Data Center Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.83 Billion |

| Market Size (2031) | USD 35.45 Billion |

| Growth Rate (2026 - 2031) | 14.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Center Security Market Analysis by Mordor Intelligence

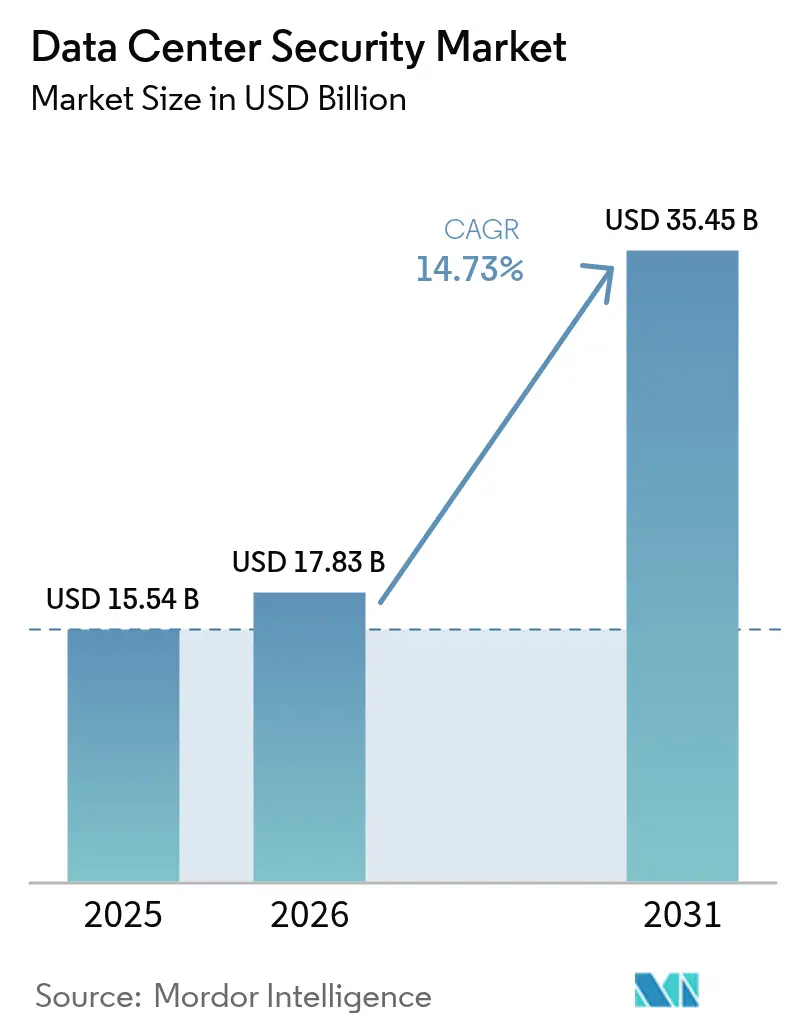

The data center security market size was valued at USD 15.54 billion in 2025 and estimated to grow from USD 17.83 billion in 2026 to reach USD 35.45 billion by 2031, at a CAGR of 14.73% during the forecast period (2026-2031). The expansion reflects mounting pressure on operators to safeguard high-density environments that now power AI training, edge analytics, and hybrid-cloud workloads. Rising cyber-attack frequency, rapid hyperscale build-outs, and tighter global compliance rules are reshaping how vendors design physical and logical controls. Companies are moving from perimeter defenses to identity-centric, zero-trust blueprints that verify every request and continuously monitor device health. Parallel investments in AI-driven threat hunting, converged physical-logical platforms, and security-as-a-service models are reshaping buying patterns, especially among resource-constrained enterprises.

Key Report Takeaways

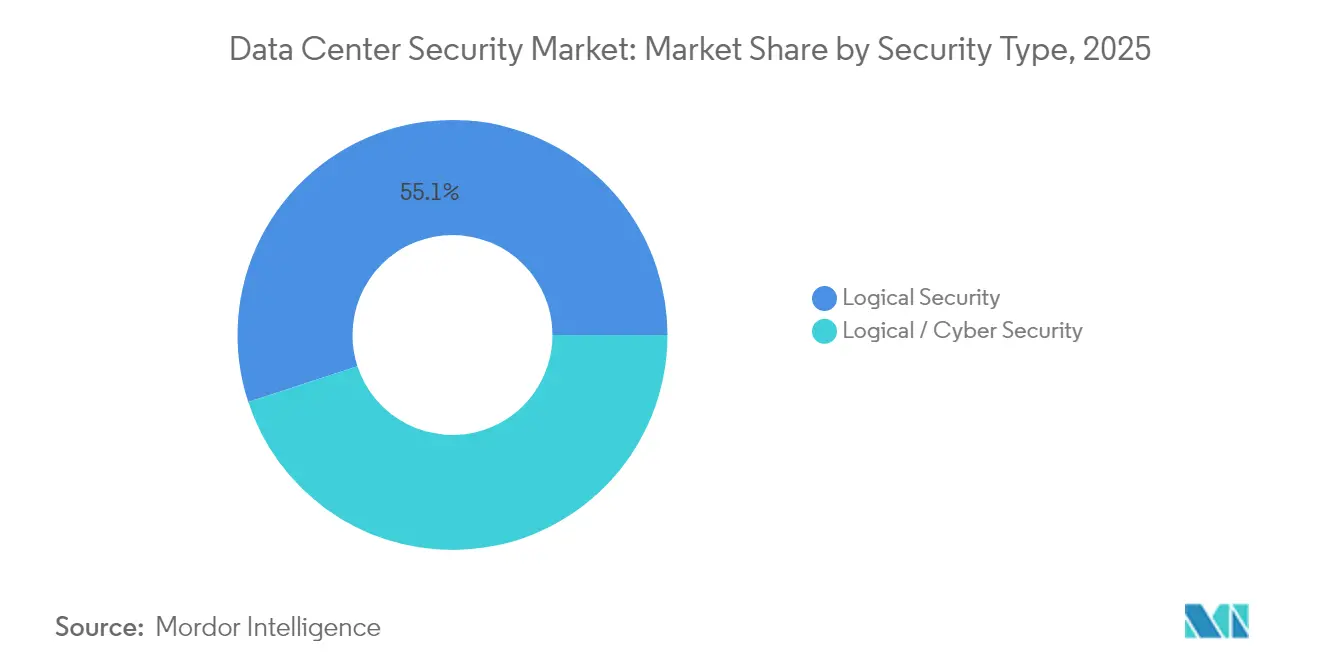

- By security type, logical security led with 55.05% of the data center security market share in 2025; physical security is forecast to expand at a 17.05% CAGR through 2031.

- By offering, solutions command 67.00% share of the data center security market size in 2025, while managed services are projected to grow at 17.12% CAGR to 2031.

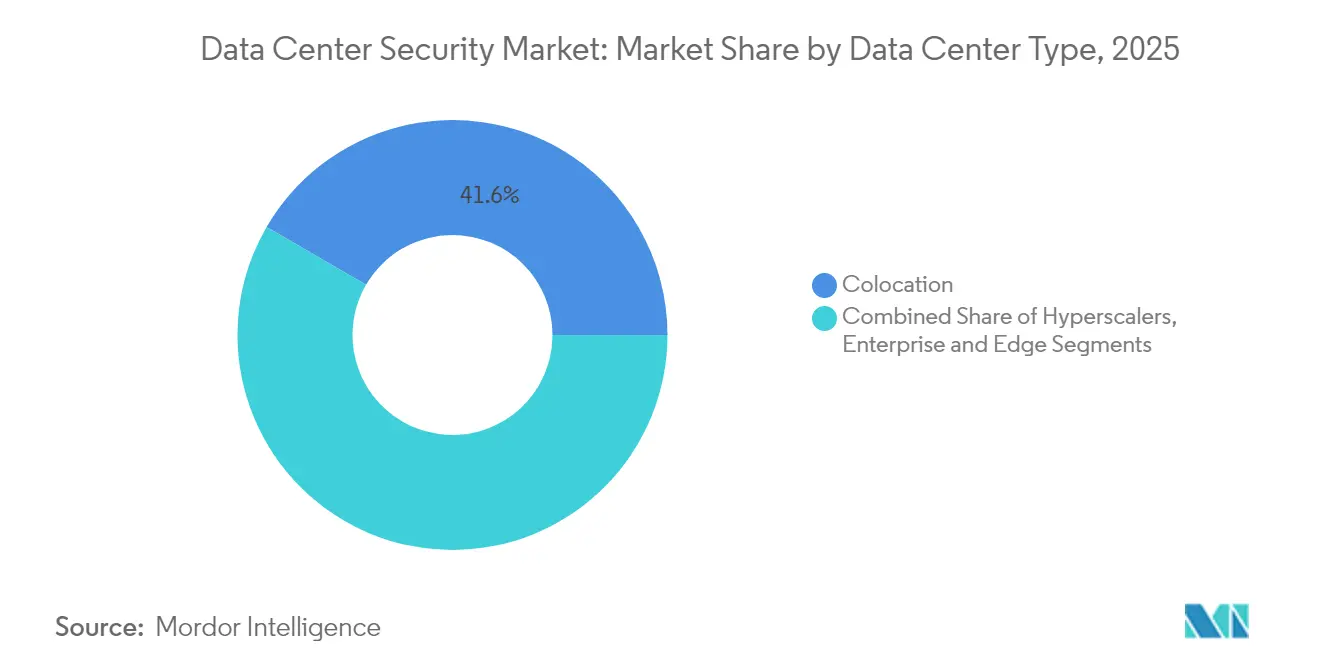

- By data center type, colocation facilities captured 41.62% of the data center security market share in 2025; hyperscalers are advancing at a 19.12% CAGR through 2031.

- By industry vertical, BFSI accounted for 31.55% of the data center security market size in 2025, whereas government & defense registers the fastest 16.84% CAGR between 2026-2031.

- By geography, North America held 36.78% of the data center security market share in 2025; Asia-Pacific is poised for a 18.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Data Center Security Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive data-traffic and hyperscale build-outs | +5.1% | Global, led by North America and Asia-Pacific | Medium term (2–4 years) |

| Escalating cyber-attack sophistication | +3.7% | Global | Short term (≤ 2 years) |

| Stringent global compliance mandates | +2.9% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Cloud and hybrid IT attack-surface expansion | +2.1% | Global | Short term (≤ 2 years) |

| AI-powered zero-trust fabric inside DC | +1.8% | North America, Europe | Medium term (2–4 years) |

| Autonomous physical security for edge/modular DC | +1.8% | Global, early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Data-Traffic and Hyperscale Build-Outs

Hyperscale operators are on track to handle 76% of global AI server shipments in 2024, concentrating valuable assets that demand hard-to-breach defenses. Power budgets for AI campuses could top 5 GW by 2030, prompting parallel upgrades in security zones, badge-less biometrics, and AI-assisted network segmentation.[1]Sean Michael Kerner, “Hyperscalers in 2024: Where Next,” Data Center Knowledge, datacenterknowledge.com; Flexential, “Navigating AI Data Center Trends,” Flexential, flexential.comVendors now ship modular security appliances that process terabits of encrypted traffic without latency spikes. Operators also embed machine-learning sensors that surface anomalous east-west flows invisible to legacy firewalls. Together these shifts stimulate sustained spending, especially across the data center security market as colocation, enterprise, and edge facilities mirror hyperscale best practices.

Escalating Cyber-Attack Sophistication

Organizations endured an average of 1,900 weekly attacks in late 2024, driven by attackers automating reconnaissance and exploit delivery. Zero-day weaponization cycles collapsed from weeks to hours, pressuring operators to deploy self-learning defenses that hunt and neutralize threats without analyst intervention.[2]Pelco, “Future of Security Technology: Industry Trends of 2025,” Pelco, pelco.com; Darktrace, “AI and Cybersecurity: Predictions for 2025,” Darktrace, darktrace.com Integration of continuous behavior analytics and adaptive policy engines is now baseline. Investment gravitates toward unified platforms that converge endpoint, workload, and network telemetry, expanding the addressable data center security market among midsize enterprises that previously relied on siloed toolsets.

Stringent Global Compliance Mandates

PCI DSS 4.0, effective 2025, enforces longer passphrases and full-stack monitoring across cardholder environments. Europe’s DORA raises similar bars for operational resilience, while multiregional sovereignty laws complicate cross-border backup topologies.[3]Thales Group, “Preparing for PCI DSS 4.0 Compliance in 2025,” Thales Group, cpl.thalesgroup.com Breach fines averaged GBP 3.5 million in the UK during 2024. These costs propel uptake of compliance automation, boosting managed service demand and widening the data center security market size tied to audit-ready reporting.

Cloud and Hybrid IT Attack-Surface Expansion

By 2025, 75% of enterprise data will be processed outside traditional halls, stretching defenses to edge racks and multi-cloud clusters datacentreworld.com. Container and serverless workloads introduce ephemeral endpoints that dissolve conventional zoning. Firms now roll out cloud-security-posture-management suites that inventory misconfigurations in real time, while zero-trust fabrics authenticate every east-west connection. Such measures inject new opportunities across the data center security market, especially for SaaS providers blending posture management with identity brokering.

Restraints Impact Analysis of Data Center Security Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX/OPEX for multi-layer security | -1.8% | Global, higher impact in emerging markets | Medium term (2–4 years) |

| Cyber-skills shortage | -1.2% | Global, acute in Asia-Pacific & Latin America | Short term (≤ 2 years) |

| Power and cooling budgets crowd out security | -0.9% | Global, concentrated in power-constrained hubs | Medium term (2–4 years) |

| Data-localization architecture complexity | -0.7% | Europe, Asia-Pacific, Middle East | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

High CAPEX/OPEX for Multi-Layer Security

Full-stack protection—from perimeter fencing to anomaly detection—regularly consumes double-digit percentages of facility budgets. Cloud security could absorb 20% of enterprise cyber spend by 2025. Operators offset costs through security-as-a-service contracts that shift capital outlays into predictable fees, yet customizing these services to legacy gear inflates integration timelines. Colocation providers navigate tight vacancy and pricing pressure, delaying upgrades and tempering growth within segments of the data center security market.

Cyber-Skills Shortage

Unfilled cyber roles crest above 3.5 million worldwide, pushing salaries up and reliance on managed detection to 40% of SMB budgets by 2025. Automation mitigates routine triage, but incident response and architecture design still demand scarce talent. Vendors that wrap guided playbooks and training into products gain favor, but adoption lags in Latin America and parts of Asia, constraining the regional data center security market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Data Center Security Market Segment Analysis

By Security Type:

Logical Controls Cement LeadLogical safeguards held 55.05% share of the data center security market in 2025 as identity-aware firewalls, micro-segmentation, and AI-enhanced monitoring became baseline. The segment is poised for a 16.62% CAGR through 2031, reflecting heightened urgency to inspect east-west traffic and verify every session. Enterprises now favor policy engines that adjust privileges dynamically, referencing device posture, geolocation, and behavioral deviations.

Physical safeguards remain foundational, particularly across edge racks where theft and tampering risks climb. AI-powered cameras, biometric turnstiles, and robotics converge with software alerts, creating integrated command centers where a single console governs locks, alarms, and packet flows. This convergence lifts cross-sell potential inside the data center security market as buyers replace siloed badge systems with unified platforms that slash blind spots.

By Offering:

Services Outpace Product GrowthSolutions contributed 67.00% to the data center security market size in 2025, ranging from next-gen firewalls to DCIM-embedded surveillance. Yet complexity, regulatory churn, and skills gaps propel managed services to a 17.12% CAGR, outstripping hardware refresh cycles. Providers now bundle threat hunting, forensic analysis, and compliance reporting under outcome-based service-level agreements.

Consulting demand likewise rises as firms recalibrate architectures against zero-trust baselines and quantum-safe roadmaps. IBM’s 24/7 managed service suite illustrates the shift, layering incident response on cloud-workload protection for enterprises lacking continuous staff coverage. This trajectory creates fresh recurring revenue and expands the global data center security market.

By Data Center Type:

Hyperscalers Accelerate InnovationColocation venues held 41.62% of the data center security market share in 2025 by aggregating enterprise gear behind standardized safeguards. Operators differentiate through customer-segmented access zones and on-prem SIEM integration.

Hyperscalers, however, register the steepest 19.12% CAGR as AI training clusters and sovereign-cloud regions multiply. Massive land purchases shift workloads into power-rich secondary metros, forcing new blueprints for remote monitoring and autonomous robotics. Lessons learned cascade into enterprise and edge designs, widening overall data center security market adoption.

By Industry Vertical:

Finance Dominates SpendBFSI players accounted for 31.55% of the data center security market size in 2025, driven by strict audit trails and high fraud exposure. Zero-trust rollouts, hardware security modules, and continuous control validation are now mandatory.

Government & defense outpaces with a 16.84% CAGR as agencies harden classified compute nodes and satellite ground stations. Healthcare and telecom likewise elevate budgets to secure e-records and 5G core slices. Regardless of vertical, executives increasingly view advanced defenses as revenue enablers rather than pure cost centers, reinforcing robust growth across the data center security market.

Geography Analysis

North America Data Center Security Market

North America led the data center security market at 36.78% in 2025, underpinned by dense hyperscale clusters and elevated regulatory scrutiny. The United States alone captured 77% of regional spend, with cloud giants announcing multi-billion-dollar AI-campus rollouts that integrate zero-trust blueprints from day one. Secondary metros such as Atlanta and Phoenix attract growth as power caps tighten in legacy hubs, compelling operators to replicate security controls across dispersed footprints.

APAC Data Center Security Market

Asia-Pacific is set for a 18.63% CAGR, the fastest among regions, thanks to double-digit capacity additions and digital-banking demand. Singapore’s moratorium-ending green permits spur secure greenfield sites, while Tokyo leverages stringent privacy laws to lure BFSI tenants. China and India emphasize localized encryption keys, prompting bespoke compliance modules and fueling the data center security market across indigenous service providers. Mitsui & Co.’s USD 118 million (JPY 18 billion) stake in a Kanagawa hyperscale facility highlights the investment tide.

EMEA and LATAM Data Center Security Market

Europe intensifies security investments in new AI clusters across Italy, Spain, and France, balancing GDPR mandates with renewable-energy targets. Latin America posted 42% growth in 2024, led by Brazil and Mexico where energy access improvements coincide with marquee cloud regions. The Middle East and Africa adopt sovereign-cloud clauses and SEZ incentives, extending the data center security market to greenfield campuses in Dubai and Johannesburg. Across all regions, data-sovereignty themes and export-control programs such as the U.S. Data Center VEU Authorization reinforce demand for tamper-proof audit trails

Regulatory Landscape

Compliance requirements for data center operators and their security vendors are tightening across major regions, with frameworks shifting from guidance to enforceable controls. In the United States, the White House Office of Management and Budget issued Memorandum M-25-03 (January 2025) to implement the Federal Data Center Enhancement Act of 2023, reinforcing expectations around cybersecurity, resiliency, and availability for federal agency data centers and influencing contracting requirements for security solutions and services. NIST also refreshed its baseline playbook with Cybersecurity Framework (CSF) 2.0 and accompanying quick-start guidance (published in 2026), aligning cybersecurity programs more explicitly to enterprise risk management and workforce practices used by data center operators and managed security providers.

In Europe, the NIS2 Directive (Directive (EU) 2022/2555) places data center service providers within scope, and the European Commission adopted Implementing Regulation (EU) 2024/2690 (October 2024) with technical and methodological cybersecurity risk-management requirements that affect monitoring, incident handling, and resilience measures. Germany's Federal Office for Information Security (BSI) updated its cloud compliance catalog via C5:2026, reflecting newer EU-aligned requirements and raising expectations for cloud and colocation environments to demonstrate audit-ready controls. These regulatory and standards updates are feeding demand for continuous control validation, standardized reporting, and a tighter link between physical resilience and logical security policies.

Value Chain Analysis

The data center security value chain runs from compliance frameworks and technical standards to solution vendors (network security, workload protection, SIEM/XDR, identity, and physical access control), systems integrators, managed security service providers (MSSPs), and data center operators (hyperscalers, colocation, and enterprise/edge). Upstream inputs increasingly include security-relevant facility infrastructure, such as power distribution and backup systems, which underpin resilience controls required by regimes like NIS2 and by assurance programs such as ISO 27001 and SOC 2. Standards including ISO/IEC 22237-6:2024 also influence physical security system design and procurement, shaping how access control, surveillance, and intrusion detection are specified and validated.

Execution risk across the chain is increasing as infrastructure supply bottlenecks extend security build-outs and refresh cycles for new halls and retrofits. By 2026, industry reporting indicates longer lead times for high-voltage components (including power transformers, switchgear, and generators), which pushes developers to place long-lead orders earlier and to align security planning with construction and commissioning milestones. In response, security vendors and integrators are packaging more modular, prevalidated architectures and managed services that better match audit and availability targets while reducing on-site integration effort in power-constrained or schedule-constrained campuses.

Competitive Landscape

The data center security market remains moderately concentrated around Cisco, IBM, Palo Alto Networks, and Fortinet. Cisco’s acquisition of Splunk positions it to correlate observability with edge policy enforcement, deepening end-to-end telemetry. Palo Alto Networks has spent USD 5.5 billion on 17 deals since 2018, most recently agreeing to buy Protect AI for USD 700 million to secure generative-AI pipelines.

Platform thinking dominates as buyers seek single consoles that span cloud workload protection, XDR, and SASE. The XDR segment could reach USD 8.8 billion by 2028 channelfutures.com. Cloud-native challengers such as CrowdStrike, Wiz, and Zscaler leverage agentless scanning and API-centric enforcement to peel away share. Integration depth and partner ecosystems are emerging as decisive factors, with Cisco and Palo Alto Networks embedding open telemetry streams to court MSSPs.

White-space opportunities persist in quantum-safe encryption, AI model integrity, and converged physical-logical orchestration. Operators favor vendors offering turnkey blueprints that fold in robotics, access control, and micro-segmentation, broadening addressable spend throughout the data center security market.

Data Center Security Industry Leaders

Cisco Systems Inc.

IBM Corporation

Check Point Software Technologies

Fortinet Inc.

Palo Alto Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Data Center Security Market Companies Covered in this Report

- Cisco Systems Inc.

- IBM Corporation

- Check Point Software Technologies Ltd.

- Symantec (Gen Digital)

- Juniper Networks Inc.

- VMware by Broadcom

- Fortinet Inc.

- Palo Alto Networks Inc.

- Trend Micro Inc.

- Dell Technologies

- Hewlett Packard Enterprise

- Citrix Systems

- Schneider Electric SE

- Siemens AG

- Honeywell International Inc.

- Genetec Inc.

- Bosch Security Systems

- Arista Networks

- Cyxtera Technologies

- Hikvision Digital Technology

- Johnson Controls

- NEC Corporation

Market Opportunities and Future Outlook

AI-driven capacity additions are creating whitespace for security architectures that protect high-density GPU environments, software supply chains, and east-west traffic at scale. Large campus expansions and new AI-ready developments point to the need for standardized, repeatable security baselines across distributed facilities and supplier ecosystems. Meta's planned expansion of its Hyperion data center campus in Richland Parish, Louisiana to 5 GW (July 2026) highlights the operational need for scalable zero-trust enforcement, privileged access governance, and converged physical-logical controls across multiple security zones and build phases.

Opportunities are also building around compliance and assurance harmonization as buyers adopt updated standards and enforcement mechanisms. Demand for audit-ready security tooling increases with the ISO/IEC 27001 transition to the 2022 version (transition period ending 31 October 2025) and the publication of ISO/IEC 27000:2026, including continuous evidence collection, configuration drift monitoring, and automated remediation workflows delivered through managed services. In parallel, AI infrastructure security gap analyses are driving demand for explicit overlays or profiles that tailor controls to AI-specific risks (including accelerator fabric management and hardware integrity). This creates room for vendors that can combine runtime vulnerability mitigation, integrity monitoring, and physical security automation for cages and entrances into a unified operating model.

Recent Industry Developments in Data Center Security Market

- July 2026: IBM and Red Hat expanded Project Lightwell with new commercial offerings designed to automate vulnerability remediation across application dependencies. The effort focuses on software supply chain defenses for hybrid-cloud and data center environments by reducing the time between vulnerability discovery and mitigation through more standardized workflows.

- October 2025: Fortinet launched its Secure AI Data Center solution to protect AI models, data, and supporting infrastructure at scale. This broadened the company's data center security portfolio toward AI-specific threats and consolidated controls that buyers can deploy across high-density training and inference environments.

- April 2024: Cisco reimagined security for data centers and clouds in the era of AI, highlighting updated architectures that unify visibility and enforcement across workloads, networks, and cloud. The announcement reinforced the market shift toward platform-led security that handles encrypted traffic and east-west segmentation without relying solely on perimeter defenses.

Data Center Security Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market is defined as revenues earned from securing data center environments through physical and logical controls, including security solutions and services that protect facilities, networks, applications, identities, and stored data used in data center operations.

Scope exclusions: it excludes general enterprise security spend that is not deployed for data center use cases, along with non-security facility construction and standard IT hardware refresh that is not security-specific.

Segments Covered in This Report

- By Security Type

- Physical Security

- Logical / Cyber Security

- By Offering

- Solutions

- Services (Consulting, Integration, Managed)

- By Data Center Type

- Hyperscalers/Cloud Service Providers

- Colocation

- Enterprise and Edge

- By Industry Vertical

- Banking and Financial Services (BFSI)

- IT and Telecom

- Healthcare and Life Sciences

- Consumer Goods and Retail

- Government and Defense

- Media and Entertainment

- Others (Energy, Education, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Singapore

- Australia

- Malaysia

- Rest of Asia-Pacific

- South America

- Brazil

- Chile

- Argentina

- Rest of South America

- Middle East

- United Arab Emirate

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map what buyers typically purchase for data center security, and to list the common triggers behind spend, such as new builds, capacity expansions, and tighter compliance requirements. Public references were also used to understand regional build activity, recurring cyber incident patterns, and baseline pricing direction for key security categories.

Sources consulted included public statistics and publications such as the International Telecommunication Union, NIST guidance and frameworks, NERC CIP materials for critical infrastructure security, Eurostat for digital economy indicators, and the World Bank for macro and investment signals. Supplementary inputs were taken from annual reports, investor presentations, security certification bodies, and reputable press. In a few places, paid subscriptions were used for company financials and intelligence, patent lookups, and shipment-level trade checks to sanity-test coverage and flag potentially missing product families. These examples are illustrative and not exhaustive, and many other sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to confirm what is actually counted as data center security spend, and what is treated as adjacent IT security that should not be mixed in. Interviews covered solution providers, system integrators, colocation and enterprise facility operators, and security leaders who manage budgets, so model inputs could be corrected where desk signals were weaker.

Because this is a global market, coverage was balanced across APAC, EMEA, and the Americas, and inputs were checked across hyperscale, colocation, and enterprise and edge environments. Where answers varied by region or data center type, assumptions were narrowed to what most respondents described as a typical buying pattern for the base year and forecast years.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | APAC: 38% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 35% |

| Smaller Players: 18% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down, demand-pool reconstruction approach, where data center build-outs and installed capacity signals were translated into security attach rates and spending per site, then scaled by region. After the first total was obtained, we corroborated it with selective bottom-up approximations, such as rolling up sampled supplier revenues by security category and checking typical ASP x volume ranges for high-visibility items like access control, surveillance, and monitoring software.

Inputs that materially shaped the model included data center capacity additions and new facility counts, the mix of hyperscale versus colocation versus enterprise and edge sites, typical security stack adoption (physical controls, identity and access, threat and application protection, and data protection), and service intensity (consulting, integration, and managed services) by customer type. In places where revenue splits were unclear, gaps were handled by using respondent-confirmed bundle ratios and then back-checking totals against reported security budget shares for data center operations.

For forecasting, scenario analysis was used so the model could reflect different build-out speeds and security posture changes, and then it was anchored back to primary inputs on expected pricing progression and adoption timing. Each year, we tracked a short set of leading indicators, including capacity pipeline announcements, compliance and audit activity, and changes in breach and incident pressure that typically pull forward security upgrades.

Data Validation & Update Cycle

Validation was done in layers so the final number did not rely on a single assumption. Outputs were compared with independent signals like regional data center expansion trends, the security services mix, and implied per-site spending, and then checked for sharp year-to-year jumps that would not align with real procurement cycles.

Before sign-off, anomalies were reviewed in analyst checks, followed by targeted re-contacts when a key variable, such as attach rates for logical security or managed services penetration, looked out of line with what practitioners described. The report is refreshed annually, and interim updates are made when material events shift capacity plans, compliance needs, or spending behavior. Right before delivery, a final review pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Global Data Center Security Market Market Size Versus Other Published Estimates

Published market sizes for data center security can differ even when the topic name looks the same, because firms choose different boundaries for what counts as data center-only security and they also use different base years and currency timing. Differences in whether services are included, how hyperscale and edge sites are treated, and how pricing is rolled forward often explain most of the spread.

The table shows that the 2026 starting value in Mordor Intelligence's model is tied to a security stack deployed for data center environments and counted together with related consulting, integration, and managed services, rather than being blended into wider enterprise security spending. When another estimate uses an earlier base year or does not clearly separate facility security from broader cybersecurity categories, its number can land lower or higher depending on the mix assumptions and the growth window applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.83 B (2026) | |

| Global Consultancy A | USD 18.42 B (2024) | Uses a 2024 base year and a 2025-2030 forecast window, and the public summary does not make the data center-only scope boundary explicit, which can shift totals if broader security programs are included. |

| Industry Publisher B | USD 13.80 B (2022) | Anchors the market at 2022, and the published snapshot provides limited detail on how services, edge sites, and logical versus physical categories are valued, which can compress the base when categories are treated narrowly. |

Across the three figures, the biggest driver is not math complexity, it is what gets counted and which year is used as the anchor. By keeping the inputs traceable to capacity and deployment signals, and by checking assumptions with practitioners before rolling forward the forecast, the resulting view stays repeatable and easier to reconcile when new information arrives.

Key Questions Answered in the Report

What is driving the rapid growth of the data center security market?

Exploding AI workloads, rising cyber-attack volumes, and stricter compliance mandates compel operators to adopt zero-trust and AI-driven defenses, supporting a 14.73% CAGR through 2031.

Which segment controls the largest portion of data center security spending?

Logical security controls lead with 55.05% share, reflecting demand for micro-segmentation, identity verification, and continuous monitoring.

Why are managed security services gaining traction?

A global cyber-skills shortage and complex regulatory landscape push organizations to outsource threat hunting and compliance, fueling a 17.12% CAGR for managed services.

Which region will grow the fastest in data center security investment?

Asia-Pacific is projected to expand at 18.63% CAGR, driven by new hyperscale builds in China, India, Japan, and Singapore.

How are hyperscalers influencing security innovation?

Hyperscalers pioneer AI-assisted anomaly detection and autonomous physical safeguards, setting templates that colocation and enterprise sites increasingly adopt.

What compliance changes should operators prioritize for 2025?

Key updates include PCI DSS 4.0’s stronger authentication rules and Europe’s DORA requirements, both elevating expectations for continuous control validation and reporting.

Page last updated on: