Bedroom Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 132.49 Billion |

| Market Size (2031) | USD 165.07 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bedroom Furniture Market Analysis by Mordor Intelligence

The Bedroom Furniture Market size is expected to grow from USD 126.80 billion in 2025 to USD 132.49 billion in 2026 and is forecast to reach USD 165.07 billion by 2031 at 4.49% CAGR over 2026-2031.

Momentum is rooted in sustained urban housing growth, widening e-commerce access, and rising consumer prioritization of high-quality sleep solutions. Beds anchor spending as the foundational purchase, while the accelerating demand for tech-integrated, space-saving pieces signals a broader transition toward multifunctional design. Wood retains its premium allure, yet recycled plastic and acrylic innovations are reshaping value propositions as regulators, retailers, and buyers converge around sustainability mandates. Regionally, Asia-Pacific solidifies its lead on the strength of rapid urbanization and middle-class expansion, whereas North America and Europe leverage wellness and eco-design trends to upgrade average selling prices. Competitive intensity is heightened as legacy leaders, digitally native brands, and contract specialists vie to embed smart features, shorten delivery cycles, and insulate margins from volatile lumber prices [1]United Nations Department of Economic and Social Affairs, “World Urbanization Prospects 2024,” un.org.

Key Report Takeaways

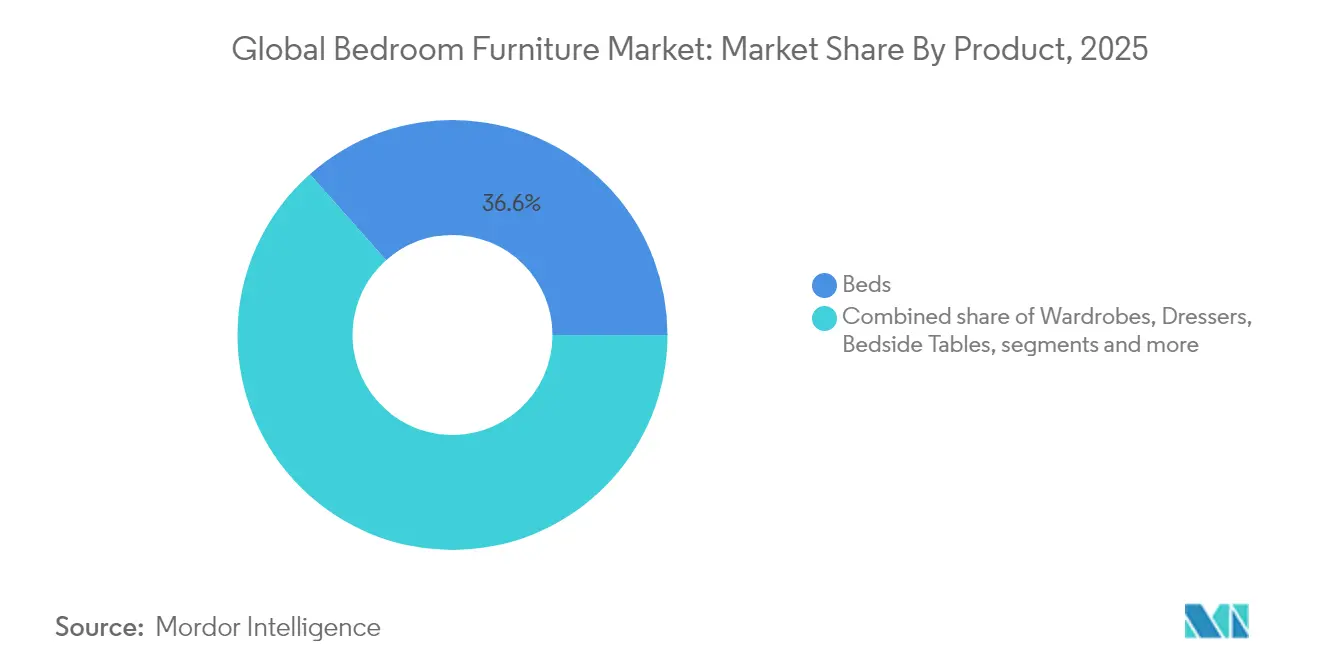

- By product, beds led with 36.55% revenue share of the bedroom furniture market in 2025; dressers/dressing tables are projected to expand at a 5.07% CAGR through 2031.

- By material, wood held 39.45% of bedroom furniture market share in 2025, while plastic/acrylic is forecast to rise at a 6.31% CAGR to 2031.

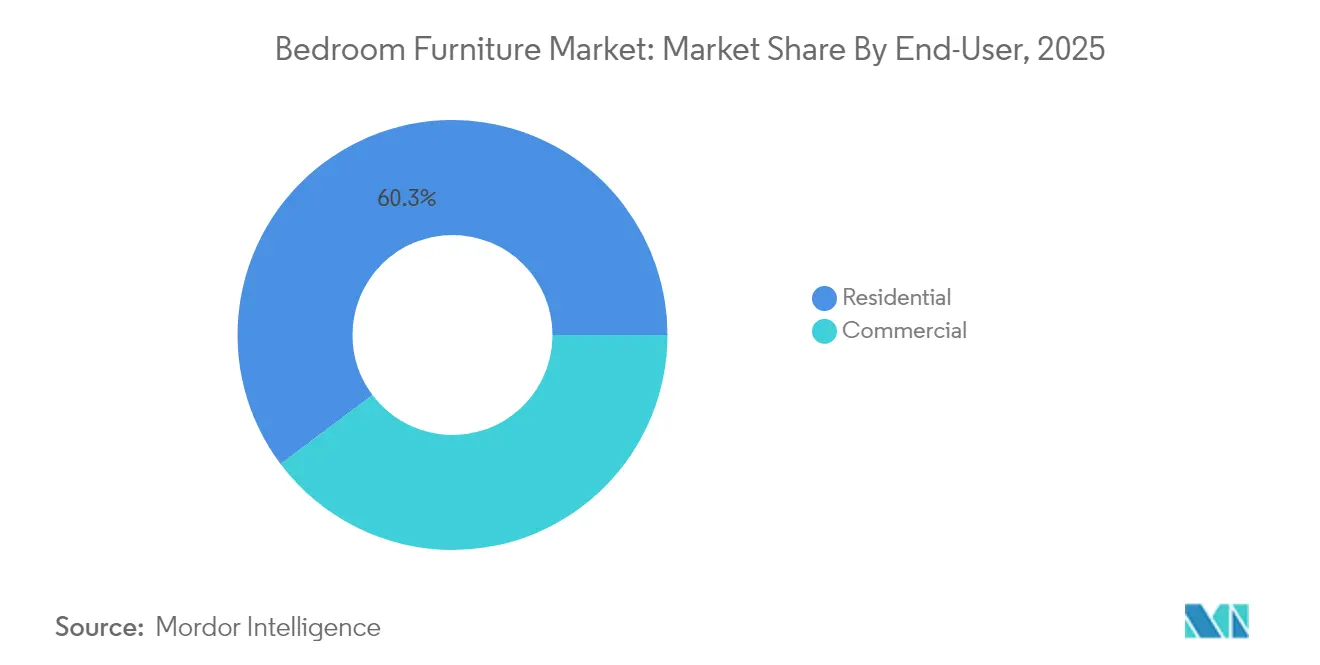

- By end-user, residential accounted for 60.25% of bedroom furniture market size in 2025; the commercial segment is advancing at a 5.47% CAGR to 2031.

- By distribution channel, the B2C retail segment commanded 74.20% share of the bedroom furniture market in 2025, whereas the B2B/direct channel is growing at a 6.05% CAGR.

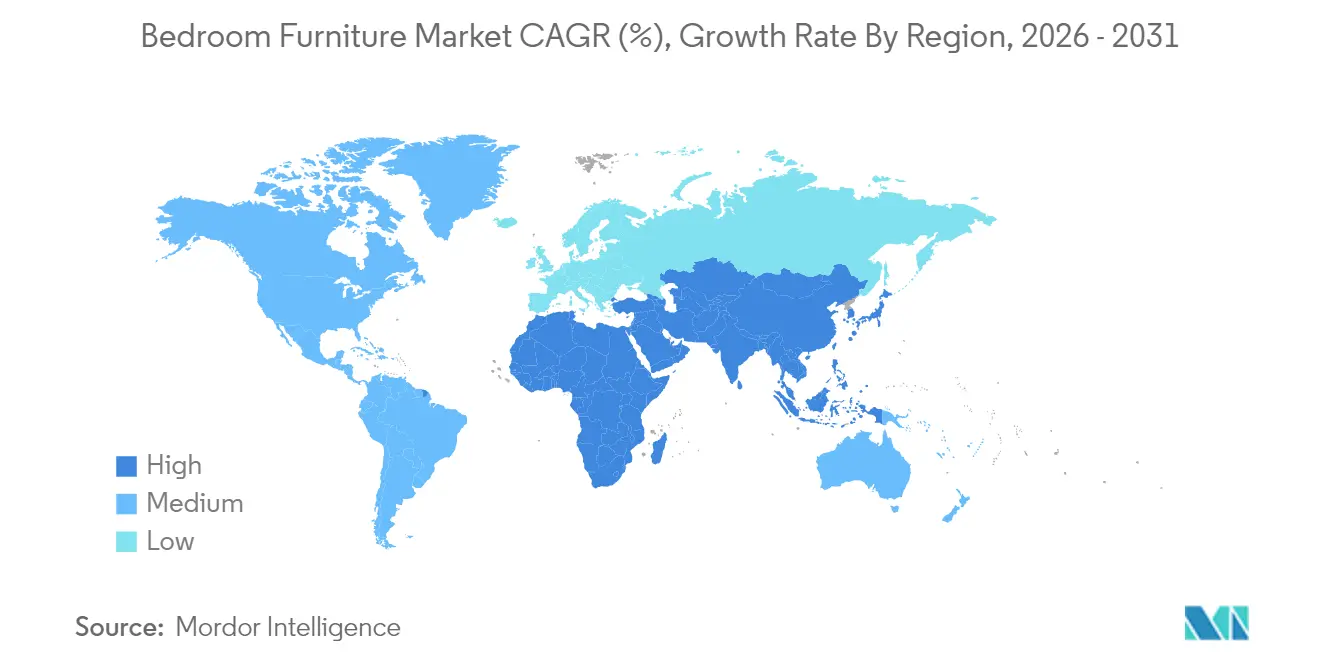

- By geography, Asia-Pacific captured 40.60% of the bedroom furniture market in 2025 and is tracking the fastest regional CAGR at 5.67% until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bedroom Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanization and housing demand | +0.8% | Asia-Pacific, Middle East & Africa | Medium term (2-4 years) |

| Growing emphasis on ensuring high-quality sleep | +0.6% | North America, Europe | Medium term (2-4 years) |

| Rising focus on home renovation and interior design trends | +0.5% | Global | Short term (≤2 years) |

| Increasing prevalence of compact living spaces boosts demand for multifunctional storage beds | +0.4% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Urbanization and Housing Demand

Urban migration is rewriting bedroom furniture market fundamentals as 68% of the world’s population is projected to live in cities by 2050[2]United Nations Department of Economic and Social Affairs, “World Urbanization Prospects 2024,” un.org. Asia-Pacific is already witnessing a residential construction boom that elevates first-time purchases of beds, wardrobes, and storage solutions. Shrinking average apartment sizes steepen the requirement for space-efficient designs, prompting manufacturers to champion lift-top beds, sliding-door wardrobes, and stackable nightstands. Developers of mid-rise and high-rise condominiums are collaborating with branded furniture vendors to package turnkey furnishing bundles, securing predictable order volumes and accelerating time-to-market. The interplay of urban density, aspirational spending, and limited floor space cements the bedroom furniture market as a direct beneficiary of housing policy and infrastructure investment.

Growing Emphasis on Ensuring High-Quality Sleep

Public health campaigns and wearable-derived data have reframed sleep quality as a wellness essential. Search interest in “smart beds” and “adjustable frames” reached a five-year high in 2025, and suppliers are integrating posture-sensing actuators, built-in circadian LED lighting, and air-purifying side tables to meet heightened expectations. Mattress bases with IoT modules feed usage analytics to connected apps, enabling subscription-based upgrade cycles that extend revenue beyond the initial sale. Retailers position premium sleep ecosystems as a holistic solution rather than discrete items, lifting average ticket values across the bedroom furniture market. As consumers link restorative sleep to productivity gains, adoption spreads from health-conscious demographics to mainstream households.

Rising Focus on Home Renovation and Interior Design Trends

Pandemic-driven nesting habits matured into sustained renovation activity, propelling demand for statement headboards, textured dressers, and artisanal nightstands. Color psychology now informs merchandising plans, with vibrant emeralds and terracotta replacing erstwhile neutrals. Reclaimed wood and organic textiles underpin narratives of authenticity and environmental stewardship, allowing manufacturers to debut higher margin eco lines. Customizable modular wardrobes enable homeowners to refresh layouts without replacing entire suites, sharpening brand loyalty. Influencer-led virtual showrooms amplify trend diffusion, accelerating global design cycle turnover and injecting additional dynamism into the bedroom furniture market.

Increasing Prevalence of Compact Living Spaces Boosting Multifunctional Storage Beds

Urban consumers increasingly seek modern, functional furniture solutions, driving heightened demand for beds, a staple of bedroom furniture. As urban areas trend towards smaller living spaces, there is a growing preference for multifunctional beds, especially those with built-in storage. The expansion of this market is significantly bolstered by e-commerce. The appeal of online shopping, paired with a vast selection, simplifies the process for customers purchasing bedroom furniture, especially beds. Additionally, trends in interior design and a push for personalized living spaces motivate consumers to invest in quality beds that resonate with their aesthetic tastes. European and Asian cities with dense footprints are frontrunners, but North American micro-studio developments are catching up, expanding the total addressable market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in lumber & engineered wood prices is affecting cost structures | -0.7% | Global, highest in North America | Short term (≤2 years) |

| Intensifying competition from low-cost unbranded manufacturers is eroding margins | -0.5% | Asia-Pacific, South America | Medium term (2-4 years) |

| Strict environmental policies on deforestation and sustainable sourcing | -0.3% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Lumber & Engineered Wood Prices

Supply chain unrest, export quotas, and freight bottlenecks have driven sharp swings in hardwood and plywood costs, especially for North American producers. Solid wood bed frames now command price premiums that outstrip disposable income growth, prompting substitution toward veneer and composite alternatives. Mid-tier brands with limited hedging capacity face margin compression, spurring consolidation and strategic sourcing partnerships. Some manufacturers are pivoting certified plantation timber and fast-growing species, but certification fees and processing adjustments weigh on near-term profitability across the bedroom furniture market.

Intensifying Competition from Low-Cost Unbranded Manufacturers

Price-driven entrants leverage lean overheads and social-commerce storefronts to reach value-oriented shoppers, compressing average selling prices in the lower quartile. Established brands counter with omnichannel loyalty programs, speedier delivery, and modular add-ons that raise switching costs. Nevertheless, discount-led campaigns undermine perceived value, slowing premiumization in budget segments. The long tail of small producers exacerbates fragmentation, making it difficult for large players to sustain scale advantages in every local market. These dynamics temper growth potential in the bedroom furniture industry until rationalization or brand-led differentiation prevails.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Beds Dominate While Dressers Accelerate

Beds generated 36.55% of revenue in 2025, anchoring the bedroom furniture market as the highest-ticket purchase around which complementary pieces orbit. Platform, canopy, and upholstered variants support design diversification, yet a unifying focus on integrated charging and adjustable bases tightens alignment with wellness themes. Dressers and dressing tables register the swiftest momentum at a 5.07% CAGR, fueled by consumer pursuit of vanity spaces and incremental storage capacity. Within the luxury stratum, personalized drawer configurations and embedded LED mirrors sustain price elasticity.

Beyond these two poles, wardrobes capture steady demand as closets standardize around modular interiors, while nightstands benefit from the inclusion of wireless pads and ambient lighting. The Murphy subcategory advances as hotels and urban studios reconfigure square footage, solidifying its importance to the broader bedroom furniture market. Manufacturers broaden SKUs to include kid-oriented loft beds with lower play zones, capturing family spending previously directed to toy storage.

By Material: Wood Dominates as Plastics Innovate

Wood kept 39.45% of bedroom furniture market share in 2025, supported by consumer associations with durability, tactile warmth, and timeless aesthetics. FSC, PEFC, and Rainforest Alliance certifications amplify trust, enabling premium positioning even during commodity price spikes. Simultaneously, recycled plastic and acrylic sets achieve a 6.31% CAGR, challenging stereotypes through matte finishes, bold colors, and closed-loop narratives. This growth repositions plastics from merely cost-focused inputs to stylized, sustainable alternatives that appeal to eco-mindful Millennials. Metal frames retain relevance in industrial-inspired décor, yet rising energy costs weigh on affordability.

Innovation converges on hybrid compositions that merge reclaimed timber surfaces with ABS plastic cores, providing structural stability without compromising visual authenticity. Eco-design legislation in Europe encourages manufacturers to engineer for disassembly, extending product life and improving recycling rates, a trend that strengthens the environmental credentials of the bedroom furniture market. As material passports become mainstream, transparency on origin and recyclability is expected to influence purchase decisions across both residential and commercial channels.

By End-User: Residential Leads, While Commercial Accelerates

Households commanded 60.25% of revenue in 2025, underscoring the primacy of personal comfort in the bedroom furniture market. Pandemic-era savings were redirected toward bedroom upgrades, and demand has remained resilient even as discretionary budgets normalize. Homeowners value longevity, buoying solid wood bed sales despite price sensitivity. The bedroom furniture market size for commercial buyers, however, is scaling faster at a 5.47% CAGR on the back of hotel refurbishment cycles, purpose-built student housing, and corporate wellness initiatives.

Hotels embed bespoke headboards, under-bed storage, and sensor-based nightlights to differentiate guest experience. Developers of co-living spaces partner with contract manufacturers to standardize furniture kits that meet stringent fire safety and durability criteria. The push for green building certifications accelerates the adoption of low-VOC finishes, repositioning bedroom suites as evidence of sustainable operational policies. As occupiers measure employee retention and guest satisfaction, premium furniture investments gain strategic relevance.

By Distribution Channel: Retail Dominates as B2B Grows

Brick-and-mortar retail captured 74.20% of sales in 2025, reflecting consumer preference to evaluate comfort, texture, and build quality in person. Showrooms deploy augmented-reality tools that map furniture to room dimensions, bridging physical and digital journeys. E-commerce penetration continues to climb on the back of free returns and AI-guided sizing advice, yet the largest gains accrue to omnichannel chains that stitch online browsing into store pickup.

Contract buyers and residential developers gravitate toward direct sourcing to optimize cost and customization, propelling the B2B channel at a 6.05% CAGR and signaling a gradual redistribution of bedroom furniture market share toward manufacturer-led commerce. Logistics platforms capable of drop-shipping assembled pieces reduce complexity, enabling mid-sized producers to service hospitality and build-to-rent projects. Embedded financing solutions and CAD-to-factory ordering trim design cycles, tightening alignment between specification changes and factory output.

Geography Analysis

Asia-Pacific dominated global revenue in 2025 with a 40.60% stake and is growing at a 5.67% CAGR through 2031. Urban migration, robust residential construction, and a rising middle class underpin sustained volume expansion, though fragmented supply chains and limited domestic raw material availability temper margin upside. Governments in India, Indonesia, and Vietnam promote furniture manufacturing clusters to capture more of the bedroom furniture market value chain locally, improving resilience against import volatility.

North America follows as the second-largest region, with demand shaped by compact apartment trends, wellness-centric design, and early adoption of tech-integrated beds. Lumber price volatility presents cost challenges, prompting substitution toward engineered wood and recycled plastics. Retailers differentiate through white-glove delivery and sleep-solution bundling, enhancing long-term engagement in a mature yet evolving marketplace.

Europe maintains a sizable share, underpinned by stringent eco-design regulations and consumer demand for certified sustainable materials . Producers respond with modular, easily repairable designs that extend product life and meet circular-economy objectives. Despite slower population growth, high replacement rates and premium price points support stable revenue. Recycling rates for metal furniture remain low, creating policy pressure and innovation opportunities that reverberate across the bedroom furniture market.

Competitive Landscape

Global leadership resides with IKEA, Ashley Furniture, and a cohort of regionally entrenched manufacturers whose combined scale affords procurement and distribution efficiencies. Ashley remains among the America’s largest producers, yet faces thinner spreads due to freight surcharges and discount competition. IKEA balances volume with sustainability milestones, targeting renewable and recycled materials for 50% of its wood use by 2030. The mid-market hosts digitally native challengers that harness social media storytelling and direct-to-consumer logistics to chip away at incumbent share, although production scaling and last-mile costs dampen profitability.

Technology integration is the decisive differentiator. Brands with in-house digital manufacturing shorten lead times and offer mass customization at near-mass production cost. La-Z-Boy’s acquisition of Joybird exemplifies the quest for omnichannel depth, blending 353 furniture galleries, 550 shop-in-shops, and a high-traffic e-storefront [4]Hooker Furnishings, “Fiscal 2025 Q4 Earnings Release,” hookerfurnishings.com Source: United States Securities and Exchange Commission, “La-Z-Boy Inc. Form 10-K 2025,” sec.gov. Contract specialists pursue turnkey procurement for hotels and co-living projects, locking multi-year agreements that stabilize factory utilization.

Margin expansion strategies revolve around vertical integration, eco-label certifications, and subscription services for IoT-enabled sleep products. Warranty extensions and refurbishment programs counter price-driven churn, strengthening customer lifetime value in the bedroom furniture market. Entry barriers persist in upholstery know-how, supply chain coordination, and compliance with diverse fire-safety codes, consolidating advantage among firms with global sourcing networks.

Bedroom Furniture Industry Leaders

IKEA

Ashley Furniture Industries, Inc.

Leggett & Platt Incorporated

Nitori Co. Ltd.

Steinhoff International Holdings N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Pulaski Furniture, part of Hooker Furnishings, is set to unveil nine new collections for the bedroom, dining, and occasional use at the Spring High Point Market,

- August 2024: Pottery Barn, a brand under Williams-Sonoma, Inc., teamed up with Michael Graves Design to unveil a new collection of home furnishings. With a reputation for championing accessible design, Michael Graves Design collaborated closely with Pottery Barn to craft bedroom furniture and upholstery that prioritized safety and accessibility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, shaped by Mordor Intelligence's scope, values the global bedroom furniture market as all new beds, mattresses, wardrobes, nightstands, dressers, and allied storage units sold to households through retail or project channels. The market is estimated at USD 131.55 billion for 2025 and is projected to reach USD 161.99 billion by 2030, advancing at 4.25% CAGR.

Scope exclusion: For clarity, we exclude contract-manufactured components, second-hand units, and purely decorative accents.

Segmentation Overview

- By Product

- Beds

- Wardrobes/Closets

- Dressers/dressing Tables

- Bedside Tables

- Other Bedroom Furniture

- By Material

- Wood

- Metal

- Plastic & Acrylic

- Other Materials

- By End-user

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B/Directly from Manufacturers

- B2C/Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed manufacturers, branded retailers, buying groups, and online platforms across Asia Pacific, North America, and Europe. Conversations confirmed average selling prices, online penetration shifts, material cost pass-through, and typical replacement intervals, while short consumer surveys illuminated the adoption of multifunctional storage beds.

Desk Research

We began with public datasets from UN Comtrade, the World Bank, Eurostat, and national census bureaus to quantify trade flows, housing completions, and disposable income. Industry bodies such as the American Home Furnishings Alliance and the China National Furniture Association helped size the installed base and replacement cycles, while company 10-Ks, investor decks, and reliable business media clarified pricing and channel splits. Subscription tools, including D&B Hoovers for financials and Dow Jones Factiva for news scans, flagged anomalies. Patent insights from Questel on smart-bed innovations and shipment lines from Volza refined regional splits. This list is illustrative; many other open sources were referenced for data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down and bottom-up blend underpins the model. We first map regional retail sales from official retail trade and household spending tables, then apply bedroom furniture shares from association ratios; supplier roll-ups and sampled price × volume checks validate totals. Key variables like housing starts, average floor space, e-commerce share, lumber and foam indices, and urban disposable income feed a multivariate regression that, through an ARIMA forecast, generates base, high, and low scenarios. Where fast-growing channels are undercaptured, weights are adjusted after analyst review.

Data Validation & Update Cycle

Before release, outputs undergo peer review; variance dashboards highlight outliers, prompting re-contacts where needed. Reports refresh annually, with interim updates when material events, such as tariff shifts, alter core drivers, ensuring clients receive the latest view.

Why Mordor's Bedroom Furniture Baseline commands reliability

Published estimates often diverge; our disciplined exclusion of refurbished goods, verified retail price benchmarks, and annual recalibration keep Mordor Intelligence's baseline grounded.

This is where Mordor Intelligence's disciplined approach around scope and pricing shines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 131.55 Bn (2025) | Mordor Intelligence | - |

| USD 266.15 Bn (2024) | Global Consultancy A | Includes living-room and bathroom furniture at producer prices |

| USD 254.30 Bn (2025) | Research Firm B | Uses shipment volumes without retail margin normalization |

| USD 99.13 Bn (2024) | Industry Publication C | Tracks economy segment only across 20 economies |

Differences stem from scope breadth, price points, and refresh cadence. By anchoring estimates to transparent variables and repeatable steps, Mordor Intelligence provides decision-makers a dependable, balanced baseline.

Key Questions Answered in the Report

What is the current size of the bedroom furniture market?

The bedroom furniture market stands at USD 132.49 billion in 2026 and is projected to reach USD 165.07 billion by 2031.

Which region generates the highest bedroom furniture market revenue?

Asia Pacific leads with 40.60% of global revenue in 2025 and holds the fastest regional CAGR at 5.67% through 2031.

Which product category grows fastest in the bedroom furniture market?

Dressers and dressing tables post the fastest growth at a 5.07% CAGR between 2026 and 2031.

How are sustainability trends influencing bedroom furniture materials?

Wood retains dominance at 39.45% share, but recycled plastic and acrylic sets are growing at a 6.31% CAGR as regulators and consumers demand eco-friendly options.

Page last updated on: