India Car Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

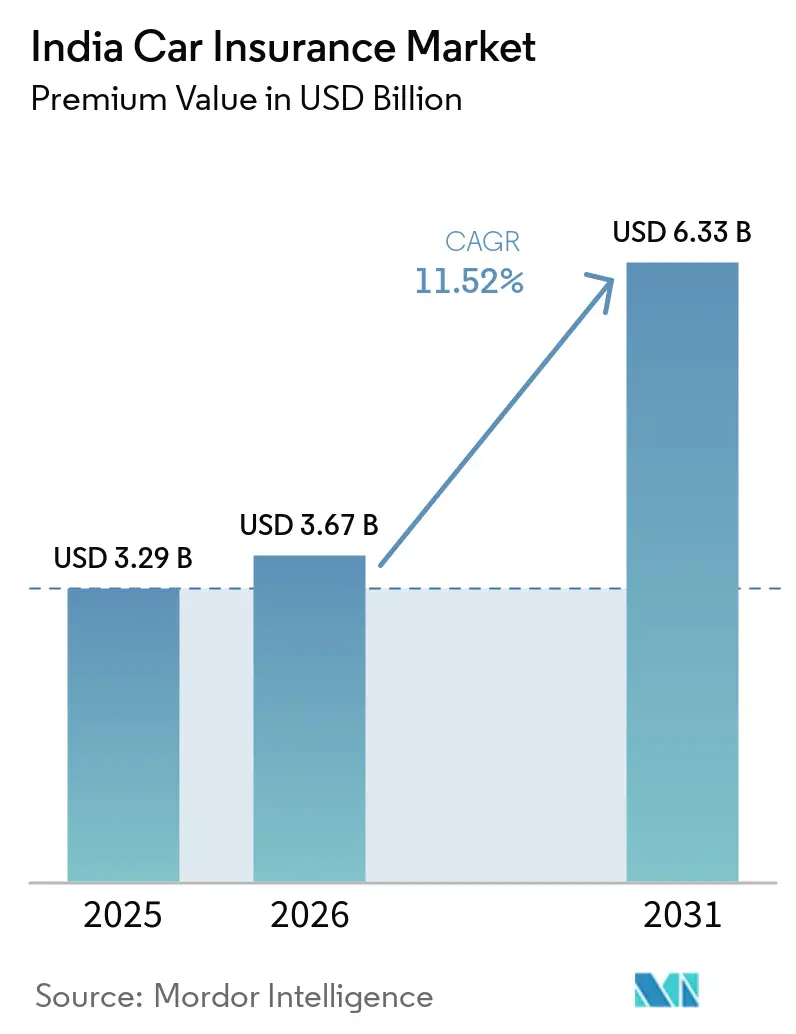

| Base Year Market Size (2025) | USD 3.29 Billion |

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 6.33 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Car Insurance Market Analysis by Mordor Intelligence

The India Car Insurance Market size in terms of premium value was valued at USD 3.29 billion in 2025 and is estimated to grow from USD 3.67 billion in 2026 to reach USD 6.33 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

Robust new-vehicle registrations after GST cuts, mandatory long-term third-party policies, and a sweeping shift toward digital distribution are expanding the India car insurance market. Demand for comprehensive coverage is rising as extreme-weather events expose the limits of basic liability products, while usage-based pricing wins regulatory support. Competitive strategies now center on telematics, artificial intelligence, and partnerships with automakers, especially in electric vehicle (EV) segments. Price competition and flat third-party tariffs weigh on underwriting margins, yet sustained vehicle sales and digital reach keep the India car insurance market on a firm growth path.

Key Report Takeaways

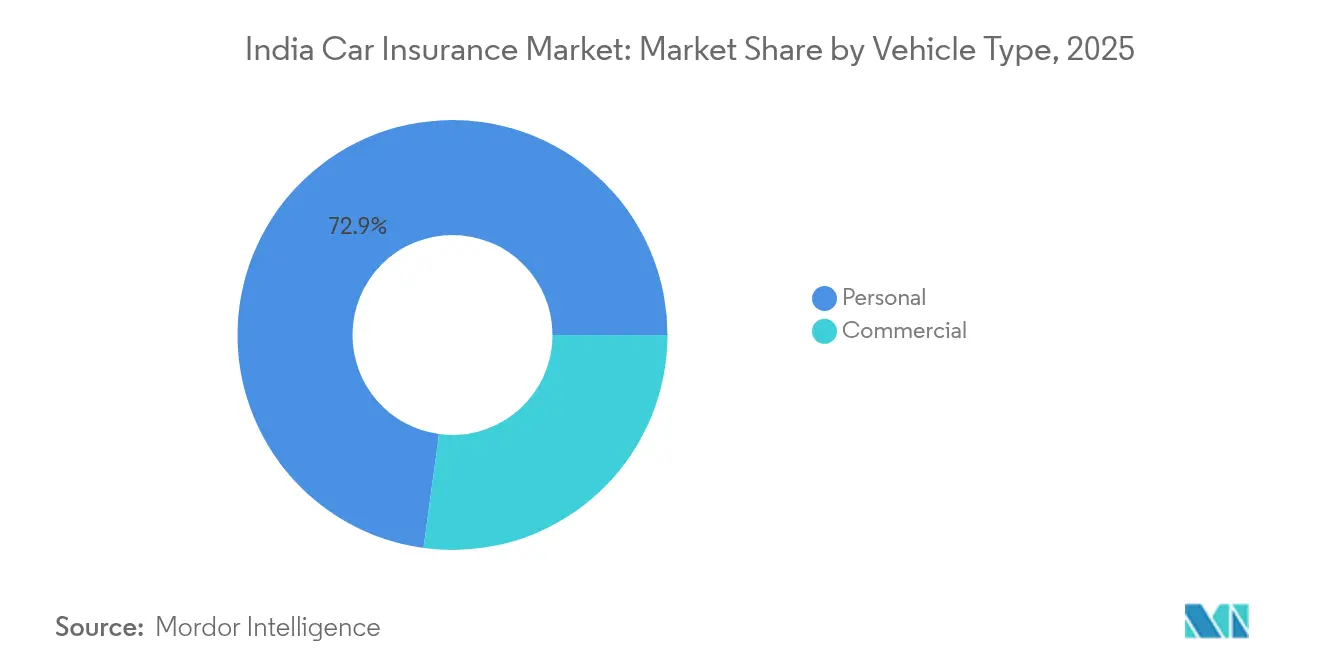

- By vehicle type, personal vehicles held 72.85% of the India car insurance market share in 2025, while commercial vehicles are advancing at an 11.34% CAGR through 2031.

- By insurance type, third-party coverage accounted for a 53.55% share of the India car insurance market size in 2025; comprehensive coverage is set to grow at a 15.12% CAGR to 2031.

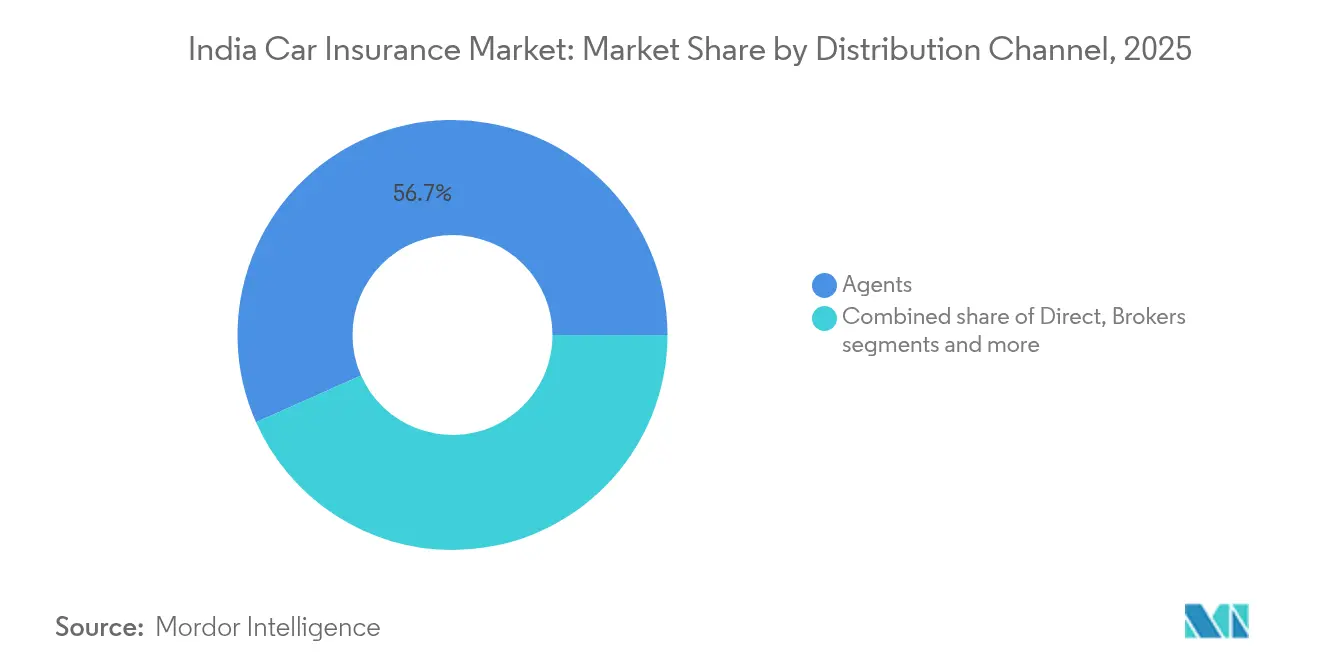

- By distribution channel, agents controlled a 56.65% share of the India car insurance market size in 2025, whereas direct digital channels are expanding at an 18.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with India being one of the contributors. Our global car insurance market size represents that cumulative total.

India Car Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong rebound in new-vehicle registrations post-FY24 GST cuts | +2.8% | National, early gains in urban centers and Tier-2 cities | Short term (≤ 2 years) |

| Mandatory long-term third-party cover & proposed TP tariff hike | +1.9% | National | Medium term (2-4 years) |

| Rapid shift to digital/aggregator distribution platforms | +2.1% | Urban and semi-urban markets | Medium term (2-4 years) |

| Telematics-based PAYD/PHYD products are gaining IRDAI sandbox approval | +1.7% | Metro cities and fleet corridors | Long term (≥ 4 years) |

| EV-specific premium-financing bundles from OEM–insurer tie-ups | +1.8% | Metro cities & EV clusters | Long term (≥ 4 years) |

| AI-driven touchless claims reduce loss-adjustment expenses | +1.4% | Urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Vehicle Registration Recovery Drives Premium Volume Growth

Post-FY24 GST cuts lowered purchase prices on entry-level cars, sparking a sharp FY25 jump in passenger-car registrations. Every new vehicle must carry at least third-party cover, so the sales surge converts straight into incremental policies and premium inflows. Gains are most visible in Tier-2 and Tier-3 cities where affordability had stalled insurance uptake and where dealer-assisted financing now bundles multi-year covers by default. Insurers are layering accessories, zero-depreciation, and return-to-invoice add-ons to capture the expanding base and lift average ticket size. Robust retail demand is expected to persist through 2026 as pandemic-era replacement cycles normalize and consumer sentiment improves. Rising showroom traffic is therefore translating into a durable premium tailwind for the India car insurance market.

Digital Distribution Platforms Reshape Customer Acquisition Dynamics

Aggregator portals and insurer apps give buyers instant quotes, video-KYC issuance, and self-service claims, winning trust among digitally native millennials. Policies processed online overtook agent-sourced comprehensive sales in metro areas during FY25, signaling a decisive tilt toward transparent, price-discovery journeys. To defend retention, incumbents are arming agents with mobile CRM tools and embedding click-to-call advisory widgets inside their sites, blending personal advice with digital speed. IRDAI’s e-insurance account framework and mandated policy document standardization further favor online channels by cutting paperwork and audit costs. Early evidence shows digital leads are 35% cheaper to acquire than branch walk-ins, strengthening margin upside. Consequently, digital reach has become a core success factor in the India car insurance market.

Telematics and Usage-Based Insurance Gain Regulatory Momentum

IRDAI sandbox approvals in 2024 legitimized pay-as-you-drive and pay-how-you-drive models, enabling premiums to mirror real-world mileage and driving behavior. Pilot cohorts report 15-20% savings for safe drivers and commercial fleets installing on-board devices, validating consumer appetite for fair pricing. Real-time acceleration, braking, and cornering data feed machine-learning engines that refine underwriting and speed up fraud detection. Smartphone-based telemetry cuts hardware costs, broadening the addressable base beyond high-end cars. Privacy safeguards such as opt-in data-sharing, encryption, and policyholder dashboards are easing adoption anxieties. As device prices fall, telematics penetration is set to spread from metros to state highways, deepening segmentation opportunities inside the India car insurance market[1]IRDAI, “Regulatory Sandbox Approvals 2024,” irdai.gov.in.

Electric Vehicle Insurance Ecosystem Develops Through OEM Partnerships

Automakers now co-design policies covering battery degradation, software glitches, and public-charger liabilities, filling gaps left by legacy motor products. EV-centric bundles wrap financing, extended warranty, and roadside assistance, smoothing the total cost of ownership for ride-hailing fleets and personal buyers alike. Access to real-time battery-health telemetry enables underwriters to fine-tune risk and keep premiums competitive despite high part costs. Collaboration also secures priority access to OEM-approved repair networks, cutting average turnaround time by 25%. Government FAME-II subsidies and state EV mandates further widen the insured base, drawing fresh capital into EV underwriting pools. Such partnerships accelerate EV uptake while unlocking new premium streams for the India car insurance market[2]Tata Motors, “EV Commercial Vehicle Insurance Collaboration,” tatamotors.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flat TP tariff revision in FY25 is hurting premium growth | −1.4% | National | Short term (≤ 2 years) |

| Price-led competition compressing motor own-damage margins | −0.9% | Urban insurer-dense markets | Medium term (2-4 years) |

| Parts inflation from EV battery imports is raising claim severity | −1.2% | Metro cities & EV clusters | Medium term (2-4 years) |

| High court backlogs are slowing third-party claim settlement | −0.8% | National, higher in major states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stagnant Third-Party Tariff Rates Constrain Revenue Growth

Third-party liability premiums have remained frozen since FY22 while medical inflation and tribunal awards march upward, squeezing top-line growth. Industry combined ratios for TP books now exceed 120%, forcing carriers to cross-subsidize losses with profits from own-damage and investment income. Several rounds of actuarial submissions to IRDAI advocating a 10-15% tariff hike remain under review, prolonging uncertainty. Smaller insurers with heavy motor portfolios face solvency pressure and may curtail product innovation until relief arrives. Prolonged margin compression risks deterring fresh capital inflows and could slow technological upgrades essential for customer experience. Without an imminent tariff revision, the India car insurance market may witness consolidation as weaker players seek scale partners[3]IRDAI, “Motor Third-Party Tariff Review Note 2025,” irdai.gov.in.

Intense Price Competition Erodes Underwriting Discipline

Aggregator comparison screens rank quotes by premium, nudging buyers toward the cheapest option and igniting a race to the bottom. New entrants leverage venture backing to undercut incumbents, while established brands discount add-ons to defend their renewal books. Although solvency norms impose guardrails, aggressive cashback offers and festival-season flash sales persist in metro markets where switching costs are minimal. Over time, chronic under-pricing threatens reserve adequacy, attracting closer regulatory scrutiny and potential rate-floor mandates. The margin squeeze is prompting carriers to seek alternative revenue via ancillary services such as roadside assistance and warranty extensions. Unless pricing discipline returns, profitability across the India car insurance market will remain under pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Policies Outpace Personal Lines Growth

Commercial vehicle premiums grew faster than personal lines in FY25, supported by e-commerce logistics expansion and rising goods-movement demand. The segment’s 11.34% projected CAGR positions it as a key volume engine for the India car insurance market. Fleet owners embrace telematics to cut accident frequency and unlock premium rebates, bolstering adoption. AI-assessed risk scores consider driver behavior, load types, and route congestion, refining policy pricing. Leasing firms bundle coverage within operating contracts, widening penetration in light-commercial sub-segments. Second-hand truck sales channels are now offering micro-tenure covers to address financing tenure mismatches, an innovation strengthening growth prospects.

Personal vehicles still contribute the largest slice, retaining 72.85% of the India car insurance market share in 2025, owing to steady car ownership growth among middle-income households. Urban buyers increasingly opt for add-ons like engine-protect and zero-depreciation covers, lifting average ticket sizes. Two-wheeler sub-lines face lapsation risk due to informal cash-use patterns, prompting insurers to roll out low-premium, multi-year products. Digital claims tracking apps raise satisfaction scores, aiding renewal conversions. Yet, slowing metro sales and premium discounting temper growth, making diversification into Tier-2 regions crucial for sustaining the India car insurance market.

By Insurance Type: Comprehensive Coverages Gain Ground

Comprehensive policies logged 15.12% CAGR forecasts, capturing consumers seeking broader safeguards against natural catastrophes and theft. Higher vehicle ASPs amplify repair costs, making own-damage protection indispensable. IRDAI-approved riders such as consumables cover and return-to-invoice benefits deepen value perception, raising uptake. Flexible EMI options facilitate affordability, especially among first-time buyers in urban fringes. Usage-based variants under sandbox rules promise tailored premiums, further boosting attraction.

Third-party lines remain mandatory and hold a 53.55% share of the India car insurance market size in 2025, yet tariff stagnation depresses revenue momentum. Tribunal awards exceeding INR 30 million (USD 0.35 million) have heightened liability exposure, prompting calls for actuarial-led tariff revisions. Insurers deploy fraud analytics to combat staged accidents and contain claim leakage. Persistently high litigation timelines motivate experiments with mediation cells to settle minor injuries out of court. Overall, balancing social-insurance objectives and commercial viability remains a pressing policy challenge.

By Distribution Channel: Digital Sales Surge While Agents Retain Scale

Direct digital channels are clocking a 18.73% CAGR, anchored by aggregator portals and insurer apps that cut acquisition costs. Embedded finance on e-commerce checkouts lets shoppers purchase insurance alongside cars booked online, compressing conversion windows. Chatbots and video KYC simplify onboarding, pushing digital’s share beyond 30% of new comprehensive policies in metros. In rural clusters, voice-assisted apps in local languages widen reach for the India car insurance market.

Agent networks still deliver 56.65% of written premiums as of 2025, valued for personalized advice and claim-assist services. Car dealers' co-brand policies to lock in captive renewals during the first ownership cycle. Bancassurance adds steady volumes, especially for bundled credit-linked covers. Insurers invest in agent-mobility suites that generate instant quotes and e-signatures, seeking to merge high-touch service with digital speed. Commission optimization and performance-based incentives aim to curb distribution costs amid mounting price pressure.

Geography Analysis

Premium generation remains heavily skewed toward Delhi, Mumbai, Bengaluru, and Chennai, which together account for roughly 45% of the national written premium. Higher vehicle ASPs and awareness levels translate into larger average policy values. Digital-first insurers pilot telematics and PAYD products in these metros because telecom coverage and smartphone penetration exceed 90%.

Tier-2 hubs such as Ahmedabad, Pune, Coimbatore, and Jaipur are the fastest-growing pockets, driven by rising disposable income and dealership expansion. GST-induced price rationalization encouraged first-time buyers, widening the base of mandatory policies. Insurers run vernacular-language campaigns and partner with micro-financiers to deepen penetration. Enhanced road networks under the Bharatmala project raise inter-city freight traffic, boosting commercial vehicle cover demand.

Rural districts see accelerating vehicle ownership but lag in insurance uptake due to awareness gaps and distribution frictions. IRDAI’s Insurance for All by 2047 roadmap mobilizes State-Level Insurance Committees to train village-level entrepreneurs as micro-agents. E-policy issuance via Aadhaar-based e-KYC cuts paperwork barriers. Government-subsidized EV schemes in agricultural belts introduce new risk pools, spurring insurers to craft low-premium modular products. Over the next five years, these initiatives could materially lift rural contributions to the India car insurance market.

Coverage of the car insurance market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia and Europe, alongside detailed country-level intelligence for Japan, China, United Kingdom, France, Germany, Brazil, and Russia, each shaped by local operating conditions.

Competitive Landscape

Public-sector titan New India Assurance, leading private carrier ICICI Lombard, and Bajaj Allianz anchor the market’s top tier, collectively writing over one-third of motor premiums. Each deploys proprietary AI engines to automate claims, with photo-based damage detection slashing settlement times to under two hours in select pilot cities. Collaborations with automakers such as Maruti Suzuki enable instant policy issuance at dealerships and tap owner databases for renewal targeting.

Digital-native insurers Acko and Go Digit apply cloud-only operations to cut expense ratios, funneling savings into competitive pricing. Their usage-based and bite-sized covers resonate with millennial drivers ordering cars online. Consistent NPS leadership has helped Acko exceed 10 million motor policies since launch, prompting incumbents to replicate app-first experiences. Venture-capital backing fuels aggressive customer-acquisition campaigns during festive sales periods, intensifying price pressure across the India car insurance market.

Industry consolidation is gathering pace as solvency norms tighten. Bajaj’s March 2025 purchase of Allianz’s 26% stake gives it full control and spurs speculation of an IPO roadmap. Allianz, in turn, is exploring a fresh joint venture with Jio Financial Services to re-enter India under a more favorable FDI regime. Smaller regions face scale disadvantages in digital investments and may become targets for merger or exit. Overall, technology capability, distribution reach, and capital strength remain decisive competitive levers.

India Car Insurance Industry Leaders

New India Assurance Co. Ltd.

ICICI Lombard General Insurance Co. Ltd.

Bajaj Allianz General Insurance Co. Ltd.

HDFC ERGO General Insurance Co. Ltd.

IFFCO TOKIO General Insurance Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ICICI Lombard reported 11.5% FY25 motor-line growth and projected beating industry expansion by 100–200 basis points in FY26 through digital claims and OEM partnerships.

- March 2025: Bajaj Group acquired Allianz SE’s 26% shareholdings in both Bajaj Allianz entities for INR 24,180 crore (USD 2,827.5 million), forming the country’s largest domestic private insurance company.

- March 2025: Allianz SE began negotiations with Jio Financial Services for a new joint venture, targeting a majority stake under the revised 100% FDI cap.

- February 2025: The Union Budget 2025-26 raised foreign direct investment limits in the insurance sector from 74% to 100% for insurers investing all premiums in India. This policy aims to attract global capital, welcome new market entrants, and support local economic growth through domestic investment mandates.

India Car Insurance Market Report Scope

Car insurance is a contract between the car owner and the insurance company where the car owner agrees to pay a fixed premium rate over some time for protection against financial loss in the event of any damage or loss to the car. Rising digital insurance and product innovations in the market are making car insurance products more inclusive among car owners. The study gives a brief description of the Indian car insurance market. It includes details on car insurance premiums, investment by car insurance companies, and the launch of new car insurance products.

India's car insurance market is segmented by coverage, by application, and by distribution channel. By coverage, the market is segmented into third-party liability coverage and collision/comprehensive/other optional coverage. By application, the market is segmented into personal vehicles and commercial vehicles. By distribution channel, the market is segmented into individual agents, brokers, banks, online, and other distribution channels. The report also covers the market sizes and forecasts for the Indian car insurance market in value (USD) for all the above segments.

| Personal |

| Commercial |

| Third Party |

| Comprehensive |

| Direct |

| Agents |

| Brokers |

| Banks |

| Other Distribution Channels |

| By Vehicle Type | Personal |

| Commercial | |

| By Insurance Type | Third Party |

| Comprehensive | |

| By Distribution Channel | Direct |

| Agents | |

| Brokers | |

| Banks | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current value of the India car insurance market?

The India car insurance market size stands at USD 3.67 billion in 2026.

How fast is the India car insurance market expected to grow?

It is projected to expand at an 11.52% CAGR, reaching USD 6.33 billion by 2031.

Which segment is growing fastest within India’s car insurance space?

Commercial vehicle policies lead with an 11.34% CAGR forecast through 2031.

Why are comprehensive policies gaining popularity in India?

Rising vehicle values and climate-related risks are pushing buyers toward broader own-damage protection and add-on covers.

How are digital platforms changing the purchasing process?

Aggregator sites and insurer apps provide instant quotes, e-KYC issuance, and self-service claims, reducing reliance on traditional agents.

What impact will telematics have on premiums?

Usage-based products approved by IRDAI can lower premiums by 15–20% for safe drivers and fleet operators through behavior-linked pricing.

Page last updated on: