Autoimmune Hemolytic Anemia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.63 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autoimmune Hemolytic Anemia Treatment Market Analysis by Mordor Intelligence

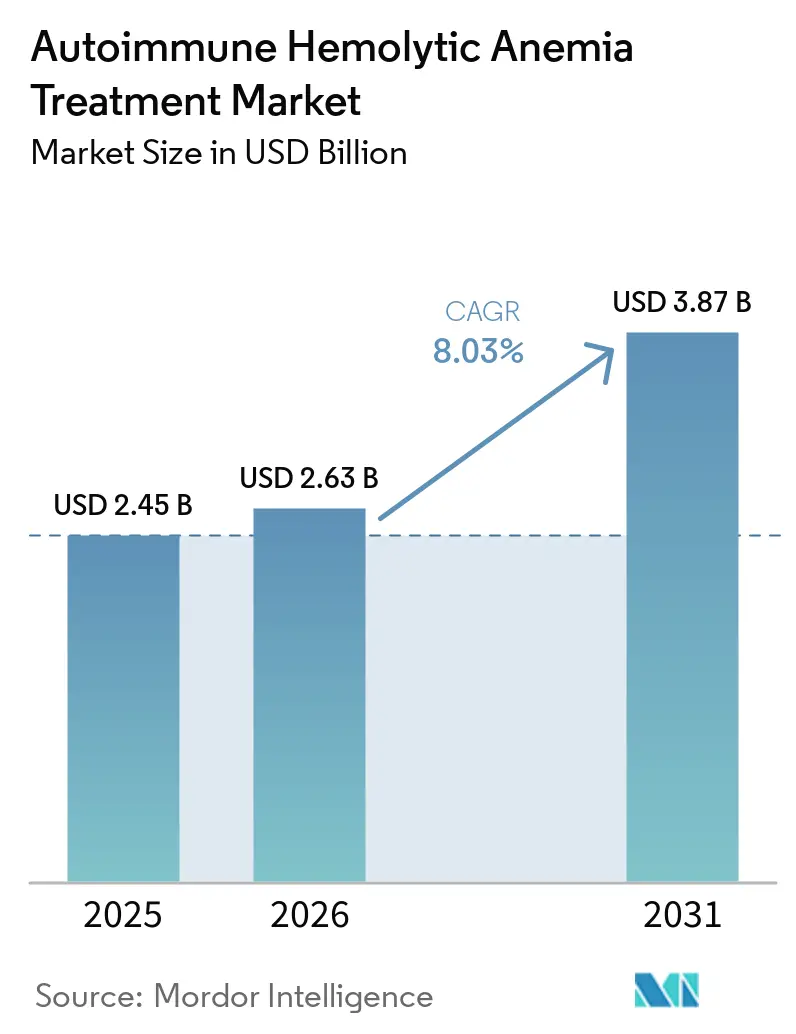

The Autoimmune Hemolytic Anemia Treatment Market size is projected to expand from USD 2.45 billion in 2025 and USD 2.63 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 8.03% between 2026 to 2031.

Warm autoimmune hemolytic anemia remains the main commercial focus because it accounts for most diagnosed cases, yet no targeted therapy is approved for this subtype in the United States as of 2026, which leaves treatment centered on off-label use and creates clear room for the first labeled entrant. The treatment approach is shifting away from broad immunosuppression because steroid relapse and long exposure toxicity continue to push patients toward later-line options and create repeat switching opportunities. Regulatory activity is also speeding up, with Johnson & Johnson’s nipocalimab under FDA Priority Review for warm autoimmune hemolytic anemia and Sanofi’s rilzabrutinib already holding Breakthrough Therapy designation for the same setting. At the same time, the autoimmune hemolytic anemia treatment market is moving into a more competitive phase as FcRn inhibitors, BTK inhibitors, complement inhibitors, and SYK inhibitors advance through late-stage development in a narrow patient pool where timing, label scope, and reimbursement will shape early advantage.

Key Report Takeaways

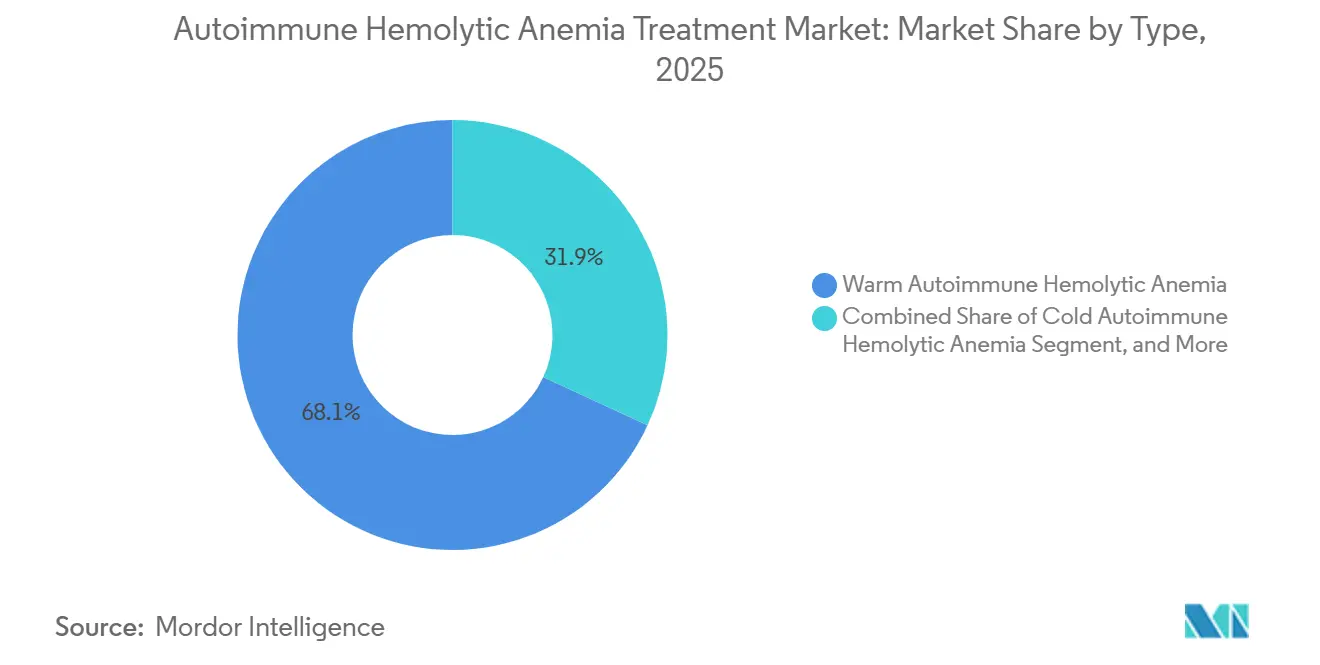

- By type, warm autoimmune hemolytic anemia led with 68.13% of the autoimmune hemolytic anemia treatment market share in 2025, while cold autoimmune hemolytic anemia is forecast to expand at an 8.78% CAGR through 2031.

- By drug class, corticosteroids held 57.38% share in 2025, while FcRn inhibitors are projected to grow at a 10.42% CAGR to 2031.

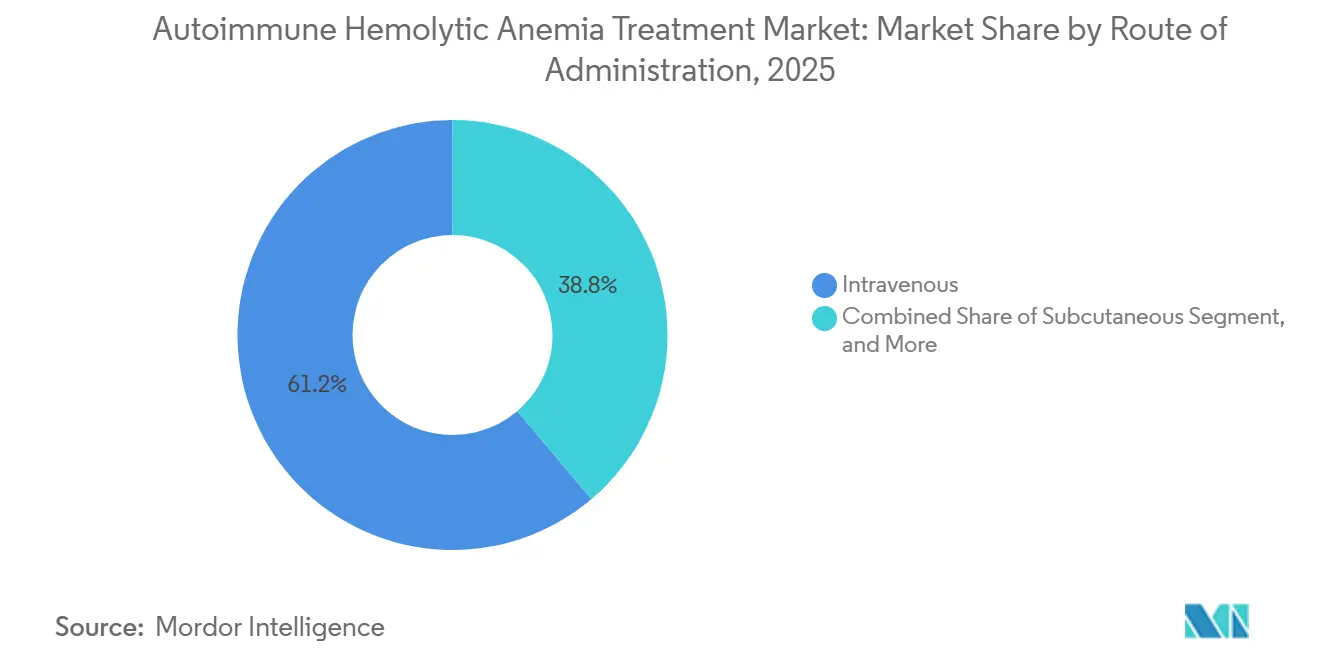

- By route of administration, intravenous therapies accounted for 61.16% of the autoimmune hemolytic anemia treatment market size in 2025, while oral therapies are advancing at a 9.83% CAGR through 2031.

- By distribution channel, hospital pharmacy captured 55.12% share in 2025, while online pharmacy is forecast to record the highest CAGR at 10.98% through 2031.

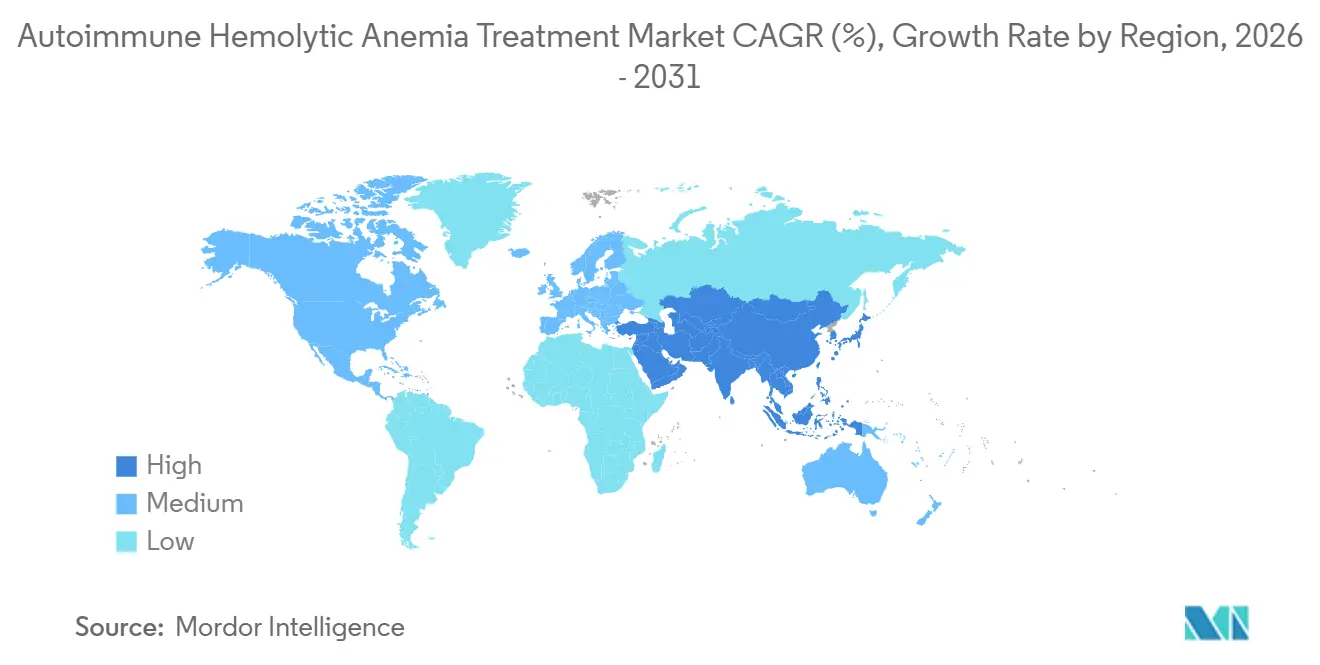

- By geography, North America held 35.63% of the autoimmune hemolytic anemia treatment market share in 2025, while Asia-Pacific is projected to expand at a 9.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autoimmune Hemolytic Anemia Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing need for steroid-sparing therapies in refractory AIHA | +2.5% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Rising pipeline readiness for complement and FcRn targeting therapies | +2.0% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Expanding orphan-drug incentives for rare hematology programs | +1.1% | North America, EU, Japan | Medium term (2-4 years) |

| Growing use of precision diagnostics to subtype warm, cold, and mixed AIHA | +0.9% | North America, EU, APAC core | Medium term (2-4 years) |

| Higher treatment switching after steroid toxicity and relapse | +0.7% | Global | Short term (≤ 2 years) |

| Increasing specialist referral networks for rare blood disorders | +0.5% | North America, Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Need for Steroid-Sparing Therapies in Refractory AIHA

Corticosteroids still produce an initial hemoglobin response in many warm autoimmune hemolytic anemia patients, but relapse remains common after tapering, and that keeps the autoimmune hemolytic anemia treatment market tied to repeat treatment cycles.[1]Bruno Fattizzo, “Management of Autoimmune Hemolytic Anemia,” Hematology, ASH Education Program, ashpublications.org Long steroid exposure also raises the burden of diabetes, metabolic complications, and osteoporosis, which lowers quality of life and adds avoidable hospital use even when hemolysis is partly controlled. Rituximab has moved into the preferred second-line position for relapsed or refractory disease, while splenectomy has shifted later because published cohort evidence showed a 12% surgical complication rate. This pattern matters for the autoimmune hemolytic anemia treatment market because every relapse on a prior agent creates a clear switching event once a targeted option is available. The current treatment sequence outlined in the 2025 ASH Education Program also places newer B-cell, plasma-cell, SYK, and FcRn approaches behind rituximab, which supports continued demand across multiple lines of care.

Rising Pipeline Readiness for Complement and FcRn Targeting Therapies

The autoimmune hemolytic anemia treatment market is now moving closer to its first broad wave of labeled targeted therapies, and FcRn blockade is at the center of that shift.[2]J.A. Petersen, “Targeting the Neonatal Fc Receptor in Autoimmune Diseases, Pipeline and Progress,” BioDrugs, link.springer.com FcRn-targeted agents can reduce circulating IgG by as much as 85%, which directly addresses the autoantibodies that drive red blood cell destruction while preserving IgA, IgM, and innate immune function. Nipocalimab is the most advanced FcRn program in warm autoimmune hemolytic anemia and is under FDA Priority Review after showing durable hemoglobin response in the Phase 2/3 ENERGY study. Cold autoimmune hemolytic anemia already has one approved targeted option through sutimlimab, and registry data in more than 70% of treated patients have supported durable real-world effectiveness without new safety signals after a mean treatment duration of more than 2 years. As labeled warm and cold options come into view at the same time, the autoimmune hemolytic anemia treatment market is likely to see stronger physician confidence and better reimbursement support.

Expanding Orphan-Drug Incentives for Rare Hematology Programs

Orphan-drug incentives continue to support investment in the autoimmune hemolytic anemia treatment market because they improve the economics of development in a rare disease setting. In the United States, orphan designation can provide 7 years of market exclusivity together with other development benefits, and Sanofi’s rilzabrutinib received this status for warm autoimmune hemolytic anemia in April 2025.[3]Sanofi, “Rilzabrutinib Granted Orphan Drug Designation in the US for Two Rare Diseases With No Approved Medicines,” Sanofi, sanofi.com Ouro Medicines also received FDA orphan designation in August 2025 for OM336 after case reports and a broader basket study strategy supported continued development in autoimmune cytopenias. Europe maintained orphan protection for Enjaymo after the product transferred to Recordati, and Japan extended orphan designation to rilzabrutinib in February 2026. With the United States, Europe, and Japan all supporting programs in this space, the autoimmune hemolytic anemia treatment market is attracting both large pharmaceutical companies and specialist biotechs.

Growing Use of Precision Diagnostics to Subtype Warm, Cold, and Mixed AIHA

Accurate subtyping is essential because the autoimmune hemolytic anemia treatment market cannot fully convert incidence into treated demand unless physicians can distinguish warm, cold, mixed, and secondary disease. The direct antiglobulin test remains central to diagnosis, yet false negatives occur in 1% to 10% of cases and leave part of the patient pool in diagnostic uncertainty. Tertiary centers are improving precision through stronger DAT methods, cold antibody titration protocols, and next-generation sequencing panels for red blood cell membrane disorders. This matters commercially because each patient who is correctly identified with cold autoimmune hemolytic anemia can be considered for sutimlimab, while poorly characterized patients often remain on default steroid treatment. ASH-cited international consensus work already supports standardized monospecific DAT as a required part of workup, and wider use of this approach should gradually broaden the treated base for targeted therapies in the autoimmune hemolytic anemia treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long diagnostic delay before confirmed hematology referral | -1.2% | Global, most acute in LMIC and South/Southeast Asia | Long term (≥ 4 years) |

| Small treatable patient pool in cold agglutinin disease and secondary AIHA | -0.9% | Global | Long term (≥ 4 years) |

| Weak standardization of clinical endpoints in warm AIHA trials | -0.6% | Global | Medium term (2-4 years) |

| High dependence on steroids, transfusion, and splenectomy in routine care | -0.5% | Global, persistent in LMIC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long Diagnostic Delay Before Confirmed Hematology Referral

Diagnostic delay remains a direct limit on the autoimmune hemolytic anemia treatment market because untreated or misdiagnosed patients do not reach hematology prescribing channels. In low and middle-income countries, pediatric cases have been reported at hemoglobin levels of 3 g/dL to 6 g/dL by the time treatment begins, which reflects long delays between symptom onset and specialist care. Cold autoimmune hemolytic anemia is especially easy to miss because acrocyanosis and cold-triggered circulatory symptoms are often linked to other conditions before hematology referral occurs. Even in higher-income settings, DAT-negative disease can require advanced crossmatch and elution methods that are not widely available in community laboratories. Until referral access, awareness, and diagnostic capability improve more broadly, the autoimmune hemolytic anemia treatment market will continue to face a ceiling on addressable volume.

Small Treatable Patient Pool in Cold Agglutinin Disease and Secondary AIHA

The autoimmune hemolytic anemia treatment market is constrained by the narrow patient base in some subtypes, especially cold agglutinin disease and secondary autoimmune hemolytic anemia. Cold agglutinin disease represents 15% to 20% of all autoimmune hemolytic anemia cases, while secondary disease adds another clinically diverse group shaped by lymphoproliferative disorders, autoimmune disease, and drug exposure. Secondary cases are often excluded from interventional trials, which leaves a gap between the patients seen in practice and the patients covered by formal evidence packages. For cold agglutinin disease, the epidemiology is especially tight at 1 case per 1 million population per year in European settings, which limits the revenue ceiling for dedicated products. Developers are responding with basket studies such as Ouro Medicines’ Phase 1b program across autoimmune cytopenias, but that approach can dilute disease-specific label strength in the autoimmune hemolytic anemia treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Warm Subtype Anchors Revenue, Cold AIHA Drives Faster Expansion

Warm autoimmune hemolytic anemia held 68.13% of the autoimmune hemolytic anemia treatment market share in 2025, which matched its position as the most common subtype globally. The autoimmune hemolytic anemia treatment market, therefore, remains centered on warm disease, even though formal targeted approval for this setting is still pending in the United States. That gap means much of the current value in warm disease still comes through corticosteroids and rituximab used off label rather than through premium branded treatment lines. The subtype remains the main target for late-stage programs because it offers the broadest commercial base and the clearest near-term path to label expansion.

Cold autoimmune hemolytic anemia is projected to grow at an 8.78% CAGR through 2031, supported by sutimlimab’s existing presence and improving real-world evidence. Mixed autoimmune hemolytic anemia remains a smaller revenue pool because it represents only 5% to 8% of cases and often overlaps with complex autoimmune backgrounds such as SLE, where 25% to 42% of mixed cases are associated. Secondary autoimmune hemolytic anemia also remains commercially limited because pivotal studies often exclude these patients, which weakens reimbursement support even when physicians still treat them. Over the longer term, refractory disease may open another layer of value as Juventas Biotechnology’s CAR-T program moved into clinical testing after NMPA IND approval in April 2025.

By Drug Class: Corticosteroids Still Lead, FcRn Inhibitors Set the Pace

Corticosteroids accounted for 57.38% of the autoimmune hemolytic anemia treatment market size in 2025, which reflects entrenched first-line use and low generic acquisition cost rather than durable disease control. That legacy position continues because most patients still begin treatment with steroids even when relapse risk is well understood. Monoclonal antibodies, especially rituximab and biosimilar-linked use, remain important in second-line care and gained fresh support in Japan after the February 2026 approval of rituximab for autoimmune hemolytic anemia. Complement inhibitors hold a defined role in cold disease through sutimlimab, but their growth is naturally capped by the smaller cold agglutinin disease population.

FcRn inhibitors are the fastest-growing class with a 10.42% CAGR through 2031, and this outlook is tied directly to nipocalimab’s late-stage progress in warm autoimmune hemolytic anemia. The class also benefits from a strong biological rationale because FcRn blockade lowers pathogenic IgG without broadly suppressing other immunoglobulins in the same way. BTK inhibitors are the other key challenger class, and rilzabrutinib posted a 64% overall hemoglobin response rate in 21 primary warm autoimmune hemolytic anemia patients before moving into Phase 3 with Breakthrough Therapy designation. Immunosuppressants, IVIG, and similar supportive options will remain in use, but they are less likely to drive the long-term revenue mix of the autoimmune hemolytic anemia industry once targeted classes become labeled and reimbursed.

By Route of Administration: Intravenous Use Leads Today, Oral Access Gains Ground

Intravenous therapies held 61.16% share of the autoimmune hemolytic anemia treatment market size in 2025 because the leading available and late-stage agents are still mostly infusion based. Sutimlimab, rituximab, and nipocalimab all reinforce a hospital-centered treatment model where diagnosis and treatment initiation are closely linked. This gives intravenous delivery a strong base in current revenue, especially in referral centers that manage severe anemia and transfusion needs. It also explains why hospital and specialty pharmacy systems have remained closely tied to the autoimmune hemolytic anemia treatment market.

Oral therapies are forecast to grow at a 9.83% CAGR through 2031, driven by BTK inhibitor development and the potential for treatment to move beyond infusion centers. Rilzabrutinib is already supported by an oral specialty distribution structure through its broader regulatory history, which lowers launch friction if warm autoimmune hemolytic anemia approval follows. Subcutaneous delivery remains a smaller but relevant future niche because less burdensome administration could improve persistence in a relapsing disease. As more convenient formats enter care pathways, the autoimmune hemolytic anemia treatment market should gradually shift toward settings that can manage chronic follow-up with less infusion dependence.

By Distribution Channel: Hospital Pharmacy Leads, Online Models Expand Faster

Hospital pharmacy retained 55.12% of the autoimmune hemolytic anemia treatment market share in 2025 because most advanced therapies still flow through inpatient or outpatient infusion settings. This pattern fits a disease area where severe cases often enter care through hospitals and where biologics require close monitoring. It also matches the current delivery profile of sutimlimab, rituximab, and likely early FcRn uptake. As a result, hospital pharmacies remain the main control point for current access in the autoimmune hemolytic anemia treatment market.

Online pharmacy is projected to expand at 10.98% CAGR through 2031 as rare disease manufacturers continue to rely on specialty hub models for adherence support and co-pay assistance. Retail pharmacy remains secondary because patient complexity, biologic handling requirements, and payer contracting still favor specialty channels. Still, a larger oral pipeline could gradually shift some prescription volume away from hospitals and into specialty and retail networks later in the forecast period. In emerging markets, this transition will remain slower because hospital systems are often still the only structured access route for the autoimmune hemolytic anemia treatment market.

Geography Analysis

North America held 35.63% of the autoimmune hemolytic anemia treatment market share in 2025, which kept it ahead of every other region. The United States remains the core revenue base because it has the deepest concentration of rare blood disorder specialists, the most active regulatory pipeline, and the highest treatment spending per patient. The current U.S. inflection point is the FDA Priority Review for nipocalimab in warm autoimmune hemolytic anemia, which could deliver the first approved targeted therapy for this subtype in late 2026 or early 2027. Commercial readiness is also stronger in this region because specialty pharmacy networks already support adjacent hematology drugs such as fostamatinib, and because Enjaymo has already established physician familiarity with targeted AIHA treatment. Canada and Mexico are expanding rare disease reimbursement, but the autoimmune hemolytic anemia treatment market remains much smaller there on a per-patient basis.

Europe remains the second major region for the autoimmune hemolytic anemia treatment market, anchored by Germany, the United Kingdom, France, Italy, and Spain. The region benefits from a supportive orphan framework, as seen in Enjaymo’s maintained orphan status and the broader openness to orphan programs in autoimmune hemolytic anemia. The United Kingdom still has a key access gap because NICE has not approved an AIHA-specific product, which makes future health technology submissions a major gating step. European clinician awareness is also rising as HUTCHMED presented pivotal sovleplenib Phase 3 data at EHA 2026 in Stockholm, which brought SYK inhibition further into the regional discussion.

Asia-Pacific is the fastest-growing geography in the autoimmune hemolytic anemia treatment market, with a 9.06% CAGR projected for 2026-2031. Japan strengthened second-line access in February 2026 when rituximab was approved for autoimmune hemolytic anemia, and Sanofi also received orphan designation there for rilzabrutinib in the same month. China is gaining importance through HUTCHMED’s priority-reviewed sovleplenib NDA and Juventas Biotechnology’s CAR-T clinical entry, while the Middle East, Africa, and South America remain smaller but are gradually opening through rare disease policy support and specialist center investment. Diagnostic limits still suppress treated volume in those smaller regions, so growth will depend as much on health system readiness as on product launches.

Competitive Landscape

The autoimmune hemolytic anemia treatment market is moderately fragmented at the current commercial stage because only one targeted therapy is labeled for any autoimmune hemolytic anemia subtype, while a large share of patient care still relies on generics and off-label use. At the same time, the pipeline is crowded because FcRn inhibitors, BTK inhibitors, complement inhibitors, SYK inhibitors, and T-cell engagers are all active across clinical development. Large companies such as Johnson & Johnson, Sanofi, Alexion or AstraZeneca, and Novartis bring orphan drug experience and established rare disease channels, while smaller specialists focus on narrower mechanistic gaps. Johnson & Johnson made the clearest near-term move by filing its supplemental BLA in February 2026 and securing Priority Review in April 2026 for nipocalimab in warm autoimmune hemolytic anemia. Rigel Pharmaceuticals also protected future positioning by settling TAVALISSE patent litigation in March 2025, which preserved pricing protection through most of the forecast period even if a warm autoimmune hemolytic anemia label is later added.

White-space opportunities remain strongest in secondary autoimmune hemolytic anemia, pediatric disease, and combinations that can address both IgG-mediated and complement-mediated hemolysis. Smaller companies are using basket-study designs to spread development cost across autoimmune cytopenias, and Ouro Medicines is a clear example through its OM336 Phase 1b program in autoimmune hemolytic anemia and immune thrombocytopenia. Chinese developers are also broadening the competitive field, with Juventas Biotechnology pushing CAR-T work and HUTCHMED moving a SYK inhibitor through priority review in China. These moves show that the autoimmune hemolytic anemia treatment market is no longer limited to a few Western orphan programs.

The most important near-term race is between FcRn inhibitors and oral BTK inhibitors for the first approved warm autoimmune hemolytic anemia label. Whichever class enters first is likely to influence prescribing order, payer reference points, and the access standard faced by later entrants in the autoimmune hemolytic anemia treatment market. HUTCHMED’s April 2026 priority-reviewed NDA for sovleplenib adds another serious contender because it brings a distinct oral SYK approach with pivotal data already in hand. The result is a market where current fragmentation is likely to persist, even as the first few approvals begin to reshape how value is distributed across the autoimmune hemolytic anemia treatment market.

Autoimmune Hemolytic Anemia Treatment Industry Leaders

AbbVie Inc.

Amgen Inc.

Bristol-Myers Squibb Company

Novartis AG

Johnson and Johnson Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The U.S. FDA granted Priority Review to Johnson & Johnson's supplemental Biologics License Application for IMAAVY (nipocalimab-aahu) for warm autoimmune hemolytic anemia, marking the first Priority Review ever granted for a wAIHA-specific indication. Supported by the pivotal Phase 2/3 ENERGY trial data demonstrating durable hemoglobin response and rapid disease control versus placebo, the designation shortens the FDA review timeline to 6 months. The ENERGY trial data were also presented at the European Hematology Association 2026 Congress, marking the first pivotal wAIHA dataset to be presented at a major European hematology forum.

- April 2026: HUTCHMED (China) Limited's New Drug Application for sovleplenib in wAIHA was accepted by China's NMPA with priority review. Phase 3 ESLIM-02 data presented at EHA 2026 in Stockholm demonstrated a 66% sustained response rate versus 15% for placebo, with 70% overall response at 24 weeks, median time to response of 3.1 weeks, and no treatment-related deaths.

- March 2026: HUTCHMED's sovleplenib received Breakthrough Therapy designation from China's NMPA for wAIHA, the second Chinese regulatory milestone for the SYK inhibitor following initiation of the ESLIM-02 Phase 3 registration stage in March 2024.

- February 2026: Sanofi's rilzabrutinib (Wayrilz) received U.S. FDA Breakthrough Therapy designation for wAIHA and Japan MHLW Orphan Drug designation for wAIHA. Concurrently, the Phase 3 LUMINA 3 trial, NCT07086976, comparing rilzabrutinib versus placebo in adults with wAIHA, was initiated.

Global Autoimmune Hemolytic Anemia Treatment Market Report Scope

The Autoimmune Hemolytic Anemia (AIHA) Treatment Market is defined as the global industry focused on therapies that manage and treat AIHA, a rare but serious condition where the immune system destroys red blood cells, leading to anemia. The market includes corticosteroids, immunosuppressants, monoclonal antibodies, blood transfusions, surgical interventions, and emerging biologics such as complement inhibitors.

The Autoimmune Hemolytic Anemia (AIHA) Treatment Market is segmented by type, drug class, route of administration, distribution channel, and geography. By type, it includes Warm Autoimmune Hemolytic Anemia, Cold Autoimmune Hemolytic Anemia, Mixed Autoimmune Hemolytic Anemia, Secondary Autoimmune Hemolytic Anemia, and Other Type Autoimmune Hemolytic Anemia. By drug class, treatments are segmented into Corticosteroids, Intravenous Immunoglobulin, Monoclonal Antibodies, Complement Inhibitors, Immunosuppressive Agents, BTK Inhibitors, FcRn Inhibitors, and Other Drug Classes. By route of administration, therapies are delivered via Oral, Intravenous, Subcutaneous, and Other Routes of Administration. By distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle_East_%26_Africa), and South America (Brazil, Argentina, Rest of South America).

| Warm Autoimmune Hemolytic Anemia |

| Cold Autoimmune Hemolytic Anemia |

| Mixed Autoimmune Hemolytic Anemia |

| Secondary Autoimmune Hemolytic Anemia |

| Other Type Autoimmune Hemolytic Anemia |

| Corticosteroids |

| Intravenous Immunoglobulin |

| Monoclonal Antibodies |

| Complement Inhibitors |

| Immunosuppressive Agents |

| BTK Inhibitors |

| FcRn Inhibitors |

| Other Drug Classes |

| Oral |

| Intravenous |

| Subcutaneous |

| Other Routes of Administration |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Warm Autoimmune Hemolytic Anemia | |

| Cold Autoimmune Hemolytic Anemia | ||

| Mixed Autoimmune Hemolytic Anemia | ||

| Secondary Autoimmune Hemolytic Anemia | ||

| Other Type Autoimmune Hemolytic Anemia | ||

| By Drug Class | Corticosteroids | |

| Intravenous Immunoglobulin | ||

| Monoclonal Antibodies | ||

| Complement Inhibitors | ||

| Immunosuppressive Agents | ||

| BTK Inhibitors | ||

| FcRn Inhibitors | ||

| Other Drug Classes | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Subcutaneous | ||

| Other Routes of Administration | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of autoimmune hemolytic anemia treatment in 2026?

The autoimmune hemolytic anemia treatment market is valued at USD 2.63 billion in 2026 and is forecast to reach USD 3.87 billion by 2031 at an 8.0% CAGR.

Which subtype drives the largest revenue pool in autoimmune hemolytic anemia treatment?

Warm autoimmune hemolytic anemia leads the field, holding 68.13% share in 2025 because it represents most diagnosed cases and remains the focus of late-stage pipeline activity.

Why are targeted therapies gaining attention in this field?

Targeted therapies are gaining traction because steroid relapse is common, long-term toxicity remains a problem, and FcRn, BTK, complement, and SYK approaches are showing stronger disease-specific potential.

Which drug class is growing fastest through 2031?

FcRn inhibitors are projected to expand at a 10.42% CAGR through 2031, supported by late-stage progress from nipocalimab in warm autoimmune hemolytic anemia.

Which region is expected to grow fastest over the forecast period?

Asia-Pacific is the fastest-growing region with a projected 9.06% CAGR for 2026-2031, helped by regulatory progress in Japan and China.

What are the main barriers to broader treatment uptake?

The main barriers are diagnostic delay, the small treatable pool in some subtypes, weak endpoint standardization in warm AIHA trials, and continued dependence on older routine care such as steroids and transfusion support.

Page last updated on: