Benelux Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.34 Billion |

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 2.23% CAGR |

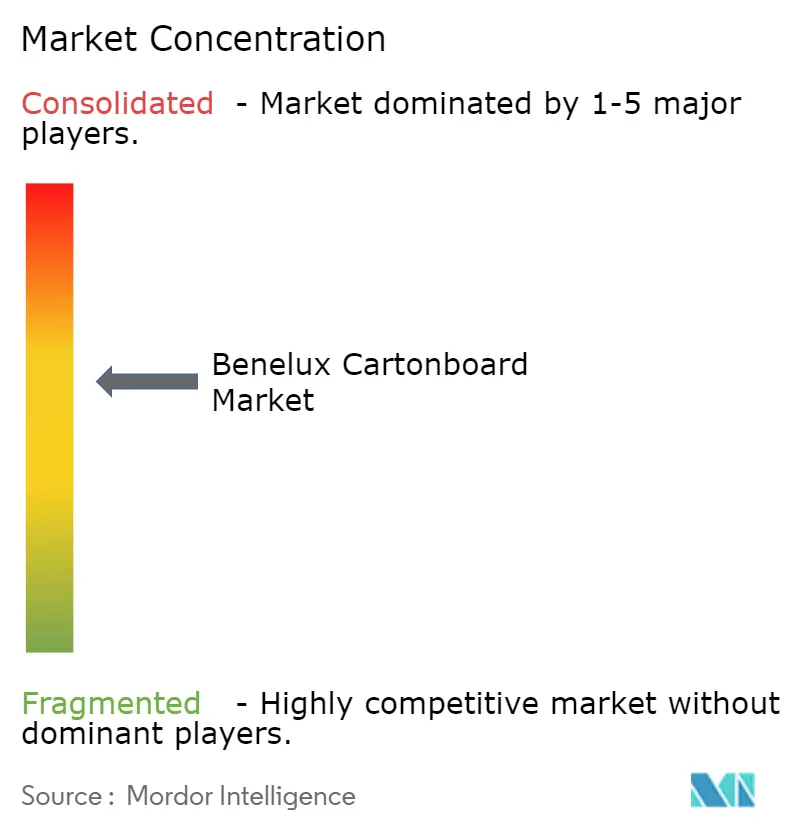

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux Cartonboard Market Analysis by Mordor Intelligence

The Benelux Cartonboard Market size was valued at USD 1.34 billion in 2025 and is estimated to grow from USD 1.37 billion in 2026 to reach USD 1.53 billion by 2031, at a CAGR of 2.23% during the forecast period (2026-2031).

Growth remains measured because this is a mature regional packaging base, and most value creation comes from grade and format premiumization rather than large volume gains. Strong recycling systems in Belgium and the Netherlands, together with the Netherlands' logistics role, keep demand steady for specification-driven board applications. The Benelux cartonboard market is also being shaped by supply pressure across Europe, where added capacity, returning U.S. export volumes, and rising Asian imports have narrowed margins for virgin-fiber grades. That pressure is pushing converters toward pharmaceutical, chilled food, and premium personal care programs where compliance, print quality, and customization matter more than lowest cost. The Benelux cartonboard market still offers room for gains in specialty applications, but the opportunity is concentrated in higher-value board grades, barrier innovation, and faster-response converting models.

Key Report Takeaways

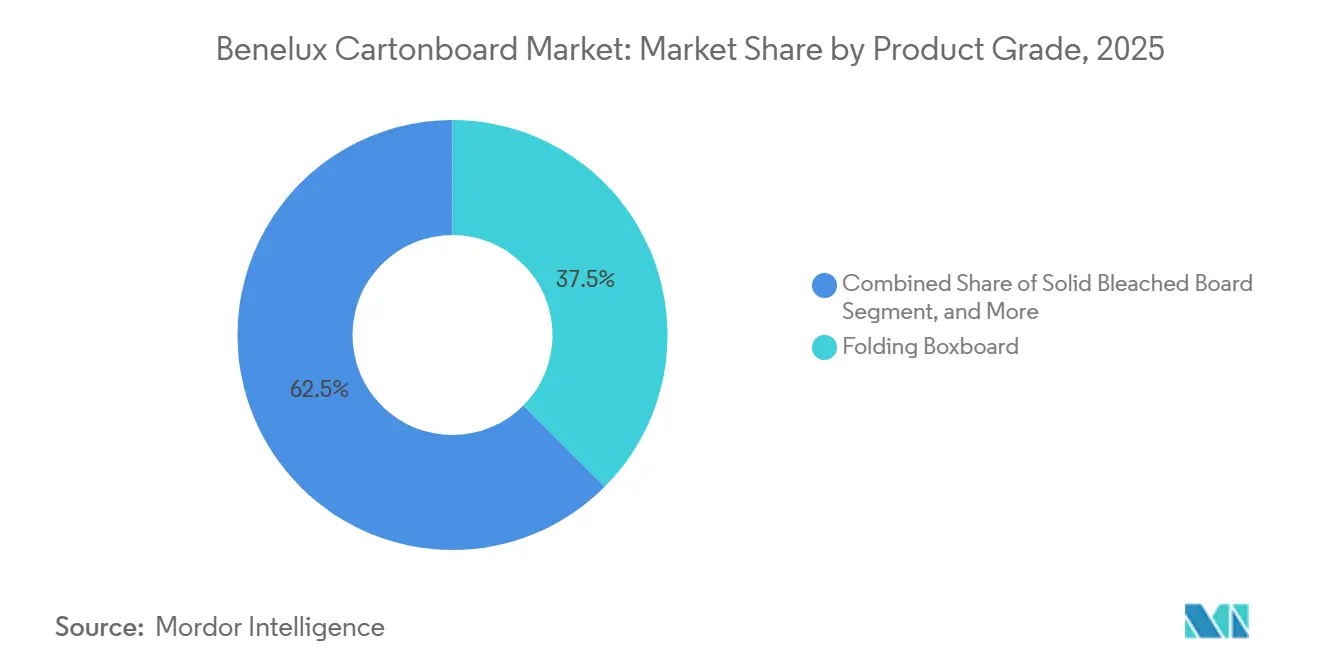

- By product grade, folding boxboard held 37.48% of the Benelux cartonboard market share in 2025, while solid bleached board is forecast to expand at a 5.56% CAGR through 2031.

- By packaging format, folding cartons accounted for 54.34% share of the Benelux cartonboard market size in 2025, while liquid packaging is projected to grow at a 5.31% CAGR through 2031.

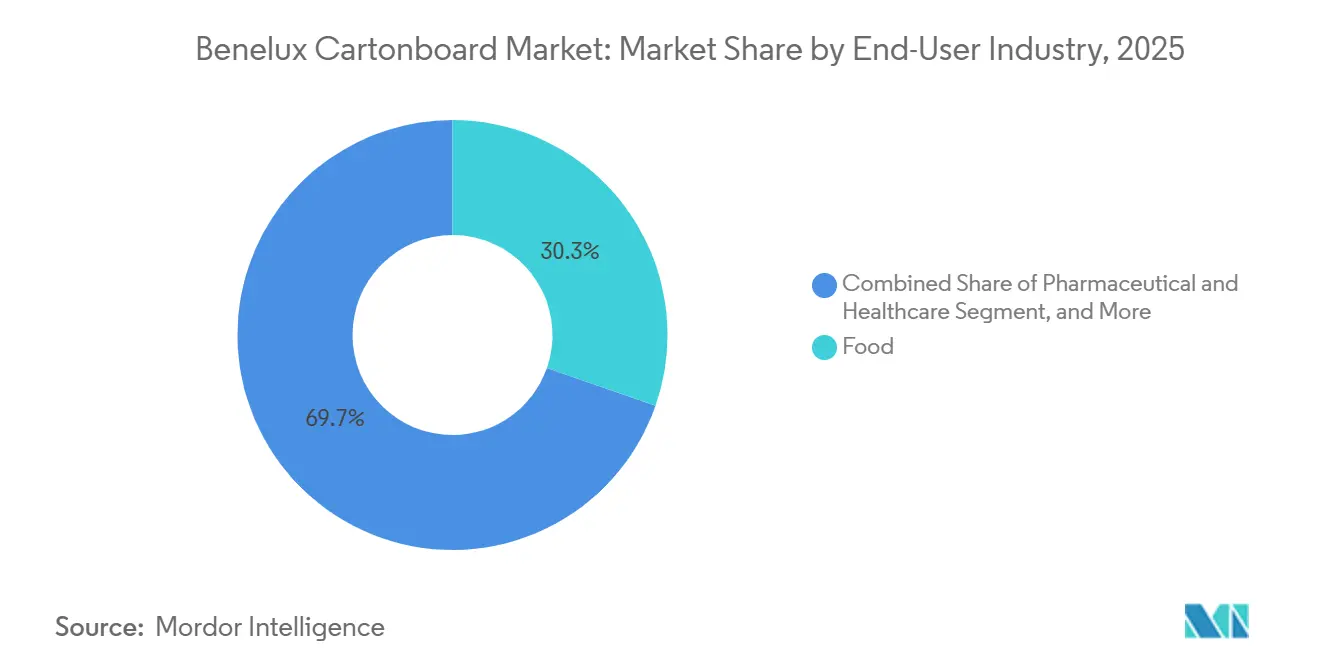

- By end-user industry, food represented 30.34% of market value in 2025, while pharmaceutical and healthcare is projected to grow at a 5.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Benelux Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Recyclable Fiber-Based Packaging | +0.65% | Global, concentrated in Belgium and Netherlands | Medium term (2-4 years) |

| Growth in Chilled, Frozen, and Convenience Food Packs | +0.45% | Belgium and Netherlands, logistics and retail hubs | Short term (≤ 2 years) |

| Premium Cartons for Pharmaceutical Compliance and Traceability | +0.40% | Belgium pharma cluster, broader Benelux | Medium term (2-4 years) |

| Short-Run Customization and Digital Print Adoption | +0.30% | Belgium and Netherlands | Short term (≤ 2 years) |

| Benelux Beverage-Carton Recycling Loop Expansion | +0.25% | Netherlands, Belgium, and Luxembourg | Medium term (2-4 years) |

| Shelf-Stable Plant-Based and Ambient Beverage Adoption | +0.20% | Netherlands and Belgium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Recyclable Fiber-Based Packaging

Regulation (EU) 2025/40 and its EPR fee-modulation framework are making recyclable fiber formats more commercially attractive across Benelux packaging decisions.[1]European Commission, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” EUR-Lex, eur-lex.europa.eu Belgium and the Netherlands entered this rule cycle with mature producer responsibility systems, so cartonboard adoption is being pulled by compliance economics as much as by sustainability positioning. Fost Plus, Valipac, and Verpact frameworks are increasing the cost of staying with harder-to-recycle packaging formats, which gives mono-material fiber options a clearer commercial case. That is creating a multi-year conversion pipeline in food, cosmetics, and e-commerce packaging for regional board converters. The pace of this shift still depends on validated PFAS-free barrier reformulation before the regulation starts applying from August 12, 2026.

Growth in Chilled, Frozen, and Convenience Food Packs

Chilled, frozen, and convenience food remain an attractive channel for premium cartonboard in Benelux because shelf-visible food packs still need structure, print quality, and barrier performance. MM Group states that its board portfolio for frozen food includes barrier-coated virgin fiber and recycled cartonboard grades designed to replace polyethylene and polypropylene coatings in demanding freezer applications. Van Genechten Packaging Group also positions recyclable frozen food cartons for ready meals, ice cream, and seafood, showing that converters are targeting performance-led substitution rather than basic pack replacement. Demand is also supported by dense urban consumer corridors in the Netherlands and Belgium, where convenience-led retail formats are well established. Because flexible pouches do not replicate cartonboard's display strength in many shelf-facing applications, this demand continues to support the folding-carton base of the Benelux cartonboard market.

Premium Cartons for Pharmaceutical Compliance and Traceability

Belgium's pharmaceutical base keeps this application among the most technically demanding uses of cartonboard in the region. Pharmaceutical packaging sold in the EU must support serialized data, tamper evidence, and traceability requirements under the Falsified Medicines Directive framework.[2]EURPACK, “Pharmaceutical Packaging Serialization, Industrial Challenges and Evolutionary Approaches,” EURPACK, eurpack.it Autajon's Belgium operations in Arlon and Brussels show how converters are investing in specialized pharmaceutical folding carton capacity with high traceability expectations. The EUDR adds another layer from December 30, 2026, because virgin-fiber cartonboard entering the EU will require due diligence statements and stronger source traceability. Buyers that need verified origin are therefore pre-qualifying integrated board suppliers, and that is helping support higher-specification solid bleached board in the Benelux cartonboard market.

Short-Run Customization and Digital Print Adoption

Short-run digital printing is becoming more practical in cartonboard because production economics now work for smaller and more variable order sizes. Agfa and Hybrid Software announced in May 2026 a collaboration to deliver full variable-data capability into digital folding carton workflows, aimed at serial-number-level customization in one press pass. That matters for pharmaceutical dosage updates, personalized cosmetics packs, and limited-edition food cartons that no longer fit long offset runs. Brand owners also reduce inventory exposure when regulatory text or artwork changes force fast reprints. This is strengthening Belgian and Dutch converters with digital assets against lower-cost plants that depend on larger conventional volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp and Energy Cost Volatility | -0.45% | Global, concentrated in Belgium and Netherlands, energy-intensive converting | Short term (≤ 2 years) |

| Competition From Flexible Pouches and Lightweight Plastics | -0.35% | Netherlands, logistics and food retail, Benelux broadly | Medium term (2-4 years) |

| EUDR Traceability Burden on Virgin-Fiber Supply Chains | -0.25% | Belgium pharma, Netherlands liquid packaging, broader Benelux | Medium term (2-4 years) |

| Coating Conversion Risk Under PFAS and Recyclability Rules | -0.20% | Belgium and Netherlands, food-contact cartonboard | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pulp and Energy Cost Volatility

The structural cost issue in the Benelux cartonboard market is sharper than the moderate top-line growth rate suggests. Metsä Board reported a comparable operating result loss of EUR -80.2 million (USD -90.6 million) in 2025 as weak demand and elevated raw material costs weighed on results. MM Group's Board and Paper division posted an adjusted operating margin of 0.2% in 2025 and recorded impairment losses of EUR 70.5 million (USD 79.7 million), which shows how little room suppliers had to absorb cost shocks. Converters without upstream pulp integration remain exposed when long-term customer contracts cannot fully pass through raw material swings. High electricity costs in Belgium and the Netherlands add pressure to printing, lamination, and die-cutting lines that already operate on tight margins.

Competition From Flexible Pouches and Lightweight Plastics

Flexible pouches and lightweight plastic formats are adapting to regulation rather than leaving the field. Under the PPWR, packaging suppliers are redesigning structures to better align with recyclability criteria, which allows plastics to retain a role in cost-sensitive applications. Billerud stated that its liquid packaging board business lost volume in the second half of 2025 because competition intensified, highlighting the substitution risk in beverage-related uses. The exposure is strongest in Dutch food retail and logistics channels, where private-label economics are highly cost sensitive. Converters can offset part of this through embossing, personalization, and shelf-ready design, but lightweight plastics still keep a material-cost advantage in non-premium applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Premium and Compliance-Led Grades Keep the Mix Elevated

Folding boxboard held 37.48% of Benelux cartonboard market share in 2025, making it the largest product-grade category in the region. Its position reflects the needs of Belgium's pharmaceutical and confectionery manufacturing base, where printability, stiffness, and hygiene compliance remain central to pack specification. Solid bleached board is the fastest-growing grade, with a 5.56% CAGR projected over 2026-2031, because pharmaceutical serialization upgrades and cosmetics premiumization both favor cleaner white surfaces and stronger grammage stability. Metsä Board completed the EUR 60 million (USD 67.8 million) renewal of its Simpele mill in October 2025, adding 10,000 tonnes of annual folding boxboard capacity while reaching 98% fossil-free energy use. Stora Enso also started operations on its new Oulu consumer board line in early 2025, with annual capacity of 750,000 tonnes of folding boxboard and coated unbleached kraft, and full ramp-up targeted for 2027.

Liquid packaging board and food service board remain the most actively developing specialty grades in the regional mix. White-lined chipboard and solid unbleached board still serve cost-sensitive uses, especially in secondary retail and industrial packaging, but they face more pressure from flexible alternatives when barrier performance is not strong enough. The PPWR creates a more even compliance screen across grades because packaging placed on the market must move toward demonstrable recyclability performance by 2030. That makes certified fiber access, barrier chemistry, and convertibility more important than simple tonnage availability in the Benelux cartonboard market. Within the Benelux cartonboard industry, suppliers that combine print performance with compliance-ready coatings are best placed to win specification-led business.

By Packaging Format: Folding Cartons Hold the Base While Liquid Packs Grow Faster

Folding cartons accounted for 54.34% share of the Benelux cartonboard market size in 2025, which kept this format well ahead of all other packaging formats. The lead reflects broad demand from pharmaceutical, food, and cosmetics applications, where secondary packs still need strong graphics, product protection, and shelf presence. Liquid packaging is the fastest-growing format, with a 5.31% CAGR projected over 2026-2031, supported by demand in plant-based milk, ambient juice, and chilled dairy. SIG Group reported aseptic carton revenue growth of 1.0% at constant currency in Q1 2026, indicating early recovery in liquid packaging demand after softer 2025 conditions. Pharmaceutical serialization rules also keep a durable floor under folding carton demand in Belgium's export-oriented healthcare packaging base.

Sleeve and tray formats are also gaining ground in chilled and frozen food applications across the region. Greenflex distributes pressed board tray solutions in Belgium and the Netherlands for frozen food, ready meals, and foodservice uses, with 90-100% renewable material content and compatibility with common European recycling streams. Mondi reinforced this direction in November 2025 when it launched an extended food packaging portfolio with additional solid board solutions and digital printing capabilities after integrating Schumacher Packaging. Other formats remain smaller, but the Benelux cartonboard market is gaining support from foodservice operators that are preparing for tighter single-use packaging rules from August 2026.

By End-User Industry: Food Anchors Volume While Healthcare Leads Growth

Food represented 30.34% share of the Benelux cartonboard market size in 2025, while pharmaceutical and healthcare is projected to expand at a 5.81% CAGR through 2031. Food remains the largest base because the region concentrates ambient, chilled, and frozen food manufacturers that depend on cartonboard for structure, graphics, and retail handling. Pharmaceutical and healthcare is growing faster because compliance, traceability, and specification discipline favor premium board grades and specialized converting. MM Group stated that its pharma and healthcare packaging business recorded encouraging growth in 2025 despite broader weakness in European packaging markets. Autajon's Belgium operations in Arlon and Brussels illustrate the specialized end of this demand, with pharmaceutical folding carton sites built around traceability and dedicated production capability.

Belgian chocolate, biscuits, and ready meals continue to support folding boxboard demand, while Dutch dairy and ready-meal producers sustain demand for liquid packaging board and food service board. Tobacco remains a stable but volume-declining outlet, because regulatory scrutiny keeps compliant carton demand in place even as design freedom narrows. Cosmetics and toiletries are among the highest-value-per-kilogram uses in the Benelux cartonboard industry, especially where brands specify UV-varnished and hot-foil finished premium cartons. The beverage category remains a structural contest between aseptic cartons and lightweight plastic alternatives, which keeps format innovation active. Other end-user groups, including toy, apparel, automotive parts, and household products, add incremental volume to the Benelux cartonboard market as EPR-led plastic substitution moves forward.

Geography Analysis

Belgium remained the dominant volume and value contributor within the Benelux cartonboard market in 2025. Its role is supported by a dense pharmaceutical, confectionery, and premium consumer goods manufacturing base that keeps local demand weighted toward compliance-led and print-sensitive board applications. Belgium also hosts Stora Enso's Langerbrugge mill, an important recycling and board facility where water discharges fell by 7% in 2025. Autajon's sites in Arlon and Brussels further reinforce Belgium's position in pharmaceutical carton conversion with dedicated market-facing capacity. VBO-FEB has presented the PPWR's August 2026 application as a strategic opening for Belgian packaging producers adapting to updated EPR frameworks.

The Netherlands holds a different place in the Benelux cartonboard market because it combines logistics scale with strength in liquid packaging and distribution. Rotterdam's gateway role makes Dutch converters natural partners for brand owners that manage packaging flows for wider European distribution. Stora Enso's De Lier corrugated packaging site continues ramp-up in 2026, and Metsä Board's January 2026 acquisition of the Winschoten Sheeting and Distribution Hub adds local depth for premium folding boxboard supply. The Netherlands also maintained one of Europe's strongest packaging recovery systems, with Verpact reporting an 88% recycling and reuse rate for all packaging in 2023. That mix of logistics reach, recovery performance, and premium board distribution keeps Dutch demand broad across food, beverage, and e-commerce applications.

Luxembourg is the smallest market in the Benelux cartonboard market and functions mainly as a consumption base supplied by Belgian and Dutch converters. Its role is expanding through cross-border e-commerce and pharmaceutical distribution, where standardized shelf-ready cartons fit regional supply models well. Luxembourg's alignment with Belgian EPR structures through Valorlux and the Interregional Packaging Commission helps suppliers serve all 3 Benelux markets on a more unified specification platform. Growth is likely to remain modest through 2031, but Luxembourg still matters as a cross-border destination that rewards compliance-ready packaging formats.

Competitive Landscape

The Benelux cartonboard market is moderately consolidated at the board-manufacturing level, where integrated suppliers such as Metsä Board, Stora Enso, Mayr-Melnhof Karton, Billerud, Reno De Medici, and Sappi provide most virgin-fiber and recycled-fiber substrate to converters. At the converting level, the structure is much more fragmented, with pan-European groups, Benelux-rooted specialists, and dedicated pharmaceutical converters all competing for regional programs. In the Benelux cartonboard market, pricing power is stronger in substrate supply than in conversion, where service depth, customization, and compliance readiness carry more weight. MM Group's Fit-For-Future program contributed EUR 70 million (USD 79.1 million) to adjusted operating profit in 2025 through structural cost reductions at converting plants. Smurfit Westrock's February 2026 medium-term plan paired European growth targets with consultations at a Netherlands converting facility, showing that portfolio optimization and innovation are moving in parallel.[3]Smurfit Westrock, “Smurfit Westrock Medium-Term Investor Update,” Smurfit Westrock, smurfitwestrock.com

The clearest competitive edge is now regulatory and operational readiness rather than simple installed capacity. Pharmaceutical buyers increasingly favor converters with serialization lines, documented fiber traceability, and controlled production environments, which narrows the pool of eligible partners. Liquid packaging specialists and premium board suppliers are reinforcing their positions through aseptic systems, lightweight grades, lower-carbon production, and certified sourcing. Metsä Board's EUR 200 million (USD 226 million) green bond issuance in May 2025 points to the investment path the Benelux cartonboard market is rewarding, namely fossil-free production, energy efficiency, and recyclability-aligned board development.[4]Metsä Board Corporation, “Financial Statements Bulletin 1 January-31 December 2025,” Metsä Group, metsagroup.com

White space remains strongest in PFAS-free food-contact barriers, short-run digital print cartons, and closed-loop grades that can clear stricter design-for-recycling scrutiny. Converters that cannot demonstrate readiness for the PPWR and EUDR timetable over the next few years are likely to face customer attrition in Belgium and the Netherlands. Koehler Paper SE sits outside the core competitive set for this study because its portfolio is centered on specialty papers rather than folding carton converting or liquid packaging board, while Iggesund Paperboard is a closer peer in fresh-fiber premium cartonboard. That leaves the Benelux cartonboard market moderately consolidated in board supply and clearly fragmented in conversion, with premium applications supporting the best margins.

Benelux Cartonboard Industry Leaders

Mayr-Melnhof Karton Aktiengesellschaft

Metsä Board Corporation

Stora Enso Oyj

Reno De Medici S.p.A.

Smurfit Westrock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Smurfit Westrock published its medium-term plan targeting adjusted EBITDA of USD 7 billion by end of 2030, with European volume growth targeted at 1.7% per year and annual capital expenditures of USD 2.4 billion to USD 2.8 billion. Simultaneously, the company entered into consultations at one Netherlands converting facility as part of continued asset optimization.

- February 2026: Elopak reported FY2025 consolidated revenues exceeding EUR 1.2 billion (USD 1.36 billion) for the first time, alongside a 39% reduction in absolute Scope 1 and 2 carbon emissions against its 2020 baseline, as the company accelerated its "Repackaging tomorrow" strategy for low-carbon, fiber-based liquid packaging.

- January 2026: Metsä Board agreed to acquire the Winschoten Sheeting and Distribution Hub in the Netherlands from Konvertia Group, strengthening its Benelux distribution infrastructure for folding boxboard and related premium grades.

Benelux Cartonboard Market Report Scope

The Benelux Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Benelux Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current size and outlook for the Benelux cartonboard market?

The Benelux cartonboard market size was USD 1.34 billion in 2025, is projected at USD 1.37 billion in 2026, and is forecast to reach USD 1.53 billion by 2031 at a 2.23% CAGR.

Which product grade leads demand in Benelux cartonboard?

Folding boxboard led product demand with a 37.48% share in 2025, supported by pharmaceutical and confectionery packaging requirements in Belgium.

Which packaging format is growing the fastest across Benelux?

Liquid packaging is the fastest-growing format, with a 5.31% CAGR through 2031, supported by demand in plant-based milk, ambient juice, and chilled dairy.

Why is pharmaceutical packaging so important in Belgium?

Belgium's strong pharmaceutical base drives demand for serialized, traceable, and high-specification cartons, which is also why pharmaceutical and healthcare is forecast to grow at a 5.81% CAGR.

How are PPWR and EUDR affecting cartonboard sourcing decisions?

PPWR is pushing recyclable and PFAS-compliant packaging design, while EUDR is increasing traceability requirements for virgin-fiber supply chains from late 2026 onward.

What is the main competitive challenge for suppliers in this space?

The biggest challenge is balancing rising pulp and energy costs with pressure from flexible pouches and lightweight plastics in cost-sensitive applications.

Page last updated on: