Renal Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

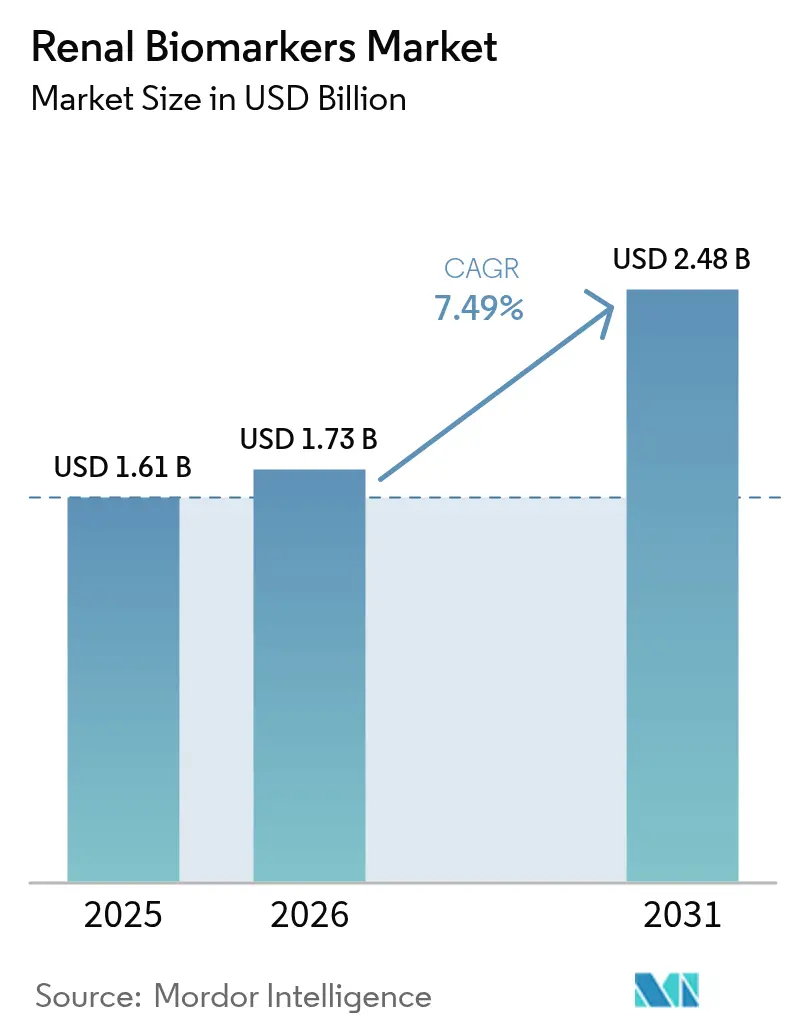

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 7.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Renal Biomarkers Market Analysis by Mordor Intelligence

The renal biomarkers market size was valued at USD 1.61 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 2.48 billion by 2031, at a CAGR of 7.49% during the forecast period (2026-2031). This expansion reflects a steady pivot from single-analyte, creatinine-centric testing toward high-content multiplex panels that track functional, structural and inflammatory kidney injury signals in one run. Laboratories in high-income countries are automating these panels on AI-enabled platforms that flag assay drift in real time, allowing faster clinical decisions and lower repeat-test rates. Broader adoption is further propelled by value-based reimbursement schemes that reward early CKD detection, while digital wearables capable of estimating real-time eGFR are opening a path for community screening programs and home-based monitoring. Despite technical advances, reimbursement for newly cleared biomarkers remains inconsistent and a lack of harmonized reference standards slows cross-lab result comparability, creating a measured but unmistakable evolution in diagnostic protocols.

Key Report Takeaways

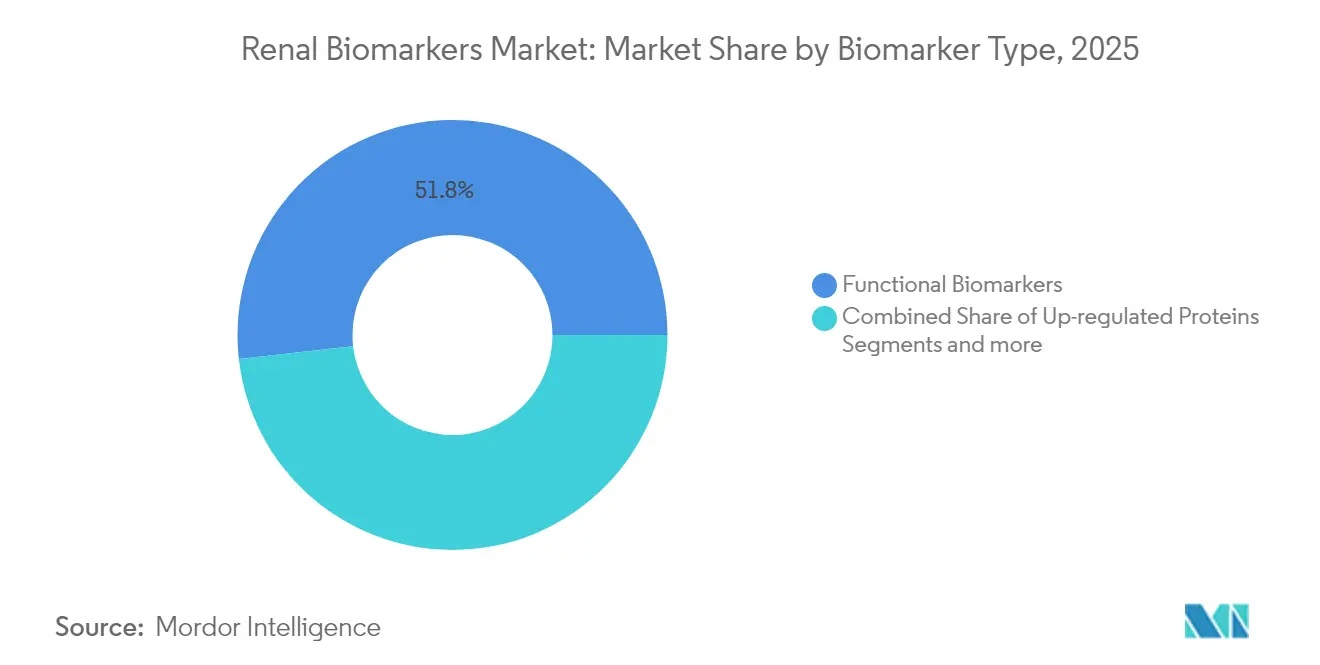

- By biomarker type, functional biomarkers led with 51.78% of the renal biomarkers market share in 2025; up-regulated proteins are projected to expand at an 8.12% CAGR to 2031.

- By diagnostic technique, ELISA accounted for 46.10% revenue in 2025, while CLIA platforms are anticipated to post the fastest growth at 8.2% CAGR through 2031.

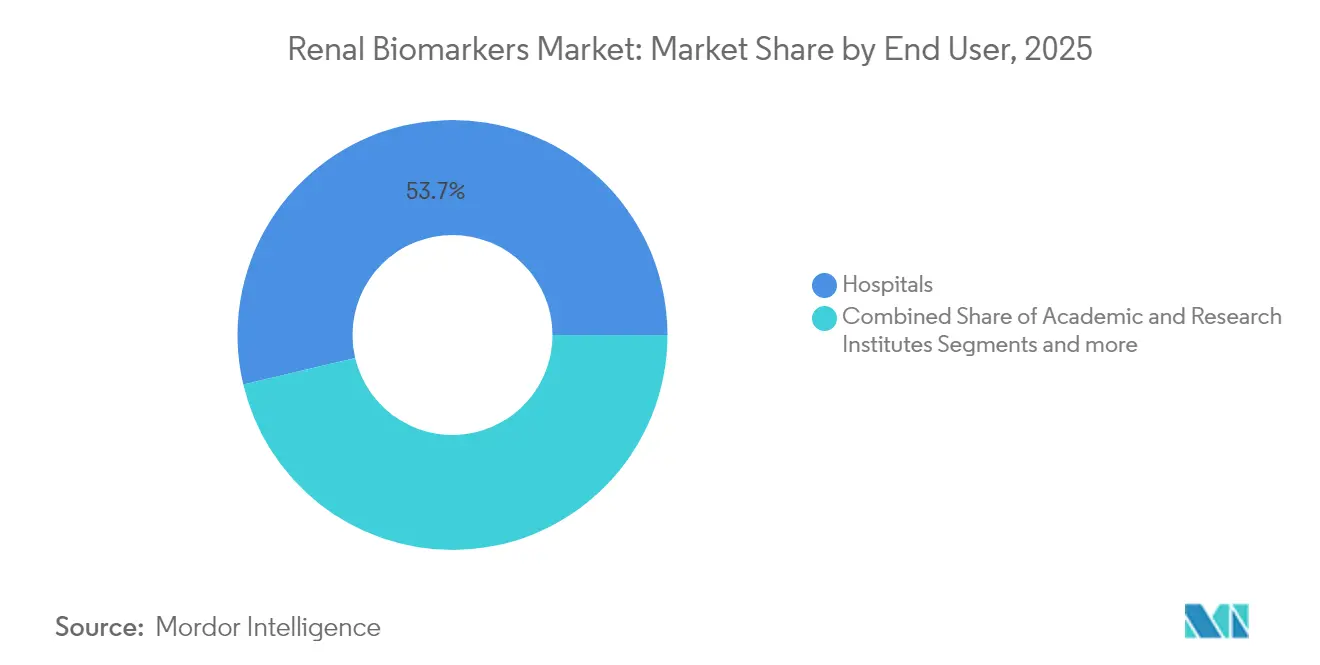

- By end user, hospitals held 53.70% of the renal biomarkers market size in 2025; academic and research institutes record the highest projected CAGR at 8.11% during 2026-2031.

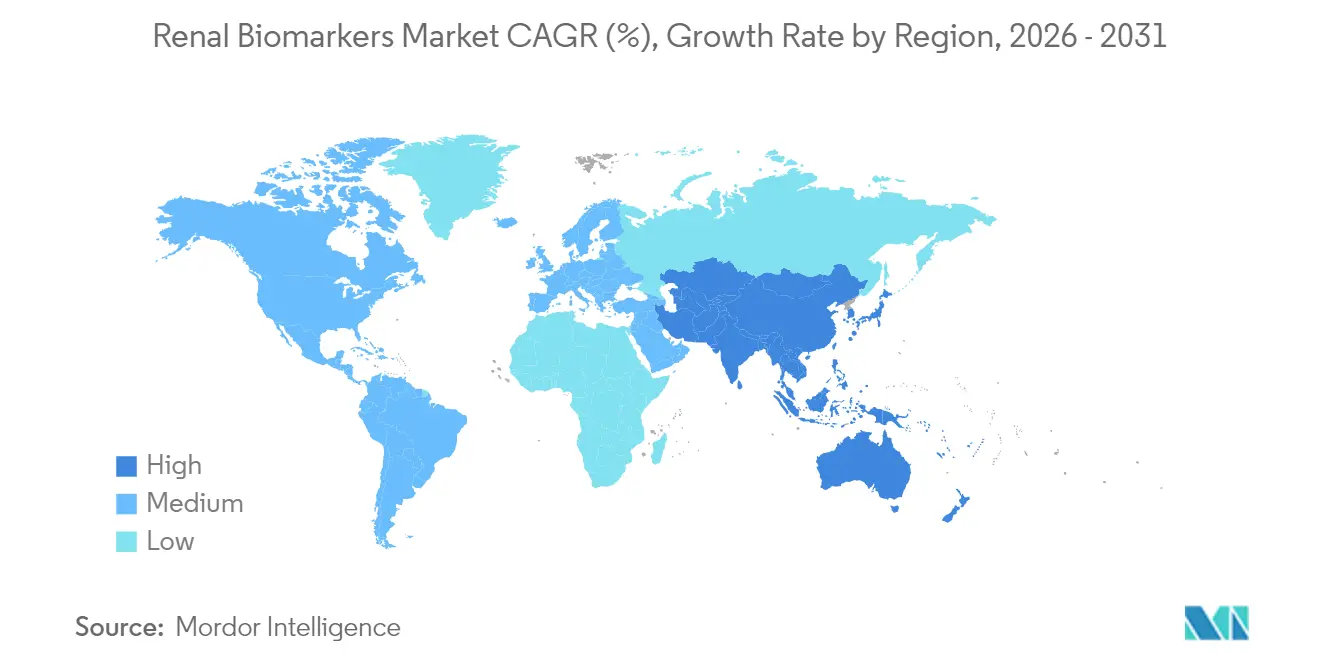

- By geography, North America commanded 41.80% of the renal biomarkers market share in 2025 and Asia-Pacific is advancing at an 8.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Renal Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of CKD & AKI | +1.5% | Global | Long term (≥ 4 years) |

| Growing diabetic & hypertensive population base | +1.2% | Global – highest impact in Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of high-throughput multiplex assays in nephrology labs | +1.8% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Government CKD screening mandates | +0.9% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| AI-enabled urinary proteomics for ultra-early detection | +1.3% | North America & Europe initially, global expansion | Long term (≥ 4 years) |

| Integration of digital wearables generating “real-time eGFR” | +0.8% | North America & Europe, premium healthcare segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Kidney Disease (CKD) & Acute Kidney Injury (AKI)

CKD affects 37 million U.S. adults and prevalence is projected to reach 17% among people aged 30 and older by 2030, driving a structural jump in test volumes as health systems move screening from nephrology clinics into primary care workflows [1]ECQI, "Kidney Health Evaluation," ecqi.org. Up to 90% of CKD cases remain undiagnosed until advanced stages, inflating treatment costs and dialysis dependence; payers therefore endorse comprehensive biomarker panels that flag injury before eGFR declines. Clinical pathways now combine creatinine with cystatin C, NGAL and urinary albumin to stratify risk and chart therapy intensity, supporting sustained demand for functional and up-regulated proteins. Population health contracts in the United States and Germany reimburse multi-analyte panels that demonstrate cost offsets from reduced hospitalization, turning renal biomarker testing into a preventive rather than confirmatory tool. Emerging-market governments are watching these outcomes closely, suggesting a long runway for global adoption momentum.

Growing Diabetic & Hypertensive Population Base

Diabetes and hypertension account for more than 60% of end-stage kidney disease referrals worldwide, and KDIGO’s 2024 guideline now directs quarterly renal biomarker testing for high-risk diabetics, not yearly reviews. Clinical laboratories are responding by bundling albumin-to-creatinine ratio, serum creatinine, cystatin C and NGAL in one orderable code that suits value-based payment metrics. SGLT2 inhibitors have added a therapeutic incentive because their dose adjustments hinge on early eGFR changes, raising clinician reliance on precise, high-frequency biomarker readings. Asia-Pacific faces the steepest uptick in type 2 diabetes incidence, so ministries in China and India are funding community screening vans that use finger-stick creatinine plus point-of-care NGAL cartridges, signaling the renal biomarkers market will embed itself in chronic-disease management pathways.

Rapid Adoption of High-Throughput Multiplex Assays in Nephrology Labs

Automated immunochemistry tracks found in “dark labs” run unattended overnight, analyzing up to 80 renal biomarkers per sample and uploading verified results at shift start. AI modules supervise reagent stability, auto-rerun flagged outliers, and suggest probable diagnostic classifications, trimming turnaround from 4 hours to 45 minutes for a complete renal injury profile. Multiplexing also slashes cost per analyte, letting regional labs in France and Japan offer expanded panels without new staffing. Novel up-regulated proteins such as KIM-1, Interleukin-18 and TIMP-2/IGFBP7 are entering these menus once antibodies reach scale, giving clinicians a single report across functional impairment, tubular stress and inflammatory load. Vendors that integrate middleware with electronic health record decision support are winning procurement bids because nephrologists can trigger automated alerts when combined biomarker signatures cross risk thresholds.

Government CKD Screening Mandates

The U.S. Congressional Kidney Caucus is pressing the USPSTF to issue an “A” grade for routine CKD screening, a step that would compel commercial payers to cover renal biomarker tests without cost-sharing. Pilot programs in Illinois and North Carolina already reimburse home collection kits measuring creatinine, cystatin C and albumin, with logistics funded under state value-based care pools. In Europe, Germany now requires annual albuminuria testing for every patient with type 2 diabetes, financed via statutory insurance, and Spain bundles serum creatinine with cystatin C in its national hypertension guideline. Singapore’s Ministry of Health subsidizes workplace screening that includes NGAL for construction workers exposed to heat stress, illustrating how localized public health priorities enlarge the renal biomarkers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of universal reference standards across laboratories | –0.8% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Stringent reimbursement hurdles for novel biomarkers | –0.6% | North America & Europe | Short term (≤ 2 years) |

| Pre-analytical sample variability in point-of-care settings | –0.4% | Global, higher impact in decentralized testing | Short term (≤ 2 years) |

| Limited validation data in minority ethnic populations | –0.3% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Universal Reference Standards Across Laboratories

NGAL, KIM-1 and penKid still lack harmonized calibrators, so inter-laboratory coefficient of variation can exceed 18%, undermining physician confidence and delaying guideline endorsement. While the International Federation of Clinical Chemistry has convened a global reference system for cystatin C, comparable workstreams for tubular injury proteins remain underfunded and technically complex. Emerging markets feel the impact most: procurement teams in Brazil and Nigeria report assay selection paralysis because platforms report different absolute values. Academic consortia in Japan and Canada are pooling biobanks to establish ethnicity-specific reference intervals, but until a certification scheme mirrors the success of IDMS-traceable creatinine, novel biomarker roll-outs will stay patchy.

Stringent Reimbursement Hurdles for Novel Biomarkers

Medicare reimburses creatinine at USD 5.46 per test but pays USD 21.83 for cystatin C only when documentation proves reduced eGFR accuracy, and it does not yet cover NGAL outside FDA-approved indications. Private insurers echo this stance, demanding multi-center outcome studies showing net savings before listing new CPT codes. European HTA bodies ask for cost-utility ratios below EUR 20,000 per QALY, a threshold difficult to achieve when early AKI detection must translate into hard endpoints such as dialysis avoidance. Smaller diagnostic firms often lack capital to generate the required evidence, slowing commercial entry and tilting negotiating power toward larger incumbents with robust HEOR teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Biomarker Type: Functional Markers Drive Current Revenue

Functional biomarkers generated USD 0.83 billion in 2025, equal to 51.78% of the renal biomarkers market. Creatinine remains ubiquitous for eGFR calculation, yet its blind spot in early injury means clinicians frequently pair it with serum cystatin C, whose broader dynamic range improves accuracy in pediatrics and the elderly. Albuminuria screening volumes are rising fastest within the functional block because diabetic care pathways link microalbumin results to therapy intensification. The segment is gaining incremental lift from smartphone-enabled dipsticks that photograph colorimetric albumin changes and relay data to cloud dashboards, widening access in rural Asia and Africa.

Up-regulated proteins are forecasted to climb at an 8.12% CAGR, outpacing all other categories. NGAL grabs the spotlight owing to its 2-hour post-insult detection window; emergency departments in Germany now add plasma NGAL to their sepsis panels to flag impending renal injury earlier than creatinine . KIM-1 assays approved in 2025 for drug-induced nephrotoxicity surveillance in oncology trials are expected to pull incremental orders from CROs. The renal biomarkers market size for up-regulated proteins could hit USD 0.52 billion by 2031 if guideline committees broaden indications as anticipated, underlining the segment’s accelerator role in overall market growth.

By Diagnostic Technique: Automation Reshapes Testing Workflows

ELISA contributed 46.10% of 2025 revenue, anchored by entrenched reagent rental contracts and wide operator familiarity. Mid-tier hospitals in Latin America favor ELISA because initial capital outlay is modest and menus cover all mainstream functional biomarkers. Weakness shows when daily test load exceeds 400 samples: manual plate washing and incubation add labor overhead and can prolong turnaround to same-day rather than hourly delivery. Laboratories are therefore graduating to open-channel ELISAs with robotic loaders that cut hands-on time, an interim step before full CLIA migration.

CLIA is advancing at an 8.2% CAGR, claiming new installations in reference networks across the United States, Japan and the Gulf Cooperation Council. These systems deliver femtogram-level sensitivity, crucial for low-abundance proteins such as TIMP-2/IGFBP7 used in critical-care renal stress panels. Vendors now bundle AI-powered middleware that flags reagent lot drifts and auto-calibrates daily runs, reducing proficiency-testing failures. PETIA and LC-MS/MS remain niche but strategic: PETIA secures high-speed creatinine throughput for health-check programs, while LC-MS enables research centers to validate candidate peptide markers before immuno-assay commercialization. Collectively, automation trends sustain the renal biomarkers market by driving higher throughput with fewer technologists .

By End User: Academic Research Drives Innovation

Hospitals generated 53.70% of 2025 revenue, a function of integrated patient flows, lab capacity and payer contracts that bundle diagnostic and treatment episodes. Many tertiary centers added NGAL, KIM-1 and cystatin C to sepsis order sets following internal cost avoidance studies that showed 1-day reductions in ICU length of stay. Hospital pharmacy-lab committees now incorporate biomarker data into antibiotic stewardship dashboards, illustrating the fluid clinical uptake when diagnostics tie directly to therapy decisions.

Academic and research institutes, while holding a smaller absolute volume, chart an 8.11% CAGR because grant-funded consortia require advanced biomarker panels for precision nephrology studies. Kidney-on-a-chip platforms that replicate glomerular filtration and tubular secretion allow scientists to screen nephrotoxic drug candidates in micro-fluidic assays, generating demand for multiplex LC-MS readouts. These institutes often collaborate with diagnostic manufacturers to co-create assay kits, accelerating time-to-market once regulatory submissions begin. Commercial reference labs pick up validated panels and make them available through direct-to-physician portals, expanding the renal biomarkers market size without requiring every hospital to bring the assays in-house.

Geography Analysis

North America held 41.80% revenue in 2025, equal to USD 0.67 billion of the renal biomarkers market size, underpinned by robust laboratory automation, clear FDA pathways and insurer willingness to reimburse novel tests that meet evidentiary thresholds. Medicare’s Merit-based Incentive Payment System links nephrology practice scores to annual albuminuria rates, sparking protocol updates and higher test ordering frequency. U.S. vendors leverage proximity to academic medical centers for rapid clinical trial enrollment, shortening biomarker validation cycles and keeping the region at the forefront of first-to-market launches.

Asia-Pacific is the growth engine at 8.45% CAGR, with China, India and South Korea combining public health mandates and cashback insurance schemes to subsidize early CKD detection. Provincial governments in China partnered with leading IVD firms to deploy mobile labs testing serum creatinine and NGAL in factory clinics, a model expected to scale to 100 units by 2027. In India, Ayushman Bharat insurance packages now remunerate albumin-to-creatinine ratio tests twice yearly for diabetic policyholders, driving steep volume increases in tier-2 cities. This policy pull, coupled with local reagent manufacturing that trims cost per test, secures enduring lift for the renal biomarkers market in the region.

Europe contributes stable, mid-single-digit revenue growth anchored in evidence-based policy frameworks. Germany’s IQWiG approved cystatin C reimbursement in 2025 following a meta-analysis that demonstrated 12% reclassification improvement in CKD staging over creatinine alone. The United Kingdom’s NICE is piloting a combined NGAL and KIM-1 panel in six NHS trusts, with early health-economic modeling suggesting dialysis deferral savings offset assay costs within 24 months. Scandinavian countries remain early adopters of digital health; Swedish startups now integrate eGFR readings from smart rings into electronic medical records, ensuring biomarker data loop seamlessly between consumer devices and clinical decision support. Collectively, European vigilance for cost-effectiveness tempers headline growth but cements long-term adoption of validated assays, maintaining a 26.90% slice of the renal biomarkers market.

Competitive Landscape

The renal biomarkers market is moderately concentrated. Abbott and Roche leverage installed chemistry analyzers and broad service networks to lock in reagent contracts, while Siemens Healthineers differentiates with Atellica’s open channels that accept third-party renal panels. Randox uses proprietary Biochip arrays to bundle 22 biomarkers in one cartridge, appealing to high-throughput reference labs in Europe and the Middle East.

Strategic M&A is an accelerant. bioMérieux’s EUR 111 million acquisition of SpinChip Diagnostics in January 2025 added a centrifugal microfluidics platform delivering renal biomarker results in 10 minutes at the bedside, positioning the firm for sepsis and emergency department workflows. Quest Diagnostics expanded upstream in February 2025 by purchasing Fresenius’s U.S. renal testing assets, bringing 45 dialysis-center satellites into its logistics grid and securing near-patient sample capture. Smaller innovators such as SphingoTec closed EUR 5 million in Series C funding to push penKid into critical care algorithms, emphasizing that venture-backed niche players can still carve space next to conglomerates.

Artificial intelligence capability is a key differentiator. Roche’s navify digital platform triages multi-analyte results and suggests risk trajectories, while Abbott’s Alinity cX uses onboard analytics to reject hemolyzed specimens automatically, reducing false positives. These workflow efficiencies keep switching costs high, fostering sticky reagent revenues and reinforcing competitive moats. Regional distributors in Latin America and Africa act as gatekeepers, negotiating exclusivity with one or two global suppliers, thus shaping local market dynamics as much as headline product innovation.

Renal Biomarkers Industry Leaders

-

Thermo Fischer Scientific Inc.

-

Abbott Laboratories

-

F. Hoffmann-La Roche AG

-

bioMérieux SA

-

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Boditech Med Inc. and SphingoTec GmbH commercially launched the AFIAS sphingotest penKid assay to provide real-time kidney function assessment in critically ill patients.

- February 2025: Quest Diagnostics acquired kidney testing assets from Fresenius Medical Care, expanding its renal diagnostics footprint across 45 dialysis centers.

- January 2025: The Foundation for the National Institutes of Health and Critical Path Institute announced FDA acceptance of a qualification plan for a urine biomarker panel to monitor drug-induced kidney injury.

- August 2024: SphingoTec closed a EUR 5 million Series C round to accelerate commercialization of penKid and bioactive Adrenomedullin biomarkers.

Global Renal Biomarkers Market Report Scope

As per the scope of the report, renal biomarkers are biomarkers that help diagnose or identify patients at risk of developing kidney diseases by measuring their blood or urine levels. They are commonly released in acute or chronic kidney injuries, which are characterized by the rapid or gradual loss of kidney function, resulting in serious clinical implications. The renal biomarkers market is segmented by biomarker type, diagnostic technique, end user, and geography.

The market is segmented as a functional biomarker, up-regulated protein, and other biomarker types based on biomarker type. Based on diagnostic technique, the market is segmented as enzyme-linked immunosorbent assay, particle-enhanced turbidimetric immunoassay (PETIA), colorimetric assay, chemiluminescent enzyme immunoassay (CLIA), and liquid chromatography-mass spectrometry (LS-MS). Based on end-users, the market is segmented as hospitals, diagnostic laboratories, and other end users. The market is segmented based on geography into North America, Europe, Asia-Pacific, the Middle East, Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD) for the above segments.

| Functional Biomarkers | Serum Creatinine |

| Serum Cystatin C | |

| Urine Albumin | |

| Up-regulated Proteins | NGAL |

| Kidney Injury Molecule-1 | |

| Interleukin-18 | |

| Other Biomarker Types |

| Enzyme-Linked Immunosorbent Assay (ELISA) |

| Particle-Enhanced Turbidimetric Immunoassay (PETIA) |

| Colorimetric Assay |

| Chemiluminescent Immunoassay (CLIA) |

| Liquid Chromatography-Mass Spectrometry (LC-MS) |

| Others |

| Hospitals |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Biomarker Type | Functional Biomarkers | Serum Creatinine |

| Serum Cystatin C | ||

| Urine Albumin | ||

| Up-regulated Proteins | NGAL | |

| Kidney Injury Molecule-1 | ||

| Interleukin-18 | ||

| Other Biomarker Types | ||

| By Diagnostic Technique | Enzyme-Linked Immunosorbent Assay (ELISA) | |

| Particle-Enhanced Turbidimetric Immunoassay (PETIA) | ||

| Colorimetric Assay | ||

| Chemiluminescent Immunoassay (CLIA) | ||

| Liquid Chromatography-Mass Spectrometry (LC-MS) | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the renal biomarkers market?

The renal biomarkers market is valued at USD 1.73 billion in 2026 and is projected to grow to USD 2.48 billion by 2031 at a 7.49% CAGR.

Which biomarker category leads revenue today?

Functional biomarkers hold 51.78% of 2025 revenue, anchored by widespread creatinine, cystatin C and urine albumin testing.

Which region shows the fastest growth?

Asia-Pacific leads with an 8.45% CAGR through 2031, propelled by government-mandated CKD screening and rising diabetes prevalence.

What technology is expanding quickest in renal biomarker testing?

Chemiluminescent immunoassay (CLIA) platforms are growing at 8.2% CAGR because laboratories favor their automation and analytical sensitivity.

Which recent deal illustrates growing point-of-care focus?

BioMérieux’s EUR 111 million purchase of SpinChip Diagnostics adds a 10-minute microfluidic immunoassay platform to its renal testing portfolio.

Page last updated on: