Bedding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

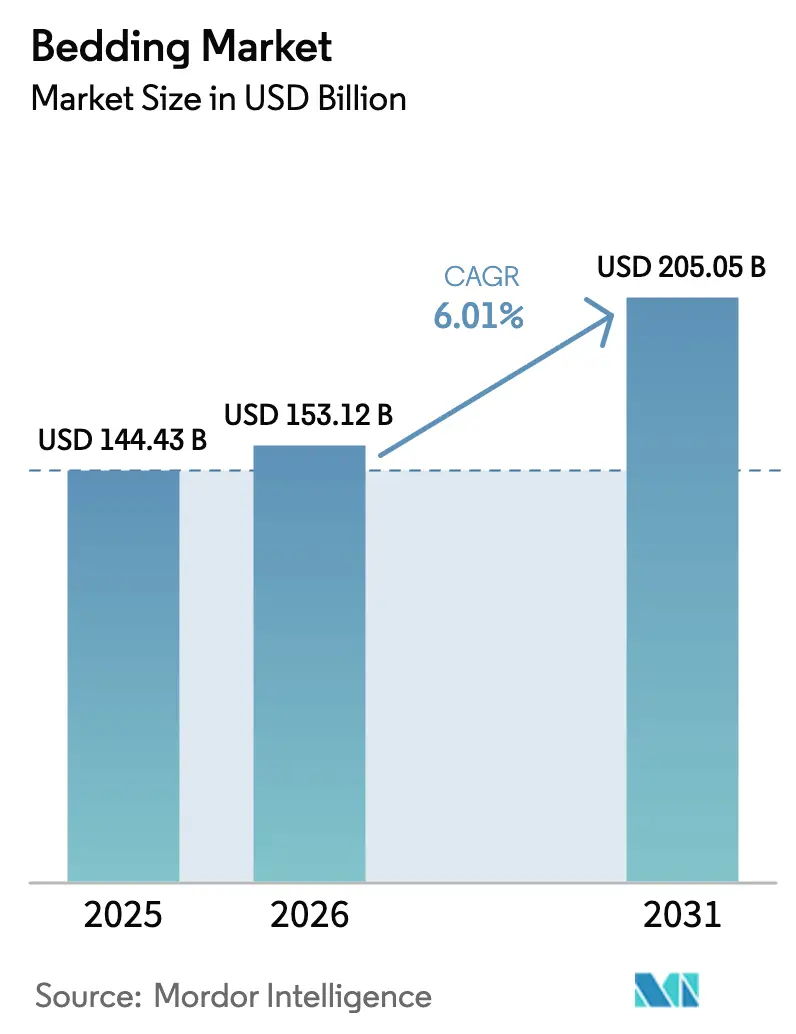

| Market Size (2026) | USD 153.12 Billion |

| Market Size (2031) | USD 205.05 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bedding Market Analysis by Mordor Intelligence

The bedding market size is expected to grow from USD 144.43 billion in 2025 to USD 153.12 billion in 2026 and is forecast to reach USD 205.05 billion by 2031 at a 6.01% CAGR over 2026-2031. A 12.86% year-on-year decline in cotton prices to USD 0.6182 per pound by November 2025 reduced input cost pressure and underscored the bedding market’s resilience to raw material volatility that often erodes margins in textile categories[1]Cotton Ginners Association, “Volatile Cotton Prices and Trade Policy Impacts,” cottongins.org, cottongins.org. Growth in the bedding market reflects a demand shift toward premium comfort, material-origin transparency, and sustainable certifications as procurement and consumer habits mature in 2026. Extended producer responsibility rules and PFAS restrictions are accelerating product refresh cycles and design changes, which support value growth even in price-sensitive subcategories. Competitive dynamics intensified after Tempur Sealy completed its acquisition of Mattress Firm in February 2025, creating an entity with stronger omnichannel control and a larger direct-to-consumer base, which is shaping pricing, assortment, and service expectations across the bedding market. These conditions position the bedding market for steady value expansion as established brands and scaled suppliers adapt portfolios, compliance systems, and distribution to new rules and changing customer journeys.

Key Report Takeaways

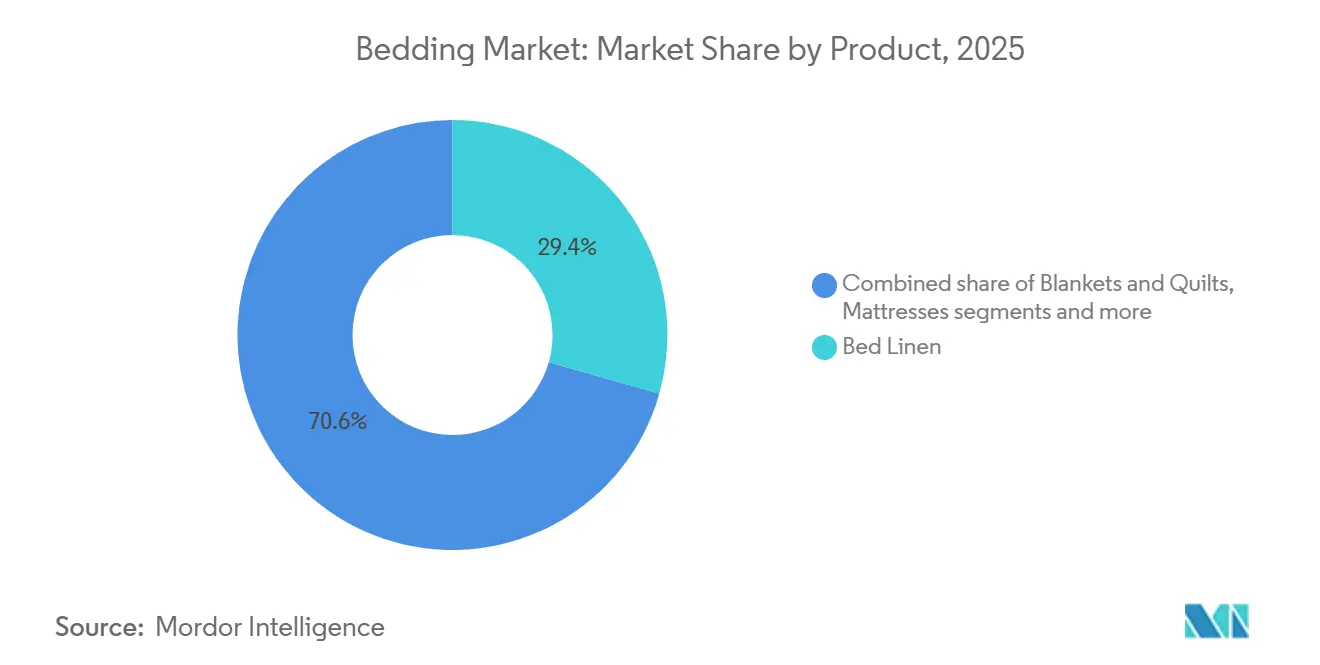

- By product category, bed linen led with 29.35% of the bedding market share in 2025, while mattress toppers and pads are projected to expand at a 7.14% CAGR through 2031.

- By end user, residential held 73.65% of the bedding market share in 2025, whereas commercial end users are projected to grow at a 6.88% CAGR through 2031.

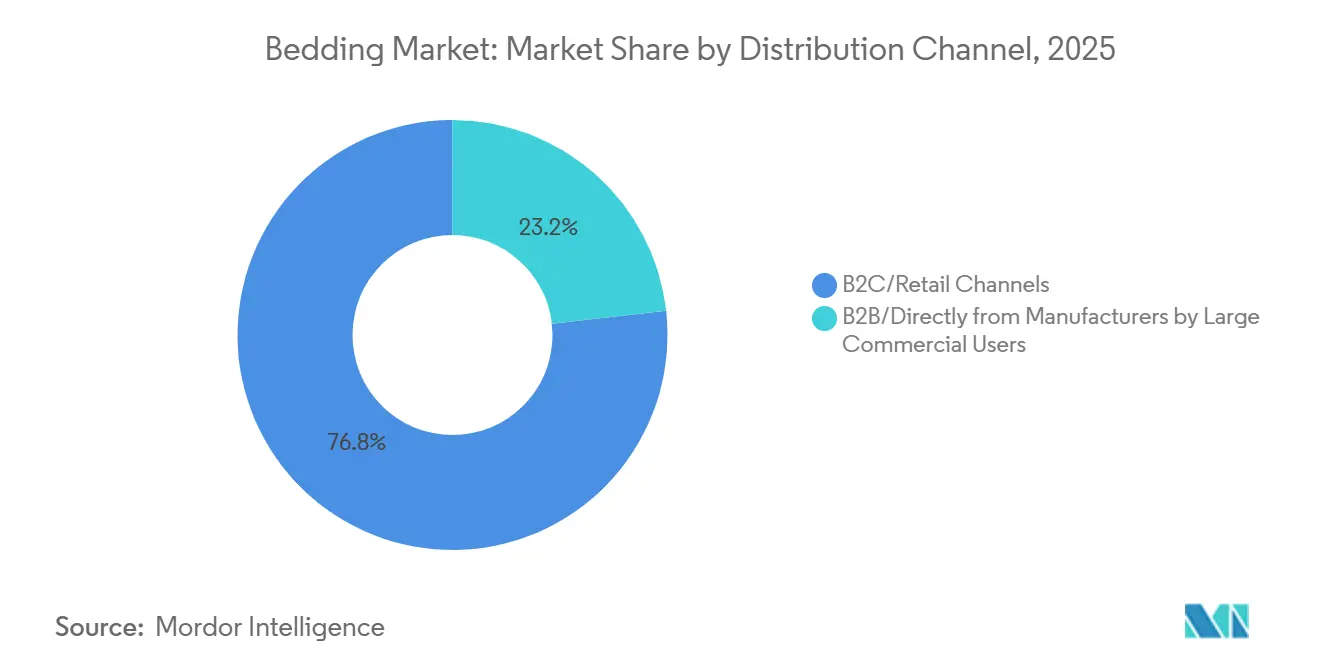

- By distribution channel, B2C retail commanded 76.80% of the bedding market share in 2025, while online B2C is projected to grow at a 7.92% CAGR through 2031.

- By geography, North America led with 32.60% of the bedding market share in 2025, while Asia-Pacific is projected to grow at a 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bedding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce and DTC penetration are raising access, assortment, and price transparency | +1.2% | Global, with North America and Asia-Pacific leading adoption | Short term (≤ 2 years) |

| Hospitality and healthcare refurbishment cycles sustaining B2B bedding replacement | +0.9% | North America & EU, Middle East, accelerating | Medium term (2-4 years) |

| Premiumization and sleep-health upgrades (cooling, ergonomic, smart features) | +1.4% | North America, Western Europe, and developed Asia-Pacific markets | Medium term (2-4 years) |

| Rising demand for certified sustainable textiles (organic, recycled, traceable) | +0.8% | EU leading with GOTS/OEKO-TEX, North America & Asia-Pacific catching up | Long term (≥ 4 years) |

| PFAS-free reformulation accelerating product refresh and certified alternatives | +0.7% | California, New York, the EU, including Denmark and France, and expanding to Canada and the United Kingdom. | Short term (≤ 2 years) |

| Mattress EPR rollouts nudging faster replacement and take-back partnerships | +0.6% | California, Connecticut, Rhode Island, and Oregon in the United States, and EU-wide by 2028 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce and DTC Penetration Raising Access, Assortment, and Price Transparency

The bedding market is shifting toward direct-to-consumer and e-commerce models that simplify discovery and compress legacy markups once tied to showroom negotiation. Direct-to-consumer and e-commerce channels now capture over USD 15 billion annually in the global bedding market, representing approximately 25% of total mattress sales. Online-first players have normalized transparent pricing, material disclosures, and returns policies, and that has nudged incumbents to adopt clearer specifications and consistent assortments[2]CSIL, “E-commerce in the Mattress Industry 2020-2025 | CSIL Report,” CSIL, worldfurnitureonline.com. Consumers now compare multiple brands in fewer clicks, a behavior that reduces friction and encourages premium feature upgrades when value stories are well presented. Omnichannel moves by scaled brands support these shifts, including store networks that double as last-mile hubs and experience centers for high-involvement products in the bedding market. The Somnigroup platform, formed in 2025, gave Tempur Sealy broader control over digital and physical touchpoints, which raised the bar on availability, delivery options, and post-purchase service across the bedding market.

Hospitality and Healthcare Refurbishment Cycles Sustaining B2B Bedding Replacement

Hotel soft goods bedding, pillows, towels wear out faster than case goods, triggering systematic replacement every 6-7 years under franchise brand Property Improvement Plans (PIPs), with Marriott mandating carpet refreshes every six years and upscale properties accelerating bedding cycles to 2-4 years in humid coastal markets where mold, UV fading, and occupancy stress compress lifespans[3]Arcedior, “Hotel Soft Goods Replacement Cycle with Timelines & Checklist,” Arcedior, arcedior.com. Upscale hotels in humid or high-occupancy locations often compress those cycles, which drives steady order cadence for certified materials and high-durability constructions. Procurement increasingly emphasizes proof of safety and environmental performance, which makes certifications and traceable inputs a requirement in many tenders. These cycles reduce volatility risk for suppliers and cushion volume during softer residential demand periods in the bedding market.

Premiumization and Sleep-Health Upgrades (Cooling, Ergonomic, Smart Features)

Premium features connected to comfort, cooling, ergonomics, and smart adjustability continue to gain traction as sleep-health awareness grows in 2026. Scaled brands are upgrading core lines and expanding price ladders to capture consumers who are willing to trade up for tangible performance gains. Tempur Sealy launched a refreshed Sealy Posturepedic lineup in early 2025 across multiple performance tiers and advanced bases that integrate guidance partnerships, signalling continued investment in product differentiation that sustains value growth in the bedding market[4]Tempur Sealy Newsroom, “Newsroom,” tempursealy.com, tempursealy.com. These offerings meet a clear use case for better temperature regulation, pressure relief, and motion isolation without requiring full bedroom overhauls. Combined with curated in-store experiences and digital education, these solutions help consumers justify higher ticket purchases in the bedding market.

Rising Demand for Certified Sustainable Textiles (Organic, Recycled, Traceable)

Buyers and procurement teams are aligning with certifications that verify material safety and environmental stewardship, which is reshaping sourcing decisions in the bedding market. OEKO-TEX 2024 updates lowered total fluorine limits and tightened input criteria, which have practical implications for mills and finishers supplying sheets, protectors, and quilts. The EU’s product policy framework is moving textiles toward durability, recycled content, and digital product passports, which will push home textiles toward more traceable designs over the second half of the decade. These signals encourage design-for-reuse practices and more modular constructions that work better with future EPR regimes. As a result, sustainability now functions as both a compliance requirement and a value driver in the bedding market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cotton, polyester, and foam chemical price volatility is squeezing margins | -0.6% | Global, with India, the United States, and Brazil, cotton producers are most exposed | Short term (≤ 2 years) |

| Intense private-label and DTC price competition is compressing ASPs | -0.8% | North America, EU online markets, spillover to Asia-Pacific | Medium term (2-4 years) |

| Compliance costs from mattress flammability and labeling norms (CPSC/others) | -0.3% | United States under CPSC, EU aligning standards | Medium term (2-4 years) |

| PFAS and circular-textiles rules are raising testing, traceability, and redesign costs | -0.5% | California and other States, and in the EU Denmark, and France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cotton, Polyester, and Foam Chemical Price Volatility Squeezing Margins

Cotton spot prices fell to USD 0.6182 per pound by late November 2025, a 12.86% year-on-year decline, which lowered input costs but also signaled future supply responses that can whipsaw procurement in the bedding market. Producers in the United States scaled back planted area and output during 2025, which sets up tighter conditions if demand rebounds faster than expected. Polyester and foam feedstocks remain tied to energy price cycles, which can move independently of natural fiber trends and complicate hedging strategies. Producer price data showed persistent upward pressure for mattresses since the pandemic, which reflects a mix of materials, logistics, and compliance costs that have not fully retraced. Demand-side signals were mixed in early 2025 as consumer confidence softened, but labor markets and wage growth remained supportive of essential purchases, a backdrop that requires careful inventory and pricing discipline in the bedding market.

Intense Private-Label and DTC Price Competition Compressing ASPs

Scale retailers and vertically integrated manufacturers used private-label strategies to set compelling entry and mid-tier price points, which puts pressure on branded ASPs in the bedding market. Association reporting documented regulatory concerns about steep and continuous discounting practices that can erode consumer trust, which has nudged some retailers toward clearer promotions and value messages. Independent testing commissioned by an industry group found that several low-cost imported mattress models failed the United States open-flame standard, and estimates suggested hundreds of thousands of such units were sold online over 2024-2025, underscoring compliance gaps that legitimate brands must compete against. The United States regulators also warned consumers in March 2025 about non-compliant imported mattresses sold via a large marketplace, which adds enforcement complexity and raises the cost of maintaining rigorous testing protocols for compliant producers. These conditions intensify price competition even as safety and documentation costs rise, which can compress margins without sufficient scale or a clearly differentiated offer in the bedding market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Mattress Toppers Retrofitting Existing Beds Faster Than Replacement Cycles

Bed linen accounted for 29.35% of category revenues in 2025, while mattress toppers and pads are projected to post the fastest growth at 7.14% CAGR through 2031 as cost-conscious households and hotels extend mattress life with targeted upgrades in the bedding market. This defer-and-upgrade pattern channels spending into cooling, pressure relief, and protection layers that deliver noticeable comfort gains without a full replacement cycle. Hybrid and foam technologies continue to shape mattress design with targeted zoning and motion control, and they also drive new requirements for modular construction that enables easier disassembly in the future. Material safety and performance verification through OEKO-TEX and related standards are now embedded in product development and supplier qualification across sheets, protectors, and quilts. The bedding market is therefore allocating more share of innovation to components that solve heat, hygiene, and pressure issues while keeping total ownership cost in check.

The bedding market also benefits from a wider range of certified inputs that address sustainability requirements in hotel RFPs and institutional tenders. Sheet and cover fabrics are being reformulated with finishes and constructions that maintain repellency and durability while meeting tighter fluorine content limits and chemical management criteria. Smart adjustability remains a premium niche that helps segment the offer and support halo effects across the portfolio. The bedding market size for mattress toppers and pads is projected to expand at a 7.14% CAGR to 2031 as consumers and operators use these SKUs to bridge comfort gaps and reduce the urgency of a full mattress purchase. This profile enables brands and retailers to position good-better-best assortments that meet different budget thresholds without sacrificing verifiable performance claims.

By End User: Commercial Segments Accelerate Replacement as PIPs Mandate Upgrades

Residential end users represented 73.65% of revenues in 2025, but commercial buyers are expected to increase purchasing at a 6.88% CAGR through 2031 as refurbishment cycles and compliance timelines tighten in hospitality and healthcare. Hotel brands refresh linens and soft goods on fixed timelines, which creates a dependable order cadence that can offset softer home spending phases in the bedding market. Healthcare and senior living facilities emphasize antimicrobial properties and consistent quality documentation, which increases the value of certified, traceable inputs and strengthens supplier switching costs. These needs also raise the importance of testing partnerships that deliver timely results on flammability and restricted substances for high-velocity SKUs.

Across commercial settings, the bedding market is moving toward designs that limit landfill disposal and support take-back programs in regions with EPR rules. EU policy continues to move toward collection, sorting, and recycling mandates for textiles, and that framework is shaping buying criteria in global hotel chains as they prepare for harmonized requirements. The bedding market size for commercial end users is projected to expand at a 6.88% CAGR through 2031 as operators prioritize products that combine durability with compliance-ready documentation. Together, these levers make the commercial channel a structural growth driver that is less sensitive to near-term consumer sentiment.

By Distribution Channel: Online B2C Eroding Brick-and-Mortar with 7.92% CAGR Surge

B2C retail accounted for 76.80% of bedding distribution in 2025, and online B2C is expected to grow at a 7.92% CAGR through 2031 as consumers embrace digital tools for discovery, comparison, and delivery in the bedding market. Brands that blend e-commerce with showrooms, pop-ups, or shop-in-shops are reducing return rates and improving attachment to high-margin accessories. The Somnigroup combination announced in 2025 highlights how scaled control of owned retail and digital assets can improve service levels and leverage data in merchandising and promotions. Alongside this, independent associations reported safety enforcement actions tied to imported mattresses that failed United States flammability rules, which underscores the role of trusted channels in compliance-sensitive categories. The bedding market is likely to see more curated digital experiences, faster delivery windows, and content-rich product storytelling as part of the path to purchase.

On the B2B side, large hotel and healthcare networks emphasize reliability, compliance support, and end-of-life options when selecting vendors. EU-aligned EPR frameworks will further incentivize take-back and refurbishment partnerships, and that encourages bedding market participants to re-engineer SKUs for easier disassembly. This will likely create new service revenue streams for firms that operate recycling or refurbishment logistics and can document carbon and waste savings. The bedding market remains competitive across channels, but the advantage is tilting toward players that align assortment, compliance, and omnichannel execution.

Geography Analysis

North America held 32.60% of the bedding market share in 2025, supported by a large installed base of hotel rooms, active refurbishment programs, and a robust premium segment that continued to invest in comfort and ergonomics. Energy-linked feedstocks influenced polyester and foam costs across 2025, and cotton price volatility added planning complexity for mills and brands serving bed linen and protectors in the bedding market. PFAS restrictions came into force in several states of the United States in 2025, which pushed manufacturers to introduce PFAS-free lines or reformulate repellents while maintaining durability targets. Extended producer responsibility programs for mattresses now operate across multiple States of the United States, and New York has set collection access and recycling rate milestones that will expand take-back coverage through the next decade. Consumer confidence softened in early 2025, though wage growth and employment trends remained supportive, which encouraged value-oriented upgrades rather than deferrals in many bedding market households.

Asia-Pacific is projected to be the fastest-growing region at a 7.05% CAGR to 2031 as digital-first models scale in key markets and middle-income households add premium features over baseline comfort. Manufacturers in India and Southeast Asia continue to enhance export competitiveness through deeper vertical integration, certifications, and selective near-market investments in support of global brands in the bedding market. As PFAS restrictions proliferate in the West, Asia-Pacific suppliers are aligning with international standards and third-party testing protocols to maintain continuity with United States and EU buyers. Japan and South Korea remain quality-focused with a tendency toward compact, well-specified solutions that include cooling and moisture management for small spaces. Australia, Singapore, and other hubs stand out for high hospitality standards and sustainability criteria that influence regional procurement for the bedding market.

Europe balances strict environmental policy leadership with an uneven macro backdrop, and that mix shapes purchasing decisions in both consumer and commercial segments of the bedding market. The EU’s revised rules for textile waste and extended producer responsibility set the stage for national schemes to be operational by 2028, with eco-modulated fees that encourage durability and recyclability in home textiles. France enacted a national PFAS ban for textiles starting in 2026 with staged expansions to 2030, while Denmark adopted a total fluorine threshold for PFAS in clothing and certain consumer products from mid-2026, creating a regulatory cluster that bedding suppliers serving the region must meet. The European Commission highlighted the long-term costs of PFAS pollution, which reinforces the political momentum for a broader restriction proposal under REACH and supports rapid market transitions to alternative finishes.

Competitive Landscape

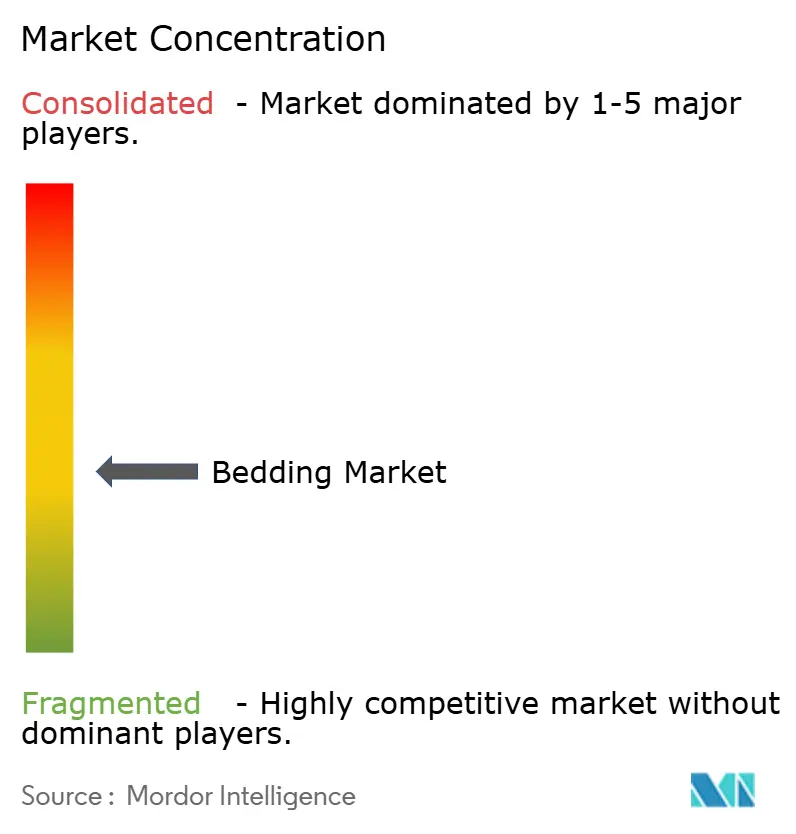

The bedding market remains moderately fragmented despite several scaled players that control manufacturing, brands, and retail networks. The long tail of regional producers and private-label programs keeps pricing competitive and increases the importance of clear performance claims and trusted distribution. The 2025 creation of Somnigroup through Tempur Sealy’s acquisition of Mattress Firm consolidated a large omnichannel footprint and gave the combined business more direct control over consumer experience and last-mile fulfillment in the bedding market. This move signaled to peers that scale and integration would be necessary to protect share as DTC models mature. Competitive intensity is likely to persist as brands compete on experience, convenience, and verified performance.

Operational execution is a key differentiator as firms balance product innovation with cost discipline and channel strategy in the bedding market. Sleep Number emphasized brand visibility and portfolio resets in 2026, including a high-profile partnership and new value-aligned products to counter a tough 2025 financial base. Purple Innovation highlighted independent lab findings for its latest mattress collections in late 2025, using third-party validation to cut through a crowded field of similar claims. These strategic moves reflect a wider industry pattern that favors manufacturers able to back claims with data, support omnichannel journeys, and deliver reliable after-sales service in the bedding market. Scale players retain advantages in procurement and testing that can be difficult for smaller firms to match.

Compliance and sustainability are creating entry barriers that favor better-capitalized operators in the bedding market. United States flammability rules require documented prototype testing and labeling, which adds ongoing costs for each construction change and is enforced on imported and domestic goods. PFAS-related restrictions and voluntary limits require analytical testing at low detection thresholds, often across multiple components, which meaningfully raises cost and cycle time for new product introductions. EPR programs for mattresses are scaling in the United States, and they are moving toward national coverage in the EU, which pushes producers to plan for take-back, sorting, and recycling fees tied to durability and recyclability. Companies that invest early in modular designs and closed-loop materials will be better positioned as these rules harden in the bedding market.

Bedding Industry Leaders

Tempur Sealy International, Inc.

Serta Simmons Bedding LLC

Sleep Number Corporation

Hilding Anders

Welspun Living Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sleep Number Corporation welcomed Travis Kelce as a strategic partner and investor, amplifying brand visibility and signaling a celebrity-endorsement pivot to counteract competitive pressure from Tempur Sealy's Mattress Firm acquisition. The company also introduced the ComfortMode Mattress, offering premium comfort at an affordable price, and released a new campaign focusing on personalized comfort

- December 2025: Purple Innovation announced independent validation studies conducted by SleepScore Labs showing its Essential and Restore mattress collections (featuring GelFlex Grid technology) reduced self-reported pain by 68% and 63% respectively, with Restore users spending 3.5 hours more in deep sleep per month and reporting a 204% increase in ability to sleep through the night without tossing and turning. These clinically validated claims differentiate Purple in a commoditized market where most brands rely on anecdotal testimonials rather than third-party sleep lab data.

- August 2025: Eight Sleep, the smart mattress company backed by Mark Zuckerberg and Elon Musk, raised USD 100 million in Series D funding from strategic investors, signaling venture capital's continued bet on sleep-tech despite broader tech slowdown.

- February 2025: Tempur Sealy International completed its acquisition of Mattress Firm Group Inc. for approximately USD 5 billion (USD 2.7 billion cash, 34.2 million shares), creating Somnigroup International Inc. (NYSE: SGI) with pro-forma sales of USD 8 billion over the twelve months ending December 31, 2024, net of intercompany sales (85% North America, 15% international, 65% direct-to-consumer, 35% third-party retailers). The company expects to divest 73 Mattress Firm retail locations and its Sleep Outfitters subsidiary (103 specialty mattress retail locations, seven distribution centers) to Mattress Warehouse in Q2 2025.

Global Bedding Market Report Scope

The bedding market is a large and diverse industry that includes a wide range of products such as sheets, pillows, blankets, duvets, and mattresses. The report gives a full background analysis of the global bedding market, including a look at the market as a whole, new trends by segment and regional market, and major changes in market dynamics.

The bedding market is segmented by type, distribution channel, and geography. By type, the market is sub-segmented into home bedding and hotel bedding. By distribution channel, the market is sub-segmented into supermarkets/hypermarkets, specialty stores, online, and other distribution channels. By geography, the market is sub-segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The report offers the market sizes and forecasts in value (USD) for all the above segments.

| Bed Linen |

| Pillows and Pillowcases |

| Blankets & Quilts |

| Mattresses |

| Mattress Toppers & Pads |

| Other Products |

| Residential | |

| Commercial | Hospitality (Hotels & Resorts) |

| Healthcare & Elderly-care Facilities | |

| Institutional (Dorms, Military, etc.) | |

| Other Commercial End Users |

| B2C / Retail Channels | Multi-Brand Stores |

| Specialty Bedding Stores (including Exclusive Brand Outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly from Manufacturers by Large Commercial Users |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product | Bed Linen | |

| Pillows and Pillowcases | ||

| Blankets & Quilts | ||

| Mattresses | ||

| Mattress Toppers & Pads | ||

| Other Products | ||

| By End User | Residential | |

| Commercial | Hospitality (Hotels & Resorts) | |

| Healthcare & Elderly-care Facilities | ||

| Institutional (Dorms, Military, etc.) | ||

| Other Commercial End Users | ||

| By Distribution Channel | B2C / Retail Channels | Multi-Brand Stores |

| Specialty Bedding Stores (including Exclusive Brand Outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly from Manufacturers by Large Commercial Users | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the bedding market through 2031?

The bedding market size is expected to grow from USD 144.43 billion in 2025 to USD 153.12 billion in 2026 and reach USD 205.05 billion by 2031, reflecting a 6.01% CAGR over 2026-2031.

Which product categories will lead to value growth in the bedding market by 2031?

Mattress toppers and pads are projected to be the fastest-growing category at a 7.14% CAGR through 2031 as buyers extend mattress life with targeted comfort and protection upgrades.

How are regulations shaping product design and sourcing in the bedding market?

PFAS restrictions, tighter OEKO-TEX limits, and expanding EPR rules are pushing PFAS-free finishes, traceable inputs, and modular constructions that enable collection, sorting, and recycling.

Which regions are set to grow fastest and why?

Asia-Pacific is projected to expand at a 7.05% CAGR through 2031, supported by digital-first models, rising middle-income households, and suppliers aligning with international standards.

What channels are gaining share in the bedding market?

Online B2C is projected to grow at a 7.92% CAGR through 2031 as brands blend digital discovery with showrooms and faster delivery to improve experience and reduce returns.

What are the key risks to margins for bedding suppliers in 2026?

Volatile input costs across cotton, polyester, and foam chemicals, plus compliance expenses tied to flammability and PFAS testing, create cost pressures that require scale and strong execution.

Page last updated on: