Cybersecurity For Autonomous Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

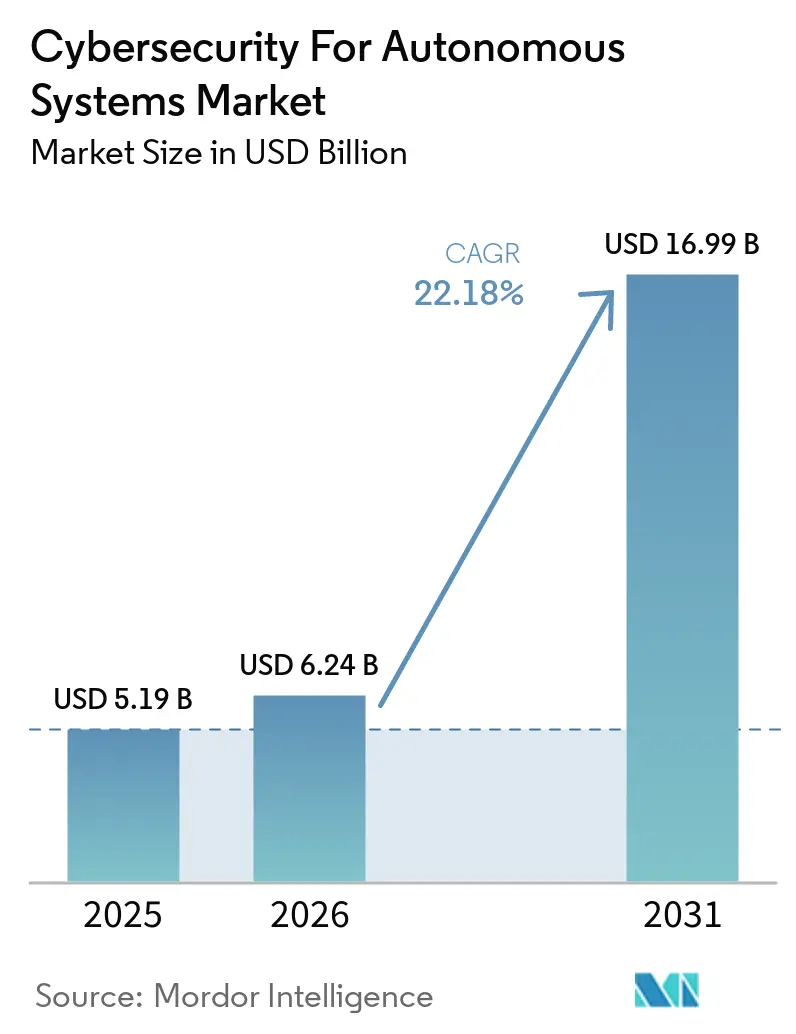

| Market Size (2026) | USD 6.24 Billion |

| Market Size (2031) | USD 16.99 Billion |

| Growth Rate (2026 - 2031) | 22.18% CAGR |

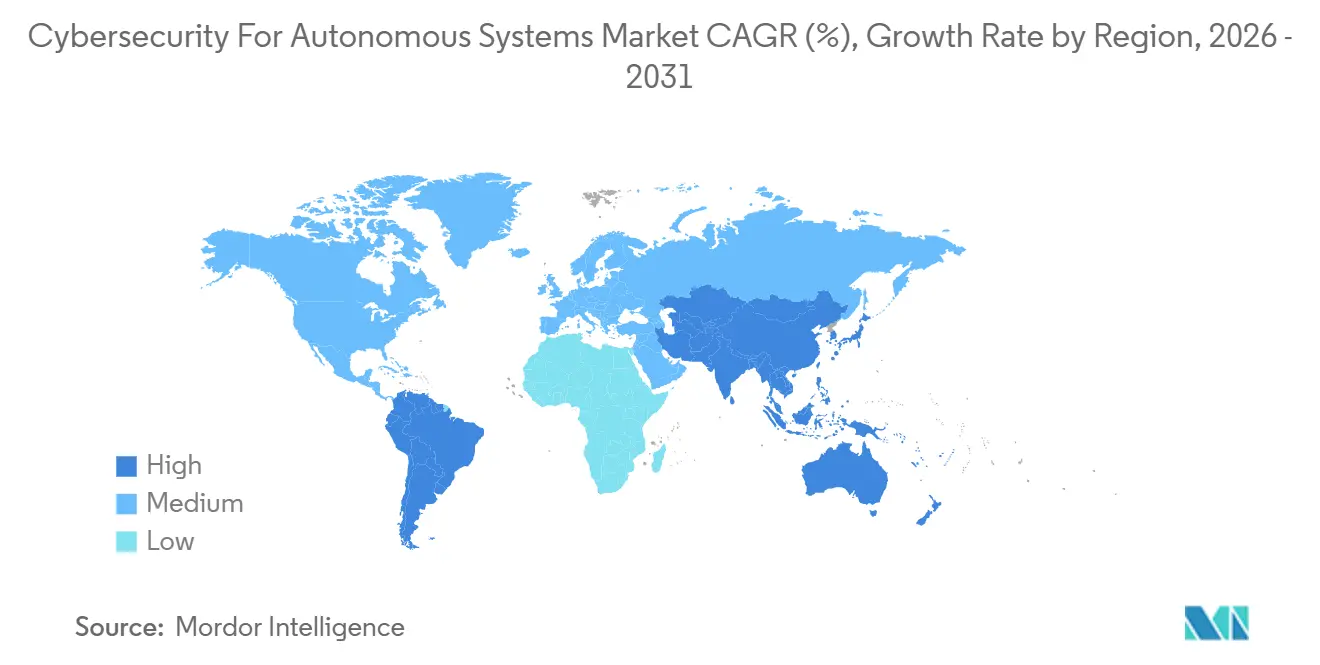

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity For Autonomous Systems Market Analysis by Mordor Intelligence

The Cybersecurity for Autonomous Systems Market size is projected to expand from USD 5.1 billion in 2025 and USD 6.2 billion in 2026 to USD 16.9 billion by 2031, registering a CAGR of 22.1% between 2026 and 2031. Regulatory rules for vehicles, medical devices, and other connected, autonomous platforms are making cybersecurity a baseline buying requirement rather than an optional add-on. The Cybersecurity for Autonomous Systems Market is also benefiting from the closer integration of operational technology and information technology, which exposes industrial robots, vehicles, and remote fleets to attack methods that older security tools were not designed to handle. AI-led attacks are now moving faster than manual response teams, which is pushing the Cybersecurity for Autonomous Systems Market toward continuous monitoring, model protection, and autonomous response tools. Liability pressure is adding urgency for OEMs, suppliers, and operators, especially when software updates, model behavior, and component integrity can affect safety outcomes. Competition is therefore shifting toward compliance automation, hardware-rooted trust, and managed services, while buyers look for vendors that can scale across automotive, industrial, healthcare, and defense deployments.

Key Report Takeaways

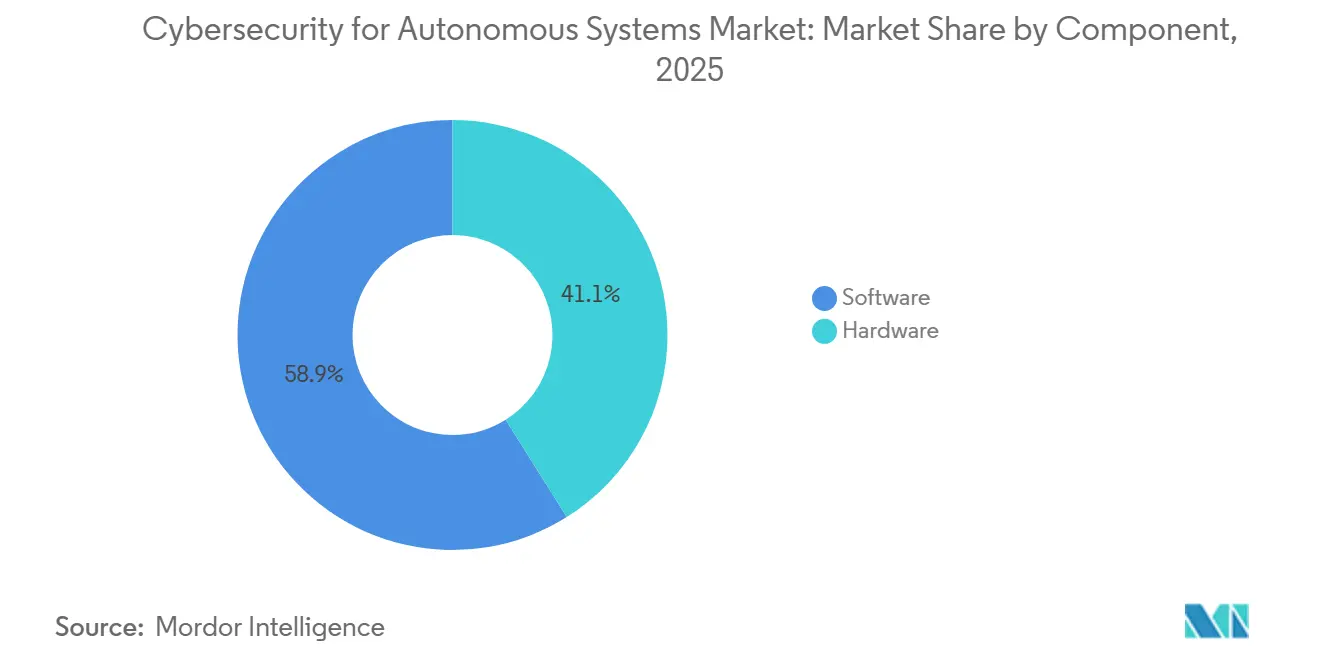

- By component, software led with a 58.9% revenue share in the Cybersecurity for Autonomous Systems Market in 2025, while hardware is projected to expand at a 23.2% CAGR through 2031.

- By security type, data and communication security held the largest share at 27.1% in the Cybersecurity for Autonomous Systems Market in 2025, while autonomous AI and model security recorded the highest projected CAGR at 23.3% through 2031.

- By deployment, cloud held 53.1% revenue share in 2025, while hybrid deployment is forecast to advance at a 23.4% CAGR through 2031.

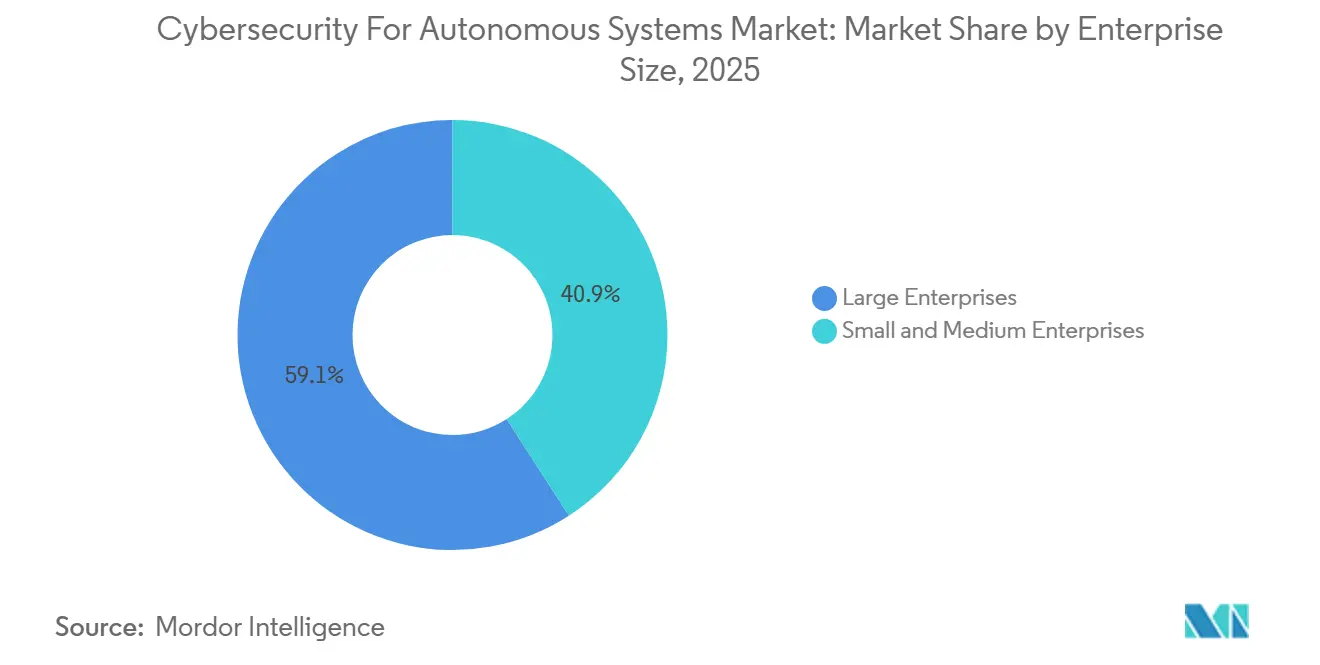

- By enterprise size, large enterprises held 59.1% revenue share of the cybersecurity for autonomous systems market in 2025, while SMEs are set to grow fastest at a 23.6% CAGR through 2031.

- By end-user industry, automotive and transportation accounted for 18.2% of the market share in 2025, while healthcare robotics is projected to grow at a 23.7% CAGR through 2031.

- By geography, North America held a 32.12% share in 2024, while the Asia Pacific is expected to grow at a 22.38% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cybersecurity For Autonomous Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Safety Certification Requirements for Autonomous Platforms | +4.3% | Global, concentrated near-term impact in EU, Japan, and South Korea | Short term (≤ 2 years) |

| Expansion of AI-Enabled Attack Surface Across Connected Autonomous Systems | +3.7% | Global, particularly North America, EU, and APAC cloud-connected fleets | Medium term (2-4 years) |

| Convergence of OT and IT in Autonomous Operations | +3.1% | North America, Europe, and APAC industrial and logistics corridors | Medium term (2-4 years) |

| Increasing Liability Exposure for OEMs, Integrators, and Operators | +2.5% | North America and EU, with spillover to APAC and GCC markets | Short term (≤ 2 years) |

| Growing Defense and Critical Infrastructure Investment in Trusted Autonomy | +2.0% | North America, NATO Europe, and APAC defense-modernizing nations | Long term (≥ 4 years) |

| Rapid Growth of OTA Update and Remote Fleet Management Workflows | +1.5% | Global, with early-mover intensity in North America and EU automotive sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Safety Certification Requirements for Autonomous Platforms

Rising certification demands are making the Cybersecurity for Autonomous Systems Market more rule-driven, especially in sectors where autonomous functions are already close to large-scale deployment. UNECE Regulation No. 155 required cybersecurity management systems for vehicle type approval across more than 60 contracting parties, and ISO/SAE 21434 remained the main technical path for lifecycle risk analysis and control design.[1]United Nations Economic Commission for Europe, “UN Regulation No. 155 – Cybersecurity and Cybersecurity Management System,” EUR-Lex, eur-lex.europa.eu In healthcare robotics, the U.S. FDA issued final guidance in June 2025 requiring software bills of materials, lifecycle threat modeling, and coordinated vulnerability disclosure for connected medical devices under Section 524B. These requirements now extend beyond OEMs, as Tier 1 and Tier 2 suppliers must also provide security-by-design evidence before programs move forward. That shift is expanding demand in the Cybersecurity for Autonomous Systems Market for tools and services that can produce audit-ready compliance records at scale.[2]World Economic Forum, “Global Cybersecurity Outlook 2026, Chapter 3, The Trends Reshaping Cybersecurity,” World Economic Forum, weforum.org

Expansion of AI-Enabled Attack Surface Across Connected Autonomous Systems

The Cybersecurity for Autonomous Systems Market is also being shaped by a larger attack surface that now includes the AI models behind autonomous decisions. The World Economic Forum reported in 2026 that 87% of respondents saw AI-related vulnerabilities as the fastest-growing cyber risk, while structured AI security assessments rose from 37% in 2025 to 64% in 2026.[3]National Institute of Standards and Technology, “NIST Mathematical Proof Supports Transition to a Continuous-Monitor-and-Update Security Model for AI Systems,” NIST, nist.gov NIST published a mathematical proof in June 2026 showing that no finite set of static guardrails can stay universally robust against adaptive adversarial prompts. OWASP also documented prompt injection, tool abuse, memory poisoning, and excessive agency as production-exploitable weaknesses in agentic AI systems. As a result, the Cybersecurity for Autonomous Systems Market is shifting budget toward continuous testing, monitoring, and updating of model behavior rather than one-time assessments.

Convergence of OT and IT in Autonomous Operations

The Cybersecurity for Autonomous Systems Market is expanding as the old separation between OT and IT breaks down. The World Economic Forum found that only 16% of organizations with industrial environments report OT security issues to their boards, 32% actively monitor OT systems with dedicated tooling, and 20% maintain dedicated OT security teams. At the same time, autonomous platforms are relying more heavily on Linux-based systems, cloud APIs, and open-source software, which lets attackers reuse familiar IT methods inside industrial settings. Kaspersky ICS CERT reported that 10,408 distinct malware families were blocked across industrial automation systems in Q2 2025 alone. This gap is pushing the Cybersecurity for Autonomous Systems Market toward unified visibility platforms that can track both enterprise and industrial assets.[4]Kaspersky ICS CERT, “Industrial Threat Report for Q2 2025,” Kaspersky ICS CERT, ics-cert.kaspersky.com

Increasing Liability Exposure for OEMs, Integrators, and Operators

Liability exposure is becoming a stronger spending driver in the Cybersecurity for Autonomous Systems Market as courts and regulators place greater weight on software behavior and update management. In August 2025, a Florida federal jury ordered Tesla to pay USD 243 million in an Autopilot case tied to a 2019 fatal crash. The broader lesson for autonomous system operators is that software defects, weak component validation, and incomplete incident response records can all carry direct financial consequences. That pressure reaches the supply chain because a weakness in a sensor or software module can trigger responsibility higher up the stack. Buyers are therefore paying closer attention to software integrity checks, software bills of materials, and documented response playbooks when evaluating vendors in the Cybersecurity for Autonomous Systems Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Standards Across Robotics, Automotive, Drone, and Industrial Autonomy Domains | -2.9% | Global, most acute in markets without mandatory cyber regulation for non-automotive autonomous systems | Medium term (2-4 years) |

| Shortage of Safety-Grade Cybersecurity Talent for Autonomous Environments | -2.3% | Global, most severe in APAC industrial centers and South America | Long term (≥ 4 years) |

| High Retrofit Cost for Legacy Autonomous and Semi-Autonomous Fleets | -1.8% | North America and Europe legacy automotive and industrial fleets | Medium term (2-4 years) |

| Long Validation, Certification, and Procurement Cycles | -1.2% | Aerospace and defense, healthcare robotics, and regulated sectors globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Standards Across Robotics, Automotive, Drone, and Industrial Autonomy Domains

The Cybersecurity for Autonomous Systems Market still faces a major brake because there is no single global security framework for all forms of autonomy. Automotive programs follow UNECE R155 and R156 alongside ISO/SAE 21434, while robotic surgical systems sit under FDA Section 524B and related medical software rules. Industrial automation also relies on a separate standards track based on IEC 62443 guidance, leaving buyers and vendors working across several rule sets at once. This patchwork forces vendors to build separate evidence packages and product positioning for each vertical, lengthening sales cycles and increasing go-to-market costs. It also slows spending in the Cybersecurity for Autonomous Systems Market, where buyers prefer to wait for clearer regulatory direction before committing to full security stacks.

Shortage of Safety-Grade Cybersecurity Talent for Autonomous Environments

The Cybersecurity for Autonomous Systems Market is also constrained by a shortage of people who understand both cybersecurity and safety-critical autonomous operations. The World Economic Forum found that only 20% of organizations operating in industrial environments maintain dedicated OT security teams, and 45% cited skills shortages as the top barrier to stronger cyber resilience. In autonomous settings, the problem is more challenging because teams need knowledge of industrial control, robotics, or vehicle engineering alongside modern cyber defense skills. The Cloud Security Alliance wrote in June 2026 that AI-powered vulnerability discovery is compressing the OT security timeline against an installed base that is slow to adapt. This is creating room in the Cybersecurity for Autonomous Systems Market for managed services and autonomous security operations platforms that can fill the staffing gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue While Hardware Investment Accelerates

Software accounted for 58.9% of the Cybersecurity for Autonomous Systems Market share in 2025, making it the largest component by revenue. The software base was supported by demand for real-time intrusion detection, AI-driven threat analytics, and software-defined policy enforcement across cloud-connected and embedded autonomous systems. In the Cybersecurity for Autonomous Systems Market, this segment also covers fleet monitoring, ECU firmware integrity checks, and AI model security orchestration for industrial robots and vehicles. Services added meaningful revenue because many organizations still relied on outside support for managed detection, penetration testing, and multi-framework compliance work.

Hardware is set to grow at a 23.2% CAGR in the Cybersecurity for Autonomous Systems Market through 2031 as OEMs add hardware security modules, trusted platform modules, and secure elements to new designs. This shift shows that trust is moving closer to silicon rather than staying only in software. A 2025 paper in Automotive Innovation argued that hardware-level isolation needed to sit at the foundation of connected and automated vehicle defense because software-only protection left room for sensor spoofing and compromise of vehicle control units. That view supports current sourcing behavior, with buyers giving more weight to cryptographic root-of-trust and embedded security design.

By Security Type: AI and Model Security Redefines the Priority Stack

Data and communication security held a 27.1% share in 2025, making it the largest security type in the Cybersecurity for Autonomous Systems Market. Its lead came from the central role of encrypted V2X links, authenticated data channels, and secure cloud pipelines across automotive, logistics, and defense deployments. Application and runtime security stayed close behind as buyers focused on protecting the live execution of autonomous decision logic. Identity, access, and device trust security also moved higher on budgets as more autonomous platforms relied on machine identities for tool access, API calls, and cross-system communication.

Autonomous AI and model security is forecast to expand at 23.3% CAGR, making it the fastest-growing security type in the Cybersecurity for Autonomous Systems Market through 2031. In June 2026, CrowdStrike introduced Continuous Identity for AI Agents to manage dynamic privileges for AI-driven workflows, addressing the growing need to control non-human identities in autonomous settings. NIST also showed in June 2026 that static guardrails cannot provide universal protection against adaptive adversarial inputs. This is moving model security spending from a research topic to a production requirement for systems operating at higher levels of autonomy.

By Deployment: Cloud Dominates, Hybrid Architecture Captures Fastest Growth

Cloud held a 53.1% revenue share in 2025, maintaining its leading deployment position in the Cybersecurity for Autonomous Systems Market. It remained the preferred setup for over-the-air update management, fleet telemetry aggregation, and centralized policy enforcement across large and dispersed device bases. For logistics, transportation, and agricultural operators, cloud deployment also offered scale and reduced infrastructure burden as fleets spread across multiple locations. On-premises deployment still mattered in defense and critical infrastructure settings, where air-gapped operations, classified workloads, or strict latency requirements limited reliance on the cloud.

Hybrid deployment is projected to grow at a 23.4% CAGR in the Cybersecurity for Autonomous Systems Market through 2031, as many operators seek cloud-level intelligence alongside local control for time-sensitive functions. Einride outlined a hybrid OTA update model that combines cloud-layer cryptographic signing with on-vehicle verification to reduce exposure to man-in-the-middle attacks. That design meets the practical needs of operators who cannot make every security decision in a remote environment. UNECE R156 also reinforces this direction by requiring structured software update management systems for regulated vehicle categories.

By Enterprise Size: Large Enterprises Lead Spend, SMEs Drive the Next Growth Phase

Large enterprises held 59.1% of the revenue share in 2025, keeping them at the center of the Cybersecurity for Autonomous Systems Market. Their lead came from concentration in automotive, defense, and industrial manufacturing, where autonomous deployment maturity and compliance obligations were already high. Large OEMs operating cybersecurity management systems and industrial groups aligning to OT security standards remained core customers for enterprise platforms. Their scale also favored vendors that could offer cloud-native reach, multi-site visibility, and integration with product development and operations toolchains.

SMEs are forecast to grow at 23.6% CAGR in the Cybersecurity for Autonomous Systems Market through 2031 as autonomous mobile robots, drone fleets, and contract manufacturing automation spread into smaller organizations. Many of these companies are adopting autonomy without large internal security teams or long legacy infrastructure cycles. RADICL in 2026 secured USD 31 million in Series A funding to build autonomous virtual SOC capabilities for smaller businesses in highly targeted sectors. Cloud-delivered security-as-a-service is therefore becoming a major enabler, as it reduces the upfront burden for buyers who cannot justify dedicated on-premises investments.

By End-User Industry: Automotive Anchors Revenue, Healthcare Robotics Accelerates

Automotive and transportation held an 18.2% share in 2025, making it the largest end-user category in the Cybersecurity for Autonomous Systems Market. This lead reflected years of connected vehicle security spending and the stronger compliance pull created by UNECE R155 across OEM supplier programs. Industrial manufacturing also remained important as autonomous welding, assembly, and materials-handling systems connected more directly to enterprise networks. Aerospace and defense, logistics and warehousing, and agriculture and drones all remained active demand areas, although their security maturity still varied by use case and procurement cycle.

Healthcare robotics is projected to expand at 23.7% CAGR in the Cybersecurity for Autonomous Systems Market through 2031, making it the fastest-growing end-user segment. The FDA issued final guidance in June 2025 requiring software bills of materials, lifecycle threat modeling, and coordinated vulnerability disclosure for connected medical devices. A 2025 study in Computer Fraud and Security showed that robotic-assisted surgical systems needed layered cryptographic authentication for navigation data streams to meet safety risk thresholds. That combination is raising the technical and documentation standard for cybersecurity procurement in healthcare robotics.

Geography Analysis

North America accounted for 31.12% of the Cybersecurity for Autonomous Systems Market share in 2025, making it the largest regional contributor. The region benefited from concentrated defense spending on trusted autonomy, a dense base of enterprise security vendors, and a strong cluster of OEM and Tier 1 suppliers aligned with vehicle cybersecurity requirements. The Cybersecurity for Autonomous Systems Market in North America also gained from the need to maintain access to global vehicle approval regimes and to support connected fleet operations at scale. Regulatory scrutiny of automated driving systems is keeping continuous software security, update integrity, and incident readiness high on spending agendas. Canada and Mexico extend this position because both are tied closely to North American automotive and manufacturing supply chains.

Asia-Pacific is forecast to post the fastest regional growth at a 23.38% CAGR, giving the Cybersecurity for Autonomous Systems Market its strongest expansion runway outside North America. Japan moved early on UN R155 for higher autonomy vehicles, and METI's Mobility DX Strategy 2025 points to stronger supplier network cybersecurity evaluation as part of the country's policy direction. China adds scale through the expansion of software-defined vehicles, while South Korea supports demand through its advanced Tier 1 automotive base. India is also widening the addressable market through industrial robotics and logistics automation. Europe remains a major revenue center because automotive and industrial operators there face overlapping cybersecurity compliance needs, which should support procurement through the forecast period.

In South America, the Middle East, and Africa, the Cybersecurity for Autonomous Systems Market is smaller today but moving into a broader adoption stage. Brazil benefits from its automotive manufacturing links to multinational OEM supply chains, while the rest of South America is seeing earlier demand from logistics and industrial automation use cases. In the Gulf, smart city investment and sovereign AI programs are creating early demand for security around autonomous systems and connected infrastructure. South Africa and Nigeria remain nascent opportunities, with mining automation and drone logistics as the most visible entry points for future expansion.

Competitive Landscape

The Cybersecurity for Autonomous Systems Market shows fragmentation, with broad enterprise security vendors holding the largest revenue positions and specialist CPS players retaining strong technical depth. Palo Alto Networks, CrowdStrike, Cisco Systems, IBM, and Microsoft form the core platform tier across cloud, identity, and response functions. CrowdStrike in March 2026 releases a Secure-by-Design AI Blueprint with NVIDIA that embeds Falcon protection into NVIDIA OpenShell autonomous agent runtimes. Cisco in 2026 expands its AI defense strategy and highlights post-quantum protections for the network layer that supports connected and autonomous operations. In 2025, IBM launched the Autonomous Threat Operations Machine, demonstrating how large vendors are packaging machine-speed triage and remediation into enterprise security operations.

The specialist tier remains important because the Cybersecurity for Autonomous Systems Market still needs deep OT, IoT, and embedded system expertise that platform vendors do not always deliver with the same precision. Claroty and Nozomi Networks are the names most often associated with this specialist position in industrial and cyber-physical security. Nozomi introduced Vantage IQ in January 2026 as a private AI assistant for OT and IoT security teams, addressing the need for faster decision support in industrial autonomous environments. White-space demand remains evident in cross-domain compliance automation, embedded AI model protection, and hardware-rooted trust for constrained edge devices. Kai Security also emerged in 2026 with USD 125 million in funding, aiming for machine-speed defense against AI-enabled threats.

Going forward, the Cybersecurity for Autonomous Systems Market is likely to reward vendors that can connect compliance, detection, identity, and response without forcing buyers into separate stacks. Buyers are also favoring vendors that can serve automotive, industrial, healthcare, and defense programs through a common control framework. That preference should support broader platforms, but it also leaves space for specialists who can prove faster deployment and stronger domain-specific coverage. The competitive balance, therefore, depends less on brand recognition alone and more on who can reduce deployment friction, produce audit evidence, and secure AI-led autonomous operations in real time.

Cybersecurity For Autonomous Systems Industry Leaders

Palo Alto Networks, Inc.

Fortinet, Inc.

Cisco Systems, Inc.

CrowdStrike Holdings, Inc.

Thales S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: CrowdStrike unveils Continuous Identity for AI Agents, a Falcon Next-Gen Identity Security capability incorporating technology from its SGNL acquisition. The feature dynamically grants, denies, and revokes access rights for AI agents based on real-time risk signals, eliminating standing privilege accumulation across autonomous system workflows.

- June 2026: Cisco unveils Cisco Cloud Control at Cisco Live as a unified agentic platform for managing and defending critical IT infrastructure, while also introducing IOS XE 26 with full-stack post-quantum cryptography protections for enterprise networks underpinning autonomous operations.

- March 2026: CrowdStrike and IBM expand their strategic AI security partnership, integrating Charlotte AI with IBM's Autonomous Threat Operations Machine for coordinated machine-speed investigation and containment, and extending the Falcon platform into IBM Consulting's managed Threat Detection and Response services.

- 2026: CrowdStrike and NVIDIA release a Secure-by-Design AI Blueprint integrating the CrowdStrike Falcon platform into NVIDIA OpenShell, embedding runtime security at the foundation of autonomous agent deployments on NVIDIA DGX Spark and DGX Station compute platforms.

Global Cybersecurity For Autonomous Systems Market Report Scope

The Cybersecurity for Autonomous Systems market focuses on solutions and services that protect autonomous technologies such as vehicles, drones, robotics, industrial automation, and defense systems from cyber threats, data breaches, and operational disruptions. It includes AI and model security, secure communication protocols, runtime application protection, and identity/device trust frameworks to ensure safe and reliable functioning. The rapid adoption of autonomous technologies, the growing sophistication of cyberattacks targeting AI-driven systems, and the need to comply with safety and security regulations are driving the market. Industries like automotive, aerospace, defense, healthcare robotics, manufacturing, logistics, and agriculture are increasingly deploying these solutions to safeguard mission-critical operations, protect sensitive data, and maintain resilience. Its primary goal is to build secure, trustworthy, and resilient autonomous ecosystems through proactive defenses, continuous monitoring, and identity governance, ensuring operational safety, compliance, and protection of digital and physical assets.

The Cybersecurity for Autonomous Systems market report is segmented by Component (Hardware, Software, and Services), Security Type (Autonomous AI and Model Security, Data and Communication Security, Application and Runtime Security, Identity, Access and Device Trust Security), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (Automotive and Transportation, Industrial Manufacturing, Aerospace and Defense, Healthcare Robotics, Logistics and Warehousing, Agriculture and Drones, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Autonomous AI and Model Security |

| Data and Communication Security |

| Application and Runtime Security |

| Identity, Access and Device Trust Security |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Automotive and Transportation |

| Industrial Manufacturing |

| Aerospace and Defense |

| Healthcare Robotics |

| Logistics and Warehousing |

| Agriculture and Drones |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Security Type | Autonomous AI and Model Security | ||

| Data and Communication Security | |||

| Application and Runtime Security | |||

| Identity, Access and Device Trust Security | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | Automotive and Transportation | ||

| Industrial Manufacturing | |||

| Aerospace and Defense | |||

| Healthcare Robotics | |||

| Logistics and Warehousing | |||

| Agriculture and Drones | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2031 outlook for cybersecurity in autonomous systems?

The Cybersecurity for Autonomous Systems Market is projected to reach USD 16.9 billion by 2031, up from USD 6.2 billion in 2026, at a 22.1% CAGR.

Which component category leads current revenue?

Software led with 58.9% revenue share in 2025 because buyers prioritized intrusion detection, analytics, policy enforcement, and fleet security orchestration.

Which security type is growing the fastest?

Autonomous AI and model security is the fastest-growing security type, with a projected 23.3% CAGR through 2031 as model-level risks become harder to manage with static controls.

Why is healthcare robotics becoming a high-growth area?

Healthcare robotics is forecast to grow at 23.7% CAGR through 2031, supported by the FDA's 2025 cybersecurity guidance for connected medical devices and stronger technical control requirements.

Which region currently leads global demand?

North America led with 31.12% share in 2025, supported by defense autonomy spending, a mature security ecosystem, and strong automotive supplier concentration.

What is driving adoption among smaller organizations?

SMEs are projected to grow at 23.6% CAGR through 2031 as autonomous mobile robots and drone deployments spread into smaller operators that prefer cloud-delivered security services.

Page last updated on: