Market Overview

| Study Period | 2020 - 2031 |

|---|---|

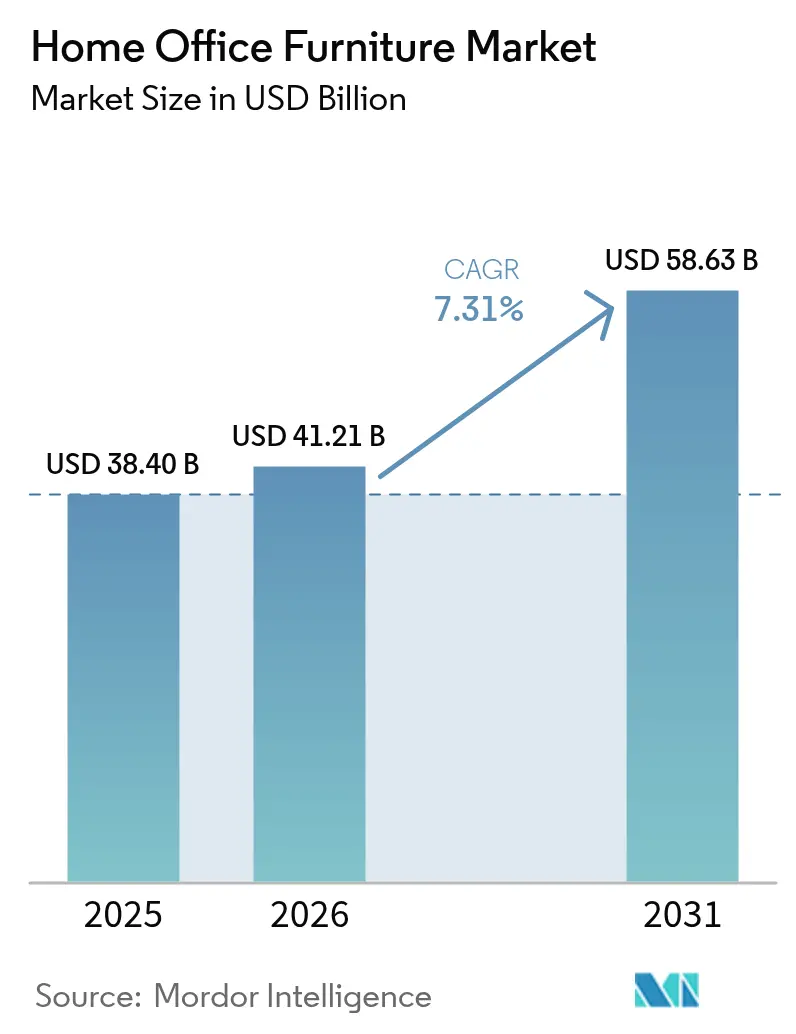

| Market Size (2026) | USD 41.21 Billion |

| Market Size (2031) | USD 58.63 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Office Furniture Market Analysis by Mordor Intelligence

The Home Office Furniture market size is expected to grow from USD 38.40 billion in 2025 to USD 41.21 billion in 2026 and is forecast to reach USD 58.63 billion by 2031 at 7.31% CAGR over 2026-2031.

Sustained hybrid-work policies have moved home workspace spending from discretionary to structural, ensuring a steady demand baseline even as corporate real-estate footprints contract. Asia-Pacific’s manufacturing depth and rising household incomes amplify this momentum, while North America and Europe remain anchored by strict ergonomic guidelines that turn compliance spending into recurring revenue. Online platforms, bolstered by social-commerce tools and quick-ship networks, compress purchase cycles and help mid-tier brands achieve national reach without store build-outs. Material substitution, especially recycled plastics, mitigates input-price shocks and enhances environmental credentials that now influence more than one-third of purchase decisions across developed markets. Competitive intensity stays moderate with the top five suppliers controlling a good chunk of the global revenues, leaving space for design-focused challengers to scale rapidly through direct-to-consumer models.

Key Report Takeaways

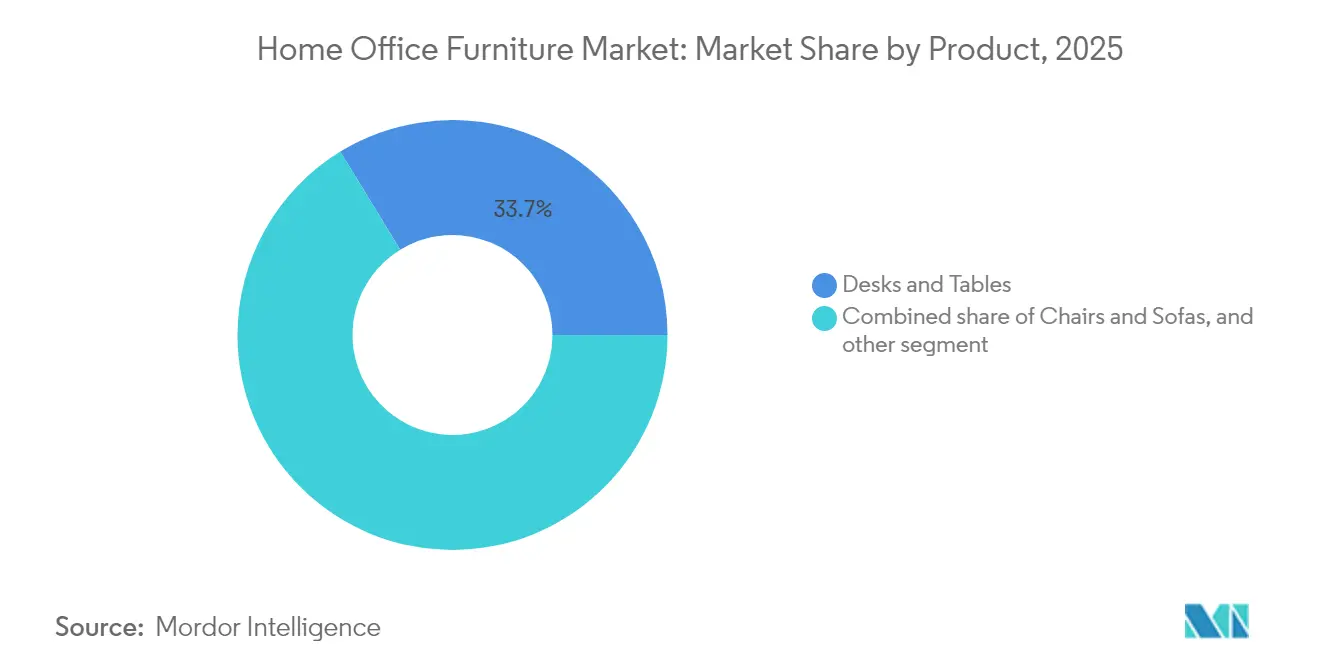

- By product, desks & tables held 33.74% of the home office furniture market share in 2025, while Smart Desks with IoT sensors are forecast to grow at a 10.23% CAGR to 2031.

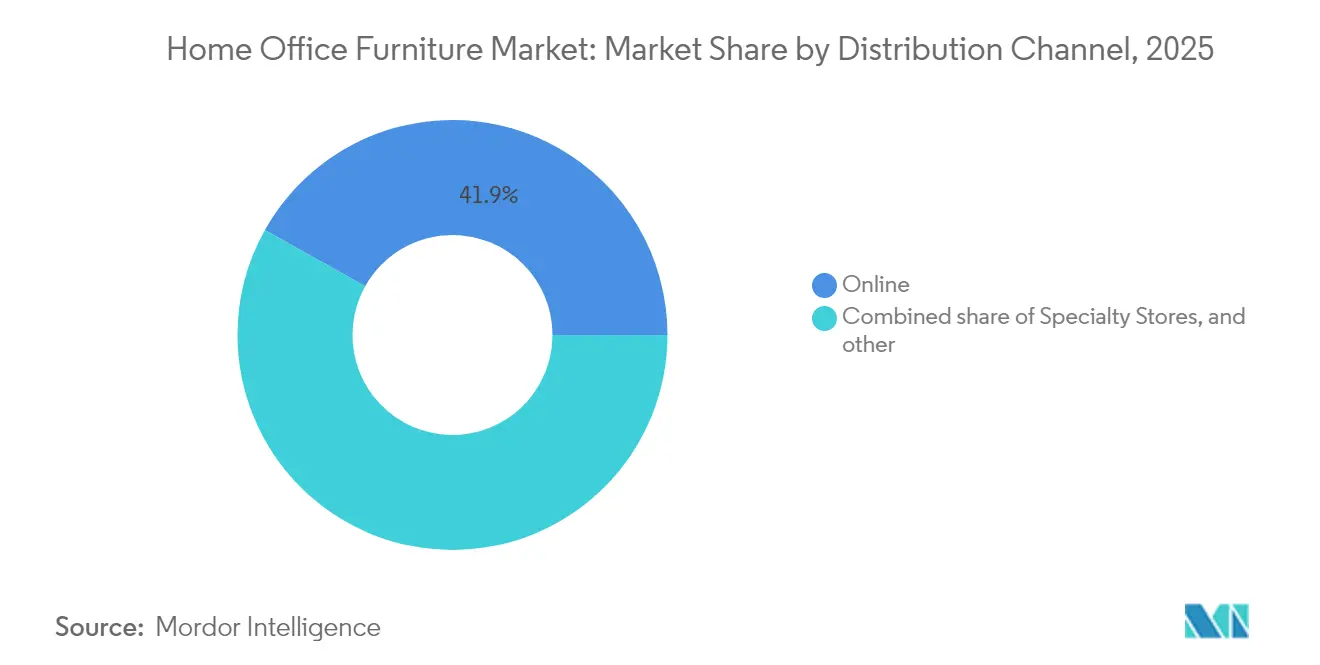

- By distribution channel, the online segment captured 41.88% of the home office furniture market share in 2025; Direct-to-Consumer sales are set to expand at a 14.10% CAGR through 2031.

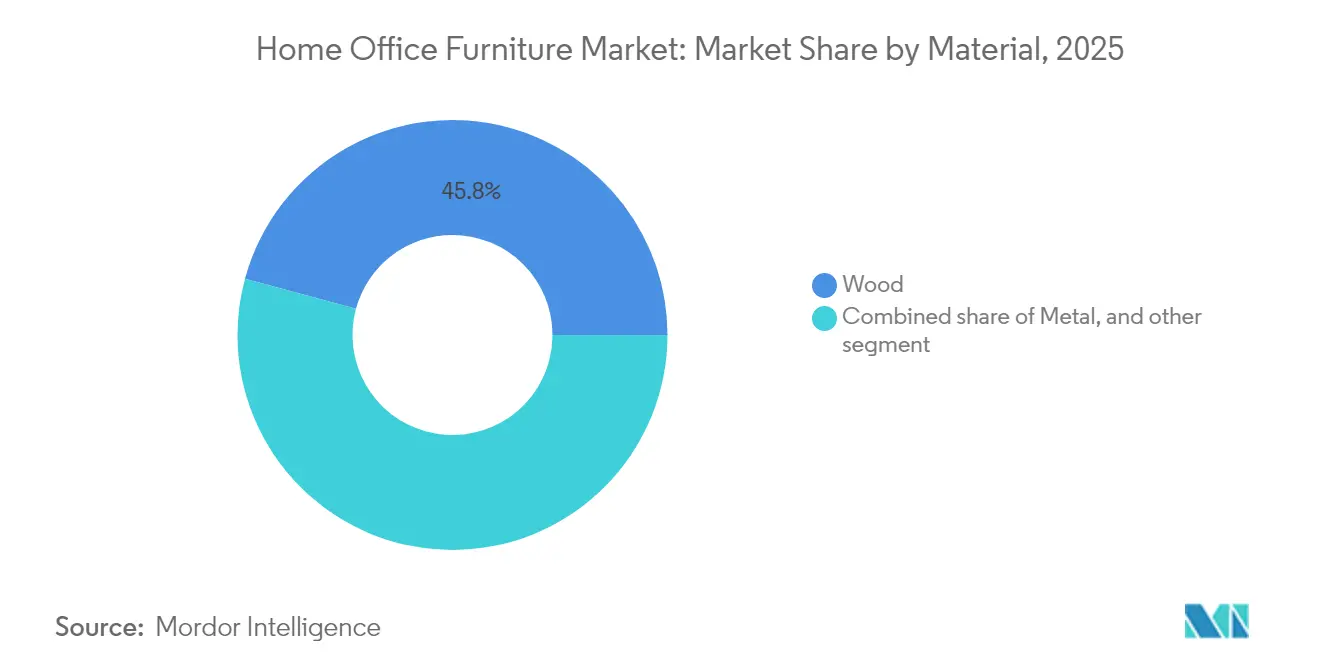

- By material, wood accounted for 45.78% of the home office furniture market size in 2025, whereas Recycled Plastics are advancing at an 8.05% CAGR during the outlook period.

- By geography, Asia-Pacific contributed 38.05% of the home office furniture market share in 2025 and is projected to register a 9.78% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid & remote-work permanence | +2.1% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Surge in ergonomic-wellness regulations | +1.8% | North America & EU primary, APAC emerging | Medium term (2-4 years) |

| Digitally native furniture brands' scale-up | +1.4% | Global, led by APAC and North America | Medium term (2-4 years) |

| Consumer shift to premium multifunctional designs | +1.2% | APAC core, spill-over to North America & EU | Long term (≥ 4 years) |

| Circular-economy resale platforms' growth | +0.7% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-enabled mass-custom manufacturing | +0.6% | APAC manufacturing hubs, global distribution | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid & Remote-Work Permanence

Corporate policies now encode two to three remote days weekly, transforming one-time lockdown purchases into predictable replacement cycles that stabilize the home office furniture market[1]Nicholas Bloom et al., “Survey: Remote Work Isn't Going Away — and Executives Know It,” Harvard Business Review, hbr.org. . Demand extends beyond knowledge workers as sectors such as financial services and healthcare adopt flexible scheduling to widen talent pools. Employers subsidize desk-chair bundles to cut workers’ compensation risk, while insurers increasingly require proof of ergonomic provisioning. Height-adjustable desks, monitor arms, and anti-fatigue mats, therefore, become standard procurement line items rather than elective perks. Sales spikes coincide with corporate hardware refreshes, locking furniture into the same three-to-five-year capex rhythm as laptops. The resulting revenue predictability supports longer production runs that lower unit costs and expand mid-price offerings. Asia-Pacific gains an export advantage because regional factories can switch swiftly between contract and consumer SKUs without violating global quality norms.

Surge in Ergonomic-Wellness Regulations

United States OSHA advisories and EU directives now cover remote settings, mandating adjustable seating, keyboard-tray ergonomics, and minimum lighting levels [2]Heather Ritz, “Top 5 Ergonomic Trends to Watch in 2025,” Briotix Health, briotix.com. . Employers that fail to comply face fines and higher health-insurance premiums, prompting bulk-purchase agreements with certified suppliers. Product certification labels—GREENGUARD, BIFMA LEVEL, and GS—act as tender pre-requisites for enterprise buyers. Manufacturers respond by integrating sensors that measure seat occupancy and posture, generating compliance reports that satisfy auditors. Insurance carriers bundle premium discounts with verified ergonomic deployments, reinforcing hardware upgrades every four years. North American demand spikes first, but similar rules appear in Japan and Australia, suggesting global standardization by 2028. The regulatory floor thus underpins a durable premium segment within the home office furniture market.

Digitally Native Furniture Brands’ Scale-Up

Pure-play e-commerce brands move from niche to mainstream, capturing over one-quarter of incremental category growth between 2022 and 2024, according to trade association shipment data[3]BIFMA, “North American Furniture Trade Under Pressure as Tariff Concerns Grow,” globalwood.org. . Their data-rich direct-to-consumer channels halve design-to-launch cycles by crowdsourcing feature feedback, letting them update SKUs at twice the speed of legacy rivals. Social-media product drops create demand spikes that logistics partners fulfill through micro-fulfillment hubs. Subscription models for desks and chairs emerge, bundling maintenance and upgrade options that flatten revenue seasonality. Traditional retailers counter with online configurators and same-day click-and-collect programs, narrowing experiential gaps. As last-mile costs fall through route-optimization software, online price premiums compress, further shifting volume away from physical stores. The home office furniture market thus pivots to an omnichannel equilibrium in which digital discovery precedes almost every store visit.

Consumer Shift to Premium Multifunctional Designs

Urban households in Tokyo, Mumbai, and São Paulo allocate under 180 square feet for combined living and working needs, spurring demand for desks that convert into dining tables and wall-mounted storage that doubles as video-conference backdrops. Buyers accept 20–35% price premiums when furniture saves space and preserves interior aesthetics. Manufacturers deploy lightweight composites and hidden casters so users can reconfigure rooms daily without specialized tools. Integrated cable-management systems keep work areas uncluttered, a feature consumers rank among their top three purchase criteria in recent user surveys published by component suppliers. Smart-lighting add-ons synchronize with desk height and ambient conditions, further elevating perceived value. As patents in convertible mechanisms rise, entry barriers harden, rewarding early innovators with licensing income. Multifunctional design, therefore, propels average selling prices faster than raw-material inflation, protecting margins across the home office furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material (wood & metal) prices | -1.9% | Global, with highest impact in North America & Europe | Short term (≤ 2 years) |

| Rising freight & logistics costs | -1.3% | Global, particularly affecting import-dependent regions | Medium term (2-4 years) |

| Work-from-home tax incentive roll-backs | -0.8% | North America primary, selective EU markets | Short term (≤ 2 years) |

| Home-space constraints in megacities | -0.6% | APAC megacities, expanding to global urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices

Lumber futures swung 38% between January and July 2025 as wildfire disruptions coincided with tariff uncertainty, eroding gross margins for wood-heavy SKUs. Steel and aluminum spot prices followed energy-cost gyrations, pushing metal-frame chair prices up 6% in North America during Q2. Manufacturers lock in supply through forward contracts, yet smaller vendors lack hedge access and pass costs downstream, dampening demand in price-sensitive segments. Recycled plastic adoption eases some pressures but faces feedstock shortages when consumer-recycling rates dip. Inventory buffers mitigate shocks yet tie up working capital, raising financing costs amid rising interest rates. Price volatility also complicates catalog updates, forcing retailers to issue frequent price-adjustment notices that curb promotional traction. These factors jointly shave nearly two percentage points off the home office furniture market CAGR forecast.

Rising Freight & Logistics Costs

Container spot rates on the Shanghai–Los Angeles route hit USD 4,200 in May 2025—up 75% year-over-year—due to equipment shortages and fuel surcharges. Furniture’s bulky dimensions attract dimension-weight penalties that add 10–12% to landed costs, especially for assembled desks. Retailers shift to flat-pack designs that fit more units per container, but last-mile assembly needs inflate service fees. Manufacturers explore regional production hubs in Mexico and Eastern Europe to shorten transit times, yet navigating multiple regulatory regimes raises compliance complexity. Ocean-freight volatility also triggers inventory-planning errors, resulting in stockouts that prompt consumers to switch brands. While multi-port routing and warehouse automation trim lead times, sustained logistics inflation still subtracts over one point from the category’s long-term growth pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Integration Outpaces Core Lines

Desks & Tables accounted for 33.74% of 2025 revenue and remain the anchor of the home office furniture market; the segment’s stability stems from universal workstation needs and rising ergonomic-height adoption rates. Within this cohort, Smart Desks—a sub-segment equipped with IoT sensors that log posture and usage metrics—are projected to expand at a 10.23% CAGR, far outrunning legacy models. This momentum benefits from enterprise wellness programs that subsidize connected hardware, making real-time analytics a procurement criterion. Chairs & Sofas follow at 29.72% share, lifted by headrest and lumbar innovations that meet updated ISO ergonomics norms. Storage Units, while holding 18.15% share, align closely with hybrid-work patterns as households seek lockable compartments to separate professional files from personal items. The remaining 18.39% share splits across lighting, acoustic panels, and accessories that round out complete workstation environments. Supplier R&D increasingly targets integrated USB-C charging, wireless-power modules, and voice-activated height presets that raise switching costs and deepen replacement cycles.

Manufacturers now market product bundles rather than single SKUs, intensifying cross-selling rates and elevating average order values by 22% according to order-management platform tallies published by leading logistics integrators. Retail analytics show that households purchasing a smart desk have a 42% probability of adding a premium task chair within six months, validating lifecycle-based marketing tactics. Intellectual-property filings for cable-management grommets, sensor arrays, and AI-adjustable actuators jumped 17% year-on-year in 2024, indicating sustained innovation depth. As tech ecosystems mature, interoperability standards emerge that mirror smart-home protocols, enabling third-party accessories to tap into desk-resident data streams. The product hierarchy therefore shifts toward platform-oriented models where desks operate as hubs for peripherals, reinforcing the home office furniture market’s premiumization trajectory.

By Distribution Channel: E-Commerce Widens Lead

Online platforms captured 41.88% of category revenue in 2025, buoyed by augmented-reality visualization tools that cut cart-abandonment rates below 4%, compared with 11% for sites lacking 3D previews. Within digital channels, Direct-to-Consumer storefronts are forecast to grow at 14.10% CAGR as vertically integrated brands exploit data analytics to optimize inventory and pricing. Specialty Stores maintain a resilient 33.94% share because professional fitting services add tangible value for high-end ergonomic chairs that require precise adjustments. Home Centers and DIY outlets hold 24.18% share, favored by cost-conscious buyers undertaking self-assembly projects. The Online segment’s ascendance forces brick-and-mortar chains to reconfigure floor space for click-and-collect lockers and in-store video-consultation booths that replicate digital research journeys. Partnership models evolve as logistics firms offer white-label same-day delivery, enabling mid-size retailers to promise Amazon-comparable lead times without building proprietary fleets.

Digital payment adoption accelerates furniture checkout conversions, with buy-now-pay-later plans accounting for 18% of online ticket volumes in North America during 2024. Enhanced product-return algorithms pre-approve size-risk orders only if margin buffers cover potential reverse-logistics costs, shielding profitability. Artificial-intelligence chatbots resolve 82% of pre-purchase queries in under three minutes, further lifting customer-satisfaction scores. Cyber-fraud remains an operational drag, however, prompting multi-factor authentication rollouts that momentarily lengthen checkout flows. The overall channel shift cements e-commerce as the primary discovery medium, even when final transactions occur in physical stores, ensuring digital touchpoints influence virtually every dollar circulating through the home office furniture market.

By Material: Circularity Gains Share

Wood remains the backbone with a 45.78% revenue share, yet life-cycle analyses reveal a 23% carbon-footprint gap between certified and non-certified lumber, driving procurement policies toward FSC-labeled sources. Recycled Plastics, growing at an 8.05% CAGR, benefit from closed-loop supply agreements where post-consumer waste is converted into polypropylene chair shells with 30-year durability warranties. Engineered Wood holds 28.34% share, offering dimensional stability that pure hardwood lacks in fluctuating humidity conditions. Metal frames account for 21.12% of sales and dominate weights-and-measures critical applications such as sit-stand bases requiring torsional rigidity. Hybrid composites—hemp fiber-reinforced polymers, mycelium foams—constitute the balance, and while currently niche, they command media attention that garners early-adopter premiums.

Material innovation aligns tightly with corporate ESG scorecards, prompting tier-one suppliers to publish environmental product declarations that quantify emissions savings. Governments in Germany, Canada, and South Korea now provide tax credits worth up to 12% of invoice values for furniture made with at least 30% recycled content, generating measurable demand spikes. Modular construction and single-fastener design philosophies ease disassembly, letting end-of-life panels re-enter supply chains more economically. Consequently, recyclability shifts from differentiator to baseline expectation, reshaping sourcing, pricing, and brand narratives across the home office furniture market size calculations.

Geography Analysis

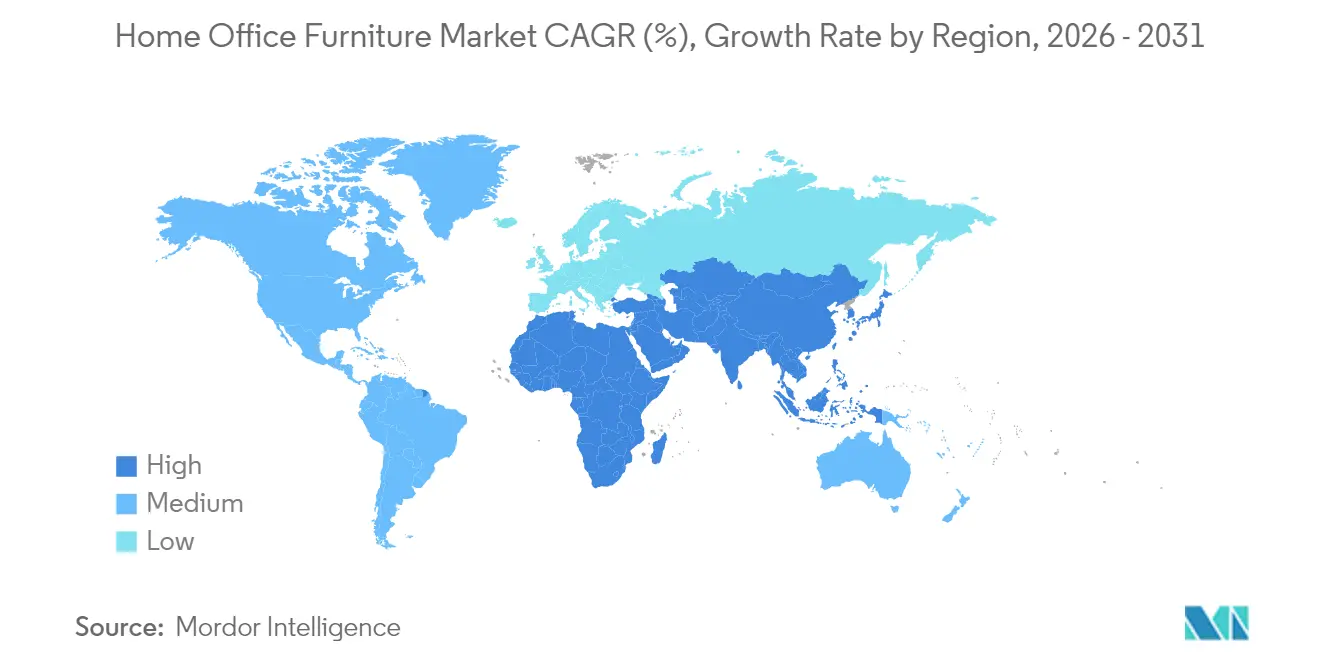

Asia-Pacific generated 38.05% of global revenue in 2025 and is projected to expand at 9.78% CAGR through 2031 the rare case where the largest market is also the fastest growing. China alone delivers over one-third of worldwide furniture output, leveraging integrated supplier clusters that compress lead times and permit custom finishes without excess inventory . India and Vietnam increasingly absorb overflow orders as wage differentials narrow, diversifying regional capacity and cushioning tariff risks. North America follows with a 32.11% share; robust corporate subsidy programs for remote-work setups offset soft residential remodeling volumes. Europe, at 29.84%, pivots toward eco-design mandates that stimulate demand for certified timber and recyclable polymers, albeit at a more measured 4.86% CAGR.

Middle East & Africa emerges as the second-fastest expanding bloc at 7.32% CAGR, catalyzed by Gulf megaprojects that incorporate smart-city work-live units demanding compact, IoT-ready furnishings. South America advances 6.54%, aided by rising white-collar employment and regional free-trade pacts that lower cross-border duties on flat-pack kits. Regional purchasing preferences differ, yet a convergent trend toward space-efficient, technology-enabled solutions underpins universal growth, making geography a function of adoption speed rather than directional divergence.

Regulatory Landscape

In major consumption markets, safety and ergonomics requirements increasingly shape product specifications and compliance costs for home office furniture sold through both retail and e-commerce. In the United States, the CPSC enforces the mandatory stability standard for clothing storage units under 16 CFR Part 1261 (STURDY Act framework), incorporating ASTM F2057-23 test methods, with enforcement activity extending to imported items that fail stability requirements. Alongside safety, workplace-wellness expectations extend into remote settings, pushing demand toward adjustable seating and workstation components that align with recognized labels and standards such as BIFMA LEVEL and GREENGUARD for enterprise and insurer-driven programs.

In Europe, Regulation (EU) 2023/988 on General Product Safety (GPSR) became applicable on December 13, 2024, widening operator obligations for consumer products, including furniture, and raising the bar for traceability and risk assessment even for used or refurbished goods placed on the market. Trade policy also remains a variable input to pricing and sourcing: a 2026 US proclamation delayed for one year scheduled tariff increases on certain upholstered wooden furniture and related categories, keeping prior duty rates in place while negotiations continued, which affects landed-cost planning for wood-heavy SKUs and reinforces multi-country sourcing strategies.

Value Chain Analysis

The home office furniture value chain starts with raw materials (lumber, engineered wood panels such as MDF/particleboard, metals for frames and sit-stand bases, plastics and recycled polymers, fabrics/foams, and electronics for smart desks), then moves through component fabrication (actuators, fasteners, casters, upholstery kits), final assembly, packaging (flat-pack optimization), and quality/compliance testing tied to safety and indoor-air standards. Asia-Pacific remains central to global manufacturing depth, while manufacturers and brands increasingly balance contract production with regional finishing and assembly to manage freight volatility and tariff uncertainty. Material substitution toward recycled plastics and certified wood feeds ESG procurement requirements, while documentation and labeling become more operationally important under widening product-safety and traceability expectations.

Downstream, distribution splits across big-box and specialty retailers, direct-to-consumer (DTC) online storefronts, and marketplaces, with last-mile delivery and in-home assembly acting as margin-critical services for bulky goods. The chain is being reshaped by consolidation and network optimization initiatives that target procurement leverage and logistics efficiency, alongside growth in reverse logistics for returns, refurbishment, and resale. Refurbished and circular channels are becoming a defined loop within the chain, with branded refurbishment storefronts and peer-to-peer resale initiatives adding new routes to market and extending product life, which in turn changes sourcing needs for spare parts, modular components, and repair-friendly designs.

Competitive Landscape

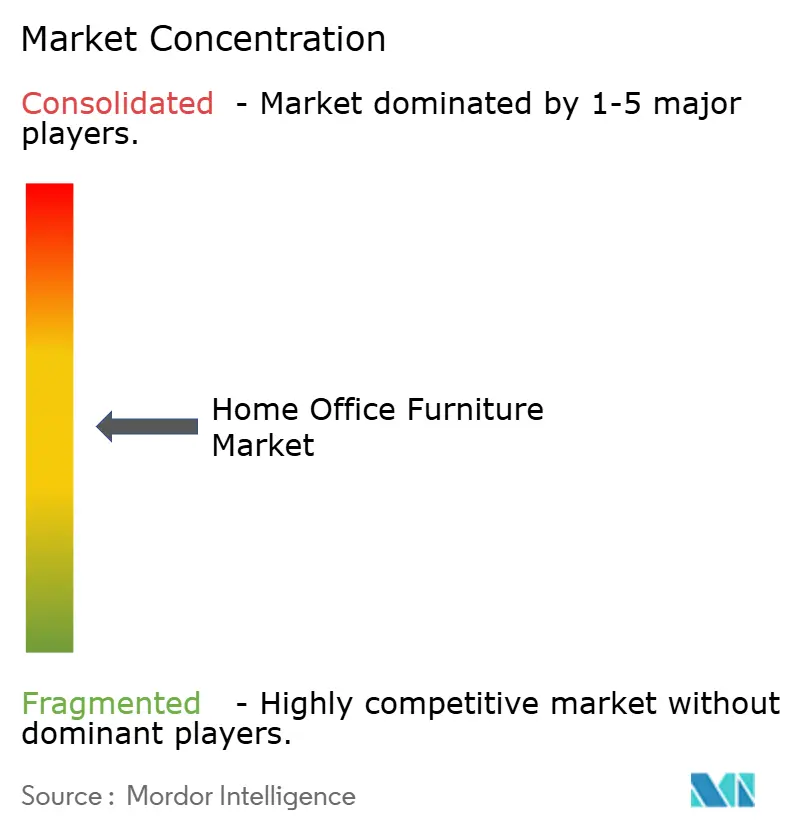

The industry shows a moderate level of concentration, with the top five players, HNI Corporation, Steelcase, MillerKnoll, IKEA, and Herman Miller, together accounting for a significant share of global sales. HNI’s acquisition of Steelcase, valued at USD 2.2 billion and expected to close by late 2025, is set to substantially increase its market presence and reshape the competitive landscape of the home office furniture market. Mergers target scale synergies in procurement and freight, as resin and steel volumes drive multi-million-dollar rebate thresholds.

Technological differentiation intensified with MillerKnoll piloting cloud-linked seating that logs posture data and feeds AI wellness dashboards, while IKEA tests circular-economy buy-back kiosks at metro-area stores. Patent race momentum shows 9% year-over-year growth in filings related to motor-noise reduction and sensor calibration. Sustainability remains a pivotal theme, with Herman Miller’s carbon-negative composites garnering enterprise RFP preference scores.

Regional specialists thrive on speed; Vietnamese contract manufacturers promise 45-day concept-to-container cycles for private-label clients, undercutting large incumbents on niche SKUs. Digital disruptors invest venture capital in last-mile assembly fleets, turning formerly profit-sapping service calls into branded customer-experience touchpoints. Altogether, rivalry centers on who best marries design, sustainability, and digital enablement rather than price alone, sustaining dynamic churn within the Home Office Furniture market.

Home Office Furniture Industry Leaders

IKEA

Steelcase Inc.

Ashley Furniture Industries

MillerKnoll (Herman Miller + Knoll)

HNI Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and channel whitespace is clearest at the intersection of space efficiency, ergonomics compliance, and digital enablement. Micro-apartment constraints and hybrid work routines are pushing demand toward modular fold-away workstations and multifunctional storage that preserves living space while meeting ergonomic expectations; this aligns with premiumization trends and adds attach opportunities for accessories such as monitor arms, lighting, acoustic panels, and cable management. On the commercial side, employer subsidy and insurer-driven ergonomic provisioning keeps recurring replacement cycles active, creating room for certified bundles (desk-chair-accessory kits) and smart desk features that generate compliance and wellness reporting as part of the value proposition.

Geographically, manufacturing and supply-chain investments in India highlight opportunities for localized capacity, faster replenishment, and organized retail expansion that can support both domestic consumption and export programs. In May 2026, the Andhra Pradesh Government and the Trade Promotion Council of India identified 1,000 acres near Gudur for an Andhra Pradesh Furniture Mega Cluster with a stated goal of large-scale investment and job creation, while private players added manufacturing capacity (for example, SOISU Furniture inaugurated a USD 7 million facility in Bhiwandi in May 2026). In parallel, materials and compliance infrastructure are becoming strategic differentiators: MDF and panel supply expansion (such as Greenply Industries announcing a multi-month capex plan to raise MDF capacity) supports flat-pack and engineered-wood-heavy home office lines, and EU-facing brands are preparing for deeper transparency and circularity requirements, including Digital Product Passport-style traceability for material composition and repairability that favors modular designs and documented recycled content.

Recent Industry Developments

- June 2026: Steelcase introduced a Made in India Fabric Collection featuring locally sourced materials for task and soft seating. The move strengthens local sourcing and helps reduce exposure to international supply disruptions while tailoring finishes to regional workplace and home office demand.

- August 2025: HNI Corporation agreed to acquire Steelcase in a USD 2.2 billion cash-and-stock deal, aiming for closure by late 2025. The combination raises purchasing leverage across materials and freight and accelerates consolidation-led competition in seating and workstation categories.

- June 2024: PARIC Holdings completed the acquisition of Corporate Concepts, a major contract furniture dealer in the US Midwest. The deal broadened service and delivery capabilities for office and hybrid-work customers, supporting bundled solutions that can spill over into home office furnishing programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers furniture bought and used to set up a working area inside a home, mainly for computer work, meetings, and study. It includes items that directly support home-based work comfort, storage, and day-to-day productivity.

Scope exclusions: We exclude office furniture bought mainly for commercial sites, along with home decor items that do not serve a functional home-work purpose.

Segmentation Overview

- By Product

- Chairs & Sofas

- Storage Units

- Desks & Tables

- Other Home Office Furniture

- By Distribution Channel

- Home Centers / DIY Stores

- Specialty Stores

- Online

- Other Distribution Channels

- By Material

- Wood

- Metal

- Plastic & Acrylic

- Engineered Wood (MDF, Particleboard)

- Other Materials

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool, pricing direction, and distribution mix for home office furniture across major regions. We relied on public sources such as U.S. Census Bureau retail and trade releases, Eurostat household and trade statistics, and UN Comtrade import and export data, plus labor force and work-from-home indicators from the ILO and national statistical offices. These were paired with furniture trade association updates and selected peer reviewed studies that discuss ergonomics and home workspace adoption.

To set realistic price bands and channel behavior, we also reviewed annual reports, investor presentations, and earnings commentary from furniture producers and retailers, along with credible business press coverage of freight, materials, and consumer spending. Where needed, paid subscriptions were used for company financials and intelligence, patent screening on ergonomic features helped triangulate product-type assumptions, and shipment-level import and export checks were used to validate supply shifts. The desk sources listed here are illustrative only, and many other public references were also reviewed for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and short surveys with manufacturers, distributors, online channel operators, and retail buyers who track desks, seating, and storage demand. We also spoke with logistics and materials-facing contacts to sanity check pricing pass-through and lead-time changes, then confirmed the same assumptions region-by-region so they did not lean too heavily on one geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | APAC: 51% |

| Mid tier: 45% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 19% | Managers: 48% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where household work-from-home penetration and home moves are used to form an addressable demand pool, then converted into furniture units using replacement cycles and purchase incidence for key items. Those units are priced using region-level average selling price ranges that reflect product mix changes, for example, the share of ergonomic seating versus basic chairs, and the split between compact and standing desks, and the totals are adjusted for online versus offline channel mix.

To keep the results grounded, we corroborated the outcome with selective bottom-up approximations, including sampled revenue roll-ups from representative manufacturers and retailers, plus channel checks on typical basket size and promotion intensity. Key inputs used in the model include remote and hybrid work share, household formation and housing turnover, retail furniture sales trends, average freight and material cost direction that affects realized pricing, and import dependence signals for desks and seating. Forecasts are built using scenario analysis supported by expert views on how hybrid work policies, housing cycles, and price normalization may move demand, and then the final curve is smoothed to avoid unrealistic year-to-year jumps. When bottom-up visibility is incomplete for smaller local brands, gap handling is done through calibrated shares based on channel presence and regional consumption indicators.

Data Validation & Update Cycle

Outputs are checked against independent signals such as furniture retail sales direction, trade flows for major furniture categories, and observed pricing movements in key markets, and then large variances are investigated before sign-off. If a region or product group shows an unexpected spike, assumptions are revisited and, when needed, a few contacts are re-engaged to confirm whether the change is real or driven by model inputs.

A multi-step internal review is followed so the logic, inputs, and calculations stay consistent across regions and years. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp changes in housing demand, freight rates, or work-from-home policies. Before delivery, an analyst runs a final pass so the client receives the latest updated view.

Mordor Intelligence's Home Office Furniture Market Size Versus Other Published Estimates

Published market sizes for home office furniture can look far apart even when the topic name is the same, because the included products, pricing basis, and the year used for the starting point are often not aligned. Differences also show up when one study relies on manufacturer revenues and another uses more retail value, which changes how margins and channel markups are treated.

One key gap driver is scope expansion into broader office furniture used at home, including adjacent categories that are not bought primarily for home working. Some estimates also mix in wider accessories and services, and the result shifts again if currency conversion timing and inflation handling are not clearly stated. The spread can also come from how fast average prices are assumed to rise for ergonomic chairs and adjustable desks, plus whether online discounting is treated as temporary or structural.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 41.21 B (2026) | |

| Trade Research Publisher A | USD 36.86 B (2025) | Uses a factory-gate revenue lens and starts from a 2025 anchor, which can understate the value seen at consumer purchase level after retail markups and mix shifts in ergonomic products. |

| Industry Research Publisher B | USD 37.07 B (2025) | Uses a different forecast window and base-year set, and the product scope described can be broader on materials and item coverage, which can move totals if pricing and channel mix assumptions are not aligned year by year. |

The table mainly shows timing and value-basis differences, not a disagreement on the direction of demand. Some published figures combine wider office furniture spending that happens to be placed in homes, then Mordor Intelligence counts only furniture categories purchased for a home-work setup and keeps channel value and price mix checks consistent across regions. With clear demand indicators and repeatable pricing steps, the estimate stays traceable even when work patterns and promotions change.

Key Questions Answered in the Report

How large is the Home Office Furniture market in 2026?

The Home Office Furniture market size is valued at USD 41.21 billion in 2026.

What is the current Home Office Furniture Market size?

In 2026, the Home Office Furniture Market size is expected to reach USD 41.21 billion.

What is the expected growth rate for Home Office Furniture through 2031?

The market is projected to expand at a 7.31% CAGR, reaching USD 58.63 billion by 2031.

Which product category leads sales today?

Desks & Tables hold the largest revenue share at 33.74% as of 2025.

Which distribution channel is growing fastest?

Direct-to-Consumer sales are forecast to grow at 14.10% CAGR through 2031.

Why is Asia-Pacific critical to future expansion?

Asia-Pacific commands 38.05% of current revenue and is set to grow at 9.78% CAGR, driven by manufacturing depth and rising consumer incomes.

What impact do raw-material costs have on the sector?

Volatile lumber and steel prices reduce the forecast CAGR by roughly 1.9%, pressuring margins and pricing strategies.

Page last updated on: