Market Overview

| Study Period | 2020 - 2031 |

|---|---|

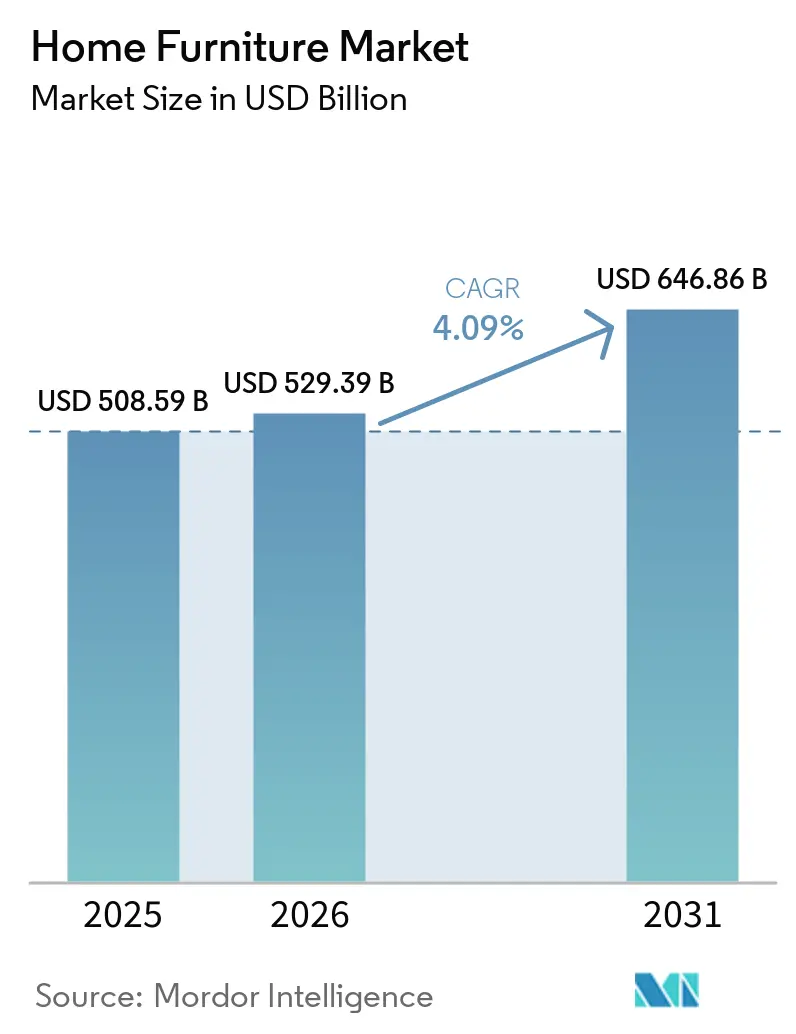

| Market Size (2026) | USD 529.39 Billion |

| Market Size (2031) | USD 646.86 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

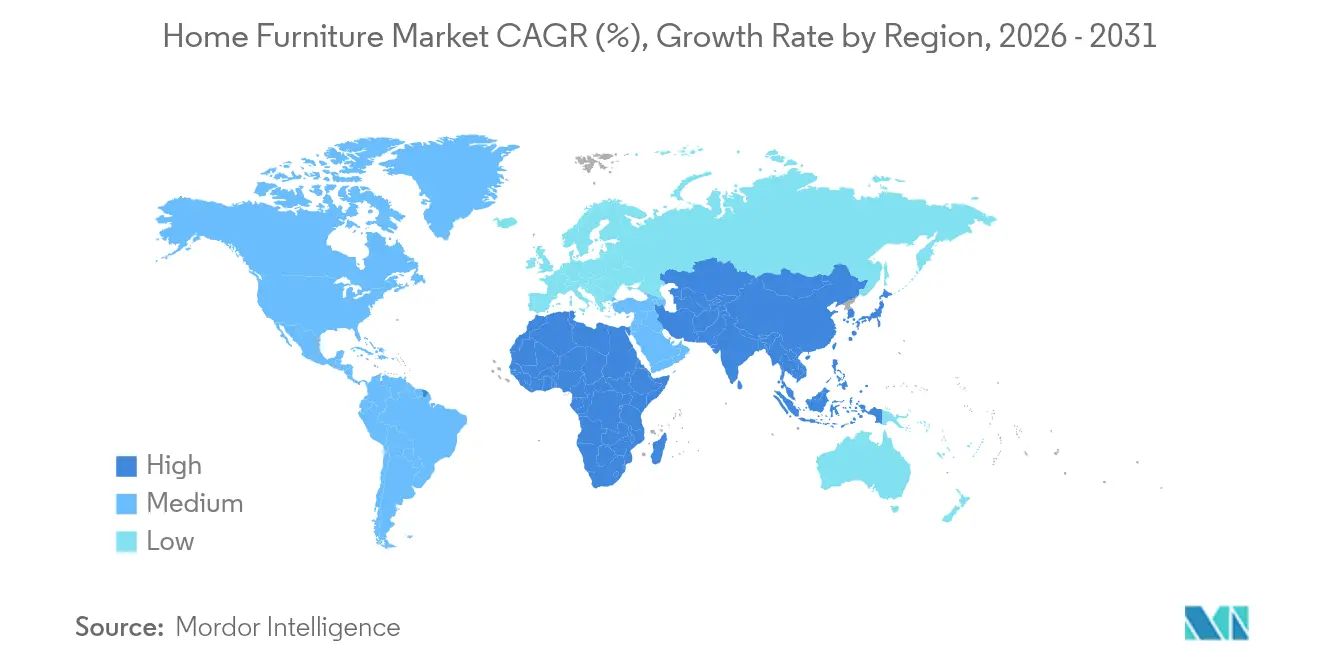

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Furniture Market Analysis by Mordor Intelligence

The Home Furniture Market size is expected to grow from USD 508.59 billion in 2025 to USD 529.39 billion in 2026 and is forecast to reach USD 646.86 billion by 2031 at 4.09% CAGR over 2026-2031.

Demand momentum is strongest in the home-office category as hybrid work models normalize, with consumers favoring multifunctional pieces that blend professional ergonomics with residential aesthetics. Digital manufacturing and artificial-intelligence-driven design shorten product cycles, enabling brands to introduce personalized collections that capture premium margins while controlling costs. Sustainability imperatives push companies toward circular production and certified timber sourcing, turning compliance into a competitive differentiator. Supply-chain optimization remains pivotal because ocean-freight volatility and currency swings directly influence pricing strategies and gross margins in the home furniture market[1]United Nations Conference on Trade and Development, “Review of Maritime Transport 2024,” unctad.org. .

Key Report Takeaways

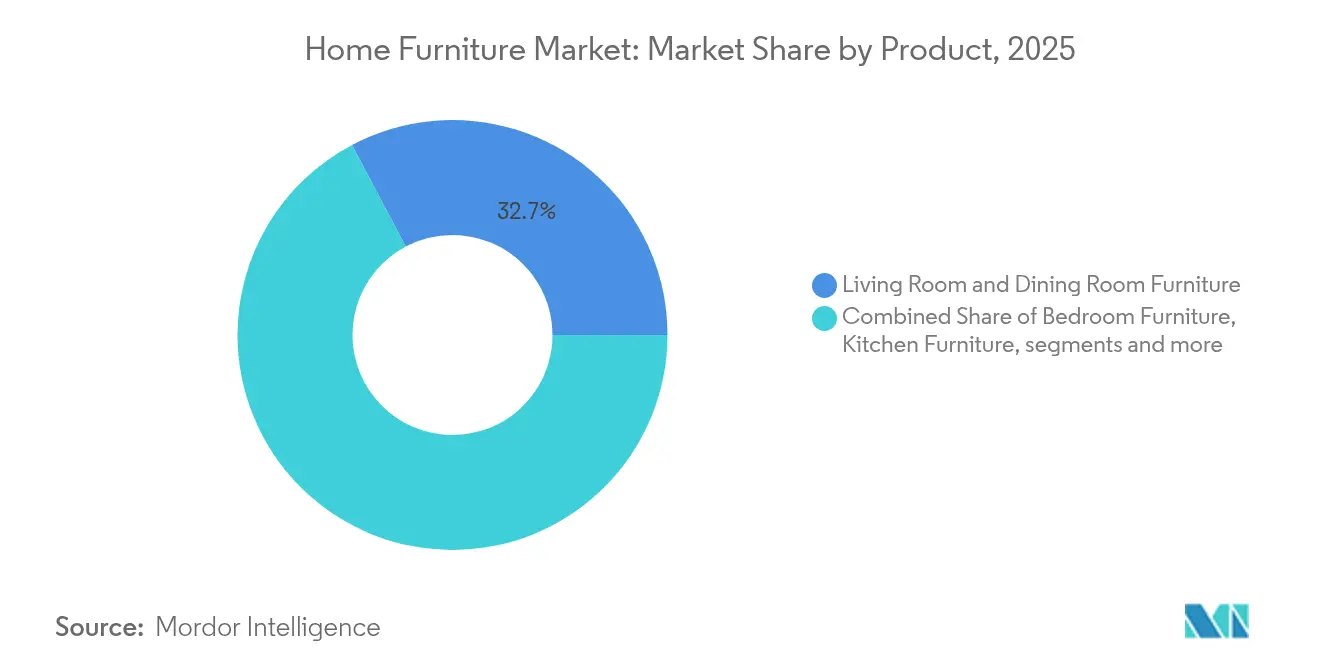

- By product, Living Room & Dining Room furniture held 32.74% of the global home furniture market share in 2025, while Home Office furniture posted the fastest 4.10% CAGR through 2031.

- By material, wood accounted for 41.88% of the home furniture market size in 2025, whereas plastic & polymer materials are pacing ahead with a 4.85% CAGR to 2031.

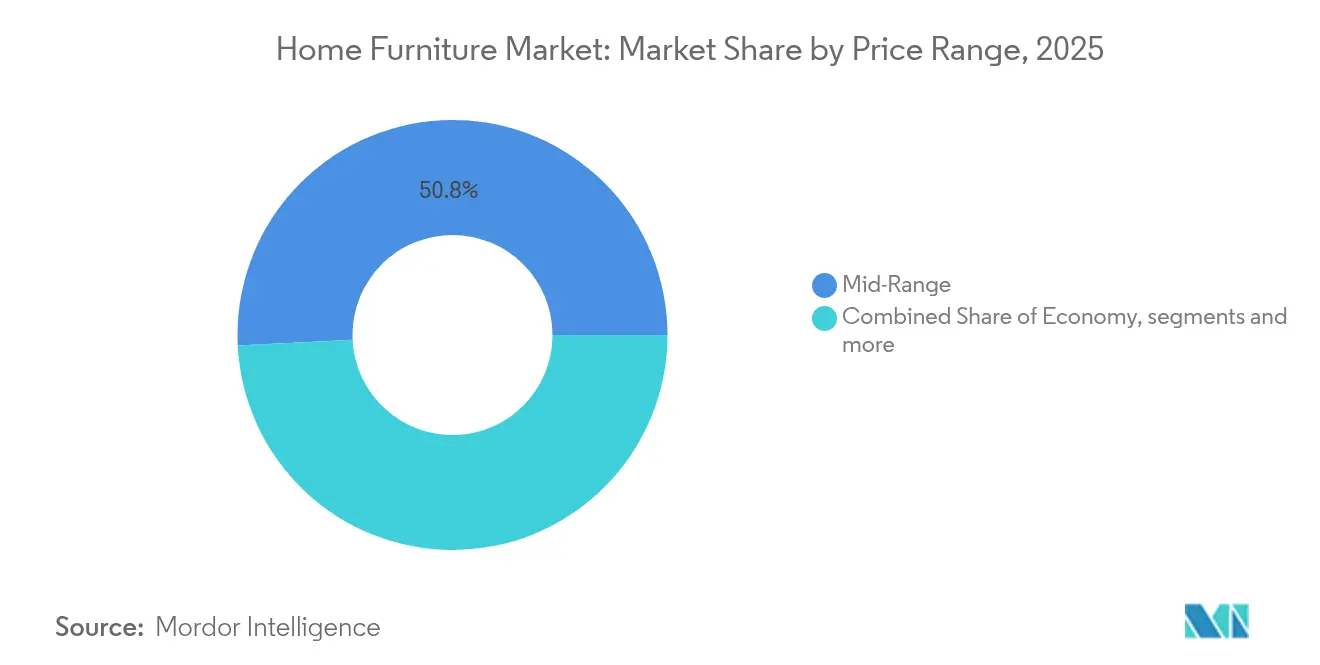

- By price range, mid-range offerings captured 50.77% of 2025 revenue; premium lines are projected to expand at a 4.61% CAGR to 2031.

- By distribution channel, specialty stores accounted for 45.02% of the revenue in 2025, while online platforms are expected to see the highest 6.38% CAGR through 2031.

- By geography, the Asia-Pacific region commanded 38.02% of 2025 revenue in the global home furniture market and is projected to grow at a 6.66% CAGR, reflecting its dual strength in manufacturing and consumption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic hybrid-working lifts home-office furniture demand | +0.8% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Growing millennial & Gen-Z home-ownership in emerging markets | +1.2% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Expansion of organized retail chains in Tier-2/3 cities | +0.6% | Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Mass-customization enabled by Industry 4.0 manufacturing | +0.7% | Global, with early adoption in North America & Europe | Long term (≥ 4 years) |

| Shift toward certified sustainable timber sourcing | +0.5% | Global, regulatory-driven in EU | Long term (≥ 4 years) |

| AI-driven design platforms shortening concept-to-launch cycles | +0.4% | Global, technology leaders first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid work lifts home-office demand

Hybrid work schedules have sustained elevated spending on home office furniture. Employers are allocating a portion of their capital expenditures (CAPEX) to subsidize ergonomic desks and chairs, aiming to enhance employee retention. Manufacturers are addressing this demand by introducing compact sit-stand desks, hidden cable systems, and mobile storage solutions that integrate seamlessly into home spaces. Regulatory overlaps between workplace safety and home ergonomics could lead to stricter product specifications, creating higher entry barriers for new players. This shift ensures durable revenue streams for manufacturers. Additionally, the trend persists even as commercial real estate occupancy rates stabilize.

Millennial & Gen-Z home-ownership growth

Millennial and Gen-Z consumers are driving demand for starter furniture suites as they increasingly become first-time homeowners in emerging economies. These groups prioritize sustainably sourced, modular furniture that accommodates frequent moves and conduct thorough online research before purchasing. Flexible payment options like Buy-Now-Pay-Later and subscription models appeal to their financial preferences, encouraging higher-value purchases. Social media plays a significant role, influencing 70% of their buying decisions, which pushes brands to optimize their influencer marketing strategies. This demographic shift is expected to sustain steady growth in furniture volumes, extending beyond urban centers in the long term.

Organized retail expansion in Tier-2/3 cities

Global brands are opening compact showrooms, typically 10,000 sq ft or smaller, to expand into secondary cities where rising disposable incomes are driving aspirational shopping. Enhanced logistics corridors have reduced delivery times, enabling same-week installations that were previously limited to capital cities. Product assortments are customized to local preferences, such as lighter colors for tropical climates and space-saving designs for smaller apartments. To compete with unorganized carpentry shops, brands are adopting aggressive price-value strategies, particularly in the mid-range segment. Government initiatives, including urbanization policies and smart-city grants, are further boosting retail traffic and furniture demand. These factors collectively position secondary cities as key growth areas for global furniture brands.

Industry 4.0 mass-customization

Artificial intelligence-driven configure-price-quote platforms now integrate seamlessly with flexible CNC lines, enabling the cost-efficient production of unique bookcases. This approach achieves cost efficiencies comparable to batch runs. Real-time order tracking has significantly reduced the concept-to-delivery timeline from months to weeks. Virtual showrooms allow consumers to co-create finishes and dimensions, enhancing emotional attachment and lowering return rates. These features support premium mark-ups, offsetting the capital investment in robotics and MES software. Over time, companies adopting digital factories are expected to widen profitability gaps compared to traditional mass producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile ocean-freight rates squeezing margins | -0.9% | Global, particularly affecting import-dependent markets | Short term (≤ 2 years) |

| Soaring lumber prices due to climate-driven supply shocks | -0.7% | Global, with regional variations based on local supply | Medium term (2-4 years) |

| EU "Right-to-Repair" & circular-economy mandates raising compliance costs | -0.4% | Europe primary, global spillover through multinational compliance | Long term (≥ 4 years) |

| Rising popularity of furniture rental curbing replacement cycles | -0.5% | Urban centers globally, strongest in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile ocean-freight rates

Between 2023 and 2024, container costs surged by 120%, significantly impacting margins for exporters dependent on long-haul shipping lanes. While some manufacturers mitigate this by securing annual freight contracts, smaller firms often lack the bargaining power to obtain favorable terms. Nearshoring efforts in regions like Mexico and Eastern Europe help avoid congested ports, though initial relocation costs limit immediate savings. To counter rising shipping rates, companies are re-engineering packaging to optimize cube utilization, fitting more units per container. Diversifying shipping routes and expanding regional warehouse networks will be critical for future margin recovery.

Growing rental popularity

Subscription platforms are experiencing triple-digit growth as urban professionals increasingly prefer flexible access over ownership, extending replacement cycles for traditional sales. Furniture designed for multiple refurbishment loops is gaining popularity, while lightweight, flat-pack designs simplify reverse logistics. Some manufacturers are experimenting with in-house leasing models to capture lifetime customer value, though managing residual asset risk introduces balance-sheet complexities. Growing awareness of the circular economy is aligning rental models with sustainability goals, enhancing their appeal to consumers. If this trend continues, it could limit unit sales growth while driving an increase in total service revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Home Office Drives Growth

Living Room & Dining Room sets held a 32.74% slice of 2025 revenue, underscoring their centrality to social interaction and entertainment trends within the home furniture market. Home Office furniture posted the quickest 4.10% CAGR as employers reimbursed ergonomic setups, boosting a niche that bridges residential comfort with professional utility. Bedroom and kitchen lines enjoy steady baseline demand because replacements follow life-stage events such as marriage or relocation, offering predictable cycles for inventory planning. Outdoor pieces attract renewed interest in suburban and rural zones where consumers extend living spaces, creating opportunities for weather-resistant composites. Multifunctionality now permeates every category, with storage ottomans and modular sofas illustrating how product innovation solves space constraints.

Designers increasingly embed USB-C chargers and IoT sensors into premium desks and nightstands, elevating perceived value while prompting higher price points in the home furniture market. Industry 4.0 production supports custom size and fabric choices, stimulating direct-to-consumer startups that bypass wholesale margins. Sustainability overlays every product brief, prompting FSC-certified wood and recycled-plastic inserts to satisfy eco-conscious buyers. Regional taste nuances-such as minimalism in Japan and ornate finishes in the Middle East-require localized SKU matrices that balance volume with design authenticity. Supply-chain data analytics guide demand forecasting, reducing markdown risks and protecting gross margin.

By Material: Sustainable Innovation Accelerates

Wood remained the material of choice in the home furniture market with a 41.88% hold on 2025 revenue, supported by certified forestry programs that assure buyers of responsible sourcing. Plastic & polymer pieces grow fastest at 4.85% CAGR because bio-based resins and recycled PET blends improve environmental footprints without sacrificing durability. Metal frames dominate institutional and garden segments, favored for longevity and sleek aesthetics that match modern architecture. Alternative materials, from bamboo composites to mushroom-based panels, inch into mainstream catalogs as experimentation scales up. Innovation in surface finishing replicates oak grain on polymer boards, helping price-sensitive customers access upscale looks.

Supply traceability platforms log chain-of-custody data, giving brands audit evidence and a marketing narrative around ethical sourcing within the home furniture market. Material diversity mitigates risk-loss of Russian birch veneer pushed European producers to Indonesian rubberwood and Brazilian eucalyptus substitutions. Composite technology blends sawdust with recycled plastics, cutting landfill input while delivering moisture resistance. Consumer education via QR codes explains life-cycle impacts, boosting trust and premium willingness. Over time, competitive advantage will hinge on mastering circular-ready materials that ease dismantling and component reuse.

By Price Range: Premium Growth Momentum

Mid-range lines captured 50.77% of 2025 spending, signaling a dominant value-conscious segment where durability meets affordability, particularly important amid inflationary pressures. Premium collections are forecast to rise at a 4.61% CAGR as affluent households pay for signature design, limited-edition collaborations, and sustainability certifications that double as status badges. Economy products still target entry-level and student populations, yet rising raw-material costs compress margins unless offset through automation. The home furniture market size for upscale pieces benefits from direct-to-consumer models that preserve luxury margins by trimming retail layers. Digital storytelling and influencer collaborations elevate perceived scarcity, nurturing brand mystique.

Flexible financing, installment plans, and Buy-Now-Pay-Later options-broaden access across tiers, lifting average order values without immediate cash-flow strain. Premium buyers expect bespoke services, driving white-glove delivery and augmented-reality room planners that visualize curated sets. Mid-range competitiveness relies on lean supply chains and modular architectures that share components across collections to achieve scale economies. Economy lines may pivot to rental fleets, generating annuity revenue while satisfying circular-economy targets. Price polarization will likely widen, requiring brands to define clear value propositions rather than straddling all tiers.

By Distribution Channel: Digital Transformation Accelerates

Specialty stores retained 45.02% of 2025 revenue because tactile evaluation and in-store advice remain critical in high-involvement purchasing decisions within the home furniture market. Online platforms, however, are projected to outpace others with a 6.38% CAGR, boosted by AR visualization, AI stylist chats, and real-time stock visibility. Home centers cater to repair or renovation buyers needing immediate pick-up of functional items. Department and hypermarket aisles capture impulse buys, particularly entry-level storage units and flat-pack accessories. Omnichannel strategies integrate click-and-collect and ship-from-store services that shorten last-mile costs and enhance convenience.

Compact studio showrooms in malls or transit hubs display only best-sellers, streaming full assortments on interactive screens, enabling footprint-light expansion into secondary cities. Direct-to-consumer brands use social commerce and micro-influencers for traffic generation, converting with seamless checkout and white-label logistics. Fulfillment networks leverage regional hubs to promise two-day delivery even on bulky sofas, protecting customer satisfaction metrics. Data pooling across channels informs dynamic pricing that reflects local promotions, competitor moves, and freight fluctuations. Regulatory scrutiny on digital-marketplace data privacy may require additional compliance investment, especially in Europe.

Geography Analysis

Asia-Pacific accounted for 38.02% of global revenue in 2025, reflecting cost-competitive production clusters and burgeoning urban middle-class demand that anchor the home furniture market. Rapid e-commerce adoption and growing home-ownership in Tier-2 Chinese and Indian cities extend market reach beyond coastal megacities. Government incentives for smart-factory upgrades accelerate technology penetration, raising local suppliers’ quality to global benchmarks. Regional design language blends minimalist Scandinavian influences with indigenous motifs, sparking product differentiation. Freight proximity to raw-material sources like Malaysian rubberwood supports margin resilience against currency swings.

North America displays mature penetration yet retains innovation leadership in circular-ready products, reclaimed lumber usage, and ergonomic research, providing a blueprint for premium differentiation in the home furniture market. The United States benefits from nearshoring in Mexico, which trims lead times and insulates brands from trans-Pacific freight shocks. Canadian demand rebounds as housing starts stabilize, especially in suburban single-family developments that require full-suite furnishing. Sustainability regulations, including California’s extended producer responsibility rules, shape supplier selection and packaging design. Digital marketplace consolidation favors larger players that can absorb rising fulfillment costs.

Europe experiences moderate growth in the home furniture market, but commands influence through stringent environmental directives like the Right-to-Repair mandate, giving local makers first-mover advantage in circular solutions. Germany and the Nordics showcase high per-capita spending and preference for certified wood lines, while Southern Europe leans toward artisanal craftsmanship and solid-wood dining sets. Currency volatility due to macroeconomic shifts prompts hedging and localized production for euro-zone sales. Middle East and Africa represent long-range opportunities, with Gulf states investing in hospitality projects that demand bespoke luxury collections. Latin America gains traction as retailers invest USD 600 million in new outlets across five countries, signaling market formalization.

Competitive Landscape

Intense fragmentation defines the home furniture market, with regional specialists coexisting alongside global giants, leaving no single firm above a single-digit share threshold. Consolidation accelerates, evidenced by HNI Corporation’s USD 2.2 billion purchase of Steelcase, expected to deliver USD 50 million yearly cost synergies from 2026. Technology-savvy leaders install MES platforms and collaborative robots, cutting unit labor costs and shrinking design-to-market lead times. Direct-to-consumer entrants leverage agile digital marketing and zero-inventory dropshipping, challenging brick-and-mortar heavyweights on speed and price transparency. Sustainability credentials transform from nice-to-have to cost-of-entry as EU regulations push recycled content quotas.

Supply-chain resilience becomes a critical moat: diversified sourcing, multi-port logistics, and dual-supplier strategies mitigate geopolitical risk and freight shocks. Brands deploy virtual reality showrooms and 3D planners, reducing return rates and boosting conversion, further blurring online–offline boundaries. Rental and furniture-as-a-service models gain investor backing; Vesta’s acquisition of Fernish and Feather underscores momentum toward subscription revenue. Product innovation targets hybrid needs, such as desks doubling as dining consoles, courtesy of slide-out mechanisms and wireless charging pads. Localized micro-factories near urban demand centers cut delivery windows to under 48 hours while fulfilling custom orders.

Competitive intensity in the home furniture market also revolves around material science: firms investing in recycled-plastic panels and FSC-certified timber enjoy procurement preference from eco-label-conscious retailers. Partnership with designers and technology start-ups injects fresh aesthetics and smart features into traditional silhouettes, sustaining consumer excitement. Marketing spends gravitate toward social storytelling, leveraging user-generated content for authenticity. Brands guard margins through strategic SKU pruning, focusing on fast-moving core assortments while licensing low-velocity designs to third parties. Longer term, leaders able to marry digital customization, circular supply chains, and omnichannel reach are poised to command outsized influence on category standards and pricing power.

Home Furniture Industry Leaders

Ikea

La-Z-Boy

Ashley Furniture Industries Inc.

Steinhoff International Holdings N.V.

Herman Miller, Inc. (inc. Knoll)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: HNI Corporation announced its acquisition of Steelcase Inc. in a USD 2.2 billion deal, creating one of the largest office furniture companies globally and expected to generate approximately USD 50 million in annual cost synergies by 2026, reflecting commercial-segment consolidation.

- August 2025: MasterBrand and American Woodmark announced their merger, combining two significant players in kitchen and bath cabinetry to enhance scale and market coverage, with operational efficiencies targeted across residential and commercial channels.

- June 2025: IKEA confirmed plans to open 58 new stores worldwide in fiscal 2025, alongside price cuts of up to 50% in its restaurants, illustrating its commitment to omnichannel expansion despite margin pressure.

- May 2025: Royaloak outlined a roadmap for 25 additional stores and revenue goals of INR 1,000 crore (USD 120 million) for FY26, signaling aggressive growth ambitions by the Indian retailer.

Global Home Furniture Market Report Scope

"Home furnishings are items placed in a room to make it comfortable and appealing. They include all the movable objects, such as furniture, curtains, carpets, and décor items that complement the room's design. Home furnishings are an essential part of interior design, and they can give a room a unique personality. A complete background analysis of the global home furniture market, which includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report.

The home furniture market is segmented by product, distribution channel, and geography. By product, the market is sub-segmented into living room and dining room furniture, bedroom furniture, kitchen furniture, lamps and lighting furniture, and plastic and other furniture. By distribution channel, the market is sub-segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels and geography, the market is sub-segmented into North America, South America, Europe, Asia-Pacific, and the Middle-East and Africa. The report offers market size and forecasts for the home furniture market in value (USD) for all the above segments."

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores (including exclusive brand outlets and local stores from the unorganized sector) |

| Online |

| Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.) |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product | Living Room & Dining Room Furniture | |

| Bedroom Furniture | ||

| Kitchen Furniture | ||

| Home Office Furniture | ||

| Bathroom Furniture | ||

| Outdoor Furniture | ||

| Other Furniture | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Others | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | Home Centers | |

| Specialty Furniture Stores (including exclusive brand outlets and local stores from the unorganized sector) | ||

| Online | ||

| Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global home furniture market in 2026?

The home furniture market size reached USD 529.39 billion in 2026, reflecting recovery momentum since pandemic lows.

What growth rate is forecast for global home furniture through 2031?

The sector is projected to post a 4.09% CAGR, lifting revenue to USD 646.86 billion by 2031.

Which region drives the fastest expansion?

Asia-Pacific leads with a 6.66% CAGR through 2031, fueled by urbanization, rising incomes, and e-commerce penetration.

Which product line shows the highest growth?

Home Office furniture is set to rise at a 4.10% CAGR as hybrid work continues to influence purchasing decisions.

How are online channels shaping sales?

E-commerce platforms will log a 6.38% CAGR, supported by AR visualization, AI design help, and enhanced logistics.

What impact do sustainability rules have on makers?

Circular-economy mandates push firms toward certified timber, recycled materials, and products designed for repair, adding compliance costs but unlocking premium pricing.

Page last updated on: