Belgium Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

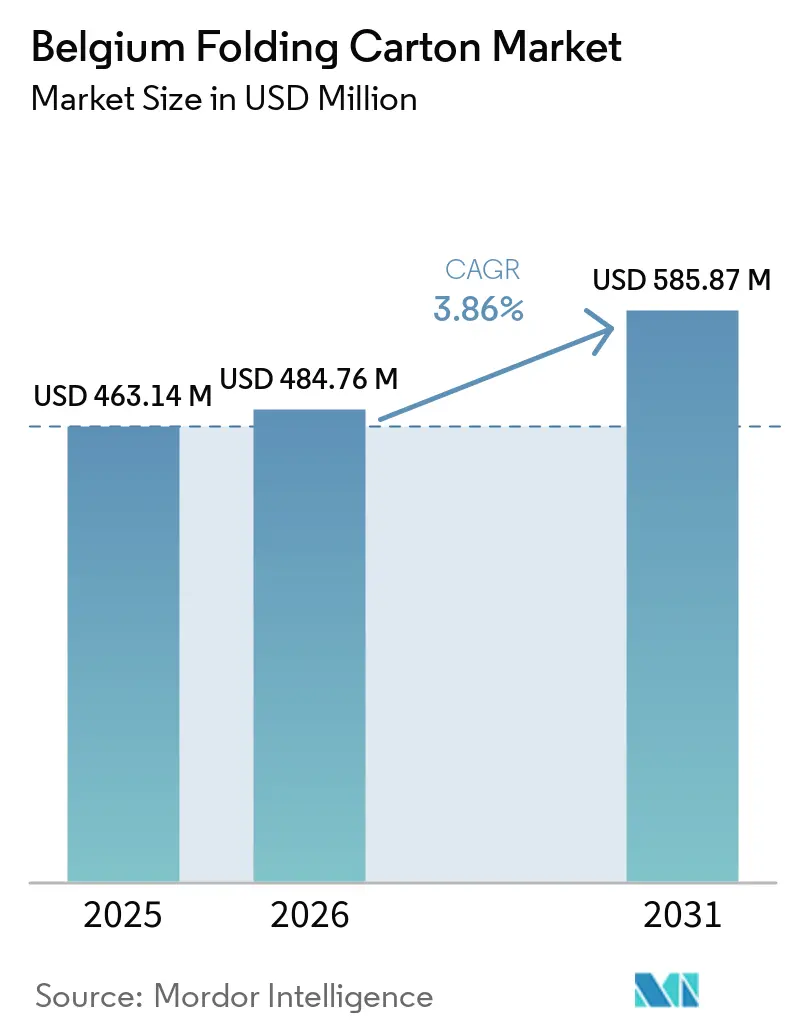

| Base Year Market Size (2025) | USD 463.14 Million |

| Market Size (2026) | USD 484.76 Million |

| Market Size (2031) | USD 585.87 Million |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

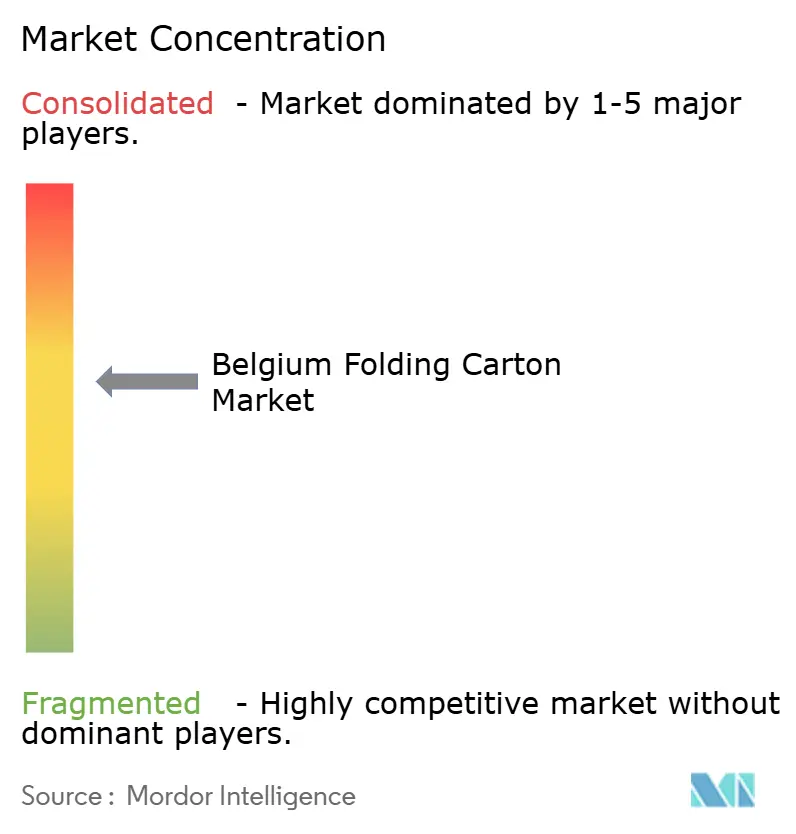

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Folding Carton Market Analysis by Mordor Intelligence

The Belgium folding carton market size is expected to increase from USD 463.14 million in 2025 to USD 484.76 million in 2026 and reach USD 585.87 million by 2031, growing at a CAGR of 3.86% over 2026-2031. The Belgium folding carton market benefits from the country’s long-standing role as a European packaging hub, strict sustainability rules, and an e-commerce logistics backbone that encourages brand owners to replace plastic with recyclable board. Regulation (EU) 2025/40, which applies from August 2026, compels converters to document recyclability pathways, supply recycled-content board, and limit empty space in parcel packaging, therefore tilting demand toward paper-based solutions. At the same time, recovered-fiber price spikes, labor shortages, and regional overcapacity pressure converter margins, prompting investment in automation and digital presses. Belgiam producers see opportunity in micro-flute designs for e-commerce, barrier-coated grades for fresh food, and serialization-ready packs for pharmaceuticals, yet these gains must offset soft short-term demand and high capital requirements.

Key Report Takeaways

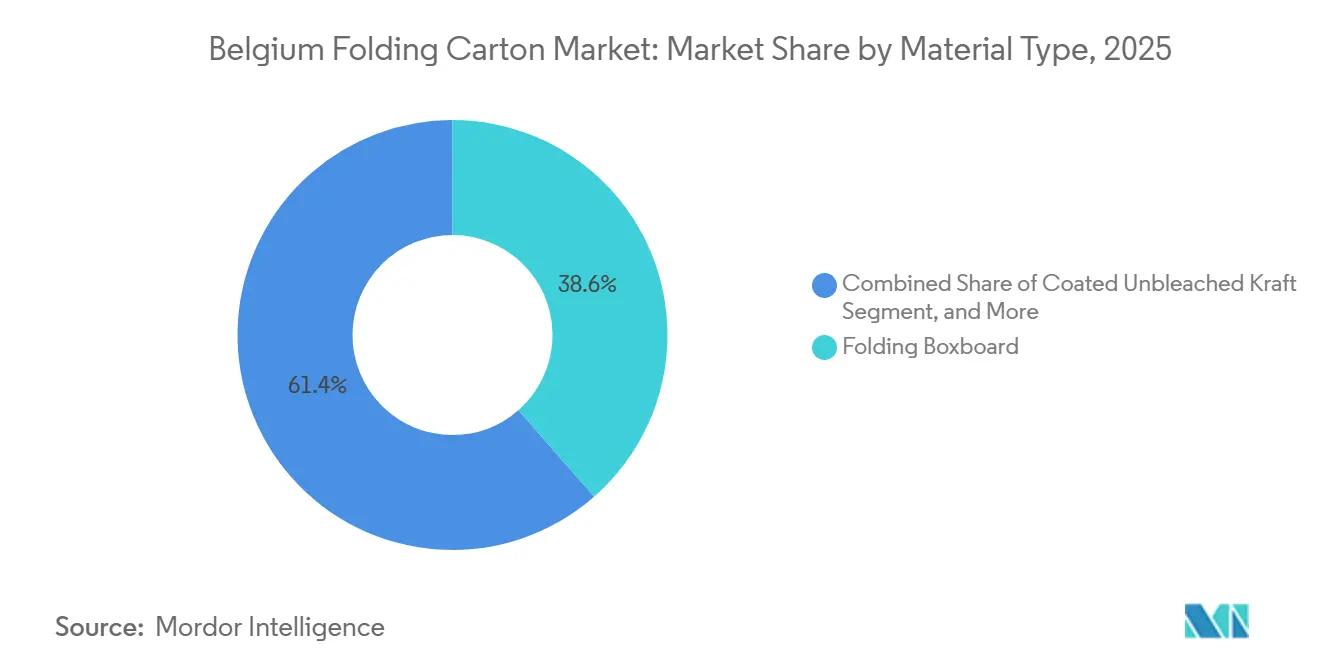

- By material type, folding boxboard captured with 38.56% of the Belgium folding carton market share in 2025.

- By printing technology, the Belgium folding carton market size for digital platforms is projected to grow at a 5.31% CAGR to 2031.

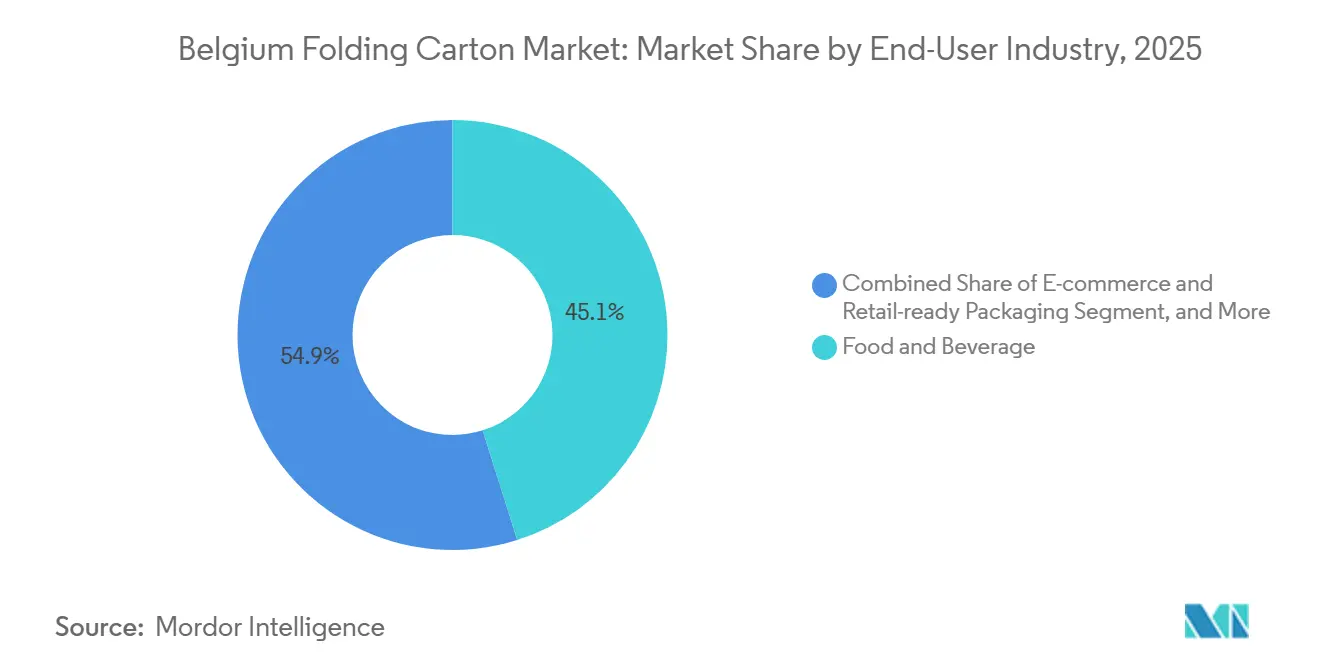

- By end-user industry, the food and beverage industry captured 45.13% of the Belgium folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Belgium Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Packaging Solutions | +1.2% | Belgium, broader EU compliance zones | Medium term (2-4 years) |

| Increasing Adoption of E-Commerce Boosting Parcel Volumes | +0.9% | Antwerp and Liège logistics corridors, national | Short term (≤ 2 years) |

| Stringent EU Regulations Favoring Recyclable Materials | +0.8% | EU-wide, Belgium as early adopter | Medium term (2-4 years) |

| Rising Consumer Preference for Premium Packaged Food and Beverages | +0.6% | Belgium, Netherlands, France | Medium term (2-4 years) |

| Surge in Craft Beer and Specialty Beverage Exports | +0.3% | Flanders brewing clusters, export markets | Long term (≥ 4 years) |

| Automation-Driven Short-Run Digital Printing | +0.2% | Belgium, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Packaging Solutions

Brand owners in Belgium favor fiber-based recyclable packs to meet corporate net-zero pledges and comply with Regulation (EU) 2025/40, which bans PFAS in food contact materials from August 2026. Stora Enso’s EUR 1.1 billion (USD 1.2 billion) Oulu line, inaugurated in August 2025, produces lightweight folding boxboard that helps confectionery exporters cut transport emissions. Mayr-Melnhof Karton’s 2025 life-cycle study shows its recycled white-lined chipboard emitting 123 kg CO₂ eq per 1,000 m², roughly 26% below the European average, bolstering its position with cost-conscious converters. Together, these developments underpin the 4.79% CAGR forecast for coated unbleached kraft that offers natural-brown aesthetics and grease protection without plastic liners.

Increasing Adoption of E-Commerce Boosting Parcel Volumes

Antwerp and Liège fulfillment centers recorded rapid parcel growth during 2024-2025, driving demand for right-sized folding cartons that comply with the regulation’s 50% maximum void ratio from 2030. DS Smith expanded Benelux e-commerce capacity, while Amazon introduced custom-fit cartons and paper bags across Europe in May 2025, confirming the market shift. Equipment vendors responded: Bobst rolled out the Expertfold 106 and 215 folder-gluers in January 2026 for micro-flute substrates used in automated parcel lines. These investments support the 4.93% CAGR outlook for the e-commerce and retail-ready segment.

Stringent EU Regulations Favoring Recyclable Materials

Regulation (EU) 2025/40 obliges converters to issue Declarations of Conformity from August 2026, document recycled content, and integrate digital watermarks for consumer sorting, heightening compliance costs. Cardboard transport packs are exempt from reuse quotas that bind plastic and rigid containers, channeling investment toward folding cartons. Valipac’s 2025 warning that plastic recycling capacity lags demand further nudges brands into paper-based substrates.[1]Valipac, “Plastic Recycling Capacity and Regranulate Demand in Belgium,” valipac.be The law’s labeling rules create demand for digital-print specialists who can apply variable QR codes at speed, widening the runway for technology adoption.

Rising Consumer Preference for Premium Packaged Food and Beverages

Belgian shoppers pay a premium for artisanal goods packaged in high-finish cartons featuring embossing, foil, and soft-touch coatings. Smurfit WestRock produced a recyclable micro-flute pack with gold-foil accents for La Trappe craft beer, underlining carton versatility. The SIXPACK research project found that reusable beer cartons cut CO₂ emissions by 46% compared with aluminum cans, reinforcing cartons’ sustainability story. Chocolate exporters rely on solid bleached sulfate for vibrant graphics, while Tetra Pak’s EUR 60 million (USD 64 million) pilot for high-paper barrier boards hints at future crossover into folding-carton grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recycled Paperboard Supply Prices | -0.7% | Belgium, broader European recovered-fiber markets | Short term (≤ 2 years) |

| Competition from Flexible Packaging Alternatives | -0.5% | Belgium, EU single-market competition | Medium term (2-4 years) |

| Capital-Intensive Transition to High-Speed Digital Presses | -0.3% | Belgium, Western Europe | Medium term (2-4 years) |

| Labor Shortages in Skilled Converting Operators | -0.2% | Belgium, Flanders and Wallonia industrial zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Recycled Paperboard Supply Prices

Sonoco raised uncoated recycled paperboard prices by EUR 80 per metric ton (USD 86 per metric ton) effective April 15, 2026, citing energy and chemical inflation. Belgian converters, who source most board from mills in Germany, Austria, and Poland, struggle to hedge these swings, while EU Waste Shipment rules that restrict recovered-fiber exports tighten local supply. Mayr-Melnhof Karton reported that new Scandinavian virgin-fiber capacity and Asian imports intensified price competition even as feedstock costs remained high, squeezing margins.

Competition from Flexible Packaging Alternatives

Stand-up pouches and flow-wrap films undercut folding cartons in terms of cost and line speed for snacks and pet treats. With recycled-content mandates deferred to 2030, flexible-packaging firms exploit a temporary regulatory gap to compete aggressively. Yet Regulation (EU) 2025/40 bans PFAS in food packaging from August 2026 and sets a 70% recyclability threshold by 2030, raising compliance costs for multi-material pouches. Belgian carton makers counter by developing micro-flute designs and barrier coatings that eliminate the need for polyethylene liners while retaining print quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Natural-Brown Kraft Gains Traction

Folding boxboard secured 38.56% of the Belgian folding carton market in 2025, favored for its printability and stiffness in food multipacks. Recycled white-lined chipboard appeals to budget-oriented converters targeting scope-3 emission cuts, as Mayr-Melnhof Karton’s 2025 audit illustrates with a 26% lower CO₂ profile than the European average. Coated unbleached kraft, backed by Stora Enso’s 750,000 tpy Oulu line, is set for a 4.79% CAGR through 2031 thanks to grease resistance and natural-brown shelf appeal.

Solid bleached sulfate remains the substrate of choice for cosmetics and pharma cartons, where bright surfaces aid serialization, although its higher cost limits its share. Weight-reduction technology such as FiberLight Tec helps converters shrink freight emissions without compromising rigidity. Micro-flute and barrier-coated boards carve out niches in e-commerce and fresh produce where cushioning and moisture control matter more than gloss. Graphic Packaging’s Waco plant, finished in 2025, boosts recycled-fiber supply and may ease price swings for Belgian buyers.[2]Graphic Packaging Holding Company, “EX-99.1 - 8-K Current Report,” graphicpkg.com

By Printing Technology: Digital Presses Accelerate Short-Run Growth

Lithographic presses held 41.28% of Belgium's folding carton market share in 2025, powering high-volume cereal and confectionery runs where color fidelity is critical. Digital printing is forecast to grow at a 5.31% CAGR through 2031, driven by demand for personalized campaigns, limited editions, and rapid prototyping. NAPCO Research noted in 2024 that 83% of brands rank variable packaging as important, a finding that spurred Xeikon, HP Indigo, and Koenig and Bauer to launch faster inkjet lines.

Converters adopting digital gain flexibility for sub-15,000-sheet orders must manage higher ink costs and learning curves. Gravure still serves ultra-long tobacco runs, while flexography targets corrugated and micro-flute transit packs. VPK Group’s 2025 machinery upgrades in Oudegem and Erembodegem underscore Belgium’s dual focus on structural and print innovation. These upgrades are expected to strengthen the company's competitive position in the European market.

By End-User Industry: Parcel Logistics Puts Wind in Carton Sails

Food and beverage accounted for 45.13% of the Belgium folding carton market in 2025, led by chocolate, confectionery, and craft beer, which rely on vivid lithographic graphics. E-commerce and retail-ready packaging is the fastest mover at a 4.93% CAGR, buoyed by Amazon’s custom-fit program and Regulation (EU) 2025/40’s void-reduction rule. Pharma demand is stable thanks to EU Directive 2011/62/EU serialization needs, while cosmetics leverage solid bleached sulfate for premium effects.

Tobacco volumes decline yet sustain high-finish gravure jobs, and collectible trading cards keep specialty converters such as Cartamundi busy after its EUR 25 million (USD 26.8 million) Turnhout expansion. Converters serving parcel hubs are adopting digital die-cutters and inline quality control to meet tight delivery schedules, compensating for the softness observed in traditional FMCG categories. This shift reflects the increasing need for efficiency and precision in the e-commerce supply chain.

Geography Analysis

Belgium’s folding carton supply chain relies on cross-border board imports from Germany, Austria, and Poland, as well as on carton exports to France, the Netherlands, and Luxembourg. Flanders hosts most converting plants near the Port of Antwerp, giving operators easy access to imported substrates and outbound logistics. Wallonia’s smaller footprint caters to regional food processors and pharma sites. Valipac’s mature extended-producer-responsibility scheme loads compliance costs earlier than in neighboring markets, but the head start may yield a competitive edge once EU rules converge after 2030.

International Paper’s USD 9.9 billion takeover of DS Smith in January 2025 and its planned EMEA spin-off by early 2027 injects uncertainty into board supply for Belgian converters that source from DS Smith mills.[3]International Paper, “International Paper Completes DS Smith Acquisition,” internationalpaper.com Smurfit WestRock’s February 2026 medium-term guidance forecasts just 1.7% CAGR for European packaging, hinting at continued overcapacity that could tighten credit or curtail technical support for smaller buyers.

Belgium’s 75% reusable beverage-packaging target by 2040 and the SIXPACK carbon study favor reusable cartons for beer and soft drinks, but achieving scale requires deposit infrastructure that only large brewers can bankroll. Consequently, converters balance home-market sustainability leadership against cost competition from Central and Eastern Europe, illustrated by Van Genechten’s EUR 10 million (USD 10.7 million) investment in a Latvian plant completed in March 2026.

Competitive Landscape

The Belgium folding carton market is moderately consolidated, with Mayr-Melnhof Karton, Smurfit WestRock plc, Stora Enso Oyj, Mondi plc, and niche players competing across overlapping applications. Mayr-Melnhof reported a 13.4% drop in European carton volumes for the first nine months of 2025 and launched a Fit-For-Future program that aims to deliver sustainable earnings gains of over EUR 250 million (USD 268 million) by 2027.[4]Mayr-Melnhof Karton AG, “Company Presentation April 2026,” mm.group

Smurfit WestRock targets USD 7 billion in EBITDA by 2030 and relies on cost cuts to weather sluggish demand. Investment themes include high-speed digital presses exceeding EUR 2 million (USD 2.1 million) per line, robotic folder-gluers, and barrier-coating assets that swap polyethylene liners for water-based alternatives. Smaller converters unable to finance such upgrades risk consolidation. This trend could reshape market dynamics, potentially leading to fewer but larger players dominating the industry.

Certifications such as FSC, PEFC, and ISO 14001 are now table stakes in multinational tenders, widening the gap between scale players and family-owned shops. White-space opportunities cluster around micro-flute designs that rival flexible pouches on thinness, plastic-free grease-barrier boards for ready meals, and RFID-enabled pharma cartons. Cartamundi’s high-precision, multi-layer coatings for trading cards highlight the pricing power that specialists can command in fast-growing niches.

Belgium Folding Carton Industry Leaders

Smurfit WestRock plc

Mayr-Melnhof Karton AG

Stora Enso Oyj

Graphic Packaging Holding Company

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sonoco raised uncoated recycled paperboard prices by EUR 80 per metric ton (USD 86 per metric ton) citing cost inflation.

- February 2026: Van Genechten Packaging completed a EUR 10 million (USD 10.7 million) capacity expansion at VG Kvadra Pak in Latvia.

- February 2026: Cartamundi launched a hiring campaign for 150 positions at its Turnhout site following its 40% capacity expansion.

- January 2026: Bobst introduced Expertfold 106 and 215 folder-gluers engineered for e-commerce micro-flute cartons.

Belgium Folding Carton Market Report Scope

This study examines the folding carton market in Belgium, providing insights into its current trends, growth drivers, and industry applications. It evaluates the market dynamics, including supply chain analysis, competitive landscape, and factors influencing demand. Additionally, the analysis covers the forecast period to offer a comprehensive understanding of the market's trajectory.

The Belgium Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Belgiam folding carton market, and what is its expected growth?

The Belgium folding carton market size reached USD 463.14 million in 2025, is estimated at USD 484.76 million in 2026, and is projected to reach USD 585.87 million by 2031, reflecting a 3.86% CAGR.

Which material type is growing fastest in Belgiam folding cartons?

Coated unbleached kraft is forecast to grow at a 4.79% CAGR through 2031 because its natural-brown look and grease barrier replace plastic liners.

How are EU regulations shaping carton demand in Belgium?

Regulation (EU) 2025/40 mandates 70% recyclability by 2030 and restricts void space in parcels, pushing brands toward recyclable folding cartons over flexible plastics.

Why is digital printing gaining share in carton converting?

Brand demand for short-run personalization and variable data campaigns drives a 5.31% CAGR outlook for digital printing, outpacing offset growth.

What impact do price swings in recovered fiber have on converters?

Price volatility, highlighted by Sonoco’s USD 87 per metric ton increase in 2026, compresses converter margins and encourages long-term supply contracts or vertical integration.

Which end-user segment shows the strongest growth potential?

E-commerce and retail-ready packaging leads growth at a 4.93% CAGR, supported by parcel expansion at Antwerp and Liège hubs and new right-sized packaging mandates.

Page last updated on: