Security Operation Center As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

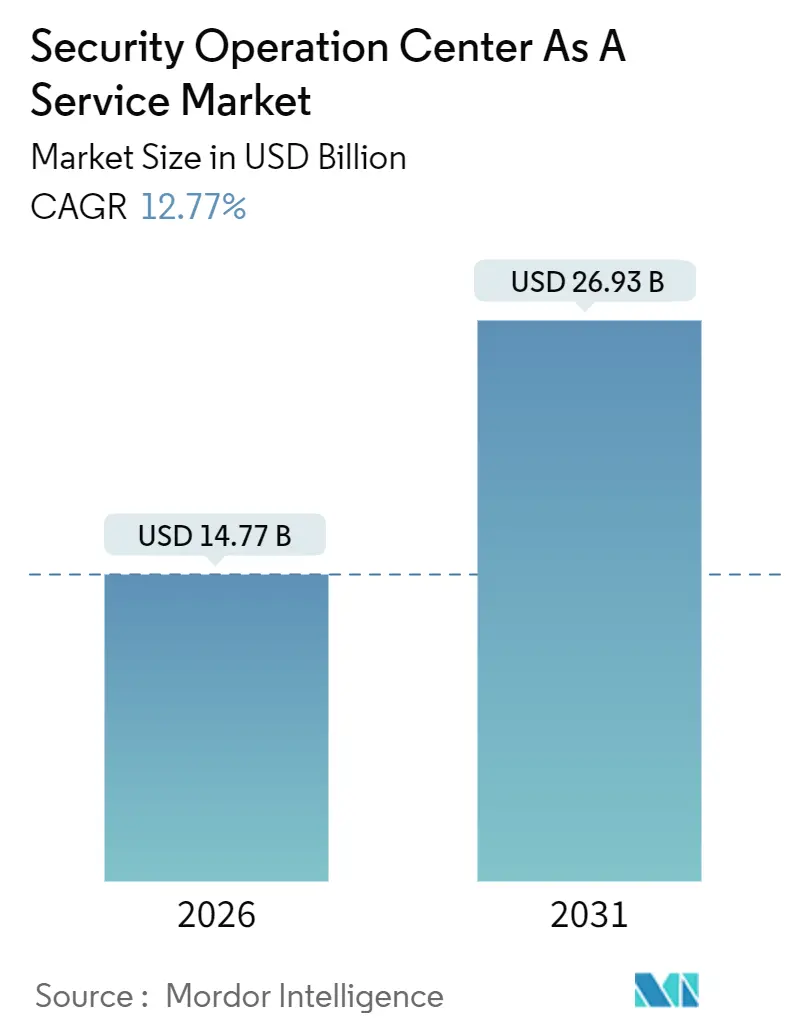

| Market Size (2026) | USD 14.77 Billion |

| Market Size (2031) | USD 26.93 Billion |

| Growth Rate (2026 - 2031) | 12.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Operation Center As A Service Market Analysis by Mordor Intelligence

The security operation center as a service market was valued at USD 14.77 billion in 2026 and is projected to reach USD 26.93 billion by 2031, advancing at a 12.77% CAGR over the forecast period. Driven by rising regulatory scrutiny, tightening cyber-insurance underwriting, and the scarcity of qualified analysts, buyers are shifting from capital-intensive, on-premises security information and event management platforms to outcome-based managed detection and response subscriptions. Enterprises also favor cloud-delivered analytics that uncover multi-vector ransomware, supply-chain, and credential-theft activity that evades signature tools. Demand is amplified by the convergence of operational technology and Internet of Things environments, which broadens the attack surface and requires unified visibility. Competitive dynamics remain fluid as telecommunications carriers, regional specialists, and artificial-intelligence-driven disruptors challenge incumbent managed security service providers.

Key Report Takeaways

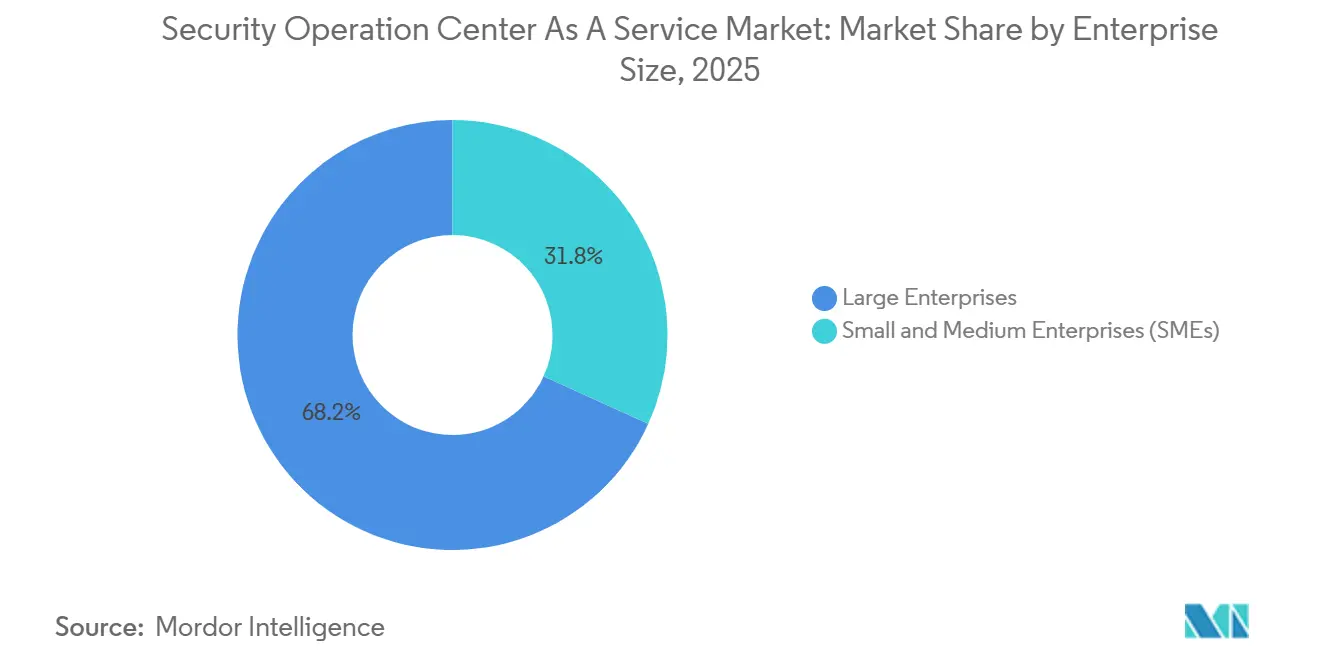

- By enterprise size, large organizations commanded 68.23% revenue share in 2025, whereas small and medium enterprises are expanding at a 13.84% CAGR to 2031.

- By service type, managed detection and response led with 41.52% of security operation center as a service market share in 2025, while incident response and threat hunting is advancing at a 13.19% CAGR through 2031.

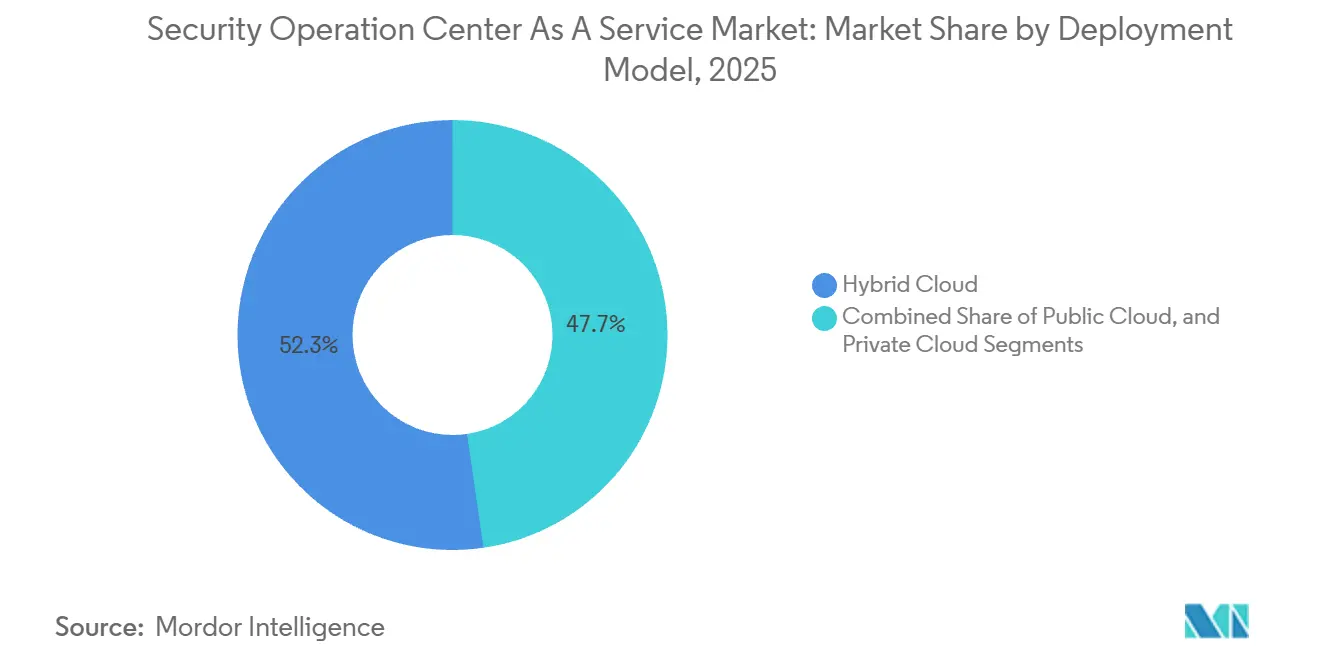

- By deployment model, hybrid cloud accounted for 52.31% of security operation center as a service market size in 2025 and is forecast to post a 14.28% CAGR to 2031.

- By end-user industry, banking, financial services, and insurance held 29.63% of 2025 revenue, whereas healthcare and life sciences is projected to grow at a 14.36% CAGR to 2031.

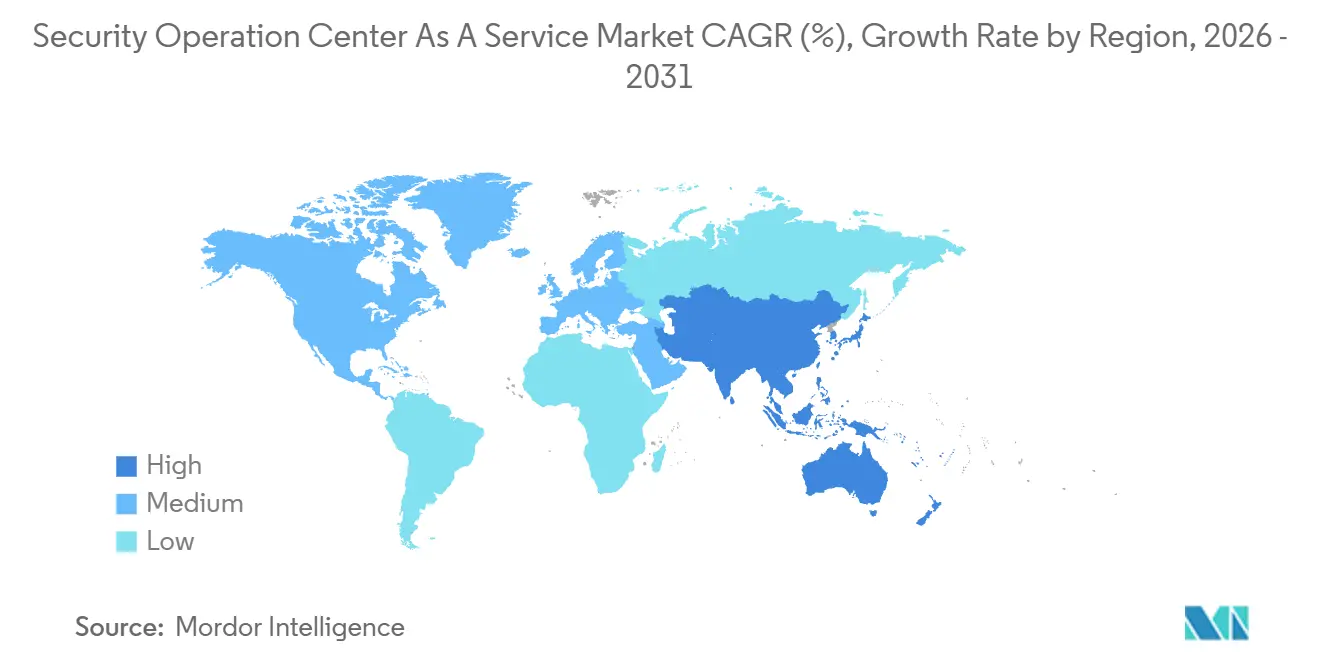

- By geography, North America captured 43.81% of 2025 revenue, while Asia Pacific is set to register the fastest 15.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Security Operation Center As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential Rise in Multi-Vector Cyber-Attacks | +2.8% | Global, with acute concentration in North America and Europe | Short term (≤ 2 years) |

| Escalating Cybersecurity-Talent Shortage | +2.4% | Global, most severe in North America, Western Europe, and Asia Pacific technology hubs | Medium term (2-4 years) |

| Expanding Cloud and Hybrid IT Attack Surface | +2.1% | Global, led by North America and Asia Pacific cloud-adoption leaders | Medium term (2-4 years) |

| Regulatory Push for Real-Time Incident Disclosure | +1.9% | North America (SEC), Europe (NIS2), Asia Pacific (emerging frameworks) | Short term (≤ 2 years) |

| Cyber-Insurance Mandates for 24/7 MDR | +1.7% | North America and Europe, with spillover to Australia and Singapore | Medium term (2-4 years) |

| OT and IoT Convergence Demanding Unified Visibility | +1.5% | Global, with early gains in manufacturing-intensive regions such as Germany, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exponential Rise in Multi-Vector Cyber-Attacks

Threat actors now chain ransomware, data exfiltration, and denial-of-service extortion in rapid succession, overwhelming in-house teams that still rely on periodic log reviews. The Federal Bureau of Investigation recorded USD 12.5 billion in cyber-crime losses during 2023, a 22% surge driven by ransomware and business email compromise.[1]Federal Bureau of Investigation, “Internet Crime Report 2023,” IC3.GOV In 2024, the Cybersecurity and Infrastructure Security Agency observed a 30% uptick in incidents involving initial-access brokers that shorten dwell time to fewer than 24 hours. This acceleration favors managed detection and response providers that maintain global analyst benches and behavioral analytics capable of identifying lateral movement within minutes. Organizations that once tolerated weekly reviews now demand sub-hour mean time to detect, creating dependencies on outsourced experts. The shift from perimeter defense to assume-breach postures further boosts incident-response retainer sales bundled with continuous monitoring.

Escalating Cybersecurity-Talent Shortage

The worldwide security workforce gap reached 4 million positions in 2024, including 700,000 vacancies in North America alone. Salary inflation for tier-one analysts topped 15% year-over-year, yet turnover remained higher than 25%, eroding institutional knowledge and expanding alert backlogs. Small and medium enterprises struggle most to match compensation levels offered by large technology and financial players, prompting them to adopt subscription-based security operation center as a service market offerings that spread analyst costs across hundreds of clients. Providers achieve economies of scale to fund advanced automation and threat-intelligence platforms that individual enterprises cannot justify. The shortage is particularly acute in cloud-native disciplines such as Kubernetes runtime protection, further solidifying the outsourcing trend.

Expanding Cloud and Hybrid IT Attack Surface

Public-cloud adoption has fragmented visibility, as traditional on-premises tooling rarely ingests audit logs from infrastructure-as-a-service, platform-as-a-service, or software-as-a-service environments. A breach of a widely used file-transfer application in 2023 impacted over 2,000 organizations, underscoring the concentration risk within shared-responsibility models. Hybrid deployments multiply complexity by adding proprietary log formats from on-premises active directory, network devices, and software-defined wide-area networks. Managed detection and response vendors fill this gap with lightweight agents that normalize telemetry into unified data lakes, enabling cross-domain threat hunting. As enterprises move to multi-cloud strategies to avoid vendor lock-in, vendor-agnostic platforms that accommodate Amazon Web Services, Microsoft Azure, and Google Cloud logs gain prominence.

Regulatory Push for Real-Time Incident Disclosure

The United States Securities and Exchange Commission’s 2023 rule obliges registrants to report material incidents within four business days. In the European Union, the Network and Information Security Directive 2 requires essential and important entities to alert national authorities within 24 hours. Singapore and Australia have enacted similar mandates. These compressed timelines force enterprises to maintain continuous monitoring, automated evidence collection, and rapid forensic analysis capabilities more readily delivered through the security operation center as a service market than through overstretched internal teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Sovereignty and Log-Residency Concerns | -1.2% | Europe (GDPR), Asia Pacific (China, India, Indonesia), Middle East | Medium term (2-4 years) |

| Integration Complexity With Legacy Tooling | -0.9% | Global, particularly acute in large enterprises with decades-old infrastructure | Short term (≤ 2 years) |

| Limited Organization-Specific Context in Outsourced SOC | -0.7% | Global, affecting mid-market and enterprise buyers with unique environments | Medium term (2-4 years) |

| Alert-Fatigue From High False-Positive Rates | -0.6% | Global, with higher impact in resource-constrained small and medium enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Log-Residency Concerns

General Data Protection Regulation restrictions on personal-data transfer compel providers to operate in-region security operations centers or adopt standard contractual clauses, adding cost and complexity.[2]European Union, “Directive (EU) 2022/2555 on Measures for a High Common Level of Cybersecurity Across the Union,” EUR-LEX.EUROPA.EU India’s Digital Personal Data Protection Act introduces similar requirements, spurring investments in domestic facilities. China’s Cybersecurity Law prevents overseas export of critical information infrastructure logs, effectively reserving that portion of demand for local champions. The resulting fragmentation hampers global providers’ economies of scale, yet gives regional specialists a home-field advantage.

Integration Complexity With Legacy Tooling

Enterprises often run decades-old firewalls, intrusion-prevention systems, and proprietary industrial-control-system protocols that lack modern application programming interfaces. Custom parsers are needed before telemetry can feed cloud-native analytics engines, delaying benefit realization and inflating professional-services costs. A SANS Institute survey found that 60% of organizations cited integration hurdles as the top impediment to managed detection and response adoption. The burden is heavier in highly segmented networks across healthcare and finance, where approval chains slow onboarding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: Consumption Economics Accelerate Small-Firm Uptake

The large-enterprise tier accounted for 68.23% of 2025 revenue in the security operation center as a service market, reflecting the breadth of hybrid estates and stringent audit obligations. These buyers often keep tier-three threat hunting and in-house intelligence but outsource tier-one triage and tier-two investigation, retaining institutional context while gaining 24/7 coverage. The security operations center-as-a-service market for small and medium enterprises is growing faster, advancing at a 13.84% CAGR, because turnkey cloud subscriptions eliminate capital expenditure and scale with headcount growth. Programmatic channel sales by managed service providers further lower acquisition costs and make advanced detection affordable.

Small companies typically adopt standardized playbooks that bundle endpoint detection, security awareness training, and vulnerability scanning, while large organizations demand bespoke runbooks and sector-specific intelligence. As chief information security officers face persistent hiring gaps, even Fortune 500 firms are increasing the portion of alerts routed to external analysts. For smaller buyers, outsourcing is becoming the only viable path to regulatory compliance and cyber-insurance eligibility.

By Service Type: Proactive Threat Hunting Becomes the Differentiator

Managed detection and response captured 41.52% of security operation center as a service market share in 2025, underpinned by continuous monitoring and guided remediation. Incident response and threat hunting services are projected to post a 13.19% CAGR to 2031, outperforming passive log aggregation as enterprises recognize that adversaries can dwell undetected for weeks without proactive searches. The security operation center as a service market size for proactive hunting remains smaller today but commands premium pricing because it requires senior analysts versed in adversary tactics.

Legacy security monitoring is commoditizing as cloud data lakes decouple storage from analytics, prompting providers to integrate automation that suppresses false positives and focuses analysts on high-fidelity signals. Bundled orchestration capabilities and vulnerability management are also emerging as growth vectors, allowing vendors to consolidate toolsets and justify higher average revenue per customer. The unified approach reduces breach costs and simplifies procurement.

By Deployment Model: Hybrid Cloud Strikes a Compliance-Performance Balance

Hybrid architectures contributed 52.31% of 2025 revenue and are rising at a 14.28% CAGR, the highest among deployment models. Organizations forward summarized telemetry to cloud analytics while retaining raw logs with personally identifiable information on-premises, satisfying both latency and privacy mandates. Edge-processing nodes now execute first-stage analytics at customer sites, slashing bandwidth and egress fees.

Public cloud options appeal to digital natives and smaller firms seeking frictionless onboarding, whereas private cloud serves government and finance buyers that require dedicated infrastructure. The security operation center as a service industry continues to innovate with containerized analytics engines that deploy inside customer environments, extending provider visibility without violating residency laws. This flexibility is a decisive factor for multinational corporations juggling multiple regulatory frameworks.

By End-User Industry: Healthcare Growth Outpaces Long-Time BFSI Leader

The banking, financial services, and insurance segment retained its top position with 29.63% of 2025 revenue, thanks to payment security mandates and incident-reporting obligations. Healthcare, however, is set to log the fastest CAGR of 14.36%, driven by ransomware targeting electronic health records and connected medical devices. A 2024 American Hospital Association study showed a 32% year-over-year rise in attacks on healthcare delivery organizations.

Manufacturing adoption is accelerating as industrial control systems merge with Internet of Things devices, generating telemetry previously invisible to corporate security teams. Government agencies, hampered by staffing freezes, increasingly contract out tier-one and tier-two operations. Retail follows as payment fraud and credential-stuffing attacks pressure margins, making managed detection and response a cost-effective mitigation.

Geography Analysis

North America accounted for 43.81% of 2025 revenue, buoyed by the United States Securities and Exchange Commission’s disclosure rule, mature cyber-insurance markets, and a concentration of Fortune 500 enterprises. The region is witnessing the replacement of legacy on-premises security information and event management platforms with cloud-native managed detection and response solutions that lower the total cost of ownership. Canada’s breach-notification regime further supports demand, while nearshoring activity in Mexico exposes regional hubs to heightened cyber risk.

Europe claimed a roughly 28% share, anchored by the Network and Information Security Directive 2 that compels 24-hour reporting across essential and important entities. Germany, France, and the United Kingdom bolster adoption through national certifications that raise service-quality baselines. Nevertheless, General Data Protection Regulation residency provisions fragment the provider landscape, favoring vendors with in-country security operations centers.

Asia Pacific is projected to expand at a 15.27% CAGR, the fastest worldwide. India’s Digital Personal Data Protection Act requires local storage of security telemetry, prompting global providers to open Mumbai and Bengaluru facilities. Singapore’s six-hour incident-reporting rule for critical information infrastructure, Australia’s Critical Infrastructure Protection Act, and South Korea’s financial-sector guidelines all create compliance-driven demand. China remains dominated by domestic suppliers due to outbound-data restrictions, yet multinational firms often execute parallel contracts for subsidiaries to maintain group-wide visibility.

South America, the Middle East, and Africa contributed nearly 15% of 2025 revenue. Brazil’s central bank cybersecurity resolution and the United Arab Emirates’ managed security licensing scheme have stimulated regional growth. Saudi Arabia’s Essential Cybersecurity Controls compel critical infrastructure to implement 24/7 monitoring, and South Africa’s regulators are enforcing cyber-resilience guidelines despite macroeconomic headwinds.

Competitive Landscape

The top five providers hold an estimated 35-40% combined share, underscoring moderate fragmentation and leaving room for regional specialists and vertical-focused entrants. Incumbents such as SecureWorks, IBM Security, Arctic Wolf, AT&T Cybersecurity, and NTT pursue land-and-expand strategies, offering low-friction entry subscriptions that later upsell threat hunting and orchestration modules. Telecommunications carriers leverage connectivity contracts to cross-sell managed detection and response, bundling services with software-defined wide-area networks to deepen account stickiness.

Private-equity-backed roll-ups continue, acquiring regional managed security firms to gain local analyst talent and satisfy data-residency obligations. Artificial-intelligence-driven newcomers automate tier-one triage, lowering price points for small and medium enterprises and pressuring incumbents to match efficiency gains. Operational technology security remains a white-space opportunity where specialists like Dragos partner with generalist vendors to monitor supervisory control and data acquisition protocols.

Financial disclosures highlight the scale advantage of diversified technology vendors. IBM reported USD 2.8 billion in security-services revenue for 2025, enabling sustained investment in threat research.[3]IBM Corporation, “Form 10-Q for the Quarterly Period Ended September 30 2025,” SEC.GOV.

Security Operation Center As A Service Industry Leaders

SecureWorks Inc.

IBM Corporation

AT&T Inc.

Arctic Wolf Networks, Inc.

Trustwave Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Arctic Wolf acquired a European managed detection and response provider for USD 180 million to establish a Frankfurt security operations center focused on Network and Information Security Directive 2 compliance.

- November 2025: IBM reported 11% year-over-year growth in its Security Services segment, securing new Fortune 100 financial contracts and extending QRadar XDR to operational technology telemetry.

- October 2025: Securonix released a generative-AI threat-hunting assistant that trimmed mean time to detect by 40% during pilot projects.

- September 2025: NTT opened a 150-seat Mumbai security operations center to meet India’s data-localization rules.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Security Operation Center-as-a-Service (SOCaaS) market as subscription-based services that supply round-the-clock threat monitoring, log analytics, incident investigation, and guided response from a cloud-hosted SOC staffed by external analysts. Clients therefore avoid the capital and staffing burden of an internal center.

Scope Exclusion: One-off consulting or audit engagements lacking continuous monitoring or incident response fall outside this scope.

Segmentation Overview

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Service Type

- Managed Detection and Response (MDR)

- Incident Response and Threat Hunting

- Security Monitoring and Log Management

- Other Service Types

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By End-User Industry

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Retail and E-Commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

According to Mordor Intelligence interviews, chief information security officers in banking, telecom, and healthcare, regional managed-detection heads across North America, Europe, and Asia, and procurement leads at mid-market manufacturers clarified alert volumes, contract tenure, and recent price compression. This allowed us to cross-check early model outputs.

Desk Research

We began with tier-1 public sources such as NIST breach statistics, ENISA threat reports, CISA advisories, and World Bank cloud-adoption data, which anchor attack frequency, exposure, and digitalization baselines. Corporate filings, IPO prospectuses, and earnings calls then revealed revenue splits and typical seat pricing for listed managed-security vendors. Our analysts mined D&B Hoovers for private-company financials, pulled SIEM shipment records from Volza, and scanned Dow Jones Factiva for contract awards that show deal size bands. The examples listed are illustrative; many additional records and journals informed validation.

Market-Sizing & Forecasting

A top-down build starts with global cybersecurity spend, isolates the share outsourced to managed SOCs using vendor disclosures and penetration ratios from interviews, and is then tested through selective bottom-up checks. This involves sample contract value multiplied by active client counts for twenty providers. Five key drivers, including public-cloud workload growth, alert velocity per endpoint, security-talent wage inflation, audit frequency, and ransomware incident rates, feed a multivariate regression to 2030. Scenario analysis gauges AI-driven productivity shifts.

Data Validation & Update Cycle

Model outputs pass three review rounds, where anomalies versus historical vendor growth or macro signals trigger renewed source contact. We refresh the dataset yearly and issue interim updates for major breaches or new regulation so clients always receive the latest baseline.

Why Our Security Operations Center As A Service Baseline Proves Consistently Reliable

Published estimates often differ because firms draw service lines differently, convert currencies on varied dates, or roll numbers forward without fresh checks.

Narrower coverage, optimistic full bottom-up claims that ignore private vendors, and slower refresh cycles that missed 2024 price dips linked to analyst automation drive most gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.07 B (2025) | Mordor Intelligence | |

| USD 7.37 B (2024) | Global Consultancy A | Excludes co-managed contracts; uses 2023 price index |

| USD 6.09 B (2024) | Trade Journal B | Counts detection only; omits response add-ons |

| USD 15.20 B (2030) | Industry Tracker C | Projects historic CAGR without checking 2024 revenue reset |

These contrasts show that Mordor Intelligence, through transparent scope choices and mixed-method triangulation, delivers a balanced, defensible starting point for decision-makers.

Key Questions Answered in the Report

How large is the security operation center as a service market in 2026?

The market reached USD 14.77 billion in 2026, reflecting widespread migration from in-house monitoring to managed detection and response subscriptions.

What is the expected growth rate for the security operation center as a service market to 2031?

The sector is forecast to expand at a 12.77% CAGR, lifting total value to USD 26.93 billion by 2031.

Which deployment model is growing fastest?

Hybrid cloud implementations are registering a 14.28% CAGR because they satisfy latency and data-residency requirements while delivering cloud-scale analytics.

Why is healthcare adopting outsourced security operations so rapidly?

Ransomware attacks on electronic health records and connected medical devices are rising, pushing healthcare organizations to seek 24/7 managed detection and response coverage that internal teams cannot sustain.

How do data-sovereignty laws influence provider selection?

Regulations in the European Union, India, and China require local log processing, favoring vendors with in-country security operations centers or regional partnerships.

What differentiates incident response and threat hunting from basic managed detection?

Proactive threat hunting involves hypothesis-driven searches for hidden adversaries, while incident response retainers provide expert containment and forensics; both services command higher pricing but reduce breach costs.

Page last updated on: