Automotive Usage-Based Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 76.59 Billion |

| Market Size (2031) | USD 162.12 Billion |

| Growth Rate (2026 - 2031) | 16.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Usage-Based Insurance Market Analysis by Mordor Intelligence

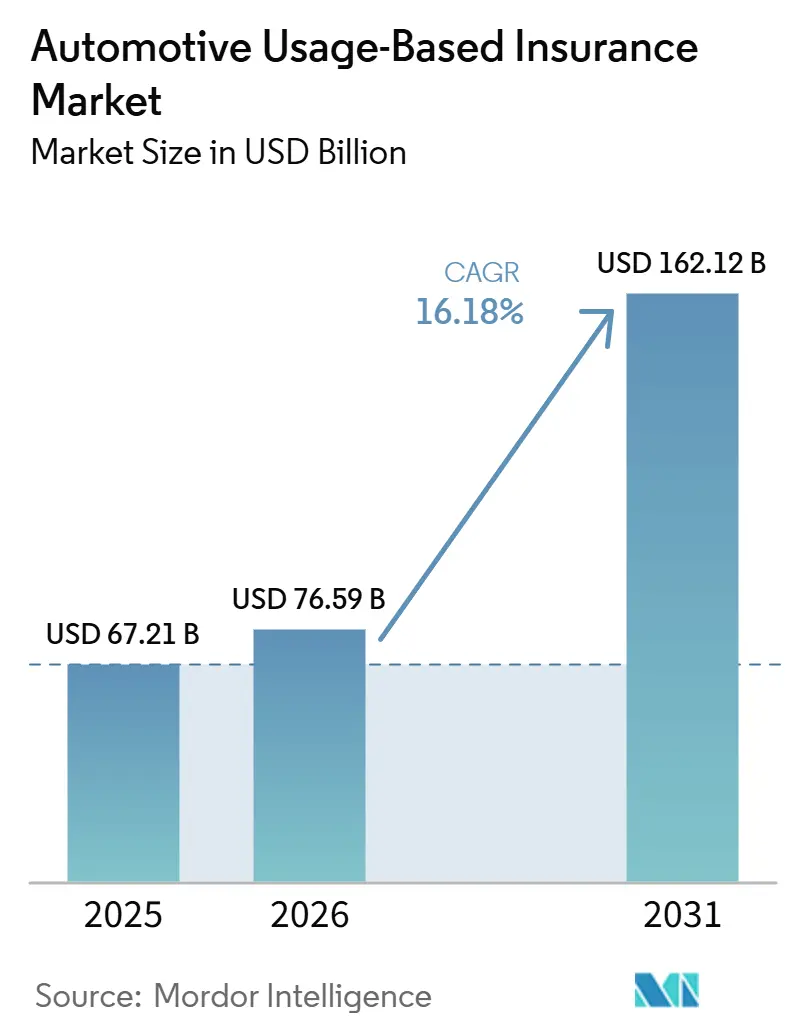

The Automotive Usage-Based Insurance Market size is expected to grow from USD 67.21 billion in 2025 to USD 76.59 billion in 2026 and is forecast to reach USD 162.12 billion by 2031 at 16.18% CAGR over 2026-2031.

The automotive usage-based insurance market is expanding as factory-fitted connectivity becomes more common in new vehicles, reducing friction in data collection and improving underwriting quality when insurers can access OEM-grade driving signals. It also benefits from the steady shift away from hardware-heavy telematics programs toward smartphone- and embedded-based models that improve onboarding speed and reduce per-policy implementation costs. Claims handling is becoming a larger source of advantage as real-time crash detection and AI-led workflows shorten response times and support lower operating costs for carriers that can connect telematics data directly to claims systems. North America remains the largest regional block because mature telematics infrastructure and insurer scale reinforce one another, while Asia-Pacific is moving faster as regulation, smartphone distribution, and connected mobility adoption create a broader entry path for newer programs. The main brake on the automotive usage-based insurance market is no longer technical readiness alone; consent design, privacy expectations, and cross-jurisdictional compliance rules now play a direct role in how quickly programs can scale across personal and commercial lines.

Key Report Takeaways

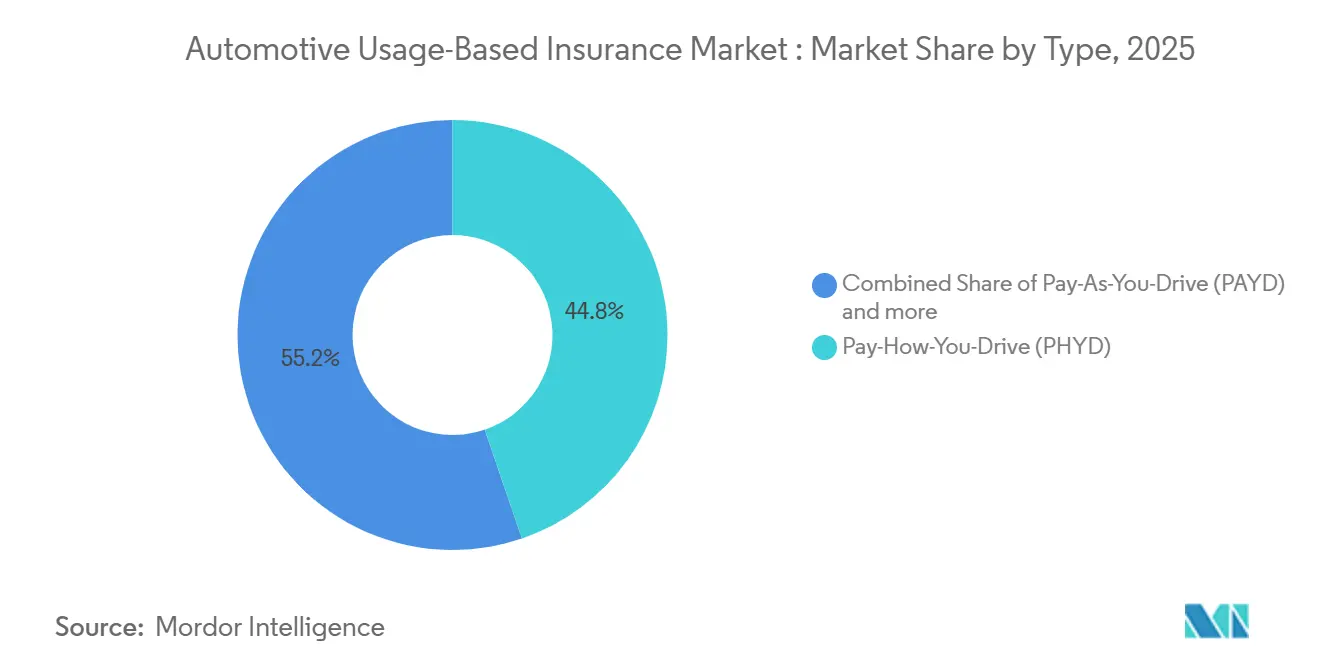

- By type, pay-how-you-drive captured 44.76% of the automotive usage-based insurance market share in 2025, while manage-how-you-drive is projected to grow at a 22.39% CAGR through 2031.

- By solution, Smartphones accounted for 37.48% of the automotive usage-based insurance market in 2025, while Embedded Solutions are projected to grow at a 23.81% CAGR through 2031.

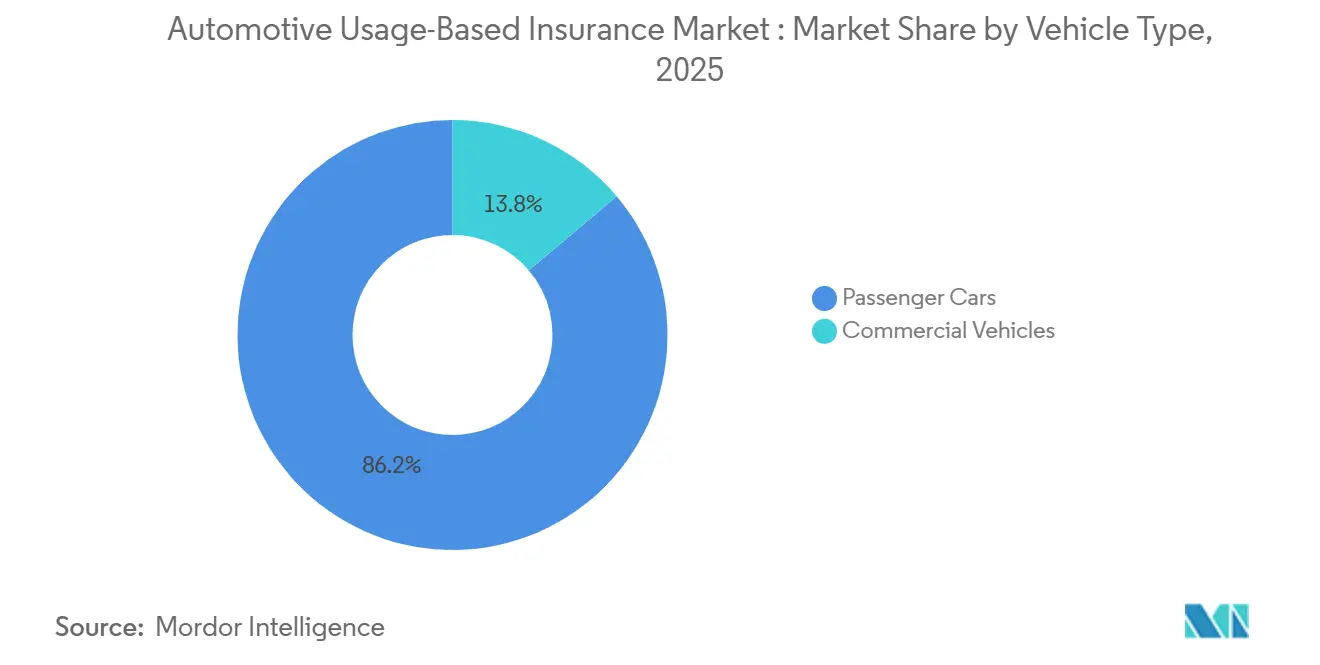

- By vehicle type, Passenger Cars accounted for 86.17% of the automotive usage-based insurance market in 2025, while Commercial Vehicles are projected to grow at a 19.74% CAGR through 2031.

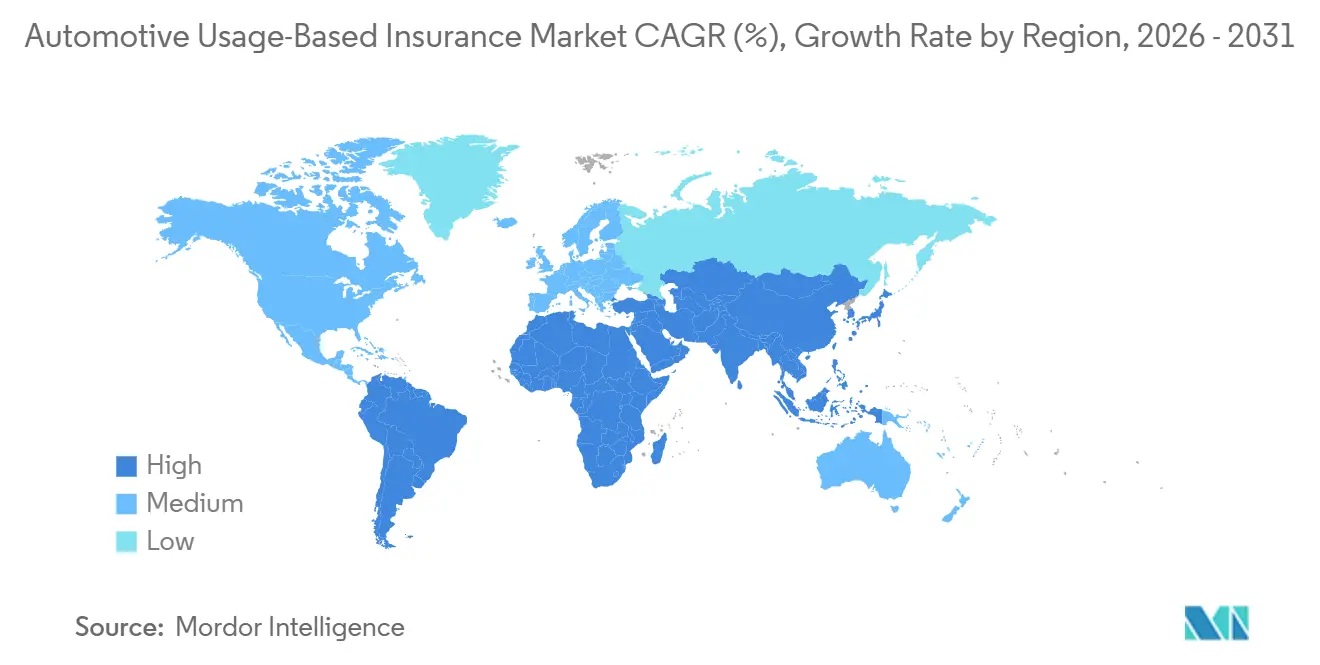

- By geography, North America held 39.84% of the automotive usage-based insurance market share in 2025, while the Asia-Pacific region is projected to grow at a 21.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Usage-Based Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Embedded Telematics Rollouts | +2.3% | Global, with EU and Asia-Pacific leading on mandatory fitment | Medium term (2-4 years) |

| Fleet Pay-Per-Mile Adoption | +1.5% | North America core, expanding to EU and Asia-Pacific logistics corridors | Short term (≤ 2 years) |

| Real-Time Crash Coaching Feedback | +1.3% | North America and Europe, with early adoption in Asia-Pacific | Medium term (2-4 years) |

| Usage-Priced EV Insurance Demand | +1.7% | Global, concentrated in the EU, China, and the United States EV corridors | Short term (≤ 2 years) |

| Claims Automation Cost Advantage | +1.4% | Global, with AI-native carriers in North America and Europe leading | Short term (≤ 2 years) |

| Connected-Car Data Monetization | +1.2% | Global, especially OEM-heavy markets in Europe, North America, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Embedded Telematics Rollouts: Factory-Fit Data Reshaping Underwriting Economics

The automotive usage-based insurance market is moving away from retrofit devices because factory-fitted telematics reduces setup friction and provides insurers with more stable access to vehicle-generated data. In March 2026, Geotab launched a native telematics integration for Hyundai vehicles across Europe, enabling hardware-free fleet data transmission and reducing the need for aftermarket installation[1]Geotab, “Geotab and Hyundai Launch Native Telematics,” Geotab, geotab.com.. IMS also confirmed that Volkswagen-embedded sensor data can now be translated into underwriting-ready pay-how-you-drive outputs through its integration with high mobility, enabling insurers to plug OEM data into existing scoring workflows without changing the front-end customer experience. IDEMIA Secure Transactions announced in February 2026 that it is managing automotive connectivity for Hyundai Motor Group across strategic global markets, which supports a broader connected-car base from the factory onward. As this installed base grows, the automotive usage-based insurance market will reward carriers that build direct OEM data pipelines, as they will be able to price risk with richer telemetry than insurers still relying solely on app or dongle inputs. This does not remove the role of smartphones, but it does raise the long-term value of embedded data partnerships within the automotive usage-based insurance market.

Fleet Pay-Per-Mile Adoption: Gig Economy and Logistics Fleets Accelerate Commercial UBI

The automotive usage-based insurance market is finding a stronger commercial growth engine as fleet managers seek pricing models that reflect actual usage and driving behavior rather than static annual assumptions. Cambridge Mobile Telematics launched the Drivewell Fleet in January 2025 to help commercial auto insurers reach full telematics coverage by ingesting data from existing connected vehicle systems and avoiding dedicated hardware where possible[2]CMT Cambridge Mobile Telematics Launches DriveWell Fleet - Cambridge Mobile Telematics. That matters because commercial deployment has historically been slowed by hardware logistics, inconsistent data capture, and the need to standardize signals across mixed fleets. The same CMT material cites findings from the IoT Insurance Observatory that fleets enrolled in UBI programs saw a 10% to 19% reduction in claims frequency within 18 months, which materially strengthens the business case for behavior-linked pricing CMT. In the automotive usage-based insurance market, this creates a margin case as much as a growth case, because lower claims frequency can offset the discounts carriers use to attract fleet operators. The result is a clearer path for commercial telematics programs in logistics, last-mile delivery, and gig-linked vehicle pools across the automotive usage-based insurance market.

Usage-Priced EV Insurance Demand: Battery and Behavior Data Unlock New Pricing Dimensions

The automotive usage-based insurance market is also gaining support from the adoption of electric vehicles, as EVs exhibit a different risk profile and a broader data trail than conventional vehicles. Academic work published in MDPI found that UBI models calibrated to EV driver behavior can reduce underwriting cost volatility by incorporating advanced safety-feature data and lower-accident-rate patterns that static demographic variables do not fully capture[3]MDPI, “Balancing Profitability and Sustainability in Electric Vehicles Insurance, Underwriting Strategies for Affordable and Premium Models,” World Electric Vehicle Journal, mdpi.com.. This matters because battery behavior, charging use, powertrain characteristics, and software-driven safety systems can create pricing differences that traditional rating tables do not capture well. Arity’s work on EVs and usage-based insurance also supports the view that behavior-linked models are becoming increasingly relevant as insurers seek pricing methods that reflect how electric vehicles are actually driven and managed over time. Within the automotive usage-based insurance market, EV coverage is therefore becoming a design problem tied to data quality rather than a simple extension of conventional auto insurance products. That makes telematics a core underwriting layer for the automotive usage-based insurance market as EV penetration rises in major urban corridors.

Claims Automation Cost Advantage: Telematics-Linked AI Closes the Expense Ratio Gap

The automotive usage-based insurance market is increasingly shaped by what happens after a crash, not only by how a premium is first priced. Allianz stated that its Project Nemo claims platform reduced processing time by 80% during its initial deployment, demonstrating how agentic AI can compress processing cycles when workflows are standardized and data is available in real time. Progressive and Cambridge Mobile Telematics launched accident response for more than 1.5 million Progressive personal auto customers in November 2025, bringing AI-based crash detection and automated claims initiation into a live insurance environment at scale[4]CMT Progressive Insurance® Accident Response Powered by Cambridge Mobile Telematics Provides Real-Time Crash Detection - Cambridge Mobile Telematics. In the automotive usage-based insurance market, this integration reduces delays at first notice of loss and provides insurers with a cleaner chain of events from detection to triage and service. It also improves the quality of labeled crash data that can later feed behavioral models, thereby strengthening pricing accuracy over time in the automotive usage-based insurance market. Carriers that combine telematics, claims automation, and feedback loops are therefore creating a more durable cost advantage than carriers that treat telematics only as a discount tool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consent Fatigue on Telematics | -1.8% | The United Kingdom, Europe, and increasingly North America as state-level privacy bills multiply | Short term (≤ 2 years) |

| Smartphone Sensor Bias Issues | -0.9% | Global, with stronger effects in emerging markets lacking OBD or embedded fallback | Medium term (2-4 years) |

| OEM Data-Access Fee Pressure | -1.2% | Europe and North America, where OEM API monetization is more developed | Medium term (2-4 years) |

| Multi-Jurisdiction Compliance Fragmentation | -1.0% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consent Fatigue on Telematics: Trust Deficit Constraining Market Depth

The automotive usage-based insurance market still faces a trust problem, even though product awareness is much stronger than it was a few years ago. IMS reported in 2026 that 72% of motorists across five international markets were open to UBI in principle, yet more than half remained reluctant to share driving data due to concerns about misuse and transparency. That gap matters because enrollment is the foundation of every scoring model, and weak opt-in rates reduce the volume and diversity of the data pool that insurers need to refine pricing. The Congressional Research Service also noted that the FTC’s proposed consent order with GM and OnStar in early 2025 would require affirmative express consent before future collection of driving behavior data and would restrict sharing with consumer reporting agencies for 5 years. In the automotive usage-based insurance market, this means consent architecture is becoming part of the product itself rather than a legal afterthought. Programs that give drivers visible control over data use, retention, and rewards will likely scale faster than programs that rely on generic terms and passive opt-in flows across the automotive usage-based insurance market.

Multi-Jurisdiction Compliance Fragmentation: Regulatory Divergence as a Market-Entry Tax

The automotive usage-based insurance market becomes harder to scale when a carrier tries to move the same program across several jurisdictions with different rules on data use, consent, and underwriting. The Congressional Research Service reported that California, Hawaii, Massachusetts, and Michigan have statutes limiting telematics data use in underwriting, while proposed rules in North Carolina and Tennessee would add written consent and disclosure requirements. Root’s Q1 2026 shareholder communication showed that the company was operating in 36 states, while Wyoming, Massachusetts, North Carolina, Michigan, Idaho, and Maine were still awaiting regulatory approval, illustrating how sequencing can be a practical barrier even for well-funded telematics-first insurers. In the automotive usage-based insurance market, each additional state or country can require a modified consent design, a different filing structure, and separate operational controls. India has permitted usage-based motor insurance add-ons, but this still does not address the broader challenge of managing diverse regulatory approaches across large markets. The effect is that the automotive usage-based insurance market tends to favor incumbents with stronger legal infrastructure and patience for staged expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: MHYD Coaching Models Disrupting the PHYD Incumbency

Pay-as-you-drive held a 44.76% share of the automotive usage-based insurance market in 2025, maintaining its lead because behavioral scoring is already familiar to both carriers and policyholders. The automotive usage-based insurance market still leans toward PHYD because it provides insurers with a broader risk picture than mileage-only models by capturing braking, acceleration, cornering, and distraction-related behaviors. Progressive reported that around 21 million policyholders were enrolled in Snapshot in Q1 2026, roughly 53% of its personal auto book, indicating that behavior-based segmentation is now deeply embedded in leading personal lines programs. This scale matters because large enrolled books help carriers refine loss modeling and price more confidently across a wider range of driver profiles. The automotive usage-based insurance market, therefore, continues to treat PHYD as the most established format where underwriting precision and program familiarity matter most.

Manage-how-you-drive is projected to grow at a 22.39% CAGR through 2031, making it the fastest-growing type in the automotive usage-based insurance market. Its appeal lies in turning telematics into an active relationship rather than a passive score, as coaching, reward loops, and crash support can improve both retention and driver behavior over time. Arity and the IoT Insurance Observatory found in 2026 that 82% of surveyed policyholders would recommend a telematics app that provides coaching feedback, crash assistance, and safe-driving rewards, and that figure rose above 90% among drivers under 53. Pay-as-you-drive remains relevant in the automotive usage-based insurance market for low-mileage urban users and hybrid workers whose annual driving volume no longer fits conventional rating assumptions. As a result, the automotive usage-based insurance market is expanding from simple price measurement to a broader model in which pricing, coaching, and service increasingly sit within the same product frame.

By Solution: Embedded Solutions Displace Dongles as the Long-Term Infrastructure Standard

Smartphones accounted for 37.48% of the automotive usage-based insurance market in 2025, reflecting the ease of launching app-native programs without hardware installation. The automotive usage-based insurance market has favored smartphone solutions because they reduce onboarding friction, shorten launch cycles, and make enrollment easier for digitally acquired policyholders. They also let insurers test pricing models quickly across broad customer pools before investing in deeper OEM or fleet integrations. This advantage is strongest in personal auto lines where fast enrollment often matters more than extracting every possible vehicle signal from day 1. Even so, the automotive usage-based insurance market is beginning to treat smartphone telematics less as the final infrastructure choice and more as the fastest entry point.

Embedded solutions are projected to grow at a 23.81% CAGR through 2031, making them the fastest-growing solution in the automotive usage-based insurance market. Geotab’s March 2026 Hyundai launch in Europe demonstrated how OEM-native data transfer can eliminate hardware installation and enable seamless integration into connected insurance and fleet workflows. IMS also showed that Volkswagen embedded data can be converted into underwriting-ready PHYD outputs, while IDEMIA’s connectivity work with Hyundai Motor Group supports broader factory-fitted data access across strategic markets. Dongles and black boxes still serve older vehicles and some fleets, but the automotive usage-based insurance market is steadily reducing dependence on them as connected-car penetration rises. That leaves the automotive usage-based insurance market in a position where source-agnostic scoring engines may matter more than any single hardware format.

By Vehicle Type: Commercial UBI Emerging as a Structurally Separate Market Opportunity

Passenger Cars accounted for 86.17% of the automotive usage-based insurance market in 2025, reflecting the scale of personal auto insurance and the long lead that consumer telematics programs established over the last decade. The automotive usage-based insurance market remains centered on passenger vehicles because most insurer telematics books were built first in personal lines, where customer acquisition volume is far higher. This base also gave carriers time to refine behavioral scoring, discount design, and claims workflows before pushing harder into commercial applications. As a result, personal auto still provides the largest installed foundation for telematics-led pricing, retention, and claims response. The automotive usage-based insurance market continues to rely on that large passenger-car base even as growth opportunities shift elsewhere.

Commercial Vehicles are projected to grow at a 19.74% CAGR through 2031, making them the fastest-growing vehicle segment in the automotive usage-based insurance market. Cambridge Mobile Telematics stated that DriveWell Fleet can extend telematics coverage across commercial books by normalizing data from existing fleet systems, thereby lowering one of the biggest barriers to CMT rollout. The same material cited reports frequency reductions of 10% to 19% within 18 months for fleets enrolled in UBI programs, which provides commercial carriers with a direct operating rationale for expanding these products. Gig-economy operators and last-mile logistics fleets are particularly important because they are highly sensitive to changes in insurance costs and vehicle utilization patterns. This is why the automotive usage-based insurance market is increasingly treating commercial telematics as a separate growth lane rather than a simple extension of passenger car products.

Geography Analysis

North America accounted for 39.84% of the automotive usage-based insurance market share in 2025, making it the largest regional contributor, on the back of mature telematics infrastructure and strong insurer participation. The automotive usage-based insurance market in North America also benefits from the scale of established programs, and Progressive reported around 21 million Snapshot-enrolled policyholders in Q1 2026, equal to roughly 53% of its personal auto book, while the company posted a consolidated combined ratio of 86.4 and net premiums written of USD 23.6 billion in the quarter. This creates a reinforcing loop in which larger data pools improve pricing and stronger pricing performance helps support further enrollment. The automotive usage-based insurance market in the region is also shaped by compliance pressure because vehicle data governance is tightening at both federal and state discussion levels. That means North America combines the deepest commercial base with some of the most visible privacy and consent challenges in the automotive usage-based insurance market.

Europe remained the second-largest region in the automotive usage-based insurance market, supported by a policy environment that has normalized telematics adoption more than in many other mature markets. IVASS reported that 17.8% of RC auto policies in Italy carried a telematic black box in 2024, which made Italy one of the clearest proof points for scaled telematics adoption in Europe. IVASS Regulation 56/2025, which mandates digital claims reporting via SPID or CIE from April 2026, strengthens the region’s move toward more digitized insurance workflows. Germany remains a slower adopter, and TH Köln found in February 2025 that telematics tariffs were still niche there and would likely scale only if the market moved toward stronger bonus-malus pricing structures. The EU eCall requirement continues to support the automotive usage-based insurance market because every new vehicle sold in the region carries an embedded emergency response system that improves telematics readiness.

Asia-Pacific is projected to grow at 21.13% CAGR through 2031, which makes it the fastest-growing region in the automotive usage-based insurance market. India is an important driver because GPS-linked vehicle tracking requirements in commercial mobility and IRDAI’s allowance for usage-based motor insurance add-ons are helping create a clearer product pathway for pay-linked covers. The automotive usage-based insurance market in Asia-Pacific is also benefiting from smartphone-led distribution and expanding EV data ecosystems, which make it easier for insurers to scale with lighter hardware models first and richer integrations later. South America and the Middle East and Africa remain earlier-stage opportunities, but the automotive usage-based insurance market is opening there as connected-vehicle sales, smart mobility programs, and fleet digitization gradually broaden the base for telematics-linked products.

Competitive Landscape

The automotive usage-based insurance market is fragmented, with traditional insurers, telematics providers, connected-vehicle technology firms, and behavioral analytics specialists competing across different parts of the value chain. While major insurers such as Progressive, State Farm, Allianz, and AXA provide substantial underwriting capacity and market reach, no single company dominates the global market. Competitive advantage is increasingly determined by ownership of telematics infrastructure, behavioral-scoring capabilities, and the ability to transform driving data into more accurate risk assessment and personalized pricing. This trend was reinforced in March 2026 when Cambridge Mobile Telematics secured a USD 350 million strategic investment from TPG's Rise Funds and Allianz X, with participation from State Farm, highlighting the growing strategic importance of behavioral data platforms. In addition, Arity reported in 2026 that its platform covered more than 50 million connected drivers and nearly 3 trillion miles of driving data in the United States, demonstrating the significant data scale required to compete effectively. As a result, competitive differentiation in the automotive usage-based insurance market is increasingly driven by the quality, scale, and analytical value of telematics data rather than by brand strength alone.

Some of the clearest open spaces in the automotive usage-based insurance market sit in commercial micro-fleets, Southeast Asian smartphone-led programs, and EV-linked embedded insurance models that are still early in their rollout cycle. Geotab's Hyundai integration in Europe is one example of how telematics providers are moving directly into OEM data channels to lower friction and improve signal quality for downstream insurance use cases. Another example is Kia Connect's January 2025 partnership with LexisNexis Risk Solutions to integrate Drive Metrics scoring into the Kia consumer mobile app across 27 EU countries and the United Kingdom, thereby embedding risk assessment directly into the OEM's digital environment. The automotive usage-based insurance market is also seeing more work on data fusion and cross-insurer scoring benchmarks, which suggests the next phase of competition will center on interoperability as much as on raw data collection. That is important because the automotive usage-based insurance market will likely reward firms that can translate multiple signal sources into a single underwriting language.

Strategic behavior is also shifting in the automotive usage-based insurance market, as incumbents are increasingly willing to partner with or acquire technology specialists rather than build every component internally. Admiral Group completed the acquisition of connected fleet insurtech Flock in June 2026, strengthening its telematics and commercial motor capabilities and providing a faster route to scale in connected fleet insurance. Progressive's launch of accident response with Cambridge Mobile Telematics in November 2025 is another example, because it extended telematics from pricing into crash detection and automated claims initiation at a meaningful scale. The automotive usage-based insurance market is therefore moving toward a structure where underwriting incumbents, OEM data channels, and telematics intelligence platforms are increasingly interdependent. That makes the automotive usage-based insurance market competitive, but not evenly so, because firms with established data distribution and claims integration already hold a measurable lead.

Automotive Usage-Based Insurance Industry Leaders

Progressive Corporation

Allstate Corporation

State Farm Mutual Automobile Insurance Company

Liberty Mutual Insurance

AXA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Admiral Group completed the acquisition of connected fleet insurtech Flock, bringing its AI-powered telematics and risk-assessment platform into Admiral's commercial motor business, strengthening the insurer's data-driven fleet insurance capabilities.

- April 2026: Admiral Group and Flock launched a telematics-driven haulage fleet insurance product in the United Kingdom, and Flock reported that fleets in its connected risk management programs recorded a 10% reduction in claims frequency, alongside lower downtime and maintenance costs.

- March 2026: Cambridge Mobile Telematics received a USD 350 million strategic investment led by TPG's Rise Funds and Allianz X, with State Farm participating, to accelerate AI-driven road safety platforms and the Universal Driving Score initiative across global markets

- March 2026: Geotab launched a native OEM telematics integration for Hyundai vehicles across Europe, enabling hardware-free fleet telematics data transmission and eliminating aftermarket device installation costs

Global Automotive Usage-Based Insurance Market Report Scope

| Pay-As-You-Drive (PAYD) |

| Pay-How-You-Drive (PHYD) |

| Manage-How-You-Drive (MHYD) |

| Dongle |

| Black Box |

| Embedded |

| Smartphones |

| Passenger Cars |

| Commercial Vehicles |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Pay-As-You-Drive (PAYD) | |

| Pay-How-You-Drive (PHYD) | ||

| Manage-How-You-Drive (MHYD) | ||

| By Solution | Dongle | |

| Black Box | ||

| Embedded | ||

| Smartphones | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected growth path for automotive usage-based insurance through 2031?

The automotive usage-based insurance market is expected to grow from USD 76.59 billion in 2026 to USD 162.12 billion by 2031, at a 16.18% CAGR over 2026-2031.

Which region leads global adoption of telematics-linked auto coverage?

North America led with 39.84% share in 2025, supported by mature telematics infrastructure and large insurer programs such as Progressive Snapshot.

Which pricing model currently leads, and which one is growing fastest?

Pay-How-You-Drive led with 44.76% share in 2025, while Manage-How-You-Drive is projected to grow fastest at 22.39% CAGR through 2031.

Why are embedded telematics solutions gaining ground over dongles?

Embedded solutions are growing at 23.81% CAGR because OEM-linked connectivity removes installation friction and gives insurers richer vehicle-level data than many standalone devices.

Why are commercial fleets becoming more important in this space?

Commercial Vehicles are projected to grow at 19.74% CAGR, and telematics-enrolled fleets have shown claims frequency reductions of 10% to 19% within 18 months in cited industry deployments.

What is the biggest challenge slowing wider adoption?

Consent and compliance remain the main obstacles, because many drivers are open to UBI in principle but still hesitate to share data, and rules differ across states and countries.

Page last updated on: