Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

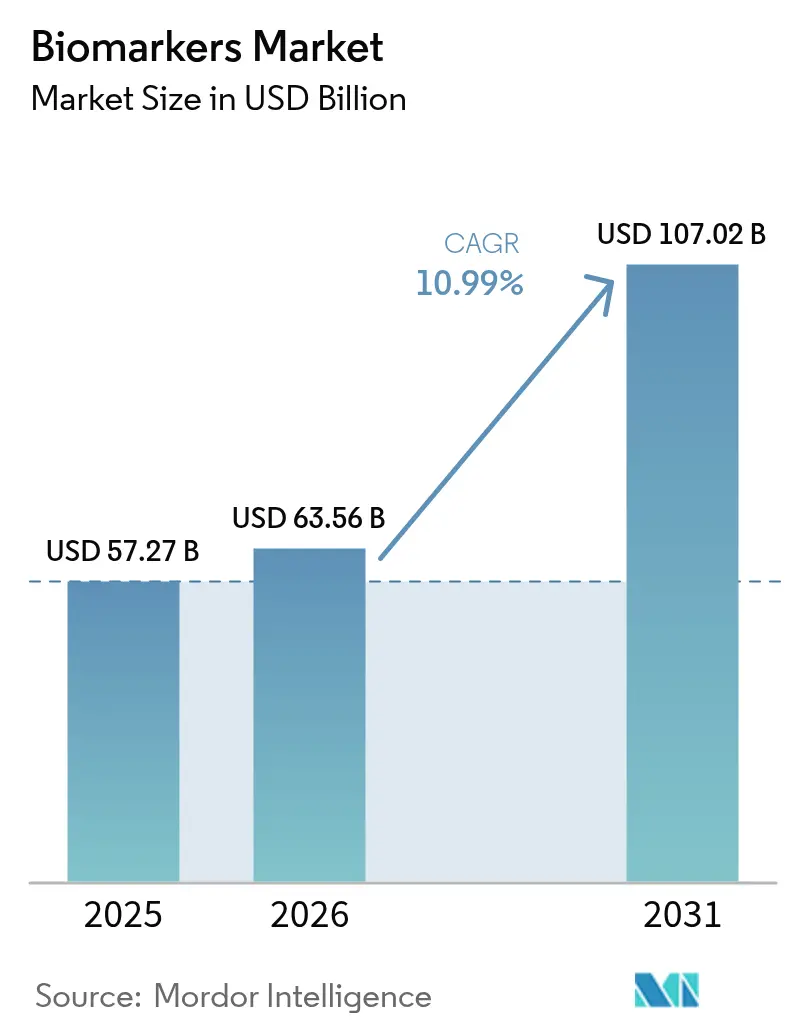

| Market Size (2026) | USD 63.56 Billion |

| Market Size (2031) | USD 107.02 Billion |

| Growth Rate (2026 - 2031) | 10.99% CAGR |

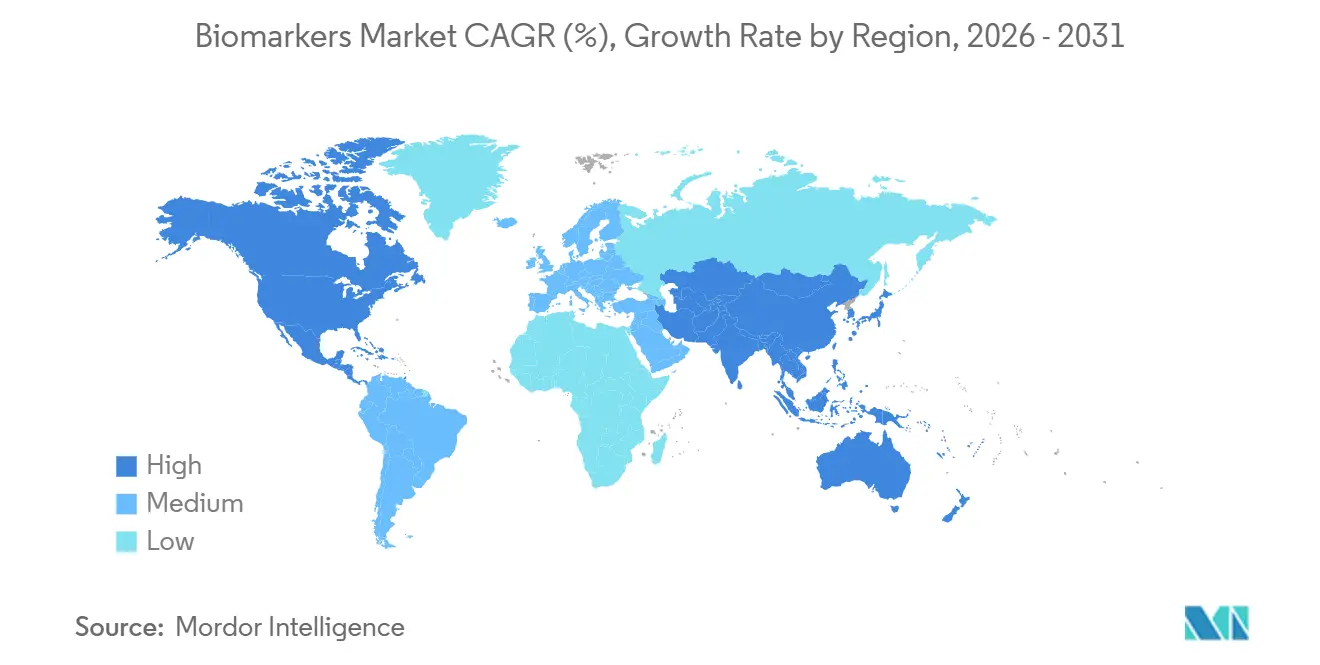

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

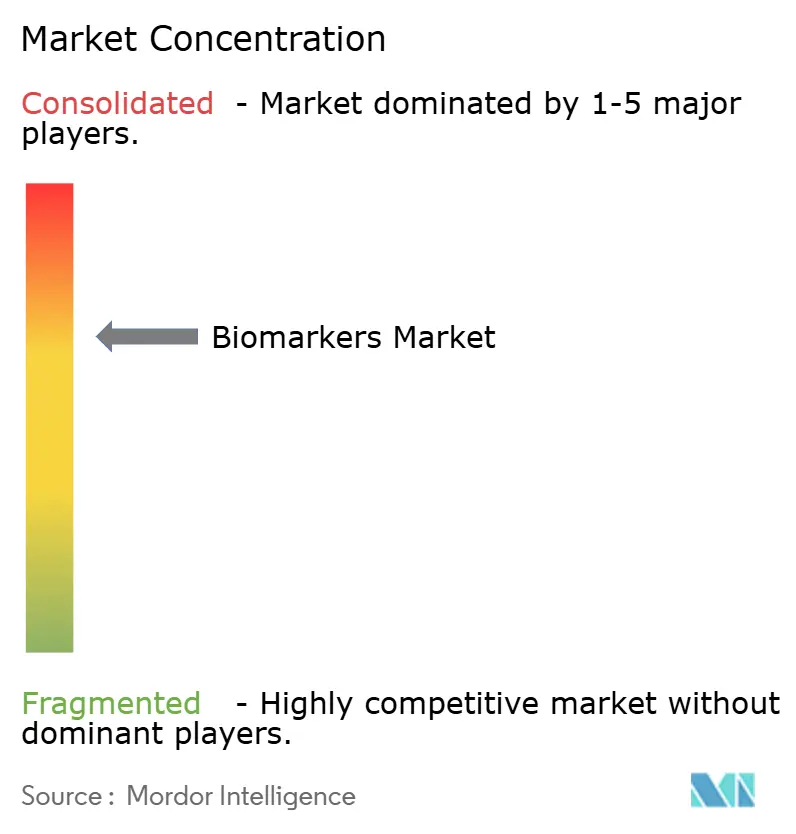

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomarkers Market Analysis by Mordor Intelligence

The Biomarkers Market size is expected to increase from USD 57.27 billion in 2025 to USD 63.56 billion in 2026 and reach USD 107.02 billion by 2031, growing at a CAGR of 10.99% over 2026-2031.

Regulatory programs that qualify novel markers, pharmaceutical pipelines built around biomarker-stratified Phase II and III trials, and payer moves that tie reimbursement to validated companion diagnostics are the primary forces behind this expansion. Liquid-biopsy assays that detect circulating tumor DNA months before imaging, multiplex cytokine panels that anticipate autoimmune flares, and single-drop proteomics that profile 11,000 proteins are broadening clinical use cases. Government funding for precision-medicine infrastructure in the United States, China, and the European Union provides long-term capital for validation cohorts, while cloud-based analytics shorten turnaround times and enable community hospitals to retain testing margins. Competitive activity centers on vertical integration—diagnostics majors now bundle sequencing, data interpretation, and outcomes datasets—creating high entry barriers for smaller laboratories.

Key Report Takeaways

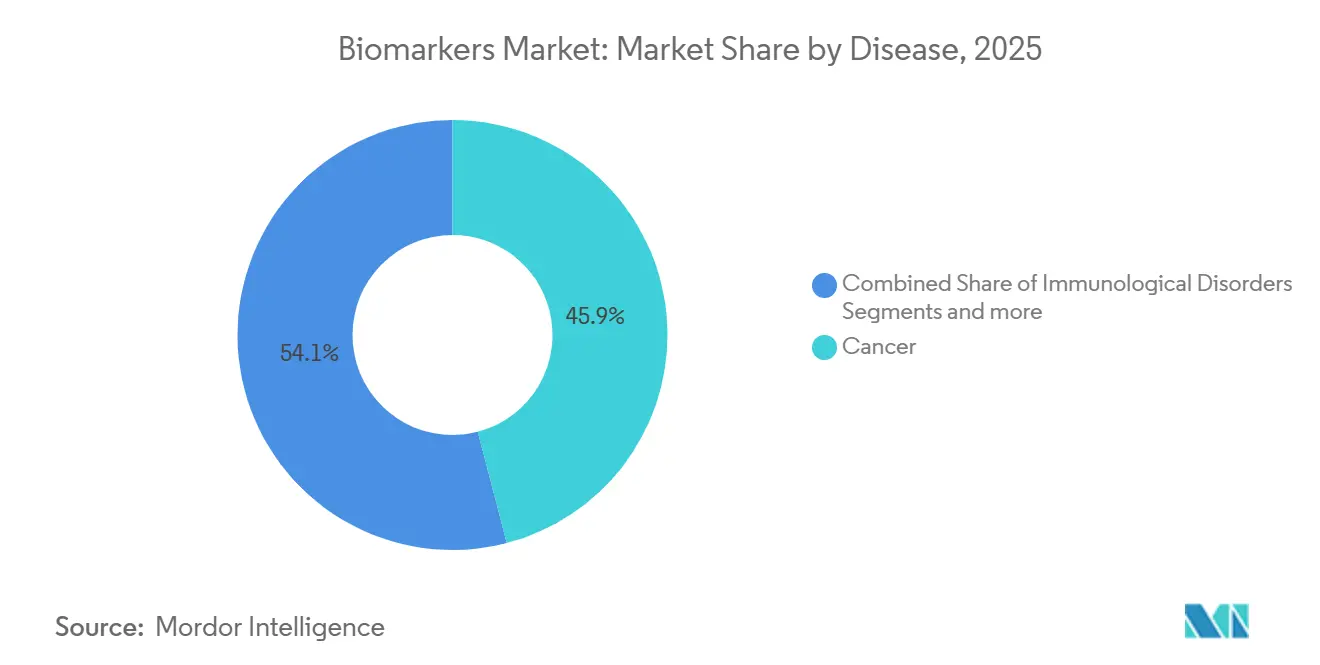

- By disease, cancer led with 45.94% revenue share in 2025 while immunological disorders are forecast to advance at a 12.65% CAGR from 2026-2031.

- By type, efficacy biomarkers captured 57.78% share in 2025 whereas safety biomarkers are projected to expand at a 12.88% CAGR through 2031.

- By mechanism, genetic biomarkers held 46.85% share in 2025 and epigenetic biomarkers are set to grow at a 13.87% CAGR over the forecast period.

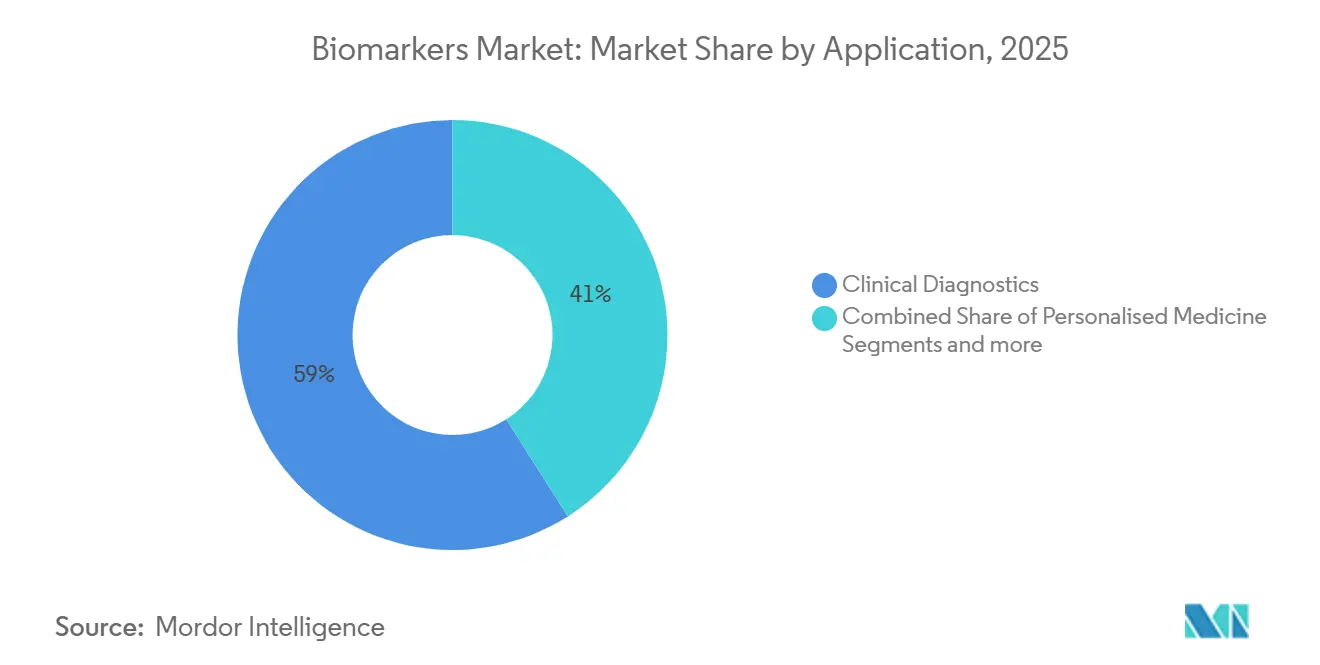

- By application, clinical diagnostics accounted for 59.02% of 2025 revenue while personalised medicine is expected to rise at a 14.11% CAGR to 2031.

- By product, consumables represented 53.71% of revenue in 2025; services and software are poised for a 13.76% CAGR during 2026-2031.

- By geography, North America dominated with 42.53% share in 2025, whereas Asia-Pacific is projected to record an 11.54% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Incidence of Chronic and Degenerative Diseases | +2.8% | Global, with acute burden in North America and Europe | Long term (≥ 4 years) |

| Growing Emphasis on Precision Medicine | +2.5% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Continuous Advances in Omics and Analytical Technologies | +2.2% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Adoption of Companion Diagnostics by Pharma Companies | +1.9% | North America, Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Expanding Government and Private Funding for Biomarker Research | +1.3% | North America, Europe, China | Long term (≥ 4 years) |

| Growing Penetration of Digital Health Platforms and Real-World Evidence | +1.1% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Chronic and Degenerative Diseases

Cancer cases rose to 20 million worldwide in 2024, a 15% jump from 2020, and cardiovascular disease remained the top killer with 18.6 million deaths in 2025. Demand for early-detection biomarkers surged as liquid biopsies revealed relapse months before radiology, and plasma phosphorylated-tau 217 hit 89% sensitivity for detecting Alzheimer’s pathology, cutting reliance on PET scans. Japan reimbursed multi-cancer blood tests in late 2025, while India rolled out kidney-injury panels in primary care as part of a nationwide chronic-disease program.

Growing Emphasis on Precision Medicine

The FDA cleared 18 companion diagnostics in 2025, spanning oncology, cardiology, and rare genetic disorders. Medicare began reimbursing tumor mutational burden and microsatellite instability sequencing in January 2025, unlocking access for 1.9 million beneficiaries[1]Centers for Medicare & Medicaid Services, “Final NCD for Next-Generation Sequencing,” cms.gov. AstraZeneca partnered with Illumina to monitor minimal residual disease in lung cancer trials, lowering late-stage failures by 30%. Dutch health systems updated 120 pharmacogenomic dosing guidelines, and a Pennsylvania hospital network embedded HL7 FHIR-based decision support that cut inappropriate prescribing by 22%.

Continuous Advances in Omics and Analytical Technologies

Whole-genome sequencing dipped below USD 500 in 2025 after Illumina’s NovaSeq X Plus launch and Oxford Nanopore’s rapid long-read upgrades. SomaLogic’s 11 K proteomics assay, Thermo Fisher’s sub-PPM Orbitrap Astral, and single-cell spatial transcriptomics from 10x Genomics redefined analytical depth. Regulators cleared the first circulating-tumor-cell system for metastatic breast-cancer monitoring in 2024, expanding the liquid-biopsy repertoire.

Rising Adoption of Companion Diagnostics by Pharma Companies

Twenty-three companion diagnostics were launched in 2025 as regulators now expect biomarker-stratified enrollment in pivotal trials. Roche’s FoundationOne CDx drove treatment changes in 68% of oncologist decisions, and Novartis secured EMA approval of a breast cancer companion test linked to PIK3CA mutations. Home-collection blood kits, such as Labcorp’s 2025 ctDNA sampler, enable decentralized sample acquisition, and BioMarin paired gene therapy with an AAV5 seronegativity assay to qualify patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory and Reimbursement Barriers | -1.8% | Global, acute in Europe and emerging markets | Long term (≥ 4 years) |

| High Costs Associated with Biomarker Validation | -1.2% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Data Privacy and Security Concerns | -0.9% | Global, stringent in Europe under GDPR | Medium term (2-4 years) |

| Lack of Standardization Across Biomarker Platforms | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Reimbursement Barriers

Multi-year qualification dossiers and independent validation cohorts slow launches; the FDA and EMA each require context-of-use submissions that can push commercialization back 3-5 years[2]European Medicines Agency, “Qualification of Novel Methodologies,” ema.europa.eu. Germany declined reimbursement for FoundationOne CDx in 2024 pending head-to-head comparisons, and proposed U.S. rules on laboratory-developed tests add pre-market review obligations. India now mandates local clinical validation, and UnitedHealthcare withheld coverage for multi-cancer testing in the absence of survival benefit data.

High Costs Associated with Biomarker Validation

Analytical, clinical, and utility studies run USD 30-80 million per marker, with pre-analytical variation adding to replication budgets. Longitudinal cohorts can span a decade, delaying ROI, and rare-disease trials face enrollment hurdles that push per-patient costs over USD 150,000. Overlapping patents in CRISPR detection and sequencing library prep force small companies into expensive license negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: Oncology Dominance Meets Autoimmune Acceleration

Cancer biomarkers accounted for 45.94% of 2025 revenue, underpinned by liquid biopsy assays that guide adjuvant therapy for colorectal, breast, and lung malignancies. Immunological disorders are advancing at a 12.65% CAGR through 2031, with cytokine panels enabling clinicians to titrate biologics before irreversible joint damage. Cardiovascular biomarkers such as high-sensitivity troponin retain clinical ubiquity, but face commoditization pressure, and neurological tests like plasma phosphorylated-tau 181 are redefining Alzheimer’s workflows. Oncology’s grip on the biomarkers market share is sustained by FDA Breakthrough Device incentives and pharma-diagnostic codevelopment models.

The segment’s momentum also benefits from broad payer coverage of tumor mutational burden sequencing in the biomarkers market, which reduces off-label therapy waste. Autoimmune growth reflects unmet need and rapid uptake of multi-analyte panels in rheumatology clinics. Cardiovascular growth plateaus as generic immunoassays anchor hospital formularies, while neurology is projected to rise once CMS finalizes payment for blood-based dementia tests. Infectious-disease panels remain vital in lower-income regions, but oncology revenue will continue to set pricing benchmarks.

By Type: Efficacy Markers Lead, Safety Panels Surge

Efficacy biomarkers accounted for 57.78% of 2025 revenue, encompassing prognostic, predictive, pharmacodynamic, and surrogate markers that accelerate approvals. Safety markers are set to climb 12.88% annually to 2031 as regulators demand cardiotoxicity and hepatotoxicity panels in oncology pipelines. Predictive assays, such as PD-L1 IHC, support immunotherapy triage, while pharmacodynamic read-outs confirm target engagement within hours of dosing.

The biomarkers market size for safety panels is forecast to expand rapidly as drug developers embed multi-analyte hepatotoxicity tests in every Phase II protocol. Market adoption is also driven by payers seeking to minimize adverse-event costs. Validation biomarkers, although the smallest niche, underpin decentralized trials by ensuring sample-handling fidelity across remote sites.

By Mechanism: Genetic Foundations, Epigenetic Frontiers

Genetic biomarkers secured 46.85% of mechanism revenue in 2025 through omnipresent next-generation sequencing panels. Epigenetic assays, especially bisulfite-free methylation tests, are running at a 13.87% CAGR as Grail’s Galleri pushes multi-cancer detection from a single vial of blood. Proteomic panels now quantify thousands of proteins in femtomolar ranges, uncovering disease signatures invisible to genomics.

Genetic assays benefit from established CPT codes and clear FDA pathways, thereby cementing their market share in the biomarker space. Epigenetic platforms, by contrast, rely on emerging reimbursement channels but gain traction through superior early-detection sensitivity. Proteomic workflows face gaps in standardization, yet cross-platform reference initiatives aim to harmonize data by 2028.

By Application: Diagnostics Anchor, Personalized Medicine Accelerates

Clinical diagnostics generated 59.02% of application revenue in 2025, with hospitals and reference labs running troponin, HbA1c, and lipid panels daily. Personalized medicine is advancing at a 14.11% CAGR as pharmacogenomics guides dosing for anticoagulants and antidepressants. Drug-discovery pipelines deploy biomarkers to shrink Phase III cohorts by 30%, saving roughly USD 200 million per asset.

The biomarkers market size for personalized-medicine services is projected to outpace diagnostics by 2030, fuelled by payer evidence that genotype-guided therapy reduces hospitalizations. Disease-risk assessment through polygenic scores opens new employer-wellness revenue streams. Diagnostics remain dominant today thanks to entrenched billing codes, but will gradually cede share as individualized care expands.

By Product: Consumables Dominate, Software Scales

Consumables accounted for 53.71% of product revenue in 2025 because each sequencing run or immunoassay consumes new reagents. Services and software will post 13.76% annual gains as cloud pipelines handle variant interpretation for community hospitals that cannot support in-house bioinformatics. Instruments face slower replacement cycles but still sustain premium pricing in niche modalities such as spatial omics.

Recurring reagent demand grants manufacturers predictable cash flows in the biomarkers market, while subscription-based platforms convert equipment users into long-term software customers. Hospitals prefer shifting capital expenditures into operational budgets, driving the services-and-software ascent.

Geography Analysis

North America accounted for 42.53% of global revenue in 2025, after Medicare expanded next-generation sequencing coverage to all advanced cancers. This policy added 800,000 beneficiaries and created USD 1.6 billion in incremental volume. The United States also qualified 12 novel biomarkers between 2024 and early 2026, further anchoring demand. Canada’s universal health system reimbursed CTDNA minimal residual disease tests for colorectal cancer nationwide in mid-2025.

Asia-Pacific is the fastest mover, growing at 11.54% CAGR through 2031. China added 23 liquid-biopsy assays to provincial insurance catalogues, Japan approved blood-based colorectal cancer screening, and India installed point-of-care troponin devices in 2,500 clinics. Government grants under China’s 14th Five-Year Plan and South Korea’s coverage of 18 new companion diagnostics amplify regional uptake.

Europe shows moderate growth as the fragmented reimbursement landscape slowly harmonizes through the European Health Data Space. Germany finally covered FoundationOne CDx in March 2025, but France and Italy still evaluate budget impacts. Cross-border consent frameworks will likely smooth multi-country studies by 2028, enabling wider biomarker market adoption.

Competitive Landscape

The biomarkers market is moderately consolidated; the top five vendors—Roche, Illumina, Thermo Fisher Scientific, Abbott, and Danaher—accounted for 38% of 2025 revenue. Roche bundles sequencing, clinical-decision software, and Flatiron’s outcomes data; Illumina partners with NVIDIA GPUs to deliver same-day reporting; Thermo Fisher deploys Azure cloud to lower hospital IT friction. Abbott and Danaher target low-resource settings with handheld molecular platforms.

Disruptors such as Guardant Health, Grail, and Freenome captured USD 1.8 billion in venture capital across 2024-2025 by focusing on multi-cancer early detection. Competitive differentiation centers on analytical sensitivity (allele fractions <0.1%), turnaround time (<24 hours), and database completeness. Patent thickets in CRISPR detection and sequencing library prep force newcomers to acquire IP or negotiate multi-party licenses, as Exact Sciences did by buying Thrive Earlier Detection. The market thus favors vertically integrated firms that control reagents, instruments, software, and data.

Biomarkers Industry Leaders

F. Hoffmann-La Roche Ltd

Thermo Fisher Scientific Inc.

Illumina Inc.

Qiagen N.V.

Bio-Rad Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Aliri Bioanalysis introduces 37 pre-configured biomarker panels, enhancing convenience and accelerating disease research. This expansion improves access to comprehensive disease insights for researchers and clinicians.

- February 2026: New England Biolabs released the Monarch Mag Cell-free DNA (cfDNA) Extraction Kit, which enables consistent, scalable extraction of low-abundance, circulating cell-free DNA (cfDNA) for downstream applications, including biomarker discovery and diagnostics development.

- July 2025: Quanterix acquired Akoya Biosciences, establishing the first integrated platform that enables measurement of biomarkers across both blood and tissue samples. This enhances capabilities for comprehensive biomedical analysis.

Global Biomarkers Market Report Scope

As per the scope of the report, a biomarker is a biomolecule or gene used to precisely evaluate the body's pharmacologic, pathogenic, and biological processes. They serve as an early warning system in the body. It can also be described as a traceable subsite introduced into the body to assess the organ's function. It can be measured and evaluated by using blood, urine, or soft tissues.

The Biomarkers Market is Segmented by Disease (Cancer, Cardiovascular, Neurological, Immunological, Renal, and Other), Type (Efficacy, Safety, Validation), Mechanism (Genetic, Epigenetic, Proteomic, Lipidomic, and Other), Application (Clinical Diagnostics, Drug Discovery, Personalised Medicine, Risk Assessment, and Other), Product (Consumables, Instruments, and Services), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Cancer |

| Cardiovascular Disorders |

| Neurological Disorders |

| Immunological Disorders |

| Renal Disorders |

| Other Diseases |

| Efficacy Biomarkers | Prognostic Biomarkers |

| Predictive Biomarkers | |

| Pharmacodynamic Biomarkers | |

| Surrogate Endpoint Markers | |

| Safety Biomarkers | |

| Validation Biomarkers |

| Genetic Biomarkers |

| Epigenetic Biomarkers |

| Proteomic Biomarkers |

| Lipidomic Biomarkers |

| Other Mechanisms |

| Clinical Diagnostics |

| Drug Discovery And Development |

| Personalised Medicine |

| Disease Risk Assessment |

| Other Applications |

| Consumables |

| Instruments |

| Services And Software |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease | Cancer | |

| Cardiovascular Disorders | ||

| Neurological Disorders | ||

| Immunological Disorders | ||

| Renal Disorders | ||

| Other Diseases | ||

| By Type | Efficacy Biomarkers | Prognostic Biomarkers |

| Predictive Biomarkers | ||

| Pharmacodynamic Biomarkers | ||

| Surrogate Endpoint Markers | ||

| Safety Biomarkers | ||

| Validation Biomarkers | ||

| By Mechanism | Genetic Biomarkers | |

| Epigenetic Biomarkers | ||

| Proteomic Biomarkers | ||

| Lipidomic Biomarkers | ||

| Other Mechanisms | ||

| By Application | Clinical Diagnostics | |

| Drug Discovery And Development | ||

| Personalised Medicine | ||

| Disease Risk Assessment | ||

| Other Applications | ||

| By Product | Consumables | |

| Instruments | ||

| Services And Software | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is global biomarker revenue forecast to reach by 2031?

It is projected to climb to USD 107.02 billion by 2031, up from USD 63.56 billion in 2026.

Which disease area accounts for the greatest share of biomarker spending today?

Cancer leads, generating 45.94% of 2025 segment revenue.

What compound annual growth rate is expected for epigenetic biomarkers during 2026-2031?

Epigenetic assays are projected to grow at a 13.87% CAGR over the forecast window.

Why are services and software lines expanding so quickly in biomarker adoption?

Hospitals favor subscription-based analytics that cut capital costs, pushing services and software toward a 13.76% CAGR through 2031.

Which geographic region is expected to record the fastest biomarker uptake through 2031?

Asia-Pacific is set to advance at an 11.54% CAGR, outpacing all other regions.

How fast will personalized medicine applications that use biomarkers expand?

They are poised to rise at a 14.11% CAGR from 2026 to 2031 as payers tie reimbursement to genotype-guided care.

Page last updated on: