Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 4.28 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

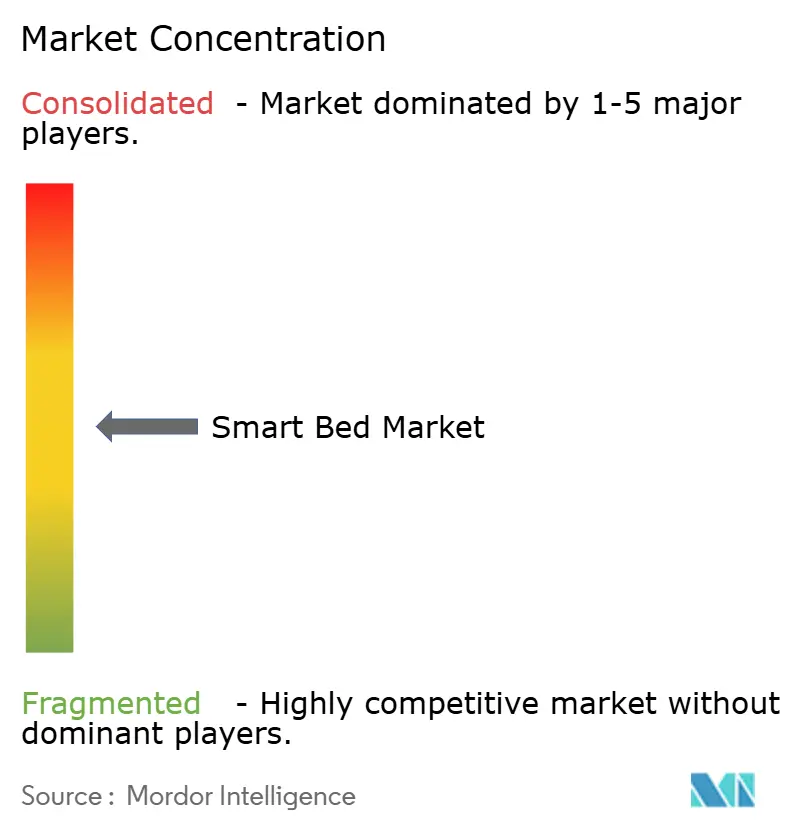

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smart Bed Market Analysis by Mordor Intelligence

The smart bed market size in 2026 is estimated at USD 3.37 billion, growing from 2025 value of USD 3.21 billion with 2031 projections showing USD 4.28 billion, growing at 4.92% CAGR over 2026-2031. Heightened interest in connected wellness, the rollout of IoT infrastructure across healthcare settings, and rapid innovation in sensor technology are moving smart beds from novelty status to mainstream healthcare and consumer products. Large hospital networks see the beds as a pathway to lower readmissions, while wellness-focused households view them as an everyday health hub. Manufacturers are capturing new revenue by bundling software subscriptions that unlock analytics and personalized sleep coaching, and by tailoring integration kits that connect directly to hospital electronic medical records. Competitive intensity is rising as medical-grade incumbents, consumer electronics brands, and smart-home platforms all target the same opportunity, prompting faster product cycles and richer feature sets that make the smart bed market one of the most dynamic segments of connected health equipment.

Key Report Takeaways

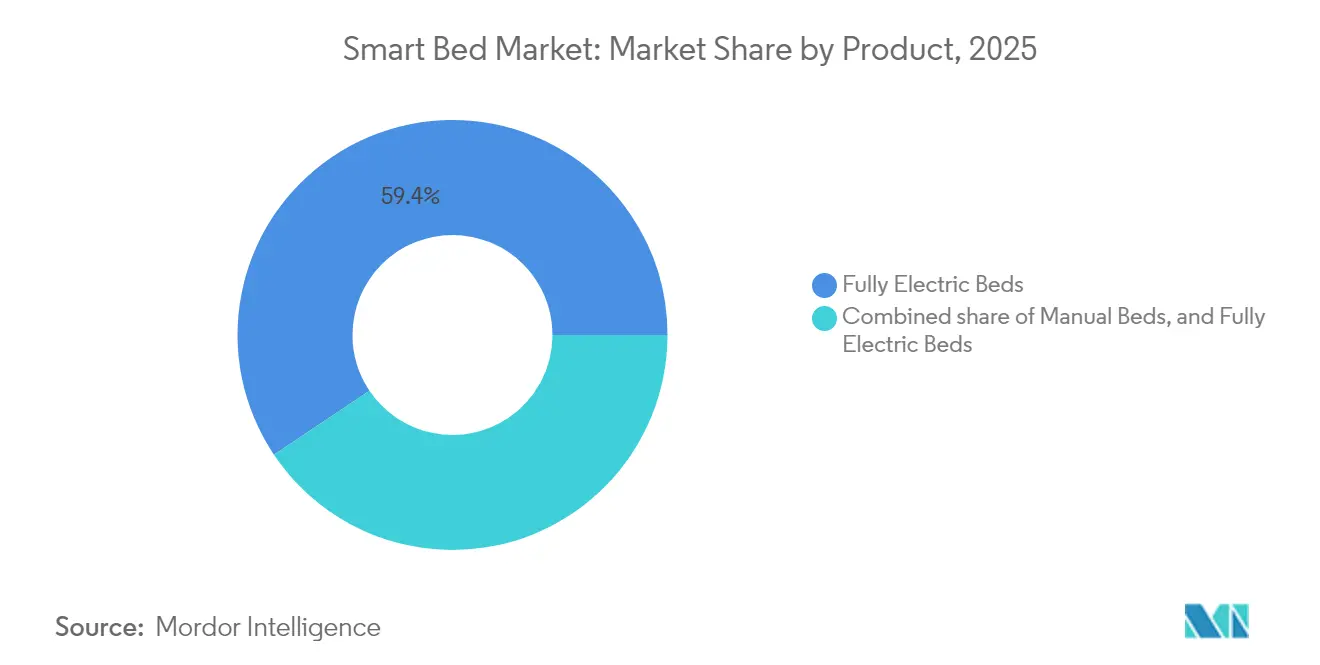

- By product category, fully electric beds led with 59.40% revenue share in 2025, while the segment is advancing at a 4.55% CAGR through 2031.

- By end-user, the commercial segment held 64.30% of the smart bed market share in 2025; the residential segment is projected to expand at a 5.95% CAGR between 2026-2031.

- By distribution channel, the B2B/Projects segment accounted for 39.30% of 2025 revenue, but the B2C channel is forecast to grow the quickest at a 6.45% CAGR to 2031.

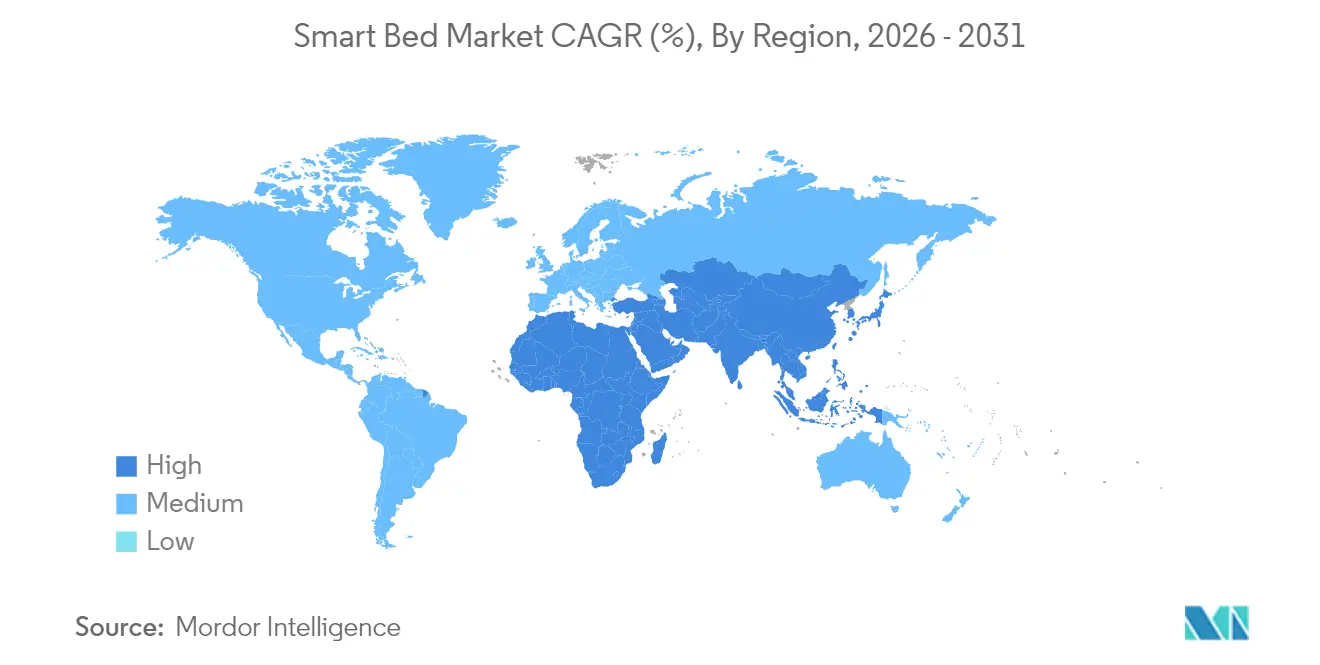

- By geography, North America commanded 41.60% of the smart bed market size in 2025, while Asia-Pacific is poised for the fastest expansion at a 6.15% CAGR during the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Bed Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IoT-enabled Post-Acute-Care Adoption | +1.2% | North America, Europe | Medium term (2-4 years) |

| Premium-Hotel Deployment of Smart Adjustable Beds in Luxury Hospitality | +0.8% | Global, with a concentration in North America, Europe, and Asia-Pacific luxury markets | Short term (≤ 2 years) |

| Aging Population & Governments' Health Directives Driving Bed Upgrades in Long-Term Care | +1.4% | Japan, Europe, North America | Long term (≥ 4 years) |

| E-commerce-led AI Sleep-Tracking Bed Sales Surge in China & South Korea | +0.6% | China, South Korea, Southeast Asia | Short term (≤ 2 years) |

| Hospital EMR Integration of Smart-Bed APIs: Automating Vital-Signs Capture | +0.9% | North America, Europe | Medium term (2-4 years) |

| Growing Expenditures in Sleep Technology | +0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IoT-enabled Post-Acute-Care Adoption

Smart beds are redefining how caregivers keep tabs on patients once they leave the acute ward. Built-in sensors track heart rate, breathing, movement, and sleep quality, then stream that information straight into hospital records under the ISO/IEEE 11073-10206 interoperability standard [1]H. Daanen et al., “Wireless Biomonitoring Architecture for Smart Beds,” Springer, springer.com. A 2024 multi-facility pilot—designed to test whether round-the-clock, bed-based monitoring could cut 30-day returns—found that the connected-bed cohort recorded a 23% drop in readmissions compared with matched patients treated the previous year. Researchers aimed to determine whether real-time alerts would let clinicians intervene at the first sign of trouble rather than waiting for scheduled vital-sign rounds. Parallel work published the same year showed that wireless biomonitoring hardware can replace tethered leads, giving patients more freedom of movement while still feeding continuous data back to the care team [2]ISO. "ISO/IEEE FDIS 11073-10206." sls.se. Taken together, these results point to a care model where proactive alerts—not readmission paperwork—drive the workflow, all while meeting FDA device guidelines for safety and data integrity.

Premium-Hotel Deployment of Smart Adjustable Beds

Boutique hotels and marquee city properties are re-imagining sleep as a revenue lever, integrating connected beds that automatically fine-tune firmness, surface temperature, and lumbar support to each guest’s circadian rhythm. Properties report nightly rate uplifts of up to 15% after introducing the technology, supported by in-app check-in that stores preferred sleep settings across chains. The adoption curve is steepest in boutique resorts, where unique wellness features translate quickly into higher booking rates and stronger satisfaction scores, confirming that experience, not price, is steering the premium end of the market [3]EHL Hospitality Insights. "Key Hospitality Technology Trends to Watch in 2025." ehl.edu. Cloud-based fleet dashboards also help operators schedule predictive maintenance, extending asset life and protecting brand consistency. Short payback periods are fueling rollouts across Asia-Pacific resort destinations and European wellness retreats, giving the smart bed market a vibrant premium-commercial subsegment that thrives on experiential differentiation rather than cost competition.

Aging Population and Government Health Directives

Policy makers in Japan, France, and several US states are incentivizing care homes to digitally monitor residents as staffing shortages intensify. Smart beds equipped with fall-detection and incontinence alerts reduce manual rounds, freeing caregivers for high-touch tasks. Government subsidies for technology that promotes aging-in-place are pushing adoption beyond institutional settings into private homes for seniors, widening the smart bed market. Manufacturers respond with models that integrate lift-assist rails, voice-activated adjustments, and emergency call routing. These elder-care features are increasingly standard rather than optional, supporting long-term demand that outlasts short equipment refresh cycles.

E-commerce-led AI Sleep-Tracking Bed Sales

Online marketplaces in China and South Korea accelerate consumer uptake by removing retail mark-ups and providing instant access to firmware upgrades. Brands collect granular usage data that feeds algorithm improvements, creating a feedback loop that drives annual product refreshes. Social-commerce livestreams demonstrate real-time pressure mapping and smart-home integrations, converting viewers into buyers within minutes. Low-barrier logistics and transparent pricing shrink go-to-market costs, enabling smaller entrants to test features such as real-time posture coaching and edge-processed snore suppression. This agile channel is now the fastest contributor to absolute unit volume growth, keeping the smart bed market firmly on its innovation edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-Hospital Budget Freezes Delaying Replacement Cycles | -0.7% | Europe, North America | Medium term (2-4 years) |

| GDPR-Driven Cloud-Connectivity Compliance Costs | -0.5% | Europe, with global implications for multinational vendors | Short term (≤ 2 years) |

| Humidity-Induced Sensor Failure Rates | -0.3% | Global, with higher impact in tropical and subtropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Public-Hospital Budget Freezes Delaying Replacement Cycles

Fiscal pressures stemming from pandemic aftershocks compel European and North American public systems to stretch bed lifespans up to 15 years. Aging fleets lack modern sensors and cannot connect to electronic records, widening the gap between public wards and privately funded facilities. Manufacturers now market retrofit sensor mats and clip-on gateways, but these partial fixes capture only basic vitals and omit software-driven comfort features. The resulting two-tier environment slows volume growth in the largest institutional buyer segment, although it also spurs innovation in modular add-ons that can later be migrated to full smart frames.

General Data Protection Regulation (GDPR)-Driven Cloud-Connectivity Compliance Costs

Biometric data streaming from smart beds qualifies as sensitive information under the General Data Protection Regulation (GDPR), requiring end-to-end encryption, granular consent workflows, and data minimization. Compliance engineering absorbs significant R&D resources, adding cost and prolonging certification cycles. Smaller firms with minimal legal infrastructure face barriers that limit European launches, consolidating bargaining power among established players. Edge analytics designs that process data locally and transmit only summaries gain traction as a compliance workaround, but add bill-of-materials expense, squeezing margins in price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Fully Electric Beds Remain the Innovation Core

Fully electric models controlled 59.40% of 2025 revenue and anchor the smart bed market because their multi-axis motors support automated anti-pressure-injury routines and effortless patient mobilization. This segment is forecast to expand to a 4.55% CAGR, adding connectivity layers such as voice assistants and health-record APIs that transform beds into care platforms. Integrated micro-controllers now enable millisecond-level pressure redistribution, and embedded RFID coils capture sleep posture data validated for sleep-apnea screening. The result is enhanced clinical utility that justifies premium pricing in hospitals and delivers tangible wellness benefits in homes.

Semi-electric designs offer electric back and knee articulation but retain manual height cranks, positioning them for price-sensitive buyers in emerging markets or cash-strapped long-term care facilities. Manual frames persist where grid power is unreliable or regulatory rules restrict electrified furniture. While these lower-spec categories provide entry points, innovation continues to cluster inside fully electric portfolios where firmware upgrades unlock recurring revenue. Consequently, manufacturers prioritize software scalability and modular sensor bays that future-proof new shipments, reinforcing the smart bed market’s steady migration toward fully digital architectures.

By End User: Commercial Buyers Drive Early Scale

Commercial end-user accounts for 64.30% of revenue in 2025 in the smart bed market. Clinical purchasers cite up to 30% reductions in hospital-acquired pressure ulcers after adoption, a quality metric that ties directly to reimbursement. Long-term-care operators embrace occupancy sensors that signal when residents attempt unsupervised transfers, reducing fall rates and satisfying insurer mandates. Hotel groups leverage connected beds to elevate guest experience analytics, tracking comfort settings that support loyalty-program personalization.

The residential segment is scaling faster, posting a 5.95% CAGR forecast as wellness-focused households seek quantifiable sleep gains. Eight Sleep’s Pod 5 claims a 34% boost in deep-sleep minutes and a 44% snore reduction, and early adopters share metrics on social media, generating organic demand. Consumer-grade platforms place equal weight on comfort, data, and aesthetic integration with smart-home ecosystems. Cross-segment learning accelerates feature transfer; for example, hospital-grade pressure-injury prevention algorithms migrate into high-end consumer lines, while home-oriented voice control moves upstream into post-acute-care suites.

By Distribution Channel: Digital First Strategies Redefine Reach

Omnichannel strategies anchor growth, but the direct-to-consumer path is the fastest, with B2C revenue expected to climb at a 6.45% CAGR. Online flagships and third-party marketplaces slash dealer mark-ups, letting brands reinvest in firmware updates and sleep-coaching subscriptions. Virtual showrooms with augmented-reality overlays illustrate bed articulation and night-time temperature graphs, shortening the buyer journey from research to checkout. MLILY’s Zero-Pressure model topped Tmall’s smart mattress rankings within six months of launch, demonstrating the velocity possible when high-engagement livestreams meet warehouse-to-door logistics.

B2B negotiations frequently include integration pilots, training packages, and multi-year maintenance, raising deal value but lengthening sales cycles. Rauland’s vendor integration program simplifies hospital IT approval by certifying bed-to-nurse-call links and EMR handshakes, reducing installation risk. Specialty furniture stores and home centers continue to serve clients who need in-person demonstrations or white-glove delivery, keeping offline channels relevant even as e-commerce volumes swell. The interplay of digital scale and localized service elevates the smart bed market’s competitive bar for customer experience.

Geography Analysis

North America commanded 41.60% of 2025 revenue, propelled by advanced care-delivery infrastructure, payer incentives that reward fall-prevention technology, and high discretionary spending on at-home wellness devices. Integrated EMR environments accelerate institutional adoption because procurement committees can quantify nursing-hour savings and shorter lengths of stay. High-income households embrace premium adjustable bases that sync with wearables, expanding the region’s cross-segment usage footprint. Canada mirrors the United States but on a smaller scale, and Mexico shows momentum in private tertiary hospitals and coastal resort corridors.

Asia-Pacific is the fastest-growing territory, posting a 6.15% CAGR forecast that reflects rising urban incomes and the ubiquity of mobile commerce. In China, 64% of residents expressed sleep-quality concerns, steering them toward algorithm-guided bedding that slots into existing smart-home ecosystems. Brands leverage direct-to-consumer apps to roll out firmware updates, addressing newly identified snoring patterns and boosting user retention. South Korea’s tech-forward culture fuels rapid uptake of AI-driven sleep coaching, while Japan’s aging society spurs demand for beds that flag nocturnal bathroom trips and trigger caregiver alerts. India edges forward as premium urban consumers purchase imported wireless monitoring frames, and Australia leads per-capita adoption through insurer-funded home tele-health pilots.

Europe maintains solid volume anchored in Germany, France, and the United Kingdom, each balancing healthcare innovation with strict data-governance mandates. GDPR builds trust among users but slows time-to-market for upgrades that rely on cloud analytics. Nordic countries register the highest household penetration, reflecting broad acceptance of smart-home devices and state-backed programs that reimburse sleep-health interventions. Southern Europe shows hospitality-led growth as upscale resorts use connected bedding to differentiate room categories. Public-sector budget caps, however, delay hospital refresh cycles, prompting manufacturers to push retrofit sensor kits that extend legacy assets while preserving care-quality gains.

Competitive Landscape

Competitive intensity is climbing as legacy medical-equipment firms, consumer-electronics giants, and smart-home disruptors converge on overlapping use cases. Hill-Rom Holdings Inc. and Stryker Corporation maintain hospital shares through life-cycle service contracts and clinical-evidence dossiers that resonate with purchasing committees. Eight Sleep and Sleep Number dominate US consumer mindshare via subscription-based coaching and national advertising that stresses measurable performance. Arjo AB leverages ergonomic heritage to tailor bariatric and geriatric lines, while LINET’s RTLS asset-tracking layer appeals to health-system supply-chain leaders.

Strategic partnerships flourish. Sensor start-ups embed hardware inside established frames, while analytics firms convert raw signals into actionable dashboards that rival stand-alone patient-monitoring systems. The RFID-embedded mattress prototype published in Nature confirms academic-industry collaboration that channels peer-review rigor into commercial roadmaps. Asian electronics majors such as Xiaomi and Huawei bundle connected bed bases into larger smart-home kits, winning first-time buyers who prefer a single-brand ecosystem. Mid-market opportunities remain relatively open; firms that deliver hospital-grade safety at near-consumer price points could unlock sizable untapped demand in private elder-care centers and four-star hotels.

Software now dictates differentiation more than mechanics. Over-the-air updates add respiratory-rate analytics or new comfort modes without altering hardware, driving recurring revenue that boosts valuation multiples. Competitive pitch decks emphasize total cost of ownership and integration depth rather than initial sticker price. With the standardization of smart bed features, market dominance will likely favor companies that prioritize brand strength, exceptional customer support, stringent data privacy, and the creation of integrated ecosystems—melding hardware, software, and services. This evolution underscores the importance of cultivating enduring customer relationships and trust, rather than merely competing on technical specs.

Smart Bed Industry Leaders

-

Stryker Corporation

-

Sleep Number Corporation

-

Hill-Rom Holdings Inc.

-

Paramount Bed Co., Ltd.

-

Arjo AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: LINET Group announced its participation in EBME Expo 2025, showcasing the LINET Smart Tracking system that uses RTLS for real-time visibility of bed fleets, improving workflow optimization for hospitals.

- October 2024: UC Davis Health unveiled the Interactive Care Platform, integrating unobtrusive sensors to monitor routines and health data for older adults while maintaining privacy protections.

- June 2024: Sleep Number introduced the c1 smart bed, offering affordable smart adjustability to broaden market reach while keeping core connectivity features.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the smart bed market as network-enabled bed frames, mattresses, and integrated sleep systems that embed sensors, micro-controllers, and wireless modules to capture user or patient data and then adjust posture, firmness, temperature, or safety rails automatically. We track units sold to households, hospitals, long-term-care centers, and hotels whenever the bed exchanges data in real time or through cloud dashboards.

Scope Exclusion: Devices lacking connectivity, ordinary adjustable bases, and wearable sleep trackers lie outside this scope.

Segmentation Overview

-

By Product

- Manual Beds

- Semi-Electric Beds

- Fully Electric Beds

-

By End User

- Residential

-

Commercial

- Hospitals

- Long-Term-Care Facilities

- Home-Healthcare Settings

- Hotels & Resorts

- Others

-

By Distribution Channel

-

B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B/Projects (directly to businesses)

-

B2C/Retail

-

By Geography

-

North America

- Canada

- United States

- Mexico

-

South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

-

Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

-

Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed hospital procurement heads in the United States and Germany, hospitality operations managers in Japan and the United Arab Emirates, and product engineers at leading smart-bed manufacturers. Insights on installation rates, discount structures, and next-generation feature roadmaps were used to validate and refine model inputs.

Desk Research

We began by pooling customs records for hospital beds from UN Comtrade, smart-home adoption figures from the International Energy Agency, sleep-disorder prevalence from the World Health Organization, and aging curves from United Nations databases. According to Mordor Intelligence analysts, company 10-Ks, investor decks, and papers from the National Sleep Foundation and the Healthcare Information and Management Systems Society helped us map pricing ladders and buying cycles.

Paid repositories inside D&B Hoovers and Questel supplied revenue splits and patent activity, letting our team benchmark innovation intensity and average selling price shifts. This list is illustrative only, and many other open portals and corporate filings fed additional cross-checks.

Market-Sizing & Forecasting

A top-down build starts with the installed base of hospital beds and annual household mattress replacements, is multiplied by verified smart penetration rates and average selling prices, and is then fine-tuned through supplier roll-ups and channel surveys. Key variables include replacement cycles, connected-home adoption, sensor cost curves, reimbursement rules for remote patient monitoring, and premium hotel renovation budgets. We forecast with multivariate regression, adding scenario analysis when penetration or prices deviate from trend.

Data Validation & Update Cycle

Outputs pass three analyst reviews that compare modeled revenue with shipment tallies and public earnings before sign-off. Reports refresh each year, with interim tweaks when material events such as reimbursement changes arise.

Why Mordor's Smart Bed Baseline Commands Reliability

Published estimates often diverge because firms select different product mixes, pricing points, and refresh cadences; we anchor ours to clear scope and annually updated drivers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.21 B (2025) | Mordor Intelligence | |

| USD 2.59 B (2023) | Global Consultancy A | Excludes hospitality units and software revenue |

| USD 3.77 B (2024) | International Data Firm B | Aggressive ASPs and counts smart mattresses outside bed-frame scope |

| USD 3.16 B (2024) | Regional Association C | Hospital-only sample and older currency rates |

These comparisons show that our disciplined scope selection and annual refresh give decision-makers a balanced, transparent baseline traceable to clear drivers and repeatable steps.

Key Questions Answered in the Report

What is the current size of the smart bed market?

The smart bed market is valued at USD 3.37 billion in 2026 and is forecast to reach USD 4.28 billion by 2031.

How fast is the market expected to grow?

Industry revenue is projected to advance at a 4.92% CAGR during 2026-2031, reflecting steady demand from hospitals, hotels, and wellness-focused households.

Which product segment holds the largest revenue share?

Fully electric beds led with 59.40% of 2025 revenue thanks to multi-axis adjustability and built-in sensors that support pressure-injury prevention and sleep analytics.

Which region will see the fastest growth?

Asia-Pacific is set to expand at a 6.15% CAGR through 2031, buoyed by rising healthcare spending, strong e-commerce channels, and high consumer interest in sleep technology.

Page last updated on: