Heated Mattress Pads Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

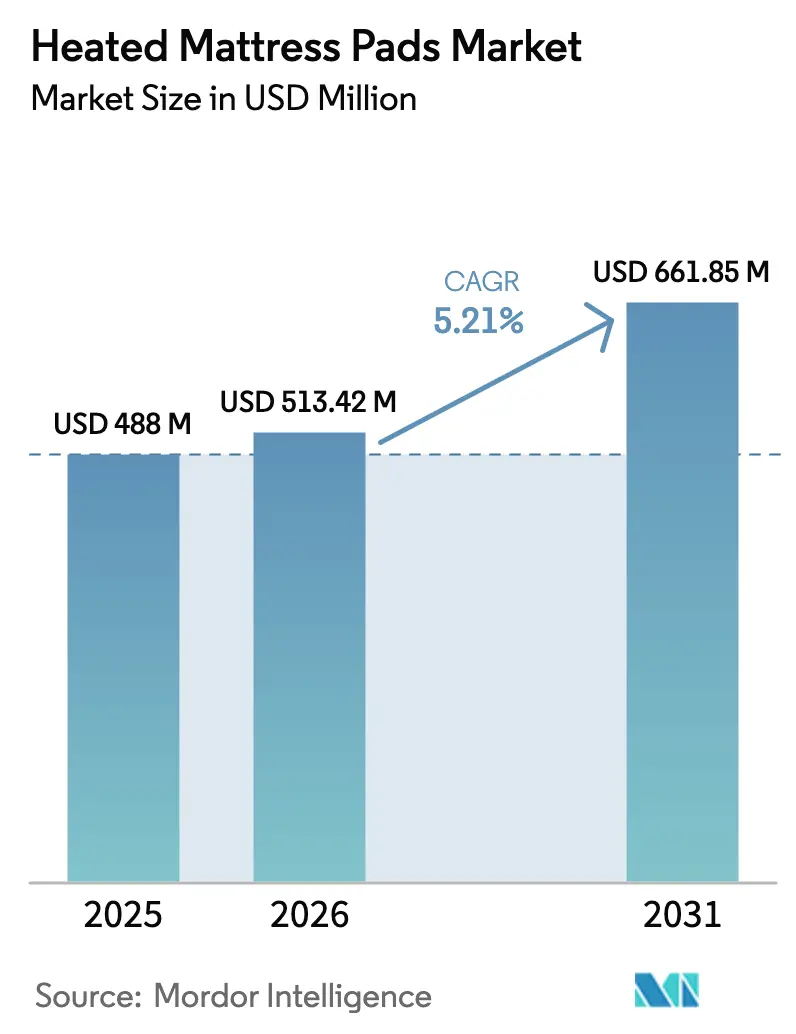

| Market Size (2026) | USD 513.42 Million |

| Market Size (2031) | USD 661.85 Million |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heated Mattress Pads Market Analysis by Mordor Intelligence

The heated mattress pads market size was valued at USD 488 million in 2025 and estimated to grow from USD 513.42 million in 2026 to reach USD 661.85 million by 2031, at a CAGR of 5.21% during the forecast period (2026-2031). Demand is climbing as more consumers turn to at-home heat therapy for arthritis, lower-back pain, and similar chronic conditions that often intensify during the night. Energy-conscious households in cold climates view low-wattage bedding as a practical alternative to whole-room heating, and product innovation from dual-zone controls to smartphone app operation continues to widen mainstream appeal. Established brands leverage safety certifications and extensive retail distribution to reinforce trust, while new entrants rely on advanced heating elements and direct-to-consumer outreach to gain ground. Stricter flammability rules raise compliance costs, yet they also create barriers that shield incumbents with proven safety records.

Key Report Takeaways

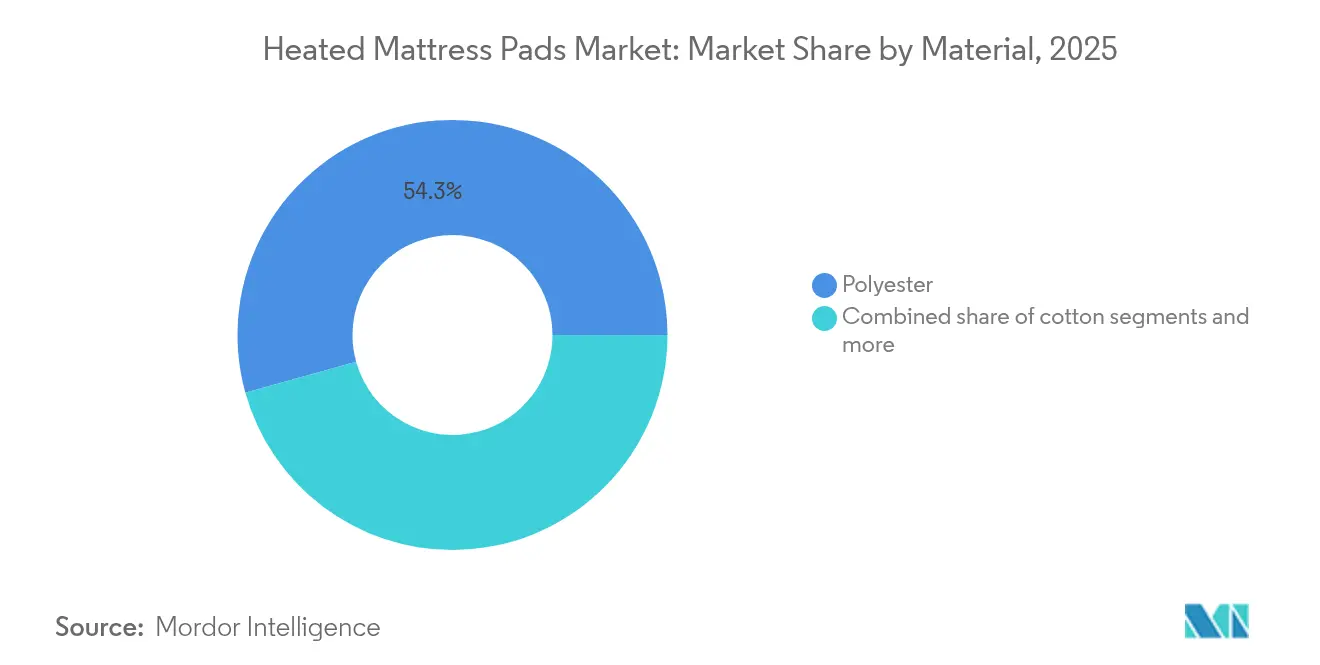

- By material, polyester led with 54.32% of the heated mattress pads market share in 2025, while organic materials are forecast to expand at a 6.27% CAGR through 2031.

- By size, queen-size products accounted for 37.45% of 2025 revenue; adjustable sizes are poised to grow at a 5.89% CAGR to 2031.

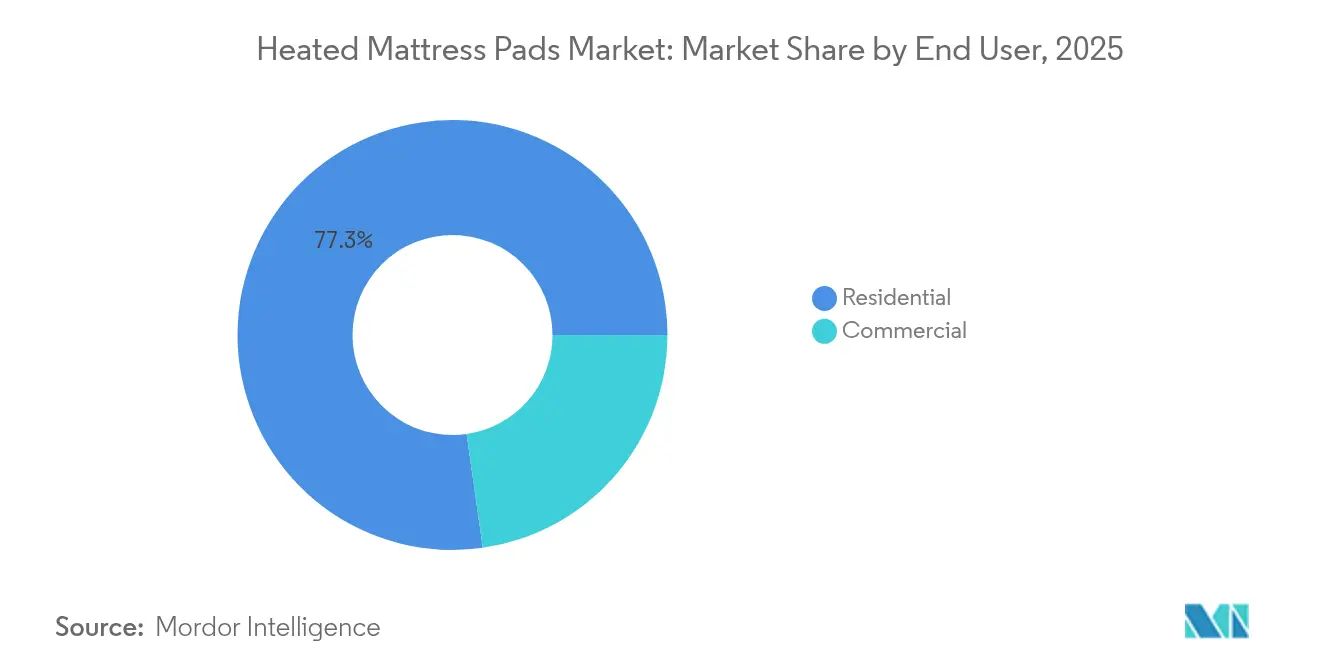

- By end user, the residential segment captured 77.25% of 2025 sales; commercial deployments are projected to rise at a 6.43% CAGR on the back of hospital and hospitality demand.

- By distribution channel, B2C retail held 81.10% share in 2025, with B2C online channels recording a 6.92% CAGR outlook.

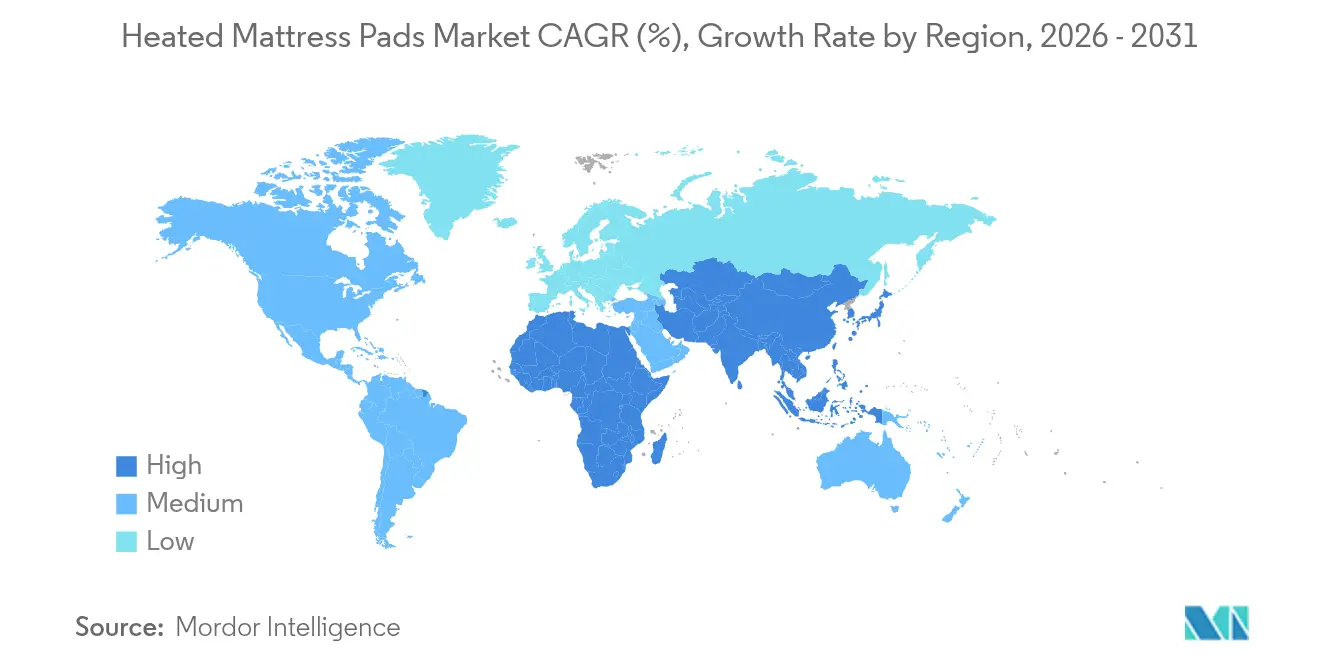

- Regionally, North America commanded a 46.35% revenue share in 2025, whereas Asia-Pacific is projected to register the fastest 5.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Heated Mattress Pads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Personalized Sleep Comfort and Convenience | +1.2% | Global, with premium adoption in North America and EU | Medium term (2-4 years) |

| Rising Prevalence of Chronic Pain Requiring Heat Therapy | +1.8% | Global, concentrated in aging populations of developed markets | Long term (≥ 4 years) |

| Expansion Of E-Commerce and DTC Channels | +1.0% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Adoption Of Energy-Efficient Carbon-Fiber and Graphene Heaters | +0.9% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Cold-Climate Energy-Subsidy Programs for Low-Wattage Bedding | +0.4% | Northern regions of North America, Europe, and Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Personalized Sleep Comfort & Convenience

Thermal individualization has become central to sleep product selection, and the heated mattress pads offer dual-zone systems that let bed partners maintain separate temperatures. Women tend to prefer slightly warmer beds than men, and benefit from programmable controls that fine-tune heat across sleep stages. Many models integrate with smartphones, smart speakers, and home automation hubs, shrinking the gap between affordable mattress pads and high-priced climate-controlled smart beds. Products with timers and automatic shut-off features appeal to safety-conscious households, while washable designs remove maintenance barriers that once limited adoption.

Rising Prevalence of Chronic Pain Requiring Heat Therapy

Healthcare teams are turning to gentle heat as an everyday tool for managing chronic pain. In a 2024 European survey of 282 clinicians, 92 % said they advise heat therapy for low-back pain and 84 % recommend it for neck pain, underscoring how common the practice has become. Temperature-controlled bedding is adding a new layer to this approach. One 2024 study showed that sleeping on a regulated mattress cover lowered resting heart rate by 2 % and lifted heart-rate variability by 7 %, both signs of better overnight recovery. The therapeutic application extends beyond pain relief to include improved circulation, reduced muscle stiffness, and enhanced sleep quality, creating a compound benefit that justifies the investment for both individual consumers and healthcare institutions. Healthcare facilities are incorporating therapeutic heated mattress pads into patient care protocols, particularly for elderly patients and those with mobility limitations benefit from consistent thermal therapy.

Expansion of E-Commerce and DTC Channels

Digital commerce transformation has fundamentally altered heated mattress pad distribution, with online channels capturing an increasing share of sales through superior product education, customer reviews, and direct-to-consumer pricing advantages. Eliminating brick-and-mortar mark-ups let brands pitch premium features, such as carbon-fiber elements and IoT connectivity, without imposing luxury-product price tags. Manufacturers gain usage data that informs rapid design improvements and facilitates personalized marketing bundles that pair pads with complementary bedding accessories. As shipping logistics mature, delivery timetables and return policies match or surpass traditional retail.

Adoption Of Energy-Efficient Carbon-Fiber and Graphene Heaters

Transitioning from metal wires to carbon-fiber strands lowers energy draw by about 30% while providing uniform warmth across the mattress. Graphene coatings drive thermal conductivity above 2.5 W/m·K, speeding responsiveness and extending element lifespan. The resulting pads often qualify for energy-saver labeling programs, which resonate with consumers facing rising utility bills. Flexibility and thin profiles also minimize pinch points, boosting long-term durability and user comfort.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety and Fire-Hazard Certification Burdens | -0.8% | Global, most stringent in North America and EU | Medium term (2-4 years) |

| Rising Electronic Component and Textile Costs | -0.6% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Tightening E-Waste and Electric-Textile Recycling Rules | -0.4% | EU leading, expanding to North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety and Fire-Hazard Certification Burdens

Complying with fire-safety rules has become an expensive hurdle for heated mattress-pad makers. In the United States, every model must pass the Consumer Product Safety Commission’s 16 CFR 1632 and 1633 tests, which expose prototypes to smoldering cigarettes and open flames before a single unit reaches store shelves. Meeting these benchmarks involves building sample pads, sending them to certified labs, documenting every step of production, and then repeating the process at regular intervals—all of which can stretch a development cycle to 12–18 months and add tens of thousands of dollars to a project budget. The regulatory burden is compounded by international variations in safety standards, requiring manufacturers to maintain multiple product certifications for global distribution, which increases complexity and costs for companies seeking to expand beyond domestic markets[1]U.S. Consumer Product Safety Commission, “16 CFR 1633 – Standard for the Flammability (Open Flame) of Mattress Sets,” cpsc.gov.

Rising Electronic Component and Textile Costs

Supply chain inflation has significantly impacted heated mattress pad manufacturing costs, with electronic components including temperature sensors, control circuits, and heating elements experiencing price increases of 15-25% since 2024. Flame-retardant textiles likewise command premiums because they must pass both safety and comfort tests. These cost surges compress margins, pressuring smaller brands to relocate production or postpone feature upgrades. Some manufacturers hedge with long-term supply contracts, but the strategy ties up working capital and raises risk during demand fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polyester Dominance Faces Organic Challenge

Polyester captured 54.32% of the heated mattress pads market share in 2025 due to its affordability, durability, and seamless compatibility with heating grids. Widespread supplier networks keep prices within reach of mass-market buyers, bolstering unit volumes in large retail chains. Cotton blends hold mid-tier positioning and appeal to consumers who favor natural fibers yet accept minor maintenance trade-offs.

Other materials, including organic blends, are advancing at a 6.27% CAGR, propelled by health-oriented shoppers who will pay 20–30% premiums to avoid synthetic dyes and chemicals. Improved spinning and weaving techniques have narrowed the performance gap between natural and synthetic fabrics, ensuring even heat distribution and extended wash cycles without shrinkage. As disposable incomes climb, particularly among millennials, brands tout traceable supply chains and third-party organic certifications to reinforce value.

By Size: Queen-Size Leadership with Adjustable Innovation

The queen-size category accounted for 37.45% of 2025 sales, reflecting its popularity among couples in North America and Europe shared warmth without oversized bedroom footprints. Single-size pads satisfy student housing, guestroom, and elder-care niches, sustaining a modest yet stable revenue stream.

Other sizes (adjustable) products are projected to grow 5.89% annually as they cater to split-king mattresses, RV bunks, and hospital beds. Advanced models feature segmented wiring harnesses that adapt to non-standard dimensions, and detachable panels enable laundering in standard washing machines. Manufacturers market these products as future-proof investments that can migrate to new mattress types during home upgrades.

By End User: Commercial Segment Accelerates Healthcare Adoption

Residential buyers commanded 77.25% of 2025 revenue, drawn by therapeutic benefits, rising sleep-wellness awareness, and convenient availability across both in-store and online retailers. Marketing campaigns stress pain-relief credentials, energy savings, and dual-temperature flexibility to secure repeat purchases during seasonal promotions.

Commercial demand is rising at a 6.43% CAGR as hospitals, rehabilitation centers, and long-term-care providers integrate heated pads into pain-management protocols. Hotels in ski resorts and high-altitude regions deploy the technology to lift guest satisfaction scores, often branding upgraded rooms as “climate-comfort suites.” Bulk orders favor models with industrial-grade cords and centralized temperature controls, helping facilities streamline maintenance schedules.

By Distribution Channel: Online Platforms Drive B2C Growth

B2C retail encompassed 81.10% of 2025 sales, and within that, online is tracking a 6.92% CAGR. Product pages display certifications, energy-use calculators, and user testimonials that translate complex technical data into everyday benefits. Free returns and extended warranties address lingering safety concerns and tip conversion rates.

Brick-and-mortar specialists still attract first-time customers who prefer tactile assessment and personalized fitting. Big-box retailers bundle pads with seasonal bedding sets, leveraging store traffic to stimulate impulse buys. Direct B2B sales to hospitals and hotels represent a smaller but high-value channel where customization and training services command premium margins.

Geography Analysis

North America led the heated mattress pads market in 2025 with 46.35% revenue share, supported by colder climates, mature healthcare coverage, and wide product availability. U.S. Medicare reimbursement for certain durable medical equipment underpins institutional purchases, while Canada’s energy-rebate pilots nudge residential uptake. Asia-Pacific is forecast to record the highest 5.62% CAGR through 2031. China’s expanding middle class values energy savings and digitally connected home goods, while Japan’s aging demographics spur therapeutic demand. South Korea’s tech-savvy consumers gravitate toward app-controlled models, and Australia’s southern states adopt pads to offset climbing home-heating costs. Local manufacturing capabilities shorten delivery cycles and tailor features, such as different voltage ratings, to regional standards.

Europe’s steady adoption stems from stringent product-safety legislation that boosts consumer confidence. Germany, the United Kingdom, and Nordic countries generate the bulk of demand due to long winters and rising residential energy tariffs. Southern Europe, led by Italy and Spain, shows emergent interest as younger households encounter climate-control bedding through online channels and vacation rentals.

South America comprises a nascent but promising region. Brazil and Argentina are early adopters, stimulated by growing e-commerce penetration and seasonal temperature swings in temperate zones. Retailers highlight low power consumption compared with traditional space heaters, aligning with household budget priorities and sustainability narratives. The Middle East and Africa display dispersed demand pockets. South Africa’s Highveld sees winter lows conducive to personal heating, whereas Gulf nations look to balance intense air-conditioning use that leaves sleepers feeling chilled. Import distributors collaborate with hospitality groups to position heated pads as niche comfort upgrades during cooler months.

Mordor Intelligence provides coverage of the heated mattress pads market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The heated mattress pads market is moderately concentrated. Sunbeam Products, Biddeford Blankets, and Beurer maintain mass-market dominance through value pricing and nationwide retail placement. Sleep Number and Serta Simmons Bedding focus on premium performance, integrating pads into broader smart-bed ecosystems that command margins two to three times above entry-level models.

Patents illustrate rising technical complexity: Sleep Number alone holds a significant number of filings covering circadian-aligned temperature control, pressure sensing, and IoT integration[3]Sleep Number Corporation, “Patent Portfolio Highlights,” sleepnumber.com. Carbon-fiber specialists partner with bedding brands to embed flexible heating layers, while graphene start-ups license coatings that boost conductivity and thinness.

Traditional firms reinforce competitive moats with long-term supplier contracts for flame-retardant textiles and in-house test labs that expedite certification. Yet lower tooling costs for printed carbon-fiber grids enable fresh entrants to prototype quickly and market through social-media influencers. As the 5.66% CAGR attracts capital, strategic collaborations—such as OEM supply deals with mattress-in-a-box vendors—are expected to intensify through 2030.

Heated Mattress Pads Industry Leaders

Sunbeam Products Inc.

Serta Simmons Bedding LLC

Sleep Number Corp.

Biddeford Blankets LLC

Beurer GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Tempur Sealy International completed its USD 5 billion acquisition of Mattress Firm, creating an USD 8 billion integrated retail-manufacturing entity.

- October 2024: Sleep Number introduced the ClimateCool™ smart bed, combining active cooling with heated mattress pad functionality and dual-zone temperature variation of up to 15 degrees.

Global Heated Mattress Pads Market Report Scope

A heated mattress pad, a bedding essential, is designed to provide warmth by being placed directly on top of your mattress. Typically, it features an electrical heating element and an electronic controller, enabling precise temperature control. The heated mattress pads market is segmented by application, distribution channel, and region. By application, the market is segmented into households, hotels, hospitals, and other applications. By distribution channel, the market is segmented into online and offline, and by region, the market is segmented into North America, Europe, South America, Asia-Pacific, and Middle East & Africa. The report offers market size and forecast for the heated mattress pads market in all the above segments in terms of value (USD).

| Polyester |

| Cotton |

| Other Materials |

| Single-size |

| Double-size |

| Queen-size |

| King-size |

| Other Sizes |

| Residential | |

| Commercial | Hospitals |

| Hotels | |

| Other Commercial End Users |

| B2B/Directly from the Manufacturers | |

| B2C/Retail Channels | Specialty Bedding and Mattress Stores |

| Multi-brand Stores/Home Centers | |

| Online | |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Aisa Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia Pacific | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Material | Polyester | |

| Cotton | ||

| Other Materials | ||

| By Size | Single-size | |

| Double-size | ||

| Queen-size | ||

| King-size | ||

| Other Sizes | ||

| By End User | Residential | |

| Commercial | Hospitals | |

| Hotels | ||

| Other Commercial End Users | ||

| By Distribution Channel | B2B/Directly from the Manufacturers | |

| B2C/Retail Channels | Specialty Bedding and Mattress Stores | |

| Multi-brand Stores/Home Centers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Aisa Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia Pacific | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

How big is the heated mattress pads market in 2026?

The heated mattress pads market size is valued at USD 513.42 million in 2026.

What is the expected growth rate for the heated mattress pads market through 2031?

The market is forecast to expand at a 5.21% CAGR, reaching USD 661.85 million by 2031.

Which material dominates sales?

Polyester commands 54.32% of 2025 revenue thanks to durability and low cost, while organic fabrics are the fastest-growing segment.

Why are hospitals adopting heated mattress pads?

Continuous low-level warmth reduces patient pain, boosts circulation and complements non-pharmaceutical recovery protocols, making pads a cost-effective therapeutic tool.

How do energy-efficient heating elements impact operating costs?

Carbon-fiber and graphene technologies cut electricity use by roughly 30%, lowering nightly operating costs to near USD 0.02 in many U.S. states.

Are there safety standards buyers should look for?

In the United States, compliant pads meet CPSC flammability rules 16 CFR 1632 and 1633; European consumers should verify EN ISO and CE markings for fire safety assurance.

Page last updated on: