Iron Deficiency Anemia Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

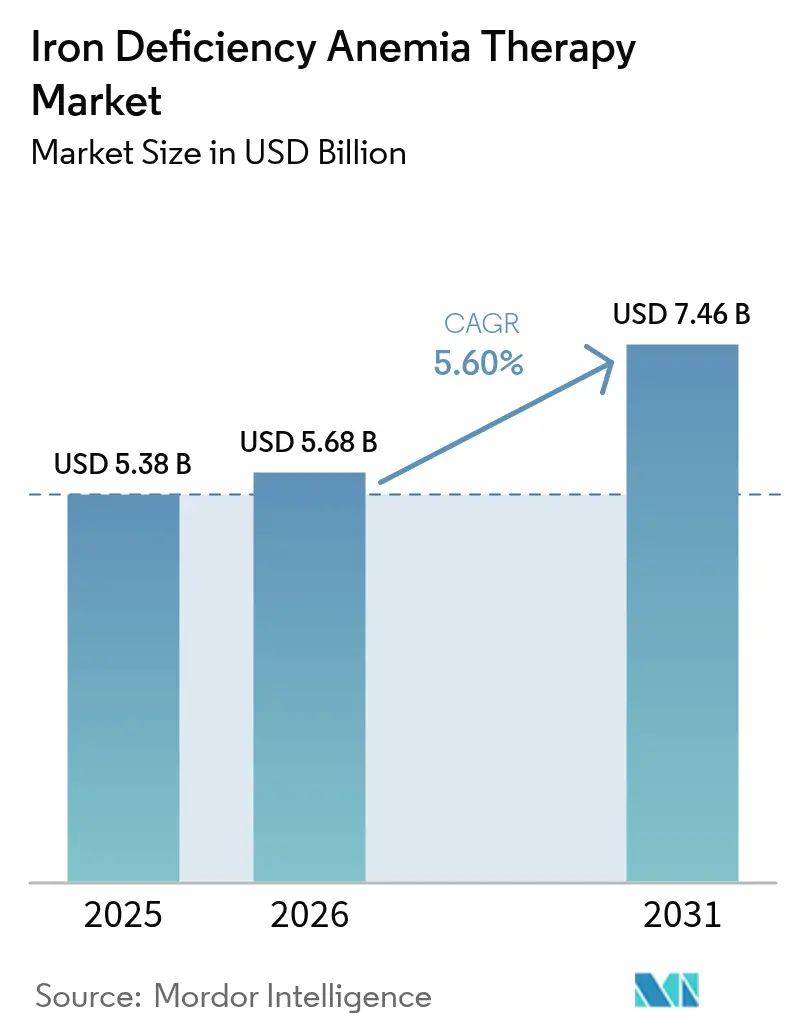

| Market Size (2026) | USD 5.68 Billion |

| Market Size (2031) | USD 7.46 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

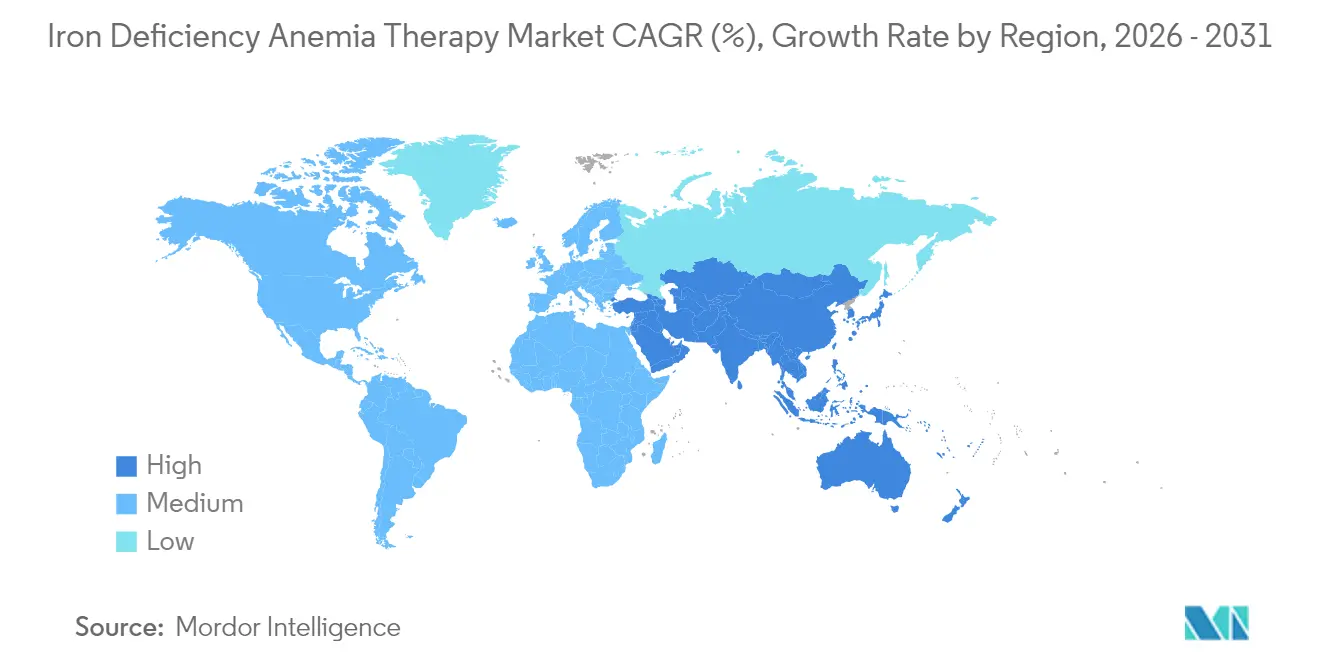

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

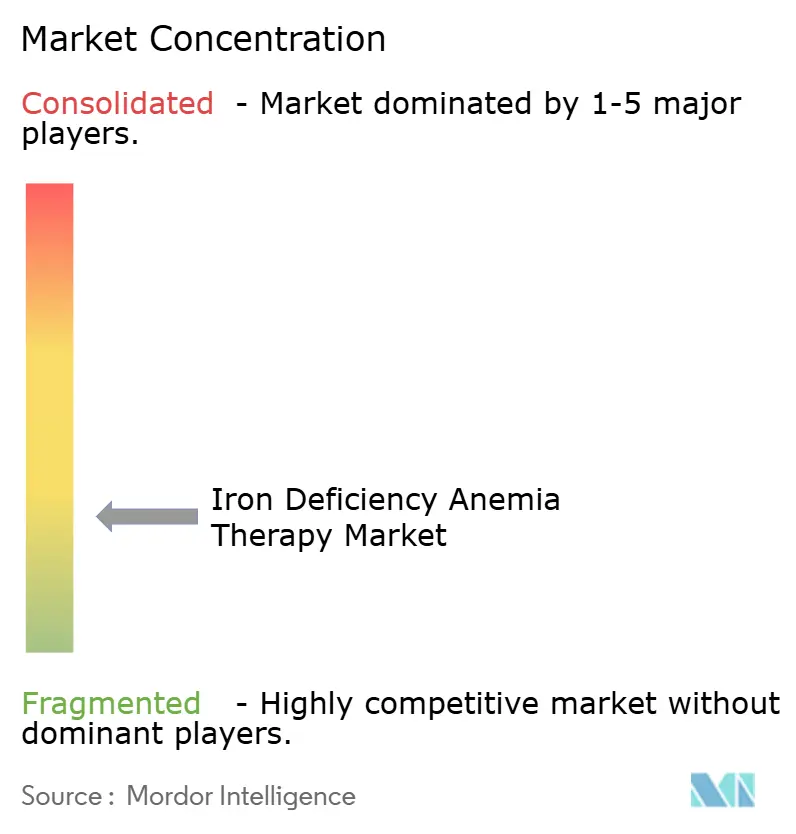

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iron Deficiency Anemia Therapy Market Analysis by Mordor Intelligence

Iron Deficiency Anemia Therapy Market size in 2026 is estimated at USD 5.68 billion, growing from 2025 value of USD 5.38 billion with 2031 projections showing USD 7.46 billion, growing at 5.60% CAGR over 2026-2031. Strong clinical evidence for intravenous iron in heart failure, chronic kidney disease, and oncology, coupled with widespread screening programs, continues to lift demand. Record numbers of women of reproductive age and children now meet diagnostic criteria for deficiency, and this epidemiological pressure is translating directly into higher treatment volumes. Hospitals are favoring single-visit total-dose infusions that reduce chair time, while digital platforms are guiding dose decisions remotely. On the supply side, new oral technologies that wrap iron in protective matrices are improving adherence and opening consumer-centric sales channels that were once inaccessible to parenteral products.

Key Report Takeaways

- By therapy type, parenteral iron therapy commanded 60.74% of iron deficiency anemia therapy market share in 2025; oral iron is projected to expand at a 7.42% CAGR through 2031.

- By age group, adults represented 65.10% of the iron deficiency anemia therapy market size in 2025, while pediatrics is the fastest riser at a 6.64% CAGR to 2031.

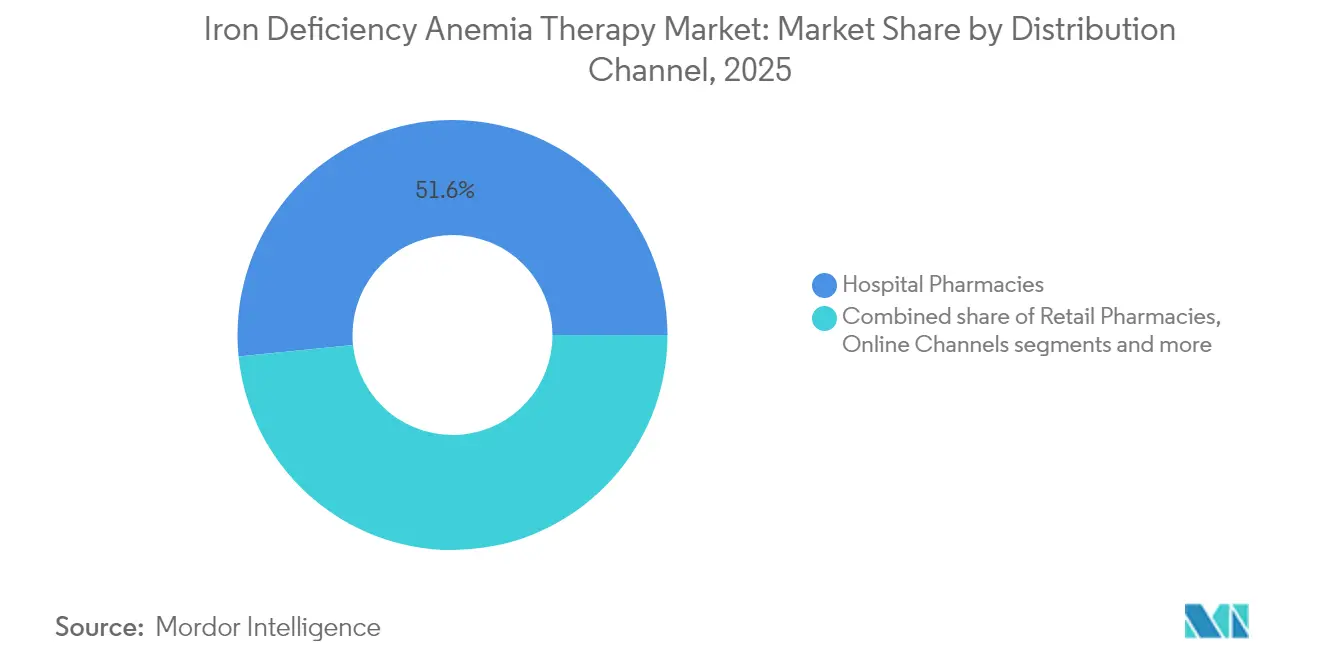

- By distribution channel, hospital pharmacies held 51.60% revenue share in 2025; online channels show the quickest advance at 7.82% CAGR through 2031.

- By geography, North America led with 37.10% revenue in 2025; Asia Pacific is set to grow at 7.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Iron Deficiency Anemia Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global iron-deficiency anemia prevalence | +1.8% | Global, highest in Asia Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Integration of iron therapy into chronic-disease care pathways | +1.2% | North America and EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Government anemia-elimination programmes | +0.9% | Asia Pacific core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Digitalized IV-dosing protocols reducing clinic time | +0.7% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Emergence of trans-mucosal and transdermal delivery formats | +0.6% | North America and EU, gradual global expansion | Medium term (2-4 years) |

| Guideline shift to mandatory ferritin screening in heart-failure surgery | +0.4% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Global Iron-Deficiency Anemia Prevalence

Nearly 29.9% of women aged 15-49 and 39.8% of children worldwide live with iron deficiency anemia, equating to close to 2 billion potential therapy candidates. National surveys in South and Southeast Asia place prevalence for women as high as 63% in the Maldives. Rapid urbanisation has shifted diets toward lower iron density, while infectious disease loads continue to impede absorption. The resulting clinical burden sustains baseline demand for the iron deficiency anemia therapy market, even before accounting for chronic disease comorbidities. Longer-term demographic trends indicate sustained growth in high-risk groups, meaning underlying prevalence will remain the most powerful volume driver across forecast years.

Integration of Iron Therapy into Standard Care Pathways for Chronic Diseases

Cardiology, nephrology, and oncology guidelines now mandate ferritin screening and proactive replenishment, materially enlarging the treated population. The IRONMAN trial confirmed significant haemoglobin gains among heart-failure patients receiving ferric derisomaltose versus standard care. [1]Source: K. Docherty et al., “Intravenous iron for heart failure: the IRONMAN trial,” European Heart Journal, academic.oup.com Similar momentum is visible in oncology, where intravenous ferric carboxymaltose achieved 52.1% haemoglobin response in solid-tumour patients compared with 32.9% for usual care. These recommendations create predictable, protocol-driven purchasing that supports premium formulations and stabilises reimbursement.

Government Anemia-Elimination Programmes

Public-health campaigns inject sizable procurement budgets into the iron deficiency anemia therapy market, but outcomes remain mixed. India’s Anemia Mukt Bharat illustrates the scale: despite large-volume tenders for iron–folic acid, compliance gaps limit clinical impact. Policy makers are now pivoting toward better diagnostics and higher-intensity intravenous regimens for severe deficiency, favouring manufacturers able to offer differentiated dosage forms. Similar initiatives across ASEAN and parts of Africa follow this trajectory, building multi-year demand pipelines for both oral and parenteral products.

Digitalised IV-Dosing Protocols Reducing Clinic Time

Single-visit total-dose infusions have cut average chair time by more than half, and algorithm-based calculators embedded in hospital software further streamline scheduling. Remote ferritin self-tests from companies such as Luma Health and Preventis are letting physicians confirm iron status without in-person labs, enabling earlier intervention. These advances lower the logistical barriers that once limited parenteral adoption outside tertiary centres. As platforms mature, dosing precision is expected to improve, supporting broader outpatient use and strengthening overall volumes for the iron deficiency anemia therapy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety and tolerability concerns discouraging long-term adherence | -0.8% | Global, higher impact where healthcare infrastructure is limited | Long term (≥ 4 years) |

| Stringent pharmacovigilance requirements for parenteral iron | -0.6% | North America and EU, expanding globally | Medium term (2-4 years) |

| Diagnostic ambiguity between functional and absolute iron deficiency | -0.5% | Global, higher impact in emerging markets | Medium term (2-4 years) |

| API supply bottlenecks for ferric derisomaltose | -0.3% | Global, concentrated impact on specific product lines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Safety and Tolerability Concerns Discouraging Long-Term Adherence

Gastrointestinal side effects still cause dropout for legacy ferrous salts, and hypersensitivity events, though rare, remain front of mind with intravenous products. Real-world audits show hypersensitivity in 3.1% of ferric derisomaltose recipients.[2]Source: A. Smith et al., “Real-world evaluation of an intravenous iron service,” Scientific Reports, nature.com Advanced oral options such as ferric maltol reduce discontinuations to under 5%, yet payer awareness is still catching up. The development of nano-encapsulated and transdermal delivery systems aims to remove these tolerability hurdles, but until such formats scale, adverse-event reluctance will weigh on uptake.

Stringent Pharmacovigilance for Parenteral Iron

Regulators have tightened post-marketing surveillance, mandating robust infusion protocols and detailed adverse-event reporting. These requirements increase compliance costs and slow product roll-outs, especially in smaller care settings that lack infusion infrastructure. The heightened scrutiny protects patient safety yet may discourage smaller players from entering the iron deficiency anemia therapy market, limiting competitive price pressure in certain geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Evolving Balance Between Intravenous and Oral Solutions

Parenteral iron delivered 60.74% of iron deficiency anemia therapy market size in 2025, reflecting hospital reliance on total-dose infusions for severe cases. Total-dose options such as ferric carboxymaltose enable complete repletion in a single visit, which aligns with value-based care metrics that reward shorter length of stay. Ongoing hospital formulary expansions, alongside protocol integration for heart failure and oncology, anchor this dominance. However, raw-material tightness for ferric derisomaltose APIs has sparked selective shortages, highlighting latent vulnerability on the supply side.

Oral products post the swiftest expansion at a 7.42% CAGR. Ferric maltol and iron-whey-protein microspheres drive this upswing by slashing common gastrointestinal complaints that once undermined adherence. As adherence rates exceed 80% in recent trials, payers are reconsidering step-therapy rules that previously required failure on generic ferrous sulphate. This policy shift could accelerate volume migration toward premium oral brands over the forecast horizon, diversifying revenue streams inside the iron deficiency anemia therapy market.

By Age Group: Stable Adult Core and Accelerating Pediatric Opportunity

Adults delivered 65.10% of the iron deficiency anemia therapy market share in 2025 on the back of routine screening in antenatal care, nephrology, and cardiology. Insurance coverage in developed markets routinely reimburses both oral and intravenous modalities, ensuring steady baseline demand. Newly issued heart-failure guidelines that classify iron deficiency as a treatable comorbidity further entrench adult utilisation, converting cardiology clinics into repeat procurement hubs.

Pediatrics records a 6.64% CAGR thanks to mandated newborn and school-age screening plus the arrival of child-friendly dose forms. Recent European paediatric consensus endorses weight-based ferric carboxymaltose from 1 year of age, widening the treatable pool. Improved palatability and dosing flexibility in oral suspensions, along with emerging data on neurodevelopmental benefits, strengthen the case for early treatment, positioning the segment as a long-run growth engine within the iron deficiency anemia therapy market.

By Distribution Channel: Hospital Strength Meets Digital Upswing

Hospital pharmacies accounted for 51.60% of iron deficiency anemia therapy market size in 2025, a figure underpinned by bundled care pathways that fold iron infusions into dialysis, chemotherapy, and heart-failure visits. Infusion-chair efficiency gains and tight pharmacovigilance workflows keep hospitals central to parenteral volume.

Online channels record 7.82% CAGR as direct-to-consumer self-testing converges with subscription delivery of advanced oral formulations. Telehealth protocols that link ferritin results to personalised refill algorithms have slashed barriers to initiation. While regulatory clarity on prescription iron varies across markets, the share of home-managed therapy is set to climb, chipping away at retail pharmacy dominance and injecting new competition into the iron deficiency anemia therapy market.

Geography Analysis

North America retained 37.10% of global revenue in 2025, buoyed by comprehensive reimbursement that covers both standard infusions and newer oral brands. Widespread adoption of single-visit ferric carboxymaltose and ferric derisomaltose regimens has reduced outpatient visits, freeing capacity in overstretched clinics. Canada’s recent authorisation of ferric carboxymaltose for paediatric use extends addressability across the life course. Mexico’s public-health insurers are piloting bundled anaemia management packages, though infrastructure limits infusion penetration outside metropolitan hubs.

Asia Pacific posts the fastest regional CAGR at 7.37%. Japan showcases sophisticated dosing algorithms that have shifted clinicians from saccharated ferric oxide to ferric carboxymaltose for efficiency gains. Australia’s primary-care lobby estimates Medicare coverage for GP-led infusions could save USD 124 million in system costs, a proposal now under active review.

Europe maintains steady expansion on the back of guideline harmonisation and supply-security strategies that favour multiple API sources. Germany, France, and the Nordic markets deploy national registries to monitor infusion safety, reinforcing physician confidence in parenteral solutions. Eastern European countries, supported by EU health-equity funds, are scaling up paediatric supplement programs, creating new frontiers for the iron deficiency anemia therapy market even as mature Western states focus on chronic-disease integration.

Regulatory Landscape

Regulatory oversight for iron deficiency anemia therapies continues to tighten around pediatric access, chronic-disease labeling, and post-marketing safety monitoring for IV iron complexes. In February 2026, the US FDA approved ACCRUFeR (ferric maltol) for iron deficiency in pediatric patients aged 10 years and older, expanding a prescription-only oral option into an age group that has historically relied heavily on supplements and select IV pathways. In Canada, Health Canada issued a Notice of Compliance in March 2024 for Ferinject (ferric carboxymaltose) in adults and pediatric patients from 1 year of age, reinforcing the global pattern of label broadening to younger cohorts.

On access and competition, the US regulatory environment also supported additional supply through generics for complex injectables. In August 2025, the FDA approved the first generic Iron Sucrose Injection, USP (Viatris) for iron deficiency anemia in adult and pediatric patients (2 years and older) with chronic kidney disease, with a separate FDA approval in the same month for Amphastar Pharmaceuticals generic iron sucrose injection. Guideline bodies further shape utilization: KDIGO released its 2026 Anemia in CKD Guideline in January 2026, recommending iron status testing at least every 3 months in people with chronic kidney disease, reinforcing protocol-driven testing and treatment cycles that affect both oral and parenteral iron demand.

Competitive Landscape

The iron deficiency anemia therapy market remains moderately fragmented. AMAG (-Covis), Pharmacosmos, and Sanofi are the key players leveraging robust clinical datasets and manufacturing scale. Pharmacosmos’ 2024 acquisition of G1 Therapeutics broadened its oncology pipeline, reinforcing competitive positioning.

Innovation is clustering around delivery improvements. Nano-encapsulated iron and plant-protein complexes promise 90% bioavailability without gastrointestinal distress, supported by early-stage funding rounds involving venture and strategic investors. Digital companion apps that track ferritin, calculate cumulative dose, and auto-reschedule infusions aim to lock in brand loyalty. Geographic partnerships are also intensifying: Fresenius and Vifor expanded their China alliance, combining local dialysis reach with premium infusion lines.

Price pressure from emerging biosimilar-adjacent entrants is muted for now because of high validation costs and strict pharmacovigilance rules. Nonetheless, supply-chain diversification, modular production plants, and risk-sharing contracts with payers are growing priorities among incumbents as they seek margin stability in the evolving iron deficiency anemia therapy market.

Iron Deficiency Anemia Therapy Industry Leaders

AbbVie Inc.

Pharmacosmos

AMAG (-Covis)

Sanofi

Fresenius SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Pediatric diagnosis and treatment pathways are widening, creating room for label expansions, age-appropriate formulations, and payer-aligned evidence packages across both oral and IV segments. In June 2026, the American Academy of Pediatrics published an updated clinical report on prevention, screening, diagnosis, and treatment strategies for iron deficiency and iron deficiency anemia in children, reinforcing routine clinical attention to this population and sharpening the need for tolerability-focused products and practical dosing. Regulatory momentum is also supporting expanded pediatric access for advanced oral products; in February 2026, the US FDA approved ACCRUFeR (ferric maltol) for pediatric patients aged 10 years and older, aligning with the market shift toward adherence-friendly oral therapies that reduce gastrointestinal discontinuation versus traditional ferrous salts.

For parenteral iron, hospital and outpatient infusion efficiency remains a concrete lever for differentiation, with single-visit repletion regimens anchoring formulary decisions in chronic disease care (notably CKD and heart failure). The January 2026 KDIGO Anemia in CKD guideline recommending iron status testing at least every 3 months formalizes repeat testing cadence and supports ongoing treatment management in nephrology settings. At the same time, the emergence of new generic iron sucrose injections in the United States (FDA approvals in August 2025 for Viatris and Amphastar) expands competitive options for CKD-related anemia management, shifting manufacturer competition toward reliable supply, pharmacovigilance infrastructure, and site-of-care support rather than unit price alone.

Recent Industry Developments

- April 2026: China Medical System Holdings Limited (CMS) signed an exclusive commercialization and supply agreement with Pharmacosmos A/S for Monofer (iron isomaltoside) and Cosmofer (iron dextran) in China. The deal strengthens Pharmacosmos presence in a high-volume market and supports more structured access through an established local commercial platform for originator IV iron brands.

- August 2025: The US FDA approved Viatris as the first generic Iron Sucrose Injection, USP, for iron deficiency anemia in adult and pediatric patients (2 years and older) with chronic kidney disease. The approval introduces a new competitive supply source for a widely used IV iron class in nephrology-driven treatment pathways.

- March 2024: Health Canada issued a Notice of Compliance for CSL Vifor Ferinject (ferric carboxymaltose) to treat iron deficiency anemia in adults and pediatric patients from 1 year of age. This expanded labeled access supports broader protocol use of high-dose IV iron in hospital and specialist settings where rapid repletion is prioritized.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the iron deficiency anemia therapy market includes medicines and clinical therapies used to correct iron deficiency anemia by restoring iron levels or replacing red cells in a care setting. The market is measured in value terms for products and services used for treatment across major regions.

Scope exclusions: We exclude fortified foods, general wellness supplements not positioned for anemia therapy, and treatments aimed at non-iron forms of anemia.

Segmentation Overview

- By Therapy Type

- Oral Iron Therapy

- Ferrous salts

- Ferric and polysaccharide complexes

- Enhanced-absorption or lipophilic

- Parenteral Iron Therapy

- Ferric carboxymaltose

- Ferric derisomaltose

- Iron sucrose

- Others

- Oral Iron Therapy

- By Age Group

- Pediatric

- Adults

- Geriatric

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Channels

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with publicly available disease and treatment context, which helps us set realistic boundaries for what is counted as therapy value. We refer to sources such as the World Health Organization for anemia and iron deficiency context, the US CDC for population health indicators, the NIH and MedlinePlus for treatment pathways, and the FDA for drug approval and labeling language that clarifies intended use.

To convert that context into a usable sizing base, we also review sources such as national health statistics portals, peer reviewed journals that discuss iron deficiency anemia burden and care patterns, and customs or trade statistics where relevant for iron preparations. Company annual reports, investor decks, and reputable press releases are used to understand portfolio focus and regional exposure, and paid subscription access for company financials and news helps with cross checking reported revenues and major event timing. These examples are not exhaustive, and we used additional public sources to collect, validate, and clarify the final assumptions.

Primary Interviews and Surveys

Primary work is used to pressure test the demand pool and pricing logic with clinicians, hospital pharmacists, payor facing roles, and supply side commercial teams that track iron therapy uptake. Since this is a global market, we validate inputs across APAC, EMEA, and the Americas to capture differences in care pathways, use of IV iron, and transfusion practices before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 51% |

| Mid tier: 49% | Functional/Unit leaders: 32% | EMEA: 29% |

| Smaller Players: 15% | Managers: 55% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where the addressable patient pool and treatment behavior are translated into therapy value by region, then reconciled to what the supply side can realistically support. In practice, our model starts from the addressable iron deficiency anemia population, applies diagnosed and treated shares, and then layers on therapy mix splits across oral iron, intravenous iron, and transfusion based care where clinically relevant.

To keep the totals grounded, we corroborate the output with selective bottom-up approximations, such as sampled volume by major therapy classes multiplied by typical price ranges, and channel checks on how much treatment is delivered through hospitals versus outpatient settings. A few inputs that matter a lot in this market are the diagnosed and treated rate, the shift toward IV iron in specific patient groups, typical dosing course patterns by therapy type, and price progression assumptions that reflect generic availability and tendering behavior. Where local data is thin, we handle gaps using proxy countries with similar care access and then adjust after expert review.

Forecasting leans on scenario analysis supported by trend checks on anemia burden indicators, expected changes in screening and awareness, and therapy preference shifts discussed in interviews. When the main drivers move in different directions, the scenario ranges help us keep a balanced view and then settle on a central case consistent with observed adoption patterns.

Data Validation & Update Cycle

Outputs are cross checked against independent signals, including therapy class growth expectations, regional care setting shifts, and major regulatory or reimbursement changes that can move utilization. When a segment shows an unusual jump, we recheck the drivers and trigger follow up calls to confirm whether the change is real or a modeling artifact.

Before sign off, the model and assumptions go through multi step analyst reviews, including variance checks across regions and a final reconciliation of growth rates against underlying demand indicators. Reports are refreshed annually, and interim updates are made when material events occur, after which we complete a fresh pre delivery pass so clients receive the latest updated view.

Mordor Intelligence's Iron Deficiency Anemia Therapy Market Size Compared With Other Published Estimates

Published market values for iron deficiency anemia therapy can look far apart because each publisher draws the line differently around what counts as treatment, and because base year choices and pricing assumptions do not always match. The table brings those differences into one view, so a reader can see how scope and timing decisions flow into different totals.

Key gap drivers for this market usually come from whether red blood cell transfusion is treated as part of therapy value, how oral iron is counted when it is bought over the counter, and whether pricing is modeled using list price or a more typical net realization. The year selected as the starting point also affects results, especially when IV iron usage is changing, and currency conversion timing can widen the spread when regional weights differ.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.68 B (2026) | |

| Global Consultancy A | USD 4.98 B (2025) | Uses an earlier base year and a broader stated segmentation set, and it can also differ if OTC oral iron is valued using retail pricing without adjusting for typical discounts and regional reimbursement patterns. |

| Industry Publisher B | USD 4.30 B (2023) | Anchors the model to a different start year and may treat transfusion related value as out of scope, which reduces totals in markets where hospital based correction is a meaningful share of care. |

The table shows a spread that is largely explained by start year timing and what gets counted around transfusion and OTC treatment, and in Mordor Intelligence's model the therapy scope includes oral iron salts, intravenous ferric formulations, and red blood cell transfusion delivered through licensed care settings, while fortified foods and general wellness products are not counted. With those scope decisions stated upfront and checked against treated population and therapy mix inputs, the final number stays traceable to clear levers that can be revalidated when the market shifts.

Key Questions Answered in the Report

What clinical trend is pushing hospitals to adopt single-visit intravenous iron infusions?

Single-visit total-dose formulations such as ferric carboxymaltose reduce chair time and nursing burden, aligning with hospital efficiency goals and value-based reimbursement models.

How are digital health tools changing iron-deficiency anemia therapy adherence?

How are digital health tools changing iron-deficiency anemia therapy adherence?

Why are paediatric formulations gaining traction despite adults remaining the core user base?

Mandatory school-age screening and child-friendly oral or low-volume IV options are expanding access for children, prompting specialised product launches and paediatric-focused clinical guidance.

What supply-chain vulnerability has recently affected parenteral iron availability?

Concentrated production of ferric derisomaltose APIs created bottlenecks, highlighting the need for diversified sourcing and contingency inventories among hospital buyers.

Which delivery innovations are most likely to overcome tolerability-related discontinuation?

Nano-encapsulated oral capsules and iontophoretic transdermal patches are demonstrating high bioavailability with minimal gastrointestinal or hypersensitivity reactions, improving patient acceptance.

How are government anemia-elimination programs influencing product mix?

Realisation that not all anemia is iron-related is steering procurement from mass-distributed generic tablets toward targeted intravenous and advanced oral formulations that include diagnostic support.

Page last updated on: