Adjustable Bed Bases Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.69 Billion |

| Market Size (2031) | USD 6.14 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

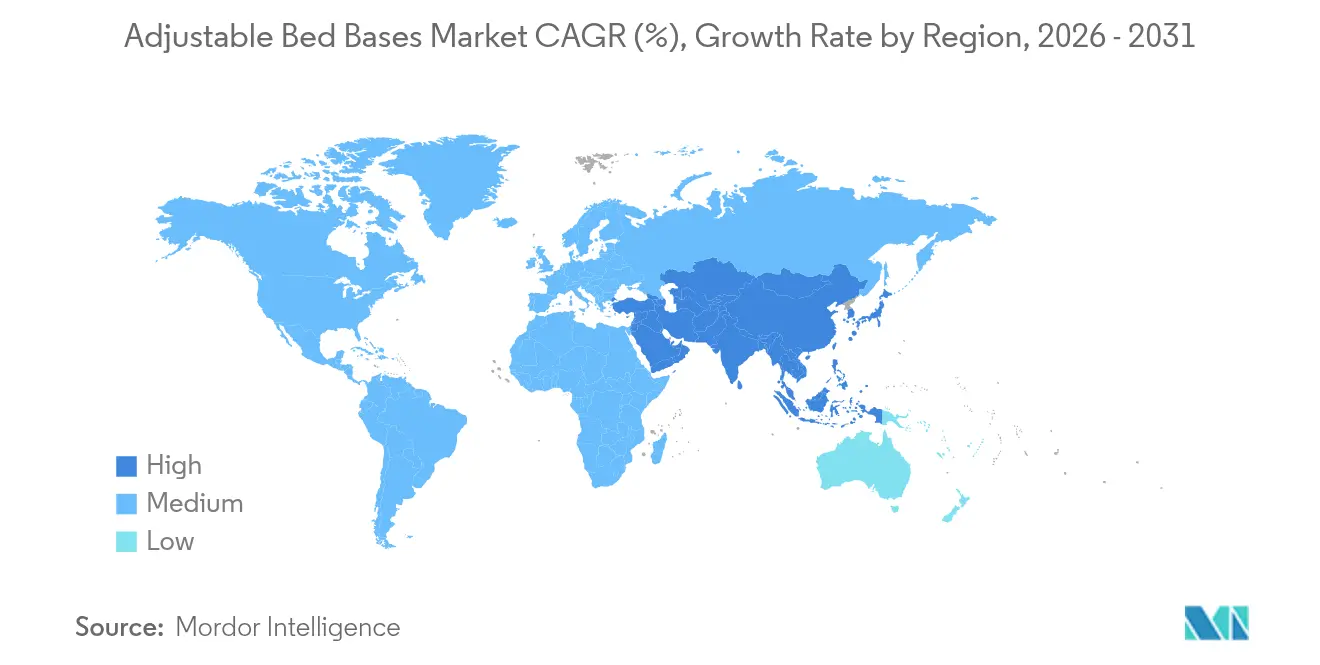

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adjustable Bed Bases Market Analysis by Mordor Intelligence

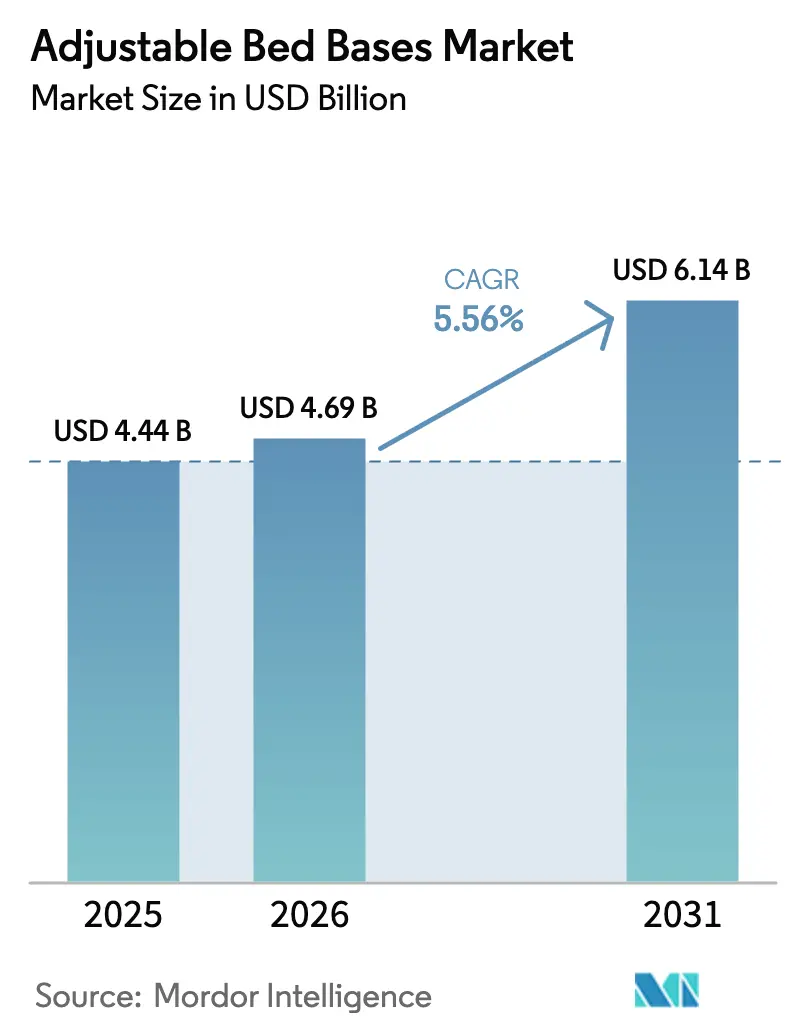

The Adjustable Bed Bases market size is expected to grow from USD 4.44 billion in 2025 to USD 4.69 billion in 2026 and is forecast to reach USD 6.14 billion by 2031 at 5.56% CAGR over 2026-2031.

Strong demand stems from aging demographics, growing consumer focus on sleep wellness, and rapid smart-home adoption. Technology upgrades—ranging from programmable presets to sensor-based sleep tracking—are moving these products from niche luxury to mainstream wellness solutions. B2B demand from hospitals and premium hotels signals a widening customer base, while modular flat-pack designs are unlocking new e-commerce reach. Pricing pressures and component shortages remain challenges, yet rising reimbursement eligibility and willingness to invest in health continue to support growth across price tiers.

Key Report Takeaways

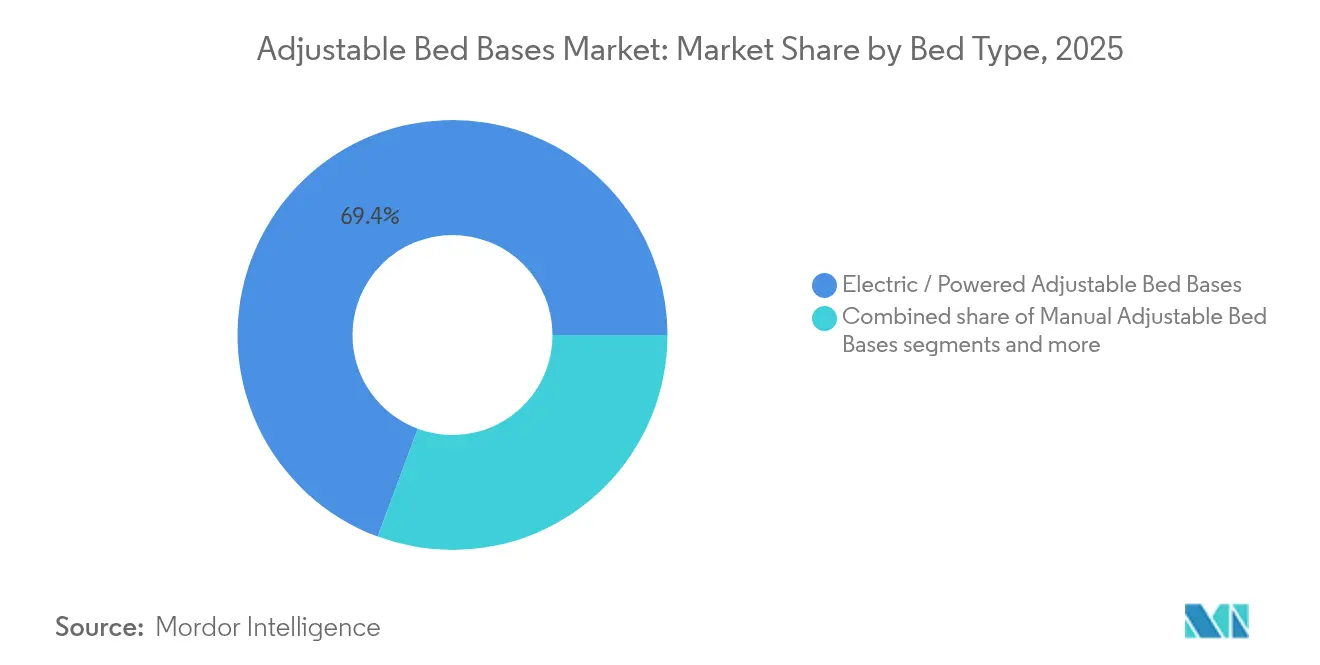

- By bed type, Electric/Powered units led with 69.35% of adjustable bed bases market share in 2025; Smart bases are set to expand at a 6.39% CAGR through 2031.

- By frame material, metal frames held 59.40% revenue share in 2025; composite and other sustainable materials are projected to rise at a 6.09% CAGR to 2031.

- By size, queen bases commanded 39.45% of the adjustable bed bases market size in 2025; twin bases will advance at a 5.69% CAGR between 2026-2031.

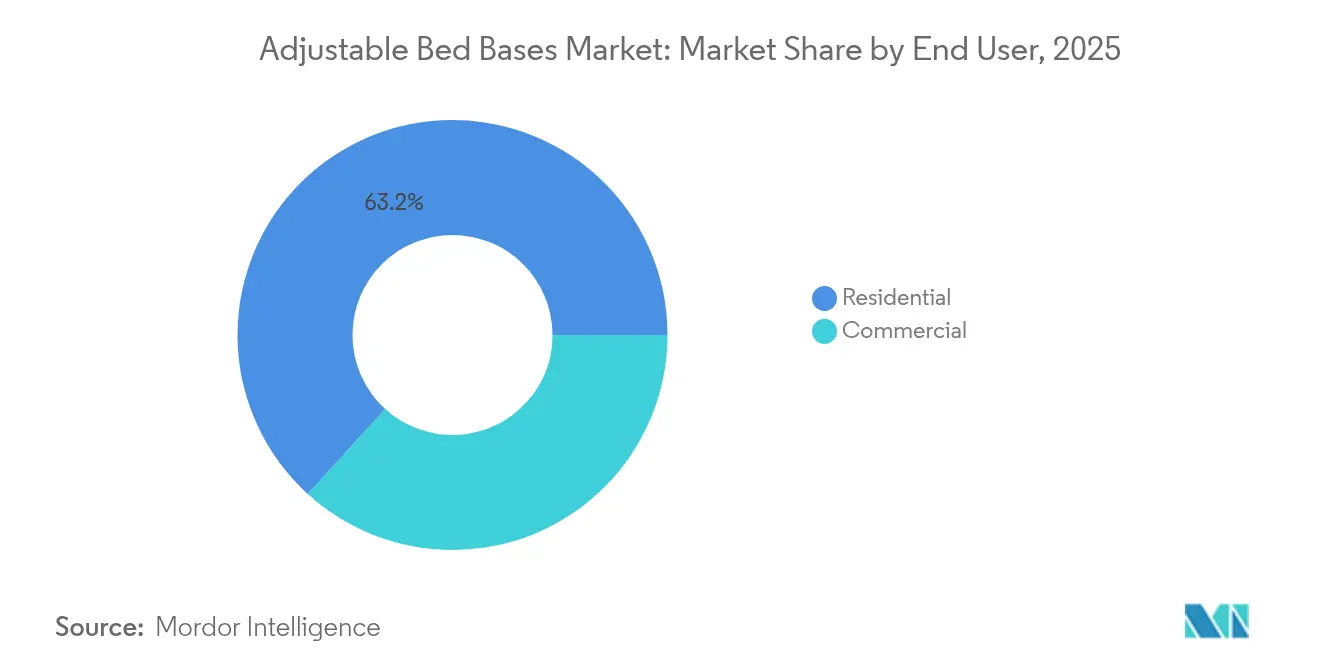

- By end user, residential customers accounted for 63.25% of 2025 sales; the commercial segment is forecast to grow at 5.43% CAGR to 2031.

- By channel, B2C retail captured 74.20% of 2025 volume; the B2B/project route is projected to climb at a 5.91% CAGR through 2031.

- By geography, North America led with a 44.55% share in 2025, while Asia-Pacific is poised for the quickest 6.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adjustable Bed Bases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| An aging population and mobility needs | +1.7% | North America, Europe, Japan | Long term (≥ 4 years) |

| Sleep wellness focus across price tiers | +1.2% | North America, Western Europe, Global | Medium term (2–4 years) |

| Home-based post-acute recovery | +0.9% | North America, Europe, and developed Asia-Pacific | Medium term (2–4 years) |

| Hospitality premiumization | +0.8% | Global luxury hubs | Short term (≤ 2 years) |

| E-commerce and flat-pack logistics | +0.6% | Global, emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Mobility Challenges Elevating Demand for Adjustable Sleep Systems Globally

Adults aged 65 and above are projected to represent 16% of the global population by 2030, and many now view adjustability as an essential aid to maintain independence. Designs increasingly target arthritis relief and easier breathing, with nine in ten older users reporting better rest quality after switching. Medicare and comparable programs reimburse adjustable bases prescribed for specific ailments, lowering out-of-pocket costs and expanding access. Manufacturers, therefore, prioritize motor strength, emergency power backup, and low-height profiles to meet both comfort and mobility needs.

Consumer Prioritization of Sleep Wellness and Ergonomic Comfort Across Price Tiers

Sleep has shifted from a luxury discussion to a measurable wellness metric. Entry-level motorized bases under USD 900 are now commonplace, widening adoption among middle-income households. Smart bases add sleep-stage sensing, automatic micro-adjustments, and app-controlled ecosystem links, turning the bed into a platform for subscription-based analytics. Brands are piloting “sleep-as-a-service” bundles that package cloud software with periodic firmware upgrades, creating new annuity revenue streams. Integration with voice assistants and circadian lighting further embeds adjustable bases within connected-home routines, reinforcing daily user engagement beyond nighttime use.

Premiumization of Hospitality Sector: Enhancing Guest Experience with Motorized Bases

Luxury and upscale hotels are elevating guest satisfaction scores by adding motorized bases capable of zero-gravity and anti-snore presets. Hotels report double-digit uplifts in room-rate premiums when adjustable beds are offered, particularly among business travelers who prioritize restorative sleep on short stays. In a study conducted by Loopon across 130+ First Hotels in Scandinavia, it was revealed that rooms featuring YouBed adjustable beds saw an average price hike of $19 (~158 kr), translating to an approximate 17% increase over standard room rates. Operators demand heavy-duty cycles, centralized reset functions, and upholstery options that match brand aesthetics. Manufacturers respond with proprietary control hubs that allow staff to standardize positions across a property after each checkout, reducing housekeeping time.

E-Commerce and Flat-Pack Logistics Expanding Global Reach for Adjustable Bed Bases

Online retail is transforming how adjustable bed bases move from factory floors to bedrooms. B2C/Retail Channels still held 67% of category sales in 2024. The share of direct-to-consumer purchases has climbed steadily as brands redesign products for parcel shipping. Engineers now prioritize modular frames and reinforced joint systems that survive long-haul transit without sacrificing stability once assembled. These changes matter most in countries that lack dense specialty-bedding store networks; shoppers there can finally access premium brands without travelling to urban showrooms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity versus traditional foundations is hindering mass adoption | -0.8% | Global, with a stronger impact in price-sensitive markets | Medium term (2–4 years) |

| Global supply-chain volatility is raising production and shipping costs | -0.7% | Global, with pronounced effects in import-dependent markets | Short term (≤ 2 years) |

| Limited consumer awareness in emerging markets is curtailing growth potential | -0.5% | Asia-Pacific emerging markets, Latin America, and parts of Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity Versus Traditional Foundations Hindering Mass Adoption

The significant price differential between adjustable bases and conventional bed foundations continues to constrain market penetration, with adjustable bases typically commanding substantial premiums over traditional foundations. The twin category, despite strong senior and single-user needs, sees the steepest premium, slowing unit velocity. Manufacturers are shifting to tiered portfolios that offer essential lift functions at entry prices while reserving mass customization and IoT integration for flagship lines.

Global Supply-Chain Volatility Raising Production and Shipping Costs

Persistent global supply chain disruptions are creating significant margin pressure across the adjustable bed bases market, with manufacturers implementing comprehensive restructuring initiatives to address cost pressures and operational challenges. Specialized motors, linear actuators, and control boards face intermittent shortages, elongating lead times, and increasing buffer inventory. Producers with wide plant networks confront higher logistics complexity, spurring consolidation and near-shoring moves. Leggett & Platt, for example, trimmed its bedding plant count from 50 to roughly 30-35 sites, a move that streamlines production and shortens delivery lines in the face of shipping and component challenges. Leading firms are rationalizing sites and pursuing dual-sourcing for electronics to reduce exposure to single-region disruptions. Mid-sized brands unable to absorb cost spikes risk margin erosion or must pass increases to consumers, potentially dampening demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bed Type: Smart Technology Redefining Sleep Experience

Electric/Powered models dominated value with a 69.35% share in 2025, anchoring the adjustable bed bases market through proven reliability and accessible pricing. Demand is buoyed by programmable presets, massage modules, and smartphone connectivity that deliver perceived luxury at mid-level costs. The adjustable bed bases market size tied to Smart bases is advancing at a 6.39% CAGR alongside wider IoT adoption. Smart platforms leverage AI algorithms to raise or lower sections based on heart-rate variability, translating biomedical data into granular position adjustments.

A growing cohort of technology firms is entering the category, partnering with bedding manufacturers to embed firmware over-the-air upgrades and cloud analytics. Price premiums remain viable as early adopters pay for advanced biofeedback loops and integration with broader wellness dashboards. Manual models retain niches in regions with unreliable grids, offering simple crank mechanisms at the lowest cost of ownership. Nonetheless, software-driven differentiation is reshaping competitive dynamics, making proprietary algorithms and user-experience design central to brand equity.

By Frame Material: Sustainability Drives Material Innovation

Metal frames accounted for 59.40% of the 2025 share, favored for strength under frequent articulation cycles and compatibility with high-torque motors. Commercial buyers in hospitality and healthcare prize the corrosion resistance and serviceability of powder-coated steel, maintaining this leadership. A 6.09% CAGR supports the adjustable bed bases market for composite and alternative frames as brands pivot toward eco-friendly solutions. Recycled aluminum alloys and fiber-reinforced wood hybrids reduce weight by up to 20%, lowering freight emissions and easing assembly.

Environmental preferences shape purchasing criteria in Europe and parts of North America, where corporate sustainability targets carry procurement weight. Manufacturers experiment with bio-resin finishes and FSC-certified timber in visible components to align with green building standards. Weight reduction also suits e-commerce logistics, enabling flat-pack cartons that stay within parcel weight limits. Consumer marketing increasingly highlights cradle-to-grave recyclability and low-VOC coatings, signaling that sustainability is transitioning from a niche advantage to a mainstream expectation.

By Size: Twin Beds Emerge as Growth Leader

Queen bases held a 39.45% share in 2025, remaining the standard pick for couples balancing space and comfort. King models rank second, attracting premium household budgets and master-suite renovations. The twin segment, although smaller, will rise at a 5.69% CAGR to 2031, outpacing other sizes. The adjustable bed bases market share attached to twin units benefits from hospital overflow to home care and preferences among aging singles who value independent adjustability.

Urban housing density in Asia-Pacific and Europe further drives twin adoption because of limited bedroom square footage. Manufacturers address this by offering stackable twin foundations that join into a king width when needed, giving retailers a flexible upsell narrative. Specialty sizes, including split-king, draw interest from partners with different firmness and elevation requirements, supporting incremental sales of high-margin accessories such as synchronized controls and gap-filler couplers.

By End User: Commercial Applications Accelerate Growth

Residential buyers represented 63.25% of 2025 shipments, propelled by rising household wellness budgets and an expanding middle class in emerging economies. The residential segment is experiencing broadening demographic appeal beyond the traditional senior market, with younger consumers increasingly prioritizing sleep quality and wellness investments. The commercial sector’s 5.43% forecast CAGR underscores surging installation in hospitals and luxury hospitality venues.

Hotels report room-rate uplifts of 12-18% where adjustable beds replace static frames, warranting capital outlay from a ROI standpoint. Assisted-living facilities also specify medical-grade beds to increase resident comfort and reduce caregiver strain. Design teams integrate upholstery choices and headboards matching brand palettes, ensuring clinical function coexists with refined aesthetics. Commercial adoption thus extends beyond functionality, becoming an experiential differentiator in both patient recovery and guest satisfaction metrics.

By Distribution Channel: B2B Projects Outpace Retail Growth

B2C retail maintained 74.20% of transactions in 2025, though channel mix is evolving. Online specialty sites gained share as immersive AR room-preview tools and liberal return policies eased hesitation toward sight-unseen purchases. The adjustable bed bases market size coursing through B2B projects is set to reach a 5.91% CAGR by 2031, making institutional procurement the fastest grower. Bulk hotel refits and hospital expansions deliver predictable demand spikes and encourage relationship-based selling.

Institutional buyers require customized specifications, such as centralized software dashboards that monitor fleet diagnostics across multiple wards or properties. Manufacturers respond with project-dedicated sales teams, on-site installer training, and service-level agreements guaranteeing uptime. Features pioneered for B2B—like durable sealed motors and quick-swap control boxes—often cascade into consumer editions after cost optimization, demonstrating technology transfer between channels. Diversifying toward project volumes thus lowers exposure to discretionary household spending cycles.

Geography Analysis

North America retained leadership with 44.55% of global revenue in 2025, underpinned by widespread sleep-health awareness and established reimbursement pathways for medically indicated beds. The United States accounts for roughly 85% of regional sales and sets technology benchmarks that ripple worldwide. Smart feature attach rates are highest here, buoying average selling prices and reinforcing premium positioning. Favorable demographics—namely, the large Baby Boomer cohort—and the prevalence of sleep apnea and acid reflux conditions sustain consistent demand.

Asia-Pacific delivers the fastest 6.67% regional CAGR for 2026-2031, reflecting rapid urbanization, rising middle-class incomes, and maturing e-commerce infrastructure. Japan leads adoption due to its aging population and enthusiasm for home automation, whereas China provides the largest addressable base. In major Chinese cities, adjustable bases command growing interest as high-rise living amplifies space constraints that favor twin and split configurations. Local brands tailor cost-optimized models with pared-down feature sets to meet price expectations without sacrificing core adjustability.

Europe contributes steady growth driven by Northern markets that blend wellness culture with environmental standards. Regulatory encouragement for recyclable materials and circular design informs procurement, especially in healthcare systems that factor lifecycle cost into purchasing. The United Kingdom and Germany headline adoption, while France and the Nordics close the gap through heightened awareness campaigns. Design-centric consumer preferences favor minimalistic aesthetics integrated seamlessly into modern interiors, prompting European manufacturers to emphasize sculpted wood veneers and concealed actuators.

Mordor Intelligence provides coverage of the adjustable bed bases market across other key regional markets. Detailed country-level analysis extends to United States and United Kingdom incorporating local coverage and market participation, as required.

Competitive Landscape

Competitive intensity with vertically integrated bedding giants such as Leggett & Platt, Tempur Sealy, and Ergomotion occupying scale advantage through proprietary component manufacturing and multi-channel distribution. These incumbents invest heavily in software ecosystems that pair beds with companion apps, extending customer lifetime value through firmware updates and subscription analytics. Mid-tier challengers focus on cost engineering, deploying standardized actuators and universal control boards to offer entry-level adjustability at lower price points while maintaining acceptable margins.

A third cluster of entrants originates from the consumer electronics realm, leveraging algorithm expertise to deliver data-rich sleep coaching modules. Partnerships between upholstery specialists and health-tech firms accelerate feature rollouts such as contact-free biometric sensors embedded within the deck. White-space growth areas include ultra-light frames tailored for parcel networks, budget-friendly smart variants for price-sensitive shoppers, and purpose-built models for senior living communities prioritizing fall mitigation and caregiver ergonomics.

Strategic moves emphasize consolidation and vertical integration for supply security. Leggett & Platt’s network rationalization, reducing facilities from 50 to around 30-35, exemplifies efforts to curtail logistics costs while concentrating R&D on next-generation mechatronics.[2]Leggett & Platt, “Form 10-K 2025,” leggett.com Tempur Sealy’s pending Mattress Firm acquisition intends to merge manufacturing and retailing, potentially reshaping channel dynamics by unifying brand experience and data capture.[3]Leggett & Platt, “Form 10-K 2025,” leggett.com Technology disruptors distinguish themselves with open-API platforms, inviting third-party app developers to expand functionality, which could spur an ecosystem effect analogous to the smartphone model.

Adjustable Bed Bases Industry Leaders

Leggett & Platt, Inc.

Ergomotion, Inc.

Tempur Sealy International, Inc.

Sleep Number Corporation

Serta Simmons Bedding, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Med Supply launched the Prime Care P503 Medical Bed featuring zero-gravity and Trendelenburg modes for the home-care segment

- Dec 2024: Baxter International added continuous cardio-respiratory sensors to its Centrella Smart + bed line

- November 2024: Casper refreshed three adjustable base models with new comfort features across varied price tiers

- January 2024: Leggett & Platt completed a restructuring of its bedding segment, trimming sites to roughly 30-35 and optimizing distribution

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts an adjustable bed base as a stand-alone or integrated frame whose head, foot, or lumbar planes can be repositioned through manual cranks or electric actuators to enhance comfort, mobility assistance, or connected smart-sleep functions. Revenue includes factory-built bases sold with or without mattresses across residential and commercial channels worldwide and is reported in USD.

Scope exclusion: motion accessories retrofitted to traditional box springs are left outside this valuation.

Segmentation Overview

- By Bed Type

- Manual Adjustable Bed Bases

- Electric/Powered Adjustable Bed Bases

- Smart Adjustable Bed Bases

- By Frame Material

- Wood

- Metal

- Other Materials

- By Size

- Queen

- King

- Twin

- Full

- Other Size

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail Channels

- Home Centers/Home Improvement Stores

- Specialty Stores

- Online

- Other Distribution Channels

- B2B/Project (direct from the manufacturers)

- B2C/Retail Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed sleep-product engineers, hospital procurement heads, specialty-store buyers, and e-commerce category managers across North America, Europe, and key Asia-Pacific economies. Their insights validated adoption rates of smart bases, realistic average selling prices, and discounting practices, then filled coverage gaps for emerging distribution models.

Desk Research

Mordor analysts started with structured reviews of public datasets from bodies such as UN DESA, Eurostat, and the U.S. Census to map aging population trends and household furniture outlays. Trade flow records from the International Trade Center and customs dashboards helped us approximate cross-border shipments of metal bed frames, while association portals (for example, the American Home Furnishings Alliance) provided price corridors. Corporate filings, selected investor decks, scholarly journals on ergonomics, and paid platforms including D&B Hoovers and Dow Jones Factiva supplied additional financial, news, and patent clues. The sources mentioned illustrate the breadth consulted; many more items supported data capture, cross-checks, and clarification.

Market-Sizing & Forecasting

The core model applies a top-down build beginning with furniture retail and contract project spending, which is then filtered through penetration rates of adjustable platforms by region and end user. Select bottom-up roll-ups of leading OEM shipment disclosures and sampled ASP x volume checks act as guardrails that tune the totals. Variables feeding the model include: - share of population aged 60 and older, - median disposable income per household, - average retail price of electric bases, - import-export volume of HS 940389 sub-codes, - online furniture share of total furniture sales, - hotel room renovation starts.

A multivariate regression against these drivers generates the forecast; scenario analysis adjusts for currency shifts or large tender awards.

Any missing micro inputs are proxied from the closest public neighbor and flagged in the audit trail before final acceptance.

Data Validation & Update Cycle

Outputs undergo variance scans versus historical time series, peer ratios, and fresh news triggers. Two analyst reviews precede sign-off. We refresh each dataset annually and release interim revisions when raw material shocks, regulatory mandates, or material corporate actions alter market math.

Credibility Anchor: Why Mordor's Adjustable Bed Bases Baseline Numbers Stand Out

Published values differ because firms pick distinct scopes, price bases, and refresh cadences.

Key gap drivers include: some studies fold mattresses into the revenue pool, others model aggressive smart bed price inflation, and a few lift totals from shipment surveys without aligning them to retail markdowns. Mordor's view stays disciplined on frame-only value, applies blended regional ASPs vetted with channel partners, and benefits from an annual refresh that balances post-COVID e-commerce spikes with maturing demand.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.75 B (2025) | Mordor Intelligence | - |

| USD 8.20 B (2024) | Global Consultancy A | Combines bases with mattress bundles and bed set accessories |

| USD 9.24 B (2025) | Industry Journal B | Uses OEM shipment data without retail price normalization |

| USD 6.24 B (2021) | Data Publisher C | Older base year and includes adjustable mattresses |

Taken together, the comparison shows how scope breadth, price calibration, and data freshness swing published totals. Mordor's disciplined, transparent build anchored to verifiable variables offers decision-makers a balanced baseline they can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the adjustable bed bases market?

The adjustable bed bases market stands at USD 4.69 billion in 2026 and is projected to reach USD 6.14 billion by 2031.

Which region leads global sales?

North America leads with 44.55% of worldwide revenue thanks to strong healthcare integration and high consumer awareness.

Which bed type is growing the fastest?

Smart adjustable bases will expand at a 6.39% CAGR through 2031 due to IoT integration and automated sleep-optimization features.

How quickly is the commercial segment expanding?

Commercial applications in healthcare and hospitality are forecast to grow at 5.43% CAGR from 2026-2031.

Why are twin-size adjustable bases gaining traction?

Twin models benefit from aging single-person households, home-care settings, and urban space constraints, driving a 5.69% CAGR outlook.

What are the main barriers to wider adoption?

High price premiums over fixed foundations and ongoing supply-chain cost volatility remain the chief restraints on mass uptake.

Page last updated on: