Genomic Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.22 Billion |

| Market Size (2031) | USD 9.82 Billion |

| Growth Rate (2026 - 2031) | 9.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Genomic Biomarkers Market Analysis by Mordor Intelligence

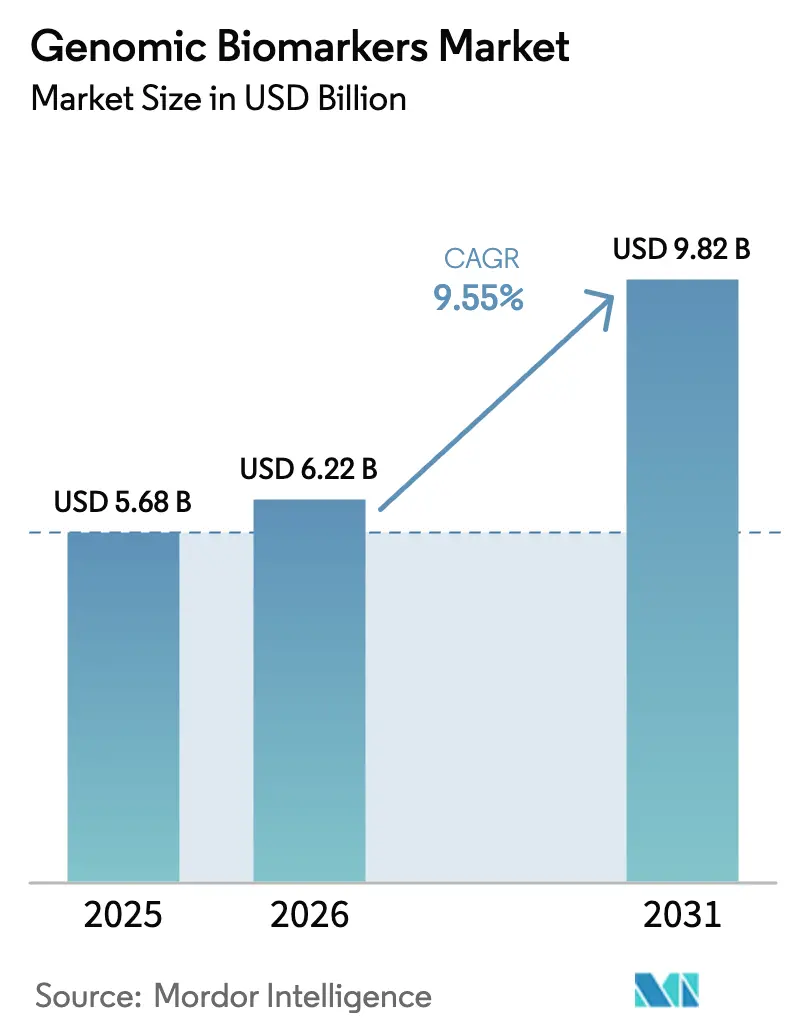

The Genomic Biomarkers Market size is projected to be USD 5.68 billion in 2025, USD 6.22 billion in 2026, and reach USD 9.82 billion by 2031, growing at a CAGR of 9.55% from 2026 to 2031.

Sustained expansion reflects a pivot from symptom-driven testing to proactive risk stratification as sequencing costs drop below USD 200 per whole genome, cloud-based federated learning unlocks rare-disease insights, and Fortune 500 employers add genetic benefits to self-funded plans. Oncology still anchors revenue, yet cardiovascular panels are advancing fastest as polygenic risk scores become routine in primary care. Diagnostic laboratories dominate today, but pharmaceutical sponsors are adopting genomic endpoints in adaptive Phase II trials, tightening links between biomarker discovery and drug development. NGS remains the workhorse technology; however, PCR assays are resurging in point-of-care pharmacogenomics, while Asia-Pacific national genome programs accelerate demand beyond traditional strongholds.

Key Report Takeaways

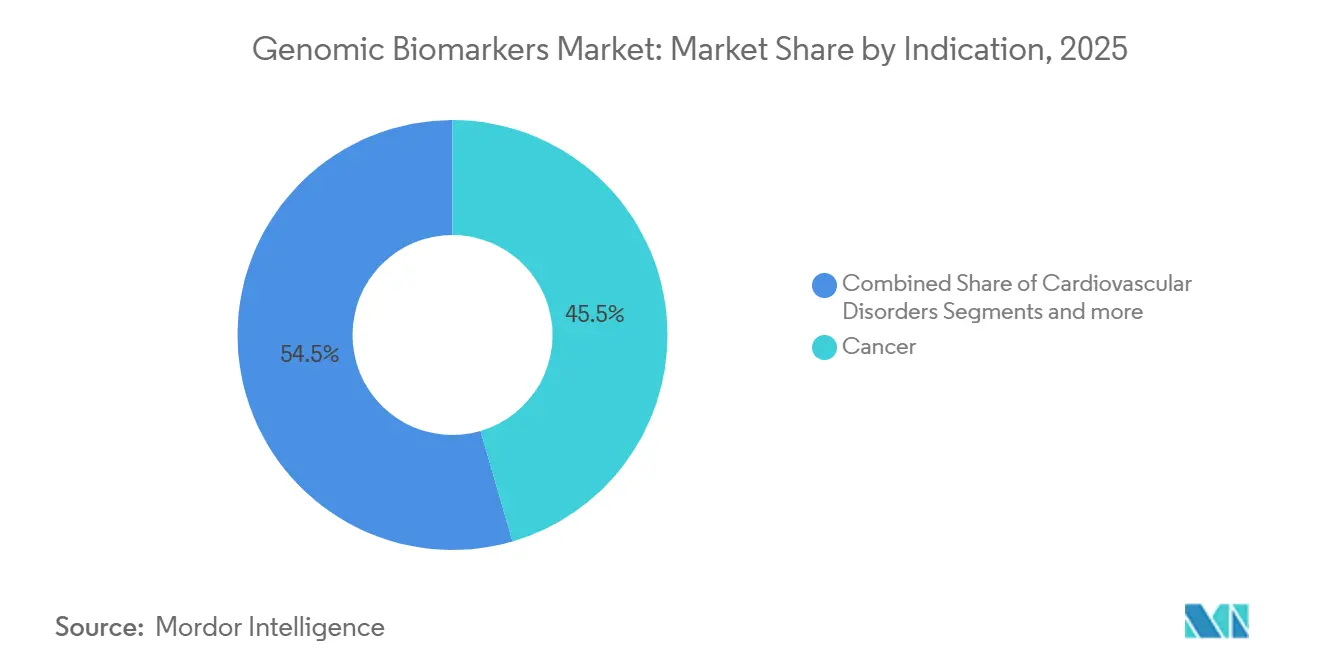

- By indication, oncology led with 45.55% revenue share in 2025, while cardiovascular genomic panels are projected to expand at a 13.85% CAGR through 2031.

- By end user, diagnostic laboratories held 38.53% of 2025 revenue, whereas pharmaceutical and biotechnology companies are on track for a 12.75% CAGR to 2031.

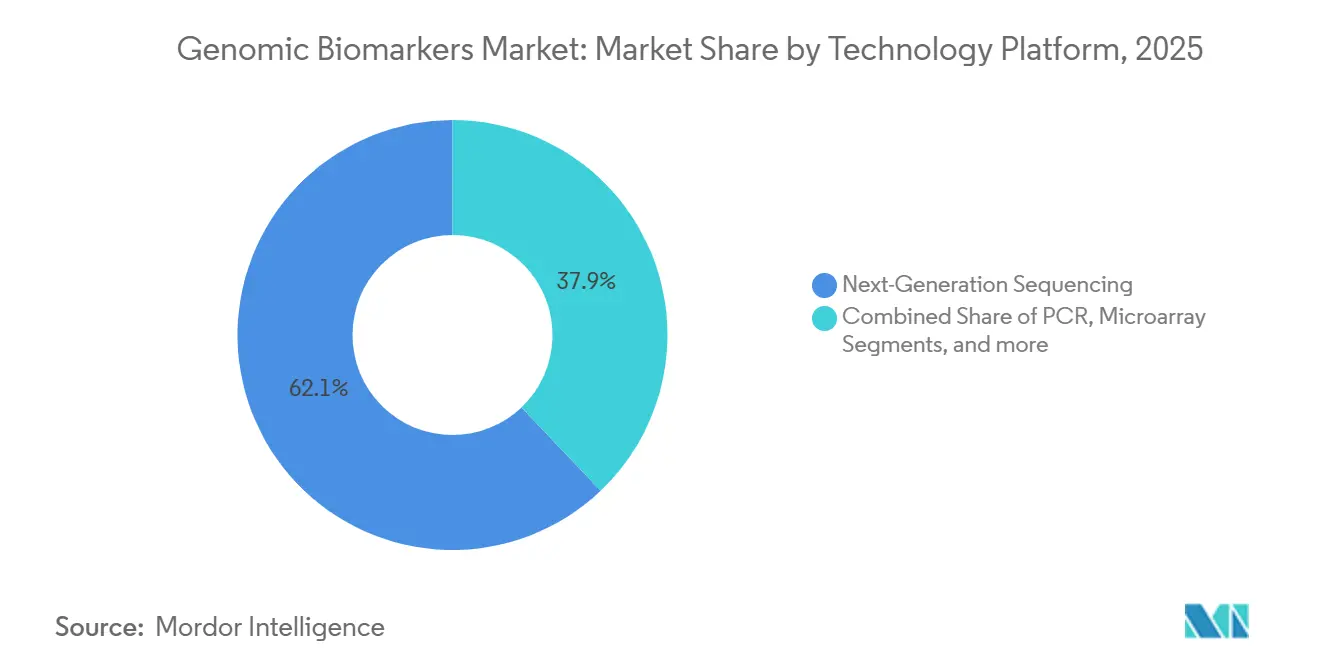

- By technology, NGS platforms captured 62.15% of 2025 revenue, and PCR-based assays are forecast to grow at an 11.82% CAGR.

- By biomarker type, predictive biomarkers accounted for 54.52% of 2025 revenue, while prognostic biomarkers are advancing at an 11.12% CAGR.

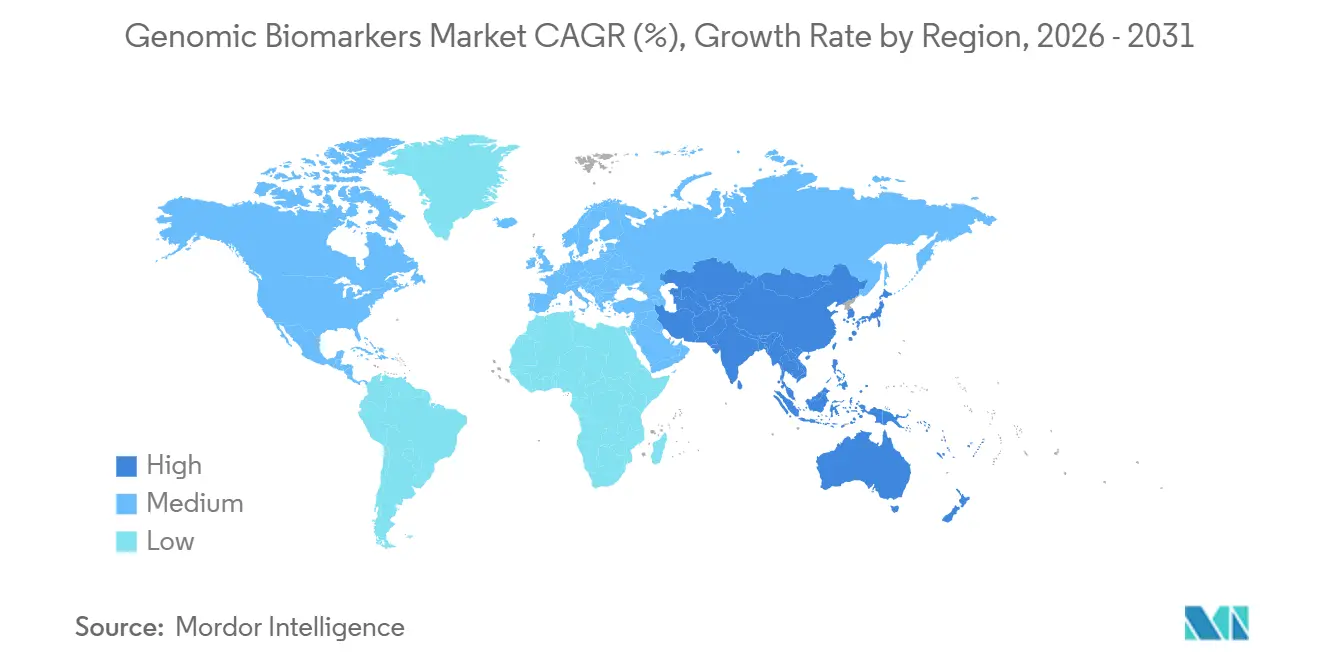

- By geography, North America commanded 38.55% genomic biomarkers market share in 2025, and Asia-Pacific is poised for an 11.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Genomic Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & lifestyle diseases | +1.8% | Global, with acute burden in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Breakthroughs in NGS, multi-omics & AI bioinformatics | +2.1% | Global, led by North America and Europe; rapid adoption in China, South Korea | Short term (≤2 years) |

| Mainstreaming of precision-medicine reimbursement models | +1.5% | North America, Western Europe; pilot programs in Australia, Japan | Medium term (2-4 years) |

| National population genomic-screening programmes | +1.3% | UK, US, China, India, Japan, Saudi Arabia | Long term (≥4 years) |

| Employer-sponsored genetic-benefit plans in self-insured firms | +0.9% | North America, with early adoption in Singapore, UAE | Short term (≤2 years) |

| Federated cloud learning accelerating rare-disease biomarker discovery | +1.0% | Global, with infrastructure concentrated in North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Lifestyle Diseases

Cancer, cardiovascular disorders, and metabolic syndromes collectively drive demand for earlier detection and individualized treatment planning. Noncommunicable diseases caused 74% of global deaths in 2024, with cancer responsible for nearly 10 million fatalities[1]World Health Organization, “Noncommunicable Diseases Fact Sheet,” WHO, WHO.INT. The American Cancer Society projects more than 2 million new U.S. cancer diagnoses in 2026, reinforcing sustained need for tumor profiling and liquid biopsy monitoring. Polygenic risk scores now flag asymptomatic adults at elevated risk of coronary artery disease decades before onset, enabling preventive statin therapy and lifestyle modification. Widening use of such tools extends the genomic biomarkers market beyond specialty oncology into primary care and population health. As screening broadens, recurring surveillance tests replace one-off diagnostics, strengthening long-term revenue visibility for service providers.

Breakthroughs in NGS, Multi-Omics and AI Bioinformatics

Sequencing throughput has doubled every 18 months since 2020, and Illumina’s NovaSeq X Plus now delivers 16 Tb per run at sub-USD 200 whole genome cost[2]Illumina Marketing Team, “NovaSeq X Plus Sequencing System,” Illumina, ILLUMINA.COM . Oxford Nanopore adaptive sampling reduces turnaround to under 12 hours in acute settings. Deep learning pipelines trained on diverse cohorts achieve 94% sensitivity and 98% specificity for pathogenic variant calls, 11 percentage points above legacy software. In 2025, the FDA cleared the first multi-omic assay that improved progression-free survival by 23% versus PD-L1 alone, signaling regulatory support for integrative biomarkers. Collectively, these advances compress analysis time, boost accuracy, and unlock clinically actionable signals that expand the genomic biomarkers market.

Mainstreaming of Precision-Medicine Reimbursement Models

CMS removed prior authorization for large comprehensive genomic profiling panels in 2024. Commercial payers such as UnitedHealthcare follow with outcome-based contracts that reimburse liquid biopsy tests only when results alter therapy choices. The UK NHS cut adverse drug reactions by 31% after embedding pharmacogenomic testing for common drugs into routine prescribing. Japan became the first nation to reimburse polygenic risk scores for cardiovascular prevention in asymptomatic adults in 2025. These policies shorten payback periods for laboratories and drive test-ordering behavior in mainstream clinical settings.

National Population Genomic-Screening Programs

The UK Our Future Health study enrolled its two-millionth participant in 2025, creating the world’s largest prospective genomic cohort. The U.S. All of Us program has produced 500,000 whole genomes, 80% from historically underrepresented groups. China’s National Population Health Science Data Center integrated 1.2 million genomes with EHRs, discovering novel biomarkers for hepatocellular and nasopharyngeal cancers. India’s Genome India cataloged 55 million variants, 22% novel, underscoring discovery potential in diverse populations. Large-scale screening expands reference databases, improves algorithm performance in non-European ancestries, and fuels demand for confirmatory clinical testing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High test cost & uncertain third-party reimbursement | -1.2% | Global, acute in emerging markets and US self-pay segment | Medium term (2-4 years) |

| Stringent & fragmented regulatory approval pathways | -0.8% | Europe (IVDR), Asia-Pacific (country-specific), Latin America | Long term (≥4 years) |

| Algorithmic bias in polygenic-risk scores for non-European populations | -0.6% | Asia-Pacific, Middle East and Africa, South America, with spillover to diverse US populations | Medium term (2-4 years) |

| Scarcity of validated digital-plus-genomic composite biomarkers | -0.4% | Global, with early impact in North America and Western Europe preventive care programs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Test Cost and Uncertain Third-Party Reimbursement

Comprehensive genomic profiling remains priced between USD 3,000 and USD 5,800, limiting access for uninsured patients and for public systems in low- and middle-income countries. Grail’s USD 949 multi-cancer early detection test lacks Medicare coverage, confining sales to executive wellness packages that touch fewer than 2% of eligible U.S. adults. Private insurers deny roughly 18% of prior authorizations for serial liquid biopsy monitoring, pushing patients toward lengthy appeals or out-of-pocket payment. In emerging markets, absent reimbursement narrows adoption to major cancer centers, widening urban–rural inequities. Quarterly minimal residual disease tests can cost more than USD 20,000 over five years, a burden few payers will shoulder.

Stringent and Fragmented Regulatory Approval Pathways

Europe’s IVDR obliges third-party conformity assessments for many lab-developed tests, creating a review backlog exceeding 300 assays and delaying launches by up to three years. The FDA now requests prospective validation for AI tools that learn iteratively, prolonging clearance of adaptive algorithms. Japan requires separate approvals per indication, stretching timelines to twice those in the United States. China added local-population validity studies in 2025, adding USD 2–5 million to development cost. Such divergence raises compliance expense, slows global scale-up, and hinders timely patient access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Oncology Strength With Cardiovascular Upswing

Oncology generated 45.55% of 2025 revenue, underpinned by guideline-mandated genomic profiling that links EGFR, KRAS, and HER2 status to targeted therapy selection[3]National Comprehensive Cancer Network, “NCCN Guidelines for Comprehensive Genomic Profiling,” NCCN.ORG. Serial minimal residual disease liquid biopsies extend revenue per oncology patient over post-surgery surveillance windows. Cardiovascular applications, though starting from a smaller base, show the fastest momentum with a 13.85% CAGR as risk scores enter annual wellness visits.

Neurologic, renal, and autoimmune indications add diversification. Pharmacogenomic panels shorten the six-week trial-and-error cycle in depression management, while early genomic identification of polycystic kidney disease triggers ACE inhibitor therapy that delays renal decline. As these use cases mature, the genomic biomarkers market size for non-oncology diseases will outpace historical averages, although oncology should still anchor half of total demand through 2031.

By End User: Laboratory Scale Meets Pharma Acceleration

Diagnostic laboratories held 38.53% of 2025 revenue, leveraging CLIA and CAP credentials and economies of scale that lower per-test costs by 30%. Hospitals, particularly academic centers, run rapid-turnaround assays for acute leukemia, meeting sub-72-hour decision windows.

Pharma and biotech represent the fastest-growing channel at 12.75% CAGR as 68% of 2024 FDA oncology drug approvals required biomarker-stratified enrollment. CROs extend testing to home-based clinical trial models, and community practices integrate result feeds directly into EHRs for real-world evidence capture. These dynamics fortify volume growth across multiple care settings, further broadening the genomic biomarkers market.

By Technology Platform: NGS Dominance, PCR Revival

NGS contributed 62.15% of 2025 revenue, thanks to multiplexed, ultra-sensitive detection and an installed base exceeding 20,000 Illumina sequencers. Long-read platforms from PacBio and Oxford Nanopore add structural variant resolution, edging into clinical workflows.

PCR assays, however, are rebounding with an 11.82% CAGR as point-of-care instruments deliver pharmacogenomic results in under 90 minutes. Digital PCR detects mutant alleles at 0.01% frequency, surpassing NGS sensitivity for minimal residual disease. The genomic biomarkers market share for microarrays remains stable in large-scale genotyping due to sub-USD 30 per-sample pricing. Hybrid workflows that combine NGS discovery with PCR reflex testing are now permitted under 2025 FDA guidance, aligning turnaround time with clinical urgency.

By Biomarker Type: Predictive Leaders, Prognostic Gainers

Predictive biomarkers held 54.52% of 2025 revenue, supported by companion diagnostics that gate reimbursement for targeted therapies. EGFR mutation testing preserves 7.4-month progression-free survival advantage when matched with osimertinib.

Prognostic assays, growing at 11.12% CAGR, guide therapy intensity by quantifying residual disease or recurrence risk. Oncotype DX and MammaPrint together exceed 150,000 annual U.S. tests, now reimbursed by Medicare. Polygenic scores for atrial fibrillation quadruple risk stratification accuracy, guiding primary prevention with anticoagulants. Regulatory draft guidance converges predictive and prognostic definitions into a single “clinical-utility biomarker,” likely streamlining future submissions.

Geography Analysis

North America accounted for 38.55% of 2025 revenue, anchored by more than 3,500 CLIA-certified molecular labs and early consumer normalization of genomic data through the All of Us portal. Public reimbursement for large gene panels and prolific private investment sustain the region’s leadership. Canada’s provincial cancer programs now reimburse comprehensive profiling for most metastatic cases, boosting national volumes.

Europe remains a substantial contributor, with Germany’s EUR 500 million National Genome Strategy earmarking sequencing centers in all federal states. The NHS Genomic Medicine Service completes roughly 100,000 genomes annually, trimming rare-disease diagnostic time to under one year. Despite IVDR-related delays, France, Italy, and Spain continue to expand BRCA and hereditary cancer testing penetration.

Asia-Pacific is projected to post the fastest growth at 11.72% CAGR through 2031 as China’s Precision Medicine Initiative deploys 50 sequencing hubs and integrates pharmacogenomics into the national formulary. India targets 1 million genomes by 2030, while Japan reimburses polygenic scores in annual health checks for 5 million citizens by 2028. Australia and South Korea add further momentum with national genome frameworks and population sequencing initiatives. Emerging programs in the UAE, Saudi Arabia, South Africa, and Brazil grow from a smaller base yet signal widespread global adoption, collectively enlarging genomic biomarkers market size across developing regions.

Regulatory Landscape

Regulatory oversight for genomic biomarkers spans IVD requirements for kits and companion diagnostics (CDx), laboratory-developed testing controls, and biomarker use in drug development, with notable divergence between the United States and Europe. In the United States, the FDA has continued to formalize expectations for nucleic acid tests and biomarker evidence, including September 2024 classification of whole exome sequencing constituent devices into Class II (special controls) and a November 2024 final guidance on circulating tumor DNA (ctDNA) as a biomarker in early-stage solid tumor trials. The agency also signaled a shift toward fit-for-purpose validation and modern trial designs through an April 2026 guidance on bioanalytical method validation for biomarkers and a January 2026 draft guidance on Bayesian methodology in clinical trials.

In Europe, implementation of the In Vitro Diagnostic Regulation (IVDR) continues to raise compliance burdens for many genetic tests through Notified Body conformity assessment and CDx coordination with medicines regulators, which in turn constrains review capacity. The European Commission issued proposals in December 2025 for an EU Biotech Act and MDR/IVDR revisions aimed at simplifying and coordinating pathways for products that pair therapeutics with diagnostics, while ongoing IVDR transition deadlines for higher-risk IVD classes keep manufacturers focused on documentation, performance evaluation, and supply continuity. Across major markets, increased scrutiny of adaptive algorithms and multi-omic approaches is pushing developers to strengthen transparency, prospective validation plans, and change-control processes for AI-enabled interpretation layers that accompany genomic assays.

Competitive Landscape

The top suppliers—Thermo Fisher Scientific, Roche, QIAGEN, and others—collectively accounted for a substantial share of global revenue in 2025 but did not exceed dominant-player thresholds, leaving room for regional labs and specialized liquid biopsy firms. Illumina’s 2024 acquisition of Grail created an end-to-end sequencing-plus-diagnostics platform, while Thermo Fisher introduced the Genexus benchtop system that reduces hands-on time to two hours.

Guardant Health has moved upstream into therapeutic trials, leveraging a databank of 150,000 genomic profiles to guide ctDNA-based treatment intensification. Quest Diagnostics and Labcorp both expanded AI variant-interpretation capabilities through acquisitions, sharpening competitive positioning in clinical interpretation. Element Biosciences, BGI, and Oxford Nanopore compete on reagent pricing and long-read accuracy, creating price discipline across the genomic biomarkers industry.

Regulatory shifts encourage data-rich real-world evidence submissions, lowering barriers for mid-tier innovators. New entrants target pharmacogenomics outside oncology where testing penetration remains under 5%, and regional labs fill mid-priced panel gaps for insured populations in emerging economies. This bifurcated landscape keeps competitive intensity high and margins variable across test categories, reinforcing the need for continuous pipeline refresh and service differentiation.

Genomic Biomarkers Industry Leaders

Thermo Fisher Scientific Inc.

F. Hoffmann-La Roche Ltd

Myriad Genetics Inc

Eurofins Scientific

QIAGEN

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial whitespace is expanding where high-frequency monitoring and broader indications increase test volume per patient, particularly in longitudinal oncology follow-up and earlier detection workflows. MRD is moving from research-heavy adoption toward wider clinical ordering as vendors broaden indications and commercial access, exemplified by Myriad Genetics expanding availability of Precise MRD to colorectal, renal, and breast cancers in June 2026. This direction creates opportunities for labs and kit suppliers to deliver standardized tumor-informed workflows (sample logistics, sequencing depth, bioinformatics, and reporting) while also meeting payer documentation needs for serial testing.

Multi-cancer early detection (MCED) and multi-omic liquid biopsy are another near-term commercialization track, reinforced by new product launches that combine whole genome and transcriptome sequencing with interpretation software. Caris Life Sciences launched Caris Detect in July 2026 as a multi-cancer early detection blood test using whole genome and transcriptome sequencing, and Precede Biosciences launched Precede Bio Insight in April 2026 focused on genome-wide transcriptional biology. At the same time, national genomics implementation programs are shifting from cohort building toward clinical service delivery and standard-setting, which increases demand for interoperable reporting, variant interpretation, and quality systems that can scale across hospital networks (for example, UK Genome UK implementation activity and Australia consultation on a 2026-2030 National Health Genomics Policy Framework). Vendors that package assays, cloud analytics, and compliance-ready evidence generation for regulators and payers are positioned to win procurement tied to these health-system rollouts.

Recent Industry Developments

- June 2026: Roche announced FDA approval of label expansions for the PATHWAY anti-HER2/neu (4B5) test and VENTANA HER2 Dual ISH DNA Probe Cocktail to help identify patients with HER2-positive metastatic breast cancer eligible for ENHERTU. The update broadens the addressable testing population within routine pathology workflows and reinforces the role of companion diagnostics in guiding targeted therapy selection at scale.

- November 2025: Thermo Fisher Scientific received FDA approval for the Ion Torrent Oncomine Dx Target Test as a companion diagnostic to identify patients eligible for Bayer's HER2-directed therapy HYRNUO (sevabertinib). The approval strengthens the clinical utility of NGS-based CDx offerings and supports decentralized adoption through established Ion Torrent workflows in molecular labs.

- March 2024: Bayer and Thermo Fisher Scientific announced a collaboration to increase patient access to precision cancer medicines by expanding biomarker testing linked to targeted therapies. The partnership underscores how pharma-diagnostics alignment can accelerate testing uptake by pairing drug development and commercialization with defined genomic testing pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the genomic biomarkers market covers revenues earned from DNA and RNA based biomarker assays, kits, reagents, and related software that help identify or monitor genetic variations for clinical or drug development decisions.

Scope exclusions: We exclude proteomic or metabolomic biomarker tools, veterinary testing, and pure research sequencing services sold as stand-alone lab services.

Segmentation Overview

- By Indication

- Cancer

- Cardiovascular Disorders

- Neurological Disorders

- Renal Disorders

- Auto-Immune & Inflammatory Diseases

- Others

- By End User

- Diagnostic Laboratories

- Hospitals

- Pharmaceutical & Biotechnology Companies

- Others

- By Technology Platform

- Next-Generation Sequencing

- PCR

- Microarray

- Others

- By Biomarker Type

- Predictive Biomarker

- Prognostic Biomarker

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public health and science sources that help ground demand signals and clinical adoption, such as US FDA references for biomarker and companion diagnostic labeling, NIH and NCBI content for genetics terminology and usage context, and WHO and OECD indicators for health system and disease burden. We also reviewed peer reviewed journals indexed on PubMed to understand how DNA and RNA markers are being used in oncology and other disease areas, and where testing volumes appear to be trending.

To connect the science to market value, we used company annual reports, earnings notes, investor decks, and reputable press to identify product mix hints, pricing direction, and major launch timing. A paid subscription focused on company financials and news was used selectively to validate revenue splits and to cross-check event timelines. We also referenced a patent database to sanity check innovation intensity by platform. The desk research sources listed here are illustrative only, and many other public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test adoption rates, typical pricing ranges, and how volumes move across NGS, PCR, and microarray workflows, which then fed into the model inputs. We spoke with a mix of assay and kit suppliers, software and analytics stakeholders, clinical lab users, and pharma and biotech teams involved in trial biomarker strategies across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 30% | EMEA: 30% |

| Smaller Players: 19% | Managers: 53% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built by reconstructing the demand pool using platform level testing activity and clinical use intensity, and then translating that into value using typical price ranges for genomic biomarker assays and consumables (with software revenues included where it is directly tied to biomarker interpretation workflows). At the same time, we corroborated totals using selective bottom-up approximations. Supplier revenue cues, sampled ASP x volume checks, and channel feedback were used to adjust gaps that appear when public data is uneven by region.

Key model inputs were chosen because they are observable and explain market movement, including the share of tests that require genomic markers in oncology care pathways, the adoption pace of NGS panels versus PCR based marker testing, average markers per patient episode in high volume indications, reimbursement and guideline momentum that changes utilization, and the timing of clinical trial activity that pulls demand from pharma programs. When a data series was missing, proxies were used in a controlled way, such as using regional lab capacity and expected utilization ranges from interviews, before the results were normalized back to the total demand pool.

For forecasting, scenario analysis was applied, since the market is sensitive to payer coverage, regulatory clearances, and the speed at which new panels move from trial use into routine diagnostics. Assumptions for each scenario were reviewed with primary respondents, and then the final forecast track was selected based on the most repeated expectations across regions and end users.

Data Validation & Update Cycle

Outputs were checked through a simple triangulation flow where the modeled value was compared against independent signals such as testing penetration direction, platform shipment commentary, and clinical workflow adoption feedback. If a region or platform showed a sharp jump that could not be explained by the input variables, the drivers were revisited and the related assumptions were re-tested with additional calls.

Before sign-off, the model and written assumptions went through more than one analyst review. We ran variance checks between historical years and the first forecast year to confirm continuity. Reports are refreshed annually, and interim updates are made when material events occur that can move demand or pricing. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's Genomic Biomarkers Market Estimate Compared With Other Published Estimates

Different published market sizes for genomic biomarkers can vary by a lot because the same term is not always counted the same way, and because some studies use different timing, currencies, and growth assumptions. In practice, differences usually come from what gets included around testing services, how software is treated, and whether values reflect clinical use only or also research-heavy activity.

Pure research sequencing services sit outside Mordor Intelligence's scope for this market, which is one of the main reasons some published totals look much larger when they bundle sequencing as a service into the same revenue pool. Other differences also come from how quickly ASPs are assumed to decline for sequencing panels, whether reimbursement expansion is treated as a near-term step change, and how regional values are converted when exchange rates move within the year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.68 B (2025) | |

| Trade Journal A | USD 8.72 B (2025) | Often bundles sequencing sold as a service and broader genetic testing revenues into the total, which inflates value beyond biomarker specific assays, kits, reagents, and tied software. |

| Industry Publication B | USD 22.63 B (2025) | Uses a wider definition that can include multi-omics and adjacent testing categories, and it tends to apply uniform growth assumptions without clearly reconciling platform mix shifts and pricing compression. |

The spread across the three values mainly tracks definition and pricing logic rather than a disagreement on demand direction. When scope is kept tied to genomic biomarker specific products and workflow-linked software, and then checked against platform uptake and clinical utilization signals, the market total becomes easier to trace and repeat year to year.

Key Questions Answered in the Report

What is the current size of the genomic biomarkers market?

The genomic biomarkers market size stood at USD 5.68 billion in 2025 and is on track to reach USD 6.22 billion in 2026.

How fast is the market expected to grow?

Between 2026 and 2031 the market is forecast to expand at a 9.55% CAGR, lifting value to USD 9.82 billion.

Which application segment is expanding quickest?

Cardiovascular genomic panels are projected to post the highest growth, advancing at a 13.85% CAGR through 2031.

Why is Asia-Pacific considered the fastest-growing region?

Large national genome initiatives in China, India, and Japan, combined with expanding reimbursement, support an 11.72% CAGR to 2031.

What restrains broader adoption of genomic tests?

High test prices and fragmented regulatory pathways slow uptake, especially in markets without universal reimbursement.

Page last updated on: