Market Overview

| Study Period | 2020 - 2031 |

|---|---|

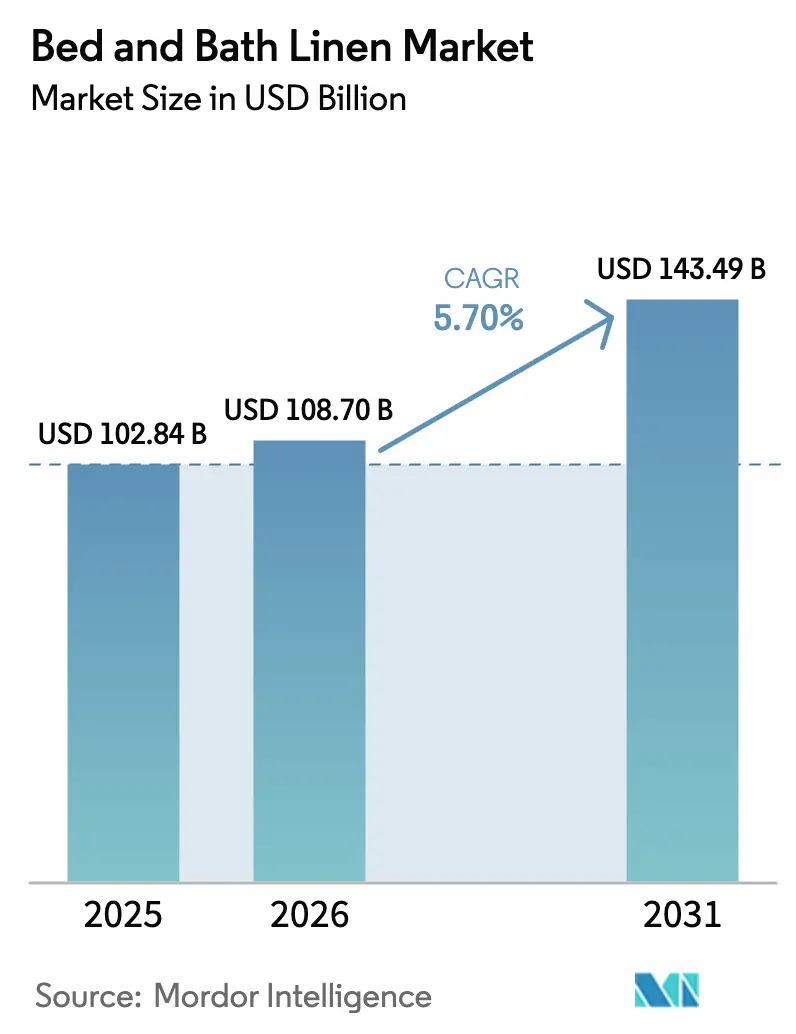

| Market Size (2026) | USD 108.70 Billion |

| Market Size (2031) | USD 143.49 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bed And Bath Linen Market Analysis by Mordor Intelligence

The bed and bath linen market size is projected to expand from USD 102.84 billion in 2025 and USD 108.70 billion in 2026 to USD 143.49 billion by 2031, registering a CAGR of 5.70% between 2026 to 2031. Bed sheets lead product revenues, residential buyers remain the largest demand pool, and offline channels still account for a higher share despite faster online gains. Asia-Pacific shows the fastest trajectory, supported by India’s exports and China’s large-scale manufacturing base, while North America sustains import-led consumption cycles. Product innovation aligns with sustainability standards as brands and manufacturers join OEKO-TEX and GOTS, and hospitality projects continue to upgrade textile specifications. Supply arrangements are also adapting to traceability requirements introduced by Better Cotton’s traceability framework.

Key Report Takeaways

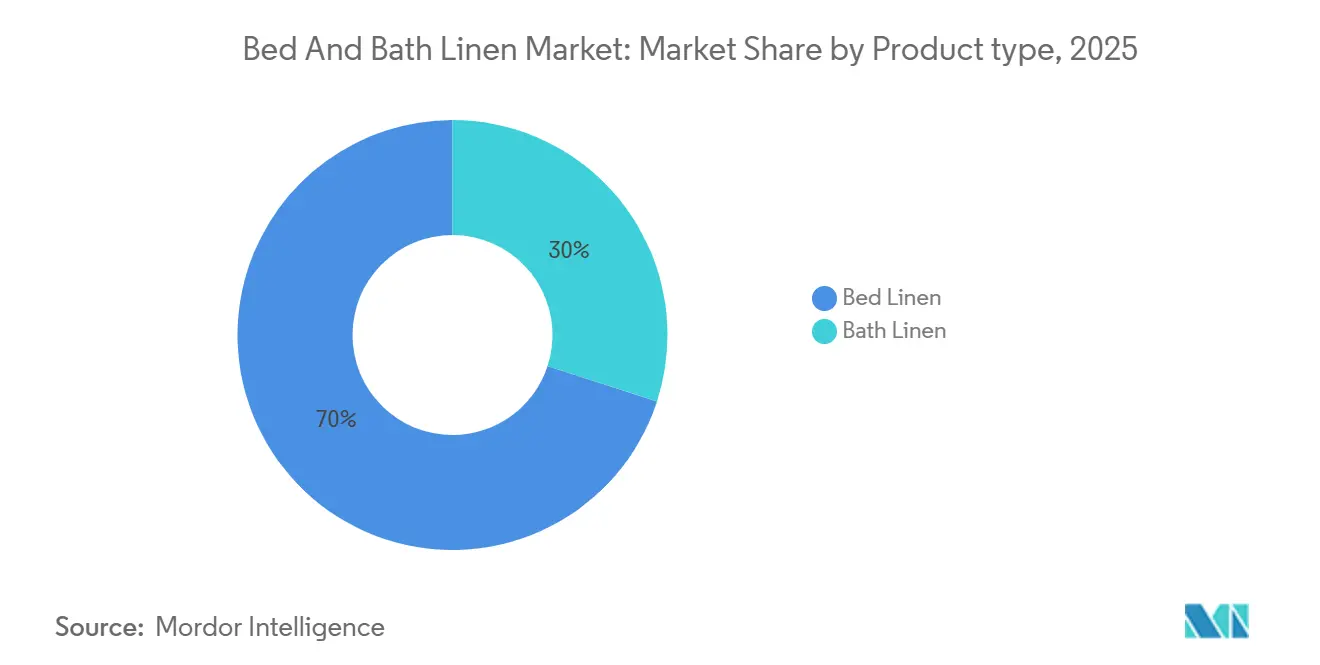

- By product, bed linen led the bed and bath linen market with 70% market share in 2025 and is projected to expand at a 6.20% CAGR through 2031.

- By material, cotton accounted for 65% of the bed and bath linen market share in 2025, while other material is projected to expand at a 5.85% CAGR through 2031.

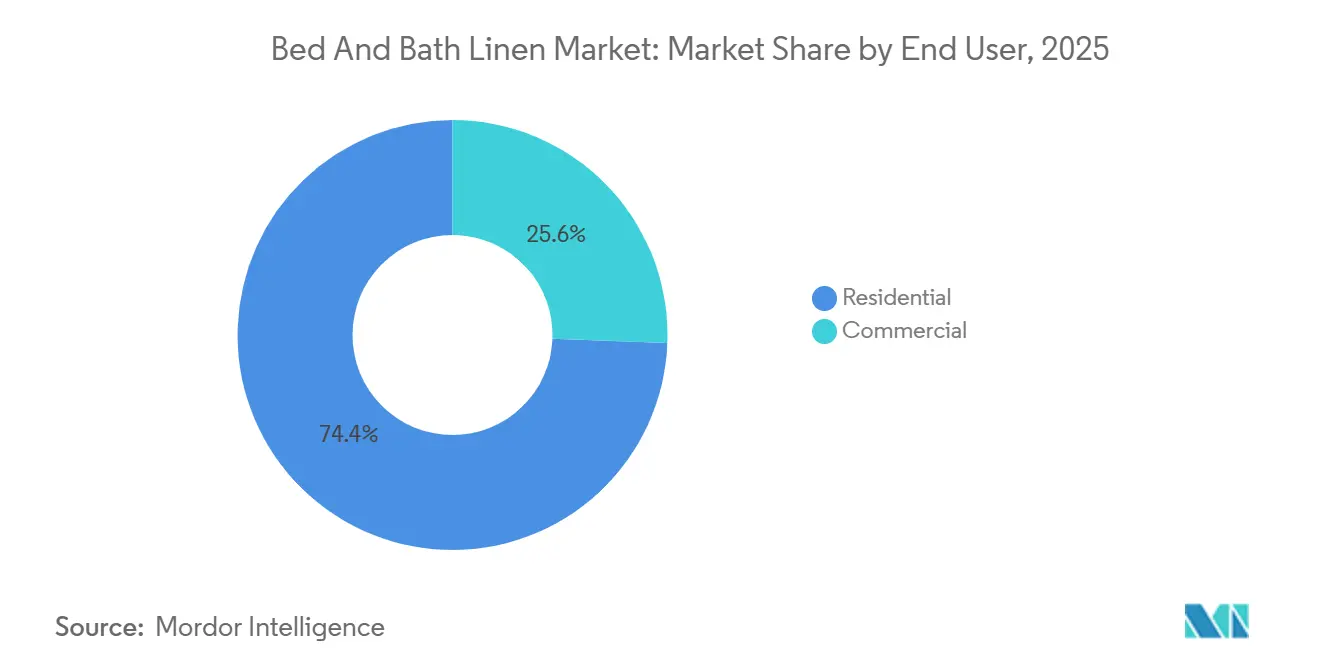

- By end user, residential accounted for 74.40% of the bed and bath linen market share in 2025, while commercial is projected to expand at a 6.54% CAGR through 2031.

- By distribution channel, B2C/Retail channels held 78% of the bed and bath linen market share in 2025, while online is projected to expand at a 7.20% CAGR through 2031, making it the fastest-growing segment of the bed and bath linen market.

- By geography, Asia-Pacific held 45.48% of the bed and bath linen market share in 2025, and is projected to expand at a 6.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bed And Bath Linen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in premium hospitality refurbishments | + 1.9% | Global, strongest in the Middle East, the North American Sunbelt, and the Asia-Pacific tourism corridors | Medium term (2-4 years) |

| Urban middle-class household formation in APAC | + 2.1% | Asia-Pacific core markets with spillover into China’s Tier 2 and Tier 3 | Medium term (2-4 years) |

| E-commerce-led private-label penetration | + 1.6% | North America and Western Europe, with emerging in Latin America | Short term (≤ 2 years) |

| Institutional pivot to hygiene-certified textiles | + 1.3% | Global, concentrated in healthcare and elderly care | Medium term (2-4 years) |

| Circular-textile take-back programs by home-fashion retailers | + 0.7% | North America and the EU | Long term (≥ 4 years) |

| Government procurement quotas for organic cotton linens | + 0.8% | EU agencies and select U.S. state or municipal entities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Premium Hospitality Refurbishments

Premium hotel and resort refurbishments replace full textile inventories every five to seven years, which concentrates large orders on high-thread-count, organic, and bespoke linens that elevate the guest experience. The Middle East tourism buildout under Saudi Vision 2030 and Dubai’s large room base has driven higher-specification purchases, while upgrade cycles in North America and parts of Asia-Pacific are reinforcing contract-manufacturer order books. Welspun reported sizable hospitality contributions from bulk towel orders, and it added a 6,400 MTPA jacquard towel unit in November 2024 to target decorative weaves associated with higher margins. Indo Count accelerated U.S. proximity and brand-led execution by acquiring Fluvitex USA and Modern Home Textiles in fiscal 2025, supporting faster delivery windows to hospitality buyers. The American Hotel & Lodging Association’s room-supply growth outlook signals incremental textile refits, while GOTS facility counts and organic cotton output trends confirm the pull toward certified inputs by European luxury operators.

Urban Middle-Class Household Formation in APAC

Urbanization and rising disposable incomes in Asia-Pacific are driving first-time household formation and prompting trade-ups from unbranded to branded linen sets. India’s domestic home textile value pool expanded, with an outlook pointing to sustained growth, while purchasing is centered in large metros with strong e-commerce penetration and modern trade. Company disclosures in 2025 for leading Indian brands highlighted double-digit revenue gains in bed and bath categories aligned to household upgrades. China’s urbanization added millions of urban residents annually, and its internal e-commerce platforms increase access to premium sets without reliance on imports. India’s South and West regional patterns also show meaningful dispersion within national demand, while exporters posted healthy year-to-date shipment values.

E-Commerce-Led Private-Label Penetration

Private-label expansion in digital channels allows producers to bypass wholesale intermediaries and hold more margin, while large retailers leverage data to refine specifications and price ladders. Williams-Sonoma maintained a high e-commerce penetration that bolstered omnichannel engagement, and it continues to emphasize in-house product design to differentiate. Direct-to-consumer brands such as Brooklinen, Boll & Branch, and Parachute achieved higher gross margins through quality positioning, sustainability credentials, and loyalty programs after launching organic-certified lines. Customer acquisition costs have risen due to privacy changes, prompting digital brands to shift toward omnichannel strategies and selective wholesale partnerships to balance paid media costs. Indian producers leverage local platforms to create direct-to-consumer offerings while preserving export relationships, and the exit of large specialty chains in 2023 redistributed share to general merchandise retailers with strong private labels.

Institutional Pivot to Hygiene-Certified Textiles

Healthcare and eldercare buyers specify certified, durable, and fluid-barrier textiles designed to withstand high-temperature, high-frequency laundering cycles. OEKO-TEX Standard 100 added stricter PFAS and BPA thresholds in April 2025 certification protocols, prompting mills to reformulate finishes and tighten chemical management. Institutional-grade linens often feature antimicrobial enhancements and performance features at scale, shifting the emphasis from brand to compliance and lifecycle durability.[1]Source: OEKO-TEX, “STANDARD 100 by OEKO-TEX,” OEKO-TEX, oeko-tex.com Procurement in large health systems consolidates orders into contract cycles that reward uniformity and documentation, supporting accreditation and public tender rules. Aging demographics in advanced markets are driving increased eldercare demand, where hygiene and comfort are equally weighted in bedding and toweling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cotton prices | - 1.8% | Global exposure in vertically integrated hubs | Short term (≤ 2 years) |

| Counterfeit branded linens on online marketplaces | - 0.7% | Global e-commerce platforms | Medium term (2-4 years) |

| PFAS and microplastic regulatory crackdown | - 1.1% | North America and the EU are ahead of the Asia-Pacific | Medium term (2-4 years) |

| Margin squeeze from rising renewable-energy surcharges in textile hubs | - 0.9% | India, China, and parts of Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Cotton Prices

Cotton price moves flow straight into input costs for integrated producers and can erode margins when contracts constrain cost pass-through. The U.S. 2025-26 crop outlook from the National Cotton Council indicated a 14.27 million bale harvest and higher yields, yet global prices still traded within a tight band through 2023-2025 [2]Source: National Cotton Council of America, “USDA December 2025 Cotton Crop Estimate,” NCC, cotton.org . Welspun’s Q2 FY26 results showed a margin squeeze driven by input pressures, illustrating how short-term volatility affects profitability for export-led mills. While hedging can limit exposure, many mid-size mills operate without formal commodity programs and bear the full brunt of spot volatility. Cotton’s primacy in bed and bath categories also limits substitution, and organic cotton premiums introduce a second layer of volatility where supply is thin.

Counterfeit Branded Linens on Online Marketplaces

Counterfeits undercut brands and damage trust by misrepresenting fiber content and avoiding third-party safety testing. Consumers discover inferior performance attributes that often translate into negative reviews and lost share for authentic sellers. Platforms provide brand-protection tools and IP takedown processes, but bad actors reappear under new identities, and enforcement remains resource-intensive for brands. The European Market Surveillance Regulation requires platform-level diligence and enables significant penalties, yet practical enforcement remains uneven across markets. Brands increasingly deploy authentication technologies linked to traceability systems to reinforce consumer confidence despite per-unit cost overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Bed Sheets Lead While Duvet Covers Surge

In the global bed and bath linen market, the product type segment is dominated by bed linen, which accounted for approximately 70% of the total market size in 2025, and it is also expected to remain the fastest-growing segment during 2026–2031, registering a CAGR of 6.20%. Bed sheets held the dominating position within the product type bed linen in 2025, and duvet covers and quilts posted the fastest momentum through 2031. Cotton remains the dominant fiber across bed and bath categories, and one 480-pound bale can yield hundreds of sheets or towels, which underscores the material’s importance in the category. U.S. textile mills reported shipments growth through September 2025 alongside an increase in inventories, which shows measured restocking among downstream buyers [3]Source: U.S. Census Bureau, “Manufacturers’ Shipments, Inventories, and Orders (M3) Survey December 2025,” U.S. Census Bureau, census.gov . Certification adoption continues to expand; global GOTS facilities and organic fiber volumes increased by 2023, which stimulated product development for fillings and fabrications in higher-value duvet and quilt lines. On the bath side, hospitality replacements and stricter institutional laundering needs are supporting terry towel demand, and producers have adjusted capacity toward higher-turnover towels.

Duvet and quilt formats continue to gain share in urban markets as consumers prioritize comfort and storage efficiency, and innovation in sustainable fillers adds differentiation. Welspun’s capacity updates in 2024 improved the product mix toward premium jacquard towels, while broader bath output was managed to align with order flow across Q2 FY26. Alok’s terry towel sales grew while bedding contracted in fiscal 2024-25, indicating a tilt toward categories with shorter replacement cycles [4]Source: Alok Industries Limited, “38th Annual Report 2024-25,” Alok Industries, alokind.com . Trade flows also show regional opportunities; Chile’s towel import structure in 2024 reflected rising shares for Indian and Chinese suppliers under favorable trade terms, and Europe’s import value for bed textiles sourced from developing countries increased steadily between 2020 and 2024. American Textile Company’s brand mix shift further illustrates how producers migrate toward differentiated SKUs with stronger pricing power.

By Material: Cotton Dominant, Alternative Materials Gaining Momentum

In the global bed and bath linen market, cotton emerged as the largest material segment in 2025, accounting for approximately 65% of total market revenue (USD billion terms). This dominance is primarily driven by cotton’s natural softness, breathability, and high comfort levels, which make it the preferred choice for everyday household use. Cotton linens are also widely valued for their durability and ease of maintenance, supporting repeated washing without significant loss of quality. In addition, the material is broadly available across price ranges, enabling strong adoption in both mass-market and premium segments. The well-established global cotton supply chain and widespread consumer familiarity further reinforced its leading market position in 2025.

Other materials, including bamboo, hemp, and blended fabrics, are expected to be the fastest-growing segment in the global bed and bath linen market during 2026–2031, registering a CAGR of 5.85%. This growth is driven by rising consumer awareness of sustainability, eco-friendly production, and reduced environmental impact. Bamboo and hemp linens are increasingly favored for their moisture-wicking, antibacterial, and temperature-regulating properties, particularly in premium and wellness-focused households. Growing urbanization and higher disposable incomes are also encouraging consumers to experiment with innovative and performance-based materials. As brands continue to expand their sustainable product portfolios, alternative materials are expected to gain stronger traction across global markets.

By End User: Residential Dominant, Hospitality Fastest

Residential accounted for 74.40% in 2025, while the commercial side is set to expand at a 6.54% CAGR in 2026-2031. Consumer channels continue to shift toward e-commerce, and Williams-Sonoma’s large online mix shows how integrated digital merchandising supports sell-through in bath and bedding. The company’s 98% sustainably sourced cotton target also serves as a de facto benchmark for the sector, pressuring smaller firms to align and certify. In the United States, shipments and inventory data for textile products through late 2025 pointed to stability, but scheduling and inventory control remain tight as retailers adjust to demand signals. For institutional buyers, the share of standardized white-label imports remains high for North American and European contracts, and Indian exporters reported substantial 2023 values in bed linens and terry towels into these markets.

Healthcare and eldercare institutions require strict laundry and hygiene standards, which concentrate volumes into large contracts and raise specification baselines for finishing and durability. Public tender documents in Europe increasingly reference OEKO-TEX Standard 100 compliance, and the 2025 PFAS and BPA thresholds cement that expectation in procurement. U.S. landfill data continues to influence take-back pilots among laundries and institutional buyers, who are testing refurbishment and life extension as part of ESG plans. Recent inventories and shipment ratios indicate balanced supply-demand rather than speculative builds in late 2025, and exporters have held volumes through 2024. Although select retail brands reported smaller segments in India relative to export giants, this asymmetry reflects distinct strategies and scale positions between domestic retail and B2B export channels.

By Distribution Channel: B2C/Retail Dominant, Online Gaining Momentum

In the global bed and bath linen market, B2C and retail distribution channels dominated in 2025, accounting for approximately 78% of total market revenue in USD billion terms. This dominance is largely driven by consumers’ preference to physically examine fabric quality, softness, and color before making a purchase. Brick-and-mortar stores also offer immediate product availability, which remains an important factor for household essentials such as bed and bath linens. In addition, established retail brands and specialty home furnishing stores provide a wide range of options across price points, supporting high sales volumes. Strong retail networks across both developed and emerging economies further reinforced B2C channels' leading position in 2025.

Online platforms within the B2C segment are expected to be the fastest-growing distribution channel in the global bed and bath linen market during 2026–2031, registering a CAGR of 7.20%. This rapid growth is driven by increasing internet penetration, smartphone usage, and the expansion of e-commerce infrastructure worldwide. Consumers are increasingly attracted to online shopping for its convenience, home delivery, and easy price comparisons across brands. The availability of detailed product descriptions, customer reviews, and flexible return policies has also improved consumer confidence in purchasing linens online. Additionally, aggressive digital marketing, discounts, and exclusive online collections by leading brands are accelerating the shift toward e-commerce channels.

Geography Analysis

North America held a meaningful share in 2025 while Asia-Pacific recorded the fastest expansion, supported by India’s export volumes and China’s manufacturing scale. U.S. imports of home furnishings were high in 2021, and subsequent declines in domestic output reinforced reliance on imports in retail channels. Year-to-date shipments and inventory balances through late 2025 indicated cautious replenishment among U.S. textile producers, consistent with a normalization path after pandemic disruptions. Intra-Asia dynamics are important, with India’s 2023 export tally for bed linens and terry towels underpinning supplier relevance in Western markets. China’s HS 6302 export base remained significant in 2023, while internal demand was largely served by its e-commerce platforms.

Asia-Pacific’s momentum also stems from regional consumption growth and supply-side integration, with India’s South and West regions showing distinct patterns in 2025 and beyond. India’s production clusters in Panipat, Karur, Erode, and Coimbatore support vertically integrated export operations across sheets, towels, and institutional products. Leading Indian producers reported fiscal 2026 and fiscal 2024 updates, showing variable utilization rates aligned with firm order flows and stable export demand. China’s textile value-added and output measures reflected structural headwinds in 2023, but urban demand remained resilient as Tier 2 and Tier 3 cities adopted Western-style bedding formats. Southeast Asian markets present mixed conditions, with developed retail in Singapore and Malaysia and emerging production-consumption dynamics in Thailand, Indonesia, and Vietnam.

Europe’s import value for bed textiles was large in 2024, and developing-country sources grew faster than the regional average, highlighting the importance of South Asian supply. Germany remained the largest EU importer, and France, the United Kingdom, and the Netherlands were also sizable demand centers for bed and bath categories. Price and confidence indicators in the Netherlands suggested stabilization by late 2025, while French textile and clothing consumption was close to pre-pandemic baselines by mid-2025. Italian textile sales tracked lower in 2023, and exports eased, with luxury producers maintaining niche positions in jacquard and premium fabrication. In Latin America, Chile’s 2024 import composition showed bed sheets and towels as the largest categories, with India leading towel imports under favorable tariff treatment, and Argentina’s import rebound in 2025 reflected a post-liberalization adjustment.

Competitive Landscape

The bed and bath linen market is fragmented, with a mix of large integrated manufacturers, powerful retail brands, and scaled direct-to-consumer players. Indian and Pakistani exporters retain a significant B2B share with vertical integration that reduces lead times and improves cost positions. Welspun operates large bath and bed capacities and reported a year-on-year revenue decline and EBITDA compression in Q2 FY26, reflecting input and demand dynamics. Indo Count pursued forward integration through U.S. acquisitions to serve hospitality segments with faster cycle times and recognized American store brands. Alok’s fiscal 2024-25 mix shift, with growth in terry towels and a decline in bedding, mirrored end-market replacement patterns and buyer priorities.

Retailers with proprietary design and omnichannel strengths exert strong category influence through pricing power and private-label development. Williams-Sonoma delivered USD 7.71 billion of fiscal 2024 net revenues, with 66% from e-commerce, demonstrating digitally enabled scale in bedding and bath. Digital-native brands leveraged sustainability certifications like GOTS to command premiums and capture repeat purchasers, supporting gross margins even with higher acquisition costs. Across institutional tenders, compliance credentials and tested durability matter more than consumer-facing brand equity, and bidders compete on total cost of ownership and performance in industrial laundering. Better Cotton’s 2025 traceability milestone marked a shift from basic compliance to proof of chain custody, increasingly central to sourcing decisions in multinational retail.

Strategy is converging on vertical integration, traceable inputs, product innovation, and energy management across mills and converters. Williams-Sonoma’s sustainably sourced cotton share set a benchmark that is influencing peer commitments and supplier scorecards. U.S. premium manufacturers intensified their process certifications to support premium positioning in luxury hospitality and residential channels. American Textile Company highlighted a long-running pivot toward branded offerings, which reinforced the margin benefits of differentiated SKUs. Regional rebalancing continues as buyers diversify their supply across South Asia, China, and nearshore options, while selective luxury producers focus on high-value niches.

Bed And Bath Linen Industry Leaders

Welspun Living Limited

Williams-Sonoma Inc.

WestPoint Home LLC

Alok Industries Limited

American Textile Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Bed Bath & Beyond announced a merger agreement to acquire The Brand House Collective for approximately USD 26.8 million, combining Bed Bath & Beyond's home brands and digital reach with The Brand House Collective's merchant-led model and store-conversion expertise to enhance growth in the home goods sector, including bed and bath products.

- September 2025: Indo Count introduced Beautyrest bedding along with new bed pillows, mattress pads, and toppers focused on deeper, cooler sleep.

- August 2025: Trident Threads UK launched a new collection of premium bedsheets, towels, bathrobes, and accessories made with eco-conscious materials and processes.

Global Bed And Bath Linen Market Report Scope

A complete background analysis of the bed and bath linen market, which includes an assessment of the parental market, emerging trends by segments and regional markets, along with significant changes in market dynamics and market overview is covered in the report.

By Product

| Bed linen | Bedsheets |

| Pillows and Pillow Cases | |

| Duvets and Duvet Cases | |

| Blankets and Quilts | |

| Mattress Protectors or Pads | |

| Other Bed Linen Products (bed skirts, throw blankets, throw pillows, pillow shams) | |

| Bath linen | Bath Towels |

| Bathrobes | |

| Bathmats | |

| Other Bath Linen Products (face towels, shower curtains) |

By Material

| Cotton |

| Linen |

| Polyester |

| Other Materials (bamboo, hemp, silk, wool, etc.) |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels & Resorts) |

| Healthcare & Elderly-care Facilities | |

| Institutional (Dorms, Military, etc.) | |

| Other Commercial End-Users |

By Distribution Channel

| B2C/Retail Channels | Multi-Brand Stores (home centers, supermarkets, departmental stores, others) |

| Specialty Bedding Stores (including exclusive brand outlets) | |

| Online | |

| Local Mom and Pop Stores (unorganized market) | |

| Other Distribution Channels (teleshopping, mail order, etc.) | |

| B2B/Directly from Manufacturers by Large Commercial Users |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Aisa-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product | Bed linen | Bedsheets |

| Pillows and Pillow Cases | ||

| Duvets and Duvet Cases | ||

| Blankets and Quilts | ||

| Mattress Protectors or Pads | ||

| Other Bed Linen Products (bed skirts, throw blankets, throw pillows, pillow shams) | ||

| Bath linen | Bath Towels | |

| Bathrobes | ||

| Bathmats | ||

| Other Bath Linen Products (face towels, shower curtains) | ||

| By Material | Cotton | |

| Linen | ||

| Polyester | ||

| Other Materials (bamboo, hemp, silk, wool, etc.) | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels & Resorts) | |

| Healthcare & Elderly-care Facilities | ||

| Institutional (Dorms, Military, etc.) | ||

| Other Commercial End-Users | ||

| By Distribution Channel | B2C/Retail Channels | Multi-Brand Stores (home centers, supermarkets, departmental stores, others) |

| Specialty Bedding Stores (including exclusive brand outlets) | ||

| Online | ||

| Local Mom and Pop Stores (unorganized market) | ||

| Other Distribution Channels (teleshopping, mail order, etc.) | ||

| B2B/Directly from Manufacturers by Large Commercial Users | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Aisa-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the bed and bath linen market?

The bed and bath linen market size is estimated at USD 108.70 billion in 2026, and is projected to reach USD 143.49 billion by 2031, at a CAGR of 5.70% during 2026-2031.

Which product and end-use segments are leading growth?

Bed linen held 70% of 2025 product revenues and is the fastest-growing product segment; residential accounted for 74.40% in 2025, and the commercial segment is projected to expand at a 6.54% CAGR during 2026-2031.

How are channels evolving in the bed and bath linen market?

B2C / Retail channels held 78% in 2025, but online (within B2C) is projected to grow at a 7.20% CAGR through 2031, supported by improved last-mile logistics and visualization tools.

What years does this Bed and Bath Linen Market cover?

The report covers the bed and bath linen market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Bed and Bath Linen Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Which regions are most influential in supply and demand?

Asia-Pacific is the fastest-growing region, driven by India’s export scale and China’s manufacturing base, while North America sustains import-led demand and Europe balances cost with sustainability in sourcing.

What certifications and regulations are shaping specifications?

OEKO-TEX Standard 100 tightened PFAS and BPA thresholds in 2025, GOTS expanded certified chain-of-custody coverage, and Better Cotton’s traceability is now a procurement baseline.

Page last updated on: