Europe Car Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 129.68 Billion |

| Market Size (2026) | USD 133.99 Billion |

| Market Size (2031) | USD 157.92 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

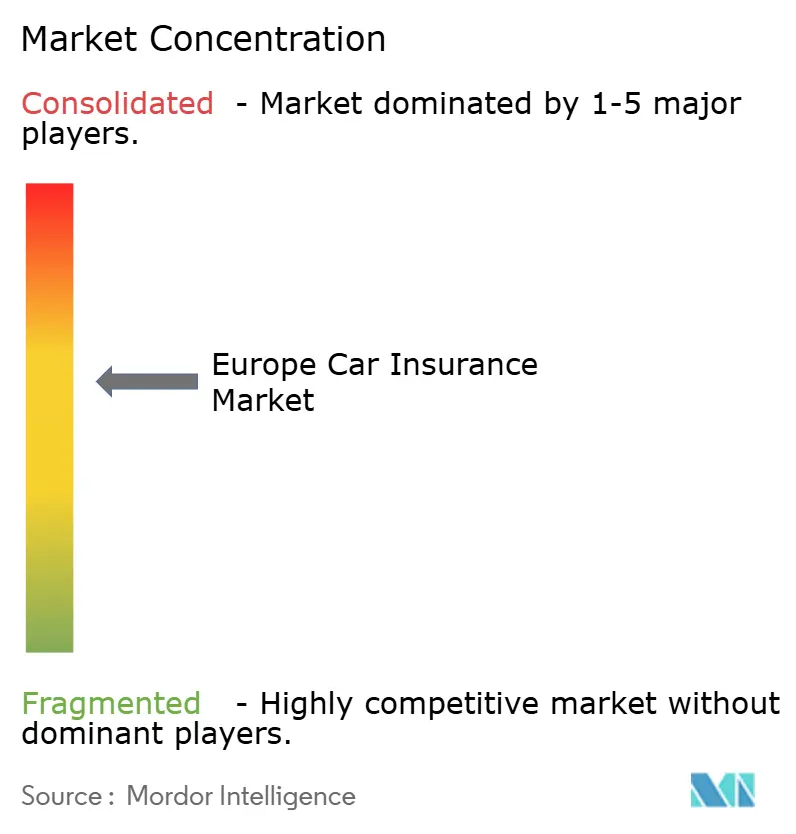

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Car Insurance Market Analysis by Mordor Intelligence

Europe car insurance market size in 2026 is estimated at USD 133.99 billion, growing from 2025 value of USD 129.68 billion with 2031 projections showing USD 157.92 billion, growing at 3.32% CAGR over 2026-2031. The expansion demonstrates a mature regulatory environment that enforces mandatory third-party liability, while telematics adoption, electrification of fleets, and artificial-intelligence-powered underwriting jointly reshape premium structures. Rising penetration of Advanced Driver Assistance Systems (ADAS) and battery-electric vehicles elevates average claim severity, prompting carriers to upgrade actuarial models and negotiate preferred-pricing agreements with certified repair networks. At the same time, direct-to-consumer digital channels are expanding rapidly, compressing acquisition costs and channeling more parametric data into pricing engines that refine risk segmentation. Ongoing consolidation—exemplified by Ageas’s GBP 1.295 billion purchase of esure—supplies scale advantages in reinsurance, analytics, and procurement that counteract margin pressure from comparison sites and regulatory rate caps.

Key Report Takeaways

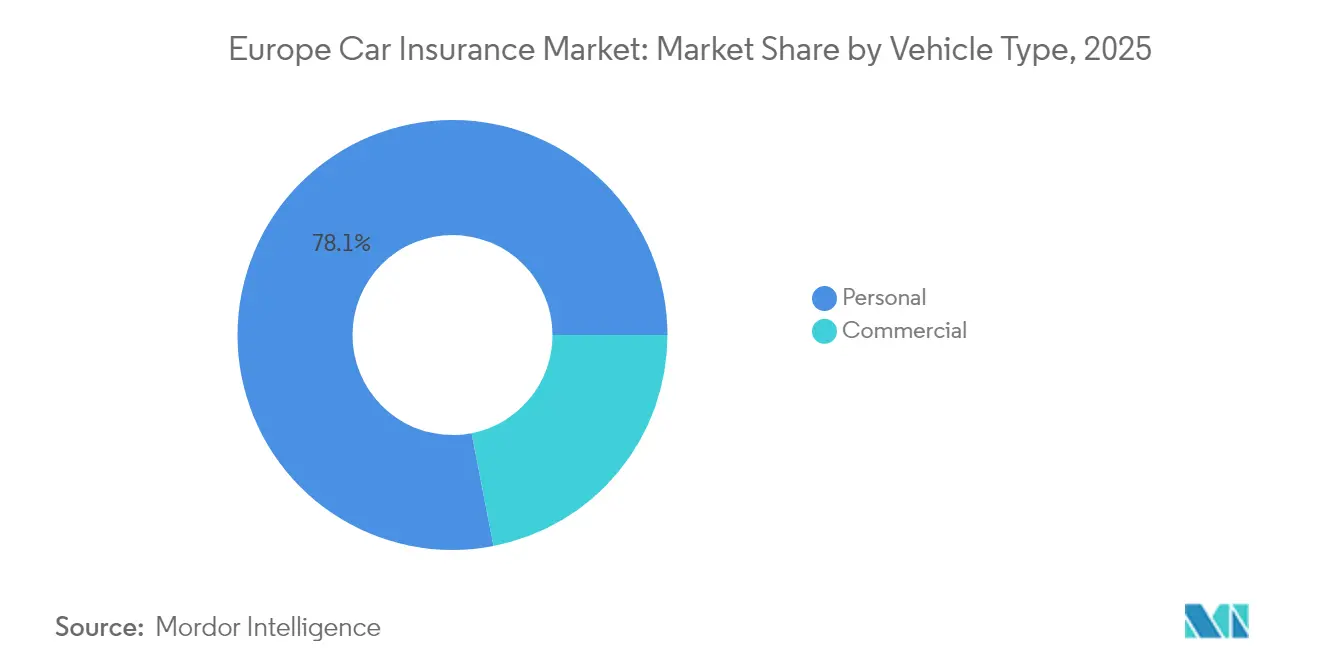

- By vehicle type, personal policies accounted for 78.06% of the Europe car insurance market share in 2025, while commercial coverage is projected to post the fastest growth, advancing at a 4.63% CAGR through 2031.

- By insurance type, third-party liability provided 60.72% of the Europe car insurance market size in 2025; however, comprehensive plans are set to expand at an 8.05% CAGR over 2026-2031.

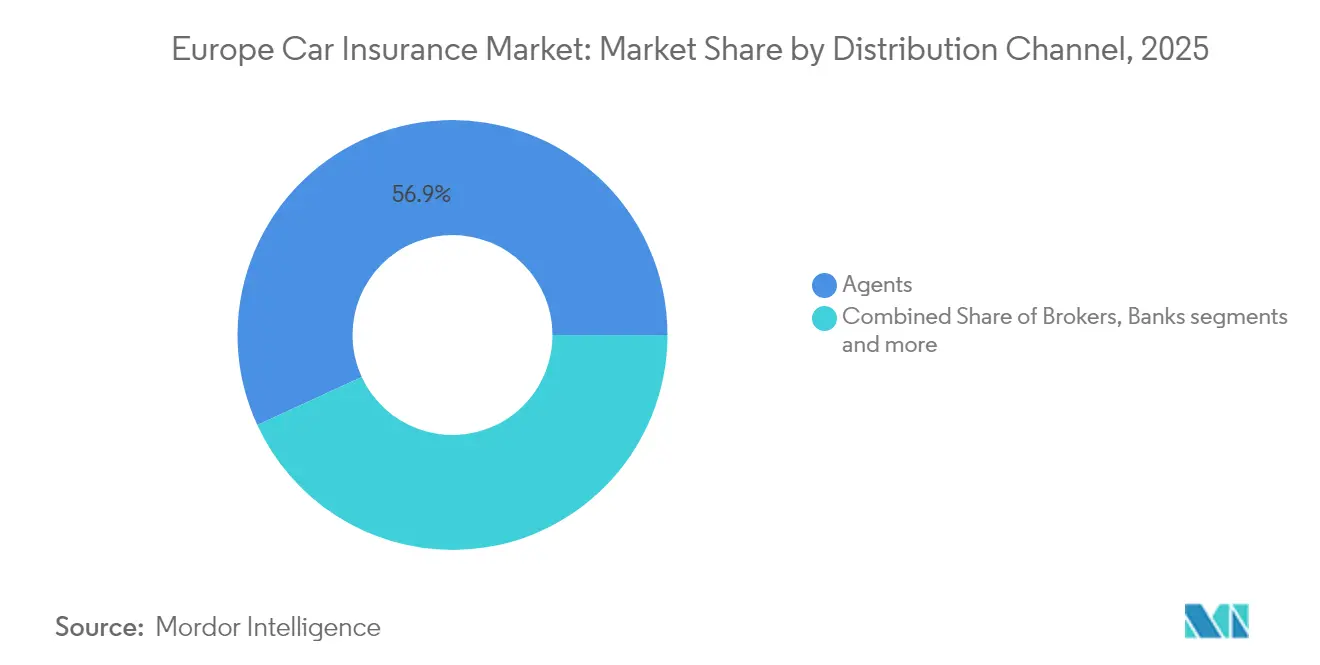

- By distribution channel, agent networks controlled 56.88% revenue share in 2025, although direct online platforms are forecast to record a 5.12% CAGR during the same period.

- By country, the United Kingdom held 22.33% of the Europe car insurance market size in 2025, whereas Italy is expected to register the highest CAGR at 5.39% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe operates as part of an interconnected international environment rather than as a self-contained unit. The car insurance market research by Mordor Intelligence places together all major regional developments across the globe within that wider frame.

Europe Car Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-wide compulsory motor liability law | +0.8% | All EU member states | Long term (≥ 4 years) |

| ADAS-linked repair cost inflation | +1.2% | Germany, United Kingdom, France, BENELUX, Nordics | Medium term (2-4 years) |

| Growth of personal leasing and PCP contracts | +0.6% | United Kingdom, Germany, Netherlands, Southern Europe | Medium term (2-4 years) |

| Expanding vehicle parc and aging fleet | +0.4% | Eastern and Southern Europe | Long term (≥ 4 years) |

| Rapid adoption of telematics-based usage-based insurance | +0.7% | Italy, United Kingdom, Germany, Nordics | Short term (≤ 2 years) |

| Digital claims processing and AI-driven underwriting | +0.5% | All European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU-wide Compulsory Motor-Liability Law Sustains Baseline Demand

European motor insurance relies on a legal framework that obligates every vehicle owner to hold third-party liability cover, ensuring the Europe car insurance market remains insulated from macroeconomic cycles. The 2024 Insurance Recovery and Resolution Directive formalized failure-resolution mechanisms, boosting consumer confidence and curbing systemic risk across borders. Harmonized enforcement under the European Insurance and Occupational Pensions Authority (EIOPA) sustains renewal volumes even when disposable incomes tighten, because non-compliance can lead to fines, vehicle impoundment, or registration suspension. This consistent policy base allows insurers to scale digital investments, knowing core premium flows are predictable. However, rate-setting freedom is curtailed as several regulators condition approval on social objectives, such as affordability for low-income drivers, which prevents carriers from passing the full burden of claims inflation through to customers. To offset this constraint, many insurers deploy usage-based products that maintain regulatory compliance while rewarding safer behavior with lower pricing bands. The resulting alignment of incentives supports both road-safety goals and stable premium growth[1]European Commission, “Intelligent Transport Systems – Road – Action Plan and Directive,” ec.europa.eu.

ADAS Technology Mandates Drive Claims Cost Inflation

Mandatory ADAS features introduced under the General Safety Regulation 2 for all new cars from July 2024 materially increased repair complexity and labor times. Sophisticated sensors housed behind bumpers or windshields require recalibration after even minor collisions, sending average repair invoices 20-30% higher than on pre-regulation vehicles. German insurers reported combined underwriting losses of more than EUR 3 billion in 2023, with HUK-Coburg alone posting a EUR 500 million deficit attributed largely to ADAS-related spare-part costs[2]Fleet Europe, “Car Insurance up 20% in Germany Due to Expensive Repairs,” fleeteurope.com. The expense is compounded by the limited availability of manufacturer-certified technicians, elongating key-to-key cycle times and pushing up courtesy-car costs. While collision frequency is starting to decline due to automatic emergency braking, the higher severity of each incident offsets these gains, forcing actuaries to recast frequency-severity assumptions in pricing models. Insurers with direct repair-network agreements negotiate bulk discounts on lidar modules and camera units, clawing back a portion of the incremental outlay. Others experiment with refurbished sensors and aftermarket calibration rigs to preserve loss-ratio targets without breaching type-approval standards.

Personal Contract Purchase Growth Expands Comprehensive Coverage Demand

Personal Contract Purchase (PCP) and leasing arrangements represented more than 40% of new passenger-car registrations in the United Kingdom and Germany during 2024. Finance companies typically obligate borrowers to secure comprehensive insurance that safeguards the vehicle’s residual value throughout the lease term, driving a structural increase in premium per policy. As more consumers prefer lower upfront commitments and predictable monthly costs, embedded insurance at the point of sale has become a primary acquisition channel for carriers. Insurers that forge exclusive partnerships with captive finance arms convert these long-term contracts into high-persistence revenue streams, enjoying lower churn than in traditional renewal cycles. In parallel, leasing penetration among last-mile delivery fleets has expanded rapidly, requiring bespoke coverages that incorporate replacement-vehicle guarantees, roadside EV charging, and battery-health monitoring. The higher average value of leased assets magnifies insured sums, amplifying the Europe car insurance market’s premium base. Yet underwriting such assets demands granular data on driver behavior, mileage patterns, and battery degradation, pushing insurers to invest in advanced telematics and predictive maintenance analytics to protect margins.

Vehicle Parc Expansion and Aging Demographics Support Volume Growth

Europe’s vehicle fleet surpassed 250 million registered units in 2024 and continues to grow at roughly 1.5-2% annually, fueled by economic convergence in Eastern Europe and replacement demand in mature economies. Simultaneously, the average age of vehicles has stretched to more than 12 years as improved reliability encourages owners to postpone new-car purchases. Older vehicles generate higher claim frequencies because aging mechanical parts fail more often, and they require more frequent roadside assistance, thereby guaranteeing a steady stream of policies despite sluggish new-vehicle sales. Insurers capitalize by bundling ancillary services—towing, glass repair, tire replacement—that create fee income while improving customer stickiness. Commercial vehicle demand also remains buoyant: e-commerce growth means urban delivery fleets expand each year, and these operators often select fleet policies that cover diverse risks, from cargo damage to driver liability. Additionally, demographic shifts reveal that aging populations prefer private transport over public alternatives, maintaining vehicle ownership rates among retirees. As a result, policy volumes rise even where average premiums remain stable, contributing to consistent top-line growth for the Europe car insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price wars ignited by comparison sites | -0.9% | United Kingdom, Netherlands, Germany | Short term (≤ 2 years) |

| Regulatory caps and bonus-malus limits on premium hikes | -0.7% | France, Italy, Spain, and select Eastern Europe | Medium term (2-4 years) |

| Persistently low investment yields | -0.4% | EU-wide | Long term (≥ 4 years) |

| Soft new-car sales in major markets | -0.3% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Competition Through Comparison Platforms Pressures Margins

Digital aggregators empower shoppers to obtain more than 50 quotes within seconds, homogenizing products and encouraging an almost mechanical focus on the lowest price. In the United Kingdom, average personal-car premiums fell 17% during 2025, the steepest annual contraction since 2014, as insurers slashed rates to hold share. The churn rate approached 40%, forcing carriers to pump marketing budgets into retention emails, auto-renewal incentives, and app-based loyalty perks that dilute net acquisition savings. Smaller underwriters with limited brand recognition often accept loss-making business in hopes of cross-selling ancillary covers, a tactic that raises long-term solvency concerns. The transparency also exposes historical pricing inequities; regulators have intervened to outlaw “price walking,” narrowing the gap between new-business and renewal quotes and compressing lifetime-value calculations. Larger insurers leverage machine-learning price-optimization engines, but the arms race raises IT costs, eroding margin advantages. Unless carriers can innovate beyond price—through bundled ADAS calibration services or EV-specific warranties, the comparison-site dynamic will remain a formidable drag on the Europe car insurance market’s profitability.

Regulatory Pricing Constraints Limit Premium Adjustment Flexibility

Several European authorities closely monitor premium revisions, seeking a balance between insurer solvency and consumer affordability. France’s 2025 cap of 6% on motor-premium increases, despite 8% repair-cost inflation, exemplifies the tension. Bonus-malus frameworks, intended to reward accident-free driving, restrict surcharges on high-risk motorists, compelling cross-subsidization that blurs actuarial fairness. Gender-neutral and age-neutral rating policies remove historically predictive variables, further challenging loss-cost alignment. In Spain and Italy, antitrust watchdogs review rate filings to prevent perceived “collective hikes,” extending approval timelines and injecting uncertainty into pricing cycles. The result is asymmetric risk transfer: insurers shoulder inflation spikes but must wait months or years to recoup via higher rates. To maintain earnings stability, many carriers now hedge claims inflation with structured reinsurance, yet this pushes up ceded-premium ratios. Together, these supervisory pressures force strategic reallocation toward risk-selection technology and cost-efficiency drives, shaping competitive behavior across the Europe car insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Fleet Electrification Redefines Commercial Risk Profiles

Commercial vehicles generated only 21.94% of written premium in 2025, yet are forecast to expand faster than any other class, clocking a 4.63% CAGR through 2031 as Europe accelerates toward net-zero targets. EU heavy-duty CO₂ regulations mandate a 45% emissions cut by 2030, spurring logistics operators to acquire battery-electric vans priced up to 80% higher than diesel equivalents. Higher asset values translate to larger insured sums, while battery-fire risk, charger-downtime exposure, and limited repair-shop familiarity increase loss volatility. Insurers respond by packaging risk-management services such as thermal-runaway monitoring, mobile charging, and scheduled battery diagnostics, capturing fee income alongside premiums. Fleet managers appreciate the holistic offerings, bolstering renewal affinities that offset lower margins in commoditized personal lines.

Personal policies sustained 78.06% of the Europe car insurance market in 2025, underpinned by mandatory cover laws and stable vehicle-ownership rates across mature economies. Nevertheless, personal lines face relentless price competition; average U.K. personal-motor premiums compressed 17% in 2025 due to aggregator influence. Insurers mitigate attrition by introducing pay-per-mile products that entice urban drivers who clock limited mileage. Telematics-enabled young-driver programs record accident reductions that support differentiated pricing, maintaining relevance even under stringent rate-approval regimes. Over time, the interplay of electrification and usage-based pricing will reshape personal-line profitability ladders, pushing analytics-savvy carriers to the forefront of the Europe car insurance market.

By Insurance Type: Complexity Fuels Shift Toward Comprehensive Policies

Third-party liability constituted 60.72% of premium income in 2025, upheld by compulsory-insurance statutes that deliver a predictable revenue floor for underwriters. However, comprehensive contracts are expanding at an 8.05% CAGR because modern vehicles integrate expensive electronics and battery systems that can push claim totals well above EUR 10,000 even after low-speed collisions. Finance houses involved in PCP deals require borrowers to carry gap and comprehensive coverage to safeguard residual value, embedding these richer policies into loan documentation. Cyber-risk endorsements, once niche, gain traction as over-the-air software updates and vehicle-to-infrastructure communications raise hacking concerns, enhancing the coverage suite in comprehensive plans.

Insurers exploiting this shift bundle glass replacement, roadside assistance, and mobility-as-a-service vouchers that appeal to urban consumers, lifting non-premium revenue. Their ability to cross-sell add-ons boosts average revenue per user, offsetting strict liability-rate caps. Furthermore, early adopters of comprehensive-EV products command premium loadings that cushion the claims-cost spike associated with battery fires or charger damage. Consequently, comprehensive policies will continue to erode the dominance of liability-only contracts, gradually increasing their proportional weight in the Europe car insurance market.

By Distribution Channel: Multichannel Models Balance Efficiency and Expertise

Agent networks retained 56.88% of gross written premium in 2025, illustrating the enduring value of personalized advice for high-complexity risks and multi-vehicle households. Agents excel at explaining nuanced coverages, navigating claim disputes, and orchestrating mid-term policy adjustments—services that purely digital interfaces sometimes mishandle. Yet direct online channels are accelerating at a 5.12% CAGR, as smartphone-native interfaces finalize quotes in under five minutes and embed payment plans that sync with digital-wallet ecosystems. Zurich’s EUR 10 million investment in Ominimo underscores incumbent recognition that AI-driven pricing engines can penetrate new geographies with lean cost bases.

Brokers remain critical in commercial lines, where fleet risks require bespoke wordings on trailers, cargo, and multinational driver pools. Bank-assurance channels leverage existing checking and savings relationships to cross-sell motor covers, though their share is slowly eroding as fintech partners layer in white-label policies at checkout. Insurers increasingly adopt omnichannel strategies, offering policyholders the freedom to begin a quote online, finalize through a call center, and lodge a claim via an app—creating a seamless journey that strengthens loyalty. Successful carriers optimize channel economics by steering low-touch renewals to self-service portals while reserving human expertise for complex risk consultations, preserving margin across the Europe car insurance market.

Geography Analysis

The United Kingdom dominated the Europe car insurance market with a 22.33% share in 2025, sustained by high vehicle density, sophisticated telematics infrastructure, and a deeply competitive distribution landscape. Ageas’s acquisition of esure forms a top-three personal-lines entity, unlocking scale benefits in marketing expenditure and repair-network negotiations while diversifying distribution across agent, broker, and direct channels. Despite maturity, the U.K. market confronts stringent Financial Conduct Authority rules against dual-pricing, squeezing renewal profitability and forcing carriers to sharpen cost-reduction programs and invest in machine-learning price engines.

Germany ranks among the continent’s largest motor markets but wrestles with profitability. Average premiums climbed 20% in 2024 as insurers attempted to counter ADAS-driven repair bills, yet many carriers still produced negative underwriting margins. The industry lobbies for broader access to OEM diagnostic data to spur competition in parts supply, a move it claims could cut claim costs by 7-9%. France presents a contrasting dynamic: regulators capped 2025 premium hikes at 6%, yet repair-cost inflation broke 8%, intensifying the hunt for operational efficiencies. French carriers deploy AI triage tools to reduce average bodily-injury settlement cycles, freeing reserves and bolstering solvency ratios. Italy provides the fastest growth trajectory with a 5.39% CAGR forecast through 2031, powered by world-leading telematics penetration exceeding 30% of active policies. AXA’s planned acquisition of digital-native Prima Assicurazioni signals confidence in this data-rich market where insurers can refine risk pricing with sub-meter driving analytics. Spain, BENELUX, and the Nordics offer mid-single-digit growth under supportive innovation frameworks, though their smaller absolute premium pools cap upside scale. Eastern Europe remains underinsured relative to GDP, and as disposable incomes climb, vehicle ownership and premium volumes are set to rise, albeit from a lower base and with higher regulatory complexity. Collectively, geographic nuances require localized product design, yet pan-European players exploit cross-border scale in reinsurance, IT platforms, and procurement to maintain competitive advantage across the Europe car insurance market.

The car insurance market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Asia, along with detailed country-level analysis for France, Germany, Russia, United Kingdom, Japan, China, India, and Brazil.

Competitive Landscape

Europe’s motor segment exhibits moderate concentration, with the five largest insurers capturing roughly two-thirds of premiums, yet none exceeding 10% individually. Generali broadened its footprint via the EUR 2.3 billion Liberty Seguros acquisition, strengthening its position in Iberia and creating claim-handling synergies. Allianz spearheaded a EUR 3.5 billion consortium purchase of Viridium, harvesting back-office economies of scale and unlocking cross-sell potential into motor from closed life-policyholder bases. Zurich’s minority stake in Ominimo exemplifies strategic ventures into agile insurtechs to fast-track AI underwriting capabilities and reach digitally savvy customers at lower acquisition costs.

Technological differentiation has emerged as the primary battleground: carriers race to deploy computer-vision claims tools, predictive fraud analytics, and behavioral pricing engines. Those with proprietary telematics datasets command competitive moats that deter pure-price entrants. At the same time, OEMs, rental platforms, and mobility-as-a-service providers test embedded insurance models, threatening to disintermediate traditional underwriters unless they partner or white-label offerings. Incumbents counter by bundling EV battery warranties, cyber-intrusion protection, and charger-breakdown services, stretching product scope beyond conventional indemnity.

Cost discipline remains paramount. Post-merger integration teams focus on consolidating IT systems, renegotiating parts contracts, and harmonizing reinsurance treaties to realize synergies. Talent shortages in data science and cybersecurity lead insurers to establish satellite hubs in tech-center cities like Berlin and Barcelona to attract specialists. Climate-related regulatory pressure also intensifies capital-allocation scrutiny, spurring investment in scenario-analysis tools that quantify flood and heat-event exposure for vehicle fleets. As these forces converge, carriers capable of balancing technology investments, capital efficiency, and customer experience will outperform peers in the Europe car insurance market.

Europe Car Insurance Industry Leaders

Allianz SE

AXA SA

Generali Group

Zurich Insurance Group

MAPFRE SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: AXA disclosed intentions to acquire Prima Assicurazioni to strengthen its foothold in Italy’s high-growth telematics segment. The move adds 2 million policies to AXA’s Italian book and provides access to Prima’s proprietary driver-scoring algorithms that enable granular risk segmentation.

- June 2025: Allianz, in partnership with BlackRock and T&D Holdings, agreed to acquire Viridium Group for approximately EUR 3.5 billion. The consortium aims to integrate Viridium’s closed-book management expertise with Allianz’s digital claims capabilities, opening avenues for motor-policy cross-selling to a legacy life-insurance customer base.

- April 2025: Ageas finalized terms to buy esure from Bain Capital for GBP 1.295 billion, establishing a top-three personal-lines insurer in the United Kingdom. Integration plans call for unified cloud-based policy administration and expanded usage-based offerings to leverage esure’s strong aggregator presence.

- April 2025: Zurich Insurance Group purchased a minority stake in Hungarian insurtech Ominimo, valuing the startup at EUR 200 million. The partnership will fast-track the rollout of AI-priced motor products across Central and Eastern Europe, beginning with Poland in late 2025.

Europe Car Insurance Market Report Scope

Car insurance is a type of insurance that provides cover for loss or damage to the car. It helps to mitigate monetary harms due to accidents causing damage to the cars. Europe's car insurance market is segmented by coverage, application, distribution channel, and by geography. By coverage, the market is segmented into third-party liability coverage and collision/comprehensive/other optional coverage. By application, the market is segmented into personal vehicles and commercial vehicles. By distribution channel, the market is segmented into individual agents, brokers, banks, online, and other distribution channels. Other distribution channels include financial institutions other than banks, phone marketing, and mail marketing. By geography, the market is segmented into Germany, the UK, France, Switzerland, and the Rest of Europe. The report also covers the market sizes and forecasts for the European car insurance market in value (USD) for all the above segments.

| Personal |

| Commercial |

| Third-Party |

| Comprehensive |

| Direct |

| Agents |

| Brokers |

| Banks |

| Other Distribution Channels |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX |

| NORDICS |

| Rest of Europe |

| By Vehicle Type (Value) | Personal |

| Commercial | |

| By Insurance Type (Value) | Third-Party |

| Comprehensive | |

| By Distribution Channel (Value) | Direct |

| Agents | |

| Brokers | |

| Banks | |

| Other Distribution Channels | |

| By Country (Value) | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe car insurance market today?

The Europe car insurance market size stands at USD 133.99 billion in 2026 and is forecast to reach USD 157.92 billion by 2031.

What factors are driving premium growth?

Rising ADAS repair costs, fleet electrification, and wider adoption of telematics-based usage-based insurance combine to lift average premiums despite regulatory price caps.

Which policy type is expanding fastest?

Comprehensive coverage is growing at an 8.05% CAGR as owners look to protect high-value sensors, batteries, and connected-vehicle systems.

Why is Italy outpacing other markets?

Italy’s telematics penetration exceeds 30%, enabling granular risk pricing that delivers both lower customer premiums and healthier loss ratios for insurers, supporting a 5.39% CAGR.

How are comparison sites affecting insurers?

Aggregators intensify price competition, leading to a 17% fall in average U.K. personal-motor premiums in 2025, which pressures underwriting margins and spurs cost-cutting programs.

What emerging covers are insurers offering for EVs?

Policies increasingly bundle battery-fire protection, mobile charging assistance, and cyber-intrusion safeguards to address the unique risks of electric vehicles.

Page last updated on: