DIY Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

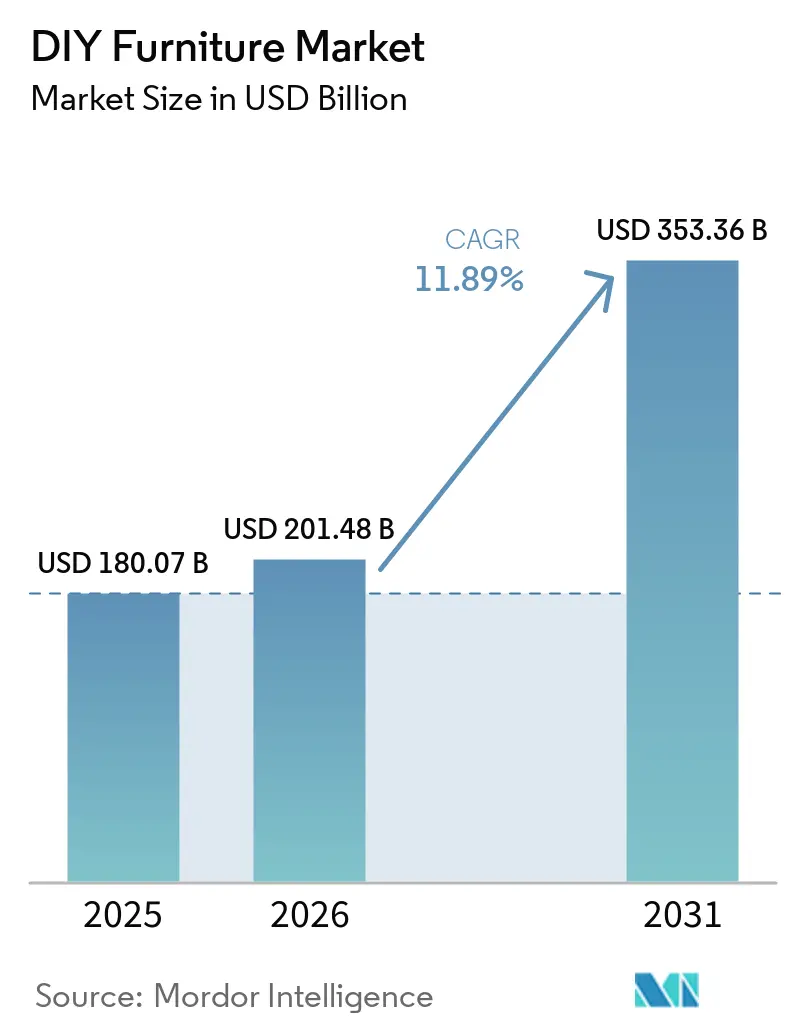

| Market Size (2026) | USD 201.48 Billion |

| Market Size (2031) | USD 353.36 Billion |

| Growth Rate (2026 - 2031) | 11.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DIY Furniture Market Analysis by Mordor Intelligence

The DIY furniture market size is expected to grow from USD 180.07 billion in 2025 to USD 201.48 billion in 2026 and is forecast to reach USD 353.36 billion by 2031 at 11.89% CAGR over 2026-2031. Surging do-it-yourself enthusiasm among Millennials and Gen Z, rapid e-commerce penetration, and steady modular design innovation are setting a brisk growth tempo. Online furniture sales doubled quarter-over-quarter in 2025 as generative-AI shopping guides simplified complex purchases[1]Amazon Press Center, “Amazon announces AI Shopping Guides,” press.aboutamazon.com. . Regulatory tightening around volatile organic compound (VOC) emissions is accelerating a shift toward low-formaldehyde wood composites and bio-based plastics. Modular connector breakthroughs that eliminate tools are lowering skill barriers, while 3D-printing pilots signal an on-demand production future. Competitive positioning is recalibrating as omnichannel leaders, direct-to-consumer disruptors, and traditional retailers race to capture share in the evolving DIY furniture market.

Key Report Takeaways

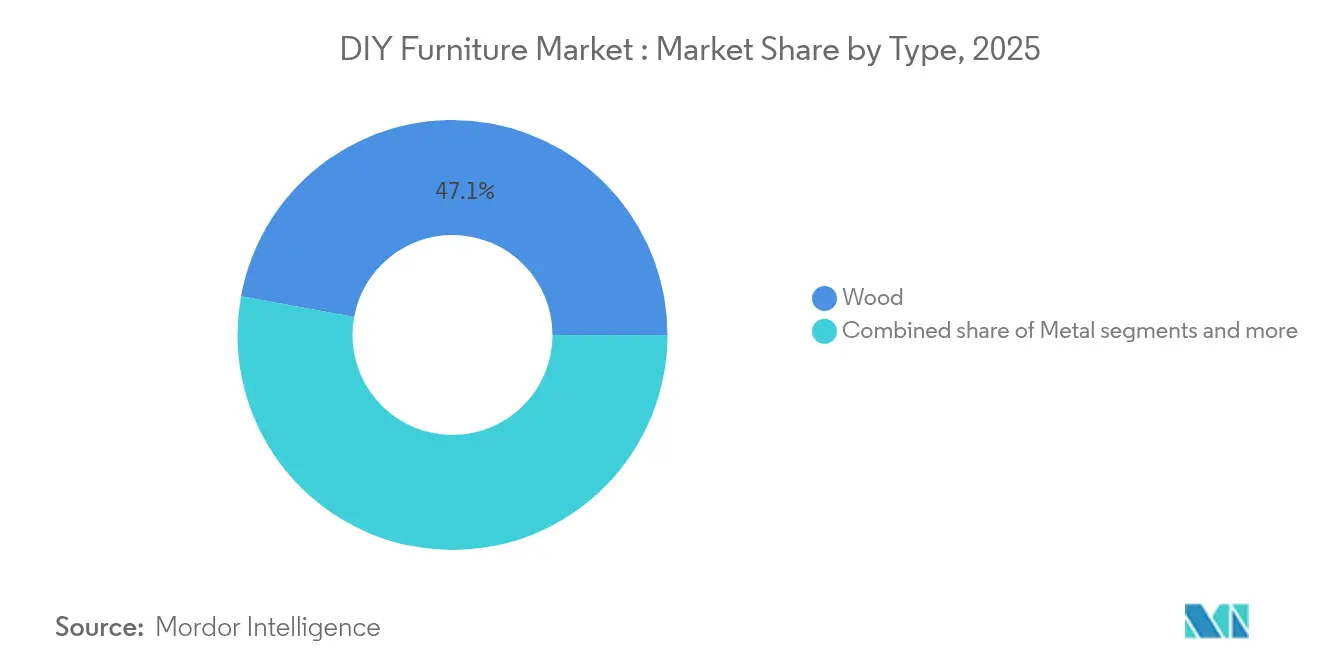

- By product type, wood accounted for 47.12% of the DIY furniture market share in 2025, while plastic products are projected to lead growth at a 9.66% CAGR through 2031.

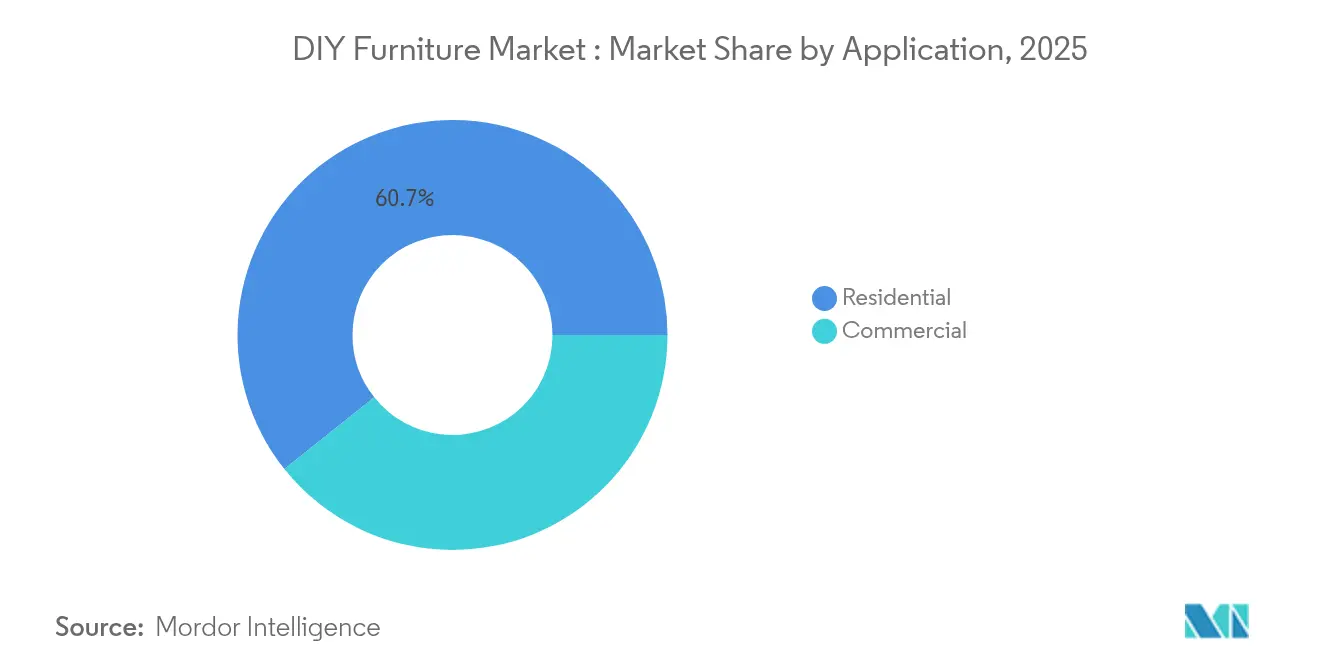

- By application, residential demand commanded 60.71% of the DIY furniture market size in 2025, whereas commercial installations are advancing at a 7.62% CAGR between 2026 and 2031.

- By distribution channel, offline outlets retained 64.52% share of the DIY furniture market in 2025; online sales are slated to climb at a 12.08% CAGR to 2031.

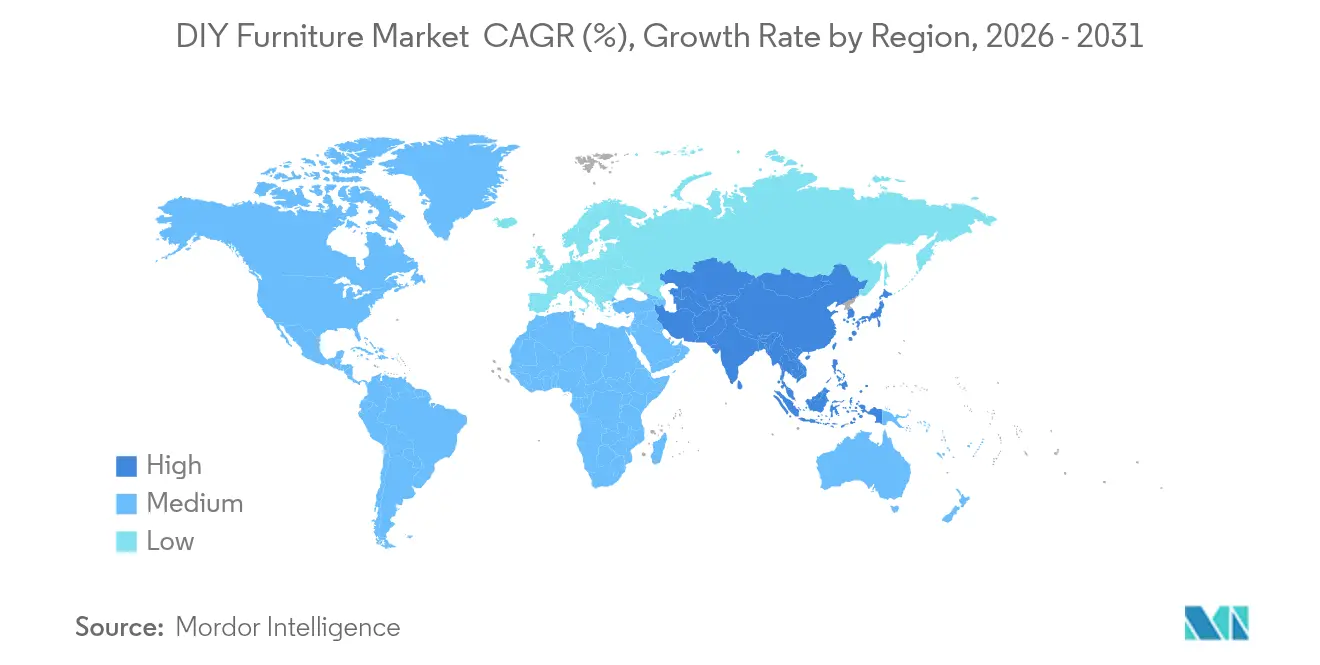

- By geography, North America led with 30.95% of the DIY furniture market share in 2025, but Asia-Pacific is on track for the fastest expansion, growing at a 9.61% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global DIY Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DIY culture among Millennials & Gen Z | +2.8% | North America, Europe, global urban hubs | Medium term (2-4 years) |

| E-commerce DIY kit platforms | +3.2% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Cost advantage versus ready-made furniture | +2.1% | Emerging markets worldwide | Long term (≥ 4 years) |

| Urbanization favoring flat-pack solutions | +2.4% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Tool-less modular connectors | +1.8% | North America, EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Influencer-led maker communities | +1.2% | Digitally connected markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing DIY culture among Millennials & Gen Z

Gen Z homeowners show 75% higher renovation intent than earlier generations at comparable life stages, viewing assembly as a creative expression as well as a budget-friendly solution [2]Caroline Spivack, “Gen Z and millennials plan more home renovations in 2025,” fortune.com. . This demographic shift reflects deeper values around personalization, sustainability, and cost consciousness that align with DIY furniture's core value proposition. Social media platforms have democratized design knowledge, with YouTube DIY tutorials generating over 2 billion views annually and Instagram's #DIYfurniture hashtag accumulating 4.2 million posts. The trend transcends mere cost savings, as younger consumers increasingly view furniture assembly as creative expression and skill development. Regulatory influence from consumer protection agencies like the Consumer Product Safety Commission ensures DIY products meet safety standards while maintaining accessibility for novice users.

Expansion of E-commerce DIY Kit Platforms

Digital commerce transformation has fundamentally altered DIY furniture distribution, with online channels capturing 34% market share and growing at 12.30% CAGR through 2030. Amazon's launch of AI Shopping Guides in October 2024 exemplifies platform evolution, using generative AI to provide product research and recommendations across 100+ categories, including furniture. The platform's "Bend the Curve" initiative, which purged billions of low-quality product listings, signals industry maturation toward curated, high-quality offerings rather than volume-based competition. IKEA's USD 2.2 billion US investment includes eight new stores in 2025, but significantly emphasizes smaller-format Plan & Order Points that bridge digital and physical experiences. Wayfair's Q1 2025 revenue of USD 2.73 billion and first large-format store opening demonstrate how pure-play e-commerce companies are pursuing omnichannel strategies to capture DIY furniture demand.

Cost Advantage Over Ready-Made Furniture

Economic pressures have intensified DIY furniture's cost appeal, with assembled furniture typically commanding 40-60% price premiums over flat-pack alternatives. However, this driver faces headwinds from rising material costs and supply chain volatility, with global supply chain disruptions increasing 38% in 2024 due to factory fires, labor disruptions, and extreme weather events. The cost advantage remains most pronounced in emerging markets, where local assembly labor costs are significantly lower than importing fully assembled pieces. Vietnam's position as the world's second-largest wooden furniture exporter, with USD 15.7 billion in exports during 2024, demonstrates how manufacturing cost arbitrage continues driving global DIY furniture supply chains. Regulatory compliance costs from tightening emission standards may compress margins, but economies of scale in flat-pack shipping and storage continue supporting the cost proposition.

Urbanization Driving Demand for Flat-Pack Solutions

Urban density increases have created structural demand for space-efficient furniture solutions, with the global urban population projected to reach 68% by 2050. Small apartment living necessitates furniture that maximizes functionality while minimizing storage and transportation footprints. IKEA's Rognan robotic furniture system, developed with Ori, exemplifies innovation in space-saving solutions, using automated mechanisms to transform studio apartments into multi-functional living spaces. India's home and interiors market growth from USD 29.5 billion in 2023 to a projected USD 48.1 billion by 2028 reflects urbanization's impact on furniture demand, with renovation cycles shortening from 15 years to 10-12 years as urban consumers embrace more frequent home updates. The trend particularly benefits modular systems that allow reconfiguration as living situations change, addressing urban mobility patterns where consumers frequently relocate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Assembly complexity for novices | –1.8% | Global, pronounced in aging markets | Medium term (2-4 years) |

| Durability concerns | –1.5% | Quality-conscious regions worldwide | Long term (≥ 4 years) |

| Tightening VOC/formaldehyde rules | –2.2% | EU, China, North America | Short term (≤ 2 years) |

| Fastener & hinge supply-chain volatility | –1.1% | Global manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Assembly complexity for novices

Assembly complexity is a significant restraint for novices in the DIY furniture market. Many DIY furniture kits include detailed instructions that can be confusing or overwhelming for beginners. Novices often lack the necessary tools and skills, which makes the assembly process more challenging. This can lead to errors, incomplete builds, or damaged parts, causing frustration and dissatisfaction. The time and effort required to complete complex assemblies may discourage first-time users from attempting future projects. Additionally, unclear or poorly translated instructions add to the difficulty. This complexity limits the market’s appeal to a wider audience, especially those who prefer quick and easy solutions. To overcome this, manufacturers need to simplify instructions and provide better customer support to improve the overall user experience[3]Standardization Administration of China, “GB 18584-2024,” sac.gov.cn..

Durability concerns

Durability concerns are a significant restraint in the DIY furniture market. Many DIY kits use materials that prioritize cost and ease of assembly over long-term strength. As a result, some pieces may weaken or break under regular use, leading to dissatisfaction among customers. Improper assembly by novices can also compromise the structural integrity of the furniture, making it less reliable. This lack of durability reduces consumer confidence and discourages repeat purchases. Furthermore, the perception that DIY furniture is less sturdy than professionally made products limits its appeal to buyers seeking lasting quality. To overcome this, manufacturers must focus on higher-quality materials and better construction methods to ensure their products withstand everyday wear and tear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Plastic momentum accelerates amid wood’s leadership

Wood maintains commanding market leadership with a 47.12% share in 2025, reflecting consumer preferences for natural aesthetics and perceived durability in residential applications. Traditional wood processing benefits from established supply chains, with Vietnam's USD 15.7 billion furniture export industry predominantly serving this segment. However, plastic segments demonstrate the strongest growth momentum at 9.66% CAGR through 2031, driven by innovations in bio-based materials and circular economy initiatives. A plant-based resin manufacturer claims 80% lower greenhouse gas emissions compared to traditional materials, while Aectual's partnership with Tetra Pak converts drink carton waste into 3D-printed furniture components.

Metal segments capture approximately 25% market share, particularly strong in commercial applications where durability and fire resistance requirements favor steel and aluminum construction. Glass segments remain niche but benefit from urbanization trends favoring visually lightweight furniture that enhances perceived space in small apartments. Regulatory compliance with formaldehyde emission standards increasingly influences material selection, with China's GB 18584-2024 effective July 2025 and EU REACH Annex XVII restrictions taking effect August 2026, creating compliance advantages for alternative materials.

By Application: Commercial workspaces shift into high gear

Residential applications dominate with 60.71% market share in 2025, supported by homeownership trends and the growing DIY culture among younger demographics. The segment benefits from renovation cycle acceleration, with urban consumers updating homes every 10-12 years compared to historical 15-year cycles. Home Depot's USD 18.25 billion SRS Distribution acquisition and 13 new store openings in 2025 demonstrate retailer confidence in sustained residential demand. Lowe's 2025 Total Home Strategy, incorporating AI frameworks with NVIDIA, OpenAI, and Palantir, reflects the segment's digital transformation toward personalized customer experiences.

Commercial applications exhibit the fastest growth at 7.62% CAGR through 2031. This acceleration reflects workplace evolution toward flexible, reconfigurable environments that favor modular furniture systems. The segment benefits from corporate sustainability mandates that increasingly favor circular economy furniture solutions. HNI Corporation's USD 2.2 billion Steelcase acquisition creates the largest workplace furnishing entity globally, signaling industry consolidation around commercial segment opportunities. ISO 14006 environmental management systems for eco-design increasingly influence commercial procurement decisions, favoring suppliers with verified sustainability credentials.

By Distribution Channel: Online Growth Reshapes Retail Landscape

Offline channels retain 64.52% market share in 2025, reflecting furniture's tactile nature and consumer preferences for physical inspection before purchase. Traditional retailers are adapting through omnichannel strategies, with IKEA's Plan & Order Points bridging digital and physical experiences while maintaining smaller footprints. Wayfair's first large-format store opening in Wilmette demonstrates how digital-native retailers are pursuing physical presence to capture hesitant online furniture buyers. Online channels demonstrate explosive growth at 12.08% CAGR through 2031, driven by improved visualization technologies and enhanced delivery capabilities. Amazon's AI Shopping Guides, launched in October 2024, exemplify platform evolution toward consultative selling that addresses traditional online furniture shopping friction. The channel particularly benefits from DIY furniture's flat-pack nature, which reduces shipping costs and damage risks compared to assembled furniture. However, the segment faces quality control challenges, with Amazon's "Bend the Curve" initiative removing billions of low-quality listings to improve marketplace integrity.

Geography Analysis

North America commands 30.95% market share in 2025, supported by a mature DIY culture and high homeownership rates. The region benefits from established retail infrastructure, with Home Depot and Lowe's combined market presence providing extensive distribution reach. However, growth moderates as market saturation increases and demographic shifts favor rental over ownership among younger consumers. The region's regulatory environment, including EPA formaldehyde standards under TSCA Title VI, creates compliance advantages for established players while potentially limiting new entrant access.

Asia-Pacific demonstrates the strongest growth trajectory at 9.61% CAGR through 2031, driven by rapid urbanization and rising disposable incomes. India's furniture market growth from USD 29.5 billion in 2023 to projected USD 48.1 billion by 2028 exemplifies regional dynamics. IKEA's expansion plan, including Pune, Chennai, and Kolkata stores, reflects confidence in the Indian market potential, while the company's 33% local sourcing strategy supports domestic manufacturing development. Southeast Asia's projected 5.1% annual GDP growth through 2034, outpacing China's 3.5-4.5%, positions the region as an increasingly important manufacturing and consumption hub.

Europe faces headwinds from economic uncertainty and stringent regulatory requirements. The EU's Ecodesign for Sustainable Products Regulation (ESPR) imposes durability, recycled content, and digital product passport requirements that increase compliance costs while potentially creating competitive moats for established players. The region's circular economy initiatives, including Veolia's 400,000 tons annual furniture recycling capacity, create opportunities for companies embracing sustainable business models.

Competitive Landscape

The DIY furniture market shows a moderate level of concentration, with a handful of major players dominating a significant portion of global revenue, while numerous smaller manufacturers cater to regional and niche markets. IKEA remains a key leader due to its early innovation in flat-pack design and a highly efficient global supply chain. However, the company faces growing competition from traditional retailers expanding their DIY product lines and newer digital-native brands appealing to younger consumers. The industry’s strategic focus is shifting toward omnichannel integration, with online-only retailers opening physical stores to enhance customer engagement. Conversely, established retailers are investing heavily in digital platforms and smaller, more flexible store formats to stay competitive. This evolving landscape is driving companies to innovate in both sales channels and customer experience. As a result, market dynamics are becoming more complex and competitive.

Recent years have seen a sharp increase in consolidation activity within the DIY furniture market, signaling industry maturation and the importance of scale for competitive advantage. Major acquisitions have reshaped the competitive landscape, allowing companies to strengthen their presence across multiple retail channels. This consolidation enables firms to better compete in omnichannel environments by combining resources and expertise. At the same time, it creates pressure on smaller players to innovate or find niche opportunities. The drive for scale and efficiency is essential as companies navigate an increasingly competitive global market. Strategic acquisitions also offer expanded product portfolios and enhanced operational capabilities. Overall, consolidation is a key trend shaping the future of the DIY furniture industry.

New opportunities are emerging in sustainability and technology innovation, opening fresh avenues for growth in the market. Companies are focusing on developing eco-friendly materials that significantly reduce greenhouse gas emissions, responding to increasing consumer demand for sustainable products. Advances in technology are also transforming the industry, with research suggesting that future furniture could feature embedded sensors to provide real-time assembly guidance. Disruptive newcomers are exploring 3D printing and circular economy models to offer more customizable and environmentally responsible solutions. Meanwhile, established companies are integrating artificial intelligence to optimize inventory management and improve customer experiences. Regulatory compliance with stricter emission standards is becoming a competitive advantage for firms with robust testing and certification processes.

DIY Furniture Industry Leaders

IKEA

The Home Depot

Lowe’s

Wayfair

Kingfisher (B&Q, Castorama)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: HNI Corporation announced a USD 2.2 billion cash-and-stock acquisition of Steelcase, creating the largest workplace furnishing entity globally with combined capabilities spanning residential building products and commercial furniture solutions.

- August 2025: MasterBrand completed an all-stock merger with American Woodmark Corporation, expanding its residential cabinet portfolio and expecting USD 90 million in cost synergies by year three post-merger.

- July 2025: China implemented GB 18584-2024 formaldehyde emission limits for furniture, establishing stricter standards that affect global supply chains serving Chinese markets.

- June 2025: IKEA announced a USD 2.2 billion US investment program, including eight new stores in 2025, emphasizing smaller Plan & Order Point formats that bridge digital and physical customer experiences.

Global DIY Furniture Market Report Scope

DIY furniture includes many products, like tables, chairs, shelves, cabinets, etc. It allows people to be creative and customize furniture according to their preferences. The DIY furniture market provides an unlimited range of collections and customized furniture. The DIY furniture market is segmented into type, application, distribution channel, and geography. By type, the market is segmented into metal, wood, plastic, and glass. By application, the market is segmented into residential and commercial. By distribution channel, the market is segmented into online and offline. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa. The report offers market size and forecasts for the DIY furniture market in value (USD) for all the above segments.

| Metal |

| Wood |

| Plastic |

| Glass |

| Residential |

| Commercial |

| Online |

| Offline |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Metal | |

| Wood | ||

| Plastic | ||

| Glass | ||

| By Application | Residential | |

| Commercial | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the DIY furniture market in 2026?

The DIY furniture market size was valued at USD 201.48 billion in 2026 and is projected to keep rising through 2031.

What is the forecast CAGR for DIY furniture between 2026 and 2031?

The market is expected to grow at a 11.89% CAGR over 2026-2031.

Which material segment is expanding the fastest?

Plastic-based DIY furniture is on track for a 9.66% CAGR, outpacing wood, metal, and glass.

Why is Asia-Pacific considering the growth engine for DIY furniture?

Rapid urbanization, income gains, and booming e-commerce are driving Asia-Pacific toward a 9.61% CAGR through 2031.

How are VOC regulations impacting manufacturers?

New Chinese and EU formaldehyde limits are raising compliance costs but also accelerating the shift toward low-emission materials and finishes.

Which companies are leading M&A activity?

HNI Corporation’s purchase of Steelcase and MasterBrand’s cabinet mergers headline current consolidation moves aimed at scale and omnichannel capabilities.

Page last updated on: