Digital Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

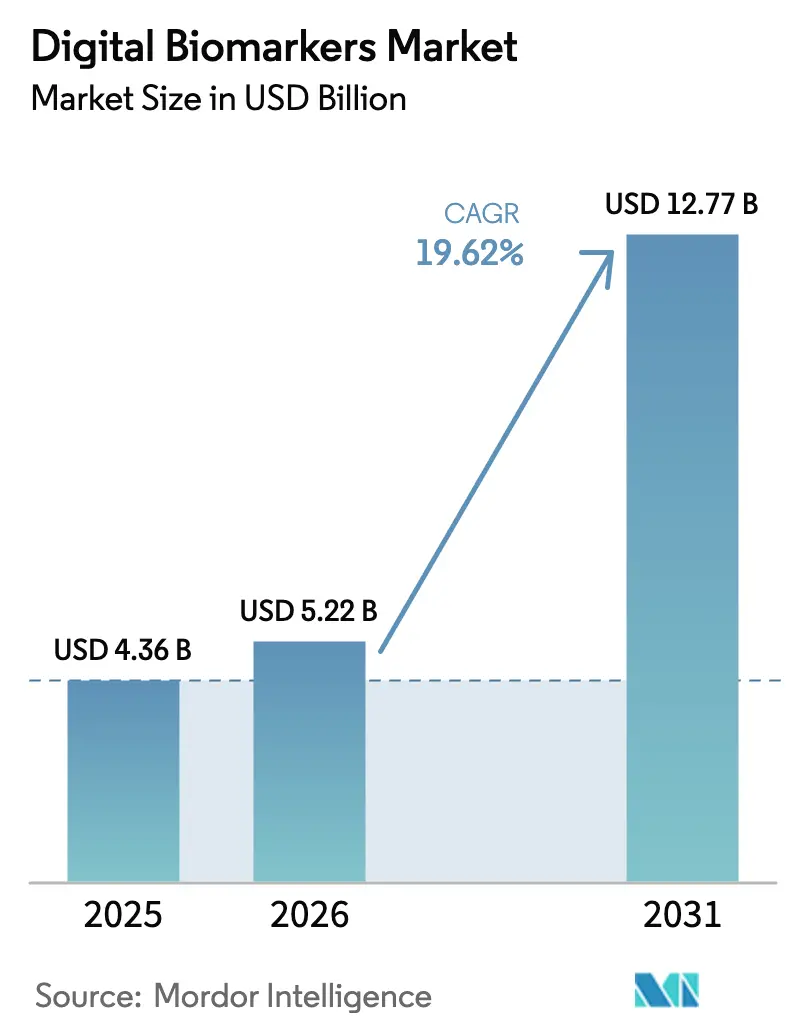

| Market Size (2026) | USD 5.22 Billion |

| Market Size (2031) | USD 12.77 Billion |

| Growth Rate (2026 - 2031) | 19.62% CAGR |

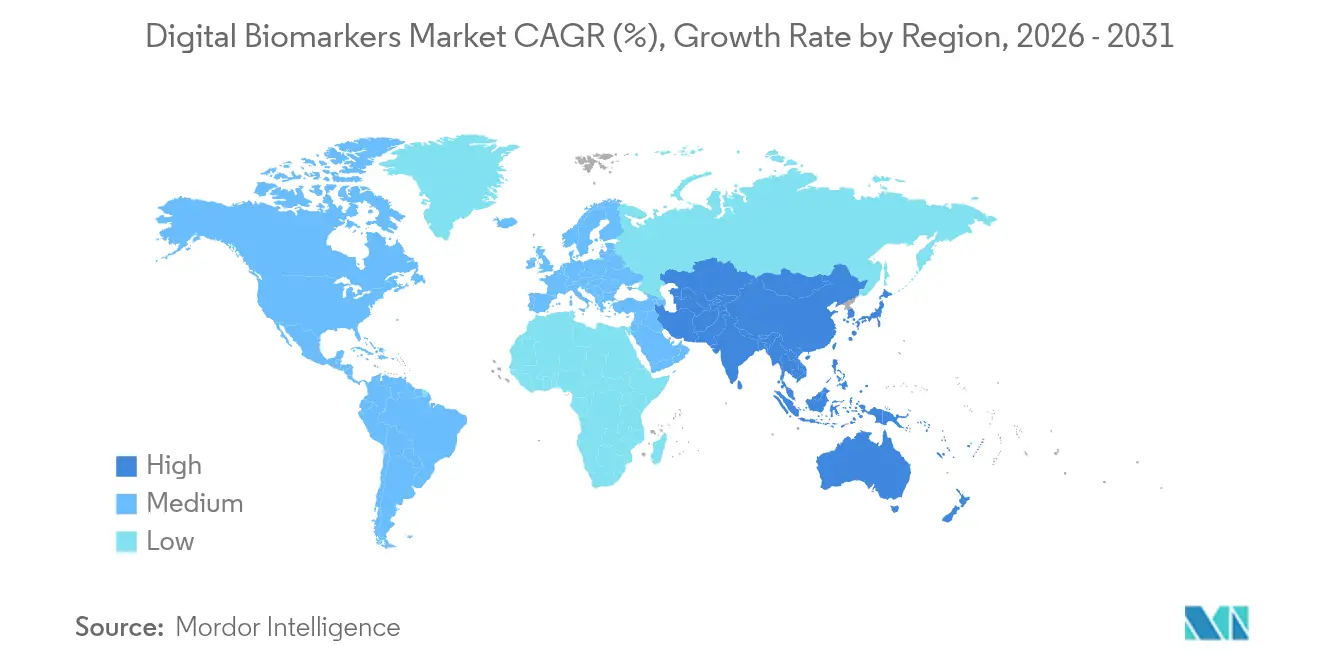

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

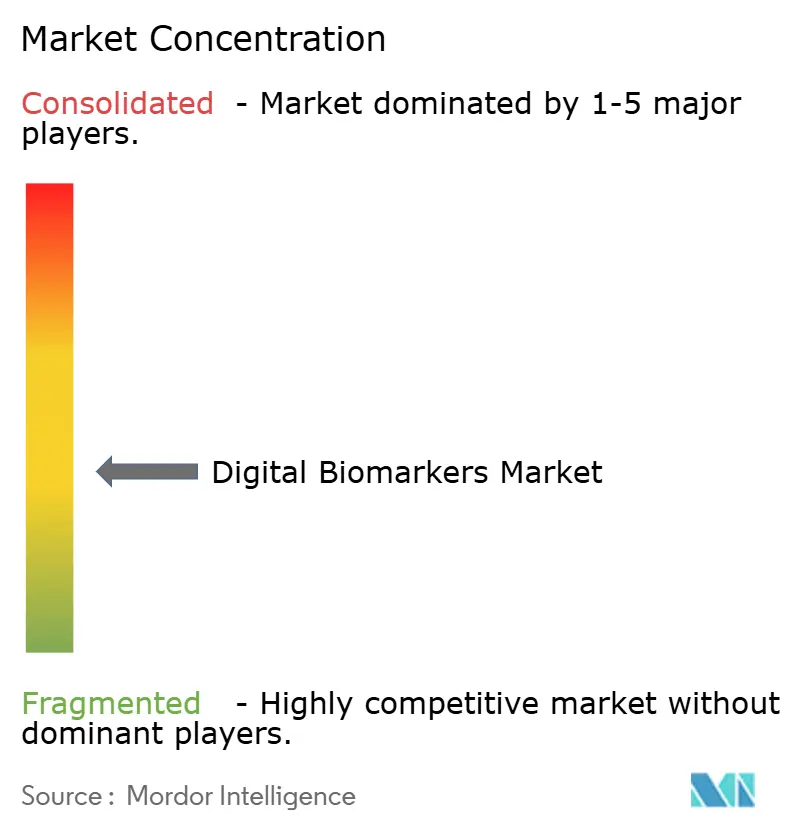

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Digital Biomarkers Market Analysis by Mordor Intelligence

Digital Biomarkers market size in 2026 is estimated at USD 5.22 billion, growing from 2025 value of USD 4.36 billion with 2031 projections showing USD 12.77 billion, growing at 19.62% CAGR over 2026-2031.

Demand accelerates as regulators certify consumer-grade devices, payers reimburse remote monitoring, and clinicians adopt algorithmic endpoints that lower trial costs. FDA qualification of the Apple Watch AFib History feature and the creation of a Digital Health Advisory Committee confirm that mainstream wearables can meet medical-grade evidence standards. At the same time, the European Medicines Agency’s green light for stride-velocity endpoints in Duchenne studies cut sample needs by 70%, spotlighting efficiency gains. Across industry, outcome-based contracts, generative-AI analytics, and real-time phenotyping shift value from raw sensing to data fusion, setting the tone for platform consolidation.

Key Report Takeaways

- By component, Data Collection Tools accounted for 65.12% of digital biomarkers market share in 2025, while Data Integration & Analytics Platforms are forecast to grow at a 20.12% CAGR to 2031.

- By data source, Wearables led with a 39.44% revenue share in 2025; Mobile Applications are projected to expand at a 20.2% CAGR through 2031.

- By therapeutic area, Cardiovascular & Metabolic Disorders held 39.98% of the digital biomarkers market size in 2025, whereas Neurological Disorders are on track for a 20.33% CAGR between 2026-2031.

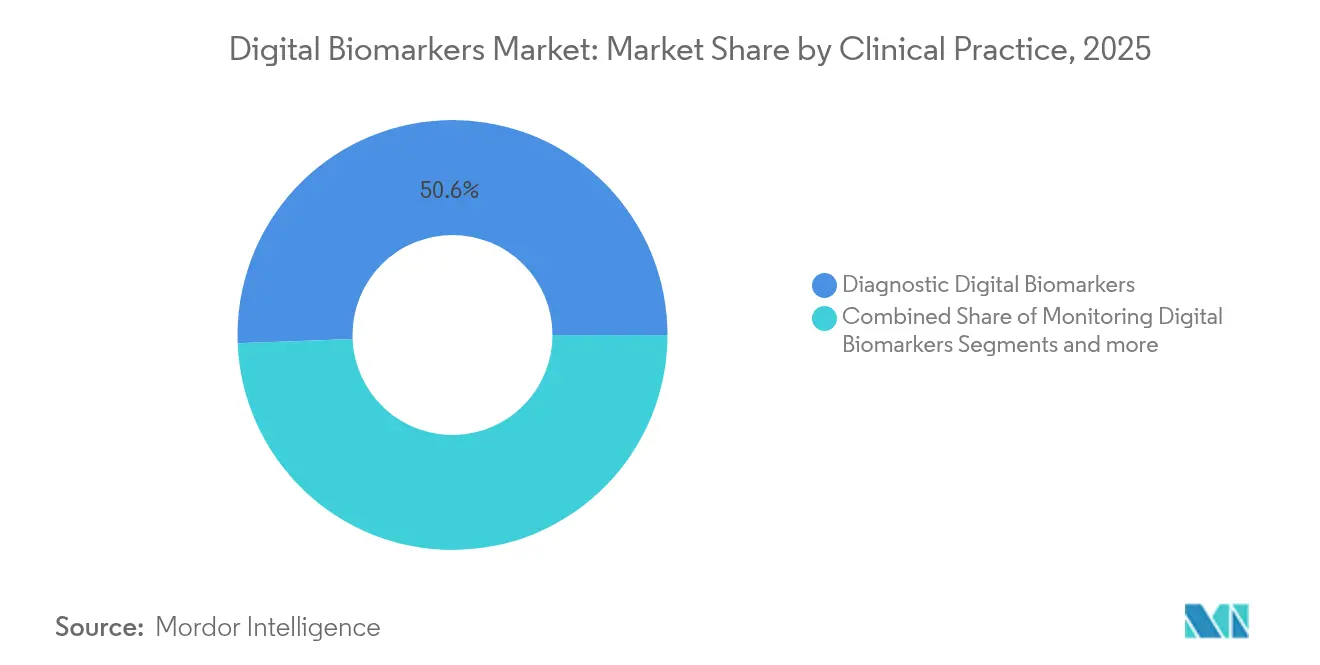

- By clinical practice, Diagnostic Digital Biomarkers represented 50.62% share in 2025, and Monitoring Digital Biomarkers are progressing at a 20.31% CAGR.

- By end user, Pharmaceutical & Biotech Companies represented 37.42% of the digital biomarker market share in 2025, and Payers & Employers are progressing at a 20.18% CAGR.

- By geography, North America captured 42.88% share in 2025; Asia-Pacific is the fastest-growing region at a 20.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of chronic & metabolic diseases | +4.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapid proliferation of clinical trials adopting sensor-based endpoints | +3.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Accelerated FDA qualification of Software-as-a-Medical-Device solutions | +3.1% | North America core, spill-over to global markets | Short term (≤ 2 years) |

| Wearable-centric disease prevention programs by payers & employers | +2.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Generative-AI-enabled multi-modal data fusion for real-time phenotyping | +2.7% | Global, led by North America & China | Long term (≥ 4 years) |

| Pharma shift to outcome-based contracts leveraging longitudinal DBx | +2.4% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing prevalence of chronic & metabolic diseases

Commercial health systems face rising costs from diabetes, obesity, and hypertension. Continuous monitoring fills clinical gaps by spotting deterioration between visits, lowering avoidable admissions, and enabling lifestyle coaching. Six in ten U.S. adults live with a chronic illness, creating healthcare spend above USD 4.1 trillion annually. Dexcom’s USD 75 million investment in Oura aligns glucose trends with sleep, exercise, and stress metrics, demonstrating multi-modal metabolic tracking that supports preventive care [1]Source: DexCom Inc., “Dexcom Invests in Oura Health for Integrated Metabolic Insights,” dexcom.com .

Rapid proliferation of clinical trials adopting sensor-based endpoints

Pharma sponsors now embed digital endpoints to reduce site visits and capture real-world function. EMA qualification of stride velocity in Duchenne studies trimmed recruitment needs by 70% and validated remote gait metrics for rare diseases. Regeneron’s internal digital biomarker laboratory and dedicated summit further prove that large sponsors view sensor data as pivotal for trial acceleration within the digital biomarkers market.

Accelerated FDA qualification of Software-as-a-Medical-Device solutions

Clearer pathways shorten time from proof-of-concept to reimbursement. The FDA Digital Health Advisory Committee, announced in February 2024, creates a permanent review channel, while draft guidance on AI model credibility outlines transparency rules for algorithm updates [2]US Food and Drug Administration, “Digital Health Advisory Committee Announcement,” Food and Drug Administration, fda.gov . Apple’s AFib History tool, cleared as a class II medical device development asset, shows that consumer devices can cross the regulatory threshold when rigorous evidence is provided.

Wearable-centric disease prevention programs by payers & employers

U.S. remote patient monitoring revenue is expected to double from 2024 to 2030, supported by Medicare CPT codes that reimburse data review and patient coaching. Employer health plans integrate step counts, heart-rate variability, and sleep scores to stratify risk and incentivize healthier behavior, generating savings through avoided emergency visits and lower premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory pathways across regions | -2.1% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Cyber-security & patient-consent hurdles for continuous data capture | -1.8% | Global, with stricter requirements in EU | Long term (≥ 4 years) |

| Lack of reimbursement codes for stand-alone digital endpoints | -1.5% | Global, with progress in North America | Short term (≤ 2 years) |

| Signal drift & algorithm bias in diverse populations | -1.2% | Global, with focus on underrepresented populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented regulatory pathways across regions

Although the EU Medical Device Regulation seeks harmonization, divergent evidence demands still force sponsors to run extra studies, raising costs [3]Carolina Amaral, "Global Regulatory Challenges for Medical Devices: Impact on Innovation and Market Access," MDPI, mdpi.com. Germany’s Digital Health Care Act grants reimbursement for DiGA apps, yet similar frameworks lag in other member states, slowing multinational launches. Japan’s historical device-approval lag illustrates how inconsistent timelines limit cross-border scalability in the digital biomarker market.

Cyber-security & patient-consent hurdles for continuous data capture

Data streams entering electronic health records must comply with GDPR in Europe and HIPAA in the United States. High-resolution behavioral data heighten breach risks, driving hospitals to request formal penetration testing and end-to-end encryption audits before deployment. Public concerns over algorithmic transparency and secondary data use can dampen enrollment, especially for mental-health monitoring applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Analytics Platforms Drive Value Creation

Data Collection Tools commanded 65.12% of digital biomarkers market share in 2025 because sensors and gateways remain essential for capturing physiological and behavioral signals. However, Data Integration & Analytics Platforms are growing at a 20.12% CAGR, reflecting a structural shift toward advanced pipelines that clean, fuse, and interpret data for clinical decision support. Study Watch by Verily converts multi-channel raw inputs into validated gait, tremor, and sleep biomarkers, illustrating how software unlocks predictive power for trial sponsors and care teams.

Platform suppliers raise entry barriers through proprietary algorithms and regulatory dossiers. Consolidation is expected as device-centric vendors acquire analytics assets, mirroring the USD 75 million Dexcom–Oura tie-up that links sensor streams with metabolic insights. In this context, data-fusion engines that deliver real-time phenotyping at point of care are projected to capture the bulk of future revenue upside.

By Data Source: Mobile Applications Gain Clinical Validation

Wearables retained 39.44% of the digital biomarker market revenue in 2025 due to wide consumer uptake and near-continuous data capture. The segment still benefits from iterative hardware upgrades such as cuffless blood pressure and noninvasive glucose sensing. Mobile Applications, forecast to rise at 20.2% CAGR, benefit from the 6.8 billion smartphone installed base and zero incremental hardware cost. Vocal biomarkers, valued highly in 2024, show how built-in microphones classify airway obstruction and neurological decline without specialist equipment.

Implantables remain niche yet offer adherence-free sensing for heart failure and epilepsy. Environmental sensors round out contextual markers, and emerging smart textiles leverage conductive fibers to monitor vitals during sleep. As ecosystem builders such as Samsung prepare the Galaxy Ring with noninvasive metabolic monitoring, multi-device orchestration will turn siloed datapoints into unified risk profiles.

By Therapeutic Area: Neurological Disorders Accelerate Innovation

Cardiovascular & Metabolic Disorders accounted for 39.98% of digital biomarkers market size in 2025 because glucose monitors, arrhythmia detectors, and blood-pressure patches are clinically entrenched. Neurological Disorders, advancing at a 20.33% CAGR, now lead innovation pipelines as motion-sensor gait metrics, touchscreen cognitive assessments, and speech analytics enable early Alzheimer’s and Parkinson’s detection. The FDA’s support for digital motor endpoints and the Parkinson’s DREAM Challenge, which crowdsourced 40 international teams, confirm the efficacy of algorithmic scoring in longitudinal studies.

Digital respiratory markers leverage chest-worn bands and phone microphones to assess cough frequency and nocturnal apnea. Musculoskeletal use cases harness inertial measurement units for rehab progress, while oncology explores fatigue and performance status via passive mobility tracking. Therapeutic expansion continues as AI models extract condition-specific features across comorbidities.

By Clinical Practice: Monitoring Applications Drive Adoption

Diagnostic Digital Biomarkers held 50.62% of the digital biomarkers market revenue in 2025 through point-in-time screening for arrhythmia, diabetic retinopathy, and mild cognitive impairment. Monitoring Digital Biomarkers are projected to post a 20.31% CAGR to 2031 as payers endorse longitudinal surveillance that flags deterioration ahead of acute events. Circadian-rhythm actigraphy, validated as a biomarker of biological aging, demonstrates how continuous patterns can forecast hospitalizations and guide lifestyle prescriptions.

Predictive & Prognostic tools layer machine-learning risk scores on streaming datasets to tailor therapy intensity and trial enrichment. The FDA’s Drug Development Tool qualification program signals that validated algorithms can de-risk pivotal studies, encouraging sponsors to incorporate monitoring signals as primary outcomes. Emerging applications such as medication-adherence tracking and behavioral-health triage expand digital biomarker reach beyond traditional vital signs.

By End User: Payers Embrace Value-Based Models

Pharmaceutical & Biotech Companies controlled 37.42% of the digital biomarkers market revenue in 2025, driven by trial efficiency and decentralized design. Biofourmis, for instance, secured platform deals with four top-20 drug makers to supply sensor-driven endpoints that compress timelines and reduce protocol deviations. Payers & Employers are on course for a 20.18% CAGR as value-based care demands evidence of preventive savings. DiMe and Elevance Health launched an independent seal that validates technical and clinical performance, giving actuaries confidence to reimburse new tools.

Healthcare Providers integrate dashboards into electronic medical records, using alerts to optimize staffing and remote titration programs. Academic centers and tech firms in the Others category pilot novel use cases such as digital stethoscopes and camera-based respiratory analysis, fertilizing the pipeline for future reimbursement.

Geography Analysis

North America generated 42.88% of digital biomarkers market size in 2025 thanks to FDA leadership, Medicare CPT codes, and widespread broadband. Large integrated delivery networks deploy remote programs that cut readmissions for chronic heart failure, incentivizing further investment. U.S.-based pharmaceutical sponsors dominate trial activity, meaning endpoints validated locally often propagate worldwide.

Asia-Pacific is projected to grow at a 20.41% CAGR through 2031, fueled by Chinese government mandates to embed AI monitoring into primary care and Japan’s super-aged society seeking fall prevention and arrhythmia screening. Local manufacturing of sensors lowers device price points, while public-private partnerships roll out regional telehealth hubs. India and Southeast Asia adopt smartphone-based respiratory and metabolic screening to bridge specialist shortages, enabling leapfrog diffusion.

Europe balances strict privacy law with supportive reimbursement. Germany reimburses prescribed apps up to EUR 700 (USD 735) per year, proving commercial pathways, while the wider European Health Data Space aims to harmonize cross-border data use. EMA qualification of digital stride metrics in neuromuscular trials underlines regulatory openness, yet differing country-level evidence standards still slow uniform coverage, keeping platform vendors focused on targeted pilot contracts.

Competitive Landscape

The digital biomarkers market houses a mix of consumer tech giants, med-tech incumbents, and software pure-plays. Apple leverages an installed base of 200 million Watch users, combining hardware control with a regulated ECG algorithm. Samsung expands the Galaxy ecosystem with cuffless blood pressure and glucose sensing, while Google-backed Verily pivots to enterprise research services. Medical device leaders respond by partnering or acquiring analytics firms; Dexcom’s tie-up with Oura extends glucose insights into holistic wellness dashboards.

Start-ups specialize in niche markers such as vocal cord resonance for COPD and camera-based tremor scoring for Parkinson’s. Competitive advantage centers on curated datasets, algorithm explainability, and evidence packages that withstand regulator scrutiny. Vendors with multi-condition portfolios and interoperable APIs align best with provider workflows, driving a gradual tilt toward platform concentration. Intellectual-property fencing around data-transformation pipelines, rather than raw sensor patents, emerges as the chief moat.

Separately, pharmaceutical sponsors increasingly bundle digital endpoints with drug label expansion strategies. Biofourmis, ActiGraph, and Koneksa secure repeat enterprise contracts by offering audit-ready data streams, turnkey dashboards, and services that manage patient tech support. Their domain expertise positions them as preferred integrators when sponsors negotiate adaptive-trial designs with regulators.

Digital Biomarkers Industry Leaders

-

ActiGraph

-

Fitbit Health Solutions

-

Biogen

-

F. Hoffmann-La Roche Ltd.

-

Huma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Biolinq raised USD 100 million to scale its microneedle biowearable for metabolic monitoring.

- April 2025: Click Therapeutics received FDA authorization for CT-132, the first prescription digital therapeutic aimed at preventing episodic migraine.

- December 2024: ŌURA secured USD 200 million in growth funding following its Dexcom integration that merges glucose and activity data.

- May 2024: Bayer and Huma Therapeutics launched digital heart-health screening for 1 million Saudis under Vision 2030 plans.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the digital biomarkers market as all software platforms, wearables, implantables, or ingestible devices that continuously capture, transmit, and translate objective physiological or behavioral signals into clinically meaningful indicators used across research, diagnosis, monitoring, and therapeutic decision-making. According to Mordor Intelligence, the valuation year 2025 stands at USD 4.36 billion.

Scope Exclusions: We exclude stand-alone laboratory or imaging biomarkers that are not generated or transmitted through a digital interface.

Segmentation Overview

-

By Component

- Data Collection Tools

- Data Integration & Analytics Platforms

-

By Data Source

- Wearables

- Implantables

- Mobile Applications

- Sensors

- Others

-

By Therapeutic Area

- Cardiovascular & Metabolic Disorders

- Neurological Disorders

- Respiratory Disorders

- Musculoskeletal Disorders

- Others

-

By Clinical Practice

- Monitoring Digital Biomarkers

- Diagnostic Digital Biomarkers

- Predictive & Prognostic Digital Biomarkers

- Others

-

By End User

- Pharmaceutical & Biotech Companies

- Healthcare Providers

- Payers & Employers

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We speak with clinicians running decentralized trials, product managers at device makers, payer medical-policy staff, and health-app data scientists across North America, Europe, and Asia-Pacific. Their insights help us validate adoption curves, average selling prices, and regulatory timelines that secondary sources leave unclear.

Desk Research

We extract baseline inputs from publicly accessible tier-1 sources such as the US FDA Digital Health Center of Excellence, NIH PubMed trials that validate wearable endpoints, Eurostat trade codes for sensors, the Digital Medicine Society's device registry, and World Bank telecom penetration data, supported by filings and investor decks that detail unit sales or SaaS users. Our team also taps D&B Hoovers and Dow Jones Factiva to size company revenue streams that are not openly reported.

These references build the factual spine of the model; however, many more articles, databases, and association releases are reviewed, so the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

We begin with a top-down reconstruction that pairs global wearable installed base figures, smartphone health-app penetration, remote monitoring reimbursement uptake, prevalence of target chronic diseases, and average device replacement cycles. Selective bottom-up supplier roll-ups (sampled ASP × unit shipments) pressure-test totals and close data gaps. Forecasts employ multivariate regression blended with exponential smoothing, where independent variables include yearly venture-funding inflows, FDA 510(k) clearances, and cloud-storage cost trends that influence pricing. When partial country data is missing, we proxy from adjacent markets with similar device adoption levels, then adjust with GDP-per-capita ratios.

Data Validation & Update Cycle

Our analysts run anomaly checks against independent indicators, revisit outliers with respondents, and route each model through a multi-step internal review before sign-off. Reports refresh annually, and we trigger interim revisions if material events, such as landmark approvals or reimbursement code changes, shift demand.

Why Mordor's Digital Biomarkers Baseline Stands Reliable

Published estimates often diverge; readers see numbers that vary by billions because firms choose different device sets, pricing ladders, or update cadences. We want buyers to understand these sources of spread before making decisions.

Key gap drivers include whether platforms that only aggregate data are counted, the extent to which clinical-trial licensing revenue is blended with commercial sales, currency conversion timing, and how aggressively declining sensor ASPs are projected.

Our model fixes definitions upfront, refreshes every twelve months, and balances growth optimism with verified usage data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.36 B (2025) | Mordor Intelligence | - |

| USD 3.80 B (2024) | Global Consultancy A | Counts wearables only; omits software analytics revenue |

| USD 5.04 B (2025) | Industry Data Provider B | Includes broader digital health platforms beyond biomarkers |

| USD 5.15 B (2025) | Regional Advisory C | Uses list prices without region-specific ASP adjustment |

These comparisons show that our disciplined scope selection, mixed-method modeling, and timely refresh provide a balanced, transparent baseline that decision-makers can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the digital biomarkers market?

The digital biomarkers market size stood at USD 5.22 billion in 2026 and is forecast to reach USD 12.77 billion by 2031 at a 19.62% CAGR.

Which component segment is growing fastest?

Data Integration & Analytics Platforms are the fastest-growing component, expanding at a 20.12% CAGR because advanced algorithms turn raw sensor readings into actionable insights.

Why are payers interested in digital biomarkers?

Payers support continuous monitoring programs that flag health risks early, lowering hospitalizations and enabling value-based reimbursement models that cut long-term costs.

Which region will register the highest growth through 2031?

Asia-Pacific is projected to post the highest regional CAGR at 20.41% due to government digitization initiatives, large aging populations, and cost-effective wearable manufacturing.

How are digital biomarkers used in clinical trials?

Sponsors deploy sensor-based endpoints to measure gait, heart rhythm, or cognition remotely, cutting study visits and reducing sample sizes by up to 70% while maintaining statistical power.

What are the main regulatory hurdles?

Fragmented international approval pathways and stringent data-privacy laws increase evidence requirements and cybersecurity costs, slowing global scale-up for digital biomarker platforms.

Page last updated on: