.

Variable Clinical Utility and PSA Overdiagnosis Concerns

The prostate cancer diagnostics market also remains constrained by the long-standing limits of PSA-led screening. PSA can generate false positives and can identify indolent cancers that do not require intervention, which keeps the screening policy cautious in several major systems. The U.S. Preventive Services Task Force's position on shared decision-making for men aged 55 to 69 and its recommendation against systematic screening at older ages continue to set practical limits on broad screening expansion. Japan still shows mixed signals because the Ministry of Health position remained cautious while the Japanese Urological Association’s 2025 guidance moved toward weak support for individual testing. A 2026 review in Cancers found that ctDNA was detectable in only 43% of localized prostate cancer cases with PSA below 10 ng/mL, which means molecular escalation is not always productive in low-risk settings. That slows adoption of more expensive multimodal protocols in health systems that still need clearer proof of incremental value above PSA alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnostic Technology: PSMA PET Converts Niche Adoption Into Clinical Standard

PSA and biomarker testing held 46.31% of the prostate cancer diagnostics market share in 2025, while PSMA PET and CT imaging is projected to grow at an 8.68% CAGR through 2031. PSA-based testing remains the broad volume base of the prostate cancer diagnostics market because it is scalable, low-cost, and widely embedded in primary care and referral pathways. PSMA PET has moved into a different position because its role is now tied more closely to staging quality and downstream treatment selection. Journal of Nuclear Medicine data showed that PSMA PET use among high-risk and very-high-risk patients in the VA system had risen to 70% by mid-2023 after guideline support strengthened. MRI and mpMRI continue to gain value as pre-biopsy triage tools, especially in health systems that want to reduce unnecessary biopsy volume while preserving detection of clinically significant disease.

Biopsy and histopathology still remain central to definitive diagnosis, grading, and subtype assessment across the prostate cancer diagnostics market. The more important change is that imaging now has stronger clinical authority before biopsy and around therapy decisions, rather than only after pathology. PSMA PET carries added relevance because it links diagnosis with theranostic pathways, which raises its importance beyond a single imaging event. This makes the prostate cancer diagnostics industry more dependent on vendors that can align clinical evidence, tracer supply, reimbursement, and physician education at the same time. At the same time, PSA and related biomarker tests are likely to remain the largest technology category because no other platform matches their population-level reach and repeat-testing frequency.

By Sample Type: Tissue Reclaims Diagnostic Relevance in the Precision Therapy Era

Blood-based samples represented 46.68% of the prostate cancer diagnostics market size in 2025, while tissue is the fastest-growing sample type with a 10.12% CAGR through 2031. Blood remains dominant because PSA testing still drives the highest routine volume in the prostate cancer diagnostics market, and ctDNA has widened the role of blood in advanced disease management. Tissue is growing faster because treatment selection increasingly depends on immunohistochemistry and genomic profiling that cannot always be replaced by liquid biopsy. This shifts tissue from a traditional confirmation role toward a recurring precision-oncology role in selected patients. Urine-based diagnostics are also drawing interest at the decentralized end of the pathway because they can fit low-friction collection models and may help refine pre-biopsy risk selection.

The sample mix now reflects a more layered clinical pathway inside the prostate cancer diagnostics market rather than a single dominant specimen logic. Blood remains the main entry point for screening and routine monitoring. Tissue becomes more important when physicians need deeper characterization for therapy planning or for higher-confidence disease classification. Urine fits best where providers want a noninvasive step between PSA signal and invasive workup, while saliva and other biospecimens remain early-stage options with limited routine use. This mix favors companies that can operate across more than one sample type and support both broad-volume testing and high-specificity downstream decisions in the prostate cancer diagnostics industry.

By Cancer Type: Rare Subtypes Drive Molecular Platform Investment

Prostatic adenocarcinoma accounted for 88.16% of the cancer type segment in 2025, making it the clear commercial core of the prostate cancer diagnostics market. Small cell carcinoma of the prostate is projected to expand at a 9.34% CAGR through 2031, even though it remains much smaller in absolute volume. The faster growth reflects rising recognition of treatment-emergent neuroendocrine differentiation in castration-resistant settings and the diagnostic difficulty created by PSA-silent biology. A 2026 study in npj Precision Oncology showed that aggressive variant prostate cancer, including small cell and neuroendocrine forms, requires integrative molecular characterization that goes well beyond standard PSA measures. That creates a commercial case for next-generation sequencing and multi-omic platforms even when the underlying subtype population is limited.

The heavy dominance of adenocarcinoma means most clinical guidelines, reimbursement rules, and companion testing logic still center on that disease form across the prostate cancer diagnostics market. Rare subtypes therefore matter less because of present volume and more because they expose the limits of conventional diagnostic frameworks. Companies that can address these gaps may gain high-value specialist demand even without a mass screening scale. This also means the prostate cancer diagnostics industry is likely to stay uneven, with broad-volume products built around adenocarcinoma and higher-complexity platforms aimed at diagnostically difficult minority populations. Over time, rare-subtype work can influence platform design more than it changes near-term revenue mix.

By Stage: Castration-Resistant Prostate Cancer Commands Investment Intensity

Localized prostate cancer held 53.62% share in 2025, while castration-resistant prostate cancer is projected to grow at an 10.98% CAGR through 2031. Localized disease remains the largest stage segment because organized screening and earlier workup generate the highest patient volumes at this point in the care pathway. Castration-resistant disease grows faster because each patient usually needs more intensive testing, more molecular selection, and closer monitoring than patients with earlier-stage disease. The prostate cancer diagnostics market, therefore, sees very different economics by stage, with localized disease driving volume and advanced disease driving testing complexity. In metastatic castration-resistant settings, biomarker selection for targeted therapies pushes genomic profiling and ctDNA tools from optional use toward treatment-linked necessity.

This split shapes product strategy across the prostate cancer diagnostics market. Vendors focused on localized disease benefit from scale, screening linkages, and efficient referral integration. Vendors focused on later-stage disease benefit from higher clinical intensity, stronger treatment dependence, and repeat-testing opportunities. Recurrent and advanced patients with rising PSA after primary therapy also support the move toward longitudinal molecular monitoring when conventional imaging is less sensitive. That is why stage mix matters not only for test volumes, but also for pricing resilience and clinical stickiness across the prostate cancer diagnostics market.

By End User: Reference Laboratories Scale to Meet Genomic Complexity

Hospital urology departments held 49.19% share in 2025, while oncology reference laboratories are projected to grow at an 8.57% CAGR through 2031. Hospitals remain the largest end-user base because biopsy, histopathology, mpMRI triage, and initial specialist workup are still centered there. Reference laboratories are growing faster because complex genomic assays and ctDNA workflows need centralized bioinformatics, high-throughput processing, and accreditation capabilities that most hospital labs do not maintain at a comparable scale. This pushes a larger share of advanced testing out of local facilities and into specialized networks. Quest Diagnostics and Labcorp are positioned to benefit from this shift because they already operate large physician-ordering and molecular-testing infrastructures.

Urology clinics are still extending their role within the prostate cancer diagnostics market, especially where office-based biopsy pathways are becoming more practical. A 2025 Scientific Reports study found that freehand transperineal prostate biopsy under local anesthesia achieved a 47.4% clinically significant cancer detection rate without infectious complications, which supports broader outpatient use. Diagnostic imaging centers also gain importance as advanced imaging becomes more integrated into staging and treatment planning. Research and academic institutes remain smaller in routine clinical volume, but they continue to influence assay development, validation design, and future workflow standards across the prostate cancer diagnostics market.

Geography Analysis

North America accounted for 43.64% of the prostate cancer diagnostics market share in 2025, which made it the leading regional contributor by value. The region benefits from high PSA testing penetration, strong specialist infrastructure, and a reimbursement environment that is gradually expanding support for genomic classifiers and advanced imaging. The United States alone is expected to record 333,830 new prostate cancer cases in 2026, which sustains a very large testing base across screening, staging, and follow-up. CMS coverage for selected genomic tools and strong uptake of PSMA PET in higher-risk patients strengthen North America’s leadership in the prostate cancer diagnostics market. Canada benefits from coordinated provincial cancer programs but still shows less advanced imaging depth outside major academic centers, while Mexico remains more PSA-centric with advanced imaging concentrated in private networks.

Europe remains clinically sophisticated, but the prostate cancer diagnostics market is more uneven there because screening policy, reimbursement depth, and implementation speed vary widely by country. Germany’s high-risk staging pathways and the wider EU regulatory environment favor established vendors with validated assay portfolios. The United Kingdom’s MRI-first approach before prostate biopsy has become a recognized model for limiting unnecessary procedures while preserving diagnostic quality. Sweden is also building evidence through region-based organized prostate cancer testing programs with standardized risk-stratified protocols. France, Spain, and Italy are expanding structured PSA access, and Lombardy’s pilot results show that large urban screening models can scale without obvious overdiagnosis in early implementation.

Asia-Pacific is the fastest-growing region, and the prostate cancer diagnostics market size there is projected to rise at a 9.96% CAGR through 2031 as screening and diagnostic infrastructure catch up with disease burden. More than 60% of prostate cancer patients in China are diagnosed at advanced stages, while the United States diagnoses around 70% at localized or regional stages, which highlights the scale of under-screening and under-staging in the region. Japan’s 2025 guideline shift toward individual PSA screening and Chinese evidence supporting the Prostate Health Index both support stronger test adoption in the region. India, South Korea, and Australia add further growth potential, while the Middle East and Africa and South America continue to expand from smaller bases with uptake led by private networks, targeted partnerships, and selective investment in advanced imaging and molecular testing.

Competitive Landscape

The prostate cancer diagnostics market operates across 2 intersecting competitive tracks. Large diversified diagnostics groups such as Roche, Siemens Healthineers, Abbott, Danaher, Thermo Fisher Scientific, QIAGEN, and bioMérieux hold broad strength in instruments, reagents, installed base, and distribution. More focused oncology diagnostics companies such as Lantheus, Veracyte, MDxHealth, OPKO Health, and Proteomedix compete through narrower clinical specialization, selected reimbursement wins, and stronger alignment with specific oncology workflows. The prostate cancer diagnostics market remains moderately consolidated because leadership is strong within certain technology verticals, but no single company dominates across screening, imaging, pathology, molecular testing, and treatment-linked diagnostics at the same time. Abbott’s completion of its USD 21 billion acquisition of Exact Sciences in March 2026 is the clearest sign that scale, platform breadth, and precision oncology capability are becoming more tightly linked in the prostate cancer diagnostics market.

Competitive white space remains strongest in AI-native diagnostics, decentralized urine and home-collection testing, and molecular tools for rare non-adenocarcinoma disease forms. Siemens Healthineers expanded its strategic collaboration with Mayo Clinic in 2025, which shows how large vendors are using clinical partnerships to build validation, real-world evidence, and specialist credibility in advanced imaging and AI-assisted workflows. Veracyte’s Q1 2026 testing revenue exceeded USD 135 million, and the company guided to USD 570 million to USD 582 million in total 2026 revenue, which shows that focused genomic players can achieve scale without matching the installed-base breadth of diversified instrument companies. Lantheus and GE HealthCare also moved to extend PYLARIFY in Japan through an exclusive licensing arrangement, which reflects how regional distribution and radiopharmaceutical infrastructure can shape competitive position as much as assay performance.

The next stage of competition in the prostate cancer diagnostics market is likely to center on who can connect broad screening volume with higher-value staging and treatment-selection decisions. Large vendors have an advantage when procurement, compliance, and workflow integration matter most. Specialists have an advantage when clinical specificity, oncology focus, and high-value evidence are the deciding factors. That balance means the prostate cancer diagnostics market is still open to partnership, licensing, and acquisition activity rather than full leadership by a single cross-modal platform.

Prostate Cancer Diagnostics Industry Leaders

Abbott Laboratories

Becton, Dickinson and Company

Illumina, Inc.

QIAGEN N.V.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Roche received EU IVDR approval for label expansions of the VENTANA MMR RxDx Panel as a companion diagnostic across multiple cancer types and immunotherapy combinations, reinforcing its IHC platform breadth in oncology settings across European markets.

- March 2026: Abbott completed the USD 21 billion acquisition of Exact Sciences, establishing Abbott as a leader in cancer screening and precision oncology diagnostics. Exact Sciences, previously generating over USD 3 billion in annual revenue, becomes a wholly owned Abbott subsidiary.

- November 2025: Abbott announced its definitive agreement to acquire Exact Sciences at USD 105 per common share, representing total equity value of approximately USD 21 billion and enterprise value of approximately USD 23 billion.

- September 2025: Lantheus Holdings and GE HealthCare signed an exclusive licensing agreement for piflufolastat F18 (PYLARIFY) in Japan, with GE HealthCare leveraging its Nihon Medi-Physics acquisition to lead clinical development, manufacturing, and commercialization of PSMA PET imaging in Japan.

Global Prostate Cancer Diagnostics Market Report Scope

The prostate cancer diagnostics market encompasses the medical tools, laboratory services, and imaging technologies used to detect and monitor prostate cancer. Valued in the billions globally, the market is driven by an aging male population, routine health screenings, and technological advancements like AI-driven liquid biopsies and genomic testing.

The Prostate Cancer Diagnostics Market is structured across several dimensions that capture the breadth of technologies, clinical applications, and geographic reach. By diagnostic technology, it encompasses PSA and Biomarker Testing, MRI and mpMRI Imaging, Biopsy and Histopathology, Molecular and Genomic Testing, and PSMA PET and CT Imaging. By sample type, the market relies on Blood, Tissue, Urine, and Saliva and Other Biospecimens. By cancer type, diagnostics target Prostatic Adenocarcinoma, Small Cell Carcinoma, Interstitial Cell Carcinoma, and Other Prostate Cancer Types. By stage, testing is applied in Localized Prostate Cancer, Recurrent and Advanced Prostate Cancer, and Castration-Resistant Prostate Cancer. By end user, the market spans Hospital Urology Departments, Oncology Reference Laboratories, Diagnostic Imaging Centers, Urology Clinics, and Research and Academic Institutes.

Geographically, it is divided into North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| PSA and Biomarker Testing |

| MRI and mpMRI Imaging |

| Biopsy and Histopathology |

| Molecular and Genomic Testing |

| PSMA PET and CT Imaging |

| Blood |

| Tissue |

| Urine |

| Saliva and Other Biospecimens |

| Prostatic Adenocarcinoma |

| Small Cell Carcinoma |

| Interstitial Cell Carcinoma |

| Other Prostate Cancer Types |

| Localized Prostate Cancer |

| Recurrent and Advanced Prostate Cancer |

| Castration-Resistant Prostate Cancer |

| Hospital Urology Departments |

| Oncology Reference Laboratories |

| Diagnostic Imaging Centers |

| Urology Clinics |

| Research and Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diagnostic Technology | PSA and Biomarker Testing | |

| MRI and mpMRI Imaging | ||

| Biopsy and Histopathology | ||

| Molecular and Genomic Testing | ||

| PSMA PET and CT Imaging | ||

| By Sample Type | Blood | |

| Tissue | ||

| Urine | ||

| Saliva and Other Biospecimens | ||

| By Cancer Type | Prostatic Adenocarcinoma | |

| Small Cell Carcinoma | ||

| Interstitial Cell Carcinoma | ||

| Other Prostate Cancer Types | ||

| By Stage | Localized Prostate Cancer | |

| Recurrent and Advanced Prostate Cancer | ||

| Castration-Resistant Prostate Cancer | ||

| By End User | Hospital Urology Departments | |

| Oncology Reference Laboratories | ||

| Diagnostic Imaging Centers | ||

| Urology Clinics | ||

| Research and Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of prostate cancer diagnostics by 2031?

The prostate cancer diagnostics market is projected to reach USD 13.86 billion by 2031, rising from USD 9.42 billion in 2026 at an 8.03% CAGR from 2026 to 2031.

Which diagnostic technology is growing the fastest?

PSMA PET and CT imaging is the fastest-growing diagnostic technology segment, with a projected 8.68% CAGR through 2031.

Why does PSA testing still lead revenue?

PSA and biomarker testing led with 46.31% share in 2025 because it remains low-cost, scalable, and widely used in primary care and referral workflows.

Which sample type is expanding the fastest?

Tissue-based testing is growing the fastest at a 10.12% CAGR through 2031 because treatment selection increasingly depends on deeper molecular and pathology-based characterization.

Which region leads current demand?

North America led with 43.64% share in 2025 due to strong screening penetration, advanced specialist infrastructure, and growing reimbursement support for higher-value diagnostics.

What is driving the strongest long-term opportunity?

The strongest long-term opportunity comes from combining broader screening with higher-value molecular monitoring, AI-assisted imaging, and treatment-linked testing pathways, especially in Asia-Pacific where growth is projected at 9.96% through 2031.

Page last updated on: