Cardiac Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.42 Billion |

| Market Size (2031) | USD 39.87 Billion |

| Growth Rate (2026 - 2031) | 13.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cardiac Biomarkers Market Analysis by Mordor Intelligence

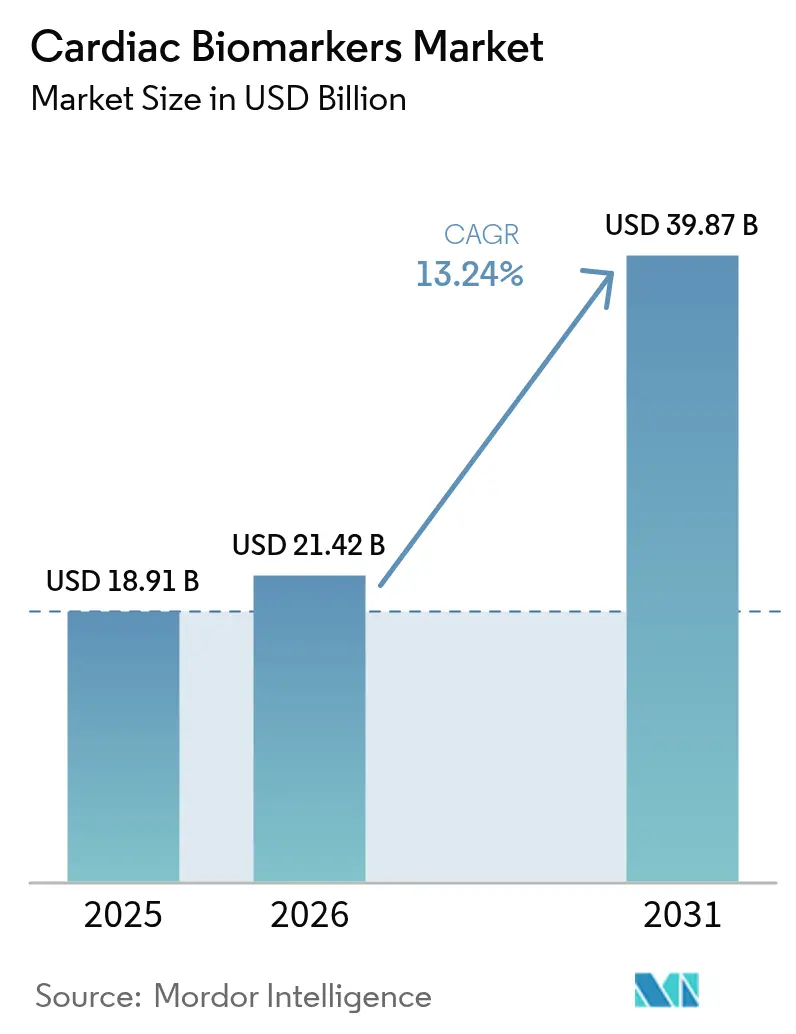

cardiac biomarkers market size in 2026 is estimated at USD 21.42 billion, growing from 2025 value of USD 18.91 billion with 2031 projections showing USD 39.87 billion, growing at 13.24% CAGR over 2026-2031. Adoption of high-sensitivity assays, rapid point-of-care platforms and AI-driven decision support systems is accelerating test volumes as health systems pursue earlier rule-out strategies for acute coronary events. Expansion of public- and private-sector proteomics funding is widening the discovery pipeline, while the FDA’s first point-of-care high-sensitivity cardiac troponin approval in 2024 has shortened emergency department rule-out times from one hour to 17 minutes. Demand is further reinforced by the 127.9 million American adults living with cardiovascular disease, equivalent to 48.6% of the population. Meanwhile, Asia-Pacific regulatory modernization is creating attractive reimbursement-linked growth prospects for novel biomarkers and decentralized testing platforms.

Key Report Takeaways

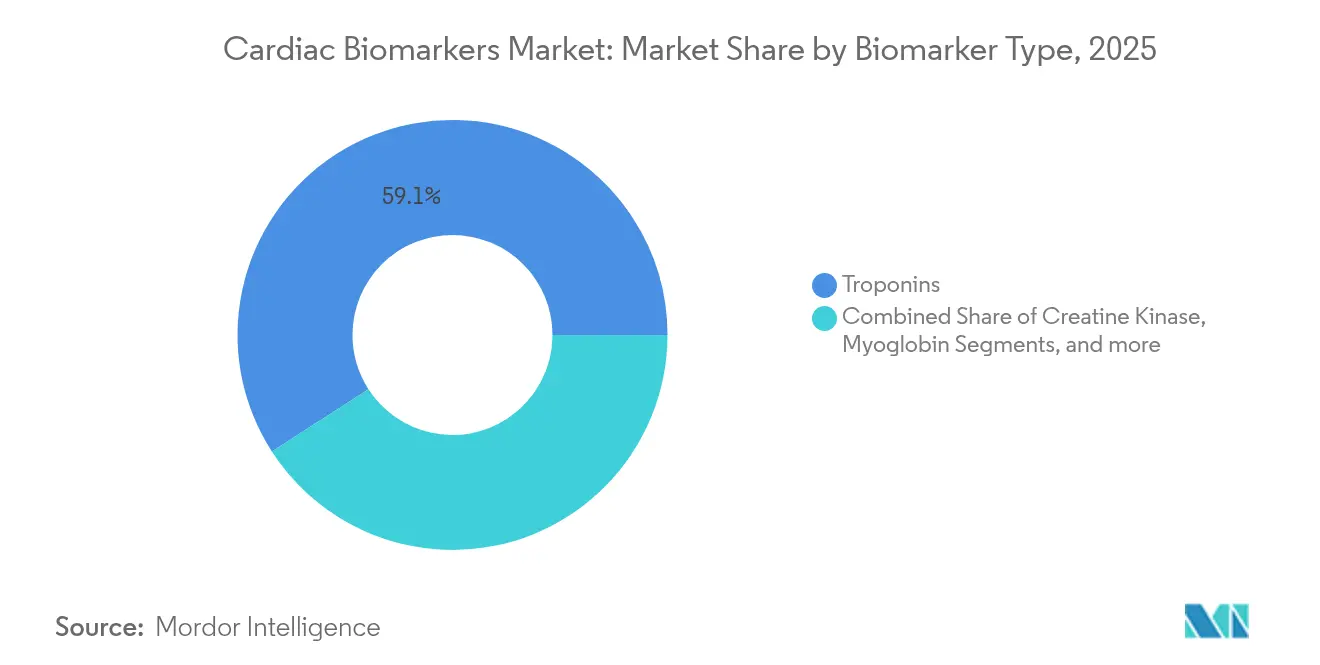

- By biomarker type, troponins held 59.12% of the cardiac biomarkers market share in 2025, while ischemia-modified albumin is projected to expand at a 13.68% CAGR to 2031.

- By application, myocardial infarction led with 39.85% revenue share in 2025; acute coronary syndrome is forecast to grow at a 13.91% CAGR through 2031.

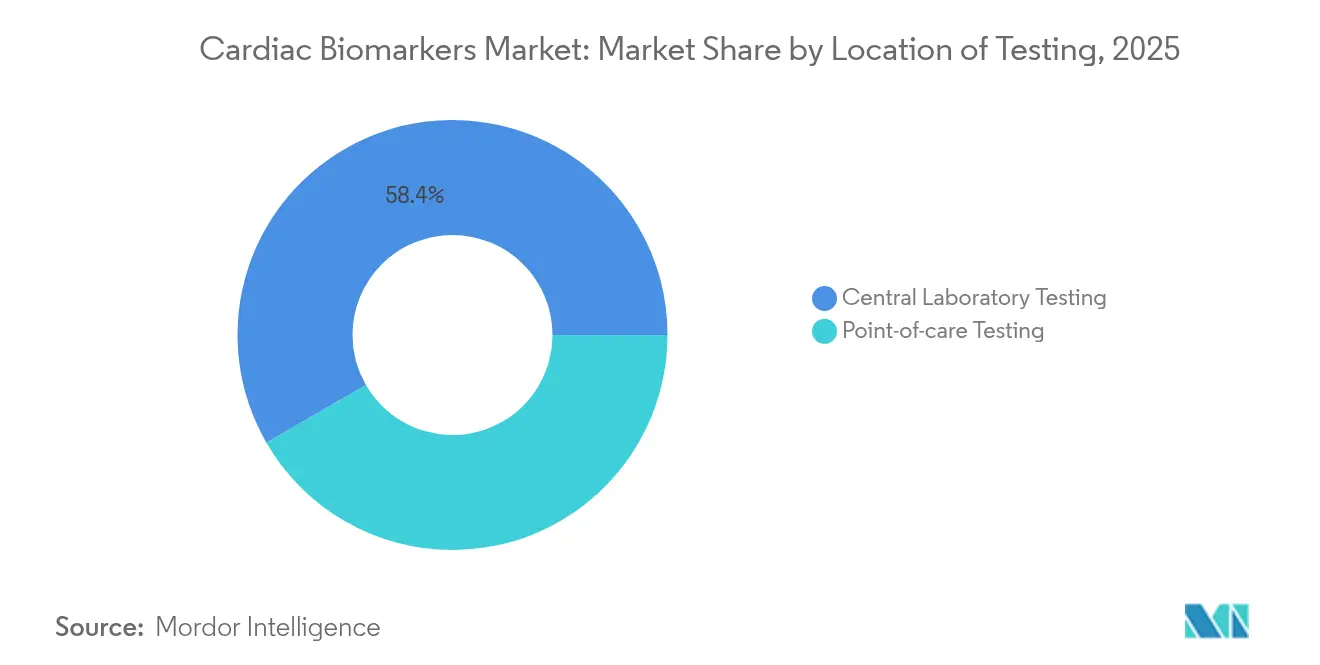

- By location of testing, central laboratories accounted for 58.35% share of the cardiac biomarkers market size in 2025, while point-of-care platforms are advancing at a 14.02% CAGR to 2031.

- By end user, hospitals commanded 53.15% share in 2025; home healthcare settings record the fastest CAGR at 14.09% through 2031.

- By region, North America captured 41.78% of the cardiac biomarkers market share in 2025, yet Asia-Pacific will register the highest CAGR at 14.11% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of cardiovascular diseases | +3.2% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Technological advances in high-sensitivity assays | +2.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Growing public- & private-sector R&D funding | +2.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Expansion of multiplex panels for early rule-out protocols | +1.9% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-enabled predictive analytics integrating troponins with EHRs | +1.7% | North America & Europe, select Asia-Pacific | Medium term (2-4 years) |

| Adoption of at-home finger-stick cardiac biomarker kits | +1.4% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing prevalence of cardiovascular diseases

Cardiovascular disorders remain the top global mortality driver, costing the United States USD 422.3 billion annually in direct medical expenses [1]Seth S. Martin, "2024 Heart Disease and Stroke Statistics: A Report of US and Global Data From the American Heart Association," American Heart Association, heart.org. Mandated ASCVD risk assessment coding under the CMS 2025 Physician Fee Schedule now requires evidence-based diagnostics that combine demographic variables with laboratory cardiac biomarkers, intensifying institutional uptake [2]Centers for Medicare & Medicaid Services, "Calendar Year (CY) 2025 Medicare Physician Fee Schedule Final Rule," cms.gov. As value-based care contracts expand, providers rely on biomarker-guided interventions to document measurable outcome gains and avoid readmission penalties.

Technological advances in high-sensitivity assays

FDA clearance of Siemens Healthineers’ Atellica IM high-sensitivity troponin I test enables prognostic risk stratification for up to one year after an index event [3]Siemens Healthineers AG, "For Patients at Risk, a Simple Blood Test Can Help Doctors Predict Likelihood of Future Heart Attack, Other Cardiac Events, and Death," siemens-healthineers.com. Laboratory-quality microfluidic cartridges now quantify troponin at 10-fold lower concentrations than legacy assays and deliver results in minutes, achieving 100% sensitivity in multi-center validation studies. Sex-specific reference ranges are closing historical diagnostic gaps among female patients, while integrated biosensors allow finger-stick whole-blood testing without plasma separation.

Growing public- & private-sector R&D funding

Thermo Fisher Scientific’s USD 3.1 billion acquisition of Olink boosts high-throughput proteomics capacity to interrogate 5,400 proteins across 600,000 UK Biobank samples—the world’s largest human proteome initiative. NIH grants are financing low-cost electrochemical sensors capable of saliva-based detection for USD 3.00 per unit, supporting rural screening programs. Private equity interest remains strong in start-ups delivering multiplex point-of-care analyzers that shorten emergency department throughput times.

Expansion of multiplex panels for early rule-out protocols

Implementation of 0/2-hour high-sensitivity troponin pathways has attained 91.1% sensitivity and 98.1% negative predictive value for 30-day cardiac events. Combining troponin with cardiac myosin-binding protein C in a single cartridge yields an AUC of 0.917, bridging diagnostic blind spots for transient ischemia. Use of HEART-CT algorithms reclassified 76.7% of moderate-risk patients to safe discharge, cutting average emergency department stay to 4.6 hours.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory frameworks | -2.1% | Global, most stringent in North America & Europe | Long term (≥ 4 years) |

| Reimbursement erosion from bundled-payment models | -1.8% | North America, expanding to Europe | Medium term (2-4 years) |

| Analytical variability of novel POC devices | -1.3% | Global, particularly in emerging markets | Short term (≤ 2 years) |

| Limited specificity generating false-positive results | -1.1% | Global, higher impact in low-resource settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory frameworks

Europe’s In-Vitro Diagnostic Regulation now obliges extensive clinical evidence, stretching CE-mark timelines. SpinChip Diagnostics expects to submit under IVDR by end-2025 with launch slated for 2026, illustrating prolonged pathways. In the United States, FDA draft rules for AI-enabled diagnostics require algorithmic transparency plus multi-ethnic validation cohorts, adding compliance costs and delaying commercial roll-out.

Reimbursement erosion from bundled-payment models

The CMS 2025 fee schedule reduces conversion factors by 2.83% while broadening ASCVD risk-assessment coverage, forcing providers to justify biomarker utilization on cost-per-episode grounds. Accountable Care Organizations risk margin compression if testing protocols do not translate into reductions in readmissions or length of stay. Private insurers mirror these bundled structures, prompting laboratories to negotiate value-based contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Biomarker Type: Troponins anchor adoption, novel markers accelerate

Troponins controlled 59.12% of the cardiac biomarkers market in 2025, validating decades of clinical trust in these gold-standard proteins. Segment revenues benefit from the shift to high-sensitivity formats that detect minute myocardial injury within two hours of symptom onset. Conversely, ischemia-modified albumin is expanding at a 13.68% CAGR, reflecting growing recognition that transient coronary vasospasm events demand markers able to capture reversible ischemia that troponin misses.

The cardiac biomarkers market size attributable to troponins reached USD 11.18 billion in 2025. Manufacturers are augmenting assay menus with microRNAs and inflammatory proteins, yet clinical uptake hinges on regulatory clearance and guideline endorsement. Creatine kinase is tapering as high-sensitivity troponins deliver superior specificity, while myoglobin remains a legacy option used primarily for ultra-early triage before troponin rises.

By Application: Acute coronary syndrome protocols shape growth

Applications in myocardial infarction generated 39.85% of segment revenue for the cardiac biomarkers market in 2025. Hospitals rely on troponin algorithms to meet door-to-needle targets, a metric directly tied to reimbursement bonuses. Acute coronary syndrome, however, is climbing at a 13.91% CAGR, driven by 0/2-hour rule-out pathways that safely discharge low-risk patients and decrease telemetry bed occupancy.

The cardiac biomarkers market size for acute coronary syndrome is estimated to be underpinned by payer incentives that reward avoidance of unnecessary admissions. Chronic care settings are also expanding use cases; BNP-based management of heart failure reduces readmission penalties under the Medicare Hospital Readmissions Reduction Program, while ASCVD coding requirements integrate biomarker panels into annual risk reviews.

By Location of Testing: Point-of-care transformation intensifies

Central laboratories preserved a 58.35% revenue share in 2025, leveraging high-throughput analyzers and consolidated procurement contracts. Yet point-of-care systems are advancing at a 14.02% CAGR thanks to FDA-cleared platforms delivering high-sensitivity troponin I results in 17 minutes. Emergency physicians value near-patient testing that avoids transport lag, improving adherence to 60-minute turnaround benchmarks.

Point-of-care expansion is further accelerated by acquisition activity; bioMérieux’s EUR 138 million SpinChip purchase adds a 10-minute whole-blood immunoassay cartridge that rivals central-lab precision. Cost of ownership is narrowing as microfluidic manufacturing scales, enabling community hospitals and ambulatory surgery centers to deploy decentralized analyzers without extensive infrastructure.

By End User: Home healthcare emerges as a catalyst

Hospitals commanded 53.15% of demand in 2025, yet home healthcare settings are projected to deliver a 14.09% CAGR through 2031. Portable saliva-based sensors now quantify galectin-3 and S100A7 within 15 minutes at USD 3.00 unit cost, supporting at-home monitoring for chronic cardiac patients. Integration of Bluetooth-enabled cartridges into telehealth apps allows clinicians to trend serial values remotely.

The cardiac biomarkers market size allocated to home use could surpass USD 5.78 billion by 2031, propelled by payer support for remote physiologic monitoring codes and patient preference for in-home sampling. Diagnostic laboratories retain relevance for complex multiplex panels, while ambulatory clinics leverage handheld analyzers for perioperative risk stratification.

Geography Analysis

North America captured 41.78% of the cardiac biomarkers market in 2025, supported by well-funded payers, mature laboratory networks and guideline alignment that validates high-sensitivity assays. CMS coding updates further entrench biomarker requirements within preventative cardiology workflows. The region’s testing volumes will keep pace with population aging, yet pricing pressure from bundled payment models is likely to temper revenue expansion.

Europe follows as the second-largest region, with public healthcare systems anchoring troponin adoption for rapid rule-out protocols. Implementation of the In-Vitro Diagnostic Regulation increases compliance costs but also elevates trust in clinically validated assays, reinforcing adoption across Germany, France and the United Kingdom. Market momentum will hinge on balancing reimbursement ceilings with cost-effective multiplex panels that reduce downstream imaging utilization.

Asia-Pacific is the fastest-growing territory, poised to post a 14.11% CAGR. Japan’s USD 40 billion medical device sector is already embracing high-sensitivity troponin and BNP testing, aided by PMDA expedited review channels. China’s National Medical Products Administration has approved 61 innovative diagnostics in 2023, signaling a friendlier path for foreign and domestic biomarker vendors. Rising cardiovascular prevalence, coupled with government insurance expansion, drives demand for decentralized point-of-care solutions in secondary hospitals.

Middle East & Africa and South America represent emerging catch-up markets. Gulf Cooperation Council states are investing in tertiary cardiac centers equipped with high-throughput analyzers, while Brazil and Mexico roll out universal health coverage pilots that reimburse early myocardial infarction diagnostics. Suppliers able to deliver affordable, stable ambient-temperature reagents will gain share as freight and cold-chain constraints persist.

Regulatory Landscape

Cardiac biomarker assays are regulated as in-vitro diagnostics, with requirements increasingly centered on analytical validation, clinical performance evidence, and post-market traceability. In the United States, the FDA continues to shape expectations for biomarker assay validation through its biomarker-focused guidance framework and the phased approach to oversight of laboratory-developed tests finalized in 2024, which increases documentation and quality-system demands for hospital and reference laboratories that previously relied on more internal flexibility.

In Europe, the In-Vitro Diagnostic Regulation (IVDR) has moved the evidence standard toward a Performance Evaluation Report covering scientific validity, analytical performance, and clinical performance. Mid-2026 is an operational pressure point as the European Commission set 26 May 2026 as a deadline for Class C legacy device manufacturers to submit formal IVDR certification applications to a Notified Body under Regulation (EU) 2024/1860, while EUDAMED module requirements for MDR/IVDR-compliant devices also add registration and vigilance workload. Parallel policy activity, including the European Commission proposal COM(2025) 1023, signals an active legislative agenda, but enforcement continues to be anchored in IVDR requirements and Notified Body capacity constraints.

Competitive Landscape

The cardiac biomarkers market remains moderately fragmented, with leading companies carving out niches through acquisitions, assay innovation and digital integration. bioMérieux’s SpinChip purchase consolidates near-patient testing assets and accelerates time-to-result to 10 minutes for whole-blood immunoassays, directly challenging Abbott’s i-STAT and Roche’s cobas h 232 portfolios. Siemens Healthineers differentiates via prognostic claims on its high-sensitivity troponin I, extending utility beyond diagnosis into one-year risk stratification.

Thermo Fisher Scientific’s Olink acquisition positions it at the discovery frontier, leveraging proximity extension assays to uncover novel proteins with potential cardiac relevance. Beckman Coulter and Ortho Clinical Diagnostics focus on menu breadth inside core labs, bundling cardiac markers with infectious disease panels for automated analyzers to protect reagent annuities. Start-ups such as RCE Technologies pursue continuous, wearable transdermal monitoring that could redefine chronic care paradigms once regulatory hurdles are cleared.

Competitive differentiation increasingly rests on embedded analytics. Vendors are integrating cloud dashboards that plot serial troponin curves against machine-learning risk scores, delivering actionable flags to physicians within electronic health records. Interoperability and cybersecurity are becoming procurement gate-checks as health systems align with zero-trust frameworks. Companies offering subscription-based decision-support modules may capture annuity revenue even as reagent prices face downward pressure.

Cardiac Biomarkers Industry Leaders

-

Abbott Laboratories

-

Becton, Dickinson and Company

-

BioMérieux

-

Bio-Rad Laboratories, Inc.

-

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory clearances and menu expansions in 2026 point to whitespace for cardiac biomarker offerings beyond troponins, particularly inflammatory and heart-failure adjuncts that fit routine chemistry and immunoassay workflows. In early 2026, multiple FDA 510(k) clearances supported this broadening: Axis-Shield Diagnostics cleared an NT-proBNP assay for Abbott Alinity i (February 2026), Beckman Coulter cleared Access BNP II (March 2026), and Roche cleared Tina-quant Cardiac high sensitivity CRP III (April 2026). These steps support opportunities for labs to standardize platforms while expanding panels used for acute triage and longitudinal risk profiling, reflecting payer and provider focus on measurable episode-level outcomes.

Decentralization also remains an opportunity where performance-grade assays and workflow design align, especially for emergency departments and pre-hospital triage pathways. Developers are pushing handheld and multiplex concepts that compress turnaround time and reduce reliance on central-lab logistics, including Proxim Diagnostics finalizing the design of a handheld point-of-care immunoassay instrument in June 2026 and initiating its regulatory path for troponin I. In parallel, published work on deep learning-enhanced multiplex vertical flow assays that quantify cTnI, CK-MB, and NT-proBNP in about 23 minutes highlights the direction toward cartridge-based multiplexing with AI-assisted readout, creating product-design and partnership opportunities for incumbents with assay IP as well as for microfluidics, connectivity, and usability-focused startups.

Recent Industry Developments

- April 2026: Becton, Dickinson and Company (BD) launched the HemoSphere Stream Module to provide continuous, noninvasive blood pressure visibility using a finger cuff. While not a biomarker assay, the capability strengthens acute and perioperative hemodynamic monitoring workflows that often run alongside rapid cardiac testing and decision support. The launch also reinforces the shift toward integrated monitoring and analytics platforms that complement near-patient diagnostics in critical care environments.

- January 2026: Abbott announced its Assert-IQ insertable cardiac monitor system, combining cardiac monitoring technology with cloud-based AI algorithms to detect and classify atrial fibrillation in near-real time. This development supports broader integration of AI-enabled decision support in cardiac care pathways, where serial biomarker testing and rhythm monitoring together inform triage and escalation. The product positions Abbott to connect diagnostics, monitoring, and data services within hospital and ambulatory care networks.

- January 2025: Abbott received FDA clearance for its i-STAT high-sensitivity troponin I cartridge, enabling lab-quality troponin results at the bedside. The clearance supports faster rule-out and rule-in workflows for suspected acute coronary syndromes in emergency and urgent care settings. It also increases competitive pressure on other point-of-care platforms to match high-sensitivity performance while maintaining operational simplicity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from in-vitro cardiac biomarker testing used to help detect, rule out, or monitor heart-related conditions in clinical settings, including both lab-based testing and point-of-care use. The sizing is captured in value terms (USD) across major regions.

Scope exclusions: We exclude research-use-only assays, non-IVD diagnostic modalities like imaging, veterinary testing, and exploratory multi-omics panels that are not routinely used for cardiac care decisions.

Segmentation Overview

-

By Biomarker Type

- Troponins

- Creatine Kinase

- Myoglobin

- Ischemia-Modified Albumin

- Other Biomarker Type

-

By Application

- Acute Coronary Syndrome

- Myocardial Infarction

- Congestive Heart Failure

- Atherosclerosis

- Other Applications

-

By Location of Testing

- Point-of-care Testing

- Central Laboratory Testing

-

By End-user

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgery Centers & Clinics

- Home Healthcare Settings

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public health and diagnostics signals so the model could be anchored to real testing demand and how care is delivered. We referenced sources such as the World Health Organization for cardiovascular burden context, the US CDC for disease and healthcare utilization indicators, and OECD health statistics for system-level testing capacity trends by country.

To ground pricing and adoption assumptions, we also checked information from the US FDA (clearances and key assay category changes), clinical guideline and evidence sources such as the American Heart Association and peer-reviewed cardiology journals, and cross-verified with company filings and investor presentations for product mix and geographic exposure. Where public data did not show consistent commercial splits, we used paid subscriptions focused on company financials and intelligence, news and financials, and patent databases to support fact checks and timeline validation. These examples are not exhaustive, and other public and paid sources were also used during the study to collect data, validate assumptions, and clarify remaining questions.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk research cannot fully answer, including typical test mix by setting, the shift toward high-sensitivity assays, and how pricing moves through reimbursement and procurement cycles. We spoke with a mix of kit and reagent suppliers, lab decision-makers, hospital stakeholders, and channel participants across major regions so assumptions on volumes, utilization, and adoption timing could be adjusted before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 51% |

| Mid tier: 44% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 20% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where disease burden and care pathways help reconstruct the addressable testing pool, and then market value is estimated by applying realistic test utilization and price bands. For cardiac biomarkers, the model was shaped around indicators such as acute chest pain and suspected myocardial infarction workups, emergency department and inpatient diagnostic throughput, installed base expansion for point-of-care platforms, test menu mix shifts toward high-sensitivity troponin, and average selling price movement by setting and region.

After the top-down totals were formed, they were corroborated with selective bottom-up approximations such as sample supplier revenue roll-ups, channel checks for reagent and kit consumption patterns, and simple ASP times volume sanity checks in a few high-visibility countries. When company disclosures or country signals were incomplete, gaps were handled by using peer-country proxies and then rechecked with expert feedback so the implied per-facility usage remained realistic.

Forecasting leaned on scenario analysis supported by year-by-year input views from interviews, because adoption pace is influenced by clinical guideline updates, regulatory timing, and procurement cycles that do not move in a straight line. The final forecast curve was adjusted to reflect expected ramp effects in newer assay types, and slower normalization where health systems face capacity or reimbursement constraints.

Data Validation & Update Cycle

Validation was done through multiple checks so the final values did not rely on a single assumption. Model outputs were compared against independent signals such as cardiovascular admissions trends, diagnostic testing workflow shifts, and supplier commentary, and then anomalies were reviewed until implied volume and pricing relationships were consistent.

Before sign-off, the work goes through multi-step analyst review, and re-contact is triggered when a major variance appears across regions, settings, or biomarker mix. Reports are refreshed annually, with interim updates when material events occur, and a final fresh pass is completed before delivery so clients receive the latest updated view.

Mordor Intelligence's Cardiac Biomarkers Market Size Compared Against Other Published Estimates

It is common to see different market sizes published for cardiac biomarkers, even when the topic label looks the same, because the counted products and timing assumptions are not always aligned. Differences also show up when one estimate is tied to clinical testing activity and another is closer to broader diagnostics revenue pooling.

Some sources blend adjacent categories like overall cardiac diagnostics, cardiac point-of-care devices, or lab equipment value into the same total, and that can inflate the number quickly. In Mordor Intelligence, the count is limited to in-vitro cardiac biomarker assay revenues in clinical use (including lab and point-of-care testing), with research-use assays, imaging, and non-routine exploratory panels kept out, and currency timing and adoption pacing checked through interviews before the total is finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.42 B (2026) | |

| Regional Consultancy A | USD 20.80 B (2024) | Uses an earlier base year and a different adoption timing curve, which can understate the uplift from high-sensitivity troponin expansion and point-of-care menu growth in the later years. |

| Global Consultancy B | USD 23.02 B (2026) | Higher 2026 value is consistent with broader product pooling or faster assumed ASP progression, and the split between lab and point-of-care settings is not always clearly separated in the published view. |

The spread across sources mostly comes from what is counted in the total and how quickly volumes and pricing are allowed to move by setting and region. By tying the value build-up to clinical testing signals and then stress-testing it with interview feedback, the estimate stays repeatable and easier to audit year to year.

Key Questions Answered in the Report

What is the current size of the cardiac biomarkers market?

The cardiac biomarkers market size stands at USD 21.42 billion in 2026 and is projected to reach USD 39.87 billion by 2031.

Which biomarker segment dominates the cardiac biomarkers market?

Troponins dominate, accounting for 59.12% share of 2025 revenues, thanks to guideline endorsement for myocardial infarction diagnosis.

How fast is the point-of-care segment growing?

Point-of-care cardiac biomarker testing is expanding at a 14.02% CAGR through 2031, driven by 17-minute high-sensitivity troponin assays.

Why is Asia-Pacific the fastest-growing region?

Regulatory modernization in Japan and China, combined with rising cardiovascular incidence, is propelling a 14.11% regional CAGR.

What impact will bundled payments have on test utilization?

Bundled payment models reduce per-test reimbursement, compelling providers to prove that biomarker-guided pathways cut readmissions and total episode costs.

Which recent acquisition reshaped the competitive landscape?

BioMérieux’s EUR 138 million takeover of SpinChip Diagnostics in 2025 strengthened its near-patient testing portfolio with a 10-minute immunoassay platform.

Page last updated on: