SCADA Security Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.17 Billion |

| Market Size (2031) | USD 11.55 Billion |

| Growth Rate (2026 - 2031) | 17.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SCADA Security Solutions Market Analysis by Mordor Intelligence

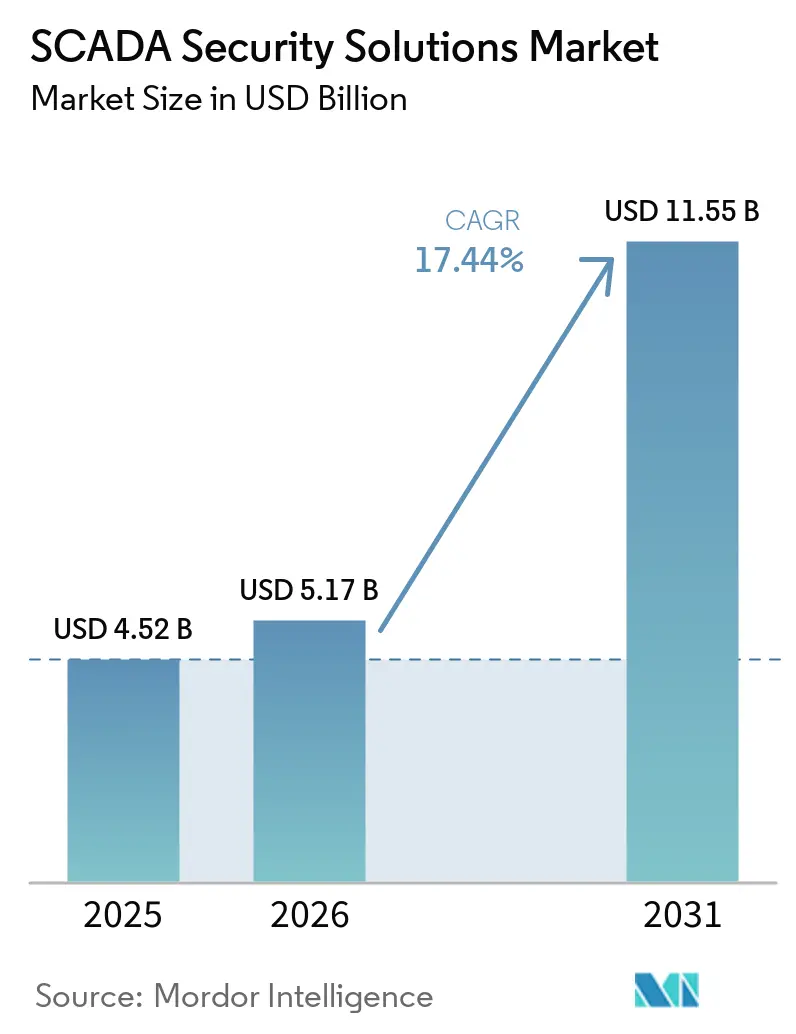

The SCADA Security Solutions Market size was valued at USD 4.52 billion in 2025 and is projected to reach USD 11.55 billion by 2031, at a CAGR of 17.44% during 2026-2031. Attackers are moving beyond simple data theft and are increasingly studying industrial control loops so they can interrupt physical operations. That change is shortening buying cycles among power, water, manufacturing, healthcare, and public sector operators that cannot absorb long outages. Demand is also rising because IT and OT environments now connect more tightly, which exposes legacy control systems to a wider set of threats. Compliance rules across North America and Europe are reinforcing spending plans, while cloud and hybrid deployment models are making continuous monitoring easier to scale across many sites. Even with high retrofit costs in older plants, the SCADA Security Solutions Market is gaining support from stronger managed services demand, growing healthcare exposure, and a large installed base of organizations that still do not actively monitor OT systems.

Key Report Takeaways

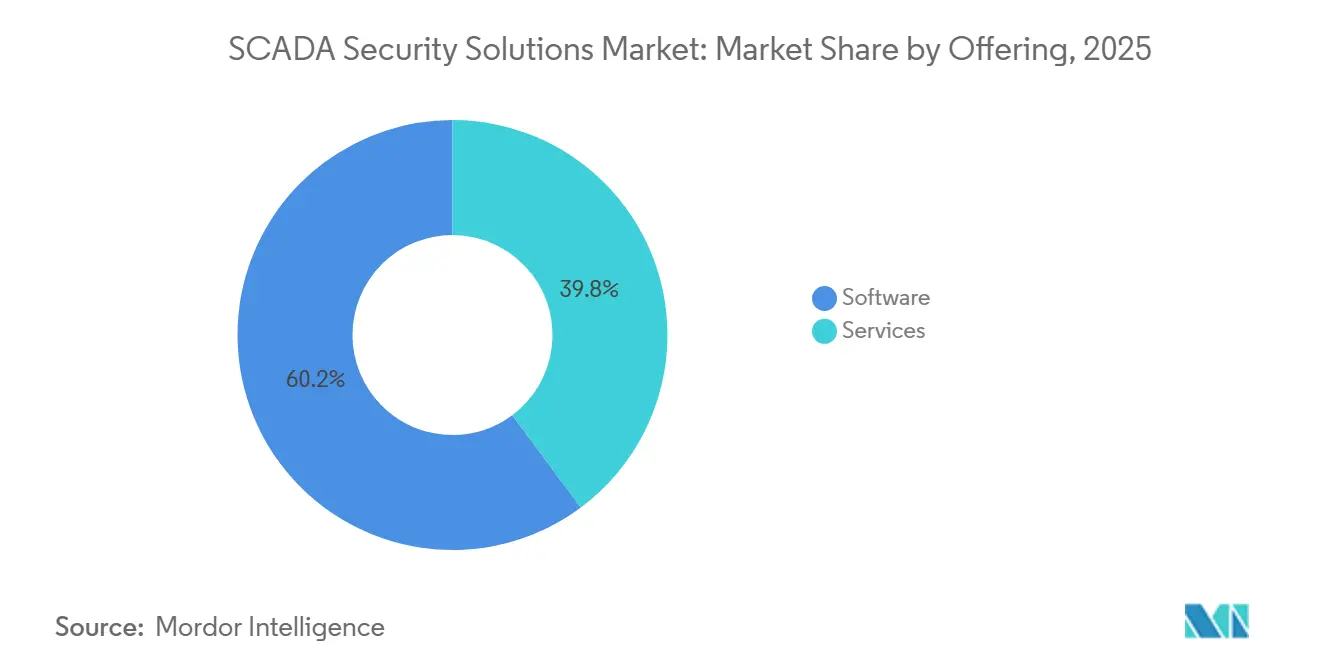

- By offering, software held 60.18% share of the SCADA Security Solutions Market in 2025, while services are projected to expand at an 18.61% CAGR through 2031.

- By security type, network security held 27.12% share in 2025, while monitoring and threat detection is projected to record the fastest CAGR of 18.72% through 2031.

- By deployment, cloud held 53.14% share in 2025, while hybrid deployment is projected to grow at an 18.83% CAGR through 2031.

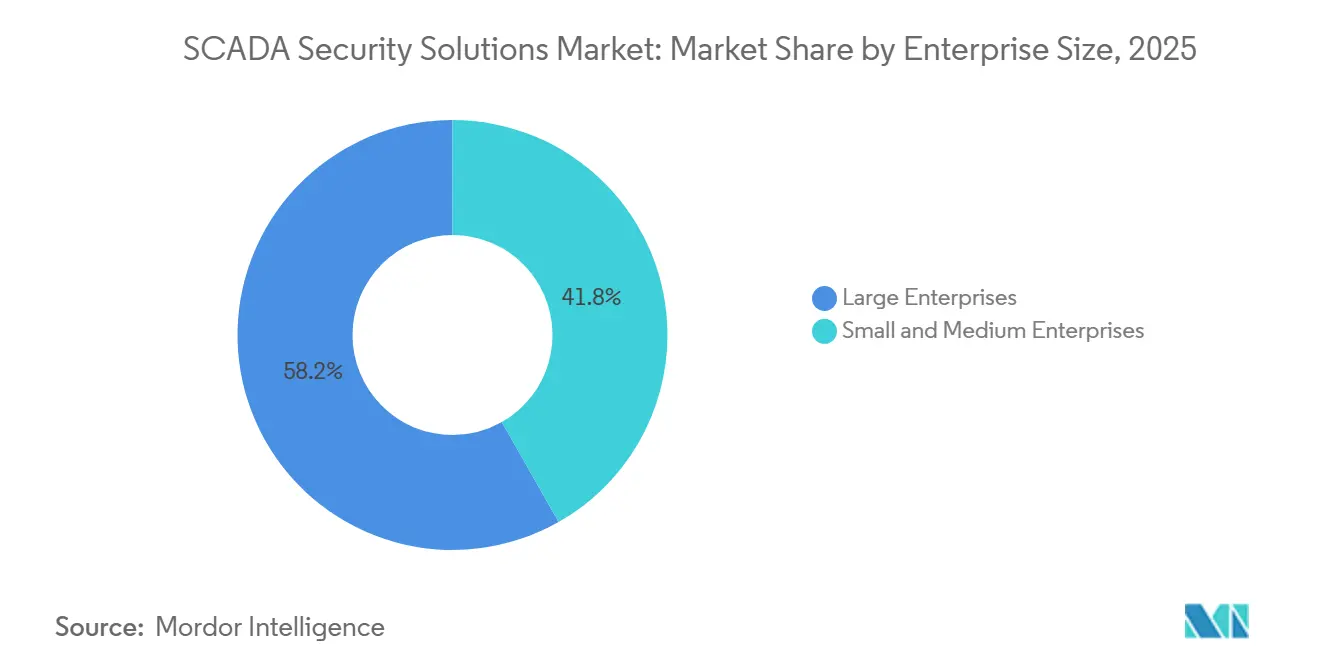

- By enterprise size, large enterprises held 58.21% share of the SCADA Security Solutions Market in 2025, while small and medium enterprises are projected to expand at an 18.94% CAGR through 2031.

- By end-user industry, BFSI held 16.17% share in 2025, while healthcare and life sciences are projected to grow at a 19.05% CAGR through 2031.

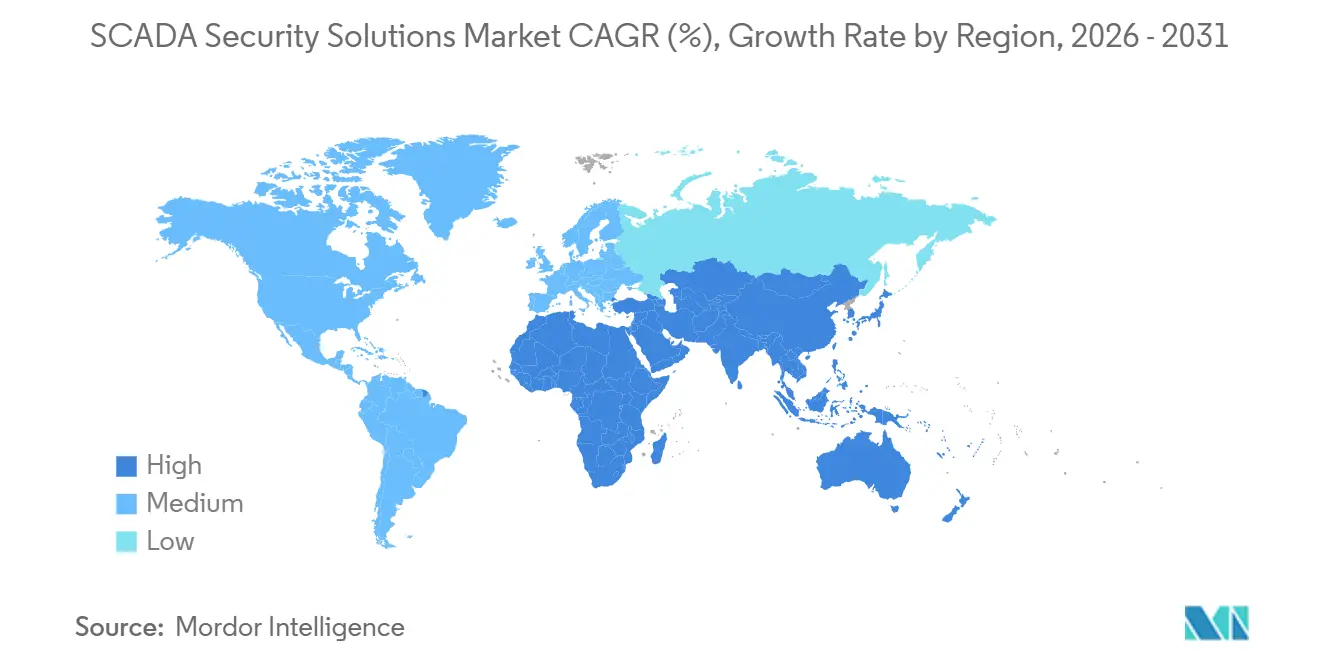

- By geography, North America held 31.16% share of the SCADA Security Solutions Market in 2025, while Asia-Pacific is projected to expand at a 19.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SCADA Security Solutions Market Trends and Insights

Rising Ransomware and Cyber-Physical Threats Targeting SCADA Environments

Attack activity against supervisory control systems rose sharply in 2025 and remained elevated in 2026, keeping the SCADA Security Solutions Market under direct threat. Dragos tracked 119 ransomware groups that affected more than 3,300 industrial organizations globally in 2025, up from 80 groups in 2024.[1]Dragos, “Dragos 2026 OT Cybersecurity Year in Review,” Dragos, dragos.com In Q1 2026, 1,020 ransomware incidents affected industrial organizations worldwide, with manufacturing accounting for 62% of those cases. Attack patterns also changed, as 77% of 2025 intrusions involved suspected data theft, and 43% targeted virtualization infrastructure that hosted SCADA software and historian servers. Dragos also described state-aligned activity focused on industrial HMIs, variable-frequency drives, and remote gateways, indicating that some attackers are mapping control loops rather than merely encrypting files. This higher-consequence profile is pushing operators to treat OT protection as an operating requirement, not a discretionary security upgrade, and that shift continues to support the SCADA Security Solutions Market.

Mandatory OT Cybersecurity Compliance Across Critical Infrastructure

Compliance mandates have turned many OT security purchases into planned and recurring programs, which gives the SCADA Security Solutions Market a steadier demand base. On March 24, 2026, FERC approved Order No. 919 and updated NERC CIP Reliability Standards, extending cybersecurity obligations to virtualized OT environments and low-impact Bulk Electric System Cyber Systems.[2]Federal Energy Regulatory Commission, “Order No. 919, Approval of Modified NERC CIP Reliability Standards for Virtualization,” Federal Register, govinfo.gov FERC also approved CIP-003-11 on the same date, which formalized updated security management controls across covered entities. These standards covered nearly 1,673 U.S. entities and took effect on May 26, 2026, which widened the pool of operators that need documented security controls and audit-ready evidence. Across North America and parts of Europe, operators are increasingly seeking unified platforms that can monitor OT activity, support reporting, and reduce the burden of managing multiple rule sets through separate tools. That mix of legal obligation and operational accountability keeps procurement moving even when internal approval cycles slow, which supports long-range expansion in the SCADA Security Solutions Market.

IT-OT Convergence Expanding the Attack Surface

The old assumption that SCADA environments were protected by isolation no longer holds, and that change is widening the attack surface across the SCADA Security Solutions Market. Dragos reported that organizations often classify compromises involving Windows servers or VMware systems that host SCADA software as IT incidents, even when the operational risk sits directly inside OT environments. In April 2026, the FBI, CISA, NSA, EPA, and DOE confirmed that Iranian-affiliated actors had targeted internet-facing PLCs at U.S. water, wastewater, and energy facilities, extracted SCADA project files, and falsified HMI display data at victim sites.[3]Cybersecurity and Infrastructure Security Agency, “Alert AA26-097A, Iranian-Affiliated Actors Target PLCs Across US Critical Infrastructure,” CISA, cisa.gov Every new IIoT gateway, cloud historian, remote access tool, and cross-site data connection creates another route for lateral movement, which makes basic network visibility alone less sufficient than before. That shift is increasing demand for security tools that connect IT and OT events into a single view, enabling operators to detect suspicious behavior sooner. As a result, the SCADA Security Solutions Market is moving toward platforms that combine context, correlation, and response support, rather than relying on narrow perimeter controls.

Remote Operations and Cloud-Connected Industrial Asset Growth

Remote monitoring and cloud-connected control environments are expanding the number of industrial assets that require constant protection, adding another layer of support to the SCADA Security Solutions Market. Cloud deployment accounted for 53.14% of the market in 2025, indicating that many operators preferred centralized monitoring and subscription-based delivery over hardware-heavy models. Japan’s Ministry of Economy, Trade, and Industry published supply chain security guidelines for power control systems in June 2025 that directly addressed remote connectivity, lifecycle management, and security specifications for SCADA-connected equipment. Hybrid deployment is projected to grow at an 18.83% CAGR through 2031 because it lets operators keep fast local response on site while moving correlation, reporting, and cross-site visibility into the cloud. This balance matters in live operating environments where local control cannot depend on wide-area network availability. It also supports the SCADA Security Solutions Market by boosting demand for managed services, as operators without resident OT specialists can still maintain continuous protection through provider-managed platforms.[4]Ministry of Economy, Trade and Industry, “Publication of the Power Control System Supply Chain Security Guidelines,” Government of Japan, meti.go.jp

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit Cost and Downtime Risk in Legacy SCADA Installations | -2.5% | Global | Medium term (2-4 years) |

| Shortage of OT-Specialized Cybersecurity Talent | -1.9% | Global | Long term (≥ 4 years) |

| Interoperability Gaps Across Proprietary Industrial Protocols | -1.4% | Global | Long term (≥ 4 years) |

| Security Fatigue and Procurement Delays in Multi-Tool OT Stacks | -1.0% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Cost and Downtime Risk in Legacy SCADA Installations

Legacy environments remain a major drag on adoption because many operators still run SCADA systems that were not designed with built-in security controls, and this slows the SCADA Security Solutions Market. These sites often rely on older operating systems and unencrypted protocols such as Modbus and DNP3, making upgrades difficult to stage without interrupting production. The SANS 2025 State of ICS Security Report identified integration complexity in legacy OT environments as a leading operational challenge across industrial organizations. A 2025 study by VDMA and Fraunhofer AISEC found that 88% of German industrial companies handled OT security entirely with internal teams, suggesting limited external specialist support during retrofit work. In continuous-process settings, a short unplanned outage during a security change can cost more than a full year of platform licensing, which encourages delay even when the risk is well understood. That cost and downtime sensitivity keeps adoption uneven across the lower end of the SCADA Security Solutions Market.

Shortage of OT-Specialized Cybersecurity Talent

The shortage of people who understand both industrial operations and cybersecurity is another structural constraint on the SCADA Security Solutions Market. OT protection requires familiarity with protocols such as Modbus, PROFINET, DNP3, and IEC 61850, as well as with the process engineering and safety implications that are not covered in standard IT security training. Dragos addressed this gap in June 2026 when it launched EmberAI as a force multiplier for analysts working across industrial environments. Honeywell reported in June 2026 that only 20% of organizations with industrial environments maintained dedicated OT security teams, underscoring the breadth of the capability gap. This shortage also slows managed service expansion, because providers must hire and retain scarce experts before they can scale delivery. The result is longer implementation lead times, higher labor costs, and slower revenue conversion in parts of the SCADA Security Solutions Market that depend on external support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads as Services Revenue Scales Rapidly

Software accounted for 60.18% of the SCADA Security Solutions Market in 2025, making it the leading offering. This position reflects strong demand for network intrusion detection and prevention systems, OT asset visibility platforms, SIEM tools, identity and access management solutions, and threat detection applications. Operators also favor centrally managed software because vendors can update models, signatures, and analytics remotely without dispatching teams to industrial sites. In practice, industrial firewall tools and OT asset visibility products often serve as the first layers of an OT security program, helping software remain central in new deployments and refresh cycles. Rockwell Automation’s IEC 62443-4-1 Maturity Level 4 certification for SecureOT also demonstrates how vendors are packaging software around secure development and compliance-readiness.

Services are projected to grow at a 18.61% CAGR from 2026 to 2031, making them the fastest-growing offering in the SCADA Security Solutions Market. This growth reflects a simple reality: many operators do not have enough OT security staff to run continuous monitoring, incident response, and tuning on their own. Managed detection and response contracts also generate recurring revenue and stronger renewal rates, gradually changing commercial models across the SCADA Security Solutions industry. The service layer has become especially important for mid-sized operators that want enterprise-grade monitoring without building internal OT security operations centers. Dragos signaled this broader service direction in 2026 through the planned integration of runZero and NetRise into its portfolio, which added exposure assessment and firmware-level device visibility. As service bundles expand, vendors in the SCADA Security Solutions Market are competing less on a single product and more on their ability to manage the full operating risk associated with that product.

By Security Type: Network Defense Anchors a Broadening Protection Stack

Network security accounted for 27.12% of the SCADA Security Solutions Market share in 2025, serving as the base layer of the broader defense stack. This category remains essential because visibility into industrial traffic, segmentation, and policy enforcement still determines how quickly operators can isolate suspicious activity. Network controls also sit closest to many legacy devices that cannot host endpoint agents, which gives them a durable role even as other security layers mature. For many operators, the first serious security program still begins with firewalling, traffic inspection, and network asset discovery. That core role means network security continues to anchor the deal structure, even as the discussion later expands to include response automation, identity controls, and device hardening.

Monitoring and threat detection are projected to grow at a 18.72% CAGR through 2031, as the SCADA Security Solutions Market shifts toward detection-led architectures that assume some attackers will get in. Claroty launched Claire in May 2026 as a CPS-native AI security agent that automates segmentation drift detection, baseline analysis, and SIEM or SOAR orchestration across more than 100 integrations. Nozomi Networks also launched Vantage IQ in January 2026 as a private AI assistant trained on an organization’s own OT and IoT asset, vulnerability, and threat data. Endpoint and asset protection is also gaining weight as engineering workstations, HMIs, and removable media continue to appear in incident pathways, and Honeywell added Secure Media Exchange to address that exact exposure. Siemens and Palo Alto Networks also introduced an IEC 62443-verified AI-driven cybersecurity architecture for industrial private 5G in March 2026, which shows that application security, identity, and monitoring are increasingly being designed together. That broadening stack is raising the technical standard across the SCADA Security Solutions Market and making single-purpose tools less persuasive than before.

By Deployment: Cloud Leads as Hybrid Becomes the Architecture of Choice

Cloud deployment accounted for 53.14% of the SCADA Security Solutions Market in 2025, giving it the largest share. Operators favored cloud models because centralized dashboards make it easier to monitor geographically distributed sites without installing large amounts of hardware at each location. Cloud delivery also supports continuous vendor updates, which helps organizations keep threat intelligence and detection content current without frequent site visits. This model aligns well with subscription pricing and managed services, lowering the entry barrier for operators seeking faster deployment and simpler operations. Even so, on-premises deployment retained an important place in nuclear, defense, and government-critical settings where data residency rules and control sensitivity still limit external connectivity.

Hybrid deployment is projected to expand at a 18.83% CAGR from 2026 to 2031, as it addresses the practical limitations of fully centralized control in industrial environments. In hybrid designs, on-site sensors handle deterministic local anomaly detection and immediate response, while cloud layers support cross-site correlation, audit reporting, and trend analysis. This pattern is becoming more common across the SCADA Security Solutions industry because it keeps local control independent of network availability while still giving operators modern analytics. NTT Communications and IIJ reinforced this direction in September 2025 when they launched an integrated OT intrusion detection and secure remote access solution with hybrid deployment features for Japan and planned ASEAN expansion in 2026. The persistence of wide-area connectivity risk means local control components will remain essential even as cloud adoption rises, which is why hybrid is becoming the preferred design path in the SCADA Security Solutions Market. Vendors that can support both local resilience and centralized visibility are therefore in a stronger position as deployment choices become more mixed.

By Enterprise Size: Large Enterprises Lead While SMEs Accelerate

Large enterprises held 58.21% of the market in 2025, making them the largest customer segment in the SCADA Security Solutions Market. Their lead reflects large multi-site SCADA estates, more complex vendor mixes, deeper compliance obligations, and the higher contract values that come with those factors. These organizations often run centralized OT security operations models, sign multi-year platform agreements, and add consulting or response retainers to improve execution. They also face strong pressure to standardize policies and telemetry across plants, utilities, campuses, and infrastructure sites that operate under different local conditions. Honeywell’s June 2026 launch of a managed OT Security Operations Center with 24-7 monitoring, incident response, and a vendor-agnostic integration hub demonstrates how suppliers are targeting large, complex environments.

Small and medium enterprises are projected to grow at a 18.94% CAGR through 2031, making them the fastest-growing customer tier in the SCADA Security Solutions Market. The shift reflects lower entry costs from SaaS monitoring, bundled remote access, and managed services, which spread spending across subscriptions rather than large up-front projects. Supply chain pressure is also changing buyer behavior, because larger industrial customers increasingly expect suppliers and integrators to show measurable OT security maturity before contracts are renewed or expanded. Claroty’s 2025 global CPS security report highlighted how economic pressure and operational risk are driving more organizations to formalize security even as budgets remain tight. The SANS 2025 ICS security report also showed that asset visibility, detection, and secure remote access remain top investment priorities across operator sizes, indicating that SME demand is increasingly aligned with large-enterprise priorities. This mix of broader access and external pressure is widening the addressable market for SCADA Security Solutions, even though the revenue center still sits with larger operators.

By End-user Industry: BFSI Leads but Healthcare and Life Sciences Grows Fastest

BFSI accounted for 16.17% of the SCADA Security Solutions Market in 2025, making it the largest end-user segment. Its position stems from the role of SCADA-linked infrastructure in ATM networks, data center power management, and secure payment processing environments, where downtime quickly translates into financial and reputational losses. These systems may not look like traditional factory control networks, but their operational dependence on monitored assets and uninterrupted service creates a strong case for OT-style security controls. The sector also tends to move earlier on monitoring, access control, and resilience planning because business continuity requirements are tightly linked to trust and service delivery. That keeps BFSI a key segment of the SCADA Security Solutions Market, even as other sectors expand more quickly.

Healthcare and life sciences are projected to grow at a 19.05% CAGR through 2031, making them the fastest-growing end-user segment in the SCADA Security Solutions Market. RunSafe Security’s 2025 Medical Device Cybersecurity Index found that 35% of healthcare executives identified OT systems as their biggest cybersecurity concern and that 75% had increased medical device and OT security budgets over the prior 12 months. Claroty’s 2025 Healthcare Exposures report found that 78% of hospital organizations had OT assets with Known Exploited Vulnerabilities, and that 65% of those assets were also internet-connected in ways that did not follow security best practices. Hospital building management systems, pharmaceutical cold-chain refrigeration, and medical gas distribution all raise the stakes, as operational failures can directly affect patient care. Information technology and telecom, industrial manufacturing, retail and e-commerce, and government also remain important, as each has a large control footprint or distinct threat pattern that drives demand across the SCADA Security Solutions Market. Manufacturing is especially exposed given its concentration in industrial ransomware activity, while government buyers focus more heavily on identity controls and continuous monitoring to manage disruptive threats.

Geography Analysis

North America accounted for 31.16% of the SCADA Security Solutions Market share in 2025, making it the largest regional contributor. This lead reflects the high concentration of regulated critical infrastructure operators and the mature procurement cycles that already support multi-year OT security spending. In March 2026, FERC approved updated NERC CIP standards, including CIP-003-11, which extended formal cybersecurity obligations to virtualized OT environments and low-impact Bulk Electric System Cyber Systems. In April 2026, U.S. agencies confirmed that Iranian-affiliated actors had compromised internet-exposed PLCs at water, wastewater, and energy facilities, extracted project files, and falsified HMI values, which reinforced urgency across the utility base. Canada’s National Cyber Threat Assessment 2025-2026 also warned of persistent threats to internet-connected OT systems within critical infrastructure. South America remained at an earlier stage, but Brazil’s industrial automation growth and Argentina’s energy modernization efforts are creating initial demand for cloud-based monitoring and managed support that can work without large in-country specialist teams.

Europe shows a compliance-driven demand pattern in the SCADA Security Solutions Market, with the highest near-term urgency in Germany, France, and the United Kingdom. Procurement in the region is being shaped by the need to align OT controls with essential service obligations, product security expectations, and audit-readiness across multiple operating environments. Industrial buyers are increasingly standardizing on IEC 62443-aligned architectures to reduce certification friction and make vendor evaluation more consistent. This favors vendors that can combine protocol visibility, documentation support, policy enforcement, and lifecycle governance in a single operating model. The SCADA Security Solutions Market in Europe is therefore advancing through compliance-led replacement cycles rather than one-time emergency buying.

Asia-Pacific is projected to expand at a 19.16% CAGR from 2026 to 2031, which makes it the fastest-growing region in the SCADA Security Solutions Market. Japan’s Ministry of Economy, Trade, and Industry published power control system supply chain security guidelines in June 2025, which raised the focus on lifecycle management and security verification for SCADA-connected equipment. NTT Communications and IIJ also launched an integrated OT security management solution in September 2025, with Japan availability first and ASEAN expansion planned for 2026, which shows regional vendors are building for broader demand. India is creating greenfield opportunities through industrial digitalization, while the Middle East and Africa are gaining momentum through infrastructure and utility modernization in Saudi Arabia, the United Arab Emirates, Nigeria, and South Africa, all of which broaden the future base of the SCADA Security Solutions Market.

Competitive Landscape

The SCADA Security Solutions Market is split into two broad competitive groups that approach customers from different starting points. OT-native specialists such as Dragos, Claroty, Radiflow, and Waterfall Security Solutions compete on threat intelligence depth, protocol-level visibility, and incident response expertise tailored to industrial environments. Industrial automation OEMs such as Honeywell, Siemens, Schneider Electric, and Rockwell Automation compete through installed-base relationships and embedded security tied to broader control platforms. That difference matters because specialists often lead with threat context, while OEMs often lead with operational familiarity, lifecycle service, and long-standing engineering access. The SCADA Security Solutions Market, therefore, rewards vendors that can show both industrial credibility and measurable security outcomes.

Competitive boundaries are also widening as major vendors expand beyond their original product categories in the SCADA Security Solutions Market. Dragos broadened its platform scope in 2026 through the planned integration of runZero and NetRise, which added exposure assessment and firmware-level software supply chain visibility to its managed services. Honeywell expanded its OT Cybersecurity Suite in June 2026 with secure media scanning, AI monitoring, governance automation, a data diode, and a managed OT Security Operations Center, which shows how OEMs are moving further into active cyber operations. Rockwell Automation also expanded SecureOT in June 2026 with assessment tools, managed services, and managed secure remote access, indicating the same shift toward recurring service models. These moves show that vendors in the SCADA Security Solutions Market are trying to capture a wider share of the customer’s operating risk instead of only selling stand-alone software or hardware.

AI has become one of the clearest differentiators in the SCADA Security Solutions Market's monitoring segment. Dragos launched EmberAI in June 2026, Nozomi Networks launched Vantage IQ in January 2026, and Claroty launched Claire in May 2026, all within a short window that highlights how quickly OT-specific AI is becoming a standard expectation. Siemens and Palo Alto Networks added another competitive signal in March 2026 when they introduced an IEC 62443-verified AI-driven cybersecurity architecture for industrial private 5G networks. Even with those larger moves, white-space opportunities remain in hybrid managed services for mid-market operators, where regional compliance knowledge and delivery capabilities still create room for newer providers across the SCADA Security Solutions Market.

SCADA Security Solutions Industry Leaders

Siemens AG

Schneider Electric SE

Honeywell International Inc.

Cisco Systems, Inc.

Fortinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Dragos launched EmberAI, an OT-native AI assistant built on the Dragos Intelligence Fabric, which processes over 5 petabytes of daily OT telemetry accumulated across a decade of industrial incident response. EmberAI enabled analysts to query industrial threat intelligence in plain language, mapped detections to known adversary groups, and accelerated alert triage and incident reporting, addressing the structural shortage of OT-specialized security professionals in critical infrastructure environments.

- June 2026: Rockwell Automation expanded its SecureOT portfolio with 3 new offerings, an OT Cybersecurity Assessment Suite, SecureOT Platform Managed Services, and Managed Secure Remote Access. The expansion was backed by the company’s IEC 62443-4-1 Maturity Level 4 certification, the highest level for secure product development lifecycle, and reflected a strategic shift toward subscription-based OT risk management services for manufacturers seeking end-to-end resilience.

- June 2026: Honeywell expanded its OT Cybersecurity Suite with 5 new capabilities, including Secure Media Exchange removable-media scanning, Cyber Proactive Defense AI monitoring, Cyber Governance Risk and Compliance automation, a Data Diode for unidirectional data transfer, and a managed OT Security Operations Center with 24-7 network and endpoint monitoring. The expansion addressed Honeywell’s finding that only 32% of organizations with industrial environments actively monitored OT systems.

- May 2026: Claroty launched Claire, the first CPS-native AI security agent, powered by a large language model trained on over a decade of OT and IoT data from the world’s largest CPS data lake. Claire automated segmentation drift detection, behavioral baseline analysis, and SIEM or SOAR ticket orchestration across more than 100 integrations, and was deployed by more than 1,300 customers including 24 of the Fortune 100.

Global SCADA Security Solutions Market Report Scope

The SCADA Security Solutions market refers to platforms and services designed to protect Supervisory Control and Data Acquisition (SCADA) systems and industrial control environments from cyber threats, unauthorized access, and operational disruptions. These solutions include intrusion detection, industrial firewalls, SIEM systems, OT asset monitoring, identity and access management, and advanced threat detection platforms tailored for critical infrastructure.

The SCADA Security Solutions market report is segmented by Offering (Software {Network Intrusion Detection and Prevention, Industrial Firewall Solutions, Security Information and Event Management (SIEM), OT Asset Visibility and Monitoring, Identity and Access Management, Threat Detection and Response Platforms], and Services), Security Type (Network Security, Endpoint and Asset Security, Application Security, Identity and Access Security, Monitoring and Threat Detection), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Network Intrusion Detection and Prevention |

| Industrial Firewall Solutions | |

| Security Information and Event Management (SIEM) | |

| OT Asset Visibility and Monitoring | |

| Identity and Access Management | |

| Threat Detection and Response Platforms | |

| Services |

| Network Security |

| Endpoint and Asset Security |

| Application Security |

| Identity and Access Security |

| Monitoring and Threat Detection |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Software | Network Intrusion Detection and Prevention | |

| Industrial Firewall Solutions | |||

| Security Information and Event Management (SIEM) | |||

| OT Asset Visibility and Monitoring | |||

| Identity and Access Management | |||

| Threat Detection and Response Platforms | |||

| Services | |||

| By Security Type | Network Security | ||

| Endpoint and Asset Security | |||

| Application Security | |||

| Identity and Access Security | |||

| Monitoring and Threat Detection | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the SCADA Security Solutions Market?

The SCADA Security Solutions Market was valued at USD 4.52 billion in 2025 and is projected to reach USD 11.55 billion by 2031 at a 17.44% CAGR during 2026-2031.

Which factor is pushing OT security budgets the fastest in SCADA environments?

The sharp rise in ransomware and cyber-physical activity is a major trigger, especially as attackers now target control loops and operational continuity rather than only data.

Which deployment model leads today and which one is growing the fastest?

Cloud led with 53.14% share in 2025, while hybrid deployment is projected to grow the fastest at an 18.83% CAGR through 2031.

Why are services growing faster than software in this space?

Services are projected to grow at an 18.61% CAGR because many operators lack in-house OT cybersecurity talent and prefer managed monitoring, detection, and response.

Which customer group is expanding the fastest by enterprise size?

Small and medium enterprises are projected to expand at an 18.94% CAGR, helped by subscription models, managed services, and supply chain pressure from larger buyers.

Which vertical and region show the highest growth through 2031?

Healthcare and life sciences is projected to grow at 19.05% CAGR among end users, while Asia-Pacific is projected to grow at 19.16% CAGR among regions.

Page last updated on: