Autonomous Security Operations Center (SOC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.41 Billion |

| Market Size (2031) | USD 31.48 Billion |

| Growth Rate (2026 - 2031) | 24.77% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Security Operations Center (SOC) Market Analysis by Mordor Intelligence

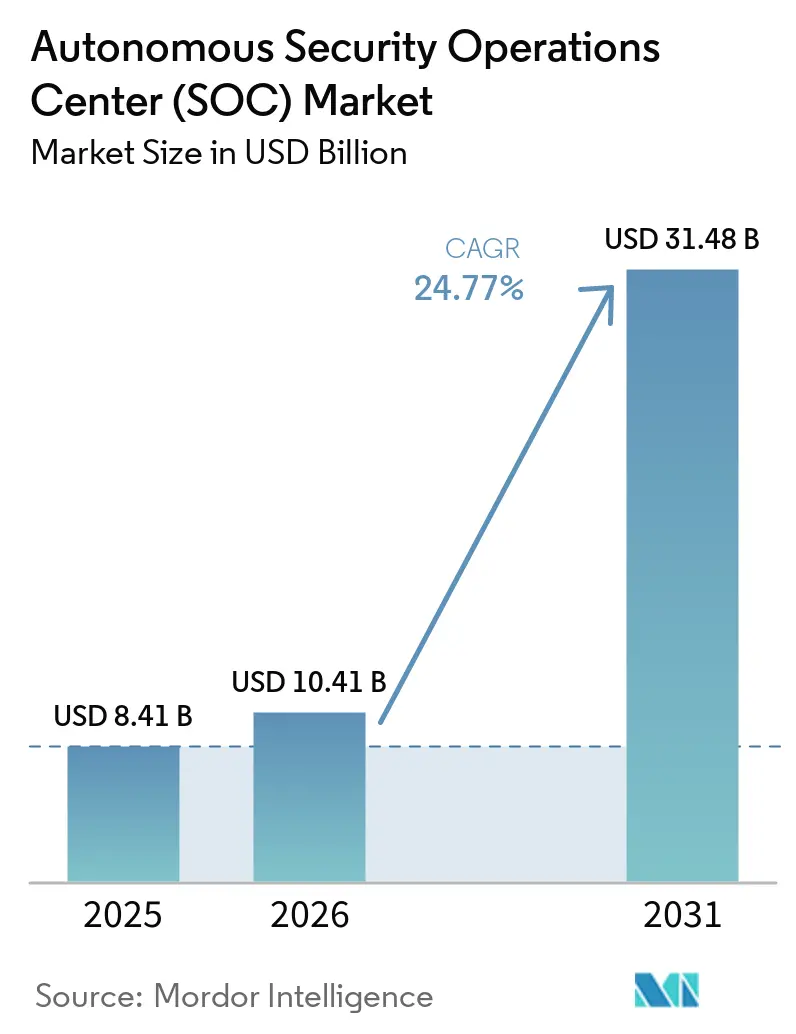

The autonomous Security Operations Center (SOC) market size is expected to grow from USD 8.41 billion in 2025 to USD 10.41 billion in 2026 and is forecast to reach USD 31.48 billion by 2031 at 24.77% CAGR over 2026-2031. The move toward AI-native security platforms is supporting growth, as enterprises now need faster detection, investigation, and response across growing attack surfaces. The market is also gaining momentum because AI-enabled adversaries increased sharply in 2025, which reduced the time available for human teams to review alerts and respond. This pressure has shifted buying priorities toward platforms that can automate triage, investigation, and response inside day-to-day security workflows. Vendor strategy is also changing, as large platform providers, endpoint security companies, and AI-focused challengers compete to become the primary operating layer for enterprise security operations. At the same time, explainability requirements, integration gaps with legacy tools, and rising compute costs are keeping governance, interoperability, and total operating cost at the center of purchase decisions.

Key Report Takeaways

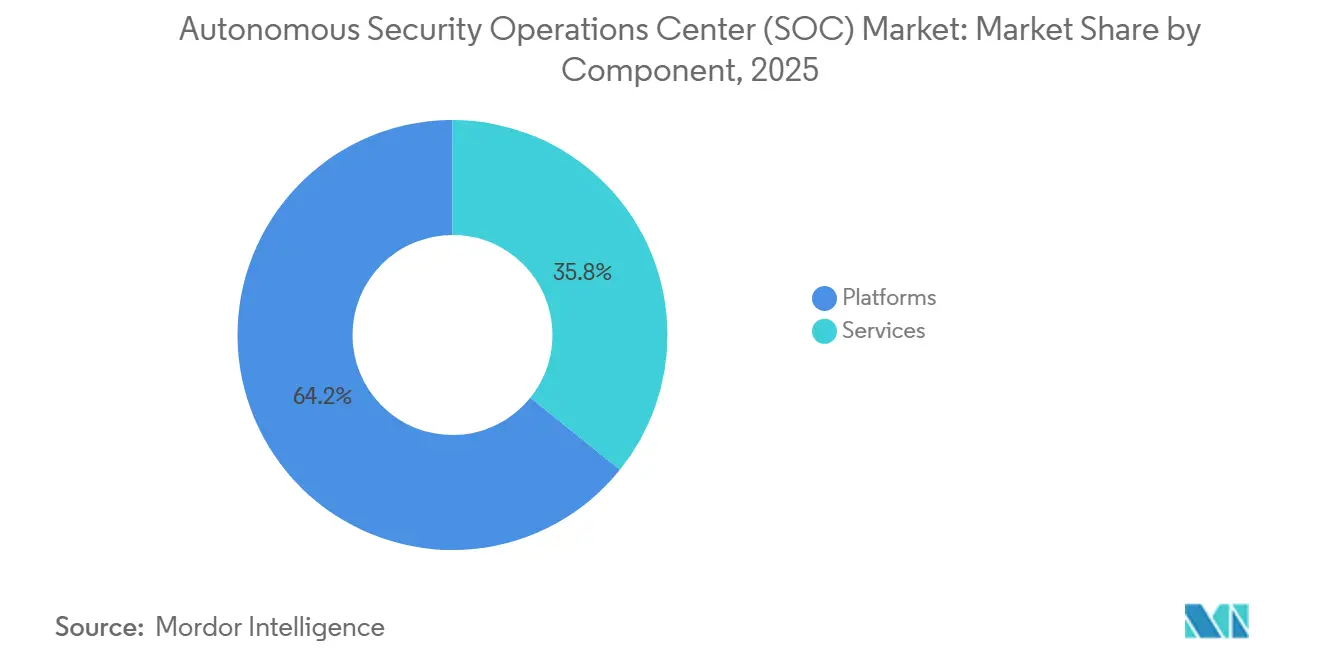

- By component, platforms held 64.21% share in 2025, while services are projected to expand at a 25.81% CAGR through 2031 in the autonomous Security Operations Center (SOC) market.

- By deployment, cloud accounted for 55.17% share in 2025, while hybrid is expected to record the fastest growth at 25.92% through 2031.

- By enterprise size, large enterprises captured 62.14% of the market in 2025, while small and medium enterprises are projected to grow at a 26.04% CAGR through 2031.

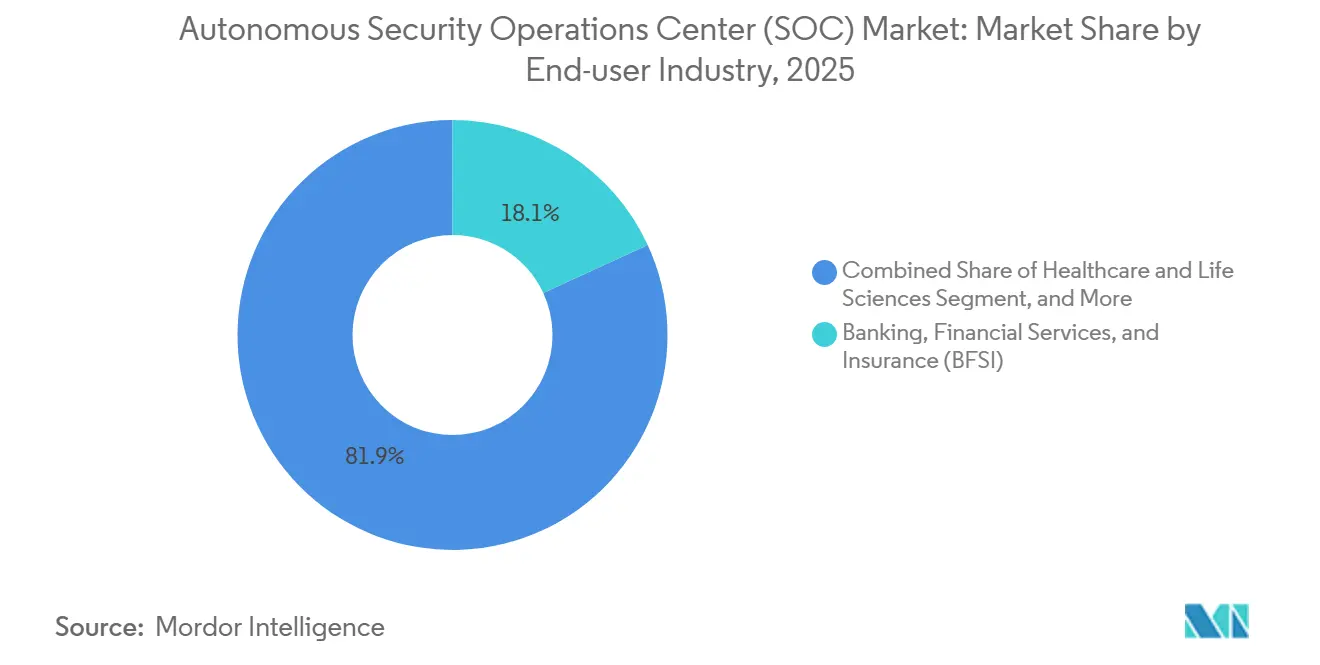

- By end-user industry, BFSI accounted for 18.12% of the autonomous Security Operations Center (SOC) market in 2025, while healthcare and life sciences are expected to expand at a 26.15% CAGR through 2031.

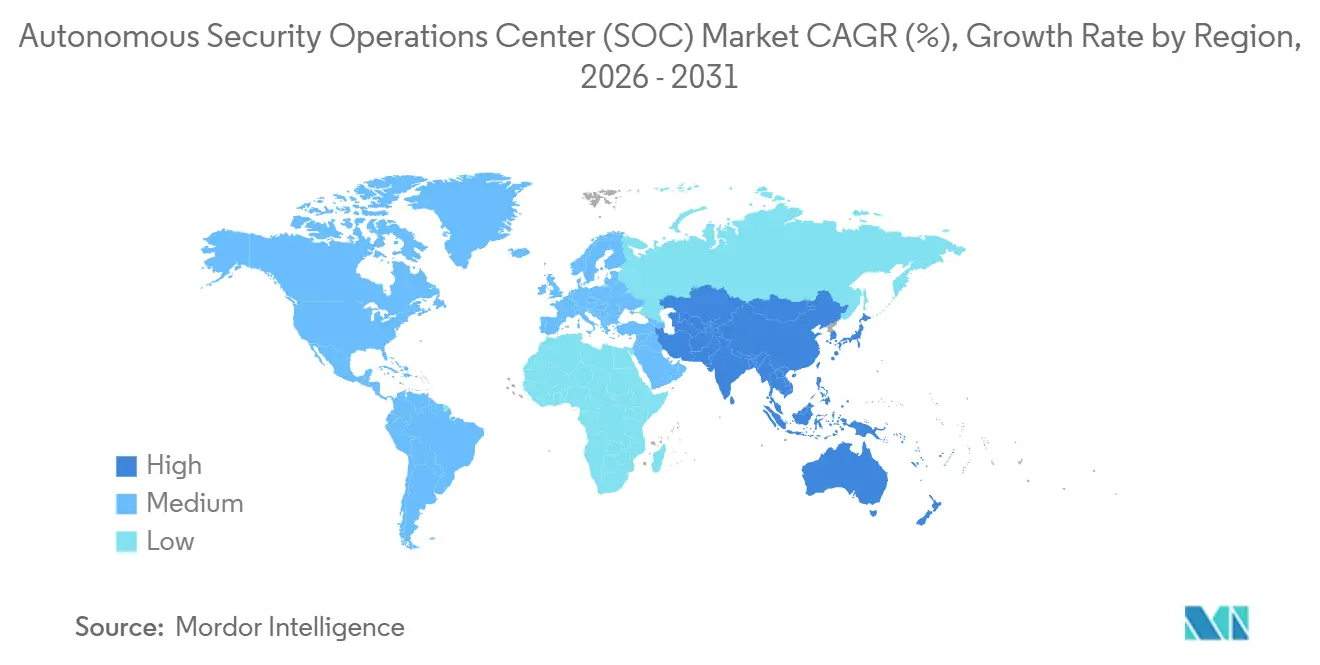

- By geography, North America held 34.18% share in 2025, while Asia-Pacific is projected to advance at a 26.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autonomous Security Operations Center (SOC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Alert Fatigue Across Security Operations Teams | +7.2% | Global | Short term (≤ 2 years) |

| Rising Adoption of AI Orchestration Across Threat Detection Workflows | +5.8% | North America and Europe, spill-over to APAC | Short term (≤ 2 years) |

| Expanding Cloud and Identity Telemetry Requiring Unified Autonomy | +4.4% | North America and APAC core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Regulatory Pressure for Continuous Control Monitoring | +3.6% | Europe and North America, spill-over to South America and APAC | Medium term (2-4 years) |

| Talent Shortages in SOC Analyst Roles | +2.9% | Global | Long term (≥ 4 years) |

| Demand For Faster Mean Time to Detect And Respond | +2.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Alert Fatigue Across Security Operations Teams

The autonomous Security Operations Center (SOC) market is benefiting from a simple operational reality: many security teams can no longer review alert volumes fast enough with human analysts alone. Cisco reported in 2025 that 59% of SOC teams faced too many alerts, 55% spent significant time on false positives, and data management issues accounted for 57% of investigation time.[1]CrowdStrike, “CrowdStrike State of Cloud Detection and Response Survey,” CrowdStrike, crowdstrike.com CrowdStrike also found that 79% of organizations believed their tools generated too many alerts, and teams spent 77% of triage time on false positives and low-priority detections. Palo Alto Networks stated that 13% of social engineering incidents in its 2025 incident response work succeeded because routine alerts were ignored or left untriaged. That operating pressure is pushing the autonomous Security Operations Center (SOC) market toward platforms that reduce analyst burden and lower the risk of missing a real attack amid the noise.

Rising Adoption of AI Orchestration Across Threat Detection Workflows

The autonomous Security Operations Center (SOC) market is also being shaped by the shift from fixed automation rules to AI orchestration that can investigate, reason, and act across several security steps. In March 2026, CrowdStrike and NVIDIA reported 5x faster investigations and 3x higher triage accuracy in Agentic MDR workloads using NVIDIA Nemotron models and NeMo Data Designer. Microsoft introduced its Security Analyst Agent at RSA 2026 to perform multi-step investigations across Defender and Sentinel telemetry and surface material risks in minutes with auditable reasoning chains. These launches show that competition in the autonomous Security Operations Center (SOC) market is moving toward systems that can coordinate multiple AI-led tasks rather than simply providing prompts or summaries.[2]Microsoft, “The Agentic SOC, Rethinking SecOps for the Next Decade,” Microsoft Security Blog, microsoft.com They also widen the gap between vendors with serious threat investigation data and those without a similar real-world feedback loop.

Expanding Cloud and Identity Telemetry Requiring Unified Autonomy

The autonomous Security Operations Center (SOC) market is expanding as cloud, identity, and AI workload telemetry become too broad to manage through isolated tools. CrowdStrike reported that 95% of organizations saw integration gaps between their cloud detection tools and primary SOC workflows, and 47% experienced suspicious activity targeting cloud-based AI and ML infrastructure during the previous 12 months. In June 2026, CrowdStrike extended Falcon AI Detection and Response across partners, including Databricks, Google Cloud, Microsoft Azure, NVIDIA, and Kong, so that AI model infrastructure could be monitored as a native attack surface. That same month, Cisco outlined a unified identity experience in Cloud Control that brings together signals from Duo, ISE, and third-party sources into one operating layer. This matters for the autonomous Security Operations Center (SOC) market because automated action is only safe when cloud behavior and identity context are visible in the same decision path.[3]Cisco, “Identity Elevated, A New Unified Identity Experience in Cisco Cloud Control,” Cisco Blog, cisco.com

Regulatory Pressure for Continuous Control Monitoring

The autonomous Security Operations Center (SOC) market is gaining support from regulations that now require continuous monitoring rather than periodic review. ISACA noted that DORA has been in effect since January 17, 2025, and requires financial entities to continuously monitor ICT systems, define alert thresholds, and report major incidents within 4 hours of classification.[4]ISACA, “Resilience and Security in Critical Sectors, Navigating NIS2 and DORA Requirements,” ISACA, isaca.org ENISA stated in its 2025 technical implementation guidance that monitoring activities should be automated and conducted continuously or at periodic intervals, while minimizing false positives and false negatives. NIS2 national transpositions, due in October 2026, and EU AI Act transparency provisions, active from August 2026, are adding further pressure for traceability and reviewability in AI-supported security operations. As a result, the autonomous Security Operations Center (SOC) market is seeing stronger demand for unified platforms that can continuously monitor, document decisions, and support audits across multiple rules simultaneously.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Model Explainability And Auditability Concerns | -3.4% | Europe and North America, spill-over to APAC | Medium term (2-4 years) |

| Integration Complexity With Legacy SIEM, SOAR, And EDR Stacks | -2.8% | Global | Short term (≤ 2 years) |

| High Compute Costs For Agentic AI Workloads | -1.9% | North America and Europe | Medium term (2-4 years) |

| Autonomous Action Risk In Mission-Critical Environments | -1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Model Explainability And Auditability Concerns

The autonomous Security Operations Center (SOC) market still faces hesitation from buyers who need clear reasoning behind automated triage and response actions. EU AI Act transparency provisions become active from August 2026, which raises the importance of traceability for systems used in security workflows. CrowdStrike has addressed part of this concern through Charlotte AI governance work, including ISO 42001 certification positioning and product claims that answerability and actions are user-authorized. Even so, the autonomous Security Operations Center (SOC) market is still dealing with the fact that strong model performance does not automatically produce explanations that buyers can audit with confidence. This issue matters most in regulated sectors where procurement teams want proof of governance controls before giving autonomous systems broader operating authority.

Integration Complexity With Legacy SIEM, SOAR, And EDR Stacks

The autonomous Security Operations Center (SOC) market is also constrained by the effort required to connect AI-native platforms with legacy multi-vendor environments. CrowdStrike found that enterprises used an average of 3 separate tools to manage cloud detections and that 67% reported significant or moderate gaps in integrating cloud events into existing SIEM workflows. Palo Alto Networks also cited IDC data showing that 45% of organizations were actively reducing their cybersecurity vendor count in 2025 and 2026, indicating that consolidation is underway but not yet complete. During that transition, the autonomous Security Operations Center (SOC) market must still work through proprietary schemas, fixed playbooks, and older ingestion models that are poorly suited to real-time AI reasoning. The result is slower deployment, longer proof-of-concept cycles, and more attention on vendors that can shorten integration effort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Lead Revenue While Services Grow Faster

Platforms accounted for 64.21% of revenue in 2025, making them the largest component of the autonomous Security Operations Center (SOC) market. Their lead came from their role as the main operating layer for threat detection, investigation, response, and data management. Buyers also tend to stay with these systems for years after telemetry is stored inside the platform, because the data improves model tuning and makes migration harder. This stickiness supports larger contract values and gives platform vendors room to deepen usage through connected endpoint, identity, cloud, and SIEM capabilities.

Services are projected to grow at a 25.81% CAGR from 2026 to 2031, making them the faster-moving part of the component mix. Growth is being driven by organizations that want autonomous workflows without building deep internal AI engineering or security operations teams. Agentic MDR and SOC transformation offerings are expanding as they combine intelligent automation with expert oversight, helping customers move faster from pilots to production. This shifts services beyond standard managed SOC support and toward higher-value operating models, where vendors take on more responsibility for detection quality, response speed, and security outcomes.

By Deployment: Cloud Holds The Lead While Hybrid Builds Momentum

Cloud deployments held 55.17% of the market in 2025, which gave them the largest share across deployment models. Their lead reflects the strong fit between cloud delivery and modern security operations, where continuous updates, shared threat intelligence, and scalable compute are important for AI-based response. Cloud platforms also align closely with the workloads, APIs, and identities that enterprises increasingly need to secure. These advantages make the cloud the starting point for many new autonomous SOC rollouts. Organizations that want quicker implementation and regular model improvement often prefer this deployment path over more infrastructure-heavy alternatives.

Hybrid deployments are projected to grow at a 25.92% CAGR from 2026 to 2031, making them the fastest-growing deployment model. This reflects the needs of organizations that must keep sensitive data in private or sovereign environments while still using cloud-based AI for speed and scale. Hybrid is especially relevant in regulated sectors where auditability, explainability, and human oversight are more important in system design. On-premises models still matter in defense, government, and critical infrastructure settings, where strict localization rules remain in place. As a result, deployment preferences are likely to remain mixed rather than fully shift toward a single operating model.

By Enterprise Size: Large Enterprises Lead While SMEs Expand Faster

Large enterprises accounted for 62.14% of revenue in 2025, which made them the leading customer group by organization size. Their position reflects higher alert volumes, more complex tool environments, and stronger budgets for integration, governance, and premium software licenses. These organizations also tend to evaluate autonomous SOC spending based on avoided breach costs and operating resilience rather than solely on workforce efficiency. Because their environments are broader and harder to manage, they gain more value from automated investigation and response at scale. This keeps large enterprises at the center of current revenue generation across the market.

Small and medium enterprises are projected to grow at a 26.04% CAGR from 2026 to 2031, making them the faster-growing size segment. Their growth shows that autonomous SOC capabilities are moving beyond large enterprise deployments and becoming easier to access through lighter delivery models. Vendors are reducing setup friction with simpler onboarding, API-led activation, and workflows that do not require a fully staffed internal security operations center. This matters because smaller firms face the same attack speed but operate with fewer skilled analysts. Over time, broader adoption of SMEs could make autonomous triage a standard security capability rather than a premium feature.

By End-User Industry: BFSI Leads While Healthcare And Life Sciences Grow Faster

BFSI held an 18.12% share in 2025, making it the largest end-user segment in the autonomous Security Operations Center (SOC) market. Its lead stemmed from a combination of heavy regulatory oversight, significant transaction exposure, and a threat landscape that demands faster detection and response. Financial institutions are under pressure to maintain continuous ICT monitoring, quicker incident classification, and stronger audit records. The segment also remains a frequent target for advanced threat actors, which increases the value of automated investigation and containment. These factors make BFSI the strongest current demand center for autonomous SOC platforms and related services.

Healthcare and life sciences are projected to grow at a 26.15% CAGR from 2026 to 2031, making them the fastest-growing end-user segment. Growth is being supported by rising focus on encryption, continuous vulnerability management, and stronger protection of electronic health information across hospitals and care systems. These organizations increasingly need persistent monitoring and faster remediation as digital tools become more central to care delivery. At the same time, the market remains broad across government, IT and telecommunication, energy and utilities, industrial manufacturing, retail, transportation, oil and gas, media, and education. That diversity supports wider expansion beyond the leading verticals.

Geography Analysis

North America held 34.18% share in 2025, making it the largest region in the autonomous security operations center (SOC) market. The United States remains the core market because it combines a deep vendor base, broad enterprise cloud adoption, and strong demand for continuous security monitoring. The region also benefits from large federal technology budgets and tighter documentation and response requirements in regulated sectors. CrowdStrike reinforced the ecosystem strength in North America when it launched the Charlotte AI AgentWorks Ecosystem at RSA 2026 with partners including AWS, Anthropic, NVIDIA, OpenAI, Salesforce, Accenture, Deloitte, Kroll, and Telefónica Tech.

Asia-Pacific is projected to grow at a 26.27% CAGR from 2026 to 2031, making it the fastest-growing regional market for autonomous Security Operations Centers (SOCs). Growth across the region is tied to rapid digital expansion, rising state-linked cyber activity, and a shortage of in-house security talent, which increases demand for managed and autonomous models. China’s Network Data Security Management Regulations, which became effective in 2025, are supporting domestic investment in sovereign-aligned security platforms. India is also contributing through stronger breach reporting expectations and wider digital infrastructure buildout across public and private systems. Japan, South Korea, Australia, and Southeast Asia are seeing increased demand for financial services, defense-related operations, and cloud-first, localized programs that modernize enterprise security.

Europe recorded meaningful revenue in 2025, supported by the German, UK, and French enterprise security markets and by the combined effect of DORA and NIS2. ENISA stated in 2025 that monitoring should be automated and carried out continuously or at periodic intervals, which directly supports the platform logic of the autonomous Security Operations Center (SOC) market. The overlap among DORA, NIS2, the EU AI Act, and the Cyber Resilience Act is compressing the upgrade cycle for enterprises that previously relied on point-in-time compliance practices. The Middle East and Africa are also opening new opportunities through sovereign AI programs, smart city investments, and critical infrastructure protection work in countries such as Saudi Arabia and the United Arab Emirates. South America remains an emerging demand pool, led by Brazil, where stronger data protection enforcement is lifting interest from financial services and government buyers.

Competitive Landscape

The autonomous Security Operations Center (SOC) market is moderately concentrated at the platform level, but it remains broad and competitive across managed services, SIEM modernization, and AI-led detection. CrowdStrike, Microsoft, and Palo Alto Networks form a leading platform group because each is tying autonomous investigation to larger product stacks across endpoint, identity, cloud, and network security. That strategy raises switching costs and gives these vendors more ways to expand contract value after the first deployment. The autonomous Security Operations Center (SOC) market also includes strong specialist competition, which limits the chance of one vendor dominating the whole value chain.

SentinelOne has pushed a multi-model path in the autonomous Security Operations Center (SOC) market through Purple AI, combining Anthropic Claude, OpenAI GPT, and its proprietary Ultraviolet models for zero-click investigation. IBM launched IBM Autonomous Security in April 2026 as a multi-agent service designed to coordinate decisions, responses, and intelligence across enterprise environments with limited human intervention. Darktrace expanded its presence by bringing its ActiveAI platform into the Microsoft Security Store and by joining the OpenAI Daybreak Cyber Partner Program in 2026. Arctic Wolf Networks, Sophos, Trellix, ReliaQuest, Exabeam, Securonix, Vectra AI, Check Point, Cisco, Fortinet, Rapid7, Splunk, Elastic, Google, and others continue to compete for different layers of the autonomous Security Operations Center (SOC) market. This keeps pricing, product design, and go-to-market models more varied than in markets dominated by only a few providers.

White space in the autonomous Security Operations Center (SOC) market remains strongest in regulated deployments, lower-cost MDR access for SMEs, and cross-domain orchestration across IT and OT environments. CrowdStrike’s Charlotte AI governance positioning and ISO 42001 certification work show how governance-ready design is becoming a practical differentiator for enterprise procurement. Lumu reported that its Autopilot had executed 7.2 million end-to-end investigation and remediation workflows autonomously since 2024, which shows that scaled autonomous operations are no longer limited to the largest platforms. The autonomous Security Operations Center (SOC) market is therefore being shaped by both platform scale and workflow execution depth, with advantage moving toward vendors that can connect data, reasoning, and action in a reliable operating loop.

Autonomous Security Operations Center (SOC) Industry Leaders

CrowdStrike Holdings, Inc.

Microsoft Corporation

Palo Alto Networks, Inc.

SentinelOne, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: IBM joined the OpenAI Daybreak Cyber Partner Program and launched an application security service using OpenAI's cyber-capable models to identify and validate software vulnerabilities with greater speed and precision, extending IBM's frontier AI cyber-defense capabilities into the enterprise software supply chain.

- June 2026: SentinelOne opened Purple AI Agentic Investigation to all customers and introduced Singularity Credits as a unified AI-work currency across its Singularity Platform. The capability delivers zero-click, autonomously initiated investigations that detect, investigate, verify, and respond to threats at machine speed using a multi-model approach combining Anthropic Claude, OpenAI GPT, and SentinelOne's proprietary Ultraviolet models.

- June 2026: CrowdStrike launched Continuous Identity for AI Agents, a new Falcon Next-Gen Identity Security capability that establishes the Falcon platform as the identity security control plane for the agentic enterprise, providing continuous behavioral monitoring of AI agent identities across enterprise environments.

- June 2026: CrowdStrike extended Falcon AI Detection and Response (AIDR) across AI gateway partners including Databricks, Google Cloud, Microsoft Azure, NVIDIA, and Kong, making AI model infrastructure a natively protected attack surface within the Falcon platform and enabling correlated threat detection and policy enforcement across AI workloads.

Global Autonomous Security Operations Center (SOC) Market Report Scope

The Autonomous Security Operations Center (SOC) market refers to platforms and services that integrate artificial intelligence, automation, and agentic security operations to transform traditional SOC functions into self-directed, adaptive systems. These solutions include AI-native SOC platforms, autonomous investigation and response platforms, and agentic security operations platforms that can detect, analyze, and respond to cyber threats with minimal human intervention.

The Autonomous Security Operations Center (SOC) market report is segmented by Component (Platforms [AI-Native SOC Platforms, Autonomous Investigation and Response Platforms, Agentic Security Operations Platforms], and Services), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (Government and Public Administration, Industrial Manufacturing, Retail and E-Commerce, Transportation and Logistics, Energy and Utilities, Oil and Gas, IT and Telecommunication, Media and Entertainment, Education and Research Institutions, Healthcare and Life Sciences, and Banking, Financial Services, and Insurance (BFSI)), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platforms | AI-Native SOC Platforms |

| Autonomous Investigation and Response Platforms | |

| Agentic Security Operations Platforms | |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Government and Public Administration |

| Industrial Manufacturing |

| Retail and E-Commerce |

| Transportation and Logistics |

| Energy and Utilities |

| Oil and Gas |

| IT and Telecommunication |

| Media and Entertainment |

| Education and Research Institutions |

| Healthcare and Life Sciences |

| Banking, Financial Services, and Insurance (BFSI) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Platforms | AI-Native SOC Platforms | |

| Autonomous Investigation and Response Platforms | |||

| Agentic Security Operations Platforms | |||

| Services | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | Government and Public Administration | ||

| Industrial Manufacturing | |||

| Retail and E-Commerce | |||

| Transportation and Logistics | |||

| Energy and Utilities | |||

| Oil and Gas | |||

| IT and Telecommunication | |||

| Media and Entertainment | |||

| Education and Research Institutions | |||

| Healthcare and Life Sciences | |||

| Banking, Financial Services, and Insurance (BFSI) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the autonomous Security Operations Center (SOC) space?

The autonomous Security Operations Center (SOC) market size stood at USD 8.41 billion in 2025, reached USD 10.41 billion in 2026, and is forecast to reach USD 31.48 billion by 2031 at a 24.77% CAGR.

Which component leads revenue in this space?

Platforms led with 64.21% share in 2025 because they act as the main layer for AI-driven detection, investigation, and response across enterprise security operations.

Which deployment model is growing the fastest?

Hybrid is projected to grow at a 25.92% CAGR through 2031 as buyers balance data residency needs with cloud-delivered AI capabilities.

Which end-user group is the largest buyer today?

BFSI held 18.12% share in 2025, supported by strict monitoring and reporting obligations under DORA and high pressure from advanced financial-sector threats.

Which region offers the fastest expansion opportunity?

Asia-Pacific is expected to expand at a 26.27% CAGR through 2031, driven by digital infrastructure growth, stronger cyber regulation, and limited in-house security talent.

What is shaping vendor competition most strongly?

Competition is centered on AI orchestration depth, cross-domain telemetry integration, governance readiness, and the ability to automate investigation and response without creating audit risk.

Page last updated on: