Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

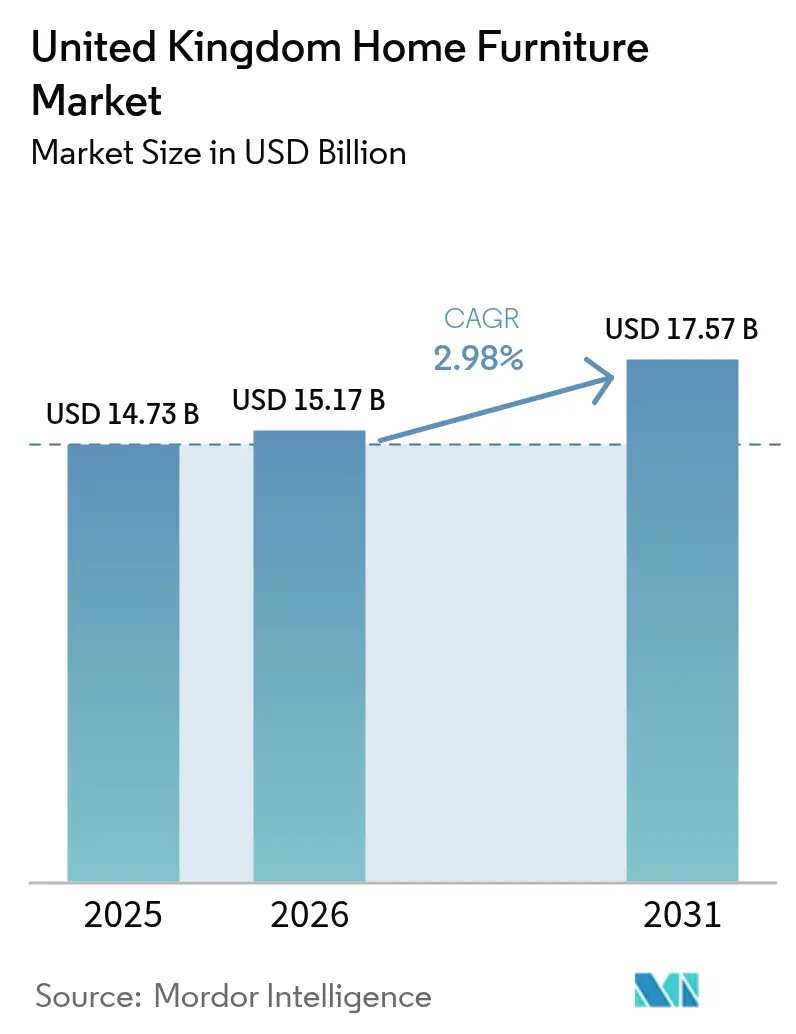

| Base Year Market Size (2025) | USD 14.73 Billion |

| Market Size (2026) | USD 15.17 Billion |

| Market Size (2031) | USD 17.57 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Home Furniture Market Analysis by Mordor Intelligence

The United Kingdom Home Furniture Market size in 2026 is estimated at USD 15.17 billion, growing from 2025 value of USD 14.73 billion with 2031 projections showing USD 17.57 billion, growing at 2.98% CAGR over 2026-2031.

The growth signals steady expansion despite raw-material inflation and heightened regulatory burdens. The trajectory rests on accelerated digitization of retail, a marked consumer preference for sustainable products, and the structural shift toward hybrid working that sustains elevated demand for home-office pieces. Build-to-Rent (BTR) developments reinforce underlying demand, as record 2024 capital inflows of USD 5.1 billion and government targets for 60,000 new rental homes annually to 2030 translate into higher institutional furniture orders. Intensifying competition comes from omnichannel incumbents and rising second-hand platforms, while compliance with the 2025 fire-safety amendments imposes additional testing and labeling costs on upholstered ranges[1]Source: UK Government, “Furniture and Furnishings (Fire) (Safety) Regulations 2025 Amendment,” gov.uk. Volatile timber and steel prices press margins; however, domestic sourcing initiatives such as Ercol’s Grown in Britain partnership illustrate how local supply chains can bolster resilience.

Key Report Takeaways

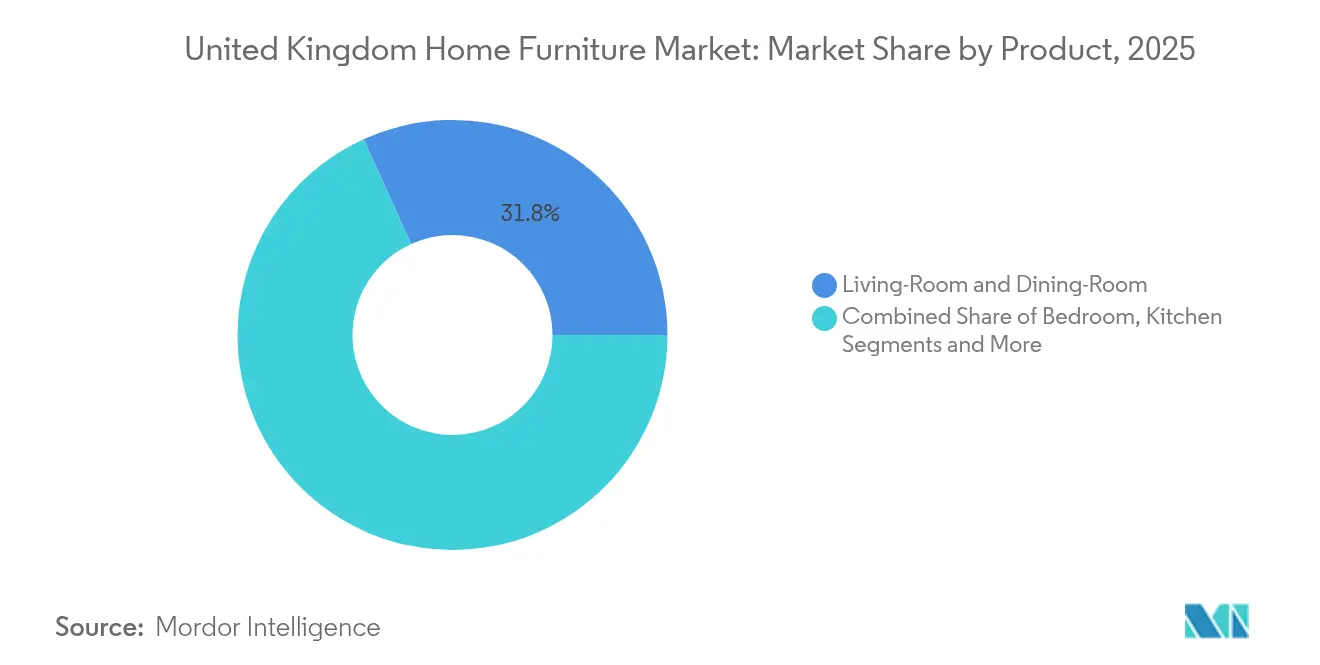

- By product, Living-Room & Dining-Room ranges led with 31.78% revenue share of the UK furniture market in 2025, whereas Home-Office pieces post the fastest 3.24% CAGR through 2031.

- By material, wood dominated with 55.92% of the UK furniture market size in 2025; metal components record the quickest 4.18% CAGR.

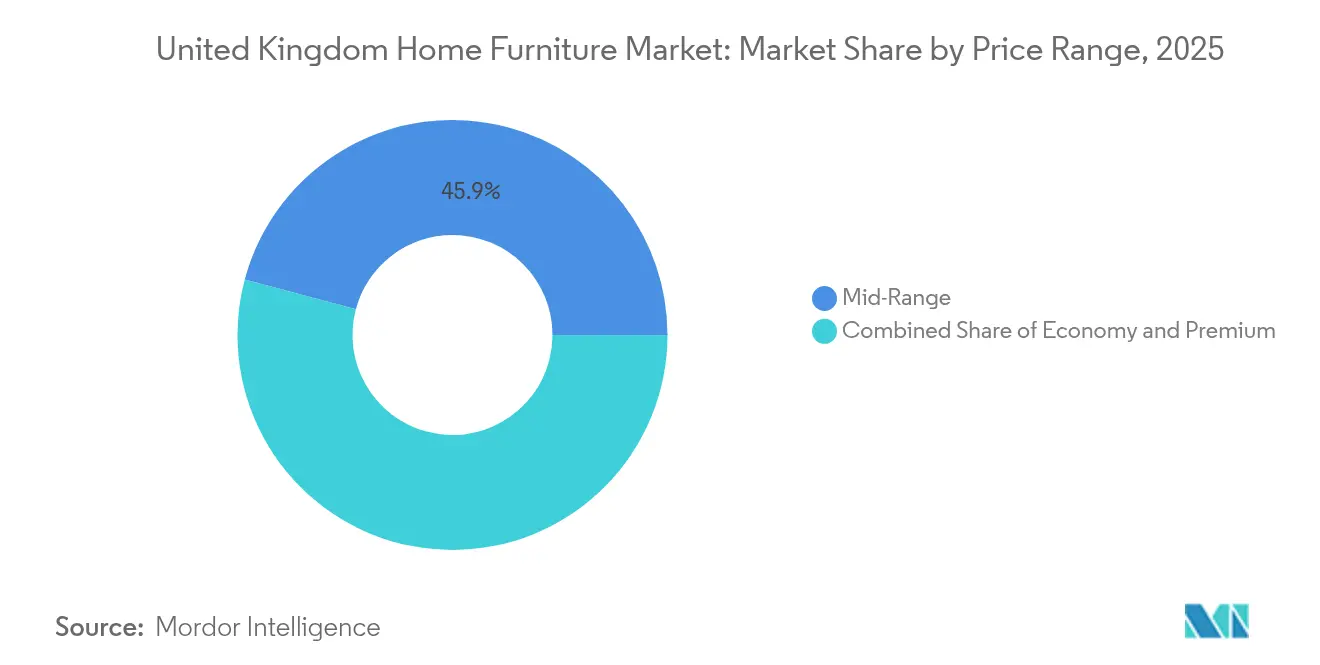

- By price range, mid-range held 45.85% share of the UK furniture market size in 2025; premium lines expand at a 3.02% CAGR.

- By distribution, home centers captured 35.12% of UK furniture market share in 2025, while online sales accelerate by 5.63% annually.

- By geography, England contributed 59.78% of total 2025 sales; Northern Ireland displays a 4.91% CAGR, the nation’s highest.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising home-improvement expenditure | +0.8% | England & Scotland | Medium term (2-4 years) |

| Growth of e-commerce furniture sales | +1.2% | Urban centers nationwide | Short term (≤ 2 years) |

| Sustainability & eco-friendly material demand | +0.6% | UK and wider EU | Long term (≥ 4 years) |

| Remote-working tax incentives | +0.4% | Metropolitan areas | Medium term (2-4 years) |

| Build-to-Rent boom | +0.7% | England & Scotland cities | Long term (≥ 4 years) |

| Circular-economy “right-to-repair” rules | +0.3% | UK-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of E-commerce Furniture Sales

Online channels are projected to account for nearly 40% of all UK furniture market transactions in 2025, driven by AR-enabled visualization tools that cut return rates and raise conversion. Retailers extend click-and-collect networks—exemplified by IKEA’s 100 Tesco collection points that enjoy 91% customer approval—to shrink last-mile costs and boost convenience[2]Source: IKEA UK, “Tesco Click & Collect Network Expands,” ikea.com. Mobile commerce shapes discovery behavior, with a majority of shoppers initiating searches on smartphones before finalizing in store or online checkout. Omnichannel integration becomes mandatory, requiring real-time inventory visibility and uniform pricing to safeguard shopper confidence. The logistics burden grows in tandem, prompting investments in automated warehouses and specialized two-man delivery fleets that can handle bulky items without damage.

Sustainability & Eco-friendly Material Demand

Seventy-eight percent of UK consumers label sustainable living a priority and 76% accept price premiums for eco-friendly furniture, magnifying the strategic imperative for certified materials[3]Source: WRAP, “Circular Change Council: Annual Report 2025,” wrap.org.uk. Two-thirds of manufacturers rank sustainability among their top three management issues, yet many cite implementation costs and knowledge gaps as barriers. Circular programs led by WRAP’s Circular Change Council aim to divert part of the 22 million furniture items discarded annually toward reuse or recycling, thereby easing landfill pressure. Retailers increasingly specify FSC-certified timber and recycled metal, embedding environmental credentials directly in product marketing. Modular, repairable designs gain traction as extended-warranty offers reinforce product longevity narratives that resonate with value-conscious buyers.

Build-to-Rent Boom Raises Demand for Durable Fixtures

The UK has delivered 123,500 completed BTR homes with another 109,800 units in the pipeline, generating consistent institutional furniture demand. Developers favor standardized packages that minimize maintenance costs yet deliver modern aesthetics to attract quality tenants in competitive rental hubs. Single-family BTR captures 51% of 2024 segment investment, catalyzing complete furnishing solutions that diverge from traditional apartment kits. Procurement teams stipulate products that support building-level sustainability certifications, pushing suppliers toward low-VOC finishes and traceable timber[4]Source: HM Treasury, “Full Expensing: Capital Allowances Policy Paper,” gov.uk. Furniture-as-a-service models surface, offering developers rental-based packages that sync with tenant turnover cycles while ensuring asset upkeep.

Remote-working Tax Incentives Boost Home-office Demand

The government’s Full Expensing policy allows 100% capital allowances on qualifying furniture expenditure until March 2026, spurring employers to equip staff home offices. Employees simultaneously claim tax deductions, reinforcing a dual-track stimulus for ergonomic desks and seating. Demand concentrates on adjustable-height tables and certified lumbar-support chairs as awareness of musculoskeletal health rises. Hybrid work patterns fuel interest in furniture that blends professional utility with residential aesthetics, such as fold-away desks that double as sideboards. Property renovation surveys show 44% of homeowners plan space conversions for work zones within two years, extending the sales runway beyond the pandemic surge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Timber, steel & foam price volatility | -0.9% | Global supply chains influencing UK producers | Short term (≤ 2 years) |

| Geopolitical shipping disruptions | -0.6% | Asia-to-UK trade lanes | Medium term (2-4 years) |

| Stricter fire-safety compliance costs | -0.4% | UK upholstery sector | Long term (≥ 4 years) |

| Second-hand resale adoption | -0.7% | Urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Timber, Steel & Foam Price Volatility Squeezing Retailer Margins

Building-material prices have climbed 38% since 2020, with kitchen furniture inputs up 36%, tightening already slim retailer gross margins. The UK imports 81% of its timber, exposing manufacturers to currency swings and geopolitical supply shocks that ripple through finished goods pricing. Government consultation on a USD 2.5 billion plan to stabilize domestic steel provides future relief, yet immediate implementation timelines leave producers vulnerable to spot-market spikes. Foam costs stay elevated because petrochemical feedstock volatility persists, particularly affecting high-density upholstery applications. Firms counter risk through multi-sourcing, local procurement partnerships, and material substitution, though each strategy demands capital outlays and may challenge established design aesthetics.

Second-hand Resale Platforms Cannibalizing New-furniture Demand

Circular-economy momentum diverts spending from new furniture, as consumer perception of resale aligns with sustainability goals and budgetary prudence. Peer-to-peer apps deliver frictionless listing, payment, and logistics, lowering barriers to second-hand adoption in urban regions with dense inventory pools. Retailers experiment with buy-back and refurbishment schemes to keep customers within brand ecosystems, but these programs can erode higher-margin new-product sales. Younger demographics prize uniqueness and heritage, increasing demand for vintage pieces that hold design relevance and perceived authenticity. The competitive response centers on differentiated craftsmanship, faster delivery, and warranty extensions that underline the superior lifetime value of new, certified items.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Living Spaces Steady, Home-Office Surging

Living-Room & Dining-Room furniture retained a 31.78% share of the UK furniture market in 2025 as open-plan layouts and social-space enhancements persisted. Home-Office pieces, while smaller in absolute terms, post a category-leading 3.24% CAGR, reflecting continuous hybrid working adoption and employer-funded ergonomic upgrades. Bedroom furnishings remain stable, underpinned by storage innovations that cater to urban dwellers with limited square footage. Kitchen furniture benefits from renovation cycles that treat the kitchen as a multi-use social hub, boosting demand for integrated seating and storage modules. Outdoor ranges saw pandemic-era uplift, yet sales moderate as weather-related seasonality returns, reinforcing the dominance of indoor core categories.

Demand patterns now prioritize multifunctionality, driving modular sofas and extendable tables that adapt to evolving household needs while guarding against premature obsolescence. Vintage-inspired designs have resurged, with retro silhouettes signaling perceived durability and design permanence that consumers equate with value. Updated fire-safety regulations add engineering complexity to upholstered products, compelling producers to source low-flame fabrics without sacrificing comfort. Premium smart furniture—with wireless charging and concealed lighting, is carving a niche, especially among urban professionals seeking seamless tech integration. Customization engines enable shoppers to tweak finishes online, shrinking the gap between bespoke craftsmanship and mass-market affordability.

By Material: Wood Dominant, Metal Ascendant

Wood accounted for 55.92% of the UK furniture market share in 2025, illustrating enduring consumer affinity for natural aesthetics and renewable sourcing narratives. Metal components grow fastest at 4.18% CAGR as industrial loft themes permeate residential settings and commercial buyers prize durability. Plastic and polymer lines retain utility in outdoor environments where low maintenance outweighs premium design aspirations. Emerging composites leverage recycled fibers and bio-resins, giving sustainability-minded shoppers new alternatives without compromising performance. The dominance of imported timber remains a structural risk, but domestic initiatives like Grown in Britain showcase the feasibility of shorter, traceable supply chains that improve carbon metrics.

Advanced kiln drying and CNC processing now yield tighter tolerances and reduced wastage, elevating consistency across mid-range price points. Hybrid constructions that fuse wood tops with metal frames deliver visual warmth and structural strength, aligning with contemporary design cues. Recycled-content mandates from large retailers encourage smelters to expand closed-loop aluminum supplies that feed into dining furniture and shelving systems. Material traceability apps let consumers scan QR codes for provenance data, reinforcing trust and reinforcing brand credentials around responsible sourcing. As domestic timber capacity scales, producers anticipate greater buffer against future currency fluctuations that have historically distorted input costs.

By Price Range: Mid-Market Anchor, Premium Momentum

The mid-range bracket claimed 45.85% of the UK furniture market size in 2025 by striking a balance between perceived quality and household budgets amid lingering inflation. Premium pieces, however, chart a 3.02% CAGR as buyers adopt buy-once-use-forever mindsets that favor higher initial outlays for long service life and eco credentials. Economy lines cater to rental properties and first-time buyers, yet margin sensitivity restricts feature upgrades when raw-material costs spike. Direct-to-consumer brands blur traditional thresholds by selling premium-grade sofas at mid-range prices via streamlined online channels. Financing tools, including interest-free installments, democratizing access to higher tiers without diluting perceived exclusivity.

Premium makers differentiate through craftsmanship stories, locally sourced wood, and lifetime guarantees that resonate with sustainability-oriented demographics. Mid-range retailers doubled down on efficient manufacturing and modularity to offset cost inflation without downgrading experience. Economy producers face direct competition from second-hand alternatives that promise similar price points with perceived environmental advantages. Polarization leaves fewer true budget options, compelling value engineering that swaps metal fasteners for engineered-wood joinery while safeguarding structural integrity. The BTR segment orders across tiers, specifying durable finishes in communal areas and premium accents in penthouse units, creating mixed demand profiles for suppliers.

By Distribution Channel: Home Centers Hold Court, Online Accelerates

Home centers retained a 35.12% slice of the UK furniture market in 2025, leveraging extensive floor space and cross-category merchandising to drive footfall. Online channels expand at a 5.63% CAGR, propelled by frictionless checkout, broader assortments, and real-time delivery tracking that cultivates shopper loyalty. Specialty stores defend share by emphasizing design consultancy and faster in-stock pickup, although cost overheads challenge smaller independents. Hypermarkets and department stores satisfy convenience-led buyers seeking entry-level lines alongside grocery missions, yet category depth remains limited. Successful retailers execute precise omnichannel orchestration, ensuring price parity, unified promotions, and seamless click-and-collect experiences that merge digital discovery with physical touchpoints.

Generative-AI tools refine product recommendations, reducing search time and boosting conversion for high-ticket categories where browsing fatigue can deter purchases. Augmented reality previews allow shoppers to visualize scale and color accuracy in situ, lowering returns and perceived risk. Smaller-format urban showrooms surface, offering curated assortments that rely on digital catalogs and rapid-fulfillment hubs to compensate for limited inventory footprints. Logistics partners tweak delivery windows and white-glove assembly add-ons to satisfy expectations shaped by e-commerce giants in adjacent categories. Marketplace platforms offer incremental reach but compress margins, forcing brands to weigh visibility gains against reduced direct customer engagement.

Geography Analysis

England contributed 59.78% of 2025 revenue in the UK furniture market, buoyed by dense population centers, active housing turnover, and a concentration of flagship retail footprints that deliver scale economies. London’s premium bias drives high-average-ticket sales, yet space constraints spur demand for modular and compact designs tailored to small apartments. Major BTR clusters in Manchester and Birmingham further stimulate bulk furniture procurement, reinforcing regional manufacturing and distribution hubs.

Northern Ireland registers the fastest 4.91% CAGR through 2031 as favorable economic indicators unlock discretionary spending on home refurbishment, while a younger demographic profile fosters early adoption of online channels. Scotland constitutes a sizeable market characterized by heritage preferences that favor locally crafted timber pieces alongside growing appetite for eco-labeled imports. Government Levelling-Up investments nurture retail infrastructure in northern counties, drawing new store openings and localized e-commerce fulfillment centers that shorten delivery lead times.

Wales maintains steady growth through tourism-linked demand for leisure and outdoor furniture suited to coastal properties, capitalizing on rising staycation trends. Regional logistics disparities influence shipping costs; remote rural zones incur higher last-mile fees, prompting retailers to pilot micro-distribution centers for inventory pooling. disparity in average house prices—from England’s GBP 430,000 to Scotland’s GBP 130,000—shapes product mix and price sensitivity across territories, compelling localized assortments within national merchandising strategies.

Regulatory Landscape

UK home furniture suppliers operate under product safety, chemical, and trade compliance requirements, with upholstered items facing the most direct regulatory burden through the Furniture and Furnishings (Fire) (Safety) Regulations 1988. In October 2025, the Furniture and Furnishings (Fire) (Safety) (Amendment) Regulations 2025 (SI 2025/531) took effect, narrowing scope for certain baby and childrens products and removing the display label requirement, while leaving core safety obligations for domestic upholstered furniture in place.

In 2026, the Office for Product Safety and Standards (OPSS) launched a final consultation (running until 23 June 2026) on broader reform of the upholstered furniture fire safety regime. The proposals shift the system toward an outcome-focused, smoulder-based approach and reduce reliance on chemical flame retardants. On the trade side, many furniture product lines fall under the UK Integrated Online Tariff framework and often carry 0% import tariffs under the UK Global Tariff and UK-EU Trade and Cooperation Agreement conditions when rules of origin are met. Border costs therefore stay concentrated on documentation and origin compliance rather than headline duty rates.

Value Chain Analysis

The UK home furniture value chain starts with raw materials and components (timber, metal, upholstery textiles, foam, adhesives, and hardware), then moves through design and engineering, fabrication and finishing (including compliance testing for upholstered items), and assembly. A large share of supply is import-linked, which creates exposure to FX and shipping disruption. Import dependency is indicated at 60.3% as of 2025, with sourcing concentrated in countries such as China (37.2%) and Italy (10.1). Fire-safety compliance for upholstered furniture adds testing and labeling workflow steps that affect material selection and supplier qualification.

Downstream, distribution splits across home centers, specialty retailers, and online-first channels, supported by large-item logistics such as two-person delivery, returns handling, and assembly. Operational efficiency is increasingly a margin lever, as sector logistics shift toward digital tracking and automation-led fulfillment practices. Financial stress among upstream manufacturers and suppliers can interrupt continuity of supply and extend lead times, which has been highlighted by administrations reported in early 2026 within the upholstery supply base. Domestic sourcing efforts, such as Ercol's Grown in Britain partnership, also illustrate a counter-trend toward shorter, more traceable supply chains.

Competitive Landscape

The UK furniture market exhibits moderate fragmentation, with leading retailers holding a significant combined share, indicative of a competitive but consolidating arena. Dunelm expanded its premium footprint via the April 2025 acquisition of Designers Guild, integrating luxury fabrics into broader assortments while defending margin through vertical sourcing. IKEA pioneered compact rapid-rollout stores in 2025, converting existing retail-park shells to compress build-out costs and speed market coverage. Wren Kitchens’ partnership with a U.S. home-improvement giant underscores a trend toward international diversification that leverages British design credibility in export markets.

Digital innovation differentiates leading players; Dunelm’s Google Cloud alliance deploys generative AI for search optimization, thereby elevating shopper engagement and reducing bounce rates. John Lewis doubled down on private-label expansion by onboarding 30 new brands and investing in experiential showrooms to restore home-category dominance. Sustainable sourcing remains a pivotal battleground: Ercol’s domestic-timber program grants it provenance transparency that appeals to eco-oriented consumers and institutional buyers alike. Smaller entrants counter scale disadvantages through direct-to-consumer models, narrowing assortments to hero SKUs and relying on social-media storytelling to cultivate niche followings.

Compliance mastery affords established manufacturers a defensive moat; updated 2025 fire-retardancy rules escalate testing costs that deter under-capitalized newcomers. Industry participants increasingly explore furniture-as-a-service subscriptions, aligning revenue recognition with longer product lifecycles and forging stickier landlord relationships in BTR portfolios. Competitive intensity therefore pivots on three vectors, sustainability credentials, digital engagement capability, and supply-chain resilience, each reinforcing the strategic premium on scale, capital access, and technological agility.

United Kingdom Home Furniture Industry Leaders

Ikea

Dunelm Group PLC

DFS Furniture PLC

John Lewis Partnership

SCS Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most immediate opportunity is compliance-led product redesign for upholstery. OPSS's 2026 consultation on reforming domestic upholstered furniture fire safety regulation places smoulder-based testing and reduced reliance on chemical flame retardants at the center of the policy direction, which creates room for suppliers to certify materials and constructions to evolving requirements. Companies can also use these changes to support sustainability narratives, including modularity and repairable designs that fit circular-economy positioning.

Capacity, distribution footprint, and logistics modernization remain practical levers for improving service levels and cost control. In 2026, named investments indicate businesses strengthening UK-based production and hub-and-spoke distribution, including Howdens' plan to invest around GBP 30 million to open new depots and refurbish existing sites, Bedkingdoms expansion into a larger Wakefield warehouse for logistics efficiency, and Barons Contract Furnitures' move to consolidate manufacturing and distribution alongside a new showroom. Separately, WRAP-aligned circular programs and industry work on unsold inventory management (as reflected by FIRA publishing an unsold furniture survey report in 2026) support the commercial case for take-back, refurbishment, and resale partnerships that keep customers in-brand while addressing waste and Scope 3 reporting demands.

Recent Industry Developments

- April 2026: Dunelm introduced the Dorma Archive collection within its home assortment, broadening premium styling cues under a recognized in-house brand. The launch supports differentiation in a market where mid-range share is high, and retailers use exclusive ranges to protect margin and reduce direct price comparability across channels.

- January 2025: Dunelm expanded its in-house Made to Measure capability for curtains, blinds, and shutters in the Midlands. The move increased control over lead times and quality for higher-service categories that complement furniture purchases and strengthen omnichannel attachment through fitted, custom orders.

- April 2024: The UK Build-to-Rent (BTR) pipeline remained large alongside completed stock, reinforcing institutional purchasing routes for standardized, durable furnishing packages in major English city clusters. This supported supplier focus on contract-grade finishes, bulk procurement workflows, and repeatable installation logistics aligned to landlord maintenance and turnover cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the UK home furniture market is counted as the value of furniture purchased for residential use across major rooms and household spaces, sold through offline and online channels, and measured in current USD.

Scope exclusions: We exclude furniture primarily bought for offices, schools, healthcare, hospitality, and other non-residential settings, along with installation-only and unrelated decor items.

Segmentation Overview

- By Product

- Living Room & Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers

- Specialty Furniture Stores (including exclusive brand outlets and local stores from the unorganized sector)

- Online

- Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.)

- By Geography

- England

- Scotland

- Wales

- Northern Ireland

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the demand context and keep the market model tied to real household signals. We review public data such as the UK Office for National Statistics (household spending and housing indicators), HM Revenue and Customs trade statistics for relevant product flows, and Bank of England releases that help explain rate-driven spending on big-ticket items.

To anchor industry structure, references are taken from sources such as UK government business and sector statistics, trade association releases covering furniture and retail, and peer-reviewed journals that discuss materials, durability, and circularity trends. Company filings, investor presentations, and reputable press reporting are also checked to understand pricing moves, channel shifts, and promotion intensity, and then company financials and news databases and a patent database are used selectively for cross-checking. These examples are not exhaustive, and many other public sources were used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary work focuses on validating what desk sources cannot fully show, especially category splits, channel mix, and near-term pricing behavior. We spoke with manufacturers, retailers, distributors, and industry specialists across the UK, and then the feedback was used to confirm assumptions such as replacement timing, online share, and the pace of price normalization after promotions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 55% | Functional/Unit leaders: 39% | |

| Smaller Players: 17% | Managers: 49% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where national household consumption and housing activity are translated into a furniture spend pool, and then adjusted to reflect the home-only scope. To make sure the totals stay realistic, we corroborate outputs with selective bottom-up approximations such as sampled price points times unit volumes by key categories, supplier and retailer revenue mix checks, and channel-level sense checks.

Inputs used in the model include household consumption trends for furniture and furnishings, housing transactions and renovation intensity as a demand trigger, import reliance and trade movements for key product groups, and observed pricing factors such as promotion depth and mix shift toward online sales. Since some data series are not perfectly aligned to the exact home-furniture definition, we handle gaps by applying conservative share assumptions that are stress-tested with interview feedback and then rebalanced so totals remain consistent.

For forecasting, we use scenario analysis because consumer confidence, mortgage-rate sensitivity, and housing turnover can move demand faster than long-run averages. The scenarios are kept practical by tying them to a small set of variables with consensus direction from industry experts, and then a central case is selected after checking that implied price and volume paths make sense.

Data Validation & Update Cycle

Outputs are validated through several checks, and each check is reviewed before sign-off. We compare the final market totals against independent indicators like furniture-related household spending, retail momentum, and trade flows, and then investigate any unusual swings before they are accepted.

When variances appear, assumptions are revisited and, if needed, experts are re-contacted to confirm whether the change is real or just a timing issue in the data. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp pricing shifts, regulatory changes, or major demand shocks. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's UK Home Furniture Market Estimate Compared With Other Published Estimates

Published market sizes for UK furniture often do not match, and the reason is usually not math, it is definition. Differences show up when one estimate tracks home-only demand, another reports all furniture, and a third uses a retail or consumer-spend lens.

The main gap comes from mixing home furniture with broader furniture categories, where Mordor Intelligence counts only residential home furniture and keeps price progression tied to channel mix and promotion intensity rather than assuming a uniform inflation path across all furniture types.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.73 B (2025) | |

| Global Consultancy A | USD 22.80 B (2025) | Uses a broader UK furniture scope that includes non-home end uses, which lifts the addressable revenue base versus a residential-only definition. |

| Trade Journal B | USD 21.89 B (2024) | Reports the total UK furniture market and uses a different base year, so the figure blends home and non-home furniture and can reflect a different currency timing and pricing environment. |

The spread across sources is largely explained by what gets included and which year is treated as the current point. By keeping the scope limited to residential home furniture and checking the model against housing and spending signals, the estimate stays traceable to clear demand drivers that can be reviewed and repeated.

Key Questions Answered in the Report

How large is the UK furniture market in 2026?

The UK furniture market size stands at USD 15.17 billion in 2026 and is projected to reach USD 17.57 billion by 2031.

What CAGR is forecast for UK furniture sales through 2031?

Industry revenue is expected to grow at a 2.98% CAGR between 2026 and 2031.

Which product category is growing fastest?

Home-Office furniture records the highest 3.24% CAGR, driven by hybrid working and supportive tax incentives.

Why are Build-to-Rent projects influencing furniture demand?

BTR schemes add thousands of rental units annually, necessitating bulk orders for durable, standardized furnishings that cut landlord maintenance costs.

How are retailers addressing sustainability concerns?

Leading brands specify FSC-certified timber, integrate recycled metals, and offer take-back programs aligned with WRAP’s circular-economy guidelines.

Page last updated on: